I’ll try to keep this one short. I was starting a post on another topic when Donald Trump distracted me… again. This time it was the $2,000 per person “tariff dividend” he’s proposed. This would be paid to all low- and middle-income Americans starting in mid-2026. As if the federal government was a profitable enterprise. Obviously that’s the wrong model! This is either sheer stupidity or willful government failure. Sure, the Fed can just print money, so why not? Who knew Trump was a closet modern monetary theorist?

It’s such a bad idea…. Tariffs themselves are bad enough. They are taxes, of course, a truth about which Trump and his central trade planners have denied since the beginning of the escapade. Tariffs hurt consumers and businesses who import inputs. Tariffs retard growth by increasing input costs, disrupting supply chains, and raising the prices of not only imports, but also domestically-produced goods that compete with imports. Surely Trump knows all this and the implications for his political capital: he’s already backtracking on tariffs for certain food items.

The tariff dividend is a transparent attempt to compensate consumers for the harms of taxation. It’s also a transparent attempt to buy or keep votes, much as he’s already sought to buy-off farmers harmed by tariffs. The income limit for the dividend hasn’t been announced, but make no mistake: this represents another form of redistribution.

It’s also striking that the tariffs won’t generate nearly as much revenue as will be required to begin paying the dividend by mid-2026. In fact, it could be short by as much as $300 million! Will the Treasury borrow the rest? More pressure on the bond market and interest rates.

Furthermore, the so-called dividend would be inflationary if the Federal Reserve fails to neutralize it. It would amount to another “helicopter drop” of cash, similar to the cash dump from Covid relief payments: money printing under the guise of fiscal policy.

To the extent that tariff revenue flows, it should be used to reduce the federal deficit or to pay down the gigantic government debt already outstanding ($38 trillion today not including the impending cost of funding entitlement programs). Instead, Trump is proudly following in the footsteps of generations of spendthrift politicians.

Keep in mind that the dividend is a promise Trump might not be able to keep. The Supreme Court will soon announce its decision on presidential power to impose tariffs. This decision will bear on the president’s authority under the International Emergency Economic Powers Act (IEEPA) — if and when an actual emergency is at hand, which it clearly is not. More broadly, the decision hinges on whether a “foreign facing” tax falls within the president’s Article II powers under the Constitution.

The proposed tariff dividend undermines the Administration’s argument before the Court that tariffs are primarily regulatory tools, and that any revenue from tariffs is merely incidental. Thank God the dividend would have to be authorized by Congress! I truly hope there are enough sensible legislators on the Hill to beat back this idiocy.

The answer to that question, kids, is a resounding no! The Federal Reserve created far too much liquidity during and after the pandemic and waited too long to reverse that policy. That’s a common view among the “monetarazzi”, but far too many analysts, in the next breath, assert that the Fed is going too far in tightening policy. Sorry, but you can’t have it both ways! Thus far, the reductions we’ve seen in the monetary aggregates (M1, M2, M3) represent barely a trickle out of the ocean of liquidity released during the previous two years. The recent slight moderation in the rate of inflation is unlikely to gain momentum without persistence by the Fed.

This Could Be Easier

I humbly concede, however, that a different approach by the Fed might have been less disruptive. A better alternative would have involved more aggressive reductions in the gigantic portfolio of securities it acquired via “quantitative easing” (QE) during the pandemic while avoiding direct intervention to raise short-term interest rates. In fact, allowing interest rates to be determined by the market, rather than via central bank intervention, is more sensible in terms of pricing debt of any duration. It also suggests a more direct and sensible approach to managing the growth of the money supply. Of course, had the Fed unwound QE more aggressively, short-term rates would surely have risen anyway, but to levels appropriate to rationing liquidity more efficiently. Furthermore, those rates could have served as a useful indicator of the market’s ability to digest a particular volume of sales from the Fed’s portfolio.

Getting Tight

The chart below shows the level of the monetary base (bank reserves plus currency) over the past five years from the Trading Economics site. The monetary base is the narrow monetary aggregate supporting growth of the money stock and is under fairly direct control of the Fed.

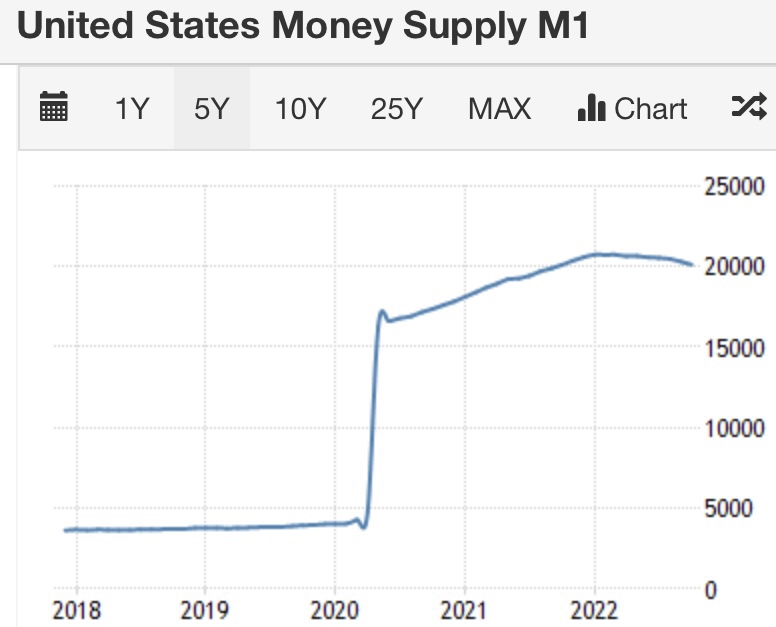

The base has declined substantially during 2022 largely as a consequence of the Fed’s restrictive policies. However, it has retraced only about a third of the massive expansion engineered by the Fed over the two prior years. Here is the corresponding plot of the M1 money stock (currency plus checking deposits):

