I’ve noted a number of policy moves by Donald Trump that I find aggravating (scroll my home page), but I still applaud his administration’s agenda to downsize government, promote operational efficiency, and deregulate the private economy. It’s just too bad that Trump demonstrates a penchant for expanding government authority in significant ways, which makes it harder to celebrate successes of the former variety. Beyond that, there have been huge obstacles to rationalizing the administrative state. We’ve seen progress in some areas, but the budgetary impact has been disappointing.

Grinding On

The Department of Government Efficiency (DOGE) was to play a large role in the effort to reduce fraud and inefficiency at the federal level. On the surface, it’s easy to surmise that DOGE has failed in its mission to root out government waste. After seven months, DOGE touts that it has saved taxpayers $205 billion thus far. That is well short of the original $2 trillion objective (subsequently talked down by Elon Musk), but it was expected to take 18 months to reach that goal. Still, the momentum has slowed considerably.

Moreover, the $205 billion figure does not represent recurring budgetary savings. Some of it is one-time proceeds from property sales or grant cancellations. Some of it ($30 billion) seems to represent savings in regulatory compliance costs to Americans, but that’s not clear as the DOGE website is lightly documented, to put it charitably. A recent analysis reached the conclusion that DOGE had exaggerated the savings it has claimed for taxpayers, which seems plausible.

But DOGE is still plugging away, reviewing federal contracts, programs, regulations, payments, grants, workforce deployment, and accounting systems. The work is desperately needed given the fraud that’s been exposed among the agency workforce, which seemed to escalate following the advent of massive Covid benefit payments during the pandemic. Some details of an investigation by the Senate DOGE Caucus, discussed at this link, are truly astonishing. Employees at multiple state and federal agencies have been collecting food stamps, survivor benefits, and even unemployment benefits while employed by government. Apparently, this was made possible by the lack of list de-duplication by the federal agencies that dole out these benefits. This might be a pretty good explanation for the lawsuits filed by federal employee unions attempting to prevent DOGE from accessing agency records. Congratulations to Senator Joni Ernst, Chairman of the Caucus, for her leadership in exposing this graft.

False Aspersions

Shortly after DOGE was constituted, most of its employees were assigned to individual agencies to identify opportunities to reduce waste and promote efficiency. This has led to confusion about the extent to which DOGE should take credit for certain savings maneuvers. However, contrary to some allegations, no DOGE employees have been “embedded” as career civil servants.

Since almost the start of Trump’s second term, DOGE has been blamed for workforce reductions that some deemed reckless and arbitrary. There were indeed some early mistakes, most notably at HHS, but a number of those key workers were rehired. Many of the force reductions were instigated by individual agencies themselves, and many of those were voluntary separations with generous severance packages.

As to the “arbitrary” nature of the force reductions, one former DOGE staffer described the difficulty of making sensible cuts at the Veterans Administration under agency rules:

“Then came a reality check about RIF rules, which turned out to be brutally deterministic:

Tenure matters most—new hires were cut first

Veterans’ preference comes next; vets are protected over non-vets

Length of service trumps performance—seniority beats skill

Performance ratings break any remaining ties

“These reduction-in-force rules–which stem from the Veterans’ Preference Act of 1944–surprised me and many others. Unlike private industry layoffs that target middle management bloat and low performers, the government cuts its newest people first, regardless of performance. Anyone promoted within the last two years was also considered probationary—first in line to go.“

It would be hard to be less arbitrary than these rules. Other agencies are subject to similar strictures on reductions in force. No wonder the Administration relied heavily on a buyout offer (“deferred resignation”) with broad eligibility in its attempt to downsize government. Furthermore, the elimination of positions was largely targeted functions that were wasteful of taxpayer resources, such as promoting DEI objectives and administering grants to NGOs driven by ideological motives.

Of course, the buyouts come with a cost to taxpayers. In fact, one report asserted that DOGE’s efforts themselves cost taxpayers $135 billion or more. Of course, buyouts carry a one-time cost. However, that figure also includes a questionable estimate of lost productivity caused by turmoil at federal agencies. I’m just a little skeptical when it comes to claims about the productivity of the federal workforce.

Obstacles

DOGE has had to grapple with other severe limitations, as Dan Mitchell has commented. These are primarily rooted in the spending authority of Congress. Only one rescission bill reflecting DOGE cuts, totaling just $9 billion, has made it to Trump’s desk. Another “untouchable” for DOGE is interest on the federal debt, which has become a huge portion of the federal budget.

Furthermore, DOGE is guilty of one self-imposed obstacle: the main driver of ongoing deficits is entitlement spending, While the Big Beautiful Bill included Medicaid reforms, the Trump Administration and Congress have shown little interest in shoring up Social Security and Medicare, both of which are technically insolvent. While DOGE would seem to have limited authority over entitlements, as opposed to the discretionary budget, some charge that DOGE made a critical error in failing to address entitlement fraud. According to Veronique de Rugy:

“It is insane not to have started there. Given DOGE’s comparative advantage in data analytics and [information technology], this is where it can have the greatest impact… Cracking down on this waste isn’t just about saving money; it’s about restoring integrity to safety-net programs and protecting taxpayers. And if fixing this problem is not quintessential ‘efficiency,’ what is?“

On the Bright Side

Michael Reitz offered a different perspective. He cited the difficulty of reforming an entrenched bureaucracy. He also noted the following, however, as a kind of hidden success of DOGE and Elon Musk:

“But others I spoke with thought Musk’s four months in government were both substantive and symbolic. He changed the conversation about waste and grift. Musk made cuts cool again, especially for Republican politicians who have forgotten fiscal restraint. He highlighted the need to follow the data and oppose bureaucrats who impede reform by controlling the flow of information.“

Of course, DOGE has been instrumental in identifying absurdly wasteful federal contracts, even if they are “small change” relative to the size of the federal budget. This includes grants to NGOs that appear to have functioned primarily as partisan slush funds. DOGE has also helped identify deregulatory actions to eliminate duplicative or contradictory agency rules on industry, reducing costly economic burdens on the private sector. The DOGE website claims (preliminarily) that it has deleted 1.9 million words of regulation, but doesn’t provide a total number of rules eliminated.

An important part of DOGE’s mission was to modernize technology, software, and accounting systems at federal agencies. This included centralization of these systems with improved tracking of payments and a written justification for each payment. These efforts were met with hostility from some quarters, including lawsuits to limit or prevent DOGE personnel from accessing agency data. Nevertheless, DOGE has pushed ahead with the initiative. This is a laudable attempt to not only modernize systems, but to encourage transparency, accountability, and efficiency.

In a related development, this week DOGE was blamed by a whistleblower for uploading a file from Social Security containing sensitive information to an unsecured cloud environment. However, a spokesperson for the Social Security Administration stated that the data was secure and that the SSA had no indication that it had been breached. We shall see.

AI Scrutiny

Now, DOGE is recommending the use of an AI tool to cut federal regulations. According to Newsweek:

“The ‘DOGE AI Deregulation Decision Tool,’ developed by engineers brought into government under Elon Musk’s DOGE initiative, is programmed to scan about 200,000 existing federal rules and flag those that are either outdated or not legally required.“

Critics are concerned about accuracy and legal complexities, but the regulations flagged by the AI tool will be reviewed by attorneys and other agency personnel, and there will be an opportunity for public comment. The process could make deregulatory progress well beyond what would be possible under purely human review. DOGE believes that up to 100,000 rules could be eliminated, saving trillions of dollars in compliance costs. If successful, this might well turn out to be DOGE’s signal accomplishment.

Conclusion

I’m disappointed at the flagging momentum of DOGE’s quest to eliminate inefficiencies in the executive branch. I’m also frustrated by the limited progress in translating DOGE’s work into ongoing deficit reduction. In addition, it was a mistake to leave aside any scrutiny of improper entitlement payments. Nevertheless, DOGE has has some significant wins and the effort continues. Also, it must be acknowledged that DOGE has faced tremendous obstacles. For too long, government itself has metastasized along with bureaucratic inefficiencies and graft. That is the rotten fruit of the symbiosis between rent seeking behavior and a bloated public sector. We should applaud the spirit motivating DOGE and encourage greater progress.

The GOP’s “Big Beautiful Bill” (BBB) has generated its share of controversy, not least between President Trump and his erstwhile ally Elon Musk. It is a budget reconciliation bill that was passed by a single vote in the House of Representatives. It’s now up to the Senate, which is sure to alter some of the bill’s provisions. That will require another vote in the House before it can head to Trump’s desk for a signature.

Slim But “Reconciled” Majority

As a reconciliation bill, the BBB is not subject to filibuster in the Senate, and only a simple majority is required for approval, not a 60% supermajority. Obviously, that’s why the GOP used the reconciliation process.

