Tags

Blackouts, Electric Reliability Council of Texas, ERCOT, February Cold Spell, Federal Energy Subsidies, Fixed-Rate Plans, Fossil fuels, Interconnection Agreements, Market Efficiency, Price Ceilings, Price Gouging, Renewable energy, Shortages, Solar Power, Supply Elasticity, Texas, Variable-Rate Plans, Wind Power, Winterization

People say the darnedest things about markets, even people who seem to think markets are good, as I do. For example, when is a market “too efficient”? In the real world we tend to see markets that lack perfect efficiency for a variety of reasons: natural frictions, imperfect information, taxes, subsidies, regulations, and too few sellers or buyers. In such cases, we know that market prices don’t properly reflect the true scarcity of a good, as they would under the competitive ideal. Nevertheless, we are usually best-off allowing market forces to approximate true conditions in guiding the allocation of resources. But what does it mean when someone asserts that a market is “too efficient”.

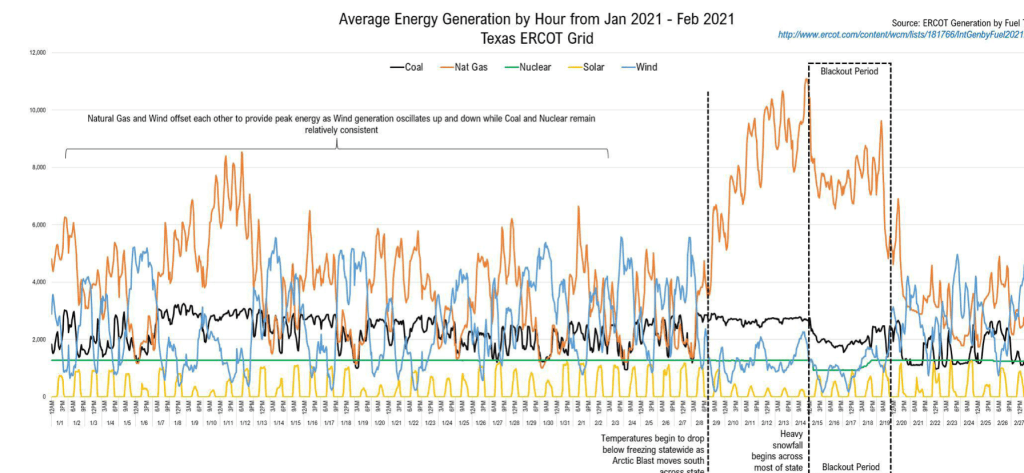

Not long ago I posted about the failure of Texas utility planners to maintain surge capacity. Instead, they plowed resources into renewable energy, which is intermittent and unable to provide for reliable baseline power loads. That spelled disaster when temperatures plunged in February. Wind and solar output plunged while demand spiked. Even gas- and coal-fired power generation hit a pause due to a lack of adequate winterization of generators. The result was blackouts and a huge jump in wholesale power prices, which are typically passed on to customers. The price to some consumers rose to the ceiling of $9/kwh for a time, compared to an average winter rate of 12c/kwh. A bill in the Texas Senate would reverse those charges retroactively.

I cross-linked my post on a few platforms, and a friendly commenter opined that the jump in prices occurred because “markets were too efficient”. For a moment I’ll set aside the fact that what we have here is a monopoly grid operator: “market efficiency” is not a real possibility, despite elements of competition at the retail level. There is, however, a price mechanism in play at the wholesale level and for retail customers on variable rate plans. Prices are supposed to respond to scarcity, and there is no question that power became scarce during the Texas cold snap. Higher prices are both an incentive to curtail consumption and to increase production or attract product from elsewhere. So, rather than saying the “market was too efficient”, the commenter should have said “power was too scarce”! Well duh…

If anything, the episode underscores how un-market-like were the conditions created by the Texas grid operator, the ironically-named Electric Reliability Council of Texas (ERCOT): it allowed massive resources to be diverted to unreliable power sources; it skimped on winterization; it failed to arrange interconnection agreements with power grids outside of Texas; and it charged customers on fixed-rate plans too little to provide for adequate surge capacity, while giving them no incentive to conserve under a stress scenario. ERCOT can be said to have created a situation in which power supply was highly inelastic, which means that a normal market force was short-circuited at a time when it was most needed.

ERCOT‘s mismanagement of power resources is partly a result of incentives created by the federal government. The installation of wind and solar power generation came with huge federal subsidies, which distort the cost of the energy they produce. Thus, not only were incentives in place to invest in unreliable power sources, but ERCOT forced electricity produced by fossil fuels to compete at unrealistically low prices. This predatory pricing forced several power producers into bankruptcy, compromising the state’s baseline and surge capacity.

There are plenty of distortions plaguing the “market” for electric power in Texas, all of which worsened the consequences of the cold snap. This was far from a case of “market efficiency”, as the comment on my original post asserted.

The very idea that markets and the price mechanism are “ruthlessly efficient” is a concession to those who say high prices are always “unfair” in times of crises and shortages. We hear about “price-gougers”, and the media and politicians are almost always willing to join in this narrative. Higher prices help to ease shortages, and they do so far more quickly and effectively than governments or charities can provide emergency supplies (unless, of course, a monopoly grid operator leaves the state more vulnerable to stress conditions than necessary). Conversely, price ceilings only serve to exacerbate shortages and the suffering they cause. So let’s not blame markets, which are never “too efficient”; sometimes the things we trade are just too scarce, and sometimes they are made more scarce by inept planners.