Tags

adverse selection, Death Spiral, Emergency room utilization, Exchange-based plans, Medicaid expansion, Mercatus Center, Michael Tanner, Non-market solutions, Obamacare, Obamacare enrollment

“… out in the real world, the bad news keeps coming, drop by drop, drip by drip, until we are seeing a virtual flood of Obamacare awfulness.“

That’s from Michael D. Tanner in “What’s Wrong With Obamacare?” Tonight, I offer you a list of some of the drippings:

- Flat enrollment, expected to be less than half of the original projection for 2016;

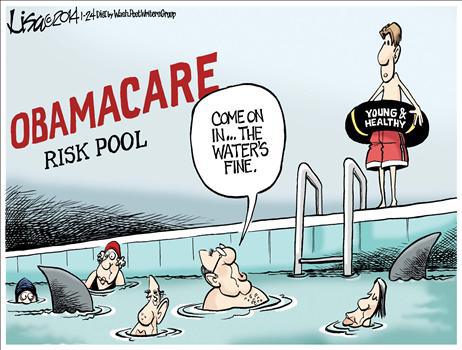

- Almost all (97%) newly insureds under Obamacare are enrolled under expanded Medicaid, unaided by the many complexities introduced by Obamacare;

- 12 of 23 federal health care insurance coops have failed as of Nov. 3;

- High medical loss ratios are threatening the viability of insurers in 27 states, a result of adverse selection by relatively sick enrollees;

- With unfavorable risk pools, premiums for all 2016 exchange-based plans are rising 20.3%, well above the 7.5% figure quoted by HHS for “Silver” plans;

- Health insurance does not guarantee health care, and many of the newly insured are finding that providers are scarce, given reimbursement rates;

- Emergency rooms utilization is up, as patients know they can get care there;

- Rationing of care is increasingly a matter of waiting time, as it is in other countries that rely on non-market solutions to health care;

- As many as 700,000 low-income enrollees are at risk of losing their coverage because they did not file tax returns;

- For many, the penalty for not having coverage ($695 next year) is lower than the premium they would pay for coverage;

- More than 5 million individuals lost their coverage under Obamacare, generally policies that were preferred over the new alternatives;

- Poor incentives and burdensome provider requirements are pushing costs up.

- Employers are attempting to minimize the cost of Obamacare. The law makes hiring more expensive and leads to substitution of part-time for full-time workers;

The “death spiral” might not be far-off for Obamacare. Here is Tanner’s assessment:

“The young and healthy simply haven’t signed up for Obamacare in the same numbers as those who are older and sicker. The only way for insurers to offset their skyrocketing [Medical Loss Ratios] is to hike premiums still further. … premiums in the worst states could have to rise by an average of 34 percent, and possibly as much as 52 percent. But premium hikes of that magnitude would almost certainly further discourage younger and healthier Americans from buying insurance.“

There is no question that Obamacare will have to be replaced or changed substantially. Unfortunately, Obamacare apologists simply can’t come to grips with the reality of the law’s failure. They would do well to start focusing on new solutions to the problems that Obamacare was intended to solve. To that end, the Mercatus Center commissioned a collection of seven essays on how best to deal with the problem of pre-existing conditions, now published on the Mercatus web site. Market-based solutions are needed to encourage competition among insurers, incentivize innovation and cost control, and reestablish the primacy of the patient-provider relationship.