I hate big bills, primarily because they tend to provide cover for all sorts of legislative mischief and pork. However, the reconciliation process imposes limits on what kinds of budgetary changes can be included in a bill. A reconciliation bill can alter only mandatory spending programs like Medicaid and other entitlements, but not discretionary or non-mandatory spending. Social Security is an entitlement, but it would be off limits in a typical reconciliation bill (owing to an arcane rule). Reconciliation bills can also address changes in revenue and the debt limit.

The BBB includes provisions to reduce Medicaid outlays such as work requirements, denial of benefits to illegal aliens, and controls on fraud. These are projected to cut spending by nearly $700 billion. Of course, this is a controversial area, but efforts to impose better controls on entitlements are laudable.

Elon Musk criticized the bill’s failure to aggressively rein-in deficit spending, prompting what was probably his first public feud with Trump. At the time, it wasn’t clear whether Musk really understood the limits of reconciliation. If he had, he might at least have been mollified by the effort to tackle Medicaid waste and fraud. Entitlement programs like Medicaid are, after all, at the very root of our fiscal imbalances.

Extending Trump’s Tax Cuts

The Congressional Budget Office (CBO) says that BBB will reduce tax revenue by $3.8 trillion over the next ten years. The Trump tariffs are not addressed in the BBB, but those won’t come close to offsetting this projected revenue loss.

The CBO’s score compares spending and tax revenue to “current law”. Thus, the baseline assumes that the 2017 tax cuts under the Tax Cuts and Jobs Act (TCJA) expire in 2026. With spending cuts under the BBB, primary federal deficits (non-interest) are projected to rise $2.4 billion over that time. With interest costs on the higher federal debt, the increase in deficits rises to about $3 trillion. I’ll briefly address some of the major provisions below, including their budget impacts.

Spending Cuts

In addition to Medicaid, other significant cuts in spending in the BBB include reductions in benefits under the Supplemental Nutritional Assistance Program (food stamps, -$267b). This includes tighter work requirements, eligibility rules, and higher matching requirements for states. Also included in BBB are more stringent student loan repayment rules and changes in other education funding programs (-$350b).

Other spending categories would increase. The bill would authorize an additional $144 billion for Armed Services and $79 billion for Homeland Security, including $50 billion for the border wall. Senator Rand Paul has called the border security provisions excessive, though many of those favoring greater fiscal discipline also believe defense is underfunded, so they probably don’t oppose these particular items.

Voting Tax Incentives

In terms of revenue, the BBB would extend the provisions of the TCJA. The deduction for state and local taxes (SALT) would be extended and increased to $40,000 at incomes less than $500,000. This would have a combined revenue impact of -$787 billion. No wonder deficit hawks are upset! A larger SALT deduction creates an even greater subsidy for states imposing high tax burdens on their residents. There’s an expectation, however, that this provision will be dialed back to some extent in the Senate version of the BBB.

There are also provisions to eliminate taxes on overtime (-$124b) and tip income (-$40b), and to increase the standard deduction for seniors (-$66b). As I’ve written before, these are all terribly distortionary policies. They would treat different kinds of income differently, create incentives to reclassify income, and impose a highly complex administrative burden on the IRS. The senior deduction creates an incremental revenue hole as a function of Social Security benefit payments. This is the wrong way to address the needs of a system that is insolvent. These policies were selected primarily with vote buying in mind.

Another notable change would eliminate subsidies and tax credits for EVs (+$191b). Some claim this was at the heart of Musk’s diatribes against the BBB. However, Musk has supported elimination of both EV subsidies and mandates for many years. Hestated as much to legislators on Capital Hill last December, so this theory regarding Musk’s opposition to BBB doesn’t wash.

Defining a Baseline

Advocates of extending the TCJA say the CBO’s baseline case is inappropriate, and that the proper baseline should incorporate the continued tax provisions of the TCJA. Again, the extension increases the ten-year deficit by $3.8 trillion, but that total includes the revenue effects of other provisions. Perhaps $3 trillion might be a more accurate upward adjustment to baseline deficits. In that case, the BBB would actually reduce ten-year deficits by $0.2 trillion.

Another criticism is that the CBO does not attempt to estimate dynamic changes in revenue induced by policy. Those in support of extending the TCJA believe that this static treatment unfairly discounts the revenue potential of pro-growth policies.

I don’t have a problem with the alternative baseline, but the fact is that deficits will still be problematic. Over the 2025-2034 time frame, a baseline incorporating an extension of TCJA would yield deficits in excess of $20 trillion. That includes mounting interest costs, which might overwhelm serious efforts at fiscal discipline in the unlucky event of an updraft in interest rates. Of course, these large, ongoing deficits raise the likelihood of inflationary pressure. The recent downgrade in the credit rating assigned to U.S. Treasuries by Moody’s is an acknowledgement that bondholder wealth could well be undermined by future attempts to “inflate away” the real value of the debt.

Debt Ceiling

In addition to its direct budgetary effects, the BBB calls for a $5 trillion increase of the federal debt limit. I admit to mixed feelings about this large increase in borrowing authority. Frequent debt limit negotiations tend to create lots of political theater and chew up scarce legislative time. Moreover, it’s easy to conclude that they usually accomplish little in terms of restraining deficit spending. Dominic Pino argues otherwise, citing historical examples in which the debt limit “was paired with” reforms and spending restraint. In other words, despite its apparent impotence, Pino asserts that deficits would have been much higher without it. I’m still skeptical, however, that frequent showdowns over the debt ceiling have much value given entitlements that are seemingly beyond legislative control. In the end, elected representatives must respect the judgement of credit markets and face consequences at the ballot box.

Final Thoughts on BBB

Superficially, the Big Beautiful Bill looks like an abomination to deficit hawks. The GOP decided to structure it as a reconciliation bill to strengthen its odds of passage. That decision sharply limited its potential for spending restraint. Other legislation will be required to make the kinds of rescissions necessary to eliminate wasteful spending identified by DOGE.

As for the bill itself, the effort to extend the 2017 Trump tax cuts was widely expected. That, in and of itself, is neutral with respect to a more reasonable baseline assumption. Elimination of EV tax subsidies is a big plus, as are the permanent incentives for business investment. Unfortunately, Trump and his congressional supporters also propose to create the additional fiscal burdens of no taxes on tips and overtime pay, as well as an increased standard deduction for seniors. The ill-advised increase in the SALT deduction was a compromise to ensure the support of certain blue-state republicans, but with any luck it will be curtailed by the Senate.

On the spending side, the big item is Medicaid. Reforms are long past due for a system so riddled with waste. In addition, there are new rules in the BBB that would reduce SNAP outlays and increase student loan repayments. Outlays for defense, Homeland Security, and border security would increase, but these were known to be Trump priorities. Too bad they’ve been paired with several wasteful tax policies.

But even with those flaws, the BBB would reduce deficits marginally relative to a baseline that incorporates extension of the TCJA. Yes, excessive ongoing deficits still have to be dealt with, but spending reductions on the discretionary side of the budget were out of the question this time due to reconciliation rules. They will have to come later, but that sort of legislation will face tough political headwinds, as will Social Security and Medicare reform. arever introduced.

I prefer a government that is limited in size and scope, sticking closely to the provision of public goods without interfering in private markets. Therefore, I’m delighted with the mission of the Department of Government Efficiency (DOGE), a rebranded version of the U.S. Digital Service created by Barack Obama in 2014 to clean up technical issues then plaguing the Obamacare web site. The “new” DOGE is fanning out across federal agencies to upgrade systems and eliminate waste and fraud.

I’m seeing scary posts about DOGE even on LinkedIn, such as the plight of Americans unable to get federal public health communications due to layoffs at HHS, while failing to mention the thousands of new HHS employees hired by Biden in recent years. As if HHS was particularly effective in dispensing good public health advice during the pandemic!

Those kinds of assertions are hard to take seriously. For reasons like these and still others, I tend to dismiss nearly all of the horror stories I hear about DOGE’s activities as nitwitted virtue signals or propaganda.

Many on the left claim that DOGE’s work is careless, and especially the force reductions they’ve spearheaded. For example, they claim that DOGE has failed to identify key employees critical to the functioning of the bureaucracy. The tone of this argument is that “this would not pass muster at a well-managed business”. A “sober” effort to achieve efficiencies within the federal bureaucracy, the argument goes, would involve much more consideration. In other words, given political realities, it would not get done, and they really don’t want it to get done.

The best rationale for the ostensible position of these critics might be situations like the dismissal of several thousand provisional employees at the FDA, a few of whom were later rehired to help manage the work load of reviewing and approving drugs. However, thus far, only a tiny percentage of the federal force reductions under consideration have involved immediate layoffs.

Of course, DOGE is not being tasked to review the practices of a well-managed business or a well-managed governmental organization. What we have here is a dysfunctional government. It is a bloated, low productivity Leviathan run by management and staff who, all too frequently, seem oblivious to the predicament. Large force reductions at all levels are probably necessary to make headway against entrenched interests that have operated as a fourth branch of government.

