A lot has changed since Kevin Warsh was nominated by President Trump to replace Jerome Powell as chairman of the Federal Reserve Board. Most notably that includes the war in Iran, the run-up in oil prices, and a bond market increasingly nervous about inflation as it attempts to digest massive supplies of new Treasury debt. Tariffs have also contributed to the updraft in measured inflation since then, which (in addition to oil prices) represents another impingement on the economy’s supply side.

Change and Change Itself

By the time Warsh was sworn in as chairman, expectations for Fed rate cuts had swung to expectations of a quarter-point increase in the federal funds rate target, if not at the mid-June meeting of the Federal Open Market Committee (FOMC) then in July. It’s not clear that Warsh is on board with that, and the status of the Iranian conflict, oil supplies, and the bond market could change dramatically before the June meeting.

Short-term inflation expectations have risen, so a rate hike by the Fed might seem reasonable if not for the possibility that current inflation is transitory (but I use that term guardedly). In terms of money growth, policy seems roughly neutral to slightly restrictive. M2 growth from a year earlier was 4.7% in April. Nominal (current dollar) GDP grew at a slightly faster 5.1% clip in the first quarter, and it might accelerate in Q2. Real GDP advanced 1.6% from a year ago in the first quarter, but the Atlanta Fed’s forecast for real GDP in Q2 is a stronger 3.2%. Meanwhile, core PCE inflation (the Fed’s preferred gauge) was 3.1% in the first quarter and 3.3% in April. If the numbers roughly follow the same track going forward, nominal GDP in Q2 could be up by about 6% – 6.5% from a year ago. Slowing the rate of M2 growth much from its recent pace might be an overreaction.

Moreover, it might be premature to raise the funds rate when a peaceful resolution to the Iran conflict is still possible. Again, we might know by the time the FOMC convenes in June. In that case, market rates could ease quickly. I am skeptical, however, that Iran will prove to be a reliable partner to any peace agreement. I’ll be surprised if the blockade on the Strait of Hormuz ends any time soon, and a few air strikes have already been renewed. Still, I expect the FOMC to defer any rate hike until at least the July meeting. In fact, I’ll be surprised to see one at all.

Sound Money or Monetary Madness

Many describe Warsh as a “sound money” guy, having been greatly influenced by Milton Friedman. He’s been critical of quantitative easing (QE): the Fed’s purchases of securities for its own balance sheet to provide liquidity to the markets and banking system. If the hostilities continue in Iran, Warsh is more likely to favor quantitative tightening (QT) in the short-term than rate hikes. QT would involve reductions holdings of securities on the Fed’s balance sheet, which Warsh has long advocated.

On the other hand, Warsh has been undaunted in insisting that the AI revolution will be a dramatic deflationary force. That’s a longer-term proposition, but it reinforces his preference for lower rates. So Warsh is for “sound money” and would like to see QT, but he also prefers lower rates and apparently believes that AI might justify a more expansionary monetary posture. So where does that leave us?

Squaring the Circle

A few months ago I described a coherent policy agenda for the Fed under Kevin Warsh, given his policy preferences. It might have lacked realism in terms of Fed politics, but it was motivated by the question of whether lower rates are compatible with QT. The discussion did not anticipate the Iran conflict and its economic and financial consequences.

Lower rates and QT would be compatible if the Fed enables and incentivizes commercial banks to hold more securities and lend more aggressively. This would require regulatory changes as well as reductions in interest on bank reserves (IOR) held at the Fed.

Judy Shelton in the Wall Street Journal has made the same point, characterizing such a policy shift as “pro-market”. That’s because it would allow banks to invest in relatively safe assets, would eliminate a subsidy masquerading as a price (IOR – though fully administered), and would mean a transition from the Fed’s emphasis on maintaining ample bank reserves to scarce bank reserves. The latter would restore activity in the market for overnight loans of reserves (federal funds), which would then trade at a price corresponding to their degree of scarcity. That would provide an important signal to other markets, not to mention the Fed itself. Today, that signal is distorted by the Fed’s provision of ample reserves (repo rates notwithstanding). Jai Kadia and Norbert Michel have madea similar argument, along with advocating for rules-based monetary policy, rather than frequently destabilizing discretionary actions.

Momentum

In April, David Beckworth noted that momentum is buildingin influential circles for this change, which he describes as a “demand driven” approach, as opposed to the “supply driven”, ample reserve operating procedure now in force. This is the more common at many foreign central banks, and it has received prominent mention in recent speeches and statements by Fed officials. As Beckworth puts it in the title of his post, “The Fed’s Overton Window Is Shifting”.

Beckworth also mentions Warsh’s desire to establish a new Treasury-Fed Accord. The original 1951 Accord established the Fed’s independence from Treasury financing operations. Today’s ample reserves approach has made it far too easy for the Fed to succumb to pressures to monetize deficits and intervene in capital markets to manipulate longer rates. Warsh would surely like to re-establish the Fed’s monetary authority as a separate and independent function from Treasury financing.

The Fed Board of Governors (BoG) must approve changes in interest on reserves (IOR). (Better yet, an act of Congress would be required to prohibit IOR.) But Warsh, who is said to have good relations with the Fed staff and other Fed governors, is less likely to get a majority on the BoG than even the FOMC. For now, he’ll have to be persuasive to gain the support of a majority of either body.

Summary

Kevin Warsh is likely to argue strenuously for reductions in the size of the Fed’s balance sheet, and would almost certainly be happy for the FOMC to defer any rate hikes pending more clarity on a resolution to the Iran conflict. He will also argue for creating greater incentives for banks themselves to invest in Treasury debt, including reformed regulations on bank asset holdings and reduced interest on reserves held at the Fed. Ultimately, that would pave the way for lower rates on a variety of assets. But the Fed should be probably be cautious and gradual in the implementation: the changes to IOR and bank regulations must be well coordinated with QT and money growth must be calibrated to meet the Fed’s inflation target (or better yet, a nominal GDP target — see Part 2 of this post).

I voted for Trump because I considered him to be far preferable to Kamala Harris across a range of issues. I still feel that way, but I’m appalled at a number of actions he’s taken and/or proposed in the 14 months since he took office. As a candidate, I gave Trump a “grade point average” of about 2.68, a solid C+. Here, I’ll grade him on most of the same categories, but I’ve made a few changes to the categories based on developments since his inauguration. My perspective here is generally domestic non-intervention and small government.

Yes, I realize this is tldr; I’m sure I elaborated more than necessary, but you can skip around and scroll to sections in which you might have greater interest. Here’s a list of topics:

Role of Government

Regulation

Border Policy

Antitrust

Foreign Policy

Trade

Taxes

Inflation

Federal Reserve Independence

Federal Spending and the Deficit

Entitlement Reform

Government Waste

Health and Health Care

Abortion

Housing

Energy

First Amendment Rights

Second Amendment Rights

DEI and Its Evil Financial Twin, ESG

Technology

Voting Rights

Education

Role of Government: It’s probably unfair to treat this as a separate category because it might double count specifics mentioned later, but Trump has demonstrated an unfortunate proclivity for wielding government power over private affairs when it suits him politically. On this point, “The Conspicuous Fist of Trump’s State Corporatism”, is a good read. Trump’s actions demonstrate the awful ways in which populism is often a close cousin to socialism. An example is Trump’s economic micro-management and abrogation of property rights in attacking share buybacks. Trump boasts of his efforts to strengthen the American economy by committing public resources to investments in private enterprises, and by “doing deals” with foreign governments to invest in the U.S. When it comes to limited government, candidate Trump’s C is now President Trump’s D.

Regulation: Despite the kinds of intrusions cited above, the Trump Administration has, at the same time, aggressively pursued deregulation of private activity. The goal is to achieve a 10-to-1 ratio of rule rollbacks to new regulatory rules. One can and should assess regulatory measures one-by-one, but there are plenty of rules that wouldn’t pass a reasonable cost-benefit test. On the whole the regulatory state has grown unwieldy and imposes significant costs on producers, and ultimately taxpayers and consumers, often with little compensatory benefit. I applaud the effort to untangle the regulatory state. My grade for Trump here remains an A.

Border Policy: Despite my preference for non-intervention, I support strong border enforcement along with expanded legal immigration.

Illegal entry has plummeted under Trump, a welcome development. Uncontrolled immigration entails a loss of sovereignty and is a poor fiscal proposition. Those with deeper criminal records, from either before or after entry, deserve no concessions. Strict vetting is also necessary to prevent incursions by potential terror threats.

While illegal entry is a crime, otherwise innocent illegals should be treated kindly. For example, rewards can be offered for voluntary deportation, an approach used extensively by the Trump Administration. There are difficult issues such as birthright citizenship, the constitutionality of which has been questioned on textual grounds, and the practicality of which can be shaky, even for children of parents who enter the U.S. legally. Either way, it seems clear that the promise of birthright citizenship should not serve as an incentive for illegal entry.

The Administration has certainly fumbled immigration enforcement in some instances, with cases of improperly detained individuals. Furthermore, very little has been done to advance the cause of increased legal immigration. On this topic I give Trump an overall B-.

Antitrust: This is a case of excessive government meddling with a big dose of favoritism thrown in. Early on, the Trump Administration chose to follow in the footsteps of Biden-era antitrust enforcement with a bias toward penalizing successful businesses on the pretext of “protecting” consumers.

Even worse, the Trump Administration has used the threat of antitrust as a cudgel in pursuit of a variety of objectives that are purely political. For example, in a recent executive order (EO), Trump threatened antitrust action against companies who invest in *too many* single-family homes, a counterproductive prohibition with hoped-for appeal to populist instincts. Then, under Trump, there have been missives from the FTC to tech companies about their failure to provide “balanced” news coverage, a prerogative protected by the First Amendment.

Trump has also interfered with Netflix’s now aborted acquisition of Warner Bros., in favor of a rival offer from Paramount. Trump also engineered the coercive extraction of a U.S. government “Golden Share” in approving the merger of U.S. Steel and Nippon Steel, which Trump claims gives him “total control”, in part by controlling the number of board seats. And he basically extorted a 15% cut for the government for approving a deal allowing Nvidea and AMD to sell the older H20 chip to China.

Trump’s approach to antitrust is very much entangled with the Administration’s uninhibited embrace of industrial policy and public control over private activity. He shares a fantasy common to interventionists that he can leverage the coercive power of government to create just the outcomes he would like.

The grade here is a D, which I think is generous.

Foreign Policy: I’ll try to keep this category separate from trade and tariff issues, though they are intertwined. Trump’s approach to foreign policy is nothing if not bold, and it’s been a mixed bag in terms of success. In the western hemisphere we have the so-called “Donroe Doctrine”, Trump’s effort to establish U.S. hemispheric leadership. So far: we gained a more effective partnership with Panama over the canal and diminished China’s control; decapitated the Maduro regime in Venezuela, asserting control over its oil shipments and undercutting the flow of narcotics through the country; brought the Cuban communist regime to near collapse by choking off its oil imports (but at the cost of greater human suffering in Cuba); partnered with Mexico in eliminating the head of a major drug cartel; and developed closer ties with several conservative regimes in Central and South America.

I’m troubled by the deadly force used against vessels said to be transporting drugs. We might have great intelligence on smuggling operations, but there must be less deadly ways to interdict.

For better or worse, Trump has trolled Canadian leadership in an effort to provoke dissent and gain influence there with respect to trade and security issues. His provocative stance on Greenland is primarily motivated by concerns over security in the Arctic.

Trump’s action against the repressive Iranian theocracy, its support of terror, and its nuclear ambitions has been a military success. Unfortunately, it has come at the cost of some American lives, at least a few civilian casualties in Iran, and a considerable economic cost. We can only hope for quick resolution and a transition to a more liberal regime for the people of Iran. However, Trump was patient to a fault with the mullahs, offering them an off-ramp during repeated rounds of negotiations. They refused to take it.

Of course, Trump is also pro-Israel and has rallied a coalition of nations who might contribute to a revitalized Gaza. I give Trump huge props for his support of Israel and his disgust with anti-Semitism in general.

Trump’s involvement in negotiations between Ukraine and Russia have been unsuccessful. It’s fair to wonder whether he’s cutting Putin way too much slack, as Putin has no intention of relenting. China remains a major threat to U.S. interests and our allies, but many of Trump’s foreign policy initiatives have served to undermine CCP interests.

Trump unique approach has alienated some of our traditional European allies, though he has had success in influencing policy abroad. In Venezuela, it’s worrisome that Trump acts as if he’s cultivating a relationship with Maduro’s replacements, who are probably no better than Maduro except for their eagerness to cowtow to Trump. Well, maybe, maybe not! Also troubling is the collateral damage suffered by the people of Cuba. There are signs of a willingness among Cuban leaders to negotiate with Trump, though hopes for a friendly successor regime might be foolish.

On the whole, I’ll give Trump a B on foreign policy. It’s bold, but he’s had some real successes.

