Tags

Alexandria Ocasio-Cortez, Bernie Sanders, Build Back Better, Child Tax Credit, Congressional Budget Office, Deficits, Federal Reserve, Fiscal policy, Fiscal Theory of the Price Level, Helicopter Drop, Inflation tax, infrastructure, Joe Biden, John Cochrane, Median CPI, Modern Monetary Theory, Monetary policy, Pandemic Relief, Seigniorage, Stimulus Payments, Student Loans, Surpluses, Trimmed CPI, Universal Basic Income

I’ll get to the weird trick right off the bat. Then you can read on if you want. The trick really is perverse if you believe in principles of sound credit and financial stability. To levy a fiscal inflation tax, all the government need do is spend like a drunken sailor and undermine its own credibility as a trustworthy borrower. One way to do that: adopt the policy prescriptions of Modern Monetary Theory (MMT).

A Theory of Deadbeat Government

That’s right! Run budget deficits and convince investors the debt you float will never be repaid with future real surpluses. That doesn’t mean the government would literally default (though that is never outside the realm of possibility). However, given such a loss of faith, something else must give, because the real value government debt outstanding will exceed the real value of expected future surpluses from which to pay that debt. The debt might be in the form of interest-bearing government bonds or printed money: it’s all government debt. Ultimately, under these circumstances, there will be a revised expectation that the value of that debt (bonds and dollars) will be eroded by an inflation tax.

This is a sketch of “The Fiscal Theory of the Price Level” (FTPL). The link goes to a draft of a paper by John Cochrane, which he intends as an introduction and summary of the theory. He has been discussing and refining this theory for many years. In fairness to him, it’s a draft. There are a few passages that could be written more clearly, but on the whole, FTPL is a useful way of thinking about fiscal issues that may give rise to inflation.

Fiscal Helicopters

Cochrane discusses the old allegory about how an economy responds to dollar bills dropped from a helicopter — free money floating into everyone’s yard! The result is the classic “too much money chasing too few goods” problem, so dollar prices of goods must rise. We tend to think of the helicopter drop as a monetary policy experiment, but as Cochrane asserts, it is fiscal policy.

We have experienced something very much like the classic helicopter drop in the past two years. The federal government has effectively given money away in a variety of pandemic relief efforts. Our central bank, the Federal Reserve, has monetized much of the debt the Treasury issued as it “loaded the helicopter”.

In effect, this wasn’t an act of monetary policy at all, because the Fed does not have the authority to simply issue new government debt. The Fed can buy other assets (like government bonds) by issuing dollars (as bank reserves). That’s how it engineers increases in the money supply. It can also “lend” to the U.S. Treasury, crediting the Treasury’s checking account. Presto! Stimulus payments are in the mail!

This is classic monetary seigniorage, or in more familiar language, an inflation tax. Here is Cochrane description of the recent helicopter drop:

“The Fed and Treasury together sent people about $6 trillion, financed by new Treasury debt and new reserves. This cumulative expansion was about 30% of GDP ($21,481) or 38% of outstanding debt ($16,924). If people do not expect that any of that new debt will be repaid, it suggests a 38% price-level rise. If people expect Treasury debt to be repaid by surpluses but not reserves, then we still expect $2,506 / $16,924 = 15% cumulative inflation.”

FTPL, May I Introduce You To MMT

Another trend in thought seems to have dovetailed with the helicopter drop , and it may have influenced investor sentiment regarding the government’s ever-weakening commitment to future surpluses: that would be the growing interest in MMT. This “theory” says, sure, go ahead! Print the money government “must” spend. The state simply fesses-up, right off the bat, that it has no intention of running future surpluses.

To be clear, and perhaps more fair, economists who subscribe to MMT believe that deficits financed with money printing are acceptable when inflation and interest rates are very low. However, expecting stability under those circumstances requires a certain level of investor confidence in the government fisc. Read this for Cochrane’s view of MMT.

Statists like Bernie Sanders, Alexandria Ocasio-Cortez, and seemingly Joe Biden are delighted to adopt a more general application of MMT as intellectual cover for their grandiose plans to remake the economy, fix the climate, and expand the welfare state. But generalizing MMT is a dangerous flirtation with inflation denialism and invites economic disaster.