Thus, I see the leftist critique of Trump’s force reductions as something of a strawman, and it falls flat for several other reasons. First, the vast bulk of the prospective reduction in headcount will be voluntary, as the separating employees have been offered attractive severance packages. Second, force reductions in the private sector always feel chaotic, and they often are. And they are sometimes executed without regard to the qualifications of specific employees. Tough luck!

Duplicative functions, poor data systems, and a lack of control have led to massive misappropriations of funds. The dysfunction has been enabled by a metastasization of nests of administrative authority inside agencies with “incomprehensible” org charts, often having multiple departments with identical functions that do not communicate. These departments frequently use redundant but unconnected systems. A related problem is the inadequacy of documentation for outgoing payments. Needless to say, this is a hostile environment for effective spending controls.

It’s worth emphasizing, by the way, DOGE’s “open book” transparency. It’s not as if Elon Musk and DOGE are attempting to sabotage the deep state in the dark of night. Indeed, they are shouting from the rooftops!

Doing It Fast

Every day we have a new revelation from DOGE of incredible waste in the federal bureaucracy. Check out this story about a VA contact for web site maintenance. All too ironically, what we call government waste tends to have powerful, self-interested, and deeply corrupt constituencies. This makes speed an imperative for DOGE. In a highly politicized and litigious environment, the extent to which the Leviathan can be brought to heel is partly a function of how quickly the deconstruction takes place. One must pardon a few temporary dislocations that otherwise might be avoided in a world free of rent seeking behavior. Otherwise, the graft (no, NOT “grift”) will continue unabated.

The foregoing offers sufficient rationale not only for speedy force reductions, but also for system upgrades, dissolution of certain offices, and consolidation of core functions under single-agency umbrellas.

The Bloody Budget

It’s difficult to know when budget legislation will begin to reflect DOGE’s successes. The actual budget deficit might be affected in fiscal year 2025, but so far the savings touted by DOGE are chump change compared to the expected $2 trillion deficit, and only a fraction of those savings contribute to ongoing deficit reduction.

Uncontrolled spending is the root cause of the deficit, as opposed to insufficient tax revenue, as evidenced by a relatively stable ratio of taxes to GDP. The spending problem was exacerbated by the pandemic, but Congress and the Biden Administration never managed to scale outlays back to their previous trend once the economy recovered. Balancing the budget is made impossible when the prevailing psychology among legislators and the media is that reductions in the growth of spending represent spending cuts.

Federal spending is excessive on both the discretionary and mandatory sides of the budget. Ultimately, eliminating the budget deficit without allowing the 2017 Trump tax cuts to expire will require reform to mandatory entitlements like Social Security, Medicare, and Medicaid, as well as reductions across an array of discretionary programs.

DOGE’s focus on fraud and waste extends to entitlements. At a minimum, the data and tracking systems in place at HHS and SSA are antiquated, sometimes inaccurate, and are highly susceptible to manipulation and fraud. Systems upgrades are likely to pay for themselves many times over.

But all indications are that it’s much worse than that.Social security numbers were issued to millions of illegal immigrants during the Biden Administration, and those enrollees were cleared for maximum benefits. There were a significant number of illegals enrolled in Medicaid and registered to vote. While some of these immigrants might be employed and contributing to the entitlement system, they should not be employed without legal status. Of course, one can defend these entitlement benefits on purely compassionate grounds, but the availability of benefits has served to attract a massive flow of illegal border crossings. This illustrates both the extent to which the entitlement system has been compromised as well as the breakdown of border security.

On the discretionary side of the budget, DOGE has identified an impressive array programs that were not just wasteful, but by turns ridiculous or politically motivated (for example, the bulk of USAID’s budget). Many of these funding initiatives belong on the chopping block, and components that might be worthwhile have been moved to agencies with related missions. In addition, authorized but unspent allocations have been identified that seem to have been held in reserve, and which now can be used to reduce the public debt.

Research Grants?

Of course, like the initial scale of the FDA layoffs, a few mistakes have and will be made by DOGE and agencies under DOGE’s guidance. Many believe another powerful argument against DOGE is the Trump Administration’s 15% limit on indirect costs as an add-on to NIH grants. Critics assert that this limit will hamstring U.S. scientific advancement. However, it won’t “kill” publicly funded research. Asthis article in Reason points out, historically public funding has not been critical to scientific advancement in the U.S. In fact, private funding accounts for the vast bulk of U.S. R&D, according to the Congressional Research Service. Moreover, it’s broadly acknowledged that indirect costs are subject to distortion, and that generous funding of those costs creates bad incentives and raises thorny questions about cross-subsidies across funders (15% is the rate at which charities typically fund indirect costs).

No doubt some elite research universities will suffer declines in grants, but their case is weakened politically by a combination of lax control over anti-Semitic protests on campus, the growing unpopularity of DEI initiatives in education, and public awareness of the huge endowments over which these universities preside. Nevertheless, I won’t be surprised to see the 15% limit on indirect research costs revised upward somewhat.

More DOGE Please

I’ve criticized the numbers posted on DOGE’s website elsewhere. They could do a much better job of categorizing and reporting the savings they’ve achieved, and they have far to go before meeting the goals stated by Elon Musk. Be that as it may, DOGE is making progress. Here is a report on a few of the latest cuts.

As I’ve emphasized on numerous occasions, the federal government is a strangling mass of tentacles, squeezing excessive resources out of the private sector and suffocating producers with an endless catalogue of burdensome rules. There are many examples of systemic waste taking place within the federal bureaucracy. For example, since its creation by Jimmy Carter, the Department of Education has managed to piss away trillions of dollars while student performance has declined. The Small Business Administration has doled out millions of dollars in subsidized loans to super-centenarians as well as children. The U.S. Postal Service keeps losing money and mail while deliveries slow to a crawl. Big projects become mired in endless iterations of reviews and revisions, such as Obama’s infrastructure plan and Joe Biden’s infrastructure and rural broadband initiative.

And again, regulatory agencies are often our worst enemies, imposing burdensome requirements with which only the largest industry players can afford to comply. Indeed, the savings achieved through the DOGE process might pale in comparison to the resources that could be liberated by rationalizing the tangle of regulations now choking private business.

A significant narrowing of the budget deficit would be a major accomplishment for DOGE. Even one-time savings to help pay down the public debt are worthwhile. In this latter regard, I hope DOGE’s work with the Department of Interior helps facilitate the sale of dormant federal assets. This includes land (not parks) and buildings worth literally trillions of dollars, and sometimes costing billions annually to maintain.

No sooner had I posted this piece on the bond market’s bemused reaction to DOGE’s cost-cutting potential than Treasury rates began to drop sharply. The 10-year Treasury note fell by about 30 basis points over the course of a week. It’s stabilized and up a little since then, but that drop had little to do with DOGE and everything to do with uncertainty about Trumpian policies and signs of a flagging economy.

Despite those probable causes, the excitement of falling rates prompted the author of this article to dive headlong into fantasy: “Interest Rates Are Falling Thanks to Cuts in Government Spending”. I hope he’s right that real cuts in government spending will be forthcoming, but that’s highly speculative at this point.

In fact, markets are grappling with massive uncertainties at the moment. Under these circumstances, a preference for safety among investors means a flight to low-risk assets like treasuries, forcing their prices up and yields down.

Tariff threats against long-time allies and adversaries alike are a huge source of uncertainty for markets, especially given Trump’s unpredictable thrusts and parries. The burden of U.S. tariffs falls largely on American buyers and tariffs are of limited revenue potential. They have already prompted announcements of retaliation, so the possibility of a trade war is real, which would create a major disruption in economic activity. This portent comes atop growing signs that a slowdown is already underway in the U.S. economy. As Eric Boehm notes, tariffs are all costs and no benefits, and their mere prospect adds significant risk to the economic and political outlook.

Budgetary developments have also been unsettling to markets. Despite promises of reduced federal spending, signs point to even larger deficits. The budget resolution passed by the House of Representatives in late February calls for various spending reductions, but it would extend the Trump tax cuts and increase defense and border control spending. On balance, deficits under the bill would be higher by $4 trillion over 10 years. That is not reassuring, and Trump still wants to eliminate taxes on tips, overtime, and Social Security benefits, which would require separate legislation. State and local tax deductions are also a hot topic. All this obviously undermines the notion that investors should take a rosy view of the outlook for reduced Treasury borrowing under Trump. Of course, higher deficits would be expected to push Treasury rates upward, but the point here is that on balance, DOGE and the Trump Administration have yet to provide a convincing case that rates should decline.

Every week the administration finds a way to demonstrate its lack of seriousness with respect to paying off the public debt. First we had the $5,000 “DOGE dividend” to all Americans. And last week a Strategic Bitcoin Reserve was authorized by Executive Order, to be funded by crypto asset forfeitures and civil penalties. While this type of funding technically qualifies as “budget neutral”, the better alternative would be to put those funds toward paying off debt. In any case, the whole idea makes about as much sense as a Hawk Tuah coin reserve.

