Tags

ADP Employment Report, Average Weekly Hours, BLS, Business Confidence, Consumer Confidence, Elise Gould, Employment Situation, Establishment Survey, Federal Reserve, Great Depression, Household Survey, Index of Leading Indicators, Inverted Yield Curve, Jerome Powell, Job Losers, Labor Force Participation, Labor Market, Lagging Indicator, Layoffs, Long and Variable Lags, Nonfarm Payrolls, Real Wages, Soft Landing, Underemployment

It’s always hard to foresee dramatic turns in the economy and their timing. One day, way back in grad school, a professor of mine went on about how the Great Depression seemed to surprise people at the time. He felt they should have known it was coming, and he emphasized that housing had been in a downturn starting around 1926. Well, hindsight’s 20/20, and I’m not sure how timely and accurate economic reporting was at the time, but today it’s not any easier to call recessions in advance.

An Array of Weak Signals

We’ve seen a downturn in housing this year, and for that and several other reasons many forecasters are predicting a recession in 2023. Consumers are depleting their savings and running up debt, and in November consumer confidence dropped for a fourth month in a row. In October, the Index of Leading Economic Indicators declined for an eighth straight month. A slump in business confidence has been underway for 12 months. Businesses are accumulating debt at much higher interest rates, and the earnings outlook (excluding energy) is bleak.

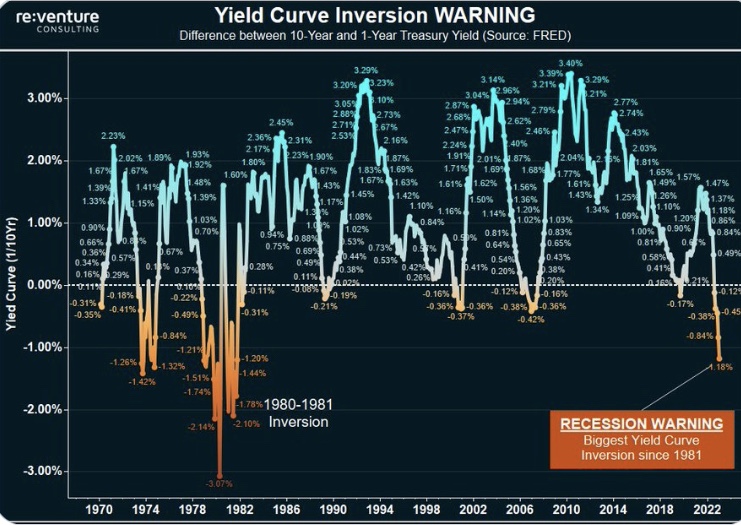

Buttressing that negative outlook is the inverted yield curve, which has been reliable (though not infallible) as a recession signal in the past. We now have a gap between the one-year Treasury yield and the 10-year Treasury yield of well over 100 basis points, which is as high as it’s been since 1981. That looks rather ominous.

The Fed’s Mission

Perhaps most importantly, the Federal Reserve has succeeded in reducing the money supply. That shift to tightening policy really only began in the late spring, however, and as Milton Friedman emphasized, the impact of money supply growth on the real economy is subject to “long and variable lags”. That could mean an economic slowdown or recession any time from now into 2024, but many analysts believe it will begin in the first half of 2023.

Denialists

Yet a few observers claim things are rosy, not least of all those within the Biden Administration. They insist the economy is in fine shape, pointing to the continuing strength in some of the employment numbers. Those gains have also been a preoccupation of the media, but employment statistics aren’t especially good predictors of changes in economic growth. Job growth and unemployment are lagging indicators, so we shouldn’t expect to see obvious signals of recession from employment data, at least until a downturn is underway. Even the Fed’s official economic forecast still calls for something of a “soft landing”, but Chairman Jerome Powell is wary of placing much confidence in particular outcomes, and with good reason.

