Tags

Adam Shapiro, Bloomberg, Cleveland Fed, Demand-Driven Inflation, Federal Reserve, Great Recession, Inflation Targets, Joe Wiesenthal, Median CPI, Modern Monetary Theory, Money Printing, Noah Smith, Omnibus Spending Bill, Optimal Rate of Inflation, Pay-As-You-Go Law, PCE Deflator, Price Stability, Quantitative Easing, Rate Targets, Strategic Petroleum Reserve, Supply-Driven Inflation, Team Transitory, Trading Economics, Trimmed CPI

The answer to that question, kids, is a resounding no! The Federal Reserve created far too much liquidity during and after the pandemic and waited too long to reverse that policy. That’s a common view among the “monetarazzi”, but far too many analysts, in the next breath, assert that the Fed is going too far in tightening policy. Sorry, but you can’t have it both ways! Thus far, the reductions we’ve seen in the monetary aggregates (M1, M2, M3) represent barely a trickle out of the ocean of liquidity released during the previous two years. The recent slight moderation in the rate of inflation is unlikely to gain momentum without persistence by the Fed.

This Could Be Easier

I humbly concede, however, that a different approach by the Fed might have been less disruptive. A better alternative would have involved more aggressive reductions in the gigantic portfolio of securities it acquired via “quantitative easing” (QE) during the pandemic while avoiding direct intervention to raise short-term interest rates. In fact, allowing interest rates to be determined by the market, rather than via central bank intervention, is more sensible in terms of pricing debt of any duration. It also suggests a more direct and sensible approach to managing the growth of the money supply. Of course, had the Fed unwound QE more aggressively, short-term rates would surely have risen anyway, but to levels appropriate to rationing liquidity more efficiently. Furthermore, those rates could have served as a useful indicator of the market’s ability to digest a particular volume of sales from the Fed’s portfolio.

Getting Tight

The chart below shows the level of the monetary base (bank reserves plus currency) over the past five years from the Trading Economics site. The monetary base is the narrow monetary aggregate supporting growth of the money stock and is under fairly direct control of the Fed.

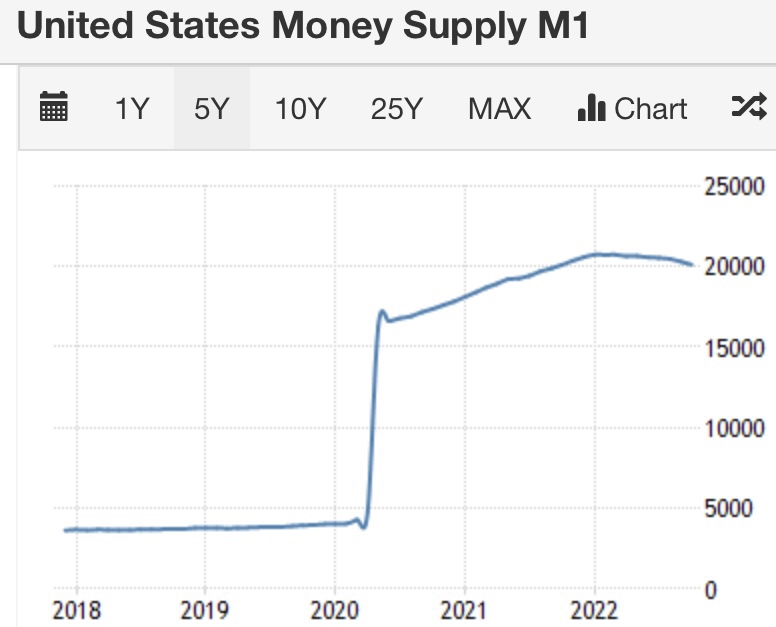

The base has declined substantially during 2022 largely as a consequence of the Fed’s restrictive policies. However, it has retraced only about a third of the massive expansion engineered by the Fed over the two prior years. Here is the corresponding plot of the M1 money stock (currency plus checking deposits):

So the reductions in the base have yet to translate into much of a reduction in the money stock, though growth in all of the aggregates has certainly declined. No one thinks this will be a walk in the park. Withdrawing liquid capital from markets accustomed to swilling in excesses will have consequences, particularly for investors who’ve grown undisciplined in their approach to evaluating prospective assets. Investors and society at large inevitably pay the price for the malinvestment encouraged by unbridled money growth (not to mention misdirected industrial policies … that’s a different can of worms).

