Social Security wasn’t designed as a true saving vehicle for workers. Instead, SS has always been a pay-as-you-go system under which current benefits are funded by the payroll taxes levied on the current employed population. In fact, many Americans earn lousy effective returns on their tax “contributions” (also see here), though low-income individuals do much better than those near or above the median income. Worst of all, under pay-as-you-go, the system can collapse like a Ponzi scheme when the number of workers shrinks drastically relative to the retired population, leading to the kind of situation we face today.

Unfunded Obligations

Payroll tax revenue is no longer adequate to pay for current Social Security and Medicare benefits, and the problem is huge: according to the Penn-Wharton Budget Model, the unfunded obligations of Social Security (including old age, survivorship and disability) through 2095 have a present value of $18.1 trillion in constant 2024 dollars (using a discount rate of 4.4%). The comparable figure for Medicare Part A is $18.6 trillion. Together these amount to more than the current national debt.

Barring earlier reform, the Social Security Trust Fund is expected to be exhausted in 2033 (excluding the disability fund). At that point, a 20% reduction in benefits will be required by law. (More on the trust fund below.)

What To Do?

The most prominent reform proposals involve reduced benefits for wealthy beneficiaries, increased payroll taxes on high earners, and an increase in the retirement age. However, President-Elect Donald Trump shows no inclination to make any changes on his watch. This is unfortunate because the sooner the system’s insolvency is addressed, the less draconian the necessary reforms will be.

A neglected reform idea is for SS to be privatized. Many observers agree in principle that current workers could earn better returns over the long-term by investing funds in a conservative mix of equities and bonds. The transition to private accounts could be made voluntary, so that no one is forced to give up the benefits to which they’re “entitled”.

Takers would receive an initial deposit from the government in a tax-deferred account. For participating pre-retirees, ongoing FICA contributions (in whole or in part) would be deposited into their private accounts. They could purchase a private annuity with the balance at retirement if they choose. The income tax treatment of annuity payments or distributions could mimic the current tax treatment of SS benefits.

Given that the balance remaining at death would be heritable, some individuals might be willing to accept an initial deposit less than the actuarial PV of the future SS benefits they’ve accumulated to-date (discounted at an internal rate of return equating future benefits “earned” to-date and contributions to-date). I also believe many individuals would willingly accept a lower initial deposit because they would gain some control over investment direction. Such voluntarily-accepted reductions in initial deposits to personal accounts would mean the government’s issue of new debt would be smaller than the decrease in future benefit obligations.

Nevertheless, funding the accounts at the time of transition would necessitate a huge and immediate increase in federal debt. Market participants and political interests are likely to fear an impossible strain on the credit market. Perhaps the transition could be staged over time to make it less “shocking”, but that would complicate matters. In any case, heavy debt issuance is the rub that dissuades most observers from supporting privatization.

Fiscal Theory of Price Level

The fiscal theory of the price level (FTPL) implies that such a privatization might not be an insurmountable challenge after all, at least in terms of comparative dynamics. Much background on FTPL can be found at John Cochrane’s Grumpy Economist Substack.

FTPL asserts that fiscal policy can influence the price level due to a constraint on the market value of government debt. This market value must be in balance with the expected stream of future government primary surpluses. This is known as the government budget constraint.

The primary surplus excludes the government’s interest expense, a budget component that must be paid out of the primary surplus or else borrowed. Of course, the market value of government debt incorporates the discounted value of future interest payments.

This budget constraint must be true in an expectational sense. That is, the market must be convinced that future surpluses will be adequate to pay all future obligations associated with the debt. Otherwise, the value of the debt must change.

Should a spending initiative require the government to issue new debt with no credible offset in terms of future surpluses, the market value of the debt must decline. That means interest rates and/or the price level must rise. If interest rates are fixed by the monetary authority (the Fed) then only prices will rise.

A SS Private Option Under FTPL

But what about FTPL in the context of entitlement reform, specifically a privatization of Social Security? Suppose the government issues debt and then deposits the proceeds into personal accounts to fund future benefits. Future government surpluses (deficits) would increase (decrease) by the reduction in future SS benefit payments.

This improved budgetary position should be highly credible to financial markets, despite the fact that benefits are not and never have been guaranteed. If it is credible to markets, the new debt would not raise prices, nor would it be valued differently than existing debt. There need not be any change in interest rates.

But Thin Ice

There are risks, of course. It might be too much to hope that other federal spending can be restrained. That kind of failure would subvert the rationale for any budgetary reform. A variety of other crises and economic shocks are also possible. Those could disrupt markets and jeopardize budget discipline as well. Given a severe shock, interest expense could more readily explode given the massive debt issuance required by the reform discussed here. So there are big risks, but one might ask whether they could turn out to be more disastrous in the absence of reform.

Other Details

The private account “offers” extended to workers or beneficiaries relative to the actuarial PVs of their future benefits would be controversial. Different offer percentages (discounts) could be tested to guage uptake.

Another issue: provisions would have to be made for individuals in “unbanked” households, estimated by the FDIC to be about 4.2% of all U.S. households in 2023. Voluntary uptake of the “offer” is likely to be lower among the unbanked and among those having less confidence in their ability to make financial decisions. However, even a simplified set of choices might be superior to the returns under today’s SS, even for low-income workers, not to mention the very real threat of future reductions in benefits. Furthermore, financial institutions might compete for new accounts in part by offering some level of financial education for new clients.

A similar reform could be applied to Medicare, which like SS is also technically insolvent. Participating beneficiaries could receive some proportion of expected future benefits in a private account, which they could use to pay for private or public health insurance coverage or medical expenses. From a budget perspective, the increase in federal debt would be balanced against the reduction in future Medicare benefits, which would constitute a credible increase (decrease) in future surpluses (deficits).

Credibility

But again, how credible would markets find the decrease in benefit obligations? Direct reductions in future entitlements should be convincing, though politicians are likely to find plenty of other ways to use the savings.

On the other hand, markets already give some weight to the possibility of future benefit cuts (or other policies that would reduce SS shortfalls). So it’s likely that markets will give the reform’s favorable budget implications significant but only “incremental credit”.

Another possible complication is that the market, prior to execution of the reform, might discount the uptake by workers and current retirees. This would necessitate better offers to improve uptake and more debt issuance for a given reduction in future obligations. Skepticism along these lines might worsen implications for the price level and interest rates.

The Trust Fund

Finally, what about the SS Trust Fund? Can it play in role in the reform discussed above? The answer depends on how the trust fund fits into the federal government’s budgetary position.

The trust fund holds as assets only non-marketable Treasury securities acquired in the past when SS contributions exceeded benefit payments. The excess payroll tax revenue was placed in the trust fund, which in turn lent the funds to the federal government to help meet other budgetary needs. Hence the bond holdings.

In terms of the government’s fiscal position, the money has already been pissed away, as it were. The bonds in the trust fund do not represent a pot of money. As noted above, with our age demographics now reversed, payroll taxes no longer meet benefits. Thus, bonds in the trust fund must be redeemed to pay all SS obligations. The Treasury must pay off the bonds via general revenue or by borrowing additional amounts from the public.

Post-reform, if continuing deficits are the order of the day, redeeming bonds in the trust fund would do nothing to improve the government’s fiscal position. If the trust fund “cashes them in” to help meet benefit payments, the federal government must borrow to raise that cash. In other words, the bonds in the trust fund would be more or less superfluous.

But what if the federal budget swings into a surplus position post-reform? In that case, federal tax revenue would cover the redemption of at least some of the bonds held by the trust fund. SS beneficiaries would then have a meaningful claim on federal taxpayers through the trust fund and the government’s surplus position, which would reduce the new federal debt required by the reform.

