Tags

Ample Reserves, David Beckworth, Fed Balance Sheet, FOMC, Inflation Expectations, Interest on Bank Reserves, Iran Conflict, Jai Kadia, Jerome Powell, Judy Shelton, Kevin Warsh, Milton Friedman, Monetization, Nominal GDP Growth, Norbert Michel, Oil Prices, Overton Window, PCE Deflator, Quantitative Easing, Quantitative Tightening, Rules vs. Discretion, Scarce Reserves, Sound Money, Strait of Hormuz, Treasury-Fed Accord

A lot has changed since Kevin Warsh was nominated by President Trump to replace Jerome Powell as chairman of the Federal Reserve Board. Most notably that includes the war in Iran, the run-up in oil prices, and a bond market increasingly nervous about inflation as it attempts to digest massive supplies of new Treasury debt. Tariffs have also contributed to the updraft in measured inflation since then, which (in addition to oil prices) represents another impingement on the economy’s supply side.

Change and Change Itself

By the time Warsh was sworn in as chairman, expectations for Fed rate cuts had swung to expectations of a quarter-point increase in the federal funds rate target, if not at the mid-June meeting of the Federal Open Market Committee (FOMC) then in July. It’s not clear that Warsh is on board with that, and the status of the Iranian conflict, oil supplies, and the bond market could change dramatically before the June meeting.