But the squeamish resist! I got a kick out of this tweet by Noah Smith in which he pokes fun at those who insist that the surge in inflation was a mere transitory phenomenon:

“Team Transitory: OMG inflation is just going to go away, you don’t need to raise interest rates.

Fed: *raises interest rates*

Inflation: *goes down a bit*

Team Transitory: SEE, I told you inflation was going away and that you didn’t need to raise interest rates!!”

Well, in fairness, “Team Transitory” has been fixated on supply disruptions that very well should resolve with private efforts over time. Some have resolved already. And again, we’ve yet to feel much impact from the Fed’s tighter policy, but I’m amused by the tweet nevertheless.

In fact, the surge in inflation has been driven by both supply and demand factors, and it’s true the Fed can do very little about the former. But stalling the effort to purge excess liquidity and demand-side inflation risks allowing expectations of inflation to edge higher, creating an environment in which price pressures are more resistant to policy actions.

Inflation And Its Proximate Sources

It is indeed good news that inflation has tapered slightly over the past few months, or at least the “headline” inflation numbers have tapered. Weaker energy prices helped a great deal, though releases from the Strategic Petroleum Reserve aren’t sustainable. Measures of “core” inflation that exclude food and energy prices, and more central measures of inflation within the spectrum of goods and services, have moved sideways or perhaps shown signs of a slight moderation.

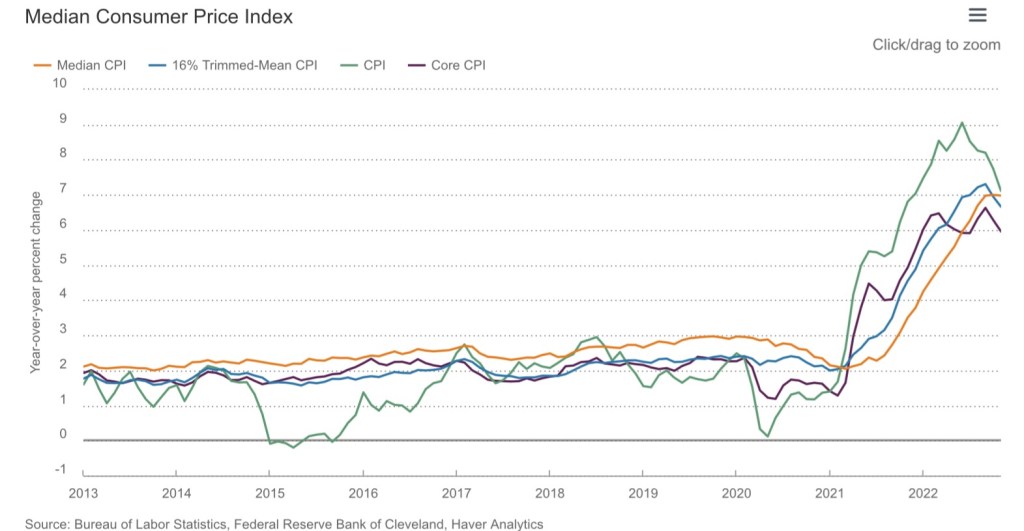

Here’s a plot of several measures of CPI inflation taken from the Cleveland Fed’s web site. Note that the median component of the CPI has finally hit a plateau, and a “trimmed” measure that excludes CPI components with extreme changes has dipped slightly. The Core CPI has fluctuated in a range just above 6% for most of the year.