Trade: I gave Trump an F on trade policy as a candidate. He’s more than justified that grade as president. He is a complete dolt when it comes to the benefits of foreign trade, the meaning of a trade deficit, the costs inflicted by tariffs, their complete inadequacy as a replacement for the income tax, and their counterproductive effect on foreign investment in the U.S. His “emergency” tariffs constituted a huge tax increase on the American people, but those were ruled unconstitutional by the Supreme Court. His latest ploy is to impose punitive tariffs under the guise of a balance of payments emergency, but the balance of payments is zero! This too will be struck down in the courts.

Some might argue that Trump’s other foreign policy achievements would not have been possible without the threat of tariffs, but the fact is Trump imposed the tariffs anyway. Yup, it’s an F.

Taxes: In terms of budget effects, the increased tariff revenue (which might not last at present levels) is much more than offset by tax provisions in the One Big Beautiful Bill Act (OBBBA) passed into law last summer. It makes permanent many of the reductions in the Tax Cuts and Jobs Act of 2017 that had been ready to expire. The standard deduction is increased and more limits are placed on itemization. The Act also creates targeted (and temporary) deductions for tips, overtime, auto loans, and seniors, which is inefficient because it treats various forms of income differently, leading to incentives for unproductive reallocations. Those changes also smack of political pandering.

The OBBBA makes permanent some tax incentives for business, such as immediate expensing of short-term asset purchases and domestic R&D investment. It also provides a temporary 100 percent deduction for certain structures and phases out tax credits for green energy production (bravo!).

To the extent that the tax package includes some pro-growth elements, I applaud it. Tax reductions generally are a good thing because they reduce distortions, but Trump has managed to introduce several distortionary elements just the same. I won’t dock Trump for deficit effects here because the deficit is fundamentally a spending problem, not a tax problem. I gave him a C+ on taxes as a candidate, but I’ll boost him to a B- for his first year.

Inflation: Trump doesn’t have real control over inflation as economists define it, but he’s managed to aggravate some price increases just the same. Unfortunately, he makes repeated claims that “prices have fallen” under his leadership, which of course is false. Egg prices perhaps, and oil prices (er… not this month). Of course, in general prices are up, including import prices. Inflation measures have been fairly steady over the past year, but remain stubbornly higher than the Federal Reserve’s target. I give Trump a grade on this topic only because he deserves a penalty for his false boasts. It’s a C, the same as candidate Trump.

Federal Reserve Independence: Trump has relentlessly badgered Jerome Powell and the Fed to somehow engineer lower interest rates. Of course, many key interest rates are market driven and outside the Fed’s direct control. Trump has gone so far as to bring lawfare to bear against Powell, accusing him of misleading Congress regarding cost overruns on the renovation of the Fed’s offices in DC. Of course, it’s not unusual for a president to jawbone the Fed, but Trump has been absurdly aggressive at a time when reducing the Fed’s rate targets would quite possibly backfire. At least Trump’s selection of the next Fed Chairman, Kevin Warsh, was more reasonable than another top candidate who would probably have been a mere punching bag. For this, I’ll lift his grade slightly, from an F to a D-.

Federal Spending and the Deficit: I discuss a few components of spending under other headings below. Beyond those points, Trump has taken every opportunity to find creative uses for taxpayer money. He has proposed a “tariff dividend” for all households funded by the revenue from import taxes. (Refunds of tariff revenue to “payers” are still in question.) At this point, the better alternative is to put extra revenue toward paying down the federal debt. The same goes for any revenue earned from the many “deals” Trump is counting on. Pay down the debt and earn an immediate, certain, and lasting return, rather than installing the government as part owner of otherwise private enterprises having uncertain returns.

Apart from that and the folly of establishing a sovereign wealth fund while the public debt is burgeoning, Trump has made no progress whatsoever on deficit reduction. Granted, he can’t count on strong legislative support despite slight majorities in both chambers of Congress.

The tax cuts in the OBBBA obviously don’t help the cause of deficit reduction. In fairness, rebuilding the military is a major priority. However, interests costs on the debt will keep rising as will discretionary non-defense outlays. At least the East-Wing Ballroom, the Arc de Trump (!), and the Kennedy Center renovation all appear to be privately funded.

Trump deserves a D here. Some of his priorities are terrible, and I can’t cut him any slack based on trends in discretionary spending.

Entitlement Reform: Trump has been silent on reforms to Social Security’s “Old Age and Survivors” programs and Medicare, except to promise no cuts in benefits under his watch. Kick the can! However, the administration has considered cuts in other entitlements, such as Social Security Disability Insurance, Medicaid and Supplemental Nutrition Assistance (SNAP). These programs have been riddled with fraud, so I applaud steps to clean them up. Nevertheless, any progress made here will still be dwarfed by the insolvency of the Retirement and Medicare programs, which Trump considers a third rail for potential reformers. I gave him an F as a candidate, but his anti-fraud efforts help him salvage a C-.

Government Waste: DOGE was short-lived as originally constituted, its execution was clumsy, and the blow-up in Trump’s relationship with Elon Musk was an embarrassment. However, DOGE was a force for stanching the flow of taxpayer dollars through politicized NGOs. The budget savings were relatively small, but the defunded programs were often egregious varieties of government waste. Subsequently, DOGE personnel had an outsized influence on downsizing the federal bureaucracy and targeting waste across various agencies. In addition, the efforts of one-time DOGE workers were put to good use in identifying entitlement fraud, which could and should result in budget savings. Trump gets a B+ on this one.

Health and Health Care: I’ll give Trump credit here for pursuing a more consumer-oriented approach to health care reform, though at least one of his initiatives is counterproductive.

His initial steps took the form of EOs reducing subsidies paid on ACA marketplace policies, ending remaining penalties for violating the ACA’s individual mandate, approving short-term coverages free of certain ACA restrictions, cutting Medicaid expansion funding, and granting more flexibility for states in defining “essential” healthcare benefits. All of these are basically good steps.

Trump issued an ill-conceived EO calling for “Most-Favored Nation” (MFN) prescription drug pricing, which should reduce Americans’ prescription costs but will dramatically undercut life-saving drug research. Hate the pharmaceutical companies all you want, but they must earn a reasonable profit to risk the massive development costs of new miracle drugs, of which they’ve brought many to market. Price controls always create more problems than they solve.

In early 2026 Trump introduced his “Great Healthcare Plan” (GHP). It would codify MFN drug pricing, fund cost-sharing reductions for ACA plans, encourage price transparency, and redirect payments to consumers and away from insurers to facilitate choice and competition. Also launched was the TrumpRx.gov platform featuring MFN pricing. Ironically, the goal here is to improve access to prescription drugs. Good luck!

Under Robert F. Kennedy, Jr., Trump’s HHS Secretary, the “Make America Healthy Again” agenda has emphasized a healthy diet and exercise, including noteworthy changes in the famous food triangle hierarchy. I can’t argue with those. However, RFK Jr. has upended research under HHS, and those actions were rash in a number cases. He wants to address chronic diseases but I’m skeptical of some of his causal claims. I also have mixed reactions to his changed guidance on vaccines. There are reports that the White House has not been comfortable with all of RFK’s pronouncements and is eager to inject more oversight.

I have varied reactions to Trump’s efforts in the health care arena. MFN price capping is a good way to destroy the advantages Americans enjoy in terms of access to innovative drugs, even if they come at a steep cost. RFK Jr. is a wild card, to be fair. Otherwise, while the GHP should help to improve healthcare affordability, it neglects other critical reforms such as ending the disparate tax treatment of health care premiums and deregulating providers. Still, Trump’s grade improved here, from a D+ as a candidate to a B- thus far in his term.

Abortion: No change here. Trump has consistently supported the right to life. He gets an A.

Housing: Build Baby Build! But aside from harping on the Fed to lower interest rates, Trump hasn’t done much to encourage housing supply.

His EO banning institutional investors from owning “too many” single-family homes won’t help affordability because so few homes are owned by large investors. But to the extent that they are, the EO will increase rents and discourage new housing supply. This is another misguided foray into central economic planning.

While I think a 50-year mortgage should be legal, it’s something I believe potential homebuyers should avoid unless they want to risk stubbornly low equity in their homes stretching into retirement. Trump shouldn’t talk this up too much.

Trump has supported the “ROAD to Housing” bill, which has garnered bipartisan support. It would codify the restrictions on ownership of single-family housing by institutional investors and restrict construction of “rent-to-own” housing by such investors. One couldn’t invent a less effective way to encourage supply and promote “affordability”. But the bill would also subsidize demand, which will increase pressure on housing prices even as the bill aims to assist particular groups (e.g., tax credits for first-time homebuyers). Despite all those downsides, the bill actually includes a few steps to boost housing supply, such as making some federal lands available for development, regulatory reform, and tax incentives for builders.

Trump has also discussed changes to government sponsored enterprises (GSEs, Fannie Mae and Freddie Mac), which purchase new mortgages from lenders, including possible privatization. He might be licking his chops for the $300 billion the GSEs owe the federal government, which could be put toward various “deals” he might like to cut. If privatization were to end the explicit government guarantee for mortgage-backed securities issued by the GSEs, mortgage interest rates would rise and it could be quite disruptive for banks.

Housing policy is another mixed bag for Trump, but I’ll give him a B on the strength of his deregulatory effort.

Energy: Drill baby drill! Despite the current disruption to oil shipments through the straight of Hormuz and the spike in oil prices, I deem Trump’s energy policies a success thus far. Largely through deregulation, Trump has opened up the spigots on domestic oil production. He has also realigned energy priorities, eliminating subsidies and mandates for intermittent renewable energy sources in favor of encouraging fossil fuels, hydroelectric, and especially a new emphasis on nuclear power. Some of these steps represent unabashed central planning, so I can’t give Trump an A on energy policy,. However, the preceding green-energy regime was central planning on steroids with the unintended consequence of instability in the power grid. I would greatly prefer a policy of complete neutrality with respect to energy sources, but at least Trump is not cowed by global warming hysteria.

And Trump is considering a temporary suspension of the Jones Act due to the energy crunch brought on by the war in Iran. That would be great except that the waiver should be permanent. The move would lower energy (and other) costs to U.S. consumers and minimize supply disruptions by allowing energy (and other goods) to flow more freely between U.S. ports.

His grade on energy policy is a B.

First Amendment Rights: Trump has not been the defender of free speech that I had hoped. On this, I gave him an A- as a candidate, but his Administration has been belligerent in attacking speech. He (and his FCC Chairman) threaten media outlets with license revocation, his Attorney General says “we will target you” for anything DOJ attorneys might define as hate speech, and Trump has called certain speech he dislikes “illegal”. I also have qualms about an EO issued last year by Trump targeting “campaigns of … radicalization”, which might, in practice, bring any sort of opposition speech under scrutiny. And there are other potentially troublesome provisions for protected speech. Trump’s pure intent might be to stop violent radicalism, which is fine in spirit but hard to bring off without mass surveillance and violations of rights. I therefore downgrade Trump to a C on free speech.

Second Amendment Rights: Trump has not been quite as consistent on gun rights as he was as a candidate. He took a number of actions to reduce burdens and restrictions on gun rights, but in other cases he let restrictions stand, including arrests for gun possession in Washington DC by federal agents and a possible proposal to restrict the gun rights of transgendered individuals. All-in-all, I’ll reduce Trump’s A on gun rights to a B+.

DEI and Its Evil Financial Twin, ESG: There is no question that Trump has done much to cut through the stranglehold that DEI doctrine had imposed on social and economic life. He issued EOs to end DEI practices in the federal government. He also threatened major universities with funding freezes and anti-discrimation actions, an approach that has met with some success. Trump’s words and actions on DEI have reverberated through the private sector as well. He has encouraged individuals who believe they’ve suffered discrimination based on DEI to file lawsuits. The thrust of the Administration’s agenda on DEI and regulatory changes has served to undermine the use of ESG measures. These are intended to draw investors to companies purporting to foster environmental and social goals, which can be at odds with creating value for shareholders. Trump has earned his A in this category.

Technology: As in other policy domains, the record here is marred by misguided industrial policies. That includes the recent snafu over the Department of Defense’s allegation of “supply chain risk” posed by Anthropic. DoD wants carte blanche access to all aspects of any AI model it adopts, including uses in autonomous weapons systems and mass public surveillance. Anthropic said it would not accept that without guardrails, so an apparently infuriated Pete Hegseth moved to designate the company a supply chain risk, an outright punishment that would obviously damage Anthropic’s economic prospects. Yet almost immediately, DoD agreed to an arrangement with OpenAI with guardrails similar to those desired by Anthropic. Now, Trump, who seems to have Hegseth’s back, is readying an EO on the topic… so we shall see. But it’s a mess. Anthropic has filed suit.

And yet Trump has generally been supportive of AI development, signing an order to prevent states from imposing a patchwork of varying, complex regulations. The White House has issued an ”AI Action Plan” to encourage AI exports, minimizing federal regulatory burdens, and “upholding free speech” on “unbiased” frontier models. Let’s hope “unbiased” has a truly neutral definition in this case. Trump has signed a series of EOs related to AI research and deployment, which are linked here.

Post-inauguration, Trump dove right into another socialist joint venture known as Stargate to build data center infrastructure. The rationale for the government’s direct involvement is national security. Of course, that’s the Administration’s rough and ready excuse for almost any kind of intervention.