Conclusion

The Social Security and Medicare systems are in desperate need reform, but there is little momentum for any such undertaking. Meanwhile, exhaustion of the SS and Medicare trust funds creeps ever closer, along with required benefit cuts. All of the reform options would be painful in one way or another. A voluntary privatization would require a huge makeover, but it might be the least painful option of all. Current workers and beneficiaries would not be compelled to make choices they found inferior. Moreover, the new debt necessary to pay for the reforms would be matched by a reduction in future government obligations. The fiscal theory of the price level implies that the reform would not be inflationary and need not depress the value of Treasury bonds, provided the reform is accompanied by long-term budget discipline.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

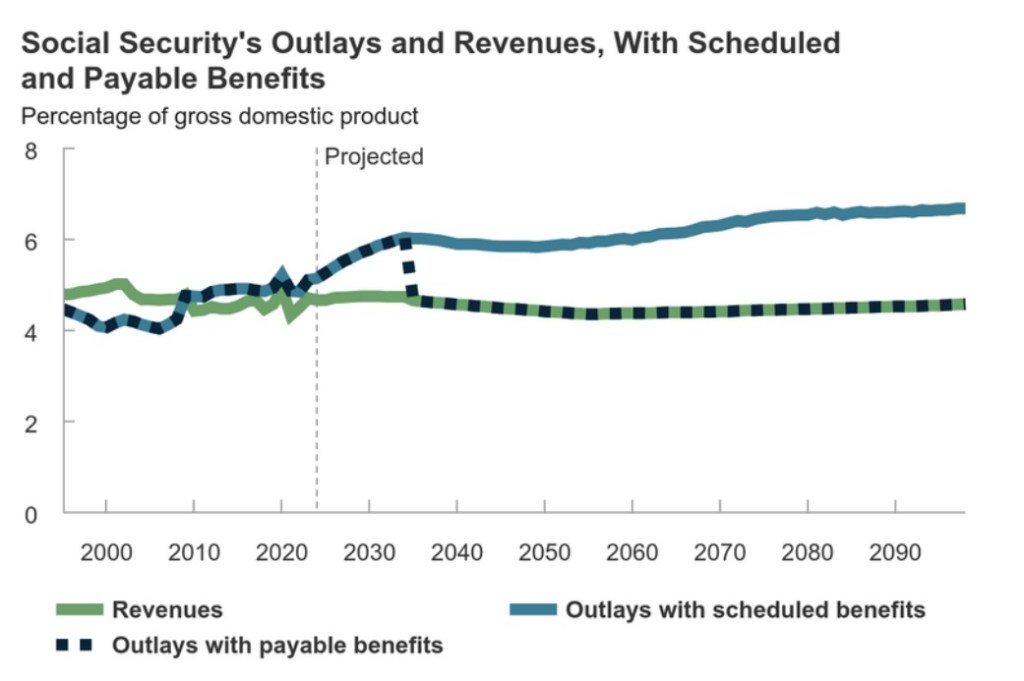

Note: the chart at the top of this post was produced by the Congressional Budget Office and appears in this publication.

Government budget negotiations never fail to frustrate anyone of a small-government persuasion. We have a huge, ongoing federal budget deficit. Spending’s gone bat-shit out of control over the past several years and too few in Congress are willing to do anything about it. Democrats would rather see politically-targeted tax increases. While some Republicans advocate spending cuts, the focus is almost entirely on discretionary spending. Meanwhile, the entitlement state is off the table, including Social Security reform.

Fiscal Indiscretion

Sadly, non-discretionary outlays (entitlements) today make a much larger contribution to the deficit than discretionary spending. That includes the programs like Social Security (SS) and Medicare, in which spending levels are programmatic and not subject to annual appropriations by Congress. When these programs were instituted there were a large number of workers relative to retirees, so tax contributions exceeded benefit levels for many decades. The revenue excesses were placed into “trust funds” and invested in Treasury debt. In other words, surpluses under non-discretionary SS and Medicare programs were used to finance discretionary spending!

The aging of Baby Boomers ultimately led to a reversal in the condition of the trust funds. Fewer workers relative to retirees meant that annual payroll tax collections were not adequate to cover annual benefits, and that meant drawing down the trust funds. Current projections by the system trustees call for the SS Trust Fund to be exhausted by 2035. Once that occurs, benefits will automatically be reduced by roughly 20% unless Congress acts to shore up the system before then.

A Few Proposals

I’ve written about the need for SS reform on several occasions (though the first article at that link is not germane here). It seems imperative for Congress and the President to address these shortfalls. By all appearances, however, many Republicans have put the issue aside. For his part, Joe Biden has apparently accepted the prospect of an automatic reduction in benefits in 2035, or at least he’s willing to kick that can down the road. He has, however, endorsed taxes on high earners to fund Medicare. Senator John Kennedy (R-LA) suggests raising the retirement age, or at least raise the minimum age at which one may claim benefits (now 62). Senators Bill Cassidy (R-La.) and Angus King (I-Maine) were working on a compromise that would create an investment fund to fortify the system, but the specifics are unclear, as well as how much that would accomplish.

Meanwhile, Senator Bernie Sanders (S-VT) proposes to expand SS benefits by $2,400 a year and add funding by extending payroll taxes to earners above the current limit of $160,000. Senator Joe Manchin (D-WV) has endorsed the latter as a “quick fix”.

There is also at least oneproposal in Congress to end the practice of taxing a portion of SS benefits as income. I have trouble believing it will gain wide support, despite the clear double-taxation involved.

Then there are always discussions of reducing benefits at higher income levels or even means-testing benefits. In fact, it would be interesting to know what proportion of current benefits actually function as social insurance, as opposed to a universal entitlement. The answer, at least, could serve as a baseline for more fundamental reforms, including changes in the structure of payroll taxes, voluntary lump-sum payouts, and private accounts.

More Radical Views

There are a few prominent voices who claim that SS is sustainable in its current form, but perhaps with a few “no big deal” tax increases. Oh, that’s only about a $1 trillion “deal”, at least for both Medicare and SS. More offensive still are the scare tactics used by opponents of SS reform any time the subject comes up. I’m not aware of any serious reform proposal made over the past two decades that would have affected the benefits of anyone over the age of 55, and certainly no one then-eligible for benefits. Yet that charge is always made: they want to cut your SS benefits! The Democrats made that claim against George W. Bush, torpedoing what might have been a great accomplishment for all. And now, apparently Donald Trump is willing to use such accusations to damage any rival who has ever mentioned reform, including Mike Pence. Will you please cut the crap?

The System

The thing to remember about SS is that it is currently structured as a pay-as-you-go (PAYGO) system, despite the fact that benefits are defined like many creaky private pensions of old. SS benefits in each period are paid out of current “contributions” (i.e., FICO payroll taxes) plus redemptions of government bonds held in the Trust Fund. Contributions today are not “invested” anywhere because they are not enough to pay for current benefits under PAYGO.

The Trust Fund was accumulated during the years when favorable demographics led to greater FICO contributions than benefit payouts. The excess revenue was “invested” in Treasury bonds, which meant it was used to fund deficits in the general budget. It’s been about 15 years since the Trust Fund entered a “draw-down” status, and again, it will be exhausted by 2035.

SSA Says It’s a Good Deal

A participant’s expected “rate of return” on lifetime payroll tax payments depends on several things: lifetime earnings, age at which benefits are first claimed, life expectancy at that time, marital status, relative earning levels within two-earner couples, and the “full retirement age” for the individual’s birth year. Payroll tax payments, by the way, include the employer’s share because that is one of the terms of a hire. A high rate of return is not the same as a high level of benefits, however. In fact, relative to career income, SS has a great deal of progressivity in terms of rates of return, but not much in terms of benefit levels.

The Social Security Administration (SSA) has calculated illustrative real internal rates of return (IRR) for many categories of earners given certain assumptions. (An IRR is a discount rate that equalizes the present value (PV) of a stream of payments and the PV of a stream of payoffs.) The SSA’s most recent update of this exercise was in April 2022. The report references Old Age, Survivors, and Disability Insurance (OASDI), but the focus is exclusively on seniors.