The Employment Situation

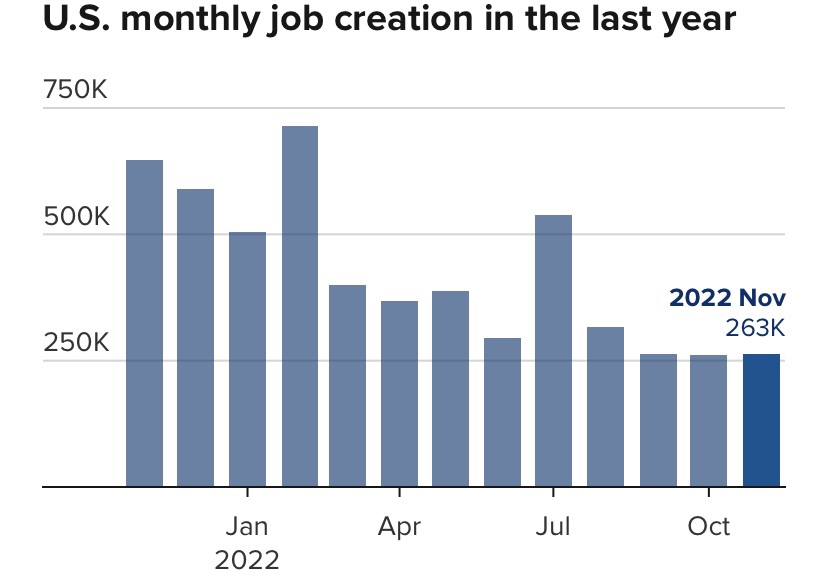

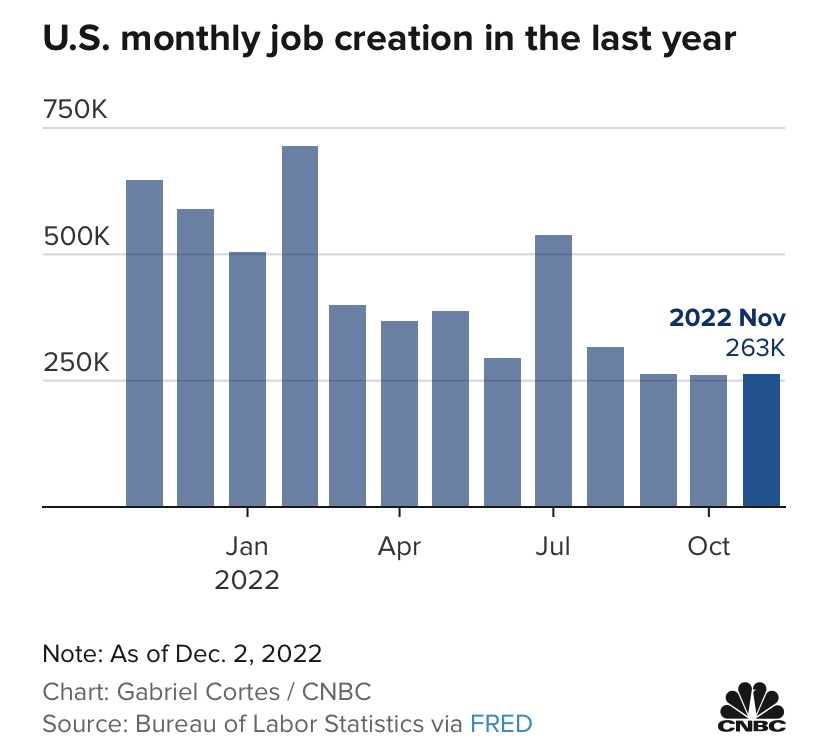

There are unusual patterns in recent employment data that might portend a weaker economy, but first, the statistics most widely followed are changes in non-farm employment (from the Bureau of Labor Statistics’ Survey of Business Establishments) and the unemployment rate (from the BLS Household Survey). The chart below shows monthly changes in nonfarm payrolls over the past year. There was a still-healthy gain in payrolls in November, but the pace of job growth slowed over the last twelve months as we came off the post-pandemic rebound.

One factor partly offsetting recent gains in non-farm employment is a decrease in the average workweek. Average weekly hours declined slightly in November and it was down 0.4 hours from a year earlier.

There are sectors of the economy that have shown recent weakness in payroll jobs. There was a decline in goods-producing employment in November, and layoffs are underway in the tech sector, a first for some of the big tech firms. Job reductions have also been announced at a few prominent financial firms.

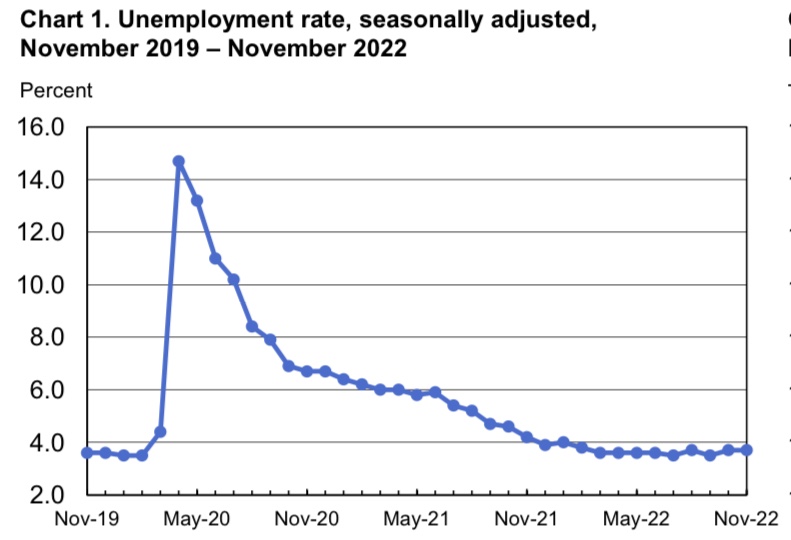

The next chart shows that the unemployment rate has remained near post-pandemic lows since early this year. An ongoing factor helping to keep it low, however, is that labor force participation is still running below pre-pandemic levels (despite rebounding well off pandemic lows during 2021). You aren’t counted as unemployed if you don’t participate in the labor force by seeking work.