Trump has helped promote the crypto industry, supporting legislation (the CLARITY Act and the GENIUS Act) enabling more widespread use of stablecoins. He even supports the payment of returns on stablecoins, a development that is unpopular with banks. Trump has also acted to promote cybersecurity and harden infrastructure against malicious actors. More recently, he initiated a program to test eVTOL technologies (electronic vertical takeoff and landing), which are expected to revolutionize local and regional transportation in coming years.

The best I can give Trump on technology is a B-, given his penchant for government control. The Anthropic controversy is a real black eye.

Voting Rights: The Trump-backed SAVE America Act would require an ID proving citizenship to vote in federal elections. It’s stalled in the Senate, seven votes short of the 60 needed to send it to Trump’s desk. GOP senators are unwilling to force a talking filibuster, let alone to use the so-called “nuclear option” to force a simple-majority vote. There is still a possibility of including a voter ID requirement in a budget reconciliation bill if anyone can convince the Senate Parliamentarian that it would have budget impacts. For his part, Trump says he’ll refuse to sign any other legislation until the SAVE Act crosses his desk, though he’s also threatened to issue an EO mandating voter ID should the Senate fail to pass the bill. The constitutionality of such an order would be challenged, of course, but for his determination on the issue, I’ll give him an A+.

Education: This is a quick addition to the list. After inserting the photo of Trump at the top, I realized that I’d completely forgotten to add education as a performance category. Trump’s effort to dismantle the wasteful and unproductive Department of Education is to be applauded. He’s also been an unwavering supporter of school choice. I’ll give him an A here.

I have to stop! That’s 22 categories and a “grade point average” of 2.55 if the categories are equally weighted. It’s a little worse than Trump’s GPA as a candidate (2.67). He could have improved his grades dramatically without his bent for economic intervention, but I’d have to vote for him again given the alternative.

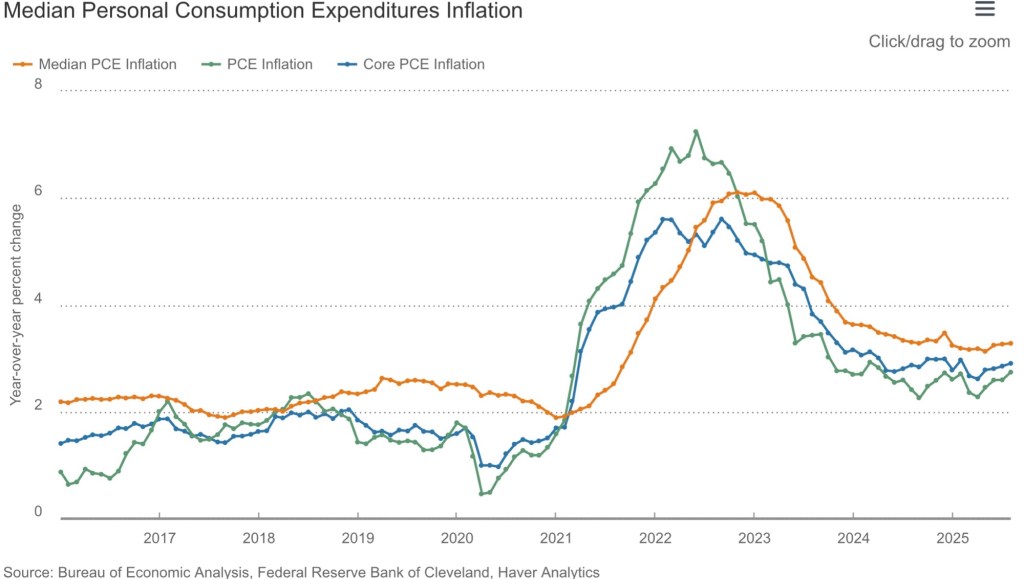

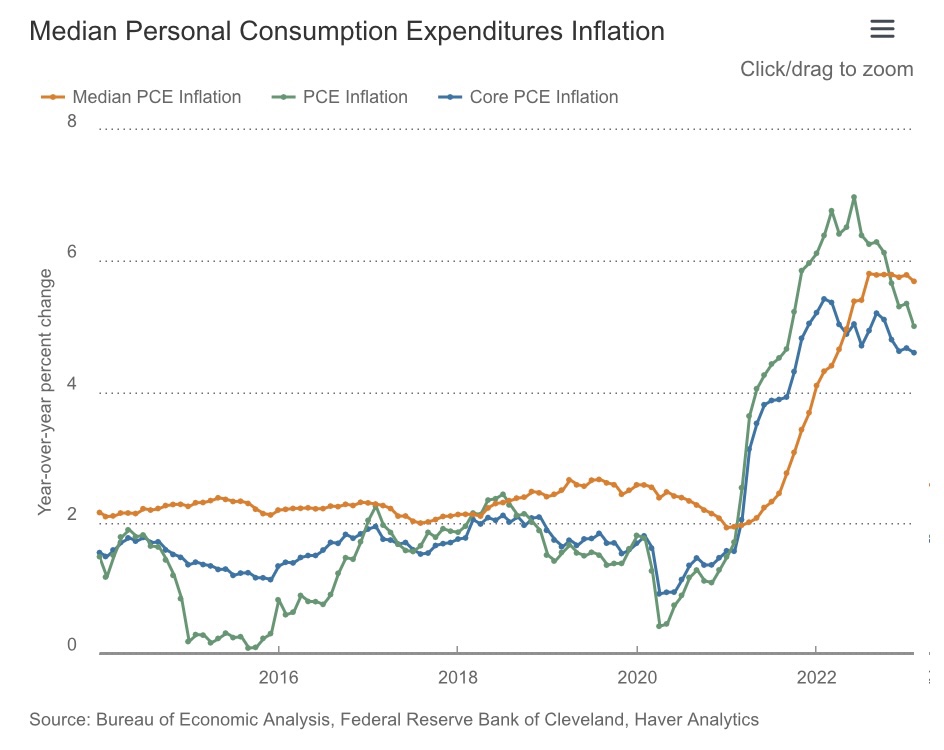

Inflation leveled off below 3% in 2024 and has drifted around the 3% level in 2025. The rate of increase in the core PCE (Personal Consumption Deflator) is the inflation measure of most interest to the Federal Reserve as a policy reference, but advances in the core CPI (Consumer Price Index) have settled at about the same level. The core inflation rates exclude food and energy prices due to the volatility of those components, but even with food and energy, inflation in the PCE and the CPI have been running near 3%.

It’s a 2% Target… Or Is It?

The Fed continues to maintain that its “official” inflation target is 2% for the core PCE. However, the central bank is now easing policy despite inflation running a full percentage point faster than the target. The rationale turns on the Fed’s dual mandate to maintain both “price stability” and full employment, goals that are not always compatible.

Currently, the labor market is showing signs of weakness, so the Fed has elected to ease policy by guiding the federal funds rate downward, and by putting a stop to run-off in its balance sheet holdings of securities. The latter ends a brief period of so-called quantitative tightening.

Just a couple of months ago, the central bank announced a new emphasis on targeting 2% inflation in the long run, with notable differences from the “flexible average inflation targeting” (FAIT) that it claimed to have adopted in 2020. In some respects, the Fed appeared to be giving more primacy to the “2%” definition of price stability than to the full employment mandate. Yet the “new approach” still allows plenty of wiggle room and might not differ much from the approach followed prior to FAIT.

“… an asymmetric approach to the dual mandate: It would implement makeup policy on misses below the inflation target, and it would respond to shortfalls from maximum employment. These asymmetries, while well- intended, created an inflationary bias that caused FAIT to fail the ‘stress test’ of the 2021–22 inflation surge. This failure caused the Fed to effectively abandon FAIT in early 2022 and become a single-mandate central bank focused on price stability.“

Scott Sumner says the Fed never really really practiced FAIT to begin with. It should have been a symmetric policy, but it wasn’t. During 2021-22, the Fed did not attempt to correct for rising inflation. Instead, it focused on the recessionary effects of Covid and the impingements of Covid-era restrictions on employment.

Clearly, Covid was a shock that monetary policy was ill-suited to address without reinforcing inflation. Furthermore, the pandemic inflation was thought by the Fed to be transitory, but easing policy was a critical error. Stimulating demand via monetary accommodation gave inflation more permanence than the Fed apparently expected.

Lost In the Tea Leaves Again

While a strong commitment to price stability is welcome, it’s not clear that is what’s guiding the Fed’s decisions at the moment. Again, the Fed’s preferred inflation gauge has flattened out at around 3%. However, with uncertainty about tariffs and tariff pass throughs in 2026, the weak dollar, and unrelenting Treasury borrowing, easier monetary conditions could well set the stage for persistent inflation above 3%, despite the official 2% target. That might help explain the failure of longer-term interest rates to decline in the wake of the Fed’s latest quarter-point cut in the federal funds target in October.

Suspicious Minds

Speculation that the Fed is allowing its true inflation target to creep upward is hardly new. Back in June, former New York Fed economist Robert Brusca noted the following:

“A Cleveland Fed survey already has the business community thinking that the REAL target for inflation is 2.5%.”

More recently, Mark Sobel of the Official Monetary and Fiscal Institutions Forum stated that the real target, for now, is probably 3%:

“But could the Fed stealthily and unintentionally end up near 3%? Even apart from above-target inflation in recent years, short- and longer-term structural forces are at play that could usher in slightly higher inflation, notwithstanding Fed speeches on the sanctity of the 2% inflation target.“