Three basic scenarios were considered: 1) current law, as scheduled, despite its unsustainability; 2) a payroll tax increase from 12.4% (not including the Medicare tax) to 15.96% starting in 2035, when the Trust Fund is exhausted; and 3) a reduction in benefits of 22% starting in 2035.

The authors of the report concludethat “… the real value of OASDI benefits is extraordinarily high.” This theme has been echoed by several other writers, such as here and here. This conclusion is based on a comparison to returns earned by investments that SSA judges to have comparably low risk.

I note here that I’ve made assertions in the past about relative SS returns based on nominal benefits, rather than inflation-adjusted values. Those comparisons to private returns might have seemed drastic because they were expressed in terms of hypothetical future nominal values at the point of retirement. The gaps are not as large in real terms or if we consider SS returns broadly to include those accruing to low career earners. Medium and high earners tend to earn lower hypothetical returns from SS.

A Mixed Bag

SSA’s calculated IRRs are highest for one-earner couples followed by two-earner couples. Single males do relatively poorly due to their higher mortality rates. Low earners do very well relative to higher earners. Earlier birth years are associated with higher IRRs, but these are not as impressive for cohorts who have not yet claimed benefits. The ranges of birth years provided in the report make this a little imprecise, but I’ll focus on those born in 1955 and later.

Of course the returns are highest under the current law hypothetical than for the scenarios involving a benefit reduction or a payroll tax hike. The current law IRRs can be viewed as baselines for other calculations, but otherwise they are irrelevant. The system is technically insolvent and the scheduled benefits under current law can’t be maintained beyond 2034 without steps to generate more revenue or cut benefits. Those steps will reduce IRRs earned by hypothetical SS “assets” whether they take the form of higher payroll taxes, lower benefits, a greater full retirement age, or other measures.

The tax hike doesn’t have much impact on the IRRs of near-term retirees. It falls instead on younger cohorts with some years of employment (and payroll tax payments) remaining. The effect of a cut in benefits is spread more evenly across age cohorts and the reductions in IRRs is somewhat larger.

With higher payroll taxes after 2034, the average IRRs for birth years of 1955+ range from about 0.5% up to about 6.25%. The returns for single females and two-earner couples are roughly similar and fall between those for single males on the low end and one-earner couples on the high end. In all cases, low earners have much higher IRRs than others.

The reduction in benefits produces returns for the 1955+ age cohorts averaging small, negative values for high-earning single men up to 5.5% to 6% for low-earning, one-earner couples.

But On the Whole…

The IRR values reported by SSA are quite variable across cohorts. Individuals or couples with low earnings can usually expect to “earn” real IRRs on their contributions of better than 3% (and above 5% in a few cases). Medium earners can expect real returns from 1% to 3% (and in some cases above 4%). Many of the returns are quite good for a safe “asset”, but not for high earners.

Again, SSA states that these are real returns, though they provide no detail on the ways in which they adjust the components used in their IRR formula to arrive at real returns. Granting the benefit of the doubt, we saw persistently negative real returns on a range of safe assets in the not-very-distant past, so the IRRs are respectable by comparison.

Qualifications

There are many assumptions in the SSA’s analysis that might be construed as drastic simplifications, such as no divorce and remarriage, uniform career duration, and no relationship between earnings and mortality. But it’s easy to be picky. Many of the assumptions discernible from the report seem to be reasonable simplifications in what could otherwise be an unruly analysis. Nonetheless, there are a few assumptions that I believe bias the IRRs upward (and perhaps a few in the other direction).

In fact, SSA is remarkably non-transparent in their explanation of the details. Repeated checking of SSA’s document for clear answers is mostly futile. Be that as it may, I’m forced to give SSA the benefit of the doubt in several respects. One is the reinvestment of cumulative remaining contributions at the IRR throughout the earning career and retirement. A detailed formula with all components and time subscripts would have been nice.

… And Major Doubts

As to my misgivings, first, the IRRs reported by SSA are based on earners who all reach the age of 65. However, roughly 14% – 15% of individuals who live to be of working age die before they reach the age of 65. Most of those deaths occur in the latter part of that range, after many years of contributions and hypothetical compounding. That means the dollar impact of contributions forfeited at death before age 65 is probably larger than the unweighted share of individuals. These individuals pay-in but receive no retirement benefit in SSA’s IRR framework, although some receive disability benefits for a period of time prior to death. It wouldn’t bother my conscience to knock off at least a tenth of the quoted returns for this consideration alone.

A second major concern surrounds the method of calculating benefits and discounted benefits. SSA assumes that benefits continue for the expected life of the claimant as of age 65. If life expectancy is 19 years at age 65, then “expected” benefits are a flat stream of benefit payments for 19 years. Discounting each payment back to age 65 at the IRR yields one side of the present value equality. This constant cash flow (CCF) treatment is likely to overstate the present value of benefits. Instead of CCFs, each payment should be weighted by the probability that the claimant will be alive to receive it with a limit at some advanced age like 100. CCF overcounts present values up to the expected life, but it undercounts present values beyond the expected life because the assumed CCF benefits then are zero!! Weighting benefit payments by the probability of survival to each age produces continuing additions to the PV, but increasing mortality and decaying discount factors become quite substantial beyond expected life, leading to relatively minor additions to PV over that range. The upshot is that the CCFs employed by SSA overstate PVs by front-loading all benefits earlier in retirement. For a given PV of contributions, an overstated PV of benefits requires a higher (and overstated) IRR to restore the PV equality, and this might be a substantial source of upward bias in SSA’s calculations.

Third, when comparing an SS “asset” to private returns, a big difference is that private balances remaining at death become assets of the earner’s estate. Meanwhile, a single beneficiary forfeits their SS benefits at death (except for a small death benefit), while a surviving spouse having lower benefits receives ongoing payments of the decedent’s benefits for life. This consideration, however, in and of itself, means that private plans have a substantial advantage: the “expected” residual at death can be “optimized” at zero or some higher balance, depending on the strength of the earner’s bequest motive.

Finally, in a footnote, the SSA report notes that their treatment of income taxes on Social Security benefits for claimants with higher incomes might bias some of the IRRs upward. That seems quite likely.

It would be difficult to recast SSA’s report based on adjustments for all of these qualifications. However, it’s likely that the IRRs in the SSA report are sharply overstated. That means many more beneficiaries with medium and higher earnings records would have returns in the 0% to 2% range, with more IRRs in the negative range for singles. Low earners, however, might still get returns in a range of 3% to 5%.

The SSA analysis attempts to demonstrate some limits to the risks faced by participants, given the scenarios involving a payroll tax increase or a benefits reduction in 2035. Nevertheless, there are additional political risks to the returns of certain classes of current and future retirees. For example, payroll taxes could be made much more progressive, benefits could be made subject to means testing, or indexing of benefits could be reduced. In fact, there are additional demographic risks that might confront retirees several decades ahead. Continued declines in fertility could further undermine the system’s solvency, requiring more drastic steps to shore up the system. As a hypothetical asset, by no means is SS “risk-free”.

Better Returns

Now let’s consider returns earned by private assets, which represent investments in productive capital. For stocks, these include the sum of all dividends and capital gains (growth in value). For compounding purposes, we assume that all returns are reinvested until retirement. Remember that private returns are much less variable over spans of decades than over durations of a few years. Over the course of 40 year spans (SSA’s career assumption), private returns have been fairly stable historically, and have been high enough to cushion investors from setbacks. Here is Seeking Alpha on annualized returns on the basket of stocks in the S&P 500:

“… the return on the S&P 500 since the beginning of valuation in 1928, is 10.22%, whereas the inflation-adjusted return on the market since that time is 7.01%…”

That real return would generate benefits far in excess of SS for most participants, but it’s not an adequate historical perspective on market performance. A more complete picture of real returns on the S&P, though one that is still potentially flawed, emerges from this calculator, which relies on data from Robert Shiller. The returns extend back to 1871, but the index as we know it today has existed only since 1957. The earlier returns tend to be lower, so these values may be biased:

Real stock market returns over rolling 40-year time spans varied considerably over this longer period. Still, those kind of stock returns would be superior to the IRRs in the SSA report going forward in all but a few cases (and then only for low and very low earners).

