Recently I mentioned the many executive orders (EOs) issued by President Trump since his inauguration. He’s on a record-setting pace! Of course, he pushes the envelope because he’s serious about his agenda, Congress is often paralyzed, and because he can. As one X poster puts it, Trump “swings for the fences”. The system allows him to take shots as chief executive, and if you don’t like it you’ll have to wait for the courts to rule on challenges. So far, in cases that have been decided, the Administration’s court record in defending Trump’s EOs would be good for an MLB batting average.

The Circle of Rent Seeking

Like his overall record as president, Trump’s EOs cover the spectrum from very good policy to just horrible. I tend to favor deregulatory actions, but a recent Trump EO bearing on corporate Environmental, Social, and Governance (ESG) scores and DEI practices is a pro-market exception to typical regulatory actions. That’s basically the view expressed by Phil Gramm and Jeb Hensarling of the American Enterprise Institute. The ESG EO addresses potential fraud and conflicts of interest in the promotion of “socially responsible” shareholder initiatives and investing.

I’ve expressed my distain for corporate ESG initiatives in the past (seehere and here). The quest to earn a high ESG score is a distraction from a firm’s core mission and often a misuse of resources. Higher ESGs are associated with government subsidies, which closes the circle on the politicization of “sustainable” investing. Plumping up ESG helps firms garner more subsidies and greater subsidies help firms boost their ESG scores. These victories might be more pyrrhic for shareholders as management enlists the firm’s assets into service for government industrial policies that are often misguided.

Seedbed For Fraud

As for protecting investors from the fallout, one can argue that abuses related to ESGs belong to a class of problems best left to the market via caveat emptor. Investors might wish to earn pecuniary returns or they might wish to earn non-pecuniary returns. However, they might not always recognize the possibility of tradeoffs between the two, or the possibility that they are being scammed outright.

Unfortunately, financial decisions involve complexities that are often beyond the ken of the investing public. Their dealings with financial advisors obviously involve information and knowledge asymmetries, which underly the need for fiduciary laws and standards. ESG investing has constituted a kind of fad that has both attracted the naive and was always ripe for abuse by overeager or unethical advisors and other industry players.

Proxy advisors have been heavily involved in counseling public companies on ESG proposals brought before shareholders for votes. At the same time, these proxy advisors often engage in selling ESG metrics, which can create conflicts of interest. In particular, the EO in question seems to target two foreign-owned proxy advisors, who effectively dominate the space.

Investor Protection

The EO in question seeks protect American investors from politicized investment advice and shareholder proposals. That might sound like standard Trumpese for “I want to make my opposition illegal along with anything I don’t like”. However, there are good reasons to support this EO. I’ll get to those below, but first some quick details.

The EO instructs the SEC to review and consider revising rules, guidance and other materials relating to ESG and DEI. Scrutiny of shareholder proxy advisor recommendations is given particular emphasis. There are provisions targeting potential antitrust violations in collaborations between investment and proxy advisors. Also, there are provisions aimed at protecting pension and retirement plans from violations of fiduciary duties and obligations.

It’s hard to argue against standards of fiduciary duty. They ought to be politically neutral by their very nature. Unfortunately, the fascination with ESG metrics has made it easier to dispense poor investment advice, even for those purported to have expertise in the area. This is of greater import given that a significant share of investors have been led to believe that signals of corporate virtue are associated with superior pecuniary returns. It should be obvious that diversion of corporate resources to “social” pursuits must be scrutinized by shareholders and stock analysts. Even more troublesome are efforts that undermine productivity in the name of broad political or social objectives.

Not Objective Measures

ESG’s are by no means standardized. There are a great many vendors of ESG metrics, and they frequently disagree as to the merit of particular companies in terms of social responsibility.

Measuring the social value of particular initiatives or policies can be highly subjective, and weighted aggregations of those measurements into E, S, and G components, and combined ESG metrics, can be highly arbitrary. It’s not an exaggeration to say that the social value of certain key elements are sometimes fictitious, such as the carbon credits so often used as “offsets” by firms whose pollution is unavoidable to one extent or another. The purchase of those credits is a performative exercise that has earned the name “greenwashing”. But it’s seldom a wash. This kind of activity is a wasteful distraction and sometimes downright harmful: so-called deforestation credits might just as well be assigned a negative social value.

ESGs have also tended to reward firms adhering to DEI hiring and promotion policies. Merit takes a back seat. While diverse perspectives can add value in business contexts, HR decisions based on race, gender, or other superficial classifications are unlikely to serve shareholder pecuniary interests.

ESG Performance

Evidence on the performance of ESG funds is checkered at best. This is noted by Gramm and Hensarling, who reference an article by Sanjai Bhagat’s in the Harvard Business Review (also see this study). Bhagat reported that not only are returns on ESG funds inferior, but they fail to deliver enhanced non-pecuniary outcomes. Moreover, ESG funds often carry higher fees to investors. One study found that the willingness to pay these higher fees is driven by financial illiteracy.

A few studies seem to contradict Bhagat’s assertions, but at best the evidence is mixed. An April 2025 paper by two Dutch authors found that only changes in the E component (environmental), as opposed to changes in S and G, were positively correlated with stock returns. Those positive abnormal returns were driven by institutional investors who, despite their presumptive expertise, might be just as cowed as certain individual investors by the appearance of social virtue.

As a reality check, note that one can pick and choose among ESG vendor scores, the stock “universe”, sample periods, and estimation techniques to find positive or negative correlations between ESGs and stock returns.

As I mentioned above, the process of assigning ESG values is highly arbitrary in any case. It’s possible to engineer ESG scores in ways that essentially reward firms with high earnings for minor gestures of ostensible social value, even while ignoring less convenient consequences of a firm’s activity. Thus, the scores can be used to buttress valuations associated with high earnings while maintaining the pretense that the score is strictly about social virtue.

Conclusion

I’d be the first to defend the right of consumers to deploy their savings to political, social, or economic purposes of their choosing. However, they should do so with their eyes wide open. It would be of great benefit if the ESG community would agree to a set of measurement standards. When seeking advice from an advisor or in reading analyst reports, investors should have confidence that the information comes from sources who respect the duties of a fiduciary. In the case of ESG funds or in selecting stocks based on ESGs, investors should be aware that their pecuniary interests might be compromised.

Furthermore, analysts and firms who are in the business of selling ESG ratings should be wholly independent of proxy advisors, investment advisors, and ESG funds to avoid conflicts of interest. Unfortunately, these simple, common-sense guidelines have been neglected. As a result, I support the thrust of Trump’s EO on ESGs to reinforce the fiduciary duties of investment and proxy advisors. It would be even better if Congress could meet this challenge via legislation.

I voted for Trump because I considered him to be far preferable to Kamala Harris across a range of issues. I still feel that way, but I’m appalled at a number of actions he’s taken and/or proposed in the 14 months since he took office. As a candidate, I gave Trump a “grade point average” of about 2.68, a solid C+. Here, I’ll grade him on most of the same categories, but I’ve made a few changes to the categories based on developments since his inauguration. My perspective here is generally domestic non-intervention and small government.

Yes, I realize this is tldr; I’m sure I elaborated more than necessary, but you can skip around and scroll to sections in which you might have greater interest. Here’s a list of topics:

Role of Government

Regulation

Border Policy

Antitrust

Foreign Policy

Trade

Taxes

Inflation

Federal Reserve Independence

Federal Spending and the Deficit

Entitlement Reform

Government Waste

Health and Health Care

Abortion

Housing

Energy

First Amendment Rights

Second Amendment Rights

DEI and Its Evil Financial Twin, ESG

Technology

Voting Rights

Education

Role of Government: It’s probably unfair to treat this as a separate category because it might double count specifics mentioned later, but Trump has demonstrated an unfortunate proclivity for wielding government power over private affairs when it suits him politically. On this point, “The Conspicuous Fist of Trump’s State Corporatism”, is a good read. Trump’s actions demonstrate the awful ways in which populism is often a close cousin to socialism. An example is Trump’s economic micro-management and abrogation of property rights in attacking share buybacks. Trump boasts of his efforts to strengthen the American economy by committing public resources to investments in private enterprises, and by “doing deals” with foreign governments to invest in the U.S. When it comes to limited government, candidate Trump’s C is now President Trump’s D.

Regulation: Despite the kinds of intrusions cited above, the Trump Administration has, at the same time, aggressively pursued deregulation of private activity. The goal is to achieve a 10-to-1 ratio of rule rollbacks to new regulatory rules. One can and should assess regulatory measures one-by-one, but there are plenty of rules that wouldn’t pass a reasonable cost-benefit test. On the whole the regulatory state has grown unwieldy and imposes significant costs on producers, and ultimately taxpayers and consumers, often with little compensatory benefit. I applaud the effort to untangle the regulatory state. My grade for Trump here remains an A.

Border Policy: Despite my preference for non-intervention, I support strong border enforcement along with expanded legal immigration.

Illegal entry has plummeted under Trump, a welcome development. Uncontrolled immigration entails a loss of sovereignty and is a poor fiscal proposition. Those with deeper criminal records, from either before or after entry, deserve no concessions. Strict vetting is also necessary to prevent incursions by potential terror threats.