Chewing On Data

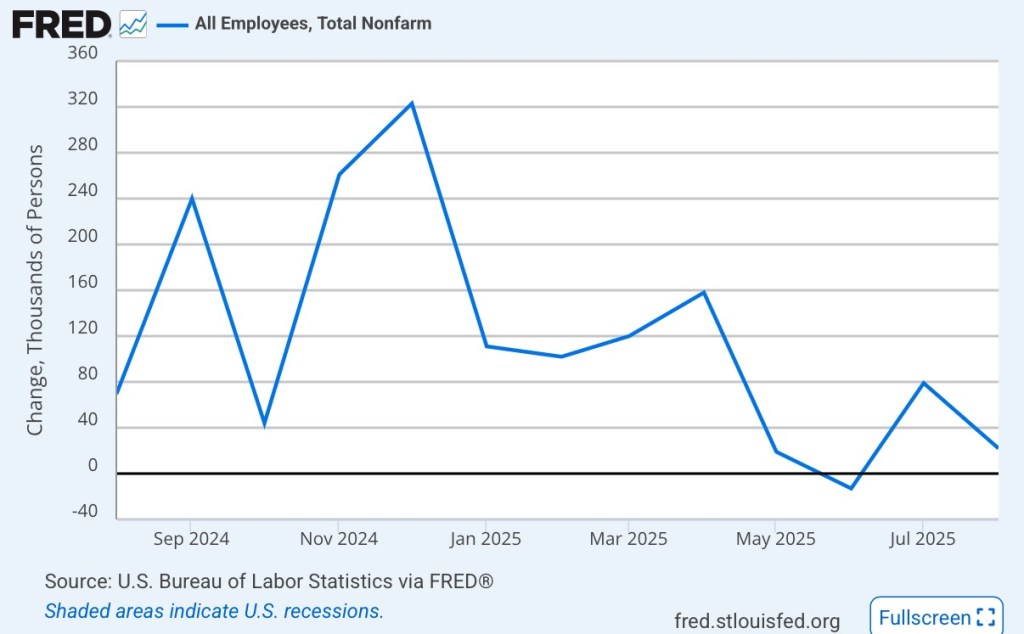

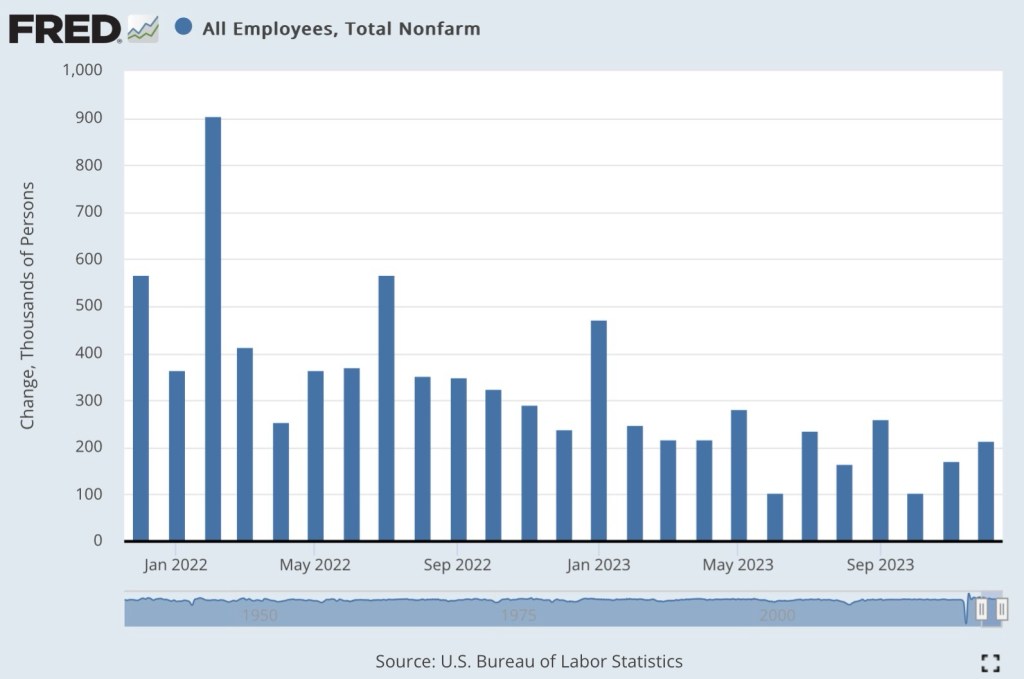

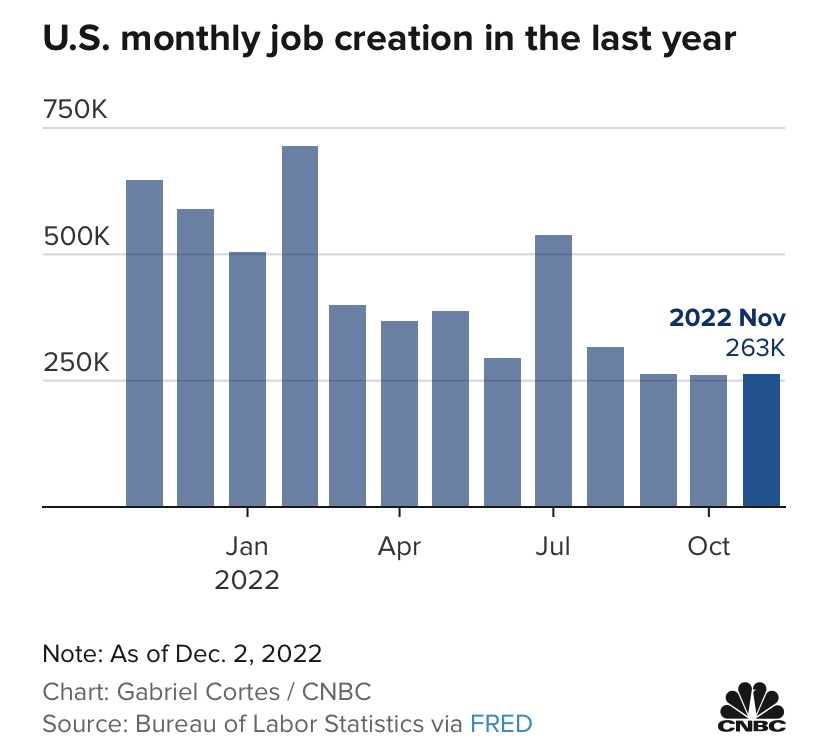

It’s pretty clear that the Fed has become a skittish about the pace of the real economy, lending more weight to the full employment part of its dual mandate. Employment growth slowed over the past year, partly due to government employee buy-outs and separations of illegal immigrants from their employers. The last official employment report was in early September, however, so the nonfarm payroll data is two months out-of-date:

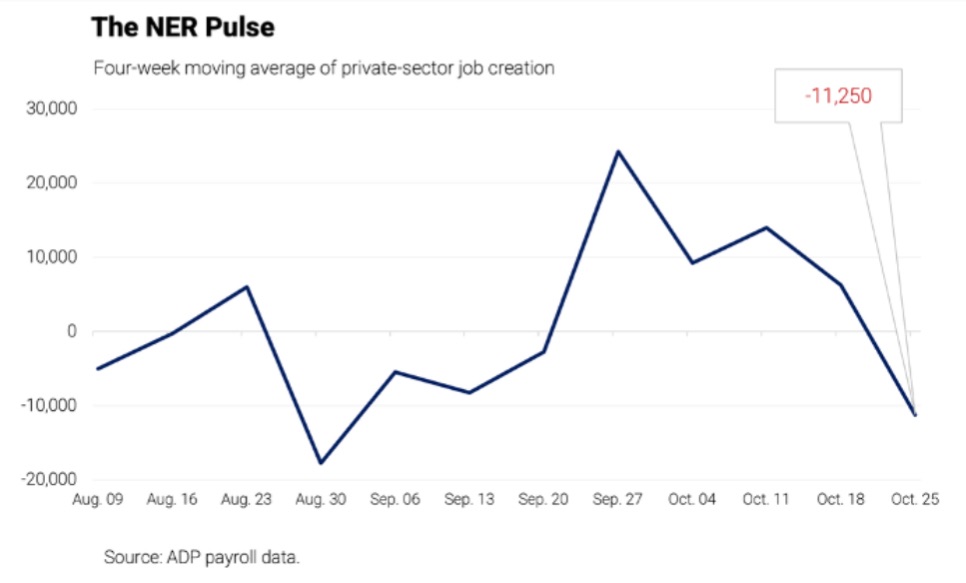

Private payroll growth from ADP over the past two months has not looked especially encouraging:

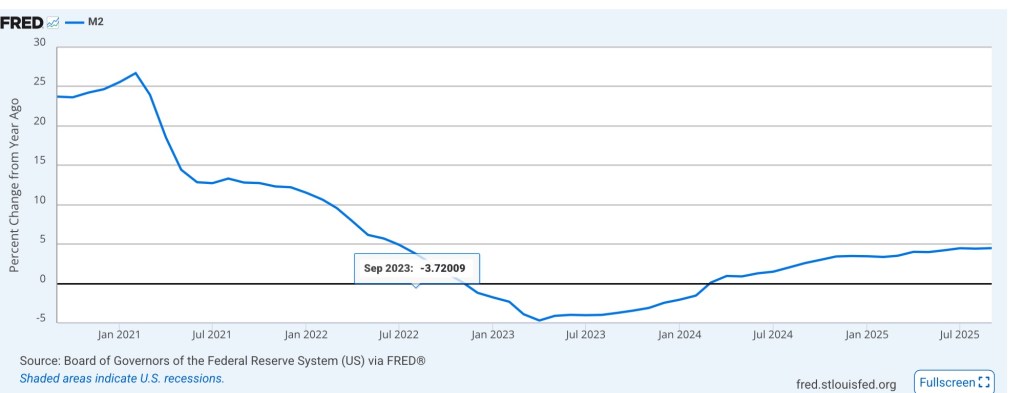

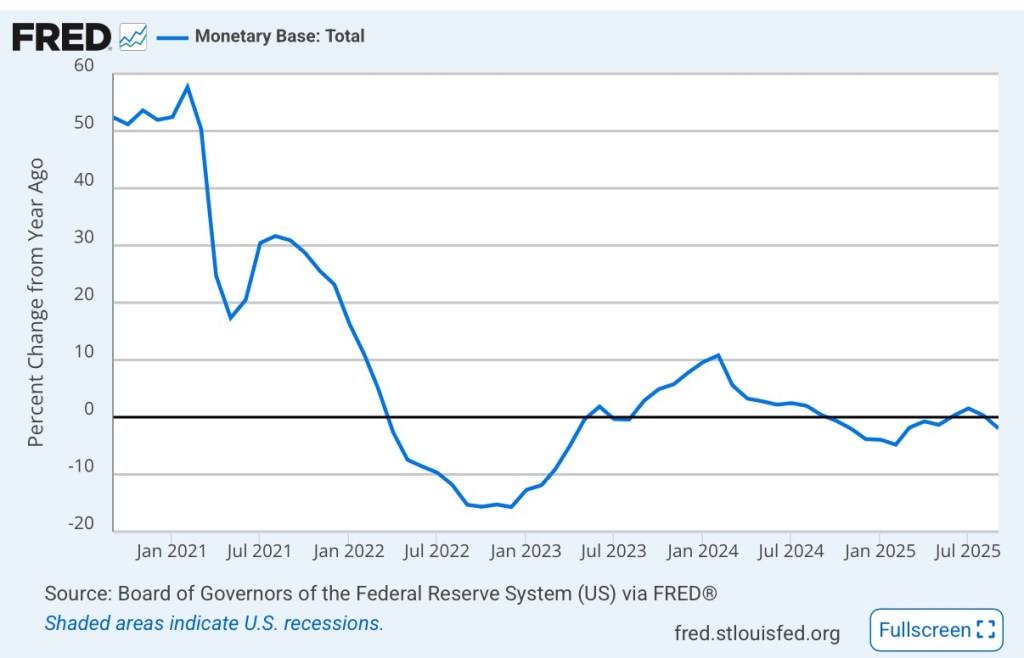

Tariffs and weakened profit margins have likely had a contractionary effect, and the six-week government shutdown just ended will shave 0.5% or more off fourth quarter GDP growth. Furthermore, while money (M2) growth has accelerated over the past year, it remains fairly restrained.

And the monetary base has been pretty flat for most of 2025:

We’ll see where these aggregates go from here. The extended “restraint” might now be of some concern to the Fed, given recent doubts about employment and economic growth. Still, in October, Fed Chairman Jerome Powell said that another quarter-point cut in the federal funds rate target in December was not a foregone conclusion. That statement seems to have worried equity investors while offering little solace to bond investors.

Aborted Landing

If (and as long as) the Fed gives primacy or greater weight in its policy deliberations to employment than inflation, it might as well have adopted an inflation target of 3% or more. The additional erosion in purchasing power wrought by that leniency is bad enough, but the effect of monetary policy on the real side of the economy is more poorly understood than its effect on nominal variables. The Fed’s shift in priorities is both unreliable on the real side and dangerous in terms of price stability. These concerns are even more salient given the upcoming appointment (in May) of a new Fed Chairman by President Trump, who seems eager for easy money.

President Trump engaged in one of his favorite pastimes on June 18 while the Federal Reserve Open Market Committee (FOMC) was concluding its meeting on the direction of monetary policy. He publicly called Fed Chairman Jerome Powell “stupid” for not having cut rates already, and later said the Fed’s board was “complicit”.

“”I don’t know why the Board doesn’t override this Total and Complete Moron!“

Trump also tagged Powell with one of his trademark appellations: “Too Late”. Yep, that’s how Trump says he refers to Powell.

Later that day, the Fed once again announced that it had decided to leave unchanged its target range for the interest rate on federal funds. Powell described the overall tenor of current Fed policy as mildly restrictive, but FOMC members still “expect” (loosely speaking) two quarter-point cuts in the funds rate by year end.

Of course, Powell and the FOMC really were far too late in recognizing that inflation was more than transitory in 2021-22. Now, with inflation measures tapering but still higher than the Fed’s 2% target, Trump says “Too Late” Powell and the Fed are again behind the curve. Of course, because the central bank is outside the President’s direct control, it makes a convenient scapegoat for whatever might ail the Trump economy, and Trump frets that unnecessarily high rates will cost the U.S. Treasury hundreds of billions in interest on new and refinanced federal debt.

The President has no appreciation for the value of an independent central bank, as opposed to one captive to the fiscal whims of Presidents and Congress. Despite his frequent criticism of inflationary sins of the past, Trump doesn’t understand the dangers of a central bank that could be bullied into inflating away government debt.

The day after the Fed’s meeting, Trump said rates should be cut immediately by a huge 2.5%! As the Donald might say, no one’s ever seen anything like it!

Trump, however, is delusional to think the Fed can engineer reductions in the spectrum of interest rates by aggressively slashing its fed funds target. The Fed does not control long-term interest rates, nor is that part of the Fed’s formal mandate. In fact, an aggressively large reduction in the fed funds rate is likely to backfire, feeding expectations of higher inflation and a selloff in credit markets.

Let me reiterate: the Fed does not control long-term interest rates. Short-term rates are more heavily influenced by the Fed’s rate actions, and by expectations of Fed policy, but the Fed is likewise influenced by those very expectations. In fact, the Fed often follows market rates rather than leading them. In any case, a general truth is that long-term interest rates go where market forces direct them, not where the Fed might try to push them.

Today the Fed is attempting to walk a line between precipitating divergent and potentially negative outcomes. It wants to see clear evidence that inflation is settling down at roughly the 2% target. Also, the Fed is wary that Trump’s tariffs might generate a near-term spike in prices. Under those circumstances, prematurely easing policy could rekindle more permanent inflationary pressures. It seems clear that the Fed currently judges inflation as the dominant risk.

At the same time, the real economy shows mixed signals. Clear signs of a downturn would likely prompt the Fed to cut its fed funds target sooner. After the latest meeting, the Fed announced that it had reduced its own forecast for real GDP growth in 2025 to just 1.4%. Recent employment gains have been moderate, but jobless claims are trending up. The unemployment rate is low, but the labor force has declined over the past few months, which incidentally might be putting upward pressure on wages.

Policy uncertainty was a major theme in the Fed’s June rate decision. Tariffs loom large and would be a threat to continued growth if producers, facing weak demand, were unable to pass the cost of tariffs through to customers, undermining their profit margins. Prospects for passage of the budget reconciliation bill create more uncertainty, providing another rationale to stand pat without cutting the funds rate.