Most workers facing a choice between investing at these rates for 40 years, with market risk, and accepting standard SS benefits, uncertain as they are, couldn’t be blamed for choosing stocks. In fact, if we think of contributions to either type of plan as compounding to a hypothetical sum at retirement, the stock investments would produce a “pot of gold” several times greater in magnitude than SS.

However, we still don’t have a fair comparison because workers choosing a stock plan would essentially engage in a kind of dollar-cost averaging over 40 years, meaning that investments would be made in relatively small amounts over time, rather than investing a lump-sum at the beginning. This helps to smooth returns because purchases are made throughout the range of market prices over time, but it also means that returns tend to be lower than the 40-year rolling returns shown above. That’s because the average contribution is invested for only half the time.

To be very conservative, if we assume that real stock returns average between 5% and 6% annually, $1 invested every year would grow to between $131 – $155 after 40 years in constant dollars. At returns of 1% to 2% from SS, which I believe are typical of the IRRs for many medium earners, the cumulative “pot” would grow to $49 – $60. Assuming that the tax treatment of the stock plan was the same as contributions and benefits under SS, the stock plan almost triples your money.

Dealing With the Transition

Privatization covers a range of possible alternatives, all of which would require federal borrowing to pay transition costs. Unfortunately, the Achilles heel in all this is that now is a bad time to propose more federal borrowing, even if it has clear long-term benefits to future retirees.

Todd Henderson in the Wall Street Journal suggests a seeding of capital provided by government at birth along with an insurance program to smooth returns. Another idea is to offer an inducement to delay retirement claims by allowing at least a portion of future benefits to be taken as a lump sum. If retirees can privately invest at a more advantageous return, they might be willing to accept a substantial discount on the actuarial value of their benefits.

In fact, there is evidence that a majority of participants seem to prefer distributions of lump sums because they don’t value their future benefits at anything like that suggested by the SSA analysis. In fact, many participants would defer retirement by 1 – 2 years given a lump sum payment. Discounts and/or delayed claims would reduce the ultimate funding shortfall, but it would require substantial federal borrowing up front.

Additional federal borrowing would also be required under a private option for investing one’s own contributions for future dispersal. The impact of this change on the system’s long-term imbalances would depend on the share of earners willing to opt-out of the traditional SS program in whole or in part. More opt-outs would mean a smaller long-term obligations for the traditional system, but it would be hampered by a costly transition over a number of years. Starting from today’s PAYGO system, someone still has to pay the benefits of current retirees. This would almost certainly mean federal borrowing. Spreading the transition over a lengthy period of time would reduce the impact on credit markets, but the borrowing would still be substantial.

For example, perhaps earners under 35 years of age could begin opting out of a portion or all of the traditional program at their discretion, investing contributions for their own future use. Thus, only a small portion of contributions would be diverted in the beginning, and amounts diverted would contribute to the nation’s available pool of saving, helping to keep borrowing costs in check. By the time these younger earners reach retirement age, nearly all of today’s retirees will have passed on. Ultimately, the average retiree will benefit from higher returns than under the traditional program, but since they won’t be (fully) paying the benefits of current or near-term retirees, the public must come to grips with the bad promises of the past and fund those obligations in some other way: reduced benefits, taxes, or borrowing.

Another objection to privatization is financial risk, particularly for lower-income beneficiaries. Limiting opt-outs to younger earners with adequate time for growth would mitigate this risk, along with a reversion to the traditional program after age 45, for example. Some have proposed limiting opt-outs to higher earners. Bear in mind, however, that the financial risk of private accounts should be weighed against the political and demographic risk already inherent in the existing system.

One more possibility for bridging the transition to private, individually-controlled accounts is to sell federal assets. I have discussed this before in the context of funding a universal basic income (which I oppose). The proceeds of such sales could be used to pay the benefits of current and near-term retirees so as to allow the opt-out for younger workers. Or it could be used to pay off federal debt accumulated in the process. The asset sales would have to proceed at a careful and deliberate pace, perhaps stretching over several decades, but those sales could include everything from the huge number of unoccupied federal buildings to vast tracts of public lands in the west, student loans, oil and gas reserves, and airports and infrastructure such as interstate highways and bridges. Of course, these assets would be more productive in private hands anyway.

The Likely Outcome

Will any such privatization plan ever see the light of day? Probably not, and it’s hard to guess when anything will be done in Washington to address the insolvency we already face. Instead, we’ll see some combination of higher payroll taxes, higher payroll taxes on high earners through graduated payroll tax rates or by lifting the earnings cap, reduced benefits on further retirees, limits on COLAs to low career earners, and means-tested benefits. Some have mentioned funding Social Security shortfalls with income taxes. All of these proposals, with the exception of automatic benefit cuts in 2035, would require acts of Congress.

The Social Security and Medicare trust funds are starting to shrink, but as they shrink something else expands in tandem, roughly dollar-for-dollar: government debt. There is a widespread misconceptions about these entitlement programs and their trust funds. Many seem to think the trust funds are like “pots of gold” that will allow the government to meet its mandatory obligations to beneficiaries. But, in fact, the government will have to borrow the exact amounts of any “assets” that are “cashed out” of the trust funds, barring other reforms or legislative solutions. So how does that work? And why did I put the words “assets” and “cashed out” in quote marks?

The Trust Funds

First, I should note that there are two Social Security trust funds: one for old age and survivorship income (OASI) and one for disability income (DI). Occasionally, for summary purposes, the accounts for these funds are combined in presentations. There are also two Medicare trust funds: one for hospitalization insurance (HI – Part A) and one for Supplementary Medical Insurance (SMI – Parts B and D). The first three of these trust funds are represented in the chart at the top of this post, which is from the Summary of the 2021 Annual Reports by the Boards of Trustees. It plots a measure of financial adequacy: the ratio of trust fund assets at the start of each year to the annual cost. The funds are all projected to be depleted, HI and OASI much sooner than DI.

Fund Accumulation

The first step in understanding the trust funds requires a clearing up of another misconception: the payroll taxes that workers “contribute” to these systems are not invested specifically for each of those workers. These programs are strictly “pay-as-you-go”, meaning that the payroll taxes (and premiums in the case of Medicare) paid this year by you and/or your employer are generally distributed directly to current beneficiaries.

Back when demographics of the American population were more favorable for these programs, with a larger number of workers relative to retirees, payroll taxes (and premiums) exceeded benefits. The excess was essentially loaned by these programs to the U.S. Treasury to cover other forms of spending. So the trust funds accumulated U.S. Treasury IOUs for many years, and the Treasury pays interest to the trust funds on that debt. On the upside, that meant the Treasury had to borrow less from the public to cover its deficits during those years. So the government spent the excess payroll tax proceeds and wrote IOUs to the trust funds.

Draining the Funds

The demographic profile of the population is no longer favorable to these entitlement programs. The number of retirees has increased so that benefit levels have grown more quickly than program revenue. Benefits now exceed the payroll taxes and premiums collected, so the trust funds must be drawn down. Current estimates are that the Social Security Trust Fund will be depleted in 2034, while the Medicare Trust Fund will last only to 2026. These dates are reflected in the chart above. It is the mechanics of these draw-downs that get to the heart of the first “pot of gold” misconception cited above.

To pay for the excess of benefits over revenue collected, the trust funds must cash-in the IOUs issued to them by the Treasury. And where does the Treasury get the cash? It will almost certainly be borrowed from the public, but the government could hike other forms of taxes or reduce other forms of spending. So, while the earlier accumulation of trust fund assets meant less federal borrowing, the divestment of those assets generally means more federal borrowing and growth in federal debt held by the public.