While illegal entry is a crime, otherwise innocent illegals should be treated kindly. For example, rewards can be offered for voluntary deportation, an approach used extensively by the Trump Administration. There are difficult issues such as birthright citizenship, the constitutionality of which has been questioned on textual grounds, and the practicality of which can be shaky, even for children of parents who enter the U.S. legally. Either way, it seems clear that the promise of birthright citizenship should not serve as an incentive for illegal entry.

The Administration has certainly fumbled immigration enforcement in some instances, with cases of improperly detained individuals. Furthermore, very little has been done to advance the cause of increased legal immigration. On this topic I give Trump an overall B-.

Antitrust: This is a case of excessive government meddling with a big dose of favoritism thrown in. Early on, the Trump Administration chose to follow in the footsteps of Biden-era antitrust enforcement with a bias toward penalizing successful businesses on the pretext of “protecting” consumers.

Even worse, the Trump Administration has used the threat of antitrust as a cudgel in pursuit of a variety of objectives that are purely political. For example, in a recent executive order (EO), Trump threatened antitrust action against companies who invest in *too many* single-family homes, a counterproductive prohibition with hoped-for appeal to populist instincts. Then, under Trump, there have been missives from the FTC to tech companies about their failure to provide “balanced” news coverage, a prerogative protected by the First Amendment.

Trump has also interfered with Netflix’s now aborted acquisition of Warner Bros., in favor of a rival offer from Paramount. Trump also engineered the coercive extraction of a U.S. government “Golden Share” in approving the merger of U.S. Steel and Nippon Steel, which Trump claims gives him “total control”, in part by controlling the number of board seats. And he basically extorted a 15% cut for the government for approving a deal allowing Nvidea and AMD to sell the older H20 chip to China.

Trump’s approach to antitrust is very much entangled with the Administration’s uninhibited embrace of industrial policy and public control over private activity. He shares a fantasy common to interventionists that he can leverage the coercive power of government to create just the outcomes he would like.

The grade here is a D, which I think is generous.

Foreign Policy: I’ll try to keep this category separate from trade and tariff issues, though they are intertwined. Trump’s approach to foreign policy is nothing if not bold, and it’s been a mixed bag in terms of success. In the western hemisphere we have the so-called “Donroe Doctrine”, Trump’s effort to establish U.S. hemispheric leadership. So far: we gained a more effective partnership with Panama over the canal and diminished China’s control; decapitated the Maduro regime in Venezuela, asserting control over its oil shipments and undercutting the flow of narcotics through the country; brought the Cuban communist regime to near collapse by choking off its oil imports (but at the cost of greater human suffering in Cuba); partnered with Mexico in eliminating the head of a major drug cartel; and developed closer ties with several conservative regimes in Central and South America.

I’m troubled by the deadly force used against vessels said to be transporting drugs. We might have great intelligence on smuggling operations, but there must be less deadly ways to interdict.

For better or worse, Trump has trolled Canadian leadership in an effort to provoke dissent and gain influence there with respect to trade and security issues. His provocative stance on Greenland is primarily motivated by concerns over security in the Arctic.

Trump’s action against the repressive Iranian theocracy, its support of terror, and its nuclear ambitions has been a military success. Unfortunately, it has come at the cost of some American lives, at least a few civilian casualties in Iran, and a considerable economic cost. We can only hope for quick resolution and a transition to a more liberal regime for the people of Iran. However, Trump was patient to a fault with the mullahs, offering them an off-ramp during repeated rounds of negotiations. They refused to take it.

Of course, Trump is also pro-Israel and has rallied a coalition of nations who might contribute to a revitalized Gaza. I give Trump huge props for his support of Israel and his disgust with anti-Semitism in general.

Trump’s involvement in negotiations between Ukraine and Russia have been unsuccessful. It’s fair to wonder whether he’s cutting Putin way too much slack, as Putin has no intention of relenting. China remains a major threat to U.S. interests and our allies, but many of Trump’s foreign policy initiatives have served to undermine CCP interests.

Trump unique approach has alienated some of our traditional European allies, though he has had success in influencing policy abroad. In Venezuela, it’s worrisome that Trump acts as if he’s cultivating a relationship with Maduro’s replacements, who are probably no better than Maduro except for their eagerness to cowtow to Trump. Well, maybe, maybe not! Also troubling is the collateral damage suffered by the people of Cuba. There are signs of a willingness among Cuban leaders to negotiate with Trump, though hopes for a friendly successor regime might be foolish.

On the whole, I’ll give Trump a B on foreign policy. It’s bold, but he’s had some real successes.

Trade: I gave Trump an F on trade policy as a candidate. He’s more than justified that grade as president. He is a complete dolt when it comes to the benefits of foreign trade, the meaning of a trade deficit, the costs inflicted by tariffs, their complete inadequacy as a replacement for the income tax, and their counterproductive effect on foreign investment in the U.S. His “emergency” tariffs constituted a huge tax increase on the American people, but those were ruled unconstitutional by the Supreme Court. His latest ploy is to impose punitive tariffs under the guise of a balance of payments emergency, but the balance of payments is zero! This too will be struck down in the courts.

Some might argue that Trump’s other foreign policy achievements would not have been possible without the threat of tariffs, but the fact is Trump imposed the tariffs anyway. Yup, it’s an F.

Taxes: In terms of budget effects, the increased tariff revenue (which might not last at present levels) is much more than offset by tax provisions in the One Big Beautiful Bill Act (OBBBA) passed into law last summer. It makes permanent many of the reductions in the Tax Cuts and Jobs Act of 2017 that had been ready to expire. The standard deduction is increased and more limits are placed on itemization. The Act also creates targeted (and temporary) deductions for tips, overtime, auto loans, and seniors, which is inefficient because it treats various forms of income differently, leading to incentives for unproductive reallocations. Those changes also smack of political pandering.

The OBBBA makes permanent some tax incentives for business, such as immediate expensing of short-term asset purchases and domestic R&D investment. It also provides a temporary 100 percent deduction for certain structures and phases out tax credits for green energy production (bravo!).

To the extent that the tax package includes some pro-growth elements, I applaud it. Tax reductions generally are a good thing because they reduce distortions, but Trump has managed to introduce several distortionary elements just the same. I won’t dock Trump for deficit effects here because the deficit is fundamentally a spending problem, not a tax problem. I gave him a C+ on taxes as a candidate, but I’ll boost him to a B- for his first year.

Inflation: Trump doesn’t have real control over inflation as economists define it, but he’s managed to aggravate some price increases just the same. Unfortunately, he makes repeated claims that “prices have fallen” under his leadership, which of course is false. Egg prices perhaps, and oil prices (er… not this month). Of course, in general prices are up, including import prices. Inflation measures have been fairly steady over the past year, but remain stubbornly higher than the Federal Reserve’s target. I give Trump a grade on this topic only because he deserves a penalty for his false boasts. It’s a C, the same as candidate Trump.

Federal Reserve Independence: Trump has relentlessly badgered Jerome Powell and the Fed to somehow engineer lower interest rates. Of course, many key interest rates are market driven and outside the Fed’s direct control. Trump has gone so far as to bring lawfare to bear against Powell, accusing him of misleading Congress regarding cost overruns on the renovation of the Fed’s offices in DC. Of course, it’s not unusual for a president to jawbone the Fed, but Trump has been absurdly aggressive at a time when reducing the Fed’s rate targets would quite possibly backfire. At least Trump’s selection of the next Fed Chairman, Kevin Warsh, was more reasonable than another top candidate who would probably have been a mere punching bag. For this, I’ll lift his grade slightly, from an F to a D-.

Federal Spending and the Deficit: I discuss a few components of spending under other headings below. Beyond those points, Trump has taken every opportunity to find creative uses for taxpayer money. He has proposed a “tariff dividend” for all households funded by the revenue from import taxes. (Refunds of tariff revenue to “payers” are still in question.) At this point, the better alternative is to put extra revenue toward paying down the federal debt. The same goes for any revenue earned from the many “deals” Trump is counting on. Pay down the debt and earn an immediate, certain, and lasting return, rather than installing the government as part owner of otherwise private enterprises having uncertain returns.

Apart from that and the folly of establishing a sovereign wealth fund while the public debt is burgeoning, Trump has made no progress whatsoever on deficit reduction. Granted, he can’t count on strong legislative support despite slight majorities in both chambers of Congress.

The tax cuts in the OBBBA obviously don’t help the cause of deficit reduction. In fairness, rebuilding the military is a major priority. However, interests costs on the debt will keep rising as will discretionary non-defense outlays. At least the East-Wing Ballroom, the Arc de Trump (!), and the Kennedy Center renovation all appear to be privately funded.

Trump deserves a D here. Some of his priorities are terrible, and I can’t cut him any slack based on trends in discretionary spending.

Entitlement Reform: Trump has been silent on reforms to Social Security’s “Old Age and Survivors” programs and Medicare, except to promise no cuts in benefits under his watch. Kick the can! However, the administration has considered cuts in other entitlements, such as Social Security Disability Insurance, Medicaid and Supplemental Nutrition Assistance (SNAP). These programs have been riddled with fraud, so I applaud steps to clean them up. Nevertheless, any progress made here will still be dwarfed by the insolvency of the Retirement and Medicare programs, which Trump considers a third rail for potential reformers. I gave him an F as a candidate, but his anti-fraud efforts help him salvage a C-.