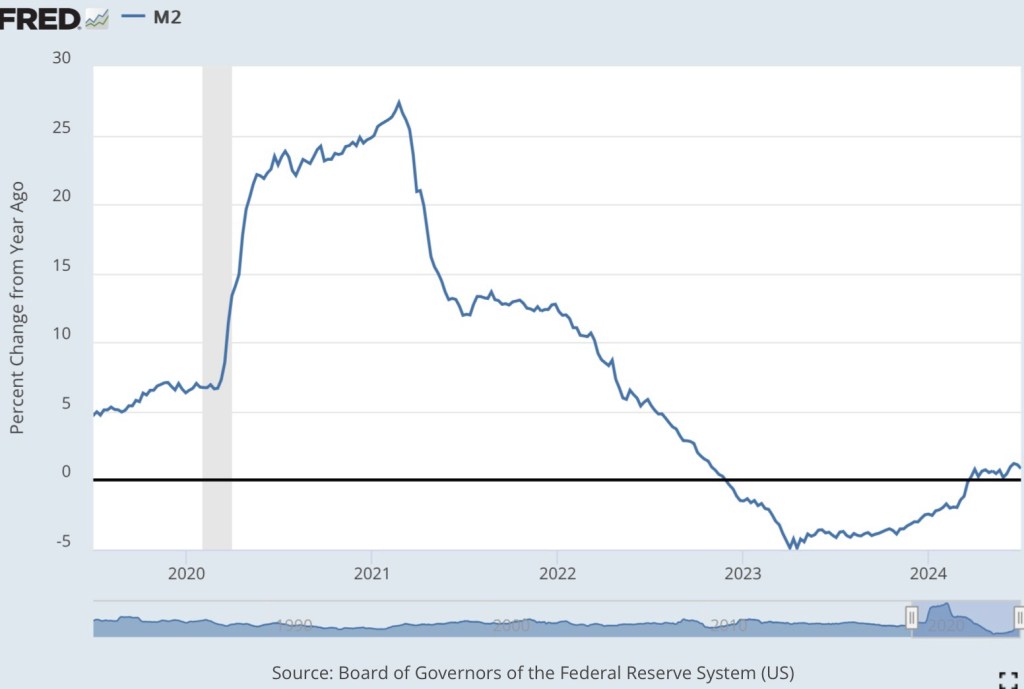

Again, Jerome Powell says that Fed policy is “modestly restrictive” at present. In fact, estimates of the “policy neutral” Fed funds rate are in the vicinity of 2.75%, well below the current target range of 4.25-4.50. However, the money supply (M2) has drifted up over the past year and by May was up 4.4% from a year earlier. That would be consistent with 2% inflation and better than 2% real growth, the latter being higher than the FOMC’s expectation.

Another consideration is that the Fed has nearly ended its quantitative tightening (QT) program, having recently trimmed the passive runoff of maturing securities in its portfolio to just $5 billion per month. This leads to less downward pressure on bank reserves and less upward pressure on the fed funds rate. In other words, policy has already shifted toward greater support for money growth. But out of caution, the Fed wants to defer reductions in the funds rate to avoid undermining the central bank’s inflation-fighting credibility.

Jerome Powell and the FOMC probably could not care less about Trump’s exhortations to reduce interest rates. For one thing, it is beyond the Fed’s power to force down rates that could spur housing and other economic activity. And Trump should be grateful: such a reckless attempt would risk great harm to markets and the economy, not to mention Trump’s economic agenda. Better to wait until near-term inflation risks and policy uncertainty clear up.

Trump can jawbone as aggressively as he wants. He cannot fire Powell, though he keeps saying he “should”. However, no matter what actions the Fed takes, he will almost certainly not reappoint Powell to lead the Fed when Powell’s term expires next May. Sadly, Trump will try to appoint a replacement he can rely upon to do his bidding. Let’s hope the Senate stands in his way to preserve Fed independence.

Matt Yglesias tweeted on X that “the bond market does not appear to believe in DOGE”. He included a chart much like the updated one above to “prove” his point. Tyler Cowen posted a link to the tweet on Marginal Revolution, without comment … Cowen surely must know that any such conclusion is premature, especially based on the movement of Treasury yields over the past month (or more, since the market’s evaluation of the DOGE agenda preceded Trump’s inauguration).

Of course, there is a difference between “believing” in DOGE and being convinced that its efforts should have succeeded in reducing interest rates immediately amidst waves of background noise from budget and tax legislation, court challenges, Federal Reserve missteps (this time cutting rates too soon), and the direction of the economy in general.

In this case, perhaps a better way to define success for DOGE is a meaningfully negative impact on the future supply of Treasury debt. Even that would not guarantee a decline in Treasury rates, so the premise of Yglesias’ tweet is somewhat shaky to begin with. Still, all else equal, we’d expect to see some downward pressure on yields if DOGE succeeds in this sense. But we must go further by recognizing that DOGE savings could well be reallocated to other spending initiatives. Then, the savings would not translate into lower supplies of Treasury debt after all.

Certainly, the DOGE team has made progress in identifying wasteful expenditures, inefficiencies, and poor controls on spending. But even if the $55 billion of estimated savings to date is reliable, DOGE has a long way to go to reach Musk’s stated objective of $2 trillion. There are some juicy targets, but it will be tough to get there in 17 more months, when DOGE is to stand down. Still, it’s not unreasonable to think DOGE might succeed in accomplishing meaningful deficit reduction.

But if bond traders have doubts about DOGE, it’s partly because Donald Trump and Elon Musk themselves keep giving them reasons. In my view, Musk and Trump have made a major misstep in toying with the idea of using prospective DOGE savings to fund “dividend checks” of $5,000 for all Americans. These would be paid by taking 20% of the guesstimated $2 trillion of DOGE savings. Musk’s expression of interest in the idea was followed by a bit of clusterfuckery, as Musk walked back his proposal the next day even as Trump jumped on board. PLEASE Elon, don’t give the Donald any crowd-pleasing ideas! And don’t lose sight of the underlying objective to reduce the burden of government and the public debt.

Now, Trump proposes that 60% of the savings accomplished by DOGE be put toward paying for outlays in future years. Sure, that’s deficit reduction, but it may serve to dull the sense that shrinking the federal government is an imperative. The mechanics of this are unclear, but as a first pass, I’d say the gain from investing DOGE savings for a year in low-risk instruments is unlikely to outweigh the foregone savings in interest costs from paying off debt today! Of course, that also depends on the future direction of interest rates, but it’s not a good bet to make with public funds.

Nor can the bond market be comforted by uncertainty surrounding legislation that would not only extend the Trump tax cuts, but will probably include various spending provisions, both cuts and increases. As of now, the mix of provisions that might accompany a deal among GOP factions is very much up in the air.

There is also trepidation about Trump’s aggressive stance toward the Federal Reserve. He promises to replace Jerome Powell as Fed Chairman, but with God knows whom? And Trump jawbones aggressively for lower rates. The Fed’s ill-advised rate cuts in the fall might have been motivated in part by an attempt to capitulate to the then-President Elect.

Trump’s Executive Order to create a sovereign wealth fund (SWF), which I recently discussed here, is probably not the most welcome news to bond investors. All else equal, placing tax or tariff revenue into such a fund would reduce the potential for deficit reduction, to say nothing of the idiocy of additional borrowing to purchase assets.

Finally, Trump has proposed what might later prove to be massive foreign policy trial balloons. Some of these are bound up with the creation of the SWF. They might generate revenue for the government without borrowing (mineral rights in Ukraine? Or Greenland?), but at this point there’s also a chance they’ll create massive funding needs (Gaza development?). Again, Trump seems to be prodding or testing counterparties to various negotiations… prodding diplomacy. It’s unlikely that anything too drastic will come of it from a fiscal perspective, but it probably doesn’t leave bond traders feeling easy.

At this stage, it’s pretty rash to conclude that the bond market “doesn’t believe in DOGE”. In fact, there is no doubt that DOGE is making some progress in identifying potential fraud and inefficiencies. However, bond traders must weigh a wide range of considerations, and Donald Trump has a tendency to kick up dust. Indeed, the so-called DOGE dividend will undermine confidence in debt reduction and bond prices.

The late, great Milton Friedman said monetary policy has “long and variable lags” in its effect on the economy. Easy money might not spark an inflation in goods prices for two years or more, though the typical lag is thought to be more like 15-20 months. Tight money seems to have similar lags in its effects. Debates surround the division and timing of these effects between inflation and real GDP, and too many remain convinced that a reliable tradeoff exists between inflation and unemployment.

With that preface, where do we stand today? The Fed executed a veritable helicopter drop of cash during the pandemic, in concert with support payments by the Treasury, with predictable inflationary results. It was also, in part, an accommodation to supply-side pressures. Then the tightening of policy began in the spring of 2022. How will the timing and strength of these shifting policies ultimately play out, as well as the impact of expectations regarding future policy moves?

Help On the Way?

Federal Reserve Chairman Jerome Powell and the Fed’s Open Market Committee (FOMC) are now poised to ease policy after three-plus years of a tighter policy stance. The FOMC is widely expected to cut its short-term interest rate target by a quarter point at the next FOMC on September 17-18. There is an outside chance that the Fed will cut the target by a half point, depending on the strength of new data to be released over the next couple of weeks. In particular, this Friday’s employment report looms large.

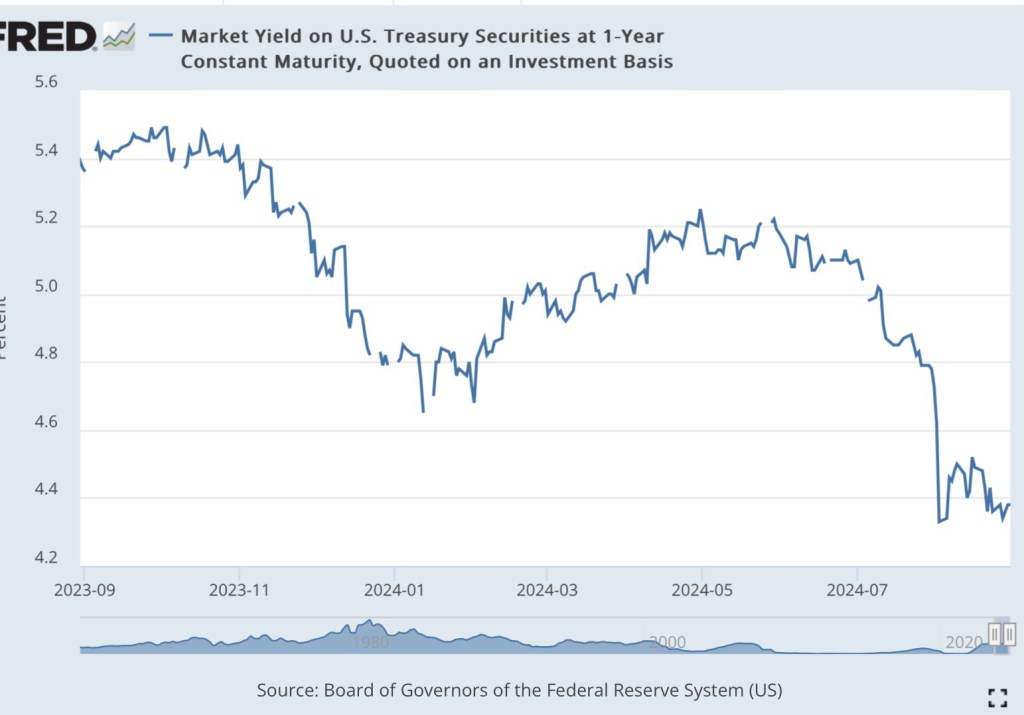

What sometimes goes unacknowledged is that the Fed will be following market rates downward, not leading them. The chart below shows the steep drop in the one-year Treasury yield over the past couple of months. Other rates have declined as well. Granted, longer rates are determined in large part by expectations of future short-term rates over which the Fed has more control.

And yet the softening of market rates may well be a signal of weaker economic activity. There is certainly concern among investors that a failure by the Fed to ease policy might jeopardize the much hoped-for “soft landing”. The lagged effects of the Fed’s tighter policy stance may drag on, with damage to the real economy and the labor market. Indeed, some assert that a recession remains a strong possibility (and see here), and the manufacturing sector has been in a state of contraction for five months.

On the other hand, the Fed has fallen short of its 2% inflation goal. The core PCE deflator, the Fed’s preferred inflation gauge, was up 2.6% for the year ending in July. Some observers fear that easing policy prematurely will lead to a new acceleration of inflation.

Powell Gives the Nod

Nevertheless, markets were relieved when Jerome Powell, in his recent speech in Jackson Hole, Wyoming, indicated his determination that a shift in policy was appropriate. From Bloomberg:

“Federal Reserve Chair Jerome Powell said ‘the time has come’ for the central bank to start cutting interest rates.