Given these facts, can you spot the misconception in this quote from Fiscal Tiger? It’s easy to miss:

“In the cases of Social Security, Medicare, and Medicaid, payroll taxes provide some revenue. Social Security also has trust funds that cover some of the program costs. However, when the government is short on funds for these programs after getting the revenue from taxes and trust funds, it must borrow money, which contributes to the deficit.”

This kind of statement is all too common. The fact is the government has to borrow in order to pay off the IOUs as the trust funds are drawn down, roughly dollar-for-dollar.

A second mistake in the quote above is that federal borrowing to pay excess benefits after the trust funds are fully depleted is not really assured. At that time, the Anti-deficiency Act prohibits further payments of benefits in excess of payroll taxes (and premiums), and there is no authority allowing the trust funds to borrow from the general fund of the Treasury. Either benefits must be reduced, payroll taxes increased, premiums hiked (for Medicare), or more radical reforms will be necessary, any of which would require congressional action. In the case of Social Security (combining OASI and DI), the projected growth of “excess benefits” is such that the future, cumulative shortfall represents 25% of projected benefits!

Again, the mandatory entitlement spending programs are technically insolvent. Charles Blahous discusses the implications of closing the funding gap, both in terms of payroll tax increases or benefit cuts, either of which will be extremely unpopular:

“How likely is it that lawmakers would immediately cut benefits by 25% for everyone, rich and poor, retiring next year and beyond? More likely, lawmakers would phase in reforms gradually, necessitating much larger eventual benefit changes for those affected—perhaps 30% or 40%. And if we want to spare lower-income individuals from reductions, they’d need to be still greater for everyone else.”

It should be noted that Medicaid is also a budget drain, though the cost is shared with state governments.

Discretionary vs. Mandatory Budgets

When it comes to federal budget controversies, discretionary budget proposals receive most of the focus. The federal deficit reached unprecedented levels in 2020 and 2021 as pandemic support measures led to huge increases in spending. Even this year (2022), the projected deficit exceeds the 2019 level by over $160 billion. Joe Biden would like to spend much more, of course, though the loss of proceeds from his student loan forgiveness giveaway does not even appear in the Administration’s budget proposal. Biden proposes to pay for the spending with a corporate tax hike and a minimum tax on very high earners, including an unprecedented tax on unrealized capital gains. Those measures would be disappointing in terms of revenue collection, and they are probably worse for the economy and society than bigger deficits. None of that is likely to pass Congress, but we’ll still be running huge deficits indefinitely..

In a further complication, at this point no one really believes that the federal government will ever pay off the mounting public debt. More likely is that the Federal Reserve will make further waves of monetization, buying government bonds in exchange for monetary assets. (Of course, money is also government debt.) The conviction that ever increasing debt levels are permanent is what leads to fiscal inflation, which taxes the public by devaluing the public debt, including (or especially) monetary assets. The insolvency of the trust funds is contributing to this process and its impact is growing..

Again, the budget discussions we typically hear involve discretionary components of the federal budget. Mandatory outlays like Social Security, Medicare, and Medicaid are nearly three times larger. Here is a good primer on the mandatory spending components of the federal budget (which includes interest costs). Blahous notes elsewhere that the funding shortfall in these programs will ultimately dwarf discretionary sources of budgetary imbalance. The deficit will come to be dominated by the borrowing required to fund mandatory programs, along with the burgeoning cost of interest payments on the public debt, which could reach nearly 50% of federal revenues by 2050.

Conclusion

It would be less painful to address these funding shortfalls in mandatory programs immediately than to continue to ignore them. That would enable a more gradual approach to changes in benefits, payroll taxes, and premiums. Politicians would rather not discuss it, however. Any discussion of reforms will be controversial, but it’s only going to get worse over time.

Political incentives being what they are, current workers (future claimants) are likely to bear the brunt of any benefit cuts, rather than retirees already enrolled. Payroll tax hikes are perhaps a harder sell because they are more immediate than trimming benefits for future retirees. Other reforms like self-directed Social Security contributions would create better tradeoffs by allowing investment of contributions at competitive (but more risky) returns. Medicare has premiums as an extra lever, but there are other possible reforms.

Again, the time to act is now, but don’t expect it to happen until the crisis is upon us. By then, our opportunities will have become more hemmed in, and something bad is more likely to be promulgated in the rush to save the day.

A 67-year-old friend told me he won’t file for Social Security (SS) benefits until he turns 70 because “it will pay off as long as I live to at least 81”. Okay, so benefit levels increase by about 8% for each year they’re deferred after your “full retirement age” (probably about 66 for him), and he has no doubt he’ll live more than the extra 11 years. Yes, his decision will “pay off” in a “break-even” sense if he lives that long: he’ll collect more incremental dollars of benefits beyond his 70th birthday than he’ll lose during the three-year deferral (but actually, he’d have to live till he’s 81.5 to break even). But that does not mean his decision is “optimal”.

Good things come to those who wait. I’ll simplify here just a bit, but let’s say an 8% increase in benefits is uniform for every year deferred beyond age 62. (It’s actually a bit more than that after full retirement age, but it’s less than 8% in some years prior to full retirement age.) 8% is a very good, “safe” return, assuming you don’t mind putting your faith in the government to make good.

The Reaper approaches: Unlike your personal savings, SS benefits end at death (a surviving spouse would continue to receive the higher of your respective benefit payments). That means the “safe” 8% return is eroded by diminishing life expectancy with each passing year. For example, average life expectancy at age 62 is 25.4 years, but it falls to 24.5 years at age 63. That’s a decline of 3.5% in the number of years one can expected to receive those higher, deferred benefits. At ages 69 and 70, remaining life expectancy is 19.6 and 18.8 years, respectively. Therefore, waiting the extra year to age 70 means a 4.1% decline in future years of benefits. So rather than a safe, 8% return, subtract about 4%. You’re looking at roughly a 4% uncertain return for deferral of benefits between age 62 and age 70. If you have health issues, it’s obviously worse.

Opportunity Cost: It would be fine to take an expected 4% annual return for deferring SS benefits if you had no immediate use for the extra funds. But you could take the early benefits and invest them! If you’re still working, you could possibly save a like amount of funds from your employment income tax-deferred. So taking the early benefits would be worthwhile if you can earn at least 4% on the funds. Sure, investment returns are uncertain, but over a few years, a 4% annualized return (which I’ll call the “hurdle” rate) should not be hard to beat.

The same logic applies to an already retired individual who would withdraw funds from savings to afford the deferral of SS benefits. Instead, if he or she takes the benefits immediately, leaving a like amount invested, any return in excess of about 4% will have made it worthwhile. But of course, all of this is beside the point if you really just want to retire and the early benefits allow you to do so. You value the benefits now!

But what about taxes? Investment income will generally be taxed, and it’s possible the incremental benefits from deferred SS benefits won’t be. That might swing the calculus in favor of waiting a few extra years to file. And taking benefits early, while still employed, might mean a larger share of the early benefits will be taxed. If 80% of your benefits are taxed at a marginal rate of 25%, state and federal, you’re out 20% of your early benefits. Also, if you expect to be in a lower tax bracket in the future (good luck!), or if you plan to move to a low-tax state at some point in the future, deferring benefits might be more advantageous.

On the other hand, if you’re subject to tax on a portion of your early benefits, you’re likely to be subject to tax on benefits you defer as well. If you’re SS benefits and investment income are both taxed, the issue might be close to a wash, but that hurdle return I mentioned above might have to be a bit higher than 4% to justify early benefits.

Optimal? So what is an “optimal” decision about when to file for SS benefits? For anyone in their 60s today who has not yet filed for SS benefits, it depends on your tolerance for market risk and your tax status.