One negative sign here is an uptick over the past two months in the share of job losers among the unemployed (as opposed to quitters or new entrants). That’s a pattern that would become more pronounced when and if a recession takes hold.

Keep in mind that these statistics are derived from surveys and extrapolated to the universe of households or non-farm employees. The Household Survey samples 60,000 households, whereas the Establishment Survey samples 131,000 employers, accounting for 670,000 employees. So the Household Survey is much smaller. Nevertheless, sample sizes of these magnitudes should be highly reliable, even for most subcategories.

Contradictory BLS Surveys

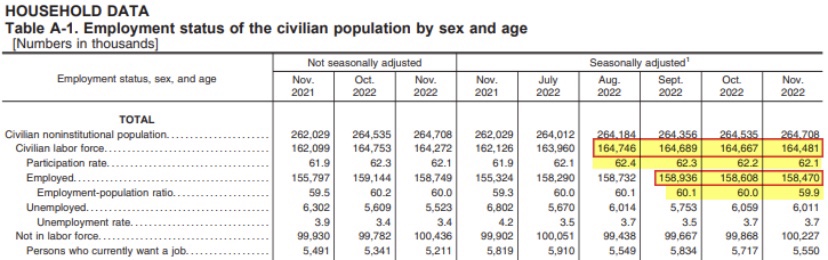

There are a few other possible signs of a weakening labor market in recent employment data. One such development is a gap between new job numbers from the Establishment Survey (non-farm payrolls) and the Household Survey (total employment). The following table (taken from the December 2nd BLS Report for households) is from a series of tweets by Elise Gould:

Total employment from the Household Survey has actually declined by almost 470,000 the past two months, while non-farm payrolls have increased by a total of over 500,000. Turning points in employment from the Household Survey tend to lead non-farm payrolls, so this could foretell a softening. While the Household Survey is smaller than the Establishment Survey, it is broader in some respects, covering several categories of workers who aren’t counted on non-farm payrolls, including agricultural workers and the self-employed. The latter are a more significant part of the employed population given the rise in the so-called gig economy. Self-employed workers (unincorporated) have declined by more than 170,000 over the past two months. However, it’s not clear that these workers would be affected earlier than others around turning points.

A separate employment report by ADP Research noted a sharp slowdown in private sector hiring in November, with the most weakness in construction and interest rate sensitive industries. The report also noted that fewer workers are leaving jobs voluntarily.

Is the Labor Market Tight Or Loose?

Nominal wages are rising at an accelerating pace, which might make it more difficult for the Fed to rein-in inflation. However, wages are still rising less than prices — as of October, real hourly earnings had declined 1.9% over the past year. November will mark 20 straight months of declines in the real wage. The drop in real weekly earnings is even steeper, given a slight decline in the average workweek. If we’re looking for a silver lining, inflation and declines in real earnings mean that employers have gained additional incentive to hire. Perhaps that can be offered as one reason for persistent strength in the payroll numbers.

There are still more than 10 million job openings across the country, but only 6 million workers are unemployed. Again, many would-be job candidates are sitting things out. (Perhaps they are mostly terrible candidates, given their apparent disinterest in work.) Some observers assume this means that the labor market is extremely tight, yet real wages are declining, as if there were an excess supply of workers! The answer to this “puzzle” is that many vacancies are ultimately filled by candidates who were already employed. Also, there is a large number of underemployed workers. Thus, the available pool of candidates is much larger than the number available due to unemployment. It’s not outlandish to think that there is actually an excess supply of labor at the moment, rather than excess demand, but that doesn’t bode well for real wage gains going forward.

Conclusion

Despite an ostensibly strong labor market, there are reasons to think that strength is waning, even without appeal to other economic and financial indicators. The BLS household survey showed recent declines in employment, as did the ADP survey, and we’ve seen an increase in the share of job losers among the unemployed. High-profile layoff announcements should also give pause. The recessionary outlook is reinforced by a number of other indicators, but most of all, the Federal Reserve’s tightening of the money supply is bound to have a stronger impact on the economy in 2023, and the Fed is not finished tightening yet.

Pingback: Price Stability: Are We There Yet? | Sacred Cow Chips