The desire for safe assets is perhaps made more urgent by the bellicosity of Trump’s foreign policy initiatives. His multiple mentions of World War III simply can’t go over well with risk-averse investors. Rightly or wrongly, he’s thrown down the gauntlet with both Iran and Hamas, and he’s taken a fairly confrontational line with Greenland, Panama, Canada, Mexico, Venezuela, China, Russia, and especially (and unfairly) Ukraine. Ah, yes, all in the spirit of negotiating deals. We shall see.

As for DOGE, I’m a big fan of its mission to reduce waste and fraud in government, though its reporting of specific accomplishments thus far has been shrouded by inconsistencies and confusion.DOGE claims to have secured $105 billion in savings in the first six weeks of the Trump presidency, but that figure includes asset sales, which can pay down debt but aren’t deficit reduction. It’s also not clear how adverse court orders are reflected in the figure. For that matter, the reported savings are not given with any time dimension. The real savings thus far certainly don’t add up to $105 billion per year. And even at face value, those savings won’t get DOGE to its goal of $2 trillion in deficit reduction by July 2026 without some spectacular wins along the way. Medicaid fraud might be a big one, but that remains to be seen. This report on DEI initiatives by agency also offers some promising targets. (But now, apparently DOGE’s goal has been scaled back to $1 trillion in savings).

And there is one other hurdle: even after DOGE and the Administration identify and impound amounts already authorized, the savings will not be permanent without congressional action on budgetary recissions. That could be tough.

So the bond market is rightly skeptical of whether DOGE and the Administration can achieve major and permanent reductions in federal deficits. The recent drop in rates has much more to do with the economy and an array of uncertainties surrounding the values of risk assets.

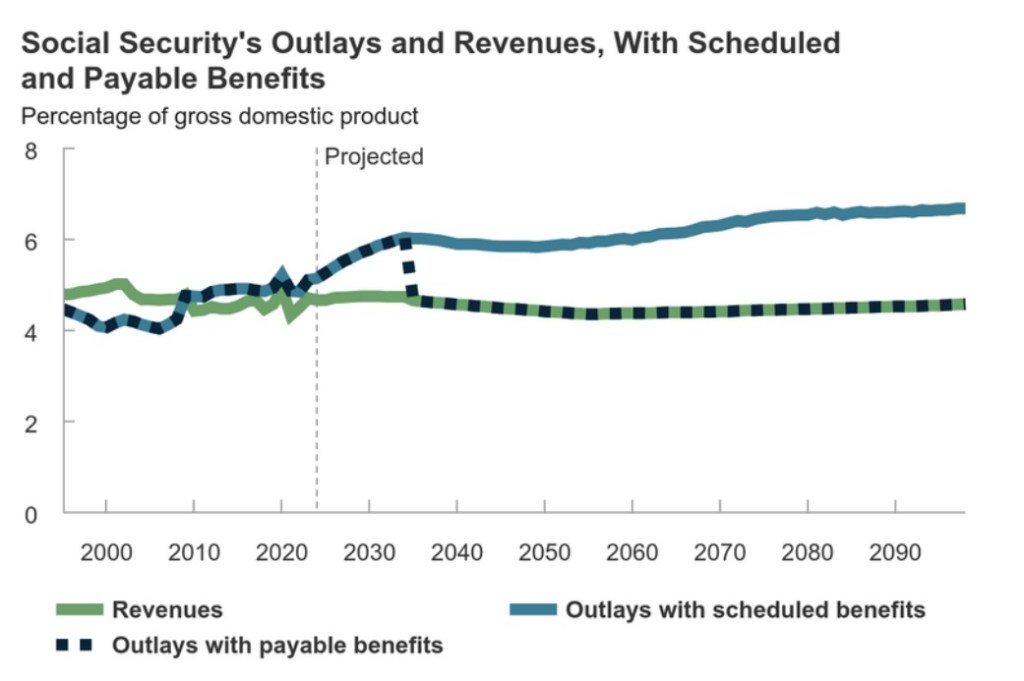

Social Security wasn’t designed as a true saving vehicle for workers. Instead, SS has always been a pay-as-you-go system under which current benefits are funded by the payroll taxes levied on the current employed population. In fact, many Americans earn lousy effective returns on their tax “contributions” (also see here), though low-income individuals do much better than those near or above the median income. Worst of all, under pay-as-you-go, the system can collapse like a Ponzi scheme when the number of workers shrinks drastically relative to the retired population, leading to the kind of situation we face today.

Unfunded Obligations

Payroll tax revenue is no longer adequate to pay for current Social Security and Medicare benefits, and the problem is huge: according to the Penn-Wharton Budget Model, the unfunded obligations of Social Security (including old age, survivorship and disability) through 2095 have a present value of $18.1 trillion in constant 2024 dollars (using a discount rate of 4.4%). The comparable figure for Medicare Part A is $18.6 trillion. Together these amount to more than the current national debt.

Barring earlier reform, the Social Security Trust Fund is expected to be exhausted in 2033 (excluding the disability fund). At that point, a 20% reduction in benefits will be required by law. (More on the trust fund below.)

What To Do?

The most prominent reform proposals involve reduced benefits for wealthy beneficiaries, increased payroll taxes on high earners, and an increase in the retirement age. However, President-Elect Donald Trump shows no inclination to make any changes on his watch. This is unfortunate because the sooner the system’s insolvency is addressed, the less draconian the necessary reforms will be.

A neglected reform idea is for SS to be privatized. Many observers agree in principle that current workers could earn better returns over the long-term by investing funds in a conservative mix of equities and bonds. The transition to private accounts could be made voluntary, so that no one is forced to give up the benefits to which they’re “entitled”.

Takers would receive an initial deposit from the government in a tax-deferred account. For participating pre-retirees, ongoing FICA contributions (in whole or in part) would be deposited into their private accounts. They could purchase a private annuity with the balance at retirement if they choose. The income tax treatment of annuity payments or distributions could mimic the current tax treatment of SS benefits.

Given that the balance remaining at death would be heritable, some individuals might be willing to accept an initial deposit less than the actuarial PV of the future SS benefits they’ve accumulated to-date (discounted at an internal rate of return equating future benefits “earned” to-date and contributions to-date). I also believe many individuals would willingly accept a lower initial deposit because they would gain some control over investment direction. Such voluntarily-accepted reductions in initial deposits to personal accounts would mean the government’s issue of new debt would be smaller than the decrease in future benefit obligations.

Nevertheless, funding the accounts at the time of transition would necessitate a huge and immediate increase in federal debt. Market participants and political interests are likely to fear an impossible strain on the credit market. Perhaps the transition could be staged over time to make it less “shocking”, but that would complicate matters. In any case, heavy debt issuance is the rub that dissuades most observers from supporting privatization.

Fiscal Theory of Price Level

The fiscal theory of the price level (FTPL) implies that such a privatization might not be an insurmountable challenge after all, at least in terms of comparative dynamics. Much background on FTPL can be found at John Cochrane’s Grumpy Economist Substack.

FTPL asserts that fiscal policy can influence the price level due to a constraint on the market value of government debt. This market value must be in balance with the expected stream of future government primary surpluses. This is known as the government budget constraint.

The primary surplus excludes the government’s interest expense, a budget component that must be paid out of the primary surplus or else borrowed. Of course, the market value of government debt incorporates the discounted value of future interest payments.

This budget constraint must be true in an expectational sense. That is, the market must be convinced that future surpluses will be adequate to pay all future obligations associated with the debt. Otherwise, the value of the debt must change.

Should a spending initiative require the government to issue new debt with no credible offset in terms of future surpluses, the market value of the debt must decline. That means interest rates and/or the price level must rise. If interest rates are fixed by the monetary authority (the Fed) then only prices will rise.

A SS Private Option Under FTPL

But what about FTPL in the context of entitlement reform, specifically a privatization of Social Security? Suppose the government issues debt and then deposits the proceeds into personal accounts to fund future benefits. Future government surpluses (deficits) would increase (decrease) by the reduction in future SS benefit payments.

This improved budgetary position should be highly credible to financial markets, despite the fact that benefits are not and never have been guaranteed. If it is credible to markets, the new debt would not raise prices, nor would it be valued differently than existing debt. There need not be any change in interest rates.

But Thin Ice

There are risks, of course. It might be too much to hope that other federal spending can be restrained. That kind of failure would subvert the rationale for any budgetary reform. A variety of other crises and economic shocks are also possible. Those could disrupt markets and jeopardize budget discipline as well. Given a severe shock, interest expense could more readily explode given the massive debt issuance required by the reform discussed here. So there are big risks, but one might ask whether they could turn out to be more disastrous in the absence of reform.

Other Details

The private account “offers” extended to workers or beneficiaries relative to the actuarial PVs of their future benefits would be controversial. Different offer percentages (discounts) could be tested to guage uptake.

Another issue: provisions would have to be made for individuals in “unbanked” households, estimated by the FDIC to be about 4.2% of all U.S. households in 2023. Voluntary uptake of the “offer” is likely to be lower among the unbanked and among those having less confidence in their ability to make financial decisions. However, even a simplified set of choices might be superior to the returns under today’s SS, even for low-income workers, not to mention the very real threat of future reductions in benefits. Furthermore, financial institutions might compete for new accounts in part by offering some level of financial education for new clients.