“Powell’s comments cemented expectations for a rate cut at the central bank’s next gathering in September. The Fed chief said the cooling of the labor market is ‘unmistakable,’ adding, ‘We do not seek or welcome further cooling in labor market conditions.’ Powell also said his confidence has grown that inflation is on a ‘sustainable path’ back to the Fed’s goal of 2%.“

The “sustainable path back to … 2%” might imply a view inside Fed that policy will remain somewhat restrictive even after a quarter or half-point rate cut in September. Or perhaps the “sustainable path” has to do with the aforementioned lags, which might continue to be operative regardless of any immediate change in policy. The feasibility of a “soft landing” depends on whether policy is indeed still restrictive or on how benign those lagged effects turn out to be. But if we take the lags seriously, an easing of policy wouldn’t have real economic force for perhaps 15 months. Still, the market puts great hope in the salutary effects of a move by the Fed to ease policy.

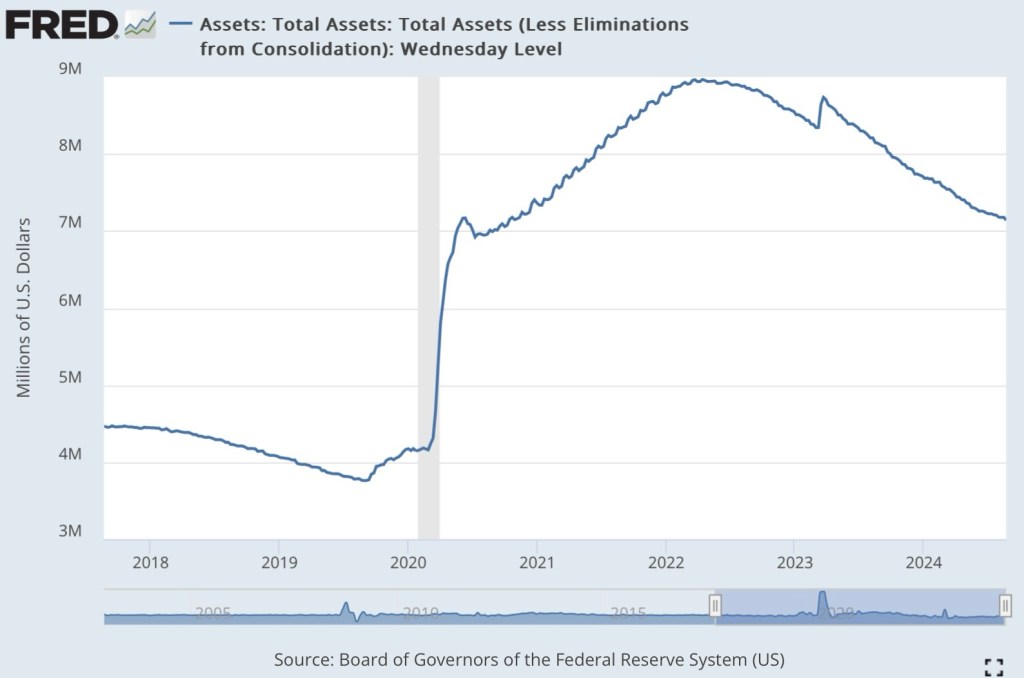

Big Balance Sheet

It can be argued that the Fed already took a step toward easing policy in May when it reduced the rate at which it was allowing runoff in its portfolio of Treasury and mortgage-backed securities. Prior to that, it had been redeeming $95 billion of maturing securities a month. The new runoff amount is $60 billion per month. Unless neutralized in other ways, the runoff has a contractionary effect on bank reserves and the money supply. It is known as “quantitative tightening” (QT). but then the May announcement was a de facto easing in the degree of QT.

Thus far, the total reduction in the Fed’s portfolio has amounted to only $1.7 trillion from the original high-water mark of $8.9 trillion. Here is a chart showing the recent evolution in the size of the Fed’s securities holdings.

The Fed’s current balance sheet of $7.2 trillion is gigantic by historical standards. It’s reasonable to ask why the Fed considers what we have now to be a more “normalized” portfolio, and whether its size (and correspondingly, the money supply) represents potential “dry tinder” for future inflation. It remains to be seen whether the Fed will further pare the rate of portfolio runoff in the months ahead.

Money growth had been running negative for roughly a year and a half, but it edged closer to zero in late 2023 before accelerating to a slow, positive rate a few months into 2024. The timing didn’t exactly correspond to the Fed’s slowing of portfolio runoff. Nevertheless, the Fed’s strong preference is to supply the banking system with “ample reserves”, and reserves drive money growth. Thus, the Fed’s reaction to conditions in the market for reserves was a factor allowing money growth to accelerate.

A Cut Too Soon?

A rate cut later this month will make reserves still more ample and support additional money growth. And again, this will be an effort to mediate the negative impact of earlier policy tightness, but the effect of this move on the economy will be subject to similar lags.

A danger is that the Fed might be easing too soon, so that inflation will fail to taper to the 2% goal and possibly accelerate again. And perhaps policy was not quite as tight as it needed to be to achieve the 2% goal. Now, new supply bottlenecks are cropping up, including a near shutdown of shipping through the Suez Canal and a potential strike by east coast dockworkers.

Fiscal Incontinence

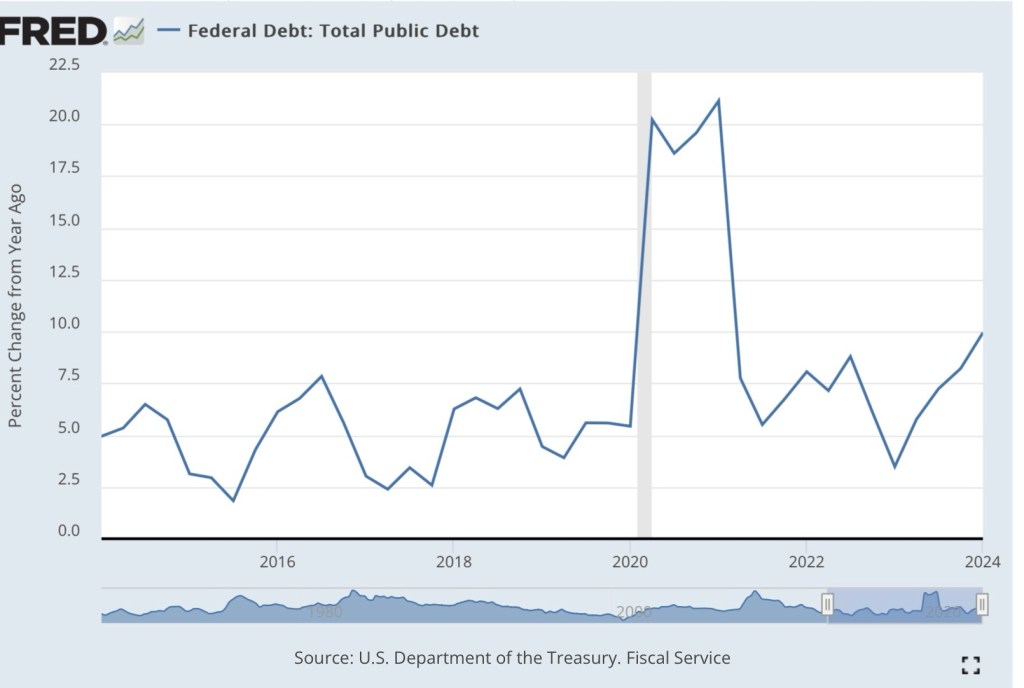

An even greater threat now, and in the years ahead, is the massive pressure placed on the economy and the Fed by excessive federal spending and Treasury borrowing. The growth of federal debt over the 12 months ending in July was almost 10%. Total federal debt stands at about $35 trillion. According to the Congressional Budget Office (CBO) projections, federal debt held by the public will be almost $28 trillion by the end of 2024 (the rest the public debt is held by the Fed or federal agencies). The CBO also projects that the federal budget deficit will average almost $1.7 trillion annually through 2027 before rising to $2.6 trillion by 2034. That would bring federal debt held by the public to more than $48 trillion.

Inflation is receding ever so slowly for now, but it’s unclear that investors will remain comfortable that growth in the public debt can be paid down by future surpluses. If not, the only way its real value can be reduced is through higher prices. Most observers believe such an inflation requires that the Fed monetize federal debt (buy it from the public with printed money). Tighter credit markets will increase pressure on the Fed to do so, but the growing debt burden is likely to exert upward pressure on the prices of goods with or without accommodation by the Fed.

Hard, Soft, Or Aborted Landing?

Some economists are convinced that the Fed has successfully engineered a “soft landing”. I might have to eat some crow…. I felt that a “hard landing” was inevitable from the start of this tightening phase. Even now I would not discount the possibility of a recession late this year or in early 2025. And perhaps we’ll get no “landing” at all. The Fed’s expected policy shift together with the fiscal outlook could presage not just a failure to get inflation down to the Fed’s 2% target, but a subsequent resurgence in price inflation.

When Federal Reserve Chairman Jerome Powell said “higher for longer” last year, it wasn’t about the Grateful Dead concerts he’s attended over the years. No, he meant the Fed might need to raise its short-term interest rate target and/or keep it elevated for an extended period to squeeze inflation out of the economy. As late as December, Powell said that additional rate hikes remain on the table. But short of that, the Fed might keep its current target rate steady until inflation is solidly in-line with its 2% objective. The obvious risk is that tight monetary policy might tip the economy into recession. The market, for its part, is pricing in several rate cuts this year.

Thus far, the release of key economic data for December 2023 has not settled the debate as to whether disinflation has truly paused short of the Fed’s goal. There were inauspicious signs from the labor market in December as well. These data releases don’t rule out a “soft landing”, but they indicate that recession risks are still with us in 2024. The Fed will face a dilemma if the economy weakens but inflation fails to abate, either due to residual stickiness or new supply shocks. The latter are unfolding even now with the shut down of Red Sea shipping.

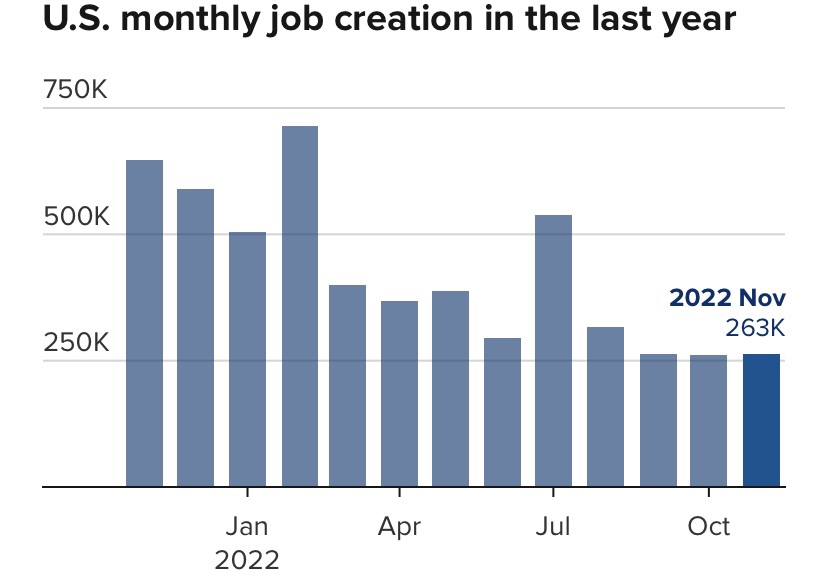

Bad Employment Report

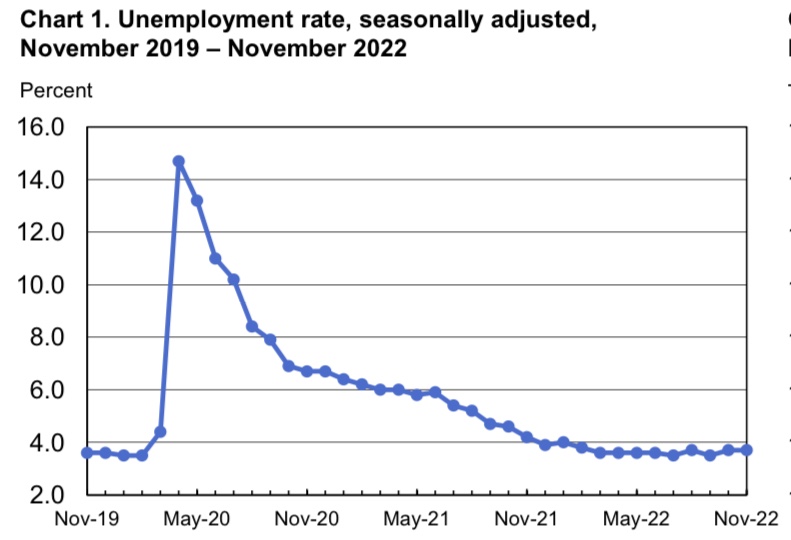

On the surface, the employment report from the Bureau of Labor Statistics (BLS) was strong relative to expectations, and the media reported it on that superficial level: nonfarm payrolls increased by 216,000 jobs, about 45,000 more than expected; unemployment was unchanged from November at 3.7%.