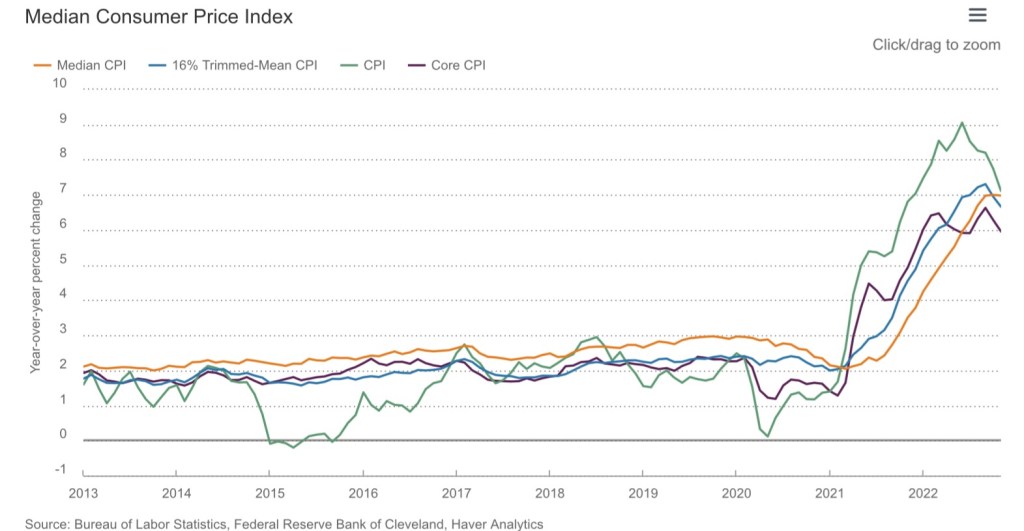

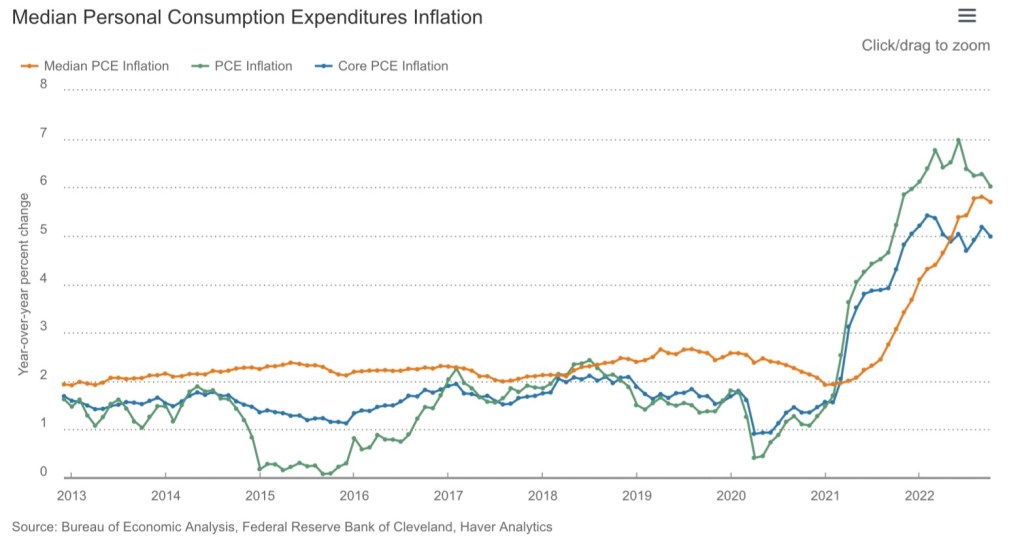

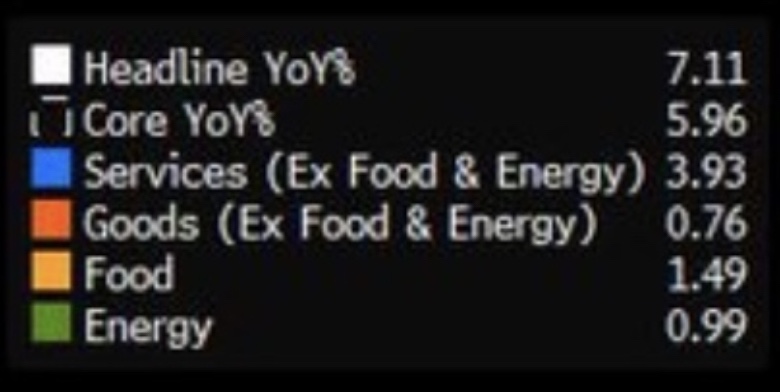

Short-term inflation expectations have risen, so a rate hike by the Fed might seem reasonable if not for the possibility that current inflation is transitory (but I use that term guardedly). In terms of money growth, policy seems roughly neutral to slightly restrictive. M2 growth from a year earlier was 4.7% in April. Nominal (current dollar) GDP grew at a slightly faster 5.1% clip in the first quarter, and it might accelerate in Q2. Real GDP advanced 1.6% from a year ago in the first quarter, but the Atlanta Fed’s forecast for real GDP in Q2 is a stronger 3.2%. Meanwhile, core PCE inflation (the Fed’s preferred gauge) was 3.1% in the first quarter and 3.3% in April. If the numbers roughly follow the same track going forward, nominal GDP in Q2 could be up by about 6% – 6.5% from a year ago. Slowing the rate of M2 growth much from its recent pace might be an overreaction.