A similar reform could be applied to Medicare, which like SS is also technically insolvent. Participating beneficiaries could receive some proportion of expected future benefits in a private account, which they could use to pay for private or public health insurance coverage or medical expenses. From a budget perspective, the increase in federal debt would be balanced against the reduction in future Medicare benefits, which would constitute a credible increase (decrease) in future surpluses (deficits).

Credibility

But again, how credible would markets find the decrease in benefit obligations? Direct reductions in future entitlements should be convincing, though politicians are likely to find plenty of other ways to use the savings.

On the other hand, markets already give some weight to the possibility of future benefit cuts (or other policies that would reduce SS shortfalls). So it’s likely that markets will give the reform’s favorable budget implications significant but only “incremental credit”.

Another possible complication is that the market, prior to execution of the reform, might discount the uptake by workers and current retirees. This would necessitate better offers to improve uptake and more debt issuance for a given reduction in future obligations. Skepticism along these lines might worsen implications for the price level and interest rates.

The Trust Fund

Finally, what about the SS Trust Fund? Can it play in role in the reform discussed above? The answer depends on how the trust fund fits into the federal government’s budgetary position.

The trust fund holds as assets only non-marketable Treasury securities acquired in the past when SS contributions exceeded benefit payments. The excess payroll tax revenue was placed in the trust fund, which in turn lent the funds to the federal government to help meet other budgetary needs. Hence the bond holdings.

In terms of the government’s fiscal position, the money has already been pissed away, as it were. The bonds in the trust fund do not represent a pot of money. As noted above, with our age demographics now reversed, payroll taxes no longer meet benefits. Thus, bonds in the trust fund must be redeemed to pay all SS obligations. The Treasury must pay off the bonds via general revenue or by borrowing additional amounts from the public.

Post-reform, if continuing deficits are the order of the day, redeeming bonds in the trust fund would do nothing to improve the government’s fiscal position. If the trust fund “cashes them in” to help meet benefit payments, the federal government must borrow to raise that cash. In other words, the bonds in the trust fund would be more or less superfluous.

But what if the federal budget swings into a surplus position post-reform? In that case, federal tax revenue would cover the redemption of at least some of the bonds held by the trust fund. SS beneficiaries would then have a meaningful claim on federal taxpayers through the trust fund and the government’s surplus position, which would reduce the new federal debt required by the reform.

Conclusion

The Social Security and Medicare systems are in desperate need reform, but there is little momentum for any such undertaking. Meanwhile, exhaustion of the SS and Medicare trust funds creeps ever closer, along with required benefit cuts. All of the reform options would be painful in one way or another. A voluntary privatization would require a huge makeover, but it might be the least painful option of all. Current workers and beneficiaries would not be compelled to make choices they found inferior. Moreover, the new debt necessary to pay for the reforms would be matched by a reduction in future government obligations. The fiscal theory of the price level implies that the reform would not be inflationary and need not depress the value of Treasury bonds, provided the reform is accompanied by long-term budget discipline.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

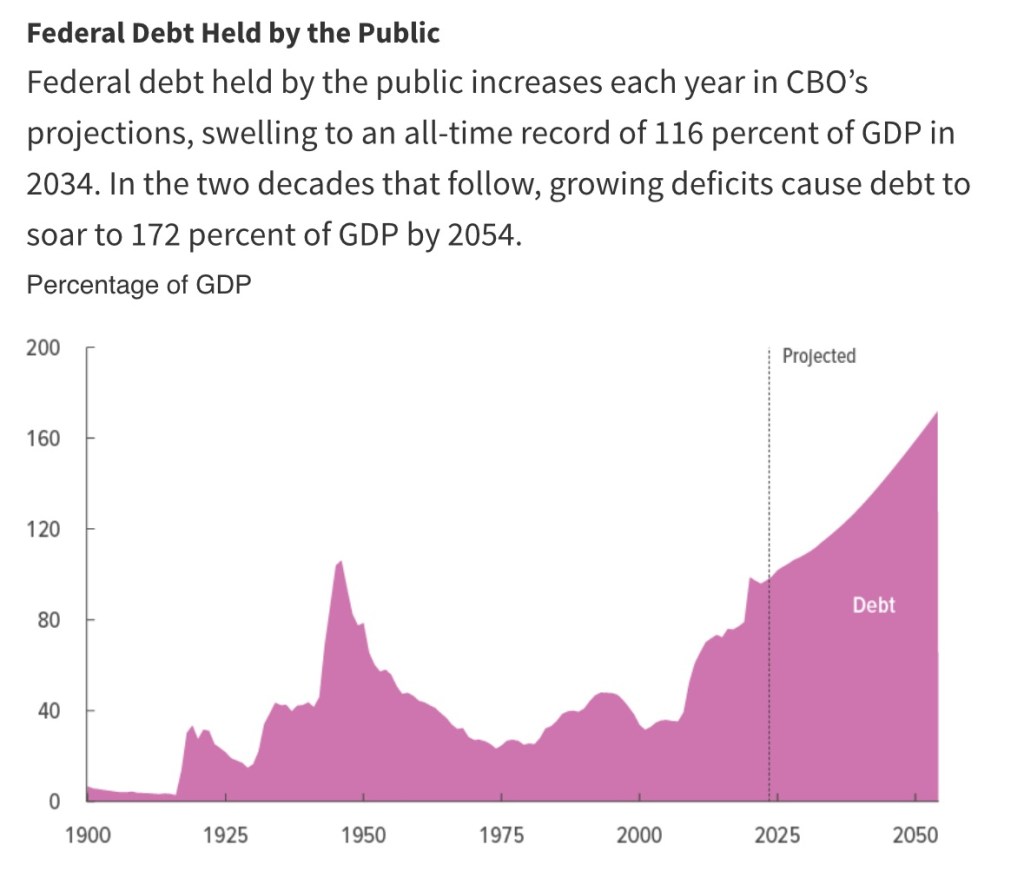

Note: the chart at the top of this post was produced by the Congressional Budget Office and appears in this publication.

Wow! We’re less than a week from Election Day! I’d hoped to write a few more detailed posts about the platforms and policies of Kamala Harris and Donald Trump, but I was waylaid by Hurricane Milton. It sent us scrambling into prep mode, then we evacuated to the Florida Panhandle. The drive there and back took much longer than expected due to the mass exodus. On our return we found the house was fine, but there was significant damage to an exterior structure and a mess in the yard. We also had to “de-prep” the house, and we’ve been dealing with contractors ever since. It was an exhausting episode, but we feel like we were very lucky.

Now, with less than a week left till the election, I’ll limit myself to a summary of the positions of the candidates in a number of areas, mostly but not all directly related to policy. I assign “grades” in each area and calculate an equally-weighted “GPA” for each candidate. My summaries (and “grades”) are pretty off-the-cuff and not adequate treatments on their own. Some of these areas are more general than others, and I readily admit that a GPA taken from my grade assignments is subject to a bit of double counting. Oh well!

Role of Government: Kamala Harris is a statist through and through. No mystery there. Trump is more selective in his statist tendencies. He’ll often favor government action if it’s politically advantageous. However, in general I think he is amenable to a smaller role for the public than the private sector. Harris: F; Trump: C

Regulation: There is no question that Trump stands for badly needed federal regulatory reform. This spans a wide range of areas, and it extends to a light approach to crypto and AI regulation. Trump plans to appoint Elon Musk as his “Secretary of Cost Cutting”. Harris, on the other hand, seems to favor a continuation of the Biden Administration’s heavy regulatory oversight. This encourages a bloated federal bureaucracy, inflicts high compliance costs on the private sector, stifles innovation, and tends to concentrate industrial power. Harris: F; Trump: A

Border Policy: Trump wants to close the borders (complete the wall) and deport illegal immigrants. Both are easier said than done. Except for criminal elements, the latter will be especially controversial. I’d feel better about Trump’s position if it were accompanied by a commitment to expanded legal immigration. We need more legal immigrants, especially the highly skilled. For her part, Harris would offer mass amnesty to illegals. She’d continue an open border policy, though she claims to want certain limits on illegal border crossings going forward. She also claims to favor more funds for border control. However, it is not clear how well this would translate into thorough vetting of illegal entrants, drug interdiction at the border, or sex trafficking. Harris: D; Trump: B-

Antitrust: Accusations of price gouging by American businesses? Harris! Forty three corporations in the S&P 500 under investigation by the DOJ? The Biden-Harris Administration. This reflects an aggressively hostile and manipulative attitude toward the business community. Trump, meanwhile, might wheedle corporations to act on behalf of certain of his agendas, but he is unlikely to take such a broadly punitive approach. Harris: F; Trump: B-

Foreign Policy: Harris is likely to continue the Biden Administration’s conciliatory approach to dealing with America’s adversaries. The other side of that coin is an often tepid commitment to longtime allies like Israel. Trump believes that dealing from a position of strength is imperative, and he’s willing to challenge enemies with an array of economic and political sticks and carrots. He had success during his first term in office promoting peace in the Middle East. A renewed version of the Abraham Accords that strengthened economic ties across the region would do just that. Ideally, he would like to restore the strength of America’s military, about which Harris has less interest. Trump has also shown a willingness to challenge our NATO partners in order to get them to “pay their fair share” toward the alliance’s shared defense. My major qualification here has to do with the candidates’ positions with respect to supporting Ukraine in its war against Putin’s mad aggression. Harris seems more likely than Trump to continue America’s support for Ukraine. Harris: D+; Trump: B-

Trade: Nations who trade with one another tend to be more prosperous and at peace. Unfortunately, neither candidate has much recognition of these facts. Harris is willing to extend the tariffs enforced during the Biden Administration. Trump, however, is under the delusion that tariffs can solve almost anything that ails the country. Of course, tariffs are a destructive tax on American consumers and businesses. Part of this owes to the direct effects of the tax. Part owes to the pricing power tariffs grant to domestic producers. Tariffs harm incentives for efficiency and the competitiveness of American industry. Retaliatory action by foreign governments is a likely response, which magnifies the harm.