—You can likely earn more than the rough 4% annual hurdle discussed over a few years in the market, so taking benefits as early as 62 might be a reasonable decision. That’s especially true if you already have some cash set aside to ride out market downturns.

—If you are an extremely conservative investor then you are unlikely to achieve a 4% return, so the “safe” return from deferring SS benefits is your best bet.

—If you believe your tax status will be more favorable later, that might swing the pendulum in favor of deferral, again depending on risk tolerance.

—If you are afraid that failing health and death might come prematurely, filing early is a reasonable decision.

—If you simply want to retire early and the benefits will enable you to do that, filing early is simply a matter of personal time preference.

So my friend who is deferring his SS benefits until age 70 might or might not be optimizing: 1) he is supremely confident in his long-term health, but that’s not something he should count on; 2) he might be an extremely cautious investor (okay…); and 3) he’s still working, and he might expect his tax status to improve by age 70 (I doubt it).

I plan to retire before I turn 65, and I think I’ll be happy to take the benefits and leave more of my money invested. As for Social Security generally, I’d be happy to take a steeply discounted lump sum immediately and invest it, rather than wait for retirement, but that ain’t gonna happen!

I’m always hearing fearful whines from several left-of-center retirees in my circle of my acquaintances: they say the GOP wants to cut their Social Security and Medicare benefits. That expression of angst was reprised as a talking point just before the midterm election, and some of these people actually believe it. Now, I’m as big a critic of these entitlement programs as anyone. They are in very poor financial shape and in dire need of reform. However, I know of no proposal for broad reductions in Social Security and Medicare benefits for now-eligible retirees. In fact, thus far President Trump has refused to consider substantive changes to these programs. And let’s not forget: it was President Obama who signed into law the budget agreement that ended spousal benefits for “file and suspend” Social Security claimants.

Both Social Security (SS) and Medicare are technically insolvent and reform of some kind should happen sooner rather than later. It does not matter that their respective trust funds still have positive balances — balances that the federal government owes to these programs. The trust fund balances are declining, and every dollar of decline is a dollar the government pays back to the programs with new borrowing! So the trust funds should give no comfort to anyone concerned with the health of either of these programs or federal finances.

Members of both houses of Congress have proposed steps to shore up SS and Medicare. A number of the bills are summarized and linked here. The range of policy changes put forward can be divided into several categories: tax hikes, deferred benefit cuts, and other, creative reforms. Future retirees will face lower benefits under many of these plans, but benefit cuts for current retirees are not on the table, except perhaps for expedient victims at high income levels.

There is some overlap in the kinds of proposals put forward by the two parties. One bipartisan proposal in 2016 called for reduced benefits for newly-eligible retired workers starting in 2022, among a number of other steps. Republicans have proposed other types of deferred benefit cuts. These include increasing the age of full eligibility for individuals reaching initial (and partial) eligibility in some future year. Generally, if these kinds of changes were to become law now, they would have their first effects on workers now in their mid-to-late fifties.

Another provision would switch the basis of the cost-of-living adjustment (COLA) to an index that more accurately reflects how consumers shift their purchases in response to price changes (see the last link). The COLA change would cause a small reduction in the annual adjustment for a typical retiree, but that is not a future benefit reduction: it is a reduction in the size of an annual benefit increase. However, one Republican proposal would eliminate the COLA entirely for high-income beneficiaries (see the last link) beginning in several years. A few other proposals, including the bipartisan one linked above, would switch to an index that would yield slightly more generous COLAs.

Democrats have favored increased payroll taxes on current high earners and higher taxes on the benefits of wealthy retirees. Republicans, on the other hand, seem more willing to entertain creative reforms. For example, one recent bill would have allowed eligible new parents to take benefits during a period of leave after childbirth, with a corresponding reduction in their retirement benefits (in present value terms) via increases in their retirement eligibility ages. That would have almost no impact on long-term solvency, however. Another proposal would have allowed retirees a choice to take a portion of any deferred retirement credits (for declining immediate benefits) as a lump sum. According to government actuaries, the structure of that plan had little impact on the system’s insolvency, but there are ways to present workers with attractive tradeoffs between immediate cash balances and future benefits that would reduce insolvency.

The important point is that enhanced choice can be in the best interests of both future retirees and long-term solvency. That might include private account balances with self-directed investment of contributions or a voluntary conversion to a defined contribution system, rather than the defined benefits we have now. The change to defined contributions appears to have worked well in Sweden, for example. And thus far, Republicans seem more amenable to these creative alternatives than Democrats.

As for Medicare, the only truth to the contention that the GOP, or anyone else, has designs on reducing the benefits of current retirees is confined the to the possibility of trimming benefits for the wealthy. The thrust of every proposal of which I am aware is for programmatic changes for future beneficiaries. This snippet from the Administration’s 2018 budget proposal is indicative:

“Traditional fee-for-service Medicare would always be an option available to current seniors, those near retirement, and future generations of beneficiaries. Fee-for-service Medicare, along with private plans providing the same level of health coverage, would compete for seniors’ business, just as Medicare Advantage does today. The new program, however, would also adopt the competitive structure of Medicare Part D, the prescription drug benefit program, to deliver savings for seniors in the form of lower monthly premium costs.”

There was a bogus claim last year that pay-as-you-go (Paygo) rules would force large reductions in Medicare spending, but Medicare is subject to cuts affecting only 4% of the budgeted amounts under the Paygo rules, and Congress waived the rules in any case. Privatization of Medicare has provoked shrieks from certain quarters, but that is merely the expansion of Medicare Advantage, which has been wildly popular among retirees.

Both Social Security and Medicare are in desperate need of reform, and while rethinking the fundamental structures of these programs is advisable, the immediate solutions offered tend toward reduced benefits for future retirees, later eligibility ages, and higher payroll taxes from current workers. The benefits of currently eligible retirees are generally “grandfathered” under these proposals, the exception being certain changes related to COLAs and Medicare benefits for high-income retirees. The tendency of politicians to rely on redistributive elements to enhance solvency is unfortunate, but with that qualification, my retiree friends need not worry so much about their benefits. I suspect at least some of them know that already.

The Social Security and Medicare trust funds should offer no comfort as the obligations of those programs outrace revenues. Between them, the funds hold about $3.1 trillion of federal government bonds purchased with past surplus “contributions” from FICA and Medicare payroll taxes. In other words, those surplus contributions were used to pay for past government deficits. Here’s what Warren Meyer has to say on the topic:

“Imagine to cover benefits in a particular year the Social Security Administration needs $1 billion above and beyond Social Security taxes. If the trust fund exists, the government takes a billion dollars of government bonds out and sells them to private buyers on the open market. If the trust fund didn’t exist, the government would …. issue a billion dollars in bonds and sell them to private buyers on the open market. In either case, the government’s indebtedness to the outside world goes up by a billion dollars.”

Therefore, the trust funds do not provide any real cushion against future obligations. As Meyer says, you can write IOUs to yourself, put them in a piggy bank and call it a trust fund of your very own, but that won’t increase your wealth.

As it happens, last week the Trustees of the Medicare (MC) Trust Fund released the latest projections showing that it will be exhausted by 2026. Likewise, the Trustees of the Social Security (SS) Trust Fund reported that it will be depleted by 2036. But again, those trusts do not enhance the federal government’s fiscal position, so they really don’t matter. Even with the interest earned on the bonds held in trust, which is itself owed by the federal government, the trusts are merely placeholders for an equivalent dollar value of unfunded federal obligations. And in a very real sense, these funds hold no more than our own future tax liabilities: that debt is our debt.

Federal spending on discretionary and other on-budget entitlements is deeply in deficit on an ongoing basis, expected to be greater than $1 trillion annually by 2020, according to the Congressional Budget Office. Then add the bonds that will be sold to the public from the SS and MC trust funds, and total government borrowing from “the public” will become that much larger. After the trust funds are exhausted, accounting for the impact of the annual SS and MC system deficits will be more transparent.

