Tags

Artificial Tradeoffs, Big Meat, Big Oil, Black Markets, central planning, Excess Demand, Federal Reserve, Inflation, Isabella Weber, Joe Biden, Money Supply, Paul Krugman, Price Controls, Relative Prices, Scientism, Shortage, Unintended Consequences

In a gross failure of education or perhaps memory, politicians, policymakers, and certain academics seem blithely ignorant of things we’ve learned repeatedly. And of all the dumb ideas floated regarding our current bout with inflation, the notion of invoking price controls is near the top. But watch out, because the Biden Administration has already shifted from “inflation is transitory” to “it only hurts the rich” to “it’s fine because people just want to buy things”, and now “greedy businessmen are the culprits”. The latter falsehood is indeed the rationale for price controls put forward by a very confused economist at the University of Massachusetts-Amherst named Isabella Weber. (See this for an excerpt and a few immediate reactions.) She makes me grieve for my profession… even the frequently ditzy Paul Krugman called her out, though he softened his words after realizing he might have offended some of his partisan allies. Of course, the idea of price controls is just bad enough to gain favor with the lefty goofballs pulling Biden’s strings.

To understand the inflation process, it’s helpful to distinguish between two different dynamics:

1. When prices change we usually look for explanations in supply and demand conditions. We have supply constraints across a range of markets at the moment. There’s also a great deal to say about the ways in which government policy is hampering supplies of labor and energy, which are key inputs for just about everything. It’s fair to note here that, rather than price controls, we just might do better to ask government to get out of the way! In addition, however, consumer demand rebounded as the pandemic waned and waxed, and the federal government has been spending hand over fist, with generous distributions of cash with no strings attached. Thus, supply shortfalls and strong demand have combined to create price pressures across many markets.

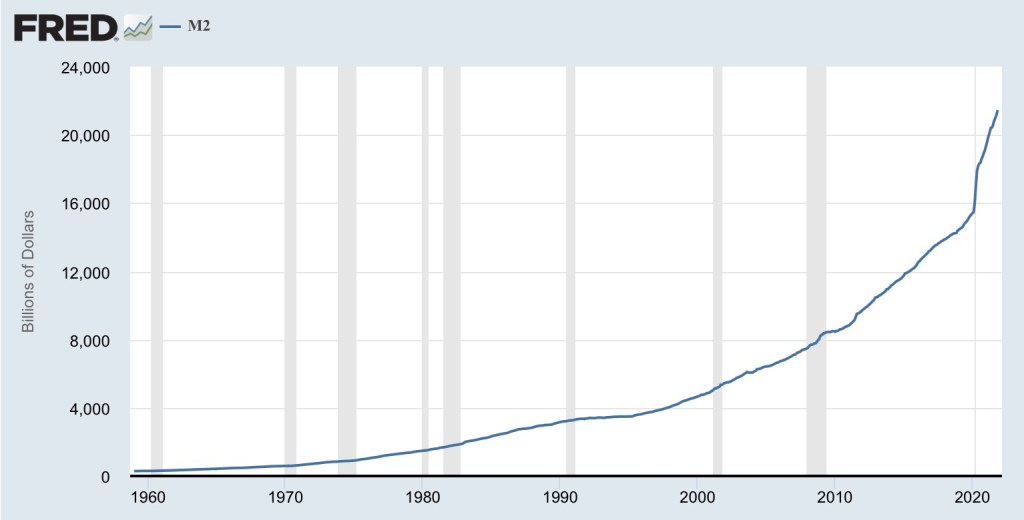

2. Economy-wide, all dollar prices cannot rise continuously without an excess supply of a monetary asset. The Federal Reserve has discussed tapering its bond purchases in 2022 and its intention to raise overnight interest rates starting in the spring. It’s about time! The U.S. money supply ballooned during 2020 and its growth remains at a gallop. This has enabled the inflation we are experiencing today, and only recently have the markets begun to react as if the Fed means business.

Weber, our would-be price controller, exhibits a marked ignorance with respect to both aspects of price pressure: how markets work in the first instance, and how monetary profligacy lies at the root of broader inflation. Instead, she insists that prices are rising today because industrialists have simply decided to extract more profit! Poof! It’s as simple as that! Well what was holding those greedy bastards back all this time?

Everyone competes for scarce resources, so prices are bid upward when supplies are short, inputs more costly, or demand is outpacing supply for other reasons. Sure, sellers may earn a greater margin on sales under these circumstances. But the higher price accomplishes two important social objectives: efficient rationing of available quantities, and greater incentives to bring additional supplies to market.

So consider the outcome when government takes the advice of a Weber: producers are prohibited from adjusting price in response to excess demand. Shortages develop. Consumers might want more, but that’s either impossible or it simply costs more. Yet producers are prohibited from pricing commensurate with that cost. Other adjustments soon follow, such as changes in discounts, seller credit arrangements, and product quality. Furthermore, absent price adjustment, transaction costs become much more significant. Other resources are consumed in the mere process of allocating available quantities: time spent in queues, administering quotas, lotteries or other schemes, costly barter, and ultimately unsatisfied needs and wants, not to mention lots of anger and frustration. Lest anyone think this process is “fair”, keep in mind that it’s natural for these allocations to take a character that is worse than arbitrary. “Important people” will always have an advantage under these circumstances.

Regulatory and financial burdens are imposed on those who play by the rules, but not everyone does. Black market mechanisms come into play, including opportunities for illegal side payments, rewards for underworld activity, along with a general degradation in the rule of law.

Price controls also impose rigidity in relative prices that can be very costly for society. “Freezing” the value of one good in terms of others distorts the signals upon which efficient resource allocation depends. Tastes, circumstances, and production technology change, and flexible relative prices enable a smoother transitions between these states. And even while demand and/or input scarcity might increase in all markets, these dynamics are never uniform. Over time, imbalances always become much larger in some markets than others. Frozen relative prices allow these imbalances to persist.

For example, the true value of good A at the imposition of price controls might be two units of good B. Over time, the true value of A might grow to four units of good B, but the government insists that A must be traded for no more than the original two units of B. Good B thus becomes overvalued on account of government intervention. The market for good A, which should attract disproportionate investment and jobs, will instead languish under a freeze of relative prices. Good B will continue to absorb resources under the artificial tradeoff imposed by price controls. Society must then sacrifice the gains otherwise afforded by market dynamism.

The history of price controls is dismal (also see here). They artificially suppress measured inflation and impose great efficiency costs on the public. Meanwhile, price controls fail to address the underlying monetary excess.

Price controls are destructive when applied economy-wide, but also when governments attempt to apply them to markets selectively. Posturing about “strategic” use of price controls reveals the naïveté of those who believe government planners can resolve market dislocations better than market participants themselves. Indeed, the planners would do better to discover, and undo, the damage caused by so many ongoing regulatory interventions.

So beware Joe Biden’s bluster about “greedy producers” in certain markets, whether they be in “Big Meat”, or “Big Oil”. Price interventions in these markets are sure to bring you less meat, less oil, and quite possibly less of everything else. The unintended consequences of such government interventions aren’t difficult to foresee unless one is blinded with the scientism of central planning.

Pingback: A Fiscal Real-Bills Doctrine? The Fiction of a Painless Inflation Tax | Sacred Cow Chips