Unfortunately, the report contained several ominous signs:

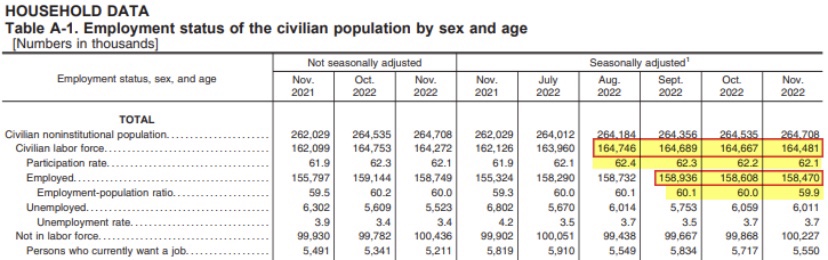

1) Employment from the BLS Household Survey declined by 683,000 in December and is essentially flat since July. This discrepancy should be rather unsettling to anyone waving off the possibility of a recession.

2) The number of full-time workers decreased by 1.53 million in December, and the number of part-time workers increased by 762,000 as the holidays approached. Retail employment was not particularly strong however, and the big loss of full-time work stands in contrast to the “strong-report” narrative.

3) The number of multiple jobholders hit a record and increased by 556,000 over the past year. This might indicate trouble for some workers making ends meet.

5) The civilian labor force declined by 676,000. What accounts for the change in status among these former workers or job seekers?

6) From the BLS Establishment Survey, government hiring accounted for 24% of the nonfarm jobs filled in December. Social Services accounted for 10% of the new hiring and health care for 18%, both of which are heavily dependent on government.

7) Nonfarm payrolls were revised downward by a total of 71,000 for October and November. We’ve seen downward revisions for 10 of the past 11 months.

8) In total, initial monthly job reports in 2023 overstated the full-year gain in nonfarm employment after available revisions by 439,000.

Those are big qualifiers on the “stronger than expected” jobs report. Furthermore, I tend to discount new government jobs as a real engine of production possibilities, so the report didn’t offer much assurance about the economy’s momentum. In addition, there are estimates that the payroll gain was due to better weather than the seasonal adjustment factors indicate.

Fictional Payroll Gains?

Still other issues cast doubt on the BLS payroll numbers. First, they are based on a survey of employers that is not complete by the time of each month’s initial report. Second, the survey is heavily skewed toward employees of government and large corporations; the sample of small employers is light by comparison. Third, seasonal adjustments often swamp the unadjusted changes in payrolls.

Finally, the BLS uses a statistical model of business births/deaths to adjust the figures. This is intended to correct for a lag in survey coverage as new businesses are formed and others close. The net effect on the payroll estimate can be positive or negative. Unfortunately, it’s difficult for even the BLS to tell how much the birth/death model affects the headline nonfarm jobs figure in any particular month. Therefore, it’s tough to put much faith in the monthly reports, but we watch them anyway.

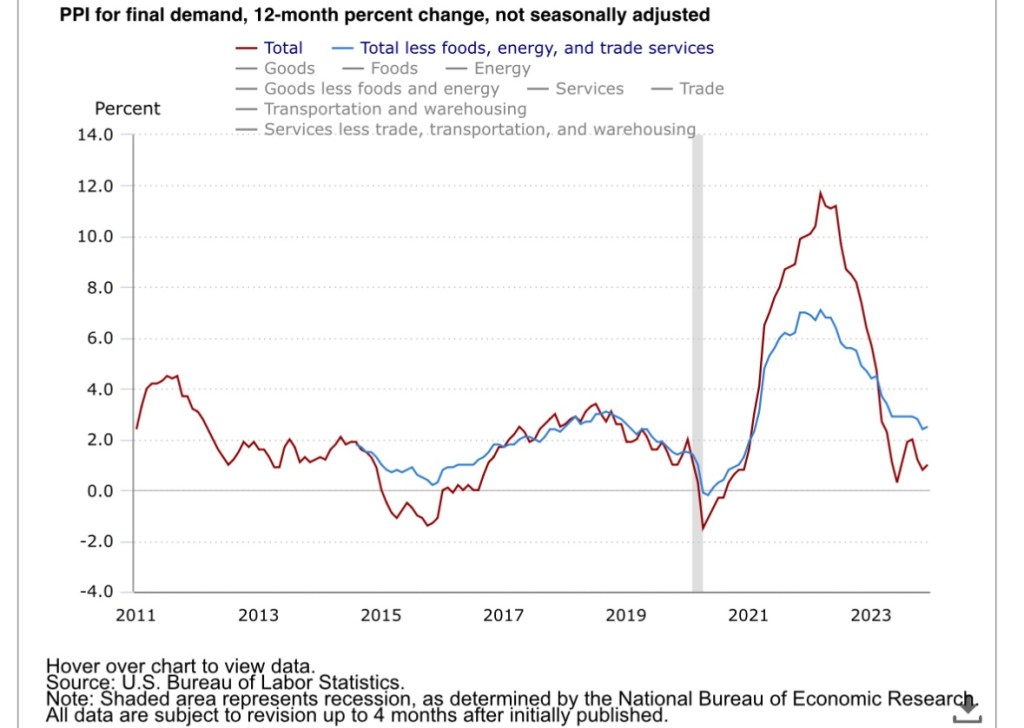

Stubborn Inflation

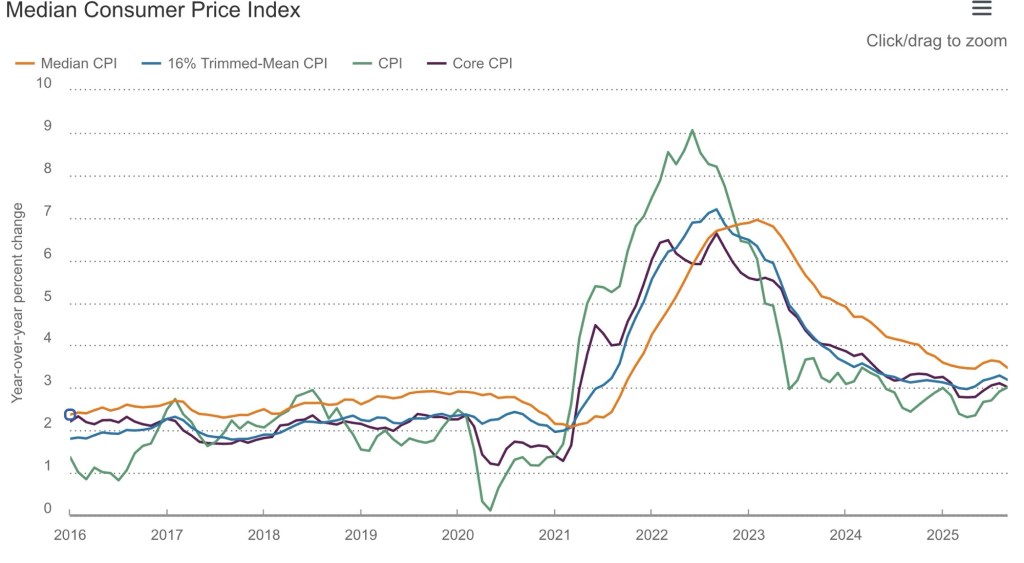

The Consumer Price Index (CPI) for December increased 0.3% over November and 3.4% year-over-year, slightly more than expectations of 0.2% and 3.2%, respectively. The “core” CPI (excluding food and energy prices) rose 3.9% year-over-year, more than the 3.8% expected. The core rate declined on a one-month and year-over-year basis, however, as did the median item in the CPI.

All CPI measures in the chart declined during 2023, though the core and median lagged the headline CPI (green line), which “flattened” somewhat during the last half of the year. So there appears to be some stickiness hindering disinflation in the CPI at this point, but the apparent “stickiness” has been confined to lagging declines in housing costs (also see here).

The Producer Price Index (PPI) reported a day later was thought to be benign. Like the CPI, disinflation in the core PPI has tapered:

In this context, it should be noted that declines in the Fed’s preferred inflation gauge, the PCE deflator, have also undergone something of a pause, and the PCE weights housing costs much less heavily than the CPI.

The CPI and PPI reports don’t offer any reason for the Fed to reduce its target federal funds rate over the next couple of Federal Open Market Committee (FOMC) meetings. There are two more sets of monthly inflation reports before the meeting in late March, so things could change. But again, the Fed has given ample guidance that it might have to leave its target rate at the current level for an extended period.

The Market View

Markets had priced-in six cuts in the Fed funds rate target in 2024 prior to the CPI report, but traders began to discount that possibility in its immediate aftermath. However, members of the FOMC expected an average of three cuts in 2024, with more to come in 2025, whether or not that’s consistent with “higher for longer”. Inflation is hovering somewhat above the Fed’s goal, but getting the rest of the job done might be tough, and indeed, might imply “longer” if not “higher”.

But why did the market ever hold the expectation of six cuts this year? Traders must have anticipated an economic contraction, which would kick the Fed into rapid response mode. The employment report offered no assurance that such a “hard landing” will be avoided. A few more negative signals on the real economy without further progress on prices would provide quite a test of the Fed’s inflation-fighting resolve.

To the great chagrin of some market watchers, the Federal Reserve Open Market Committee (FOMC) increased its target for the federal funds rate in March by 0.25 points, to range of 4.75 – 5%. This was pretty much in line with plans the FOMC made plain in the fall. The “surprise” was that this increase took place against a backdrop of liquidity shortfalls in the banking system, which also had taken many by surprise. Perhaps a further surprise was that after a few days of reflection, the market didn’t seem to mind the rate hike all that much.

Switchman Sleeping

There’s plenty of blame to go around for bank liquidity problems. Certain banks and their regulators (including the Fed) somehow failed to anticipate that carrying large, unhedged positions in low-rate, long-term bonds might at some point alarm large depositors as interest rates rose. Those banks found themselves way short of funds needed to satisfy justifiably skittish account holders. A couple of banks were closed, but the FDIC agreed to insure all of their depositors. As the lender of last resort, the Fed provided banks with “credit facilities” to ease the liquidity crunch. In a matter of days, the fresh credit expanded the Fed’s balance sheet, offsetting months of “quantitative tightening” that had taken place since last June.

Of course, the Fed is no stranger to dozing at the switch. Historically, the central bank has failed to anticipate changes wrought by its own policy actions. Today’s inflation is a prime example. That kind of difficulty is to be expected given the “long and variable lags” in the effects of monetary policy on the economy. It makes activist policy all the more hazardous, leading to the kinds of “boom and bust” cycles described in Austrian business cycle theory.

Persistent Inflation

When the Fed went forward with the 25 basis point hike in the funds rate target in March, it was greeted with dismay by those still hopeful for a “soft landing”. In the Fed’s defense, one could say the continued effort to tighten policy is an attempt to make up for past sins, namely the Fed’s monetary profligacy during the pandemic.

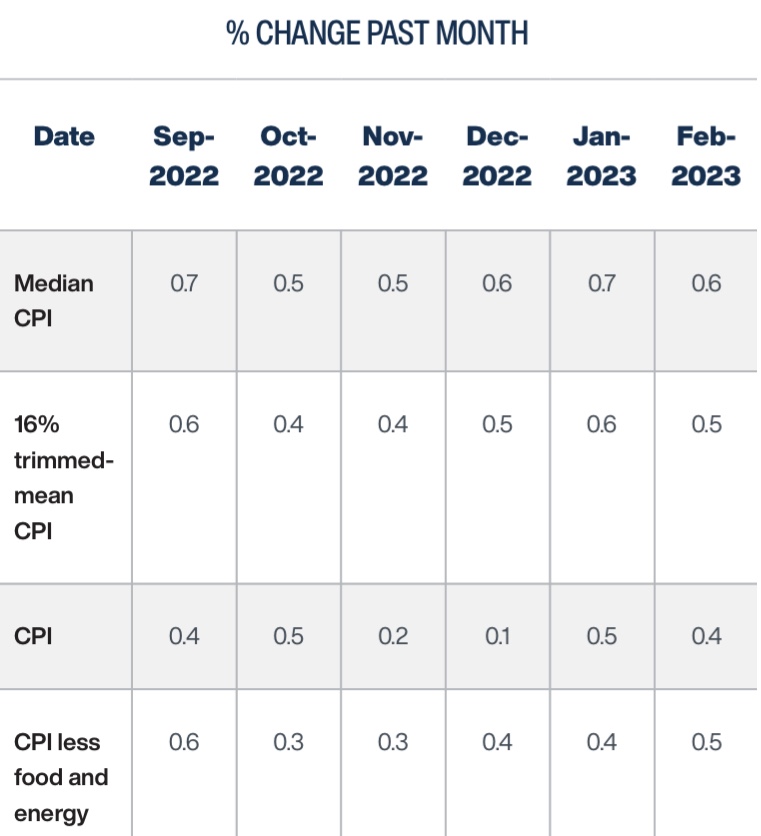

The Fed’s rationale for this latest rate hike was that inflation remains persistent. Here are four CPI measures from the Cleveland Fed, which show some recent tapering of price pressures. Perhaps “flattening” would be a better description, at least for the median CPI:

Those are 12-month changes, and just in case you’ve heard that month-to-month changes have tapered more sharply, that really wasn’t the case in January and February:

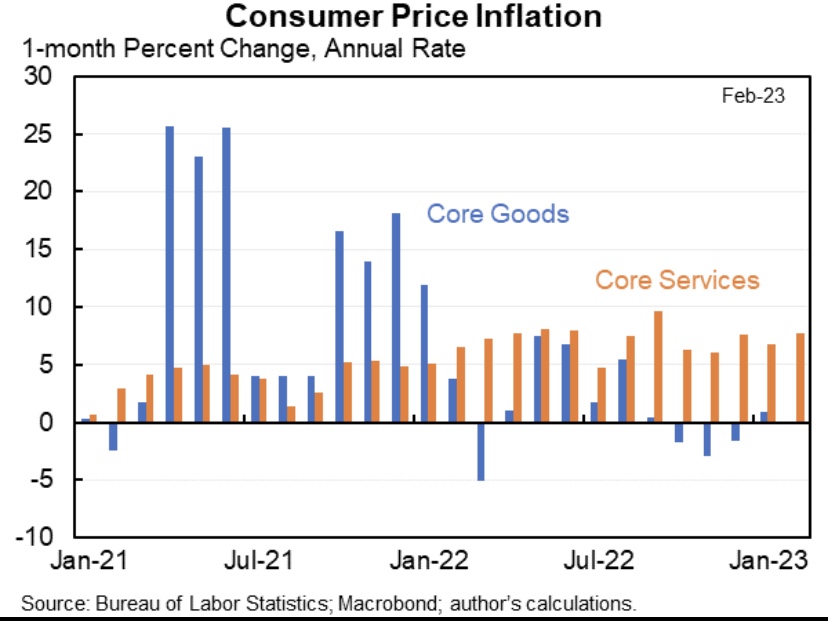

Jason Furman notedin a series of tweets that the prices of services are driving recent inflation, while goods prices have been flat:

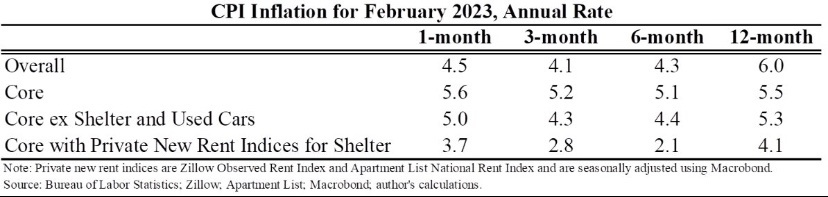

A compelling argument is that the shelter component of the CPI is overstating services inflation, and it’s weighted at more than one-third of the overall index. CPI shelter costs are known as “owner’s equivalent rent” (OER), which is based on a survey question of homeowners as to the rents they think they could command, and it is subject to a fairly long lag. Actual rent inflation has slowed sharply since last summer, so the shelter component is likely to relieve pressure on CPI inflation (and the Fed) in coming months. Nevertheless, Furman points out that CPI inflation over the past 3 -4 months was up even when housing is excluded. Substituting a private “new rent” measure of housing costs for OER would bring measured inflation in services closer the Fed’s comfort zone, however.

The Fed’s preferred measure of inflation, the deflator for personal consumption expenditures (PCE), uses a much lower weight on housing costs, though it might also overstate inflation within that component. Here’s another chart from the Cleveland Fed:

Inflation in the Core PCE deflator, which excludes food and energy prices, looks as if it’s “flattened” as well. This persistence is worrisome because inflation is difficult to stop once it becomes embedded in expectations. That’s exactly what the Fed says it’s trying to prevent.

Rate Targets and Money Growth

Targeting the federal funds rate (FFR) is the Fed’s primary operational method of conducting monetary policy. The FFR is the rate at which banks borrow from one another overnight to meet short-term needs for reserves. In order to achieve price stability, the Fed would do better to focus directly on controlling the money supply. Nevertheless, it has successfully engineered a decline in the money supply beginning last April, and recently the money supply posted year-over-year negative growth.

That doesn’t mean money growth has been “optimized” in any sense, but a slowdown in money growth was way overdue after the pandemic money creation binge. You might not like the way the Fed executed the reversal or its operating policy in general, and neither do I, but it did restrain money growth. In that sense, I applaud the Fed for exercising its independence, standing up to the Treasury rather than continuing to monetize yawning federal deficits. That’s encouraging, but at some point the Fed will reverse course and ease policy. We’ll probably hope in vain that the Fed can avoid sending us once again along the path of boom and bust cycles.

In effect, the FFR target is a price control with a dynamic element: the master fiddles with the target whenever economic conditions are deemed to suggest a change. This “controlled” rate has a strong influence on other short-term interest rates. The farther out one goes on the maturity spectrum, however, the weaker is the association between changes in the funds rate and other interest rates. The Fed doesn’t truly “control” those rates of most importance to consumers, corporate borrowers, government borrowers, and investors. It definitely influences those rates, but credit risk, business opportunities, and long-term expectations are often dominant.

The FOMC’s latest rate increase suggests its members don’t expect an immediate downturn in economic activity or a definitive near-term drop in inflation. The Committee may, however, be willing to pause for a period of several meeting cycles (every six weeks) to see whether the “long and variable lags” in the transmission of tighter monetary policy might begin to kick-in. As always, the FOMC’s next step will be “data dependent”, as Chairman Powell likes to say. In the meantime, the economic response to earlier tightening moves is likely to strengthen. Lenders are responding to the earlier rate hikes and reduced lending margins by curtailing credit and attempting to rebuild their own liquidity.

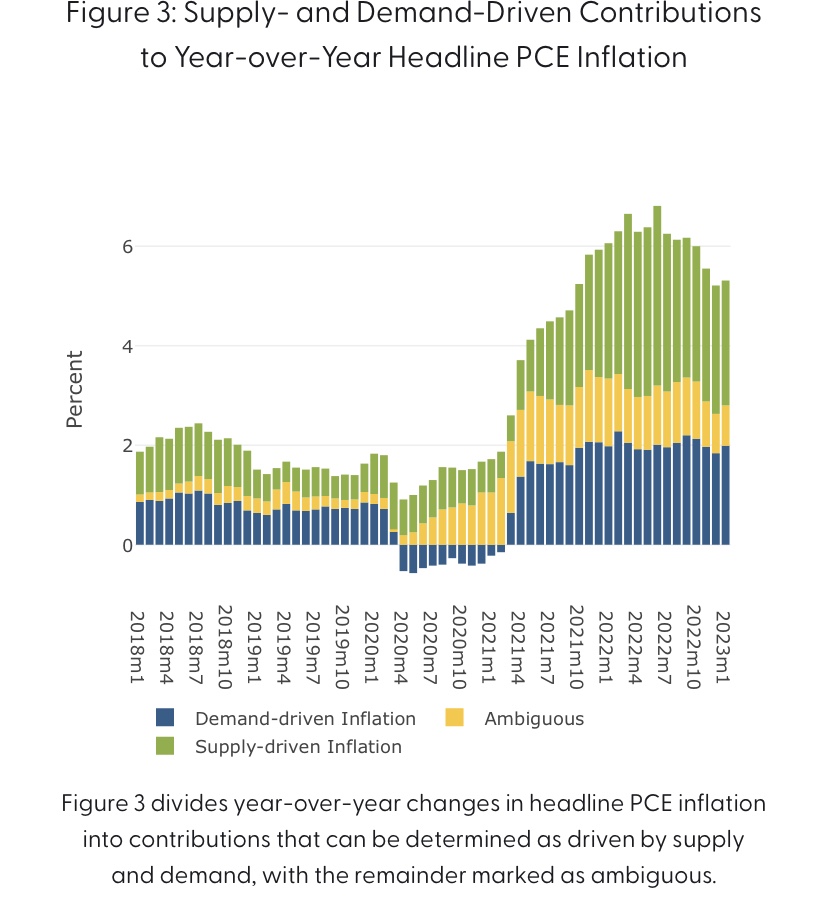

Is It Supply Or Demand?

There’s an ongoing debate about whether monetary policy is appropriate for fighting this episode of inflation. It’s true that monetary policy is ill-suited to addressing supply disruptions, though it can help to stem expectations that might cause supply-side price pressures to feed upon themselves (and prevent them from becoming demand-side pressures). However, profligate fiscal and monetary policy did much to create the current inflation, which is pressure on the demand-side. On that point, David Beckworth leaves little doubt as to where he stands:

“The real world is nominal. And nominal PCE was about $1.6 trillion above trend thru February. Unless one believes in immaculate above-trend spending, this huge surge could 𝙣𝙤𝙩 have happened without support from fiscal and monetary policy.”

In reality, this inflationary episode was borne of a mix of demand and supply-side pressures, and policy either caused or accommodated all of it. Nevertheless, it’s interesting to consider efforts to decompose these forces. This NBER paper attributed about 2/3 of inflation from December 2019 – June 2022 to the demand-side. Given the ongoing tenor of fiscal policy and the typical policy lags, it’s likely that the effects of fiscal and monetary stimulus have persisted well beyond that point. Here is a page from the San Francisco Fed’s site that gives an edge to supply-side factors, as reflected in this breakdown of the Fed’s favorite inflation gauge:

Of course, all of these decompositions are based on assumptions and are, at best, model-based. Nevertheless, to the extent that we still face supply constraints, they would impose limits to the Fed’s ability to manage inflation downward without a “hard landing”.

There’s also no doubt that supply side policies would reduce the kinds of price pressures we’re now experiencing. Regulation and restrictive energy policies under the Biden Administration have eroded productive capacity. These policies could be reversed if political leaders were serious about improving the nation’s economic health.

The Dark Runway Ahead

Will we have a recession? And when? There are no definite signs of an approaching downturn in the real economy just yet. Inventories of goods did account for more than half of the fourth quarter gain in GDP, which may now be discouraging production. There are layoffs in some critical industries such as tech, but we’ll have to see whether there is new evidence of overall weakness in next Friday’s employment report. Real wages have been a little down to flat over the past year, while consumer debt is climbing and real retail sales have trended slightly downward since last spring. Many firms will experience higher debt servicing costs going forward. So it’s not clear that the onset of recession is close at hand, but the odds are good that we’ll see a downturn as the year wears on, especially with credit increasingly scarce in the wake of the liquidity pinch at banks. But no one knows for sure, including the Fed.

It’s always hard to foresee dramatic turns in the economy and their timing. One day, way back in grad school, a professor of mine went on about how the Great Depression seemed to surprise people at the time. He felt they should have known it was coming, and he emphasized that housing had been in a downturn starting around 1926. Well, hindsight’s 20/20, and I’m not sure how timely and accurate economic reporting was at the time, but today it’s not any easier to call recessions in advance.

An Array of Weak Signals

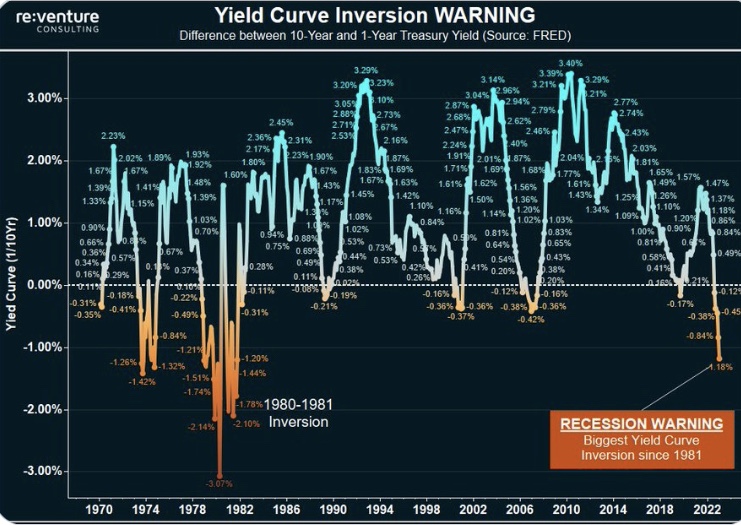

We’ve seen a downturn in housing this year, and for that and several other reasons many forecasters are predicting a recession in 2023. Consumers are depleting their savings and running up debt, and in November consumer confidence dropped for a fourth month in a row. In October, the Index of Leading Economic Indicators declined for an eighth straight month. A slump in business confidence has been underway for 12 months. Businesses are accumulating debt at much higher interest rates, and the earnings outlook (excluding energy) is bleak.

Buttressing that negative outlook is the inverted yield curve, which has been reliable (though not infallible) as a recession signal in the past. We now have a gap between the one-year Treasury yield and the 10-year Treasury yield of well over 100 basis points, which is as high as it’s been since 1981. That looks rather ominous.

The Fed’s Mission

Perhaps most importantly, the Federal Reserve has succeeded in reducing the money supply. That shift to tightening policy really only began in the late spring, however, and as Milton Friedman emphasized, the impact of money supply growth on the real economy is subject to “long and variable lags”. That could mean an economic slowdown or recession any time from now into 2024, but many analysts believe it will begin in the first half of 2023.

Denialists