Tags

Capitalism, Daniel Waldenström, Housing Assets, income inequality, Pension Assets, Popular Assets, Progressive Taxation, regulation, rent seeking, Social Security, Wealth Concentration, Wealth Inequality

My theme in “What’s To Like About Income Inequality?” was the existence of natural drivers of an unequal distribution of income, as where institutions reward merit and legal systems assign strong property rights. I also discussed trends in income and wealth inequality and how standard measures of inequality are distorted by income taxes and transfer payments, including differences in unrealized and realized capital gains. Furthermore, income mobility makes “snapshots” of inequality less compelling, as individuals are not “stuck” for all time at a point in the income distribution, but are typically moving across the distribution and usually upward as they age through their working years.

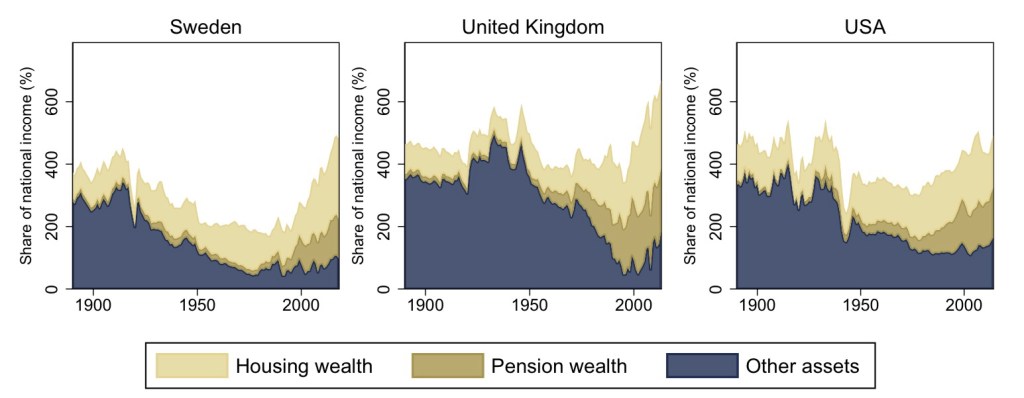

Wealth inequality is another matter, but a new paper by Daniel Waldenström entitled “Wealth and History: An Update” shows that wealth concentration, which he defines as the share of wealth held by the top 1%, declined markedly between 1920 and 1970 in Europe and the U.S. After 1970, however, the share remained flat in Europe and was flat in the U.S. as well if unfunded pensions and Social Security benefits are valued as wealth. However, the near-entirety of the earlier decline in U.S. wealth concentration occurred by about 1950.

So a great thinning in the fat right tail of the wealth distribution occurred during the middle years of the 20th century. Waldenström attributes this transition to growth of homeownership and pension assets. These are so-called “popular assets” because they are held more broadly than the legacy wealth of the 1800s and early twentieth century:

“… the structure of private wealth has changed over the twentieth century, from being dominated by elite fortunes in agriculture or businesses to consisting mainly of widely dispersed assets in housing and funded pensions.”

Waldenström concludes that the facts run contrary to claims that wealth inequality has worsened in Western, capitalist economies over the years:

“These new findings have implications for the historiography of Western wealth accumulation and wealth concentration. They cast doubt over the view that an unfettered capitalism, such as in pre-democratic and pre-taxation nineteenth-century Europe, generates extreme levels of capital accumulation. The new findings also question the pivotal role of wars, crises and progressive taxation as the sole important factors behind the wealth equalization of the twentieth century.

Waldenström considers the role of progressive taxation in equalizing wealth, but he acknowledges that taxes undermined wealth accumulation at all levels, so the effect was ambiguous. A point on which I’d take issue with Waldenström is the role of regulation, which he believes “curbed the growth of large fortunes”. That might be true in some cases, but this effect is also subject to ambiguity. Regulation is often welcomed by powerful market players as a way of consolidating market position and hindering new competition. The regulatory state has long been considered a primary channel for rent seeking, so the impact on the wealth distribution is likely to be mixed.

Market institutions, together with rising education levels, labor reforms, and gains in productivity enabled this broadening in the accumulation and distribution of wealth. Social Security certainly played a part as well, though we don’t know how private pensions might have evolved in its absence. Of course, Social Security has a terrible record as an “investment” of payroll taxes. Private control over the investment direction of those funds would have done far better, and still could, which would be a further boon to wealth for the lower 99%.

It is true that inequality in both income and wealth is to be expected under merit-based systems of rewards. However, Daniel Waldenström’s paper offers evidence that markets do not merely concentrate wealth at the expense of workers. Rather, they deliver gains to all participants, who are in turn free to accumulate wealth in the kinds of “popular assets” discussed by Waldenström.