Government Waste: DOGE was short-lived as originally constituted, its execution was clumsy, and the blow-up in Trump’s relationship with Elon Musk was an embarrassment. However, DOGE was a force for stanching the flow of taxpayer dollars through politicized NGOs. The budget savings were relatively small, but the defunded programs were often egregious varieties of government waste. Subsequently, DOGE personnel had an outsized influence on downsizing the federal bureaucracy and targeting waste across various agencies. In addition, the efforts of one-time DOGE workers were put to good use in identifying entitlement fraud, which could and should result in budget savings. Trump gets a B+ on this one.

Health and Health Care: I’ll give Trump credit here for pursuing a more consumer-oriented approach to health care reform, though at least one of his initiatives is counterproductive.

His initial steps took the form of EOs reducing subsidies paid on ACA marketplace policies, ending remaining penalties for violating the ACA’s individual mandate, approving short-term coverages free of certain ACA restrictions, cutting Medicaid expansion funding, and granting more flexibility for states in defining “essential” healthcare benefits. All of these are basically good steps.

Trump issued an ill-conceived EO calling for “Most-Favored Nation” (MFN) prescription drug pricing, which should reduce Americans’ prescription costs but will dramatically undercut life-saving drug research. Hate the pharmaceutical companies all you want, but they must earn a reasonable profit to risk the massive development costs of new miracle drugs, of which they’ve brought many to market. Price controls always create more problems than they solve.

In early 2026 Trump introduced his “Great Healthcare Plan” (GHP). It would codify MFN drug pricing, fund cost-sharing reductions for ACA plans, encourage price transparency, and redirect payments to consumers and away from insurers to facilitate choice and competition. Also launched was the TrumpRx.gov platform featuring MFN pricing. Ironically, the goal here is to improve access to prescription drugs. Good luck!

Under Robert F. Kennedy, Jr., Trump’s HHS Secretary, the “Make America Healthy Again” agenda has emphasized a healthy diet and exercise, including noteworthy changes in the famous food triangle hierarchy. I can’t argue with those. However, RFK Jr. has upended research under HHS, and those actions were rash in a number cases. He wants to address chronic diseases but I’m skeptical of some of his causal claims. I also have mixed reactions to his changed guidance on vaccines. There are reports that the White House has not been comfortable with all of RFK’s pronouncements and is eager to inject more oversight.

I have varied reactions to Trump’s efforts in the health care arena. MFN price capping is a good way to destroy the advantages Americans enjoy in terms of access to innovative drugs, even if they come at a steep cost. RFK Jr. is a wild card, to be fair. Otherwise, while the GHP should help to improve healthcare affordability, it neglects other critical reforms such as ending the disparate tax treatment of health care premiums and deregulating providers. Still, Trump’s grade improved here, from a D+ as a candidate to a B- thus far in his term.

Abortion: No change here. Trump has consistently supported the right to life. He gets an A.

Housing: Build Baby Build! But aside from harping on the Fed to lower interest rates, Trump hasn’t done much to encourage housing supply.

His EO banning institutional investors from owning “too many” single-family homes won’t help affordability because so few homes are owned by large investors. But to the extent that they are, the EO will increase rents and discourage new housing supply. This is another misguided foray into central economic planning.

While I think a 50-year mortgage should be legal, it’s something I believe potential homebuyers should avoid unless they want to risk stubbornly low equity in their homes stretching into retirement. Trump shouldn’t talk this up too much.

Trump has supported the “ROAD to Housing” bill, which has garnered bipartisan support. It would codify the restrictions on ownership of single-family housing by institutional investors and restrict construction of “rent-to-own” housing by such investors. One couldn’t invent a less effective way to encourage supply and promote “affordability”. But the bill would also subsidize demand, which will increase pressure on housing prices even as the bill aims to assist particular groups (e.g., tax credits for first-time homebuyers). Despite all those downsides, the bill actually includes a few steps to boost housing supply, such as making some federal lands available for development, regulatory reform, and tax incentives for builders.

Trump has also discussed changes to government sponsored enterprises (GSEs, Fannie Mae and Freddie Mac), which purchase new mortgages from lenders, including possible privatization. He might be licking his chops for the $300 billion the GSEs owe the federal government, which could be put toward various “deals” he might like to cut. If privatization were to end the explicit government guarantee for mortgage-backed securities issued by the GSEs, mortgage interest rates would rise and it could be quite disruptive for banks.

Housing policy is another mixed bag for Trump, but I’ll give him a B on the strength of his deregulatory effort.

Energy: Drill baby drill! Despite the current disruption to oil shipments through the straight of Hormuz and the spike in oil prices, I deem Trump’s energy policies a success thus far. Largely through deregulation, Trump has opened up the spigots on domestic oil production. He has also realigned energy priorities, eliminating subsidies and mandates for intermittent renewable energy sources in favor of encouraging fossil fuels, hydroelectric, and especially a new emphasis on nuclear power. Some of these steps represent unabashed central planning, so I can’t give Trump an A on energy policy,. However, the preceding green-energy regime was central planning on steroids with the unintended consequence of instability in the power grid. I would greatly prefer a policy of complete neutrality with respect to energy sources, but at least Trump is not cowed by global warming hysteria.

And Trump is considering a temporary suspension of the Jones Act due to the energy crunch brought on by the war in Iran. That would be great except that the waiver should be permanent. The move would lower energy (and other) costs to U.S. consumers and minimize supply disruptions by allowing energy (and other goods) to flow more freely between U.S. ports.

His grade on energy policy is a B.

First Amendment Rights: Trump has not been the defender of free speech that I had hoped. On this, I gave him an A- as a candidate, but his Administration has been belligerent in attacking speech. He (and his FCC Chairman) threaten media outlets with license revocation, his Attorney General says “we will target you” for anything DOJ attorneys might define as hate speech, and Trump has called certain speech he dislikes “illegal”. I also have qualms about an EO issued last year by Trump targeting “campaigns of … radicalization”, which might, in practice, bring any sort of opposition speech under scrutiny. And there are other potentially troublesome provisions for protected speech. Trump’s pure intent might be to stop violent radicalism, which is fine in spirit but hard to bring off without mass surveillance and violations of rights. I therefore downgrade Trump to a C on free speech.

Second Amendment Rights: Trump has not been quite as consistent on gun rights as he was as a candidate. He took a number of actions to reduce burdens and restrictions on gun rights, but in other cases he let restrictions stand, including arrests for gun possession in Washington DC by federal agents and a possible proposal to restrict the gun rights of transgendered individuals. All-in-all, I’ll reduce Trump’s A on gun rights to a B+.

DEI and Its Evil Financial Twin, ESG: There is no question that Trump has done much to cut through the stranglehold that DEI doctrine had imposed on social and economic life. He issued EOs to end DEI practices in the federal government. He also threatened major universities with funding freezes and anti-discrimation actions, an approach that has met with some success. Trump’s words and actions on DEI have reverberated through the private sector as well. He has encouraged individuals who believe they’ve suffered discrimination based on DEI to file lawsuits. The thrust of the Administration’s agenda on DEI and regulatory changes has served to undermine the use of ESG measures. These are intended to draw investors to companies purporting to foster environmental and social goals, which can be at odds with creating value for shareholders. Trump has earned his A in this category.

Technology: As in other policy domains, the record here is marred by misguided industrial policies. That includes the recent snafu over the Department of Defense’s allegation of “supply chain risk” posed by Anthropic. DoD wants carte blanche access to all aspects of any AI model it adopts, including uses in autonomous weapons systems and mass public surveillance. Anthropic said it would not accept that without guardrails, so an apparently infuriated Pete Hegseth moved to designate the company a supply chain risk, an outright punishment that would obviously damage Anthropic’s economic prospects. Yet almost immediately, DoD agreed to an arrangement with OpenAI with guardrails similar to those desired by Anthropic. Now, Trump, who seems to have Hegseth’s back, is readying an EO on the topic… so we shall see. But it’s a mess. Anthropic has filed suit.

And yet Trump has generally been supportive of AI development, signing an order to prevent states from imposing a patchwork of varying, complex regulations. The White House has issued an ”AI Action Plan” to encourage AI exports, minimizing federal regulatory burdens, and “upholding free speech” on “unbiased” frontier models. Let’s hope “unbiased” has a truly neutral definition in this case. Trump has signed a series of EOs related to AI research and deployment, which are linked here.

Post-inauguration, Trump dove right into another socialist joint venture known as Stargate to build data center infrastructure. The rationale for the government’s direct involvement is national security. Of course, that’s the Administration’s rough and ready excuse for almost any kind of intervention.

Trump has helped promote the crypto industry, supporting legislation (the CLARITY Act and the GENIUS Act) enabling more widespread use of stablecoins. He even supports the payment of returns on stablecoins, a development that is unpopular with banks. Trump has also acted to promote cybersecurity and harden infrastructure against malicious actors. More recently, he initiated a program to test eVTOL technologies (electronic vertical takeoff and landing), which are expected to revolutionize local and regional transportation in coming years.

The best I can give Trump on technology is a B-, given his penchant for government control. The Anthropic controversy is a real black eye.