If This Goes On…

Amid this lunacy we have Joe Biden and his party hoping to find avenues for “Build Back Better”. Fortunately, it’s looking dead at this point. The bill considered in the fall would have amounted to an additional $2 trillion of “infrastructure” spending, mostly not for physical infrastructure. Moreover, according to the Congressional Budget Office, that bill’s cost would have far exceeded $2 trillion by the time all was said and done. There are ongoing hopes for separate passage of free community college, an extended child tax credit for all families, a higher cap for state and local income tax deductions, and a host of other social and climate initiatives. The latter, relegated to a separate bill, is said to carry a price tag of over $550 billion. In addition, the Left would still love to see complete forgiveness of all student debt and institute some form of universal basic income. Hey, just print the money, right? Warm up the chopper! But rest easy, cause all this appears less likely by the day.

Are there possible non-inflationary outcomes from ongoing helicopter drops that are contingent on behavior? What if people save the fresh cash because it’s viewed as a one-time windfall (i.e., not a permanent increase in income)? If you sit on such a windfall it will erode as prices rise, and the change in expectations about government finance won’t be too comforting on that score.

There are many aspects of FTPL worth pondering, such as whether bond investors would be very troubled by yawning deficits with MMT noisemakers in Congress IF the Fed refused to go along with it. That is, no money printing or debt monetization. The burgeoning supply of debt would weigh heavily on the market, forcing rates up. Government keeps spending and interest costs balloon. It is here where Cochrane and critics of FTPL have a sharp disagreement. Does this engender inflation in the absence of debt monetization? Cochrane says yes if investors have faith in the unfaithfulness of fiscal policymakers. Excessive debt is then every bit as inflationary as printing money.

Real Shocks and FTPL

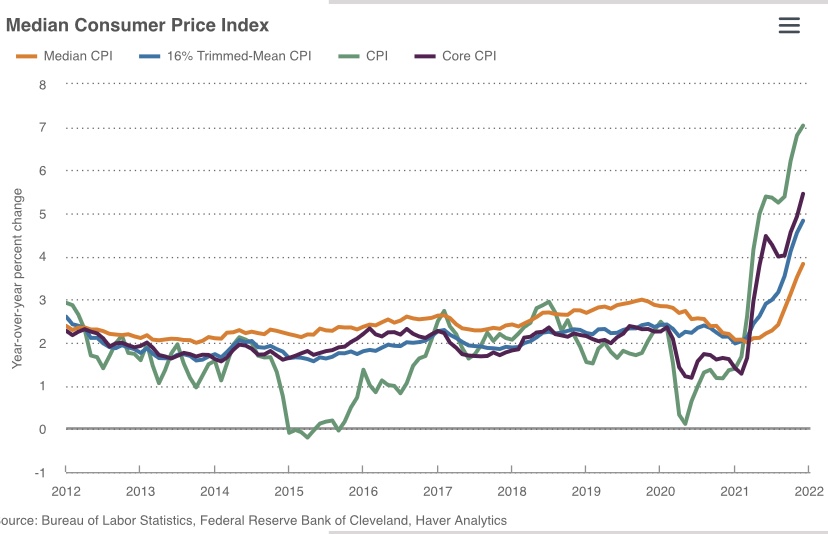

It’s natural to think supply disruptions are primarily responsible for the recent acceleration of inflation, rather than the helicopter drop. There’s no question about those price pressures in certain markets, much of it inflected by wayward policymakers, and some of those markets involve key inputs like energy and labor. Even the median component of the CPI has escalated sharply, though it has lagged broader measures a bit.

Broad price pressures cannot be sustained indefinitely without accommodating changes in the supply of money, which is the so-called “numeraire” in which all goods are priced. What does this have to do with FTPL or the government’s long-term budget constraint? The helicopter drop certainly led to additional money growth and spending, but again, FTPL would say that inflation follows from the expectation that government will not produce future surpluses needed for long-term budget balance. The creation of either new money or government debt, loaded the chopper as it were, is sufficient to accommodate broad price pressures over some duration.

Conclusion

Whether or not FTPL is a fully accurate description of fiscal and monetary phenomena, few would argue that a truly deadbeat government is a prescription for hyperinflation. That’s an extreme, but the motivation for FTPL is the potential abandonment of good and honest governing principles. Pledging an inflation tax is not exactly what anyone means by the full faith and credit of the U.S. government.

Pingback: Social Insurance, Trust Fund Runoff, and Federal Debt | Sacred Cow