To be fair, Trump believes he can use tariffs as a negotiating tool in nearly all international matters, whether economic, political, or military. This might work to achieve some objectives, but at the cost of damaging relations more broadly and undermining the U.S. economy. Trump is an advocate for not just selective, punitive tariffs, but for broad application of tariffs. Someone needs to disabuse him of the notion that tariffs have great revenue-raising potential. They don’t. And Trump is seemingly unaware of another basic fact: the trade deficit is mirrored by foreign investment in the U.S. economy, which spurs domestic economic growth. Quashing imports via tariffs will also quash that source of growth. I’ll add one other qualification below in the section on taxes, but I’m not sure it has a meaningful chance.

Harris: C-; Trump: F

Inflation: This is a tough one to grade. The President has no direct control over inflation. Harris wants to challenge “price gougers”, which has little to do with actual inflation. I expect both candidates to tolerate large deficits in order to fulfill campaign promises and other objectives. That will put pressure on credit markets and is likely to be inflationary if bond investors are surprised by the higher trajectory of permanent government indebtedness, or if the Federal Reserve monetizes increasing amounts of federal debt. Deficits are likely to be larger under Trump than Harris due in large part to differences in their tax plans, but I’m skeptical that Harris will hold spending in check. Trump’s policies are more growth oriented, and these along with his energy policies and deregulatory actions could limit the inflationary consequences of his spending and tax policies. Higher tariffs will not be of much help in funding larger deficits, and in fact they will be inflationary. Harris: C; Trump: C

Federal Reserve Independence: Harris would undoubtedly like to have the Fed partner closely with the Treasury in funding federal spending. Her appointments to the Board would almost certainly lead to a more activist Fed with a willingness to tolerate rapid monetary expansion and inflation. Trump might be even worse. He has signaled disdain for the Fed’s independence, and he would be happy to lean on the Fed to ease his efforts to fulfill promises to special interests. Harris: D; Trump: F

Entitlement Reform: Social Security and Medicare are both insolvent and benefits will be cut in 2035 without reforms. Harris would certainly be willing to tax the benefits of higher-income retirees more heavily, and she would likely be willing to impose FICA and Medicare taxes on incomes above current earning limits. These are not my favorite reform proposals. Trump has been silent on the issue except to promise no cuts in benefits. Harris: C-; Trump: F

Health Care: Harris is an Obamacare supporter and an advocate of expanded Medicaid. She favors policies that would short-circuit consumer discipline for health care spending and hasten the depletion of the already insolvent Medicare and Medicaid trust funds. These include a $2,000 cap on health care spending for Americans on Medicare, having Medicare cover in-home care, and extending tax credits for health insurance premia. She supports funding to address presumed health care disparities faced by black men. She also promises efforts to discipline or supplant pharmacy benefit managers. Trump, for his part, has said little about his plans for health care policy. He is not a fan of Obamacare and he has promised to take on Big Pharma, whatever that might mean. I fear that both candidates would happily place additional controls of the pricing of pharmaceuticals, a sure prescription for curtailed research and development and higher mortality. Harris: F; Trump: D+

Abortion: The Supreme Court’s 2022 decision in Dobbs v. Jackson essentially relegated abortion law to individual states. That’s consistent with federalist principles, leaving the controversial balancing of abortion vs. the unborn child’s rights up to state voters. Geographic differences of opinion on this question are dramatic, and Dobbs respects those differences. Trump is content with it. Meanwhile, Harris advocates for the establishment of expanded abortion rights at the federal level, including authorization of third trimester abortions by “care providers”. And Harris does not believe there should be religious exemptions for providers who do not wish to offer abortion services. No doubt she also approves of federally funded abortions. Harris: F; Trump: A

Housing: The nation faces an acute housing shortage owing to excessive regulation that limits construction of new or revitalized housing. These excessive rules are primarily imposed at the state and local level. While the federal government has little direct control over many of these decisions, it has abetted this regulatory onslaught in a variety of ways, especially in the environmental arena. Harris is offering stimulus to the demand side through a $25,000 housing tax credit for first-time home buyers. This will succeed in raising the cost of housing. She has also called for heavier subsidies for developers of low-income housing. If past is prologue, this might do more to line the pockets of developers than add meaningfully to the stock of affordable housing. Harris also favors rent controls, a sure prescription for deterioration in the housing stock, and she would prohibit software allowing landlords to determine competitive neighborhood rents. Trump has called for deregulation generally and would not favor rent controls. Harris: F; Trump B

Taxes: Harris has broached several wildly destructive tax proposals. Perhaps the worst of these is to tax unrealized capital gains, and while she promises it would apply only to extremely wealthy taxpayers, it would constitute a wealth tax. Once that line is crossed, the threat of widening the base becomes a very slippery slope. It would also be a strong detriment to domestic capital investment and economic growth. Harris would increase the top marginal personal tax rate and the corporate tax rate, which would discourage investment and undermine real wage growth. She’d also increase estate tax rates. As discussed above, she unwisely calls for a $25,000 tax credit for first-time homebuyers. She also wants to expand the child care tax credit to $6,000 for families with newborns. A proposed $50,000 small business tax credit would allow the federal government to subsidize and encourage risky entrepreneurial activity at taxpayers’ expense. I’m all for small business, but this style of industrial planning is bonkers. She would sunset the Trump (TCJA) tax cuts in 2026.

Finally, Harris has mimicked Trump in calling for no taxes on tips. Treating certain forms of income more favorably than others is a recipe for distortions in economic activity. Employers of tip-earning workers will find ways to shift employees’ income to tips that are mandatory for patrons. It will also skew labor supply decisions toward occupations that would otherwise have less economic value. But Trump managed to find an idea so politically seductive that Harris couldn’t resist.

Trump’s tax plans are a mixed bag of good and bad ideas. They include extending his earlier tax cuts (TCJA) and restoring the SALT deduction. The latter is an alluring campaign tidbit for voters in high-tax states. He would reduce the corporate tax rate, which I strongly favor. Corporate income is double-taxed, which is a detriment to growth as well as a weight on real wages. He would eliminate taxes on overtime income, another example of favoring a particular form of income over others. Wage earners would gain at the expense of salaried employees, so one could expect a transition in the form employees are paid over time. Otherwise, the classification of hours as “overtime” would have to be standardized. One could expect existing employees to work longer hours, but at the expense of new jobs. Finally, Trump says Social Security benefits should not be taxed, another kind of special treatment by form of income. This might encourage early retirement and become an additional drain on the Social Security Trust Fund.

The higher tariffs promised by Trump would collect some revenue. I’d be more supportive of this plank if the tariffs were part of a larger transition from income taxes to consumption taxes. However, Trump would still like to see large differentials between tariffs and taxes imposed on the consumption of domestically-produced goods and services.