Voting Rights: The Trump-backed SAVE America Act would require an ID proving citizenship to vote in federal elections. It’s stalled in the Senate, seven votes short of the 60 needed to send it to Trump’s desk. GOP senators are unwilling to force a talking filibuster, let alone to use the so-called “nuclear option” to force a simple-majority vote. There is still a possibility of including a voter ID requirement in a budget reconciliation bill if anyone can convince the Senate Parliamentarian that it would have budget impacts. For his part, Trump says he’ll refuse to sign any other legislation until the SAVE Act crosses his desk, though he’s also threatened to issue an EO mandating voter ID should the Senate fail to pass the bill. The constitutionality of such an order would be challenged, of course, but for his determination on the issue, I’ll give him an A+.

Education: This is a quick addition to the list. After inserting the photo of Trump at the top, I realized that I’d completely forgotten to add education as a performance category. Trump’s effort to dismantle the wasteful and unproductive Department of Education is to be applauded. He’s also been an unwavering supporter of school choice. I’ll give him an A here.

I have to stop! That’s 22 categories and a “grade point average” of 2.55 if the categories are equally weighted. It’s a little worse than Trump’s GPA as a candidate (2.67). He could have improved his grades dramatically without his bent for economic intervention, but I’d have to vote for him again given the alternative.

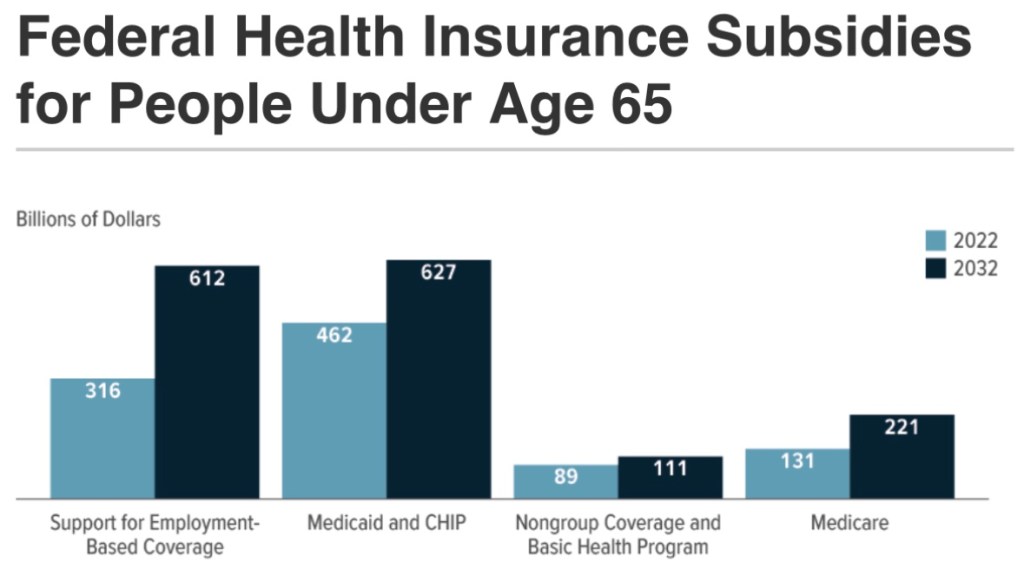

The impasse at the heart of the seemingly unending government shutdown revolves around health care subsidies.

First, there is disagreement about whether to extend the expanded Obamacare subsidies promulgated during the COVID pandemic. That expansion allowed individuals earning more than four times the federal poverty level (the original limit under the Affordable Care Act (ACA)) to receive tax credits for the purchase of health coverage on the exchange “marketplace”. Republicans find this highly objectionable. Many of them also object that the subsidies help pay for “essential health benefits” under the ACA that include so-called gender-affirming care.

Democrats and the insurance lobby would very much like to reinstate or retain the tax credits. The ten-year cost of extending them is more than $400 billion. Incredibly, it turns out that roughly 40% of individuals taking those tax credits did not file a medical claim in 2024. It was pure cash for insurers at the expense of taxpayers.

Second, the One Big Beautiful Bill Act (OBBB), among other things, restricts access to Medicaid by imposing work or job search requirements for overall eligibility. It also formally denies coverage to illegal aliens. This, of course, is opposed by Democrats, who insist that those requirements be rescinded.

Health Care Central Planning

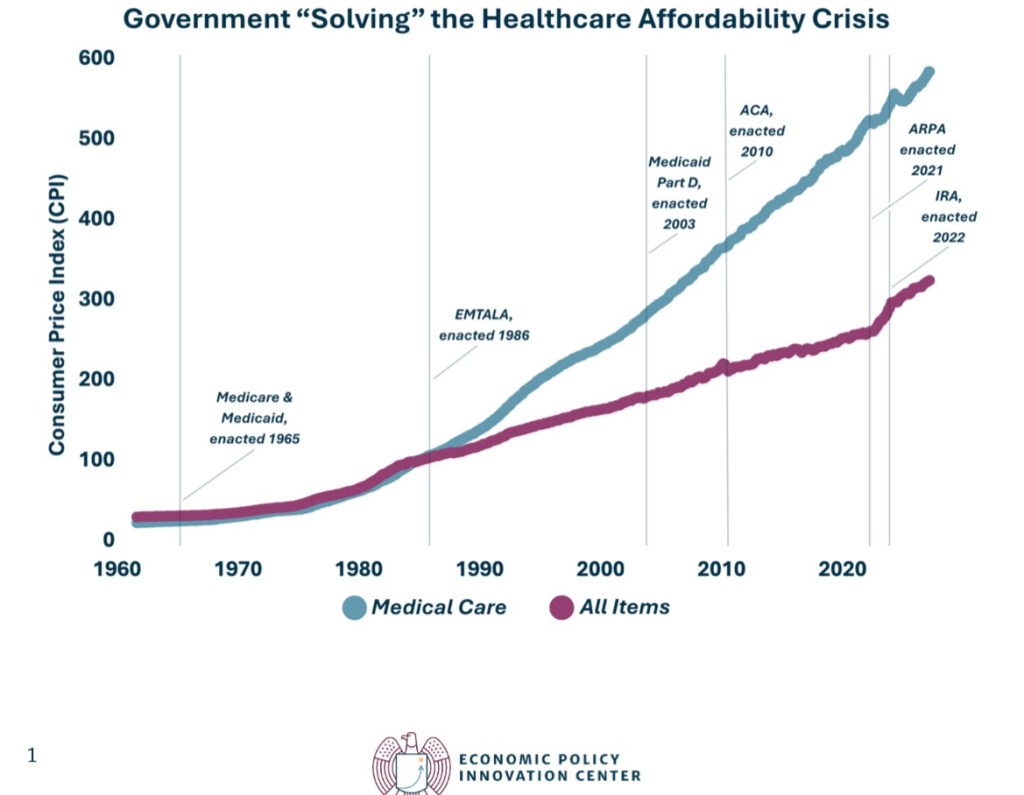

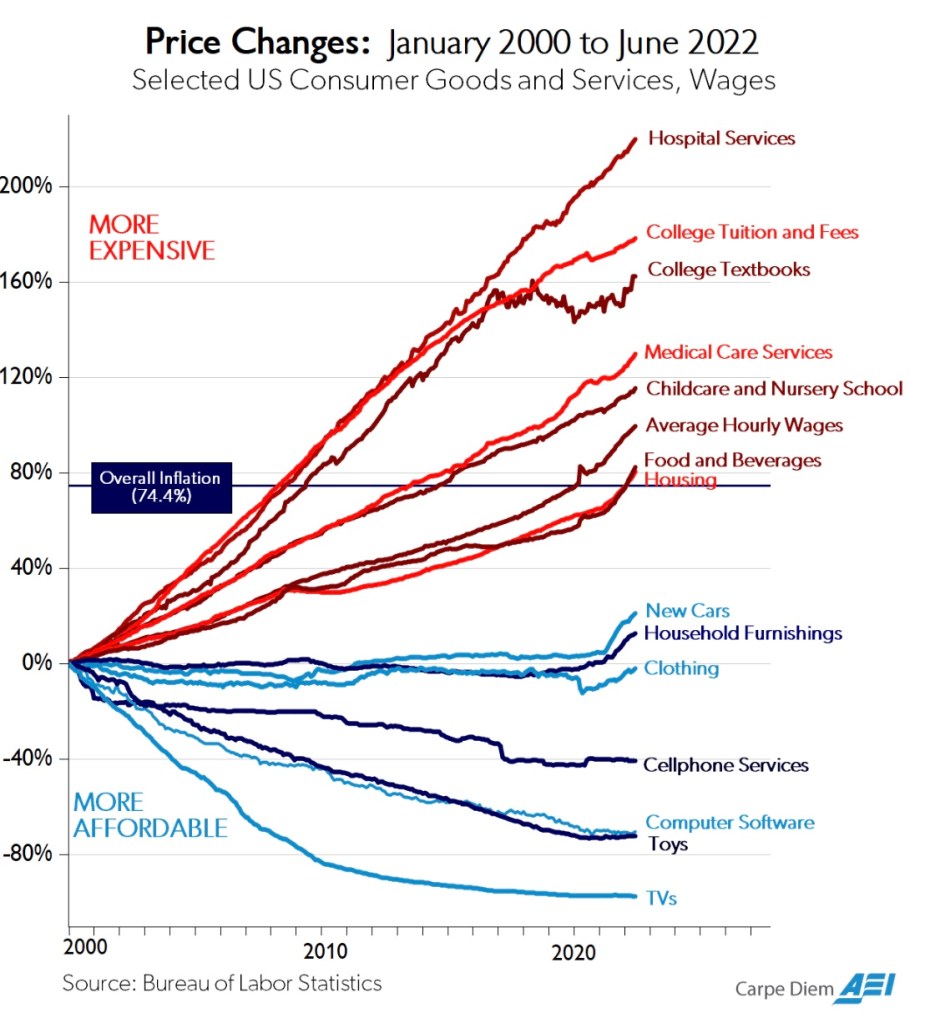

These issues are part of a much larger debate over government dominance of the health care system. Almost every institutional arrangement in health care coverage and delivery is dictated by rules and practices imposed by government, and it would seem they are intentionally designed to escalate costs and compromise the delivery of care. The chart at the top of this post illustrates, in a high-level way, the futility of these efforts.