The previous use of SS and MC contributions to pay for other government outlays strikes many as a violation of trust. Remember, however, that contributions to these systems are taxes, after all. And despite apparent impressions to the contrary, and perhaps for worse, individual vesting was never part of the SS system. But if the government must borrow a dollar (on a unified basis), is it always better to do it later? That was essentially the decision made (repeatedly) when FICA and Medicare taxes were used to purchase government bonds. The answer depends on whether the government has an immediate uses for the surplus that can be expected to earn returns superior to investment opportunities of suitable risk otherwise available to the trust funds. I would argue, however, that most of the “spent” funds from surplus FICA and Medicare taxes were put toward government consumption, and much less to investment in physical or social infrastructure. In fact, the availability of the SS and MC surpluses probably encouraged that consumption. To that extent, it was a certainly a mistake.

If the question is at what point must the government address the shortfall in its ability to pay future obligations to seniors, the answer is not “2026 and 2034”. It is now. The programs are racking-up obligations to future retirees that will be impossible to meet. The long-run (75-year) SS deficit projected by the trustees has a present value of $13.2 trillion, with an annual deficit growing to about 1.5% of GDP. By then, the Medicare deficit is expected to bring the combined shortfall of the two programs up to 2.3% of GDP. The trustees estimate that SS benefits would have to be cut by 25% in order to eliminate that deficit, with additional cuts to Medicare.

Oh, but those estimates treat the trust funds as if they are meaningful assets, and they are not! Of course, there are other solutions to the funding shortfall, but I truly hope that current workers have realistic expectations. They should adjust their saving rates to avoid excessive reliance on government social and medical insurance programs.

It’s one thing for indignant seniors (or anyone nearing retirement) to defend the crappy returns they get on their lifetime Social Security payroll taxes … er, contributions, against the arguments of reformers. It’s another for younger individuals to rant about the threat to the crappy returns they will get while resisting an idea for reform that would almost certainly improve their eventual well-being: privatization. Both of the aforementioned reactions are marked by confusion over the use of the word “entitlement” in federal budgeting, though in another sense, entitlement is manifested in the very defensiveness of the reform critics. At its root, this self-righteous naiveté is a product of ignorance about the program, its insolvency, how its rewards compare to private savings, and longstanding media propaganda favoring big government as grubstaker… because it feels virtuous.

There’s really not much to like about Social Security, though the status quo will always appeal to some.

Insolvency: The trust fund held $2.7 trillion of reserves at the end of 2016, but benefit payments are growing faster than contributions (plus interest on the public bonds held by the fund). The wave of retiring baby boomers and increasing longevity (and a declining number of workers per retiree) are placing a strain on the system. According to the trustees, depletion of the fund will begin in earnest in 2022, and the Old Age Survivors and Disability Insurance (OASDI) fund will be exhausted by 2034. This might be delayed if the economy and employment grow faster than expected. The actuarial deficit through 2091 is $12.5 trillion, as Brenton Smith notes in this post.

“Suppose you are given an option to invest your FICA taxes (and your employer’s contributions) over your working life in a stock market index fund. After 40 years or so, based on historical returns, you’ll have stashed away about 12 – 18 times your total contributions (that range is conservative — 40 years through 2014 would have yielded 19x contributions). A horrible preretirement crash might leave you with half that much. At the low-end, you might have as little as 4.5 times contributions if the crash is as bad as the market decline of 1929-32. That would be very bad.

But you don’t have that option under current law. Instead, the return you can expect from Social Security will leave you with only 1 to 4 times your contributions — without further changes in the program — based on your current age, lifetime earnings, marital status and retirement age. The latter range is based on the Social Security Administration’s (SSA’s) own calculations, as quoted in ‘Social Security: Saving or Tax? Proceeds or Aid‘ on Sacred Cow Chips.”

Reforms? The prototypical reform proposals always involve cutting benefits or raising taxes in one way or another. No wonder there is so much suspicion among the public! For seniors and near-retirees, the lousy returns noted above are at least fairly certain: generally, reform proposals haven’t applied to those of age 55+. Nonetheless, those projected returns are not a promise. There is a risk that the benefits could be changed or eroded by Congress, as discussed here by Lance Robert. For youngsters, the returns are much more uncertain, and changing the structure of distant benefits is always more politically palatable.

Examples of typical reform proposals include delaying the age at which benefits can be claimed, increasing the income cap on payroll taxes, and changing the way in which benefits are indexed to inflation. Many of the “new ideas” shown at this link are variations on finding additional tax revenue or delaying benefits. Rep. Sam Johnson has proposed a set of fairly conventional reforms, including gradual increases in the retirement age and elimination of the earnings test, so that some income could be earned without reducing benefits. Also, Johnson’s plan would redistribute benefits toward low-income beneficiaries. AARP provides a summary of 12 proposals, one of which is to index benefits for life expectancy at each age: as expected longevity increases, annual benefits would decrease. There are other proposals with a strongly redistribution aspect, such as reducing benefits for those with high lifetime earnings or means-testing benefits.

Better ideas: There are currently some incentives in place for retirees to delay benefits for a few years, and some of the proposals at the “new ideas” link would attempt to strengthen those rewards. Another idea mentioned there is to offer an inducement to delay claims by allowing at least a portion of future benefits to be taken as a lump sum. This is more novel and has greater potential savings to the system in a world with increasing longevity. To the extent that retirees can privately invest at more advantageous returns, they might be willing to accept a substantial discount on the actuarial value of their benefits.

The interests of future beneficiaries would be served most effectively by allowing them to choose between contributing to the traditional program or setting a portion of their contributions aside in a private account. These accounts would give individual workers flexibility over investment direction. As discussed above, better returns than the traditional program can be had with near-certainty given sufficient time until retirement. Michael Tanner at CATO is correct in insisting that workers control their own accounts should they opt-out of the traditional program. And the government itself should stay out of private capital markets.

It is this proposal that is always greeted with the most vitriol by opponents of reform. The very idea of private accounts seems to them an affront. One explanation is the fear of financial risk, but this would be mitigated by limiting the opt-out to younger workers with adequate time for growth. Another explanation is the fear that lower-income beneficiaries would not fare well under this reform. In fact, there is a strong semblance of redistribution in the system’s existing benefit formulas, but these features do not amount to much once adjusted for the differing life expectancies of income groups and the benefits paid to survivors. There is no reason, however, why the private account option would prevent redistribution through the traditional portion of contributions. Moreover, there is value in creating greater transparency when it comes to redistribution, as it promotes more effective scrutiny.

Funding: Unfortunately, the Social Security program has long relied on funding current benefits to retirees with dollars contributed by current workers. This is one of the biggest areas of misunderstanding on the part of the public. Allowing workers to opt-out would improve the long-term benefits received by those retirees, but it would also remove a portion of the funding for current retirees, thus accelerating a portion of the system’s unfunded obligations. A similar acceleration of the funding gap would accompany any reform to discount future benefits in exchange for payment of a lump sums in advance. The tradeoff is favorable over a time horizon lengthy enough to cover the retirement of today’s younger workers, but the near-term shortfall can only be met by reduced benefits, borrowing, or new sources of funds.

Asset Sales: The best option for bridging the funding needs of a transition to private, individually-controlled accounts is to sell federal assets. I have discussed this before in the context of funding a universal basic income, which I oppose. The proceeds of such sales, however, could be used to pay the benefits of current and near-term retirees so as to allow the opt-out for younger workers. The asset sales would have to proceed at a careful and deliberate pace, perhaps stretching over a decade or more, but those sales could include everything from unoccupied federal buildings to vast tracts of public lands in the west, student loans, oil and gas reserves, and airports and infrastructure such as interstate highways and bridges. In 2011, it was estimated that the federal government owned $1.6 trillion worth of liquid assets alone. The value of less liquid federal assets would be in the many trillions of dollars. (Read this eye-opening assessment of federal assets.) Of course, these assets would be more productive in private hands.