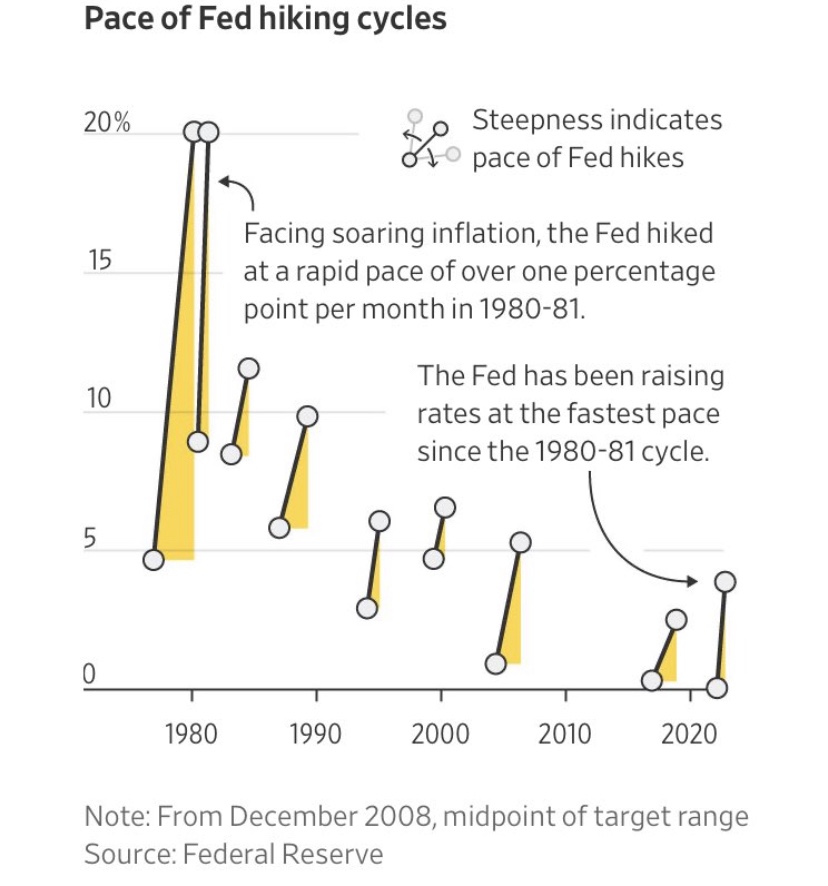

Moreover, it might be premature to raise the funds rate when a peaceful resolution to the Iran conflict is still possible. Again, we might know by the time the FOMC convenes in June. In that case, market rates could ease quickly. I am skeptical, however, that Iran will prove to be a reliable partner to any peace agreement. I’ll be surprised if the blockade on the Strait of Hormuz ends any time soon, and a few air strikes have already been renewed. Still, I expect the FOMC to defer any rate hike until at least the July meeting. In fact, I’ll be surprised to see one at all.

Sound Money or Monetary Madness

Many describe Warsh as a “sound money” guy, having been greatly influenced by Milton Friedman. He’s been critical of quantitative easing (QE): the Fed’s purchases of securities for its own balance sheet to provide liquidity to the markets and banking system. If the hostilities continue in Iran, Warsh is more likely to favor quantitative tightening (QT) in the short-term than rate hikes. QT would involve reductions holdings of securities on the Fed’s balance sheet, which Warsh has long advocated.

On the other hand, Warsh has been undaunted in insisting that the AI revolution will be a dramatic deflationary force. That’s a longer-term proposition, but it reinforces his preference for lower rates. So Warsh is for “sound money” and would like to see QT, but he also prefers lower rates and apparently believes that AI might justify a more expansionary monetary posture. So where does that leave us?

Squaring the Circle

A few months ago I described a coherent policy agenda for the Fed under Kevin Warsh, given his policy preferences. It might have lacked realism in terms of Fed politics, but it was motivated by the question of whether lower rates are compatible with QT. The discussion did not anticipate the Iran conflict and its economic and financial consequences.