Medicare and Medicaid dominate government health care spending, as this report from the Peter G. Peterson Foundation shows. However, that strict budgetary view greatly understates the control government now exerts on the health care sector.

“… government controls a larger share of health spending in the United States than in 27 out of 38 OECD-member nations, including the United Kingdom (83%) and Canada (73%), each of which has an explicitly socialized health-care system. When it comes to government control of health spending, the United States is closer to communist Cuba (89%) than the average OECD nation (75%).

“Nor does the United States have market prices for health care. Direct government price-setting, price floors, and price ceilings determine prices for more than half of U.S. health spending, including virtually all health-insurance premiums.“

ObamaSnare

Government “control” takes a variety of forms, including regulatory intrusions under the aegis of Obamacare. The Affordable Care Act (ACA), as its name implies, was sold as a way to keep health care and health insurance costs affordable. And it was billed as a way to extend individual health care coverage to the previously uninsured population. It failed badly on the first count and met with only limited success on the second.

One leg upon which the ACA stood was kicked away in 2017: the penalty for violating the Act’s individual mandate for health coverage was eliminated by the Tax Cuts and Jobs Act (TCJA). The penalty was arguably unconstitutional as a tax on non-commerce, or the non-purchase of insurance on the exchange. However, the Supreme Court had ruled narrowly in favor of the penalty in 2012, claiming that it was within the scope of Congress’ taxing power. Following passage of the TCJA, however, the toothlessness of the mandate caused the risk pool to deteriorate. This was aggravated by the ACA’s insistence on comprehensive coverage, which applies not just to policies sold on the Obamacare exchange, but to almost all private health insurance sold in the U.S.

A well-functioning marketplace would instead have promoted the availability of more moderately-priced coverage options. Ultimately, subsidies were all that prevented a broad exit from the marketplace. But they did nothing to slow the escalation in coverage costs and deteriorating quality of coverage and care:

“The result has been a race to the bottom in terms of the quality of insurance coverage for the sick. …individual-market provider networks [have] narrow[ed] significantly… They have eroded coverage through ‘poor coverage for the medications demanded by [the sick]’ … higher deductibles and copayments; mandatory drug substitutions and coverage exclusions for certain drugs; more frequent and tighter preauthorization requirements; highly variable coinsurance requirements; inaccurate provider directories; and exclusions of top specialists, high-quality hospitals, and leading cancer centers from their networks. ….

“The healthy suffer, too. … ‘currently healthy consumers cannot be adequately insured against the negative shock of transitioning to one of the poorly covered chronic disease states.’ A coalition of dozens of patient groups has complained that this dynamic ‘completely undermines the goal of the [Affordable Care Act].’”

Price Distortions

Cannon emphasizes another persistent myth: that government sets prices at levels that would prevail in a free market. Here is one baffling aspect of the many prices set by government for individual services under the Medicare and Medicaid programs.

“One of the more striking indications of widespread mispricing is that Medicare routinely sets different prices for identical items depending solely on who owns the facility.“

For example, ambulatory surgical centers are compensated much less for the same services as hospitals. The same is true of compensation for skilled nursing facilities vs. long-term care hospitals, and there appears to be no economic rationale for the differences. Furthermore, it’s an open secret that Medicare sets higher prices for lower-cost providers (and treatment of lower-cost patients). As Cannon notes, this explains the rapid growth of specialty hospitals owned by physicians.

Cannon provides much more detail on Medicare and Medicaid mis-pricing, including the blunting of patients’ price-sensitivity and the shifting of costs to private payers.

Divorcing Risk and Insurance

The price of insurance and insurer reimbursements are also prescribed by government. Cannon’s discussion includes the ACA’s abolition of risk-based insurance pricing, which is an astonishing case of economic malpractice. Depending on one’s health status, “community pricing” acts as either a price ceiling or a price floor. This creates perverse incentives for both the healthy and the unhealthy. Premiums fall short of the cost of caring for the sick.

The federal government attempts to compensate by subsidizing insurers based on the health status of individuals in their risk pool, but that falls short in terms of the quality of coverage for unhealthy individuals. Thus, both the healthy and taxpayers must shoulder an ever-increasing cost burden of insuring the unhealthy.

Circular Scam

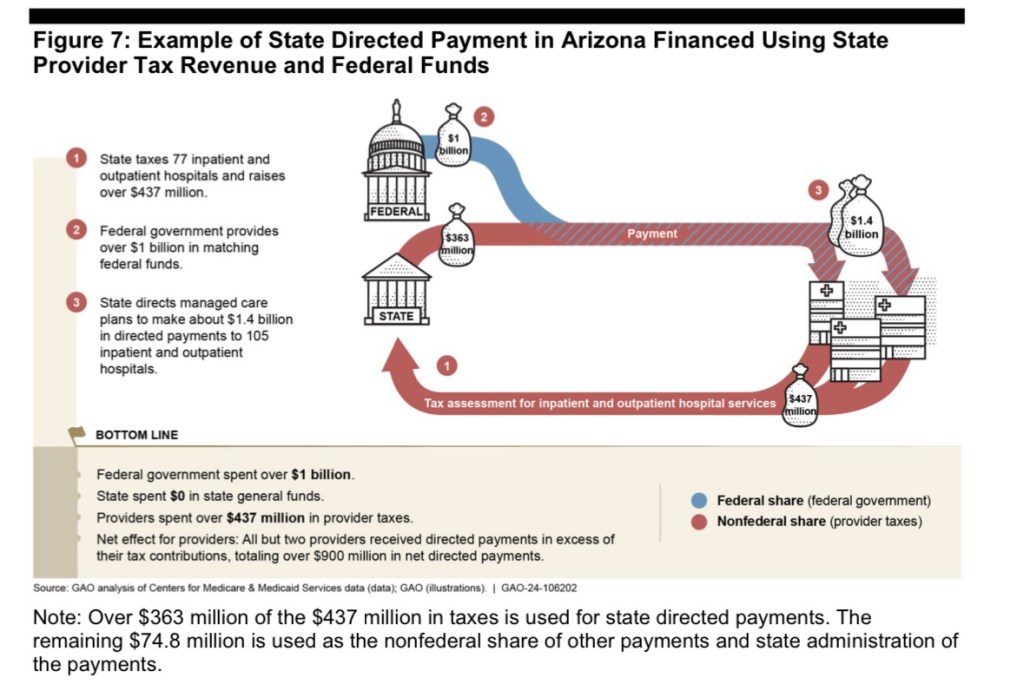

As for Medicaid, certain arrangements drive up the cost of the program to taxpayers. For example, last March I wrote about this apparent scam allowing state governments to inflate their Medicaid costs, qualifying for hundreds of billions of federal matching funds:

“Here’s the gist of it: increases in state Medicaid reimbursements qualify for a federal match at a rate known as the Federal Medical Assistance Percentage (FMAPs). First, increases in Medicaid reimbursements must be funded at the state level. To do this, states tax Medicaid providers, but then the revenue is kicked back to providers in higher reimbursements. The deluge of matching federal dollars follows, and states are free to use those dollars in their general budgets.“

Unfortunately, FMAP reform is not directly addressed in the “clean” Continuing Resolution before Congress, though reduced funding levels might lead to reductions in FMAP percentages.

And Another Circular Scam

John Cochrane is largely in agreement with Cannon’s piece, but he focuses first on cross subsidies flowing to “eligible” hospitals dispensing prescription drugs to low-income patients. These hospitals get the drugs from pharmaceutical companies at a steep discount mandated by the so-called 340B program, but the hospitals then bill insurers (or Medicare and Medicaid), a significant markup over their acquisition cost. The Medicaid expansion under the ACA led to an increase in the number of hospitals eligible for the drug discounts.

But that’s not the end of the story. This arrangement creates an obvious incentive for the drug companies to raise their pre-discounted prices. Another unintended outcome cited by Cochrane is that eligible hospitals do not use the proceeds of their mark-ups to offer better care (or care at a lower cost) to low-income consumers. Instead, the funds tend to be directed to investment accounts. The program also creates another incentive for hospital consolidation.