Harris: F; Trump C+

Climate Policy: This topic has undergone a steep decline in relative importance to voters. Harris favors more drastic climate interventions than Trump, including steep renewable subsidies, EV mandates, and a panoply of other initiatives, many of which would carry over from the Biden Administration. Harris: F; Trump: B

Energy: Low-cost energy encourages economic growth. Just ask the Germans! Consistent with the climate change narrative, Harris wishes to discourage the use of fossil fuels, their domestic production, and even their export. She has been very dodgy with respect to restrictions on fracking. Her apparent stance on energy policy would be an obvious detriment to growth and price stability (or I should say a continuing detriment). Trump wishes to encourage fossil fuel production. Harris: F; Trump: A

Constitutional Integrity: Harris has supported the idea of packing the Supreme Court, which would lead to an escalating competition to appoint more and more justices with every shift in political power. She’s also disparaged the Electoral College, without which many states would never have agreed to join the Union. Under the questionable pretense of “protecting voting rights”, she has opposed steps to improve election integrity, such voter ID laws. And operatives within her party have done everything possible to register non-citizens as voters. Harris: F; Trump: A

First Amendment Rights: Harris has called for regulation and oversight of social media content and moderation. A more descriptive word for this is censorship. Trump is generally a free speech advocate. Harris: F; Trump A-

Second Amendment Rights: Harris would like to ban so-called “assault weapons” and high-capacity magazines, and she backs universal background checks for gun purchases. Trump has not called for any new restrictions on gun rights. Harris: F; Trump: A

DEI: Harris is strongly supportive of diversity and equity initiatives, which have undermined social cohesion and the economy. That necessarily makes her an enemy of merit-based rewards. Trump has no such confusion. Harris: F; Trump: A

Hysteria: The Harris campaign has embraced a strategy of demonizing Donald Trump. Of course, that’s not a new approach among Democrats, who have fabricated bizarre stories about Trump escapades in Russia, Trump as a pawn of Vladimir Putin, and Russian manipulation of the 2016 Trump campaign. Congressional democrats spent nearly all of Trump’s first term in office trying to find grounds for impeachment. Concurrently, there were a number of other crazy and false stories about Trump. The current variation on “Orange Man Bad” is that Trump is a fascist and a Nazi, and that all of his supporters are Nazis. And that Trump will use the military against his domestic political opponents, the so-called “enemy within”. And that Trump will send half the country’s populace to labor camps. The nonsense never ends, but could anything more powerfully ignite the passions of violent extremists than this sort of hateful rhetoric? Would it not be surprising if at least a few leftists weren’t interested in assassinating “Hitler” himself. This is hysteria, and one has to wonder if that is not, in fact, the intent.

Can any of these people actually define the term fascist? Most fundamentally, a fascist desires the use of government coercion for private gain (of wealth or power) for oneself and/or one’s circle of allies. By that definition, we could probably categorize a great many American politicians as fascists, including Barack Obama, Joe Biden, Donald Trump, and a majority of both houses of Congress. That only demonstrates that corporatism is fundamental to fascist politics. Less-informed definitions of fascism conflate it with everything from racism (certainly can play a part) and homophobia (certainly can play a part) to mere capitalism. But take a look at the demographics of Trump’s supporters and you can see that most of these definitions are inapt.

Is the Trump campaign suffering from any form of hysteria? It’s shown great talent at poking fun at the left. Of course, Trump’s reactions to illegal immigration, crime, and third-trimester abortions are construed by leftists to be hysterical. I mean, why would anyone get upset about those kinds of things?

Harris: F; Trump: A

“Grade Point Average”

I’m sure I forgot an area or two I should have covered. Anyway, the following are four-point “GPAs” calculated over 20 categories. I’m deducting a quarter point for a “minus” grade and adding a quarter point for a “plus” grade. Here’s what I get:

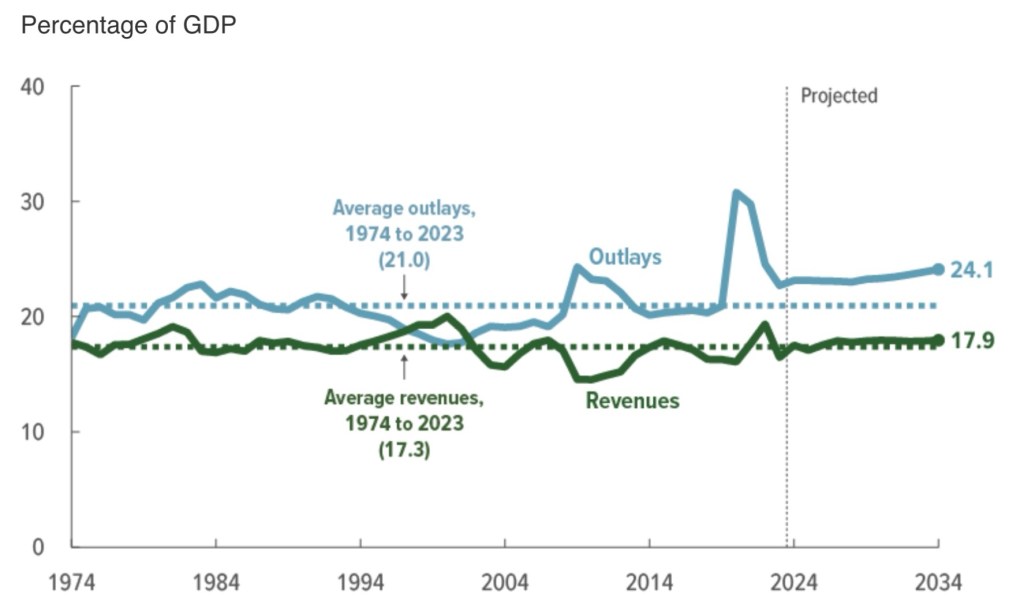

The chart above makes a convincing case that we have a spending problem at the federal level. Really, we’ve had a spending problem for a long time. But at least tax revenue today remains reasonably well-aligned with its 50-year historical average as a share of GDP. Not spending. Even larger deficits opened up during the pandemic and they haven’t returned to pre-pandemic levels.

We’ve seen Joe Biden break spending records. His initiatives, often with questionable merit, have included the $1.8 trillion American Rescue Plan and the nearly $0.8 trillion Infrastructure Investment and Jobs Act, along with several other significant spending initiatives such as the Promise to Address Comprehensive Toxics Act and the subsidy-laden CHIPS Act. Meanwhile, emergency spending has become a regular occurrence on Biden’s watch. More recently, he’s made repeated efforts to forgive massive amounts of student loans despite the Supreme Court’s clear ruling that such gifts are unconstitutional.

Indeed, while Biden keeps pretty busy spinning tales of his days driving an 18-wheeler, cannibals devouring his Uncle Bosie Finnegan, his upbringing in black churches, synagogues, or in the Puerto Rican community, he still finds time to dream up ways for the government to spend money it doesn’t have. Or his kindly puppeteers do.

Biden’s New Budget

Eric Boehm expressed wonderment at Biden’s fiscal 2025 budget not long after its release in March. He was also mystified by the gall it took to produce a “fact sheet” in which the White House congratulated itself on fiscal responsibility. That’s how this Administration characterizes deficits projected at $16 trillion over the next ten years. No joke!

Furthermore, the Administration says the record spending will be “paid for”. Well, yes, with tax increases and lots of borrowing! There are a great many fabulist claims made by the White House about the budget. This link from the Office of Management and Budget includes a handy list of propaganda sheets they’ve managed to produce on the virtues of their proposal.

The Congressional Budget Office (CBO) projects ten-year deficits under current law that are $3 trillion higher than Biden’s proposed budget. That’s the basis of the White House’s boast of fiscal restraint. But the difference is basically paid for with a couple of accounting tricks (see below). More charitably, one could say it’s paid for with higher taxes, aided by the assumption of slightly faster economic growth. The latter will be a good trick while undercutting incentives and wages with a big boost to the corporate tax rate.

The revenue projected by the While House from those taxes does not come anywhere close to eliminating the gap shown in the CBO’s chart above. Federal spending under Biden’s budget grows at about 4% annually, just a bit slower than nominal GDP. Thus, the federal share of GDP remains roughly constant and only slightly higher than the CBO’s current projection for 2034. Nevertheless, spending relative to GDP would continue at an historically high rate. Over the next decade, it would average more than 3% higher than its 50-year average. That would be about $1.3 trillion in 2034!

Meanwhile, the ratio of tax revenue to GDP under Biden’s proposal, as they project it, would average slightly higher than its 50-year average, reaching a full percentage point above by 2034 (and higher than the CBO baseline). That’s probably optimistic.

There is little real effort in this budget to reduce federal deficits, with Treasury borrowing rates now near 15-year highs. Interest expense has grown to an alarming share of spending. In fact, it’s expected to exceed spending on defense in 2024! Perhaps not coincidentally, the White House assumes a greater decline in interest rates than CBO over the next 10 years.

Treats or Tricks?

