Tags

Asset Sales, COLA, Defined Benefits, Defined Contributions, Entitlement Reform, Federal Borrowing, Medicare, Medicare Advantage, Pay-As-You-Go, Paygo, payroll taxes, Social Security, Social Security Trust Fund, Swedish Public Pensions

I’m always hearing fearful whines from several left-of-center retirees in my circle of my acquaintances: they say the GOP wants to cut their Social Security and Medicare benefits. That expression of angst was reprised as a talking point just before the midterm election, and some of these people actually believe it. Now, I’m as big a critic of these entitlement programs as anyone. They are in very poor financial shape and in dire need of reform. However, I know of no proposal for broad reductions in Social Security and Medicare benefits for now-eligible retirees. In fact, thus far President Trump has refused to consider substantive changes to these programs. And let’s not forget: it was President Obama who signed into law the budget agreement that ended spousal benefits for “file and suspend” Social Security claimants.

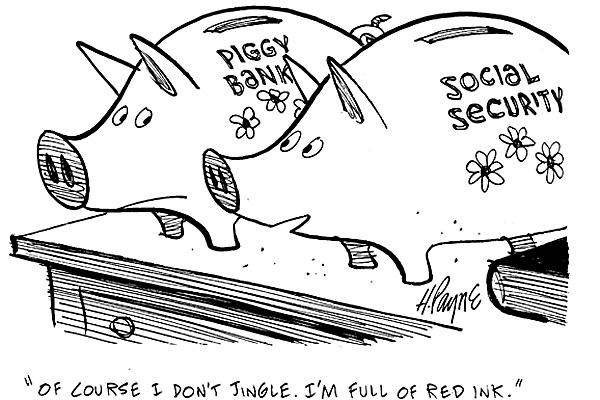

Both Social Security (SS) and Medicare are technically insolvent and reform of some kind should happen sooner rather than later. It does not matter that their respective trust funds still have positive balances — balances that the federal government owes to these programs. The trust fund balances are declining, and every dollar of decline is a dollar the government pays back to the programs with new borrowing! So the trust funds should give no comfort to anyone concerned with the health of either of these programs or federal finances.

Members of both houses of Congress have proposed steps to shore up SS and Medicare. A number of the bills are summarized and linked here. The range of policy changes put forward can be divided into several categories: tax hikes, deferred benefit cuts, and other, creative reforms. Future retirees will face lower benefits under many of these plans, but benefit cuts for current retirees are not on the table, except perhaps for expedient victims at high income levels.

There is some overlap in the kinds of proposals put forward by the two parties. One bipartisan proposal in 2016 called for reduced benefits for newly-eligible retired workers starting in 2022, among a number of other steps. Republicans have proposed other types of deferred benefit cuts. These include increasing the age of full eligibility for individuals reaching initial (and partial) eligibility in some future year. Generally, if these kinds of changes were to become law now, they would have their first effects on workers now in their mid-to-late fifties.

Another provision would switch the basis of the cost-of-living adjustment (COLA) to an index that more accurately reflects how consumers shift their purchases in response to price changes (see the last link). The COLA change would cause a small reduction in the annual adjustment for a typical retiree, but that is not a future benefit reduction: it is a reduction in the size of an annual benefit increase. However, one Republican proposal would eliminate the COLA entirely for high-income beneficiaries (see the last link) beginning in several years. A few other proposals, including the bipartisan one linked above, would switch to an index that would yield slightly more generous COLAs.

Democrats have favored increased payroll taxes on current high earners and higher taxes on the benefits of wealthy retirees. Republicans, on the other hand, seem more willing to entertain creative reforms. For example, one recent bill would have allowed eligible new parents to take benefits during a period of leave after childbirth, with a corresponding reduction in their retirement benefits (in present value terms) via increases in their retirement eligibility ages. That would have almost no impact on long-term solvency, however. Another proposal would have allowed retirees a choice to take a portion of any deferred retirement credits (for declining immediate benefits) as a lump sum. According to government actuaries, the structure of that plan had little impact on the system’s insolvency, but there are ways to present workers with attractive tradeoffs between immediate cash balances and future benefits that would reduce insolvency.

The important point is that enhanced choice can be in the best interests of both future retirees and long-term solvency. That might include private account balances with self-directed investment of contributions or a voluntary conversion to a defined contribution system, rather than the defined benefits we have now. The change to defined contributions appears to have worked well in Sweden, for example. And thus far, Republicans seem more amenable to these creative alternatives than Democrats.

As for Medicare, the only truth to the contention that the GOP, or anyone else, has designs on reducing the benefits of current retirees is confined the to the possibility of trimming benefits for the wealthy. The thrust of every proposal of which I am aware is for programmatic changes for future beneficiaries. This snippet from the Administration’s 2018 budget proposal is indicative:

“Traditional fee-for-service Medicare would always be an option available to current seniors, those near retirement, and future generations of beneficiaries. Fee-for-service Medicare, along with private plans providing the same level of health coverage, would compete for seniors’ business, just as Medicare Advantage does today. The new program, however, would also adopt the competitive structure of Medicare Part D, the prescription drug benefit program, to deliver savings for seniors in the form of lower monthly premium costs.”

There was a bogus claim last year that pay-as-you-go (Paygo) rules would force large reductions in Medicare spending, but Medicare is subject to cuts affecting only 4% of the budgeted amounts under the Paygo rules, and Congress waived the rules in any case. Privatization of Medicare has provoked shrieks from certain quarters, but that is merely the expansion of Medicare Advantage, which has been wildly popular among retirees.

Both Social Security and Medicare are in desperate need of reform, and while rethinking the fundamental structures of these programs is advisable, the immediate solutions offered tend toward reduced benefits for future retirees, later eligibility ages, and higher payroll taxes from current workers. The benefits of currently eligible retirees are generally “grandfathered” under these proposals, the exception being certain changes related to COLAs and Medicare benefits for high-income retirees. The tendency of politicians to rely on redistributive elements to enhance solvency is unfortunate, but with that qualification, my retiree friends need not worry so much about their benefits. I suspect at least some of them know that already.