Someone Else’s Money

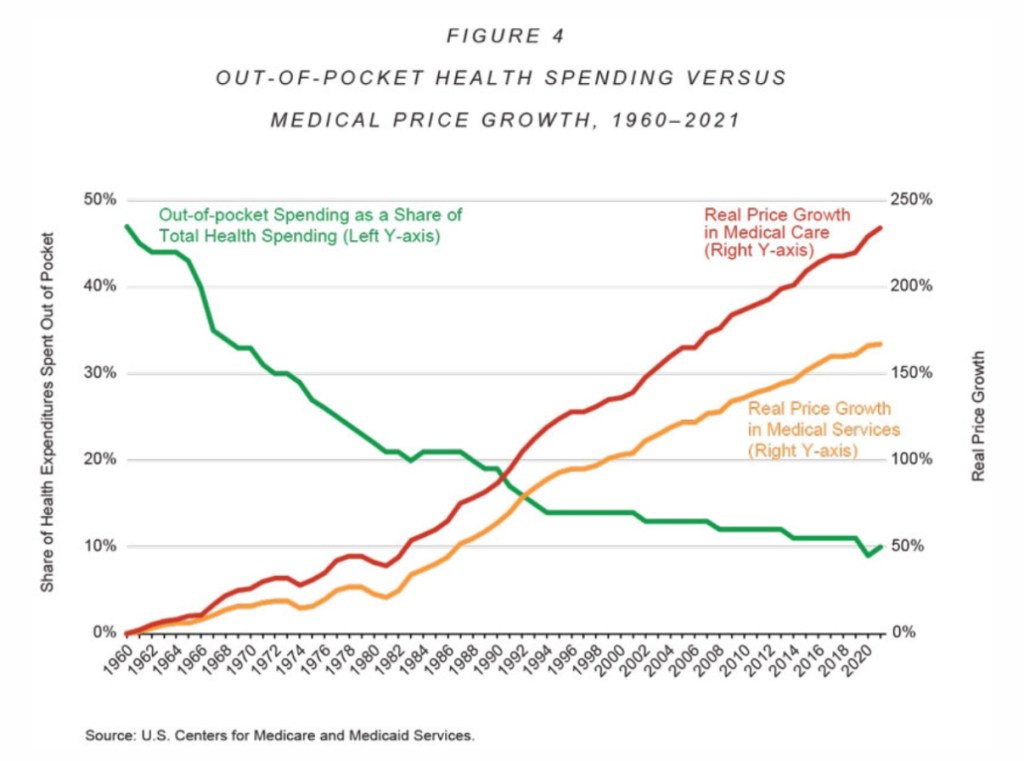

Unfortunately, the dysfunction in health care goes deeper than Obamacare, Medicare, and Medicaid. The third-party payment system itself has been at the root of cost escalation. It largely relieves consumers of their sovereignty over purchasing decisions, rendering them much less sensitive to variations in price. This can be seen clearly in one of Cannon’s charts, reproduced below:

In addition, the disparate income tax treatment of employer-provided health coverage exacerbates cost escalation. Obviously, employees receiving this deduction can afford higher-quality and more comprehensive coverage. This exemption has acted to drive up the cost of all health care and insurance coverage over the almost nine decades of its existence..

What To Do?

The claim that the U.S. health care system operates within a free market ecosystem is obviously absurd. Together, the Cochrane and Cannon pieces represent something of a gripe session, but it is well deserved. Both authors devote sections to reforms, however. They don’t break new ground in the debate, but the overarching theme of the suggested reforms is to give consumers authority over their health care spending. That means keeping government out of health care in all the myriad ways it now intrudes. It also means that insurers should not have authority to dictate how health care is priced. The key is to allow competition to flourish among health care providers and insurers.

Ending FMAPs and the tax exemption for employer-provided coverage is one thing, but it’s another to contemplate dismantling Medicare, Medicaid, and the many rules and pricing arrangements enforced under Obamacare.

Cochrane takes an accommodating approach to the health care needs of seniors and those in need of a safety net. He calls for Medicare and Medicaid to be replaced with the issuance of vouchers (rather than cash) toward the purchase of affordable private health care plans. Then, health coverage can be provided in a lightly regulated, competitive market without all the distortions and sneaky opportunities for graft embedded in our current entitlements.

ConflictingRightsand Reality

And what of the argument that health care is a human right? That notion is, of course, very popular on the left. The idea subtly shifts a meaningful portion of the responsibility for one’s health onto others, including providers and taxpayers. But smokers, heavy drinkers, reckless drivers, hard drug users, and the avoidably obese should not be led to expect a free ride for risky behaviors.

Of course, it’s not a basic human right to demand, by force of government, involuntary service of health care workers, or that taxpayers give alms, but Cochrane answers with this:

“Yes! It is a basic human right that I should be free to offer my money to a willing physician or hospital, in a brutally competitive and innovative market.”

“Willing” is a key word, and to that we should add “able”, but those are qualifying conditions that markets help facilitate.

Jane Menton has discussed the notion of a human right to health care, wisely explaining that conditions are not always compatible with fulfilling such a right. Her primary concern is the future supply of medical personnel, and an acute shortage of nurses.

“In our current political environment, young people seem to think that claiming something as an entitlement means someone will inevitably show up to do the work.“

To codify a right to health care would be an ill-fared call for a nationalized solution. It would be a prescription for still higher costs and lower quality care. As in any other sector, centralized decision-making leads to misallocated resources, higher costs, and inferior outcomes for patients. Our current mess gives a strong hint of the kind of over-regulated dysfunction that nationalization would bring.

Insurance On Insurability

Pre-existing conditions motivate much of the discussion surrounding a presumed right to health care. Individual portability of group health coverage goes partway in addressing coverage for pre-existing conditions. Portability is mandated by the Health Insurance Portability and Accountability Act of 1996, but like community rating, it shifts costs to others. That is, the cost of covering pre-existing conditions becomes the responsibility of employers in general, group insurers, and ultimately healthy (and younger) workers.

Given time, the debate over a right to health care can be rendered moot via market processes. Cochrane has long supported the concept of health status insurance. Such policies would allow healthy consumers to guarantee their insurability against the risk of future health contingencies. Guaranteed renewability is a limited form of this type of coverage. General availability of health status insurance contracts, offered regardless of current coverage, could allow for a range of future insurability options at affordable prices. Then, pre-existing conditions would cease to be such a huge driver of cross subsidies.

I prefer a government that is limited in size and scope, sticking closely to the provision of public goods without interfering in private markets. Therefore, I’m delighted with the mission of the Department of Government Efficiency (DOGE), a rebranded version of the U.S. Digital Service created by Barack Obama in 2014 to clean up technical issues then plaguing the Obamacare web site. The “new” DOGE is fanning out across federal agencies to upgrade systems and eliminate waste and fraud.

I’m seeing scary posts about DOGE even on LinkedIn, such as the plight of Americans unable to get federal public health communications due to layoffs at HHS, while failing to mention the thousands of new HHS employees hired by Biden in recent years. As if HHS was particularly effective in dispensing good public health advice during the pandemic!

Those kinds of assertions are hard to take seriously. For reasons like these and still others, I tend to dismiss nearly all of the horror stories I hear about DOGE’s activities as nitwitted virtue signals or propaganda.

Many on the left claim that DOGE’s work is careless, and especially the force reductions they’ve spearheaded. For example, they claim that DOGE has failed to identify key employees critical to the functioning of the bureaucracy. The tone of this argument is that “this would not pass muster at a well-managed business”. A “sober” effort to achieve efficiencies within the federal bureaucracy, the argument goes, would involve much more consideration. In other words, given political realities, it would not get done, and they really don’t want it to get done.

The best rationale for the ostensible position of these critics might be situations like the dismissal of several thousand provisional employees at the FDA, a few of whom were later rehired to help manage the work load of reviewing and approving drugs. However, thus far, only a tiny percentage of the federal force reductions under consideration have involved immediate layoffs.

Of course, DOGE is not being tasked to review the practices of a well-managed business or a well-managed governmental organization. What we have here is a dysfunctional government. It is a bloated, low productivity Leviathan run by management and staff who, all too frequently, seem oblivious to the predicament. Large force reductions at all levels are probably necessary to make headway against entrenched interests that have operated as a fourth branch of government.

Thus, I see the leftist critique of Trump’s force reductions as something of a strawman, and it falls flat for several other reasons. First, the vast bulk of the prospective reduction in headcount will be voluntary, as the separating employees have been offered attractive severance packages. Second, force reductions in the private sector always feel chaotic, and they often are. And they are sometimes executed without regard to the qualifications of specific employees. Tough luck!

Duplicative functions, poor data systems, and a lack of control have led to massive misappropriations of funds. The dysfunction has been enabled by a metastasization of nests of administrative authority inside agencies with “incomprehensible” org charts, often having multiple departments with identical functions that do not communicate. These departments frequently use redundant but unconnected systems. A related problem is the inadequacy of documentation for outgoing payments. Needless to say, this is a hostile environment for effective spending controls.

It’s worth emphasizing, by the way, DOGE’s “open book” transparency. It’s not as if Elon Musk and DOGE are attempting to sabotage the deep state in the dark of night. Indeed, they are shouting from the rooftops!

Doing It Fast

Every day we have a new revelation from DOGE of incredible waste in the federal bureaucracy. Check out this story about a VA contact for web site maintenance. All too ironically, what we call government waste tends to have powerful, self-interested, and deeply corrupt constituencies. This makes speed an imperative for DOGE. In a highly politicized and litigious environment, the extent to which the Leviathan can be brought to heel is partly a function of how quickly the deconstruction takes place. One must pardon a few temporary dislocations that otherwise might be avoided in a world free of rent seeking behavior. Otherwise, the graft (no, NOT “grift”) will continue unabated.

The foregoing offers sufficient rationale not only for speedy force reductions, but also for system upgrades, dissolution of certain offices, and consolidation of core functions under single-agency umbrellas.