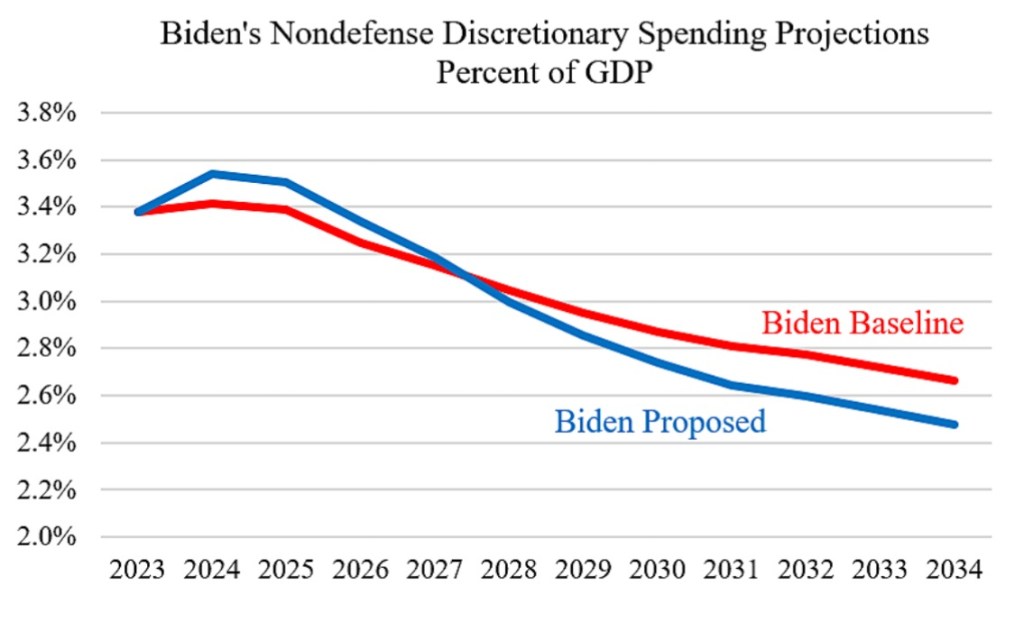

The situation is likely worse than the White House depicts, given that its budget incorporates assumptions that look generous to their claim of fiscal restraint. First, they frontload nondefense discretionary spending, allowing Biden to make extravagant promises for the near-term while pushing off steep declines in budget commitments to the out-years. The sharp reductions in this category of spending pares more than $2 trillion from the 10-year deficit. From the link above:

Biden also proposes to restore the expanded the child tax credit — for one year! How handy from a budget perspective: heroically call for an expanded credit (for a year) while avoiding, for the time being, the addition of a couple of trillion to the 10-year deficit.

Code Red

So where does this end? The ratio of federal debt to GDP will resume its ascent after a slight decline from the pandemic high. Here is the CBO’s projection:

The Biden budget shows a relatively stable debt to GDP ratio through 2034 due to the assumptions of slightly faster GDP growth, lower Treasury borrowing rates, and the aforementioned “fiscal restraint”. But don’t count on it!

The government’s growing dominance over real resources will have negative consequences for growth in the long-term. Purely as a fiscal matter, however, it must be paid for in one of three ways: revenue from explicit taxes, federal borrowing, or an implicit tax on the public more commonly known as the inflation tax. The last two are intimately related.

Bond investors always face at least a small measure of default risk even when lending to the U.S. Treasury. There is almost no chance the government would ever default outright by failing to pay interest or principal when due. However, investors hold an expectation that the value of their bonds will erode in real terms due to inflation. To compensate, they demand an “inflation premium” in the interest rate they earn on Treasury bonds. But an upside surprise to inflation would constitute a “soft default” on the real value of their bonds. This occurred during and after the pandemic, and it was triggered by a burgeoning federal deficit.

Brief Mechanics

John Cochrane has explained the mechanism by which acts of fiscal profligacy can be transmitted to the price of goods. The real value of outstanding federal debt cannot exceed the expected real value of future surpluses (a present value summed across positive and negative surpluses). If expected surpluses are reduced via some emergency or shock such that repayment in real terms is less likely, then the real value of government debt must fall. That means either interest rates or the price level must rise, or some combination of the two.

The Federal Reserve can prevent interest rates from rising (by purchasing bonds and increasing the money supply), but that leaves a higher price level as the only way the real value of debt can come into line. In other words, an unexpected increase in the path of federal deficits would be financed by money printing and an inflation tax. The incidence of this unexpected “implicit” tax falls not only to bondholders, but also on the public at large, who suffer an unexpected decline in the purchasing power of their nominal assets and incomes. This in turn tends to free-up real resources for government absorption.

Government Debt Is Risky

It appears that investors expect the future deficits now projected by the CBO (and the White House) to be paid down someday, to some extent, by future surpluses. That might seem preposterous, but markets apparently aren’t surprised by the projected deficits. After all, fiscal policy decisions can change tremendously over the course of a few years. But it still feels like excessive optimism. Whatever the case, Cochrane cautions that the next fiscal emergency, be it a new pandemic, a war, a recession, or some other crisis, is likely to create another huge expansion in debt and a substantial increase price level. Joe Biden doesn’t seem inclined to put us in a position to deal with that risk very effectively. Unfortunately, it’s not clear that Donald Trump will either. And neither seems inclined to seriously address the insolvencies of Social Security and Medicare. If unaddressed, those mandatory obligations will become real crises over the next decade.

Choosing between the lesser of evils is a bummer, but that’s often the reality for voters. That goes almost without saying… our choices are politicians! I’ll certainly be in that quandary if Donald Trump is the Republican nominee for president in 2024, which looks increasingly likely. I held my nose and voted for him — twice — primarily because the Big Government solutions promoted consistently by Democrats are so awful.

At this point I’m not fully on board with any GOP candidate. That could change, but not yet. Now, if you’re a Trump supporter and you think the rambling opinions below are too critical of your guy, cut me some slack. I’m not a “Never Trumper”. I’m a “Never Statist”. And while I’ve never had much faith that Trump is with me on that count, he will almost surely be the lesser of evils.

The Abused Politician

Trump has been subjected to despicable treatment by political opponents since well before his inauguration in 2016, and his abusers in and out of government never let up. Many of the charges and accusations against him have been pure fiction and at this point represent obvious election interference. So I’m somewhat sympathetic to him despite some of his positions and often disagreeable manner. Still, I credit him for being a fighter, and as an aside, I’ll add that I actually enjoy some of his rants. He has the style of a nasty stand-up comic, which gives me some occasional laughs.

I agree with Trump on certain policy matters. On others, including some fundamental points, I find it hard to trust him as a leader, and I said that long before he was elected in 2016. He claims not to be a politician, but he is a politician through and through. He’s also a populist. And while populism can serve as a valuable check on certain excesses of government, it often cuts the wrong way, favoring what I like to call “do-somethingism”. That usually means public intervention. Populism is a perfectly natural home for a “pick-and-choose” statist like Trump, however. Moreover, I’m not happy that he refused to debate his opponents, and that too was a purely political decision.

Malign Neglect

If you need proof of Trump’s base instincts as a politician, look no further than his refusal to engage on the subject of entitlement reform. It’s no secret that both Social Security (SS) and Medicare are technically insolvent. This is probably the most important fiscal issue the country will face in the foreseeable future.

Without reform, SS benefits will be cut 23% in 2034. That would bring certain outrage among seniors and anyone approaching retirement. Sure, it’s a decade down the road, but addressing it sooner would be far less painful. Does Trump favor a huge cut in benefits? Probably not. Does he think benefits can simply continue without additional funding or reform of some kind? Does he prefer a greater inflation tax, rather than reform? Does he secretly favor “just print the money” like the modern monetary theorists of the Left? There are much better alternatives, but where is his leadership on this issue?

His unwillingness to discuss entitlements, and indeed, his denigration of anyone who so much as mentions the need for serious reforms, is a disgrace. He knows the train wreck is coming, but his focus is squarely on short-term politics. Why are so many on the Right willing to fall for this? Maybe they too understand it’s an elephant in the room, but an elephant that must not be named. After all, it’s not as if the Democrats have done a thing to address the issue.

False Fealty to Workers

Trump is a protectionist, given to the mercantilist fallacy that only exports are good and imports are bad. We import heavily because we are a high-income nation. The other side of that coin is that the world craves our assets, including the U.S. dollar (which is in absolutely no danger of losing its dominance as the primary currency of international transactions).

Here’s a little truth from “Trade Flows 101”: U.S. imports of goods and services correspond to purchases of U.S. assets by the rest of the world. In other words, U.S. trade deficits present opportunities for foreign investors to supply us with capital. That helps foster greater U.S. productive capacity, greater worker productivity, and higher wages.

On the other hand, government intervention to discourage imports via quotas or tariffs increases domestic prices and erodes real wages in the U.S. Furthermore, to favor certain industries (exporters) over others (importers) is a grotesque application of corporatist industrial policy. Why does the Right tolerate Trump’s advocacy for this sort of government central planning? Part of the answer is national security, which I accept to a limited extent, but not when “critical industries” are extended favors by government that are redundant to already powerful market forces.

Protectionism owes some of its popularity to the appeal of nationalism, as distinct from patriotism. However, it promotes sclerosis among domestic producers by shielding them from competition, causing direct harm to U.S. consumers. There is nothing patriotic about protectionism.

Real Stuff

A fallacy closely related to protectionism, and one to which Trump subscribes, is that the U.S. must produce more “things” — more commodities and manufactured goods. That’s not the market’s judgement, but one that appeals to the instincts of interventionists. In any case, services are often more highly valued than physical goods. If your comparative advantage is in producing a highly-valued service, don’t beat yourself up over neglecting to produce hard goods at which you’re comparatively lousy. Specialization and trade are under-appreciated as true social and economic miracles.