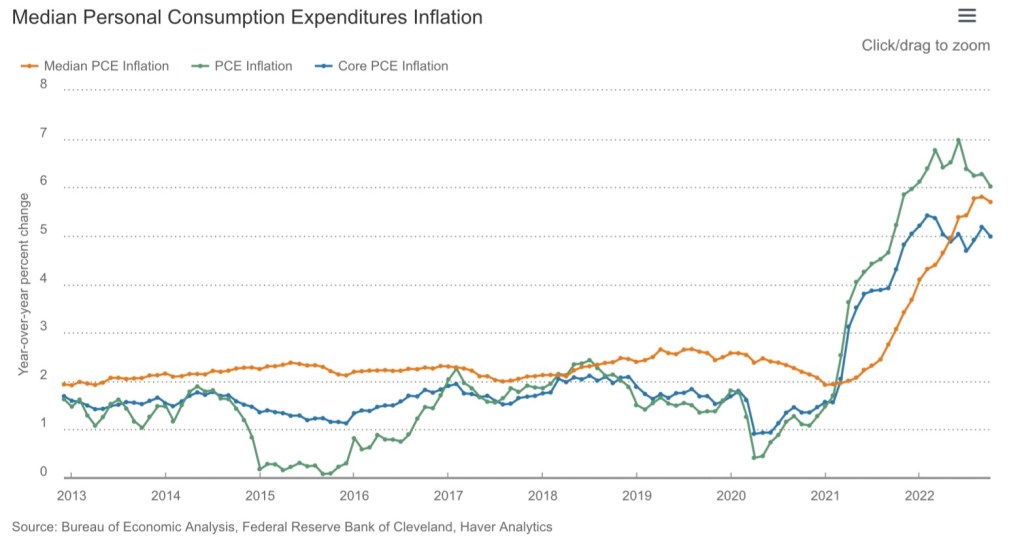

The deflator for personal consumption expenditures (PCE) gets more emphasis from the Fed in its policy deliberations. The latest release at the start of December showed patterns similar to the CPI:

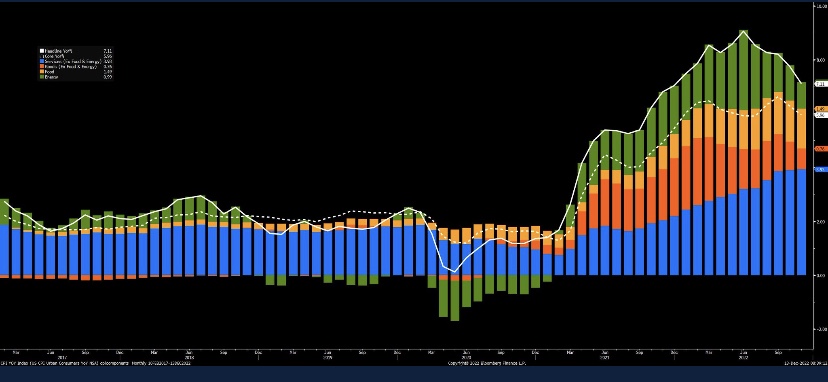

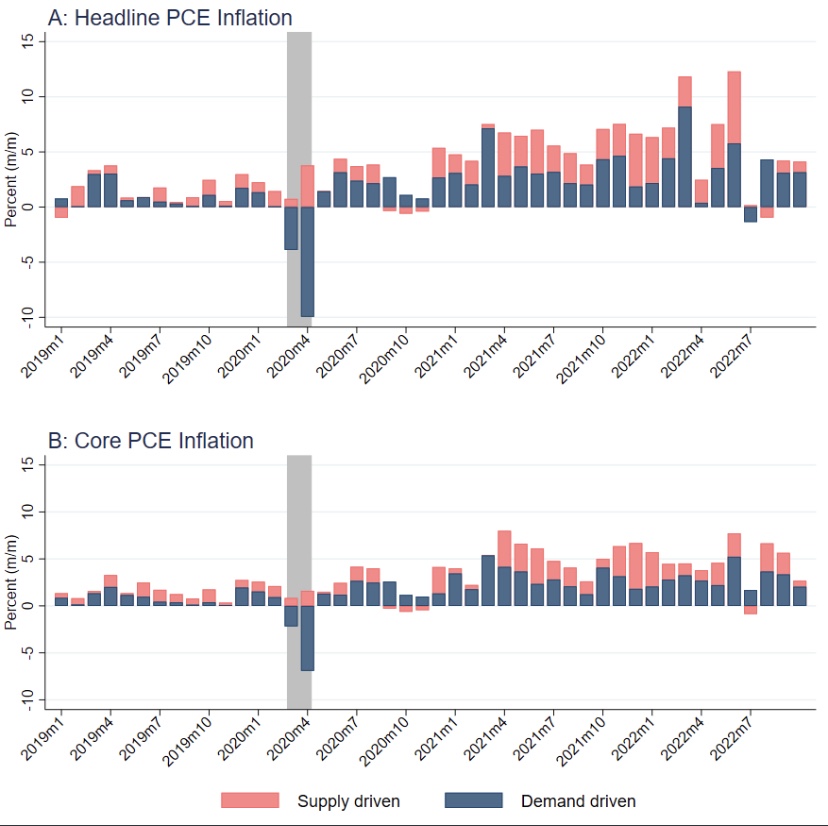

With respect to the PCE deflator, the slight dampening of price pressure we’ve seen recently came primarily from the supply side, with some progress on the demand side as well. Energy was one factor on the supply side, but even the core PCE deflator shows less supply pressure. Adam Shapiro has a decomposition of the PCE deflator into supply-driven and demand-driven components (but the chart only goes through October):

First, without endorsing Shapiro’s construction of this dichotomy, I note that the impact of monetary policy is primarily through the demand side of the economy. Of course, monetary instability isn’t good for producers, and excessive money growth and inflation create uncertainty that inhibits supply. But what we’ve seen recently has more to do with the curing of supply chain bottlenecks that cropped up during the pandemic (or in its wake), and Shapiro attempts to capture that kind of phenomenon here.

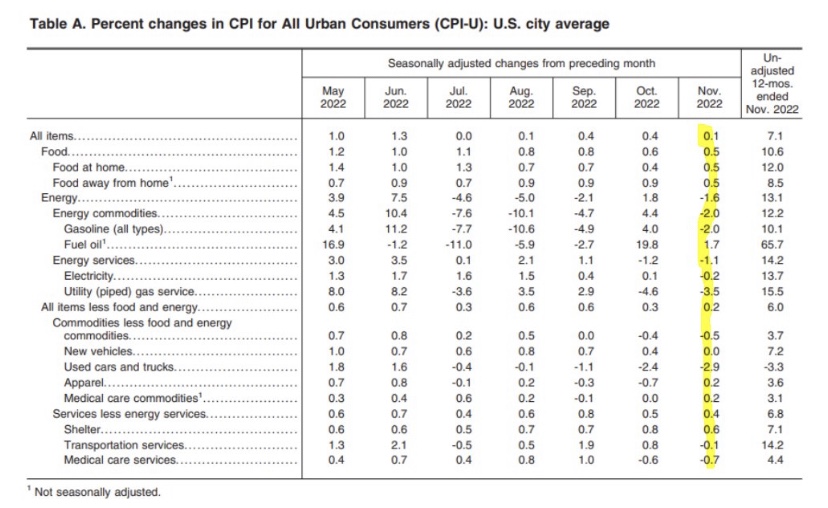

Still, many would argue that the November CPI showed sufficient progress for the Fed to pause its tightening campaign. The reductions in the monthly price increases were fairly widespread, as shown by this table from the CPI report:

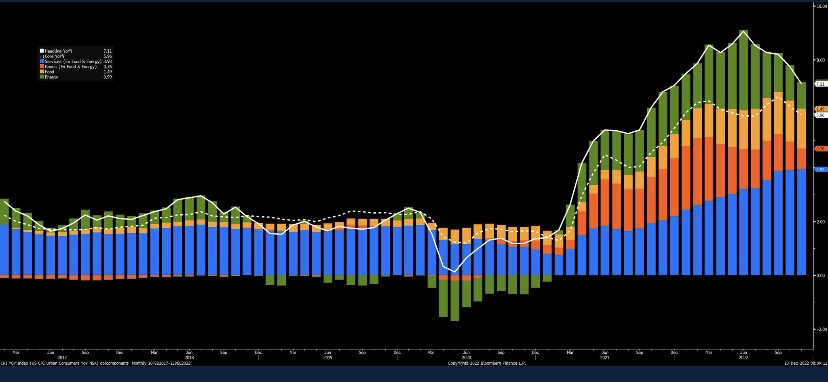

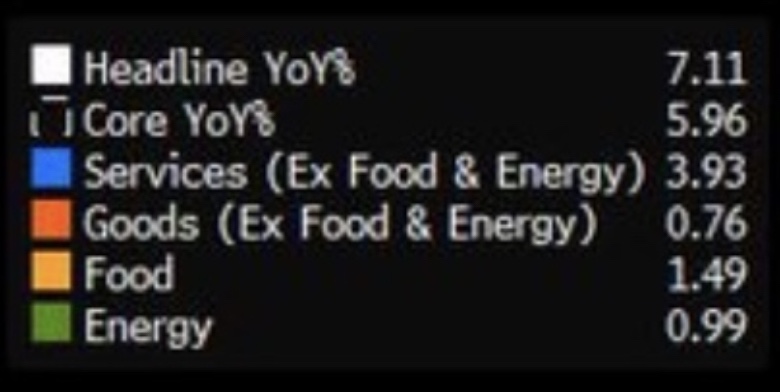

The next chart from Joe Wiesenthal (via Bloomberg) displays trends in broad CPI categories, but it shows vividly that the reductions were concentrated in energy components and goods prices, while services and food inflation did not really abate. (The legend is so hard to read that I took the liberty of blowing it up a bit below the chart itself):