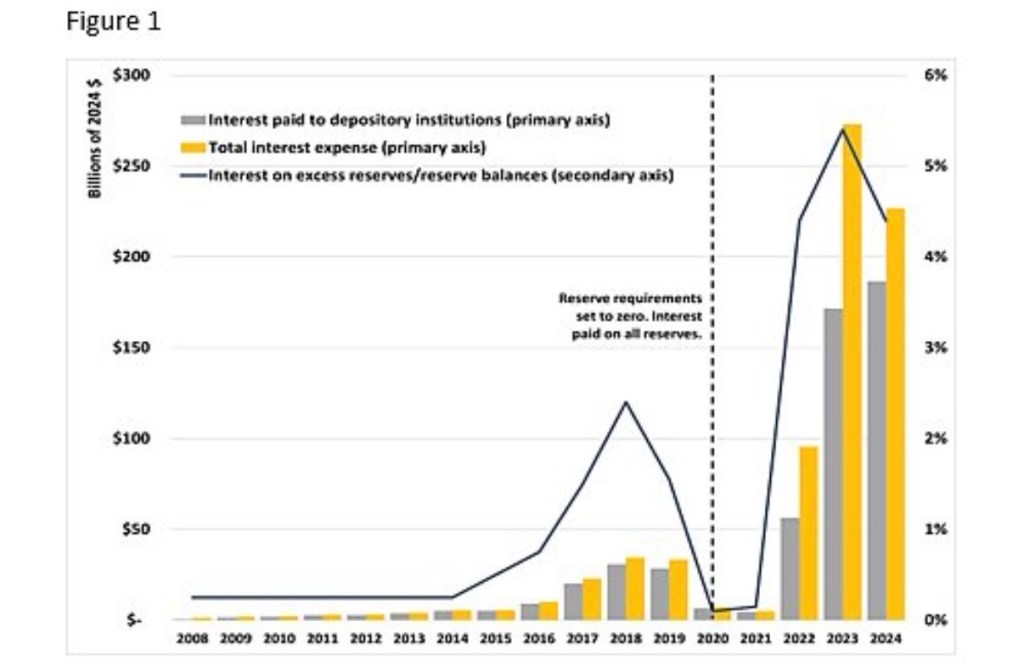

Lower rates and QT would be compatible if the Fed enables and incentivizes commercial banks to hold more securities and lend more aggressively. This would require regulatory changes as well as reductions in interest on bank reserves (IOR) held at the Fed.

Judy Shelton in the Wall Street Journal has made the same point, characterizing such a policy shift as “pro-market”. That’s because it would allow banks to invest in relatively safe assets, would eliminate a subsidy masquerading as a price (IOR – though fully administered), and would mean a transition from the Fed’s emphasis on maintaining ample bank reserves to scarce bank reserves. The latter would restore activity in the market for overnight loans of reserves (federal funds), which would then trade at a price corresponding to their degree of scarcity. That would provide an important signal to other markets, not to mention the Fed itself. Today, that signal is distorted by the Fed’s provision of ample reserves (repo rates notwithstanding). Jai Kadia and Norbert Michel have made a similar argument, along with advocating for rules-based monetary policy, rather than frequently destabilizing discretionary actions.

Momentum

In April, David Beckworth noted that momentum is building in influential circles for this change, which he describes as a “demand driven” approach, as opposed to the “supply driven”, ample reserve operating procedure now in force. This is the more common at many foreign central banks, and it has received prominent mention in recent speeches and statements by Fed officials. As Beckworth puts it in the title of his post, “The Fed’s Overton Window Is Shifting”.

Beckworth also mentions Warsh’s desire to establish a new Treasury-Fed Accord. The original 1951 Accord established the Fed’s independence from Treasury financing operations. Today’s ample reserves approach has made it far too easy for the Fed to succumb to pressures to monetize deficits and intervene in capital markets to manipulate longer rates. Warsh would surely like to re-establish the Fed’s monetary authority as a separate and independent function from Treasury financing.

The Fed Board of Governors (BoG) must approve changes in interest on reserves (IOR). (Better yet, an act of Congress would be required to prohibit IOR.) But Warsh, who is said to have good relations with the Fed staff and other Fed governors, is less likely to get a majority on the BoG than even the FOMC. For now, he’ll have to be persuasive to gain the support of a majority of either body.

Summary

Kevin Warsh is likely to argue strenuously for reductions in the size of the Fed’s balance sheet, and would almost certainly be happy for the FOMC to defer any rate hikes pending more clarity on a resolution to the Iran conflict. He will also argue for creating greater incentives for banks themselves to invest in Treasury debt, including reformed regulations on bank asset holdings and reduced interest on reserves held at the Fed. Ultimately, that would pave the way for lower rates on a variety of assets. But the Fed should be probably be cautious and gradual in the implementation: the changes to IOR and bank regulations must be well coordinated with QT and money growth must be calibrated to meet the Fed’s inflation target (or better yet, a nominal GDP target — see Part 2 of this post).