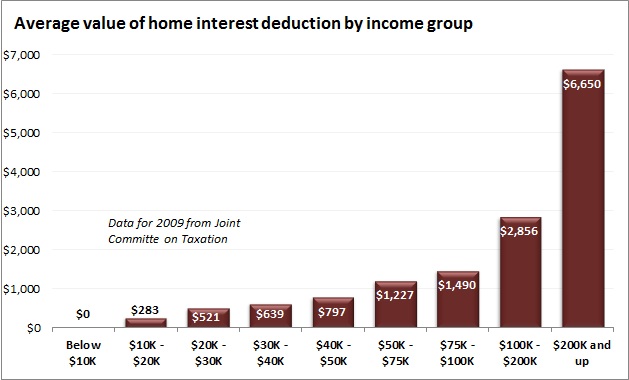

The home mortgage interest deduction does not encourage home ownership and it disproportionately benefits high-income taxpayers. A study of the MI deduction’s various impacts in National Affairs demonstrates the extent to which its benefits are skewed to high-earners, wealthy suburbs, the coasts and other areas with high real estate prices. The study also discusses the perverse incentives created by the deduction.

If you think the MI deduction helps you personally, remember that it almost certainly inflated the price you paid for your home and the amount you had to finance, and it likely has caused the income tax rate you pay to be higher than it would be in its absence. There is little or nothing to recommend the deduction as policy. Even the ostensible goal of a federally-directed increase in home ownership is of questionable value. Reform of the tax code will be politically charged, and this provision will have its share of staunch defenders. The authors discuss various alternatives and approaches to reform that could ease the transition away from the deduction.