Sustainability: The outrage greeting ideas for entitlement reform largely denies the economic reality of inadequate funding. Social Security is just one example of an unsustainable entitlement program. Few participants in the system seem to realize that their benefits are paid out of contributions made by current workers, or that surpluses of the past were simply borrowed by the government and used to fund other spending. It was sustainable only with a sufficient number of contributing workers to support a stable class of retiree-beneficiaries. It cannot withstand an expanding class of longer-living beneficiaries relative to the labor force.

Ideally, reform would address the system’s insolvency as well as the weak returns to beneficiaries on their payments into the system. Self-direction and individual control over at least a portion of invested contributions should be viewed as a long-term fix for both. It will yield much better returns than the traditional system, but for workers this depends on the amount of time remaining until retirement. Young workers can elect to opt-out of the traditional system at little risk because they have the time to invest over several market cycles, but older workers must be circumspect. In any case, it is unlikely that politicians would take the chance of allowing older workers to opt-out, then face a potential backlash after a market downturn.

The insolvency problem, and the short-term funding shortfall created via the opt-out alternative, require hard decisions, but asset sales can bridge a large part of the gap, if not all of it. Lump-sum benefit payments might also be made at a savings, but they would worsen the short-term gap between benefit payments and contributions. In the long-run, the tradeoffs would become more favorable as today’s young workers age and retire with the more handsome returns available via individually-controlled and privately-invested accounts.

Social Security benefit levels are anything but sure for current workers, given the likelihood of benefit cuts to preserve the long-term solvency of the system. In fact, even without those cuts, Social Security provides very poor yields for retirees on their lifetime contributions. Instead of a tradeoff between risk and return, the system offers bad outcomes along both dimensions: lousy benefit levels that are not at all “safe”.

To get a clear sense of just how bad the returns on Social Security contributions (i.e., FICA tax deductions) truly are, take a look at this Sacred Cow Chips post from late 2015: “Stock Crash At Retirement? Still Better Than Social Security“. According to the Social Security Administration’s own calculations, without any future changes in the program, a retiree can expect to get back 1 to 4 times their lifetime contributions (obviously, this is not discounted). If you think that’s acceptable, consider a real alternative:

“Suppose you are given an option to invest your FICA taxes (and your employer’s [FICA] contributions) over your working life in a stock market index fund. After 40 years or so, based on historical returns, you’ll have stashed away about 12 – 18 times your total contributions (that range is conservative — 40 years through 2014 would have yielded 19x contributions). A horrible preretirement crash might leave you with half that much.“

Allowing workers to self-direct their contributions over a lengthy working life, whether they invest in equities, government bonds, or other assets, holds much more promise as a way to provide for their retirement needs.

As for risk, projected benefit levels are worse when possible program changes are considered. It’s widely accepted that changes must be made to the way contributions by current workers are handled and how future benefits are determined, or else the system’s value to them will be a greatly diminished. The Social Security Trust Fund, which once funded government deficits via FICA surpluses over benefit disbursements (while the demographics of the labor force allowed), has dwindled, and it has never been invested to earn the returns necessary for long-term solvency. Shall today’s workers face later eligibility? Reduced benefit levels? Or both? Or can we face up to the reality that workers will do better by choosing the way their funds are invested?

The contributions of today’s workers are paid out directly to current retirees. This practice must be modified, but the nation still faces a large and immediate liability to current retirees. How will it be paid if the system is overhauled to allow self-directed investment alternatives? Current workers must pay for some portion of that liability, but that portion could be phased out over several decades. The transition, however, would initially require additional taxes, borrowing, or voluntary conversion by some retirees to a discounted cash-balance equivalent, much as most private sector defined-benefit pensions have been converted to cash-balance equivalents.

Ultimately, workers should benefit from their own individual contributions. One objection is that self-directied investments and “privatization” of one’s own contributions would cause the system to lose its function as social insurance. Recall, however, that eligibility for benefits requires contributions, so it is not a general program of assistance. Nevertheless, there are several ways in which Social Security fulfills an insurance function. In a strong sense, it provides insurance against the risk of failure to save for retirement. More fundamentally, disabled workers can qualify for benefits, and the dependents of a deceased contributor are also eligible (survivors’ benefits). In addition, the current system provides greater returns to individuals with relatively low contributions. Under self-direction, these features could be retained via minor redistributional elements applied to investment returns, particularly given the superior returns available to equities over periods of sufficient length.

When U.S. politicians discuss the future of Social Security, they usually say they’ll fight against the dark intent of those who wish to take away hard-earned benefits from seniors. This despite the fact that few (if any) observers have suggested cutting benefits for current retirees, or even for those now approaching eligibility. The self-righteous proclamations about protecting retirees are a dodge that avoids the need to take a position on dealing with the system’s insolvency. But an easy answer is available: reform the system by allowing workers to self-direct their contributions into more promising investment vehicles.

That’s right! Suppose you are given an option to invest your FICA taxes (and your employer’s contributions) over your working life in a stock market index fund. After 40 years or so, based on historical returns, you’ll have stashed away about 12 – 18 times your total contributions (that range is conservative — 40 years through 2014 would have yielded 19x contributions). A horrible preretirement crash might leave you with half that much. At the low-end, you might have as little as 4.5 times contributions if the crash is as bad as the market decline of 1929-32. That would be very bad.

But you don’t have that option under current law. Instead, the return you can expect from Social Security will leave you with only 1 to 4 times your contributions — without further changes in the program — based on your current age, lifetime earnings, marital status and retirement age. The latter range is based on the Social Security Administration’s (SSA’s) own calculations, as quoted in “Social Security: Saving or Tax? Proceeds or Aid” on Sacred Cow Chips.

Social Security, billed as the most reliable source of retirement income because it is not dependent on market risk — would almost certainly buy you less than a private investment even when a horrible market outcome is factored in immediately prior to retirement. Keep in mind that this is an unfair baseline for equity investments, because historical returns already factor-in historical market crashes, and we are imposing an extra, instantaneaous crash at the end-point! Note also that the calculations above do not account for ongoing, post-retirement returns in private investments. In view of this comparison, Social Security’s status as an “untouchable” third-rail of U.S. politics is a testament to the economic ignorance of the American voter.

Wharton’s Jeremy Siegel offers perspective at wsj.com based on his own experience in “My Sorry Social Security Return” (gated — Google “wsj Siegel Social Security”). Siegel’s Social Security benefits represent about a third of what he could have earned in private investments; the value of his benefits is also much less than what Siegel would have earned for retirement had those funds been invested exclusively in government bonds, as the Social Security “Trust Fund” does when there are surplus contributions over and above benefits paid. The return Siegel can expect over his retirement years on Medicare taxes paid is similarly bad. Siegel is just the kind of high earner whom many assume Social Security favors.

Even worse, Social Security benefits for future retirees are quite risky, given the long-term demographic changes underway in the U.S. The Social Security system is not solvent. Only recently, we have witnessed the revocation of “Restricted Application” filing for married filers born after 1953. This change can mean a significant reduction in benefits to any married couple, but it may be a more meaningful blow to married filers in the age cohort now approaching retirement or full-filing eligibility. This will not be the last revocation of future benefits, because the system is now “cash-flow negative” (benefit payments exceed payroll-tax contributions) and it will be for the foreseeable future. There will be hikes in payroll-taxes and reductions in benefits down the road.

This post is a follow-up to earlier discussions on Sacred Cow Chips of Social Security’s horrid returns to retirees: “Reform Not: Play Social Security Slots” in October and the link given in the second paragraph (above) from August. The Social Security “Trust Fund” is not an asset with any net value to the economy. Earlier surpluses have been used to fund the government’s general budget, so the SS Trust Fund is not “saving” your contributions in any real sense. Government debt held by the Trust Fund as an “asset” must be repaid to the SS system via future taxes. Some asset for the public!