So the reductions in the base have yet to translate into much of a reduction in the money stock, though growth in all of the aggregates has certainly declined. No one thinks this will be a walk in the park. Withdrawing liquid capital from markets accustomed to swilling in excesses will have consequences, particularly for investors who’ve grown undisciplined in their approach to evaluating prospective assets. Investors and society at large inevitably pay the price for the malinvestment encouraged by unbridled money growth (not to mention misdirected industrial policies … that’s a different can of worms).

But the squeamish resist! I got a kick out of this tweet by Noah Smith in which he pokes fun at those who insist that the surge in inflation was a mere transitory phenomenon:

“Team Transitory: OMG inflation is just going to go away, you don’t need to raise interest rates.

Fed: *raises interest rates*

Inflation: *goes down a bit*

Team Transitory: SEE, I told you inflation was going away and that you didn’t need to raise interest rates!!”

Well, in fairness, “Team Transitory” has been fixated on supply disruptions that very well should resolve with private efforts over time. Some have resolved already. And again, we’ve yet to feel much impact from the Fed’s tighter policy, but I’m amused by the tweet nevertheless.

In fact, the surge in inflation has been driven by both supply and demand factors, and it’s true the Fed can do very little about the former. But stalling the effort to purge excess liquidity and demand-side inflation risks allowing expectations of inflation to edge higher, creating an environment in which price pressures are more resistant to policy actions.

Inflation And Its Proximate Sources

It is indeed good news that inflation has tapered slightly over the past few months, or at least the “headline” inflation numbers have tapered. Weaker energy prices helped a great deal, though releases from the Strategic Petroleum Reserve aren’t sustainable. Measures of “core” inflation that exclude food and energy prices, and more central measures of inflation within the spectrum of goods and services, have moved sideways or perhaps shown signs of a slight moderation.

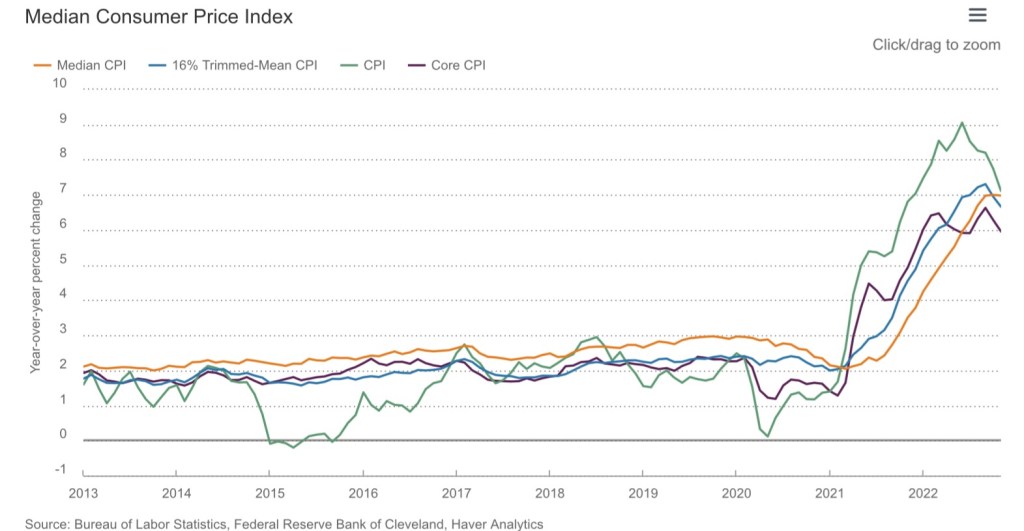

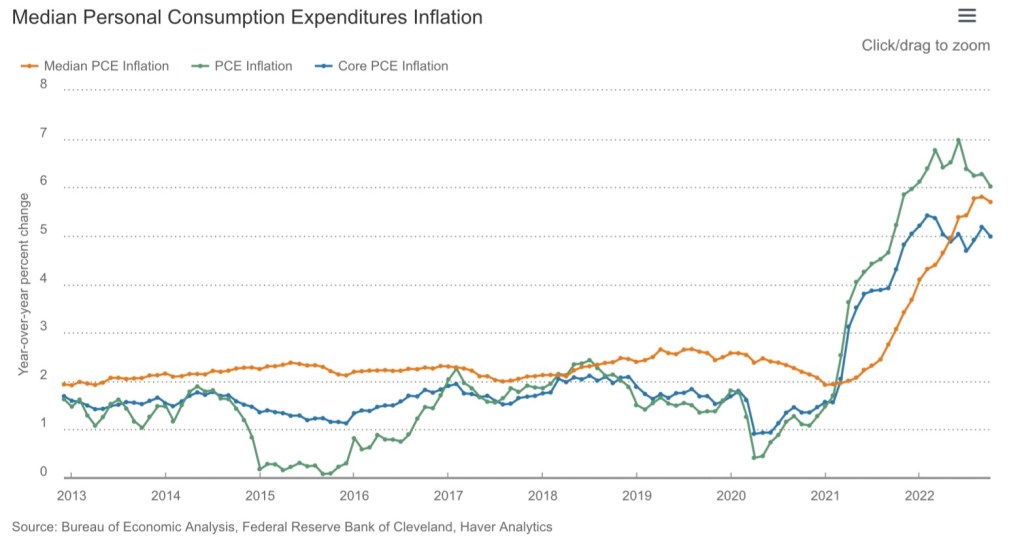

Here’s a plot of several measures of CPI inflation taken from the Cleveland Fed’s web site. Note that the median component of the CPI has finally hit a plateau, and a “trimmed” measure that excludes CPI components with extreme changes has dipped slightly. The Core CPI has fluctuated in a range just above 6% for most of the year.