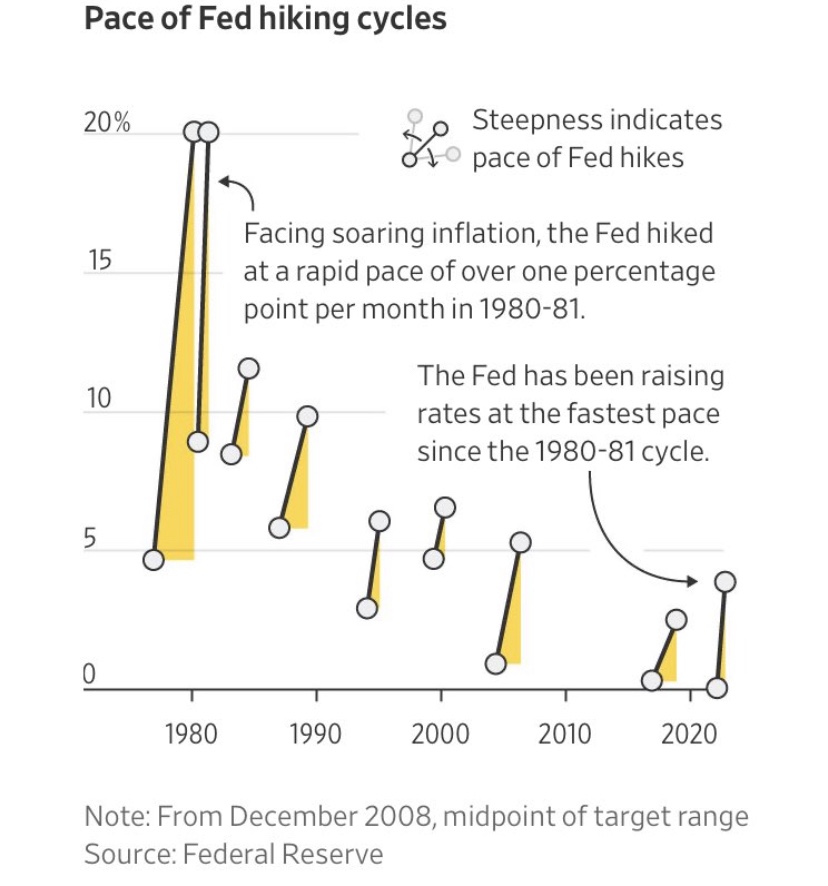

Playing Catch-Up

While the Fed’s effort to restrain inflation began in earnest in the spring of this year, it lifted the federal funds rate target rapidly. Here’s another chart from Adam Shapiro, via the Wall Street Journal: the Fed’s current tightening cycle is the fastest in 40 years in terms of those rate hikes:

Fast, yes, but they got a late start in the face of a rapid acceleration of inflation, and for what it’s worth, the Fed’s rate target remains below the rate of inflation. Yes, I’m forced to acknowledge here that the Fed’s preference for rate intervention and targeting is just what they do, for now. In any case, top-line inflation and strictly demand-side inflation are still above the Fed’s 2% target.

Fabian Fiscal Expansionists

One “fix” recommended in some circles suggests that the Fed’s inflation target is too low, as if price stability had nothing to do with its mandate! The idea that low-grade inflation is a healthy thing has never been convincingly demonstrated. In fact, the monetary literature leans strongly in the direction of price stability and an optimal rate of inflation of zero! That the Fed should aim for higher inflation seems like a cop-out intended to appease those who still subscribe to the discredited notion that there exists a reliable long-run tradeoff between inflation and unemployment.

In fact, proposals to increase the central bank’s inflation target would enable more deficit spending financed with the “printing press”, which is at the root of the demand-side inflation problem we now face. A major justifications for ballooning levels of federal spending has been so-called Modern Monetary Theory (MMM), which has gained adherents among statists in the years since the Great Recession. MMM holds that “important” initiatives can simply be paid for with new money creation, rather than interest bearing debt, or God forbid, taxes! “Partisan” is probably a better description than “theorist” for any fan of MMM, and they have convinced themselves that money financed deficits are without inflationary consequences. Of course, this represents a complete suspension of the law of resource scarcity, not to mention years of monetary history. Raising the Fed’s inflation target plays well with the same free-lunch advocates who rally behind MMM.

The Fed’s Unfaithful Fiscal Partner

Federal budget control is likely to take another hit this week with passage of the $1.7 omnibus spending bill. It includes spending increases with no immediate offsets as required under the pay-as-you-go budget law. It delays those offsets to 2025 and increases deficits in the interim by hundreds of billions of dollars. It also sets a new, higher baseline for discretionary appropriations in future years. The federal deficit has already risen dramatically compared to a year ago under the fiscal profligacy of Congress and the Administration. Another contributing factor, however, is that the interest cost of servicing the national debt has spiked as interest rates have risen. Needless to say, none this makes the Fed’s job any easier, especially as it seeks to reverse QE.

Say Uncle!?

When will the Fed begin to take its foot off the brake? It “only” raised the Fed funds target by 50 basis points at its meeting last week (after four 75 bps moves in a row. It is expected to raise the target another 50 bps in early February and perhaps another 25 in March. Strong signals of imminent recession would be needed for the Fed to call it off any sooner, and we’re definitely seeing more hints of a weakening economy in the data (and see here, here, here, and here). More definitive declines in inflation would obviously help settle things. Otherwise, the Fed may pause after March in order to gauge progress toward its goal of 2% inflation.