The Bloody Budget

It’s difficult to know when budget legislation will begin to reflect DOGE’s successes. The actual budget deficit might be affected in fiscal year 2025, but so far the savings touted by DOGE are chump change compared to the expected $2 trillion deficit, and only a fraction of those savings contribute to ongoing deficit reduction.

Uncontrolled spending is the root cause of the deficit, as opposed to insufficient tax revenue, as evidenced by a relatively stable ratio of taxes to GDP. The spending problem was exacerbated by the pandemic, but Congress and the Biden Administration never managed to scale outlays back to their previous trend once the economy recovered. Balancing the budget is made impossible when the prevailing psychology among legislators and the media is that reductions in the growth of spending represent spending cuts.

Federal spending is excessive on both the discretionary and mandatory sides of the budget. Ultimately, eliminating the budget deficit without allowing the 2017 Trump tax cuts to expire will require reform to mandatory entitlements like Social Security, Medicare, and Medicaid, as well as reductions across an array of discretionary programs.

DOGE’s focus on fraud and waste extends to entitlements. At a minimum, the data and tracking systems in place at HHS and SSA are antiquated, sometimes inaccurate, and are highly susceptible to manipulation and fraud. Systems upgrades are likely to pay for themselves many times over.

But all indications are that it’s much worse than that.Social security numbers were issued to millions of illegal immigrants during the Biden Administration, and those enrollees were cleared for maximum benefits. There were a significant number of illegals enrolled in Medicaid and registered to vote. While some of these immigrants might be employed and contributing to the entitlement system, they should not be employed without legal status. Of course, one can defend these entitlement benefits on purely compassionate grounds, but the availability of benefits has served to attract a massive flow of illegal border crossings. This illustrates both the extent to which the entitlement system has been compromised as well as the breakdown of border security.

On the discretionary side of the budget, DOGE has identified an impressive array programs that were not just wasteful, but by turns ridiculous or politically motivated (for example, the bulk of USAID’s budget). Many of these funding initiatives belong on the chopping block, and components that might be worthwhile have been moved to agencies with related missions. In addition, authorized but unspent allocations have been identified that seem to have been held in reserve, and which now can be used to reduce the public debt.

Research Grants?

Of course, like the initial scale of the FDA layoffs, a few mistakes have and will be made by DOGE and agencies under DOGE’s guidance. Many believe another powerful argument against DOGE is the Trump Administration’s 15% limit on indirect costs as an add-on to NIH grants. Critics assert that this limit will hamstring U.S. scientific advancement. However, it won’t “kill” publicly funded research. Asthis article in Reason points out, historically public funding has not been critical to scientific advancement in the U.S. In fact, private funding accounts for the vast bulk of U.S. R&D, according to the Congressional Research Service. Moreover, it’s broadly acknowledged that indirect costs are subject to distortion, and that generous funding of those costs creates bad incentives and raises thorny questions about cross-subsidies across funders (15% is the rate at which charities typically fund indirect costs).

No doubt some elite research universities will suffer declines in grants, but their case is weakened politically by a combination of lax control over anti-Semitic protests on campus, the growing unpopularity of DEI initiatives in education, and public awareness of the huge endowments over which these universities preside. Nevertheless, I won’t be surprised to see the 15% limit on indirect research costs revised upward somewhat.

More DOGE Please

I’ve criticized the numbers posted on DOGE’s website elsewhere. They could do a much better job of categorizing and reporting the savings they’ve achieved, and they have far to go before meeting the goals stated by Elon Musk. Be that as it may, DOGE is making progress. Here is a report on a few of the latest cuts.

As I’ve emphasized on numerous occasions, the federal government is a strangling mass of tentacles, squeezing excessive resources out of the private sector and suffocating producers with an endless catalogue of burdensome rules. There are many examples of systemic waste taking place within the federal bureaucracy. For example, since its creation by Jimmy Carter, the Department of Education has managed to piss away trillions of dollars while student performance has declined. The Small Business Administration has doled out millions of dollars in subsidized loans to super-centenarians as well as children. The U.S. Postal Service keeps losing money and mail while deliveries slow to a crawl. Big projects become mired in endless iterations of reviews and revisions, such as Obama’s infrastructure plan and Joe Biden’s infrastructure and rural broadband initiative.

And again, regulatory agencies are often our worst enemies, imposing burdensome requirements with which only the largest industry players can afford to comply. Indeed, the savings achieved through the DOGE process might pale in comparison to the resources that could be liberated by rationalizing the tangle of regulations now choking private business.

A significant narrowing of the budget deficit would be a major accomplishment for DOGE. Even one-time savings to help pay down the public debt are worthwhile. In this latter regard, I hope DOGE’s work with the Department of Interior helps facilitate the sale of dormant federal assets. This includes land (not parks) and buildings worth literally trillions of dollars, and sometimes costing billions annually to maintain.

It’s been underway in various forms for a long time, at least since the early 1980s. It’s a basic variant of what the National Library of Medicine once called “creative financing” by some states “to get more federal dollars than they otherwise would qualify for” under Medicaid. It was evenrecognized as a scam by Joe Biden during Barack Obama’s presidency, and more recently by a number of legislators. Perhaps DOGE can do something to bring it under scrutiny, but ending it would probably take legislation.

Here’s the gist of it: increases in state Medicaid reimbursements qualify for a federal match at a rate known as the Federal Medical Assistance Percentage (FMAPs). First, increases in Medicaid reimbursements must be funded at the state level. To do this, states tax Medicaid providers, but then the revenue is kicked back to providers in higher reimbursements. The deluge of matching federal dollars follows, and states are free to use those dollars in their general budgets.

FMAPs vary based on state income level, so states with poorer residents have higher matching rates. The minimum FMAP is 50%, and it ranges up to 90% for marginal reimbursements falling under expanded Medicaid under Obamacare. The dollar value of the federal match is not capped.

“Let’s say, for example, a state imposes a provider tax on hospitals that raises $100 million. And then it returns that $100 million to the hospitals in the form of higher Medicaid reimbursement rates. There’s been no increase in benefits. Providers aren’t better off. But the state gets an extra $50 million from the federal government’s matching fund, money that it can use for anything it wants.“

However, whatever the increment to state coffers, and no matter what state programs are funded as a result, the increment is always expressed as a federal contribution to state Medicaid spending. That bit of shading helps cover for the convoluted and pernicious nature of the scheme. The lack of transparency is obvious, cloaking the circular nature of the flow of funds from providers to states and then back to providers. It’s possible that the arrangement inflates total annual Medicaid costs by as $50 – $65 billion a year, or by 6% – 8%.

Of course, this is also a blatant example of bureaucratic waste, and the allocation of “supplemental reimbursements” are a potential seedbed for cronyism and graft.

It would be better for the federal government to simply give states the money under block grants without the rigmarole. But of course that would change the character of the rent seeking already taking place, and the political daylight might not serve beneficiary states and providers well.

Putting aside the deception inherent in the funding mechanism, states vary tremendously in their reliance on federal matching revenue. States with large populations and high average incomes rely more heavily on the circular inflating of Medicaid reimbursements. California and New York lead the way in both Medicaid provider taxes and federal matching funds. Alaska, however, imposes no Medicaid provider taxes, and smaller states like Wyoming collect little in provider taxes.

High income states receive lower FMAPs, which seemingly encourages both higher Medicaid provider taxes and more “generous” provider reimbursements in order to harvest more federal matching funds. In addition, states have an incentive to participate in expanded Medicaid under the Affordable Care Act in order to receive higher matching rates.

The reciprocal nature of state-level Medicaid provider taxes and provider reimbursements implies a substantial but fictitious component of state Medicaid costs. The purpose is to qualify for federal matching dollars under Medicaid. The governments of 49 states have carried on with this escapade for years. Their misguided defenders insist that the federal contribution is necessary to protect benefits that states might otherwise have to cut. But even that stipulation would not justify the pairing of taxes on and reimbursements to Medicaid providers, which inflates the spending base upon which federal reimbursements are calculated. You have to wonder whether federal taxpayers should forgive the overstatement of costs and misallocation of funds.

Ongoing increases in the resources dedicated to health care in the U.S., and their prices, are driven primarily by the abandonment of market forces. We have largely eliminated the incentives that markets create for all buyers and sellers of health care services as well as insurers. Consumers bear little responsibility for the cost of health care decisions when third parties like insurers and government are the payers. A range of government interventions have pushed health care spending upward, including regulation of insurers, consumer subsidies, perverse incentives for consolidation among health care providers, and a mechanism by which pharmaceutical companies negotiate side payments to insurers willing to cover their drugs.

It’s not yet clear whether the Trump Administration and its “Make America Healthy Again” agenda will serve to liberate market forces in any way. Skeptics can be forgiven for worrying that MAHA will be no more than a cover for even more centrally-planned health care, price controls, and regulation of the pharmaceutical and food industries, not to mention consumer choices. Robert F. Kennedy Jr., who is likely to be confirmed by the Senate as Donald Trump’s Secretary of Health and Human Services, has strong and sometimes defensible opinions about nutrition and public health policies. He is, however, an inveterate left-winger and is not an advocate for market solutions. Trump himself has offered only vague assurances on the order of “You won’t lose your coverage”.

Government Control

The updraft in health care inflation coincided with government dominance of the sector. Steven Hayward points out that the cost pressure began at about the same time as Medicare came into existence in 1965. This significantly pre-dates the trend toward aging of the population, which will surely exacerbate cost pressures as greater concentrations of baby boomers approach or exceed life expectancy over the next decade.

Government now controls or impinges on about 84% of health care spending in the U.S., as noted by Michael F. Cannon. The tax deductibility of employer-provided health insurance is a massive example of federal manipulation and one that is highly distortionary. It reinforces the prevalence of third-party payments, which takes decision-making out of consumers’ hands. Equalizing the tax treatment of employer-provided health coverage would obviously promote tax equity. Just as importantly, however, tax-subsidized premiums create demand for inflated coverage levels, which raise prices and quantities. And today, the federal government requires coverages for routine care, going beyond the basic function of insurance and driving the cost of care and insurance upward.

The traditional non-portability of employer-provided coverage causes workers with uninsurable pre-existing conditions to lose coverage when they leave a job. Thus, Cannon states that the tax exclusion for employer coverage penalizes workers who instead might have chosen portable individual coverage in a market setting without tax distortions. Cannon proposes a reform whereby employer coverage would be replaced with deposits into tax-free Universal Health Accounts owned by workers, who could then purchase their own insurance.

In 2024, federal subsidies for health insurance coverage were about $2 trillion, according to the Congressional Budget Office (CBO). Those subsidies are projected to grow to $3.5 trillion by 2034 (8.5% of GDP). Joel Zinberg and Liam Sigaud emphasize the wasteful nature of premium subsidiesfor exchange plans mandated by the Affordable Care Act (ACA), better known as Obamacare. Subsidies were temporarily expanded in 2021, but only until 2026. They should be allowed to expire. These subsidies increase the demand for health care, but they are costly to taxpayers and are offered to individuals far above the poverty line. Furthermore, as Zinberg and Sigaud discuss, subsidized coverage for the previously uninsured does very little to improve health outcomes. That’s because almost all of the health care needs of the formerly uninsured were met via uncompensated care at emergency rooms, clinics, medical schools, and physician offices.

Proportionate Consumption

Perhaps surprisingly, and contrary to popular narratives, health care spending in the U.S. is not really out-of-line with other developed countries relative to personal income and consumption expenditures (as opposed to GDP). We spend more on health care because we earn and consume more of everything. This shouldn’t allay concern over health care spending because our economic success has not been matched by health outcomes, which have lagged or deteriorated relative to peer nations. Better health might well have allowed us to spend proportionately less on health care, but this has not been the case. There are explanations based on obesity levels and diet, but important parts of the explanation can be found elsewhere.

It should also be noted that a significant share of our decades-long increases in health care spending can be attributed to quantities, not just prices, as explained at the last link above.

Health Consequences

The ACAdid nothing to slow the rise in the cost of health care coverage. In fact, if anything, the ACA cemented government dominance in a variety of ways, reinforcing tendencies for cost escalation. Even worse, the ACA had negative consequences for patient care. David Chavous posted a good X thread in December on some of the health consequences of Obamacare:

1) The ACA imposed penalties on certain hospital readmissions, which literally abandoned people at death’s door.

2) It encouraged consolidation among providers in an attempt to streamline care and reduce prices. This reduced competitive pressures, however, which had the “unforeseen” consequence of raising prices and discouraging second opinions. The former goes against all economic logic while the latter goes against sound medical decision-making.

3) The ACA forced insurers to offer fewer options, increasing the cost of insurance by encouraging patients to wait until they had a pre-existing condition to buy coverage. Care was almost certainly deferred as well. Ultimately, that drove up premiums for healthy people and worsened outcomes for those falling ill.

4) It forced drug companies to negotiate with Pharmacy Benefit Managers (PBMs) to get their products into formularies. The PBMs have acted as classic middlemen, accomplishing little more than driving up drug prices and too often forcing patients to skimp on their prescribed dosage, or worse yet, increasing their vulnerability to lower-priced quackery.

The Insurers

So the ACA drastically increased the insured population (including the new burden of covering pre-existing conditions). It also forced insurers to meet draconian cost-control thresholds. Little wonder that claim rejection increased, a phenomenon often at the root of public animosity toward health insurers. Peter Earle cites several reasons for the increase in denial rates while noting that claim rejection has made little difference in insurer profit margins.

Matt Margolis points out that under the ACA, we’ve managed to worsen coverage in exchange for higher premiums and deductibles. All while profits have been capped. Claim denials or delays due to pre-authorization rules (which delay care) have become routine following the implementation of Obamacare.

Perhaps the biggest mistake was forcing insurers to cover pre-existing conditions without allowing them to price for risk. Rather than forcing healthy individuals to pay for risks they don’t face, it would be more economically sensible to directly subsidize coverage for those in high-risk pools.

Noah Smith also defends the health insurers. For example, while UnitedHealth Group has the largest market share in the industry, its net profit margin of 6.1% is only about half of the average for the S&P 500. Other major insurers earn even less by this metric. Profits just don’t explain why American health care spending is so high. Ultimately, the services delivered and charges assessed by providers explain high U.S. health care spending, not insurer profits or administrative costs.

Under the ACA, insurance premiums pay the bulk of the cost of health care delivery, including the cost of services more reasonably categorized as routine health maintenance. The latter is like buying insurance for oil changes. Furthermore, there are no options to decline any of the ten so-called “essential benefits” under the ACA, thus increasing the cost of coverage.

Medical Records

Arnold Kling argues that the ACA’s emphasis on uniform, digitized medical records is not a productive avenue for achieving efficiencies in health care delivery. Moreover, it’s been a key factor driving the increasing concentration in the health care industry. Here is Kling:

“My point is that you cannot do this until you tighten up the health care delivery process, making it more rigid and uniform. And I would not try to do that. Health care does not necessarily lend itself to being commoditized. You risk making health care in America less open to innovation and less responsive to the needs of people.

“So far, all that has been accomplished by the electronic medical records drive has been to put small physician practices out of business. They have not been able to absorb the overhead involved in implementing these systems, so that they have been forced to lose their independence, primarily to hospital-owned conglomerates.”

Separating Health and State

The problem of rising health care costs in the U.S. is capsulized by Bryan Caplan in his call for the separation of health and state. The many policy-driven failures discussed above offer more than adequate rationale for reform. The alternative suggested by Caplan is to “pull the plug” on government involvement in health care, relying instead on the free market.

Caplan debunks a few popular notions regarding the appropriate role for markets in health care and health insurance. In particular, it’s often alleged that moral hazard and adverse selection would encourage unhealthy behaviors and encourage the worst risks to over-insure, causing insurance markets to fail. But these problems arise only when risk is not priced efficiently, precisely what the government has accomplished by attempting to equalizing rates.

Pulling the plug on government interference in health care would also mean deregulating both insurance offerings and pricing, encouraging the adoption of portable coverage, expediting drug approvals based on peer-country approvals, reforming pharmacy benefit management, ending deadly Medicare drug price controls, and encouraging competition among health care providers.

Value Vs. Volume

There are a host of other reforms that could bring more sanity to our health care system. Many of these are covered here by Sebastian Caliri, with some emphasis on the potential role of AI in improving health care. Some of these are at odds with Kling’s skepticism regarding digitized health records.

Perhaps the most fundamental reforms entertained by Caliri have to do with health care payments. One is to make payments dependent on outcomes rather than diagnostic codes established and priced by the American Medical Association. To paraphrase Caliri, it would be far better for Americans to pay for value rather than volume.

Another payment reform discussed by Caliri is expanding direct payments to providers such as capitation fees, whereby patients pay to subscribe to a bundle of services for a fixed fee. Finally, Caliri discusses the importance of achieving “site-neutral payments”, eliminating rules that allow health systems to charge a higher premium relative to independent providers for identical services.

For what it’s worth, Arnold Kling disagrees that changing payment metrics would be of much help because participants will learn to game a new system. Instead, he emphasizes the importance of reducing consumer incentives for costly treatments having little benefit. No dispute there!

Avoid the Single-Payer Calamity

I’ll close this jeremiad with a quote from Caliri’s piece in which he contrasts the knee-jerk, leftist solution to our nation’s health care dilemma with a more rational, market-oriented approach:

“Single payer solutions and government control favored by the left are no solutions at all. Moving to a monopsonist system like Canada is a recipe for strangling innovation and rationing access. Just ask our neighbors to the north who have to wait a year for orthopedic surgery. The UK’s National Health Service (NHS) is teetering on the brink of collapse. We need to sort out some other way forward.

“Other parts of the economy provide inspiration for what may actually work. In the realm of information technology, for example, fifty years has taken us from expensive four operation calculators to ubiquitous, free, artificial intelligence capable of passing the Turing Test. We can argue about the precise details but most of this miracle came from profit-seeking enterprises competing in a free market to deliver the best value for the buyer’s dollar.“

Wow! We’re less than a week from Election Day! I’d hoped to write a few more detailed posts about the platforms and policies of Kamala Harris and Donald Trump, but I was waylaid by Hurricane Milton. It sent us scrambling into prep mode, then we evacuated to the Florida Panhandle. The drive there and back took much longer than expected due to the mass exodus. On our return we found the house was fine, but there was significant damage to an exterior structure and a mess in the yard. We also had to “de-prep” the house, and we’ve been dealing with contractors ever since. It was an exhausting episode, but we feel like we were very lucky.