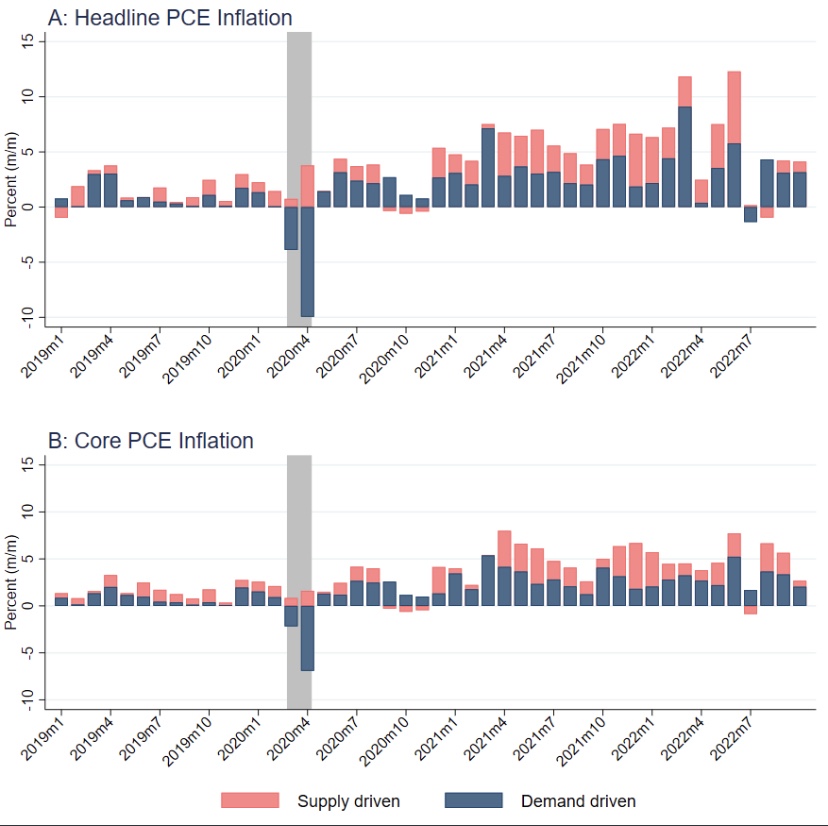

The deflator for personal consumption expenditures (PCE) gets more emphasis from the Fed in its policy deliberations. The latest release at the start of December showed patterns similar to the CPI:

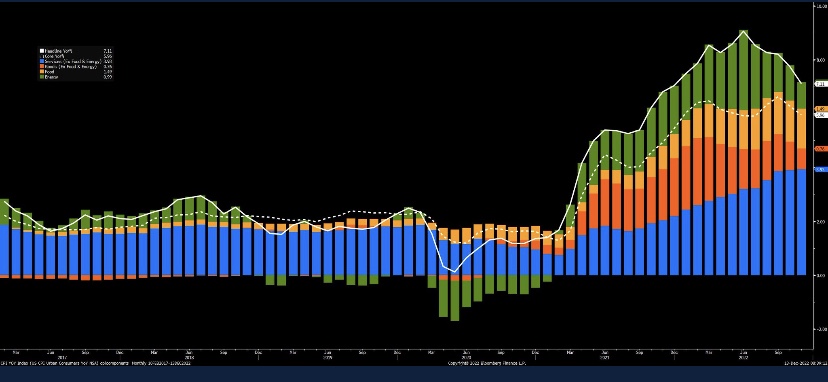

With respect to the PCE deflator, the slight dampening of price pressure we’ve seen recently came primarily from the supply side, with some progress on the demand side as well. Energy was one factor on the supply side, but even the core PCE deflator shows less supply pressure. Adam Shapiro has a decomposition of the PCE deflator into supply-driven and demand-driven components (but the chart only goes through October):

First, without endorsing Shapiro’s construction of this dichotomy, I note that the impact of monetary policy is primarily through the demand side of the economy. Of course, monetary instability isn’t good for producers, and excessive money growth and inflation create uncertainty that inhibits supply. But what we’ve seen recently has more to do with the curing of supply chain bottlenecks that cropped up during the pandemic (or in its wake), and Shapiro attempts to capture that kind of phenomenon here.

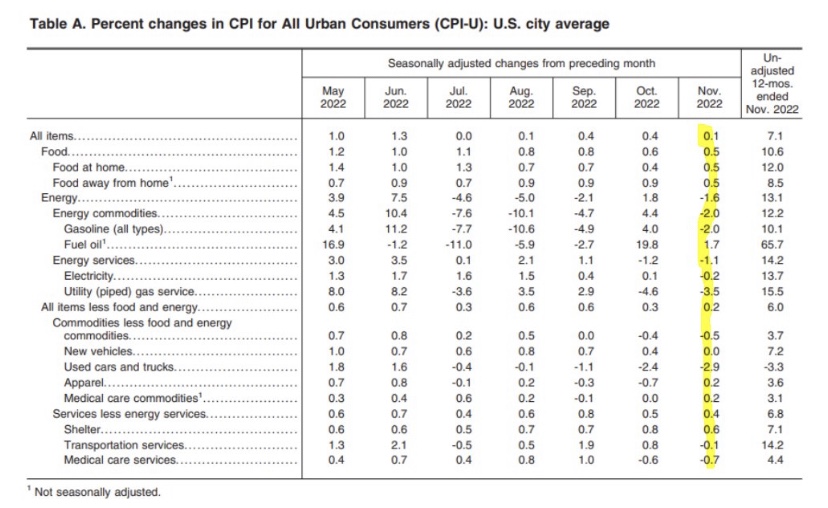

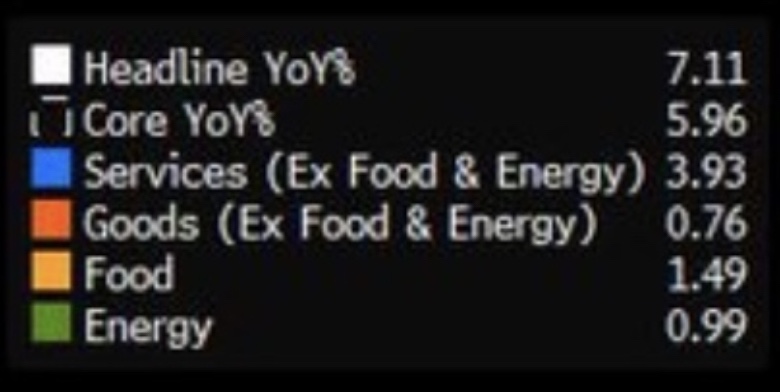

Still, many would argue that the November CPI showed sufficient progress for the Fed to pause its tightening campaign. The reductions in the monthly price increases were fairly widespread, as shown by this table from the CPI report:

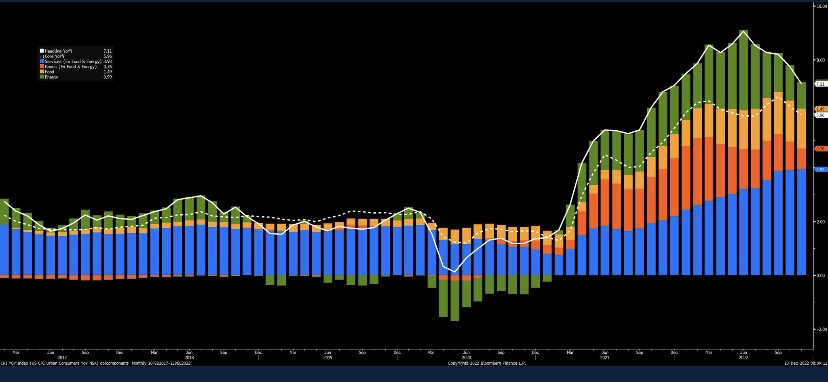

The next chart from Joe Wiesenthal (via Bloomberg) displays trends in broad CPI categories, but it shows vividly that the reductions were concentrated in energy components and goods prices, while services and food inflation did not really abate. (The legend is so hard to read that I took the liberty of blowing it up a bit below the chart itself):

Playing Catch-Up

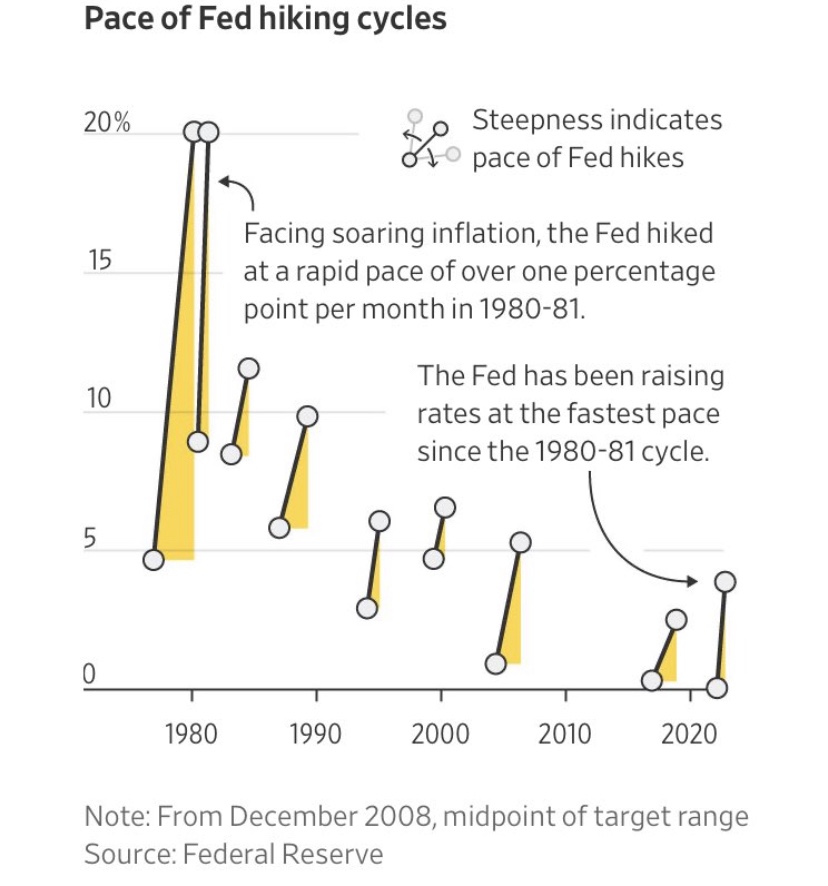

While the Fed’s effort to restrain inflation began in earnest in the spring of this year, it lifted the federal funds rate target rapidly. Here’s another chart from Adam Shapiro, via the Wall Street Journal: the Fed’s current tightening cycle is the fastest in 40 years in terms of those rate hikes:

Fast, yes, but they got a late start in the face of a rapid acceleration of inflation, and for what it’s worth, the Fed’s rate target remains below the rate of inflation. Yes, I’m forced to acknowledge here that the Fed’s preference for rate intervention and targeting is just what they do, for now. In any case, top-line inflation and strictly demand-side inflation are still above the Fed’s 2% target.

Fabian Fiscal Expansionists

One “fix” recommended in some circles suggests that the Fed’s inflation target is too low, as if price stability had nothing to do with its mandate! The idea that low-grade inflation is a healthy thing has never been convincingly demonstrated. In fact, the monetary literature leans strongly in the direction of price stability and an optimal rate of inflation of zero! That the Fed should aim for higher inflation seems like a cop-out intended to appease those who still subscribe to the discredited notion that there exists a reliable long-run tradeoff between inflation and unemployment.

In fact, proposals to increase the central bank’s inflation target would enable more deficit spending financed with the “printing press”, which is at the root of the demand-side inflation problem we now face. A major justifications for ballooning levels of federal spending has been so-called Modern Monetary Theory (MMM), which has gained adherents among statists in the years since the Great Recession. MMM holds that “important” initiatives can simply be paid for with new money creation, rather than interest bearing debt, or God forbid, taxes! “Partisan” is probably a better description than “theorist” for any fan of MMM, and they have convinced themselves that money financed deficits are without inflationary consequences. Of course, this represents a complete suspension of the law of resource scarcity, not to mention years of monetary history. Raising the Fed’s inflation target plays well with the same free-lunch advocates who rally behind MMM.

The Fed’s Unfaithful Fiscal Partner

Federal budget control is likely to take another hit this week with passage of the $1.7 omnibus spending bill. It includes spending increases with no immediate offsets as required under the pay-as-you-go budget law. It delays those offsets to 2025 and increases deficits in the interim by hundreds of billions of dollars. It also sets a new, higher baseline for discretionary appropriations in future years. The federal deficit has already risen dramatically compared to a year ago under the fiscal profligacy of Congress and the Administration. Another contributing factor, however, is that the interest cost of servicing the national debt has spiked as interest rates have risen. Needless to say, none this makes the Fed’s job any easier, especially as it seeks to reverse QE.

Say Uncle!?

When will the Fed begin to take its foot off the brake? It “only” raised the Fed funds target by 50 basis points at its meeting last week (after four 75 bps moves in a row. It is expected to raise the target another 50 bps in early February and perhaps another 25 in March. Strong signals of imminent recession would be needed for the Fed to call it off any sooner, and we’re definitely seeing more hints of a weakening economy in the data (and see here, here, here, and here). More definitive declines in inflation would obviously help settle things. Otherwise, the Fed may pause after March in order to gauge progress toward its goal of 2% inflation.

A remarkable proposal made recently by Representative Ro Khanna (D -CA) would have the Biden Administration impose price controls, which would be bad enough. Khanna also would like the federal government to cover the inflation losses incurred by Americans by having it directly purchase certain goods and services and resell them “cheap” to consumers. In fairness, Khanna says the government should attempt to take advantage of dips in prices for oil, food commodities, and perhaps other necessities, which of course would limit or reverse downward price changes. When asked about Khanna’s proposal, Pete Buttigieg, Joe Biden’s Transportation Secretary, replied that there were great ideas coming out of Congress and the Administration should consider them. Anyway, the idea is so bad that it deserves a more thorough examination.

Central Planners Have No Clothes

First, such a program would represent a massive expansion in the scope of government. It would also present ample opportunities for graft and cronyism, as federal dollars filter through the administrative layers necessary to manage the purchases and distribution of goods. Furthermore, price and quantity would then be shaded by a heavy political component, often taking precedence over real demand and cost considerations. And that’s beyond the crippling “knowledge problem” that plagues all efforts at central planning.

One of the most destructive aspects of allowing government to absorb a greater share of total spending is that government is not invested with the same budgetary discipline as private buyers. Take no comfort in the notion that the government might prove expert at timing these purchases to leverage price dips. Remember that government always spends “other people’s money”, whether it comes from tax proceeds, lenders, or the printing press (and hence future consumers, who have absolutely no agency in the matter). Hence, price incentives take on less urgency, while political incentives gain prominence. The loss of price sensitivity means that government expenditures are likely to inflate more readily than private expenditures. This is all the more critical at a time when inflation is becoming embedded in expectations and pricing decisions. Khanna thus proposes an inflation “solution” that puts less price-sensitive bureaucrats in charge of actual purchases. That’s a prescription for failure.

If anyone in Biden’s White House is seriously considering a program of this kind, and let’s hope they’re not, they should at least be aware that direct subsidies for the purchase of key goods would be far more efficient. It’s also possible to hedge the risk of future price increases on commodities markets, perhaps simply distributing hedging gains to consumers when they pay off. However, having the federal government participate as a major player in commodities options and futures is probably not on the table at this point … and I shudder to think of it, but it might be more efficient than Khanna’s vision.

A Fiscal Real Bills Doctrine

Khanna’s program would almost surely cause inflation to accelerate. Inflation itself a form of taxation imposed by profligate governments, though it’s an inefficient tax since it creates greater uncertainty. Higher prices deflate the real value of most government debt (borrowed from the public), assets fixed in nominal value, and incomes. Read on, but this program would have the government pay your inflation tax for you by inflating some more. Does this sound like a vicious circle?

Khanna’s concept of inflation-relief is a fiscal reimagining of a long-discredited monetary theory called the “Real Bills Doctrine”. According to this doctrine, rising prices and costs necessitate additional money creation so that businesses have the liquidity to pay the bills associated with ongoing productive efforts. The “real” part is a reference to the link between business expenses and actual production, despite the fact that those bills are expressed in nominal terms. The result of this policy is a cycle of ever-higher inflation, as ever-more money is printed. This was the policy utilized by the Reichsbank in Weimar Germany during its hyperinflation of 1922-23. It’s really quite astonishing that anyone ever thought such a policy was helpful!

In Khanna’s version of the doctrine, the government spends to relieve cost pressure faced by consumers, so the rationale has nothing to do with productive effort.

Financing and the Central Bank Response

It’s reasonable to ask how these outlays would be financed. In all likelihood, the U.S. Treasury would borrow the funds at interest rates now at 10-15 year highs, which have risen in part to compensate investors for higher inflation.

My bet is that Khanna imagines the Fed would simply “print” money (i.e., buy the new government debt floated by the Treasury to pay for the program). This is the prescription of so-called Modern Monetary Theory, whose adherents have either forgotten or have never learned that money growth and inflation is a costly and regressive form of taxation.

Most economists would say the response of the Federal Reserve to this fiscal stimulus would bear on whether it really ignites additional inflationary pressure. Of course, rather than borrowing, Congress could always vote to levy higher taxes on the public in order to pay the public’s inflation tax burden! But then what’s the point? Well, taxing at least has the virtue of not fueling still higher inflation, and the Fed would not have a role to play.

But if the government simply borrows instead, it adds to the already bloated supply of government debt held by the public. This borrowing is likely to put more upward pressure on interest rates, and the federal government’s mounting interest expense requires more financing. What then might the Fed do?

The Fed is an independent, quasi-government entity, so it would not have to accommodate the additional spending by printing money (buying the new Treasury debt). Either way, investors are increasingly skeptical that the growing debt burden will ever be reversed via future surpluses. The fiscal theory of the price level holds that something must reduce the real value of government debt (in order to satisfy the long-term fiscal budget constraint). That “something” is a higher price level. This position is not universally accepted, and some would contend that if the Fed simply set a nominal GDP growth target and stuck to it, accelerating inflation would not have to follow from Khanna’s policy. The same if the Fed could stick to a symmetric average inflation target, but they certainly haven’t been up to that task. Hoping the Fed would fully assert its independence in a fiscal hurricane is probably wishful thinking.

Conclusion

There are no choke points in the supply chain for bad ideas on the left wing of the Democratic Party, and they are dominating party centrists in terms of messaging. The answer, it seems, is always more government. High inflation is very costly, but the best policy is to rein it in, and that requires budgetary and monetary discipline. Attempts to make high inflation “painless” are misguided in the first instance because they short-circuit consumer price responses and substitution, which help restrain prices. Second, the presumption that an inflation tax can be “painless” is an invitation to fiscal debauchery. Third, expansive government brings out hoards of rent seekers instigating corruption and waste. Finally, mounting public debt is unlikely to be offset by future surpluses, and that is the ultimate admission of Modern Monetary Theory. A fiscal real bills doctrine would be an additional expression of this lunacy. To suggest otherwise is either sheer stupidity or an exercise in gaslighting. You can’t inflate away the pain of an inflation tax.

Recent years have seen explosive growth in federal deficits along with growth rates in the money supply that would have made John Maynard Keynes blush. It’s no coincidence that a new school of thought has developed among certain “monetary economists”. But as someone trained in monetary economics, I wish I could make those quote marks larger. This new school of thought is known as Modern Monetary Theory (MMT), and it asserts that the money spigot is a perfectly legitimate means of financing government spending and, furthermore, that it is not necessarily inflationary. Here is how Scott Sumner and Patrick Horan describe MMT:

“A central idea of MMT is that a government that issues its own fiat currency can pay its bills in that same currency. These governments need not worry about budget deficits when contemplating additional spending. Thus because the US government has a monopoly on money creation, our federal government does not need to raise all its revenue through tax or bond finance. A government with its own currency cannot go bankrupt because it can always issue more currency to cover any budget deficit. … MMT advocates argue that this why the US government can afford expensive programs such as a jobs guarantee and universal healthcare.”

Spend and Print

Joe Biden’s $3.5 trillion “social infrastructure” package would be just a start, but that’s likely to be more like $5.5T once the budget gimmicks are stripped out. We can be somewhat hopeful, because that initiative looks increasingly likely to fail in Congress, at least this time around. But the tax side of that bill was already $2.6T short of the latter spending figure, and the tax provisions keep shrinking. Now, it’s looking more like a shortfall of $3.5T would require financing. Moderate Democrats may not support this crazy bill in the end, but Dems from deep blue states want to reinstate state and local tax deductibility, which would cut the tax component still more. Well who cares? Print the money, say the brave MMT advocates.

Sumner gets to the heart of the problem in this piece. Progressives, with false assurance from MMT, want loose monetary policy to make their expansive programs “affordable”. As he explains, if this happens while the economy is near its production potential, inflation is a sure thing. These lessons were learned long ago, but have been conveniently forgotten by the political class (or they simply prefer to ignore them), instead jumping onto the MMT bandwagon.

Inflation Is Taxation

No conscientious observer of government finance should ever forget that inflation is a form of taxation. Assets whose values are either fixed or subject to some inertia are devalued by inflation in terms of purchasing power, or in real terms, as economists put it. Strictly speaking, this is true when inflation is unexpected… if it is expected, then lenders and borrowers can negotiate terms that will compensate for these changes in real value. But when inflation is unexpected, the losses to lenders are offset by gains to borrowers. Of course the federal government is a gigantic borrower, so inflation can represent a confiscation of wealth from the public.

It’s not small potatoes. Currently, about $22T of U.S. Treasury debt is held by the public, and its average maturity is more than 5 years. If the Federal Reserve engineers an unexpected 1% jump in the rate of inflation, it shaves over $1T off the real value of that debt before it’s repaid, and it reduces the real interest cost of that debt as well. Of course, the holders of that debt will suffer an immediate loss if they are forced to sell prior to maturity for any reason, since new buyers will be demanding higher yields to compensate for higher inflation if it is expected to persist.

The Poor Losers

Inflation causes redistributions to take place, especially when it is unexpected inflation. We’ve already discussed lenders and borrowers, but similar considerations apply to anyone entering into fixed price contracts for goods or labor. Here’s what Claudio Bario of the Bank of International Settlements (BIS) has to say about these shifts:

“Inflation shifts income and wealth away from those who are least aware of it, or least able to protect against it. These segments of the population often coincide with lower-income groups, which explains why inflation has often been portrayed as a most regressive form of tax. The ‘inflation tax’ takes its toll through the erosion of the value of financial assets and contracts fixed in nominal terms.”

Inflation is a regressive tax! In this respect, economist Noah Smith echos Bario in a recent op-ed in which he discusses “money illusion”, or the confusion of real and nominal income:

“Workers … who are slow to perceive the rise in prices they pay for goods like cars and groceries, won’t realize this, and will be happy with their unusually large raises. But companies, whose accountants and managers certainly know the true inflation rate, will also be happy, because they know they’re not actually paying more for labor.

That information asymmetry between workers and employers may be exactly what keeps wages from rising faster than inflation. If workers take a year to realize how much prices have gone up, they may be satisfied with the raises they got during the time of high inflation — even if that inflation ultimately turns out to be transitory. By then, it might be too late to negotiate for a real, inflation-adjusted raise.”

Inflation taxes and redistributions become more acute at higher rates of inflation, but any unexpected escalation in the rate of inflation will take a toll on the poor. Bario elaborates on the mechanisms by which inflation inflicts budgetary pain on the those at the lower end of the socioeconomic spectrum.

“As regards wealth distribution, the financial assets that are most vulnerable to inflation are cash and bank accounts – the typical savings vehicles held by the poorest segments of the population. This is mostly because the poorest have access only to limited investment options to protect their savings. …

… wages and pensions – the main sources of income for a large majority of households and even more so for the poorest half of the population – are typically fixed in nominal terms and hence vulnerable to inflation. Indexation mechanisms, such as those adopted in many [advanced economies] in the 1970s, are no panacea: they may fail to keep pace as inflation accelerates; …”

In addition to the inflationary gains reaped by government, it’s clear that inflation gives rise to redistributions between private parties: generally from those with lower incomes and wealth to their employers, producers, financial institutions, and pension payers (businesses, state and local governments). An exception is some low income debtors might benefit if they owe long term obligations at fixed interest rates, but low income individuals are often constrained from obtaining this form of credit.

Causing, Then Exploiting, Inequality

Another especially galling aspect of the Left’s focus on money finance is how its consequences fly in the face of their concerns about income and wealth inequality. Inflation is typically manifested in rising equity prices: nominal stock values tend to escalate in an inflationary environment, protecting their owners from losses to the real value of their investments. Stocks are generally a good inflation hedge. Yet we know that stocks are disproportionately owned by those in the highest strata of the income and wealth distributions. Later, of course, the Left will seek to level the burgeoning inequality wrought by their own policies by “taxing the rich”! Apparently, for the Left, consistency is never considered a virtue. This is not unlike another trick, which is to blame “greedy corporations” for the inflation wrought by Leftist policies.

It’s a great irony that the Left, which purports to support the poor and working people, would propose a form of government finance that is so regressive in its effects. To be generous, perhaps it’s just another case of “progressives” unknowingly hurting the ones they love. The expansive programs they advocate will confer government benefits to many individuals in higher income brackets, not just the poor, but those government alms will help to compensate for higher inflation. But this too takes advantage of money illusion, because those benefits might well buy progressives the loyalty of beneficiaries unable to recognize the ongoing erosion in their standard of living, and who are unwilling to come to grips with their increasing dependency.

But Tut, Tut, They Say

Advocates of MMT, in combination with expansive government, also have a tendency to deny that inflation has ever been a consequence of such policies. As Sumner points out, they have forgotten historical episodes that run contrary to the theory, and most “popular” advocates of MMT fail to recognize the important role played by limits on the economy’s production potential. When money growth outruns the economy’s ability to produce real goods and services, the prices of goods will rise.

Happy with the government’s management of the pandemic? Happy with how much government grew during the pandemic? How well do you think governments would manage our realization that we have nearby extraterrestrial observers? It’s hard to know what that would mean for our future, but such a presence could well pose a singular menace to humanity. It might ignite panic, to say nothing of the bedlam that would ensue with the actual ingress of extraterrestrials or their intelligent machinery.

How would governments handle it? If the pandemic is any guide, my guess is they would follow the authoritarian impulse. For our own safety, that is. Hoarding and shortages of key goods might ensue. Curfews and stay-at-home orders would be seen as a way to limit civil disorder. Depending on the perceived threat, draconian measures such as limiting the use of electronics and communication devices might be considered. No telling what might seem appropriate to political leaders, but a military component to the response is much more likely than under a pandemic, and not just because of the external threat.

Let’s assume we’re talking about observers, not battalions of landing parties. A lot would depend on what’s known about them, or more specifically what the government knows. Why are they probing our atmosphere? Why are they studying our planet and our civilization? Are they waiting for a larger force to arrive? Can their machines self-replicate using resources mined from elsewhere in the solar system? Of course, the reaction of the public depends on how the government characterizes the presence of our observers. That gap in knowledge is of great concern.

But let’s take a step back. Is it real? We know the pandemic was “real”, but many question its true severity and the appropriateness of stringent non-pharmaceutical interventions, including yours truly. Some would say the government’s response was opportunistic, calibrated to force a change in political leadership, and calibrated to transform the role of government in our lives as well as attitudes about that role. Now imagine the opportunity for even more drastic change in the role of government given the prospect of an intersection with a potentially grabby alien civilization!

Like many others, I am fascinated by the possibility of life beyond our planet. Discussions of the Drake equation and the Fermi paradox are like candy to me. UFO sightings are always a matter of curiosity, except now we’re learning to call them “unexplained aerial phenomena” (UAPs) under guidance from government and military authorities. Lately, we’re hearing a lot about UAPs observed and filmed by military aircraft and detected by other forms of telemetry. These admissions are considered a sea change in the government’s attitude toward sharing sensitive, and possibly socially disruptive, information with the public. By June 1, a large batch of information on additional UAP sightings is due to be released under the Intelligence Authorization Act of 2021, which was signed into law by President Trump in December.

I’m as curious as anyone, but there are many reasons to be skeptical about UAP sightings, at least insofar as entertaining the possibility that these are extraterrestrial beings or machines. For example, there are natural (and technical) explanations for the images seen in the Navy videos. But some have speculated that these are sightings of top-secret technologies developed by an agency of the federal government such as the Defense Advanced Research Project Agency (DARPA). A former Pentagon UFO Program Chief dismisses that as improbable. Well, if you say so. Another possibility is that a foreign government has leaped far ahead of the U.S. in the science of flight. That would be threatening to U.S. security, though perhaps not as threatening as the machinery of an interstellar expeditionary force.

Whether the potential threat is an intersection with extraterrestrials or simply advanced technology possessed by an earthbound adversary, might it be in the interests of certain factions to promote our vulnerability? Or to manufacture evidence of such a vulnerability? Forgive my tin-foil hat, but I think the answer is yes. For example, it would be an opportunity for the defense establishment to garner more funding. It’s also a potential opportunity for those who wish to impose a more authoritarian order. There is always something to be gained from potential threats, so much so that major segments of our society seem to thrive on them. But is that what’s happening?

Defense funding is one thing, but the kinds of threats in question might call for widespread actions on public safety at all levels of government. Federal funding will be required to meet these needs, after all, and only the federal government can print money to create the means of competing for resources with the private sector. This is consistent with other federal initiatives that, beyond their stated public purposes, seem almost designed to eviscerate the power of state and local governments:

“The plan to federalize government is already moving and has three parts:

Flood every unit of local government with federal cash, irrespective of need, while prohibiting tax cuts, thereby bailing out failing states and cities.

Make that flood of federal money made regular and permanent.

Annul or override state laws that make certain states competitive, thereby eliminating their competitive advantages, and federalize elections to make it all permanent.”

The third point has as much relevance in the context of any threat to our security as did the pandemic. Once lower levels of government are dependent on federal funds, there is little they can do to resist federal demands. The more credible the threat of an incursion by an extraterrestrial or foreign force with awesome technological power, the more likely are voters to accept expansive programs to enhance their safety, including assistance to lower levels of government for providing various forms of local protection … the federal way.

The pandemic did little to promote faith in the government’s ability to manage a crisis. Nevertheless, look no further than the federal budget explosion induced by the pandemic for evidence that advocates of expansive government did not let the crisis go to waste. Will they want new crises? I’m sure they will. There’s certainly a possibility that a drummed-up threat from UAP’s would be a candidate down the road. It might need a little more percolation, but make no mistake: it has potential value to statists.

I still prefer to call them UFOs, and it’s still fun to think about them, but if they’re “real”, or even if they belong to a foreign power, we might be in big trouble. If they’re not “real”, our own state actors might toy with us enough to make us wish we’d never heard of UFOs.

In advanced civilizations the period loosely called Alexandrian is usually associated with flexible morals, perfunctory religion, populist standards and cosmopolitan tastes, feminism, exotic cults, and the rapid turnover of high and low fads---in short, a falling away (which is all that decadence means) from the strictness of traditional rules, embodied in character and inforced from within. -- Jacques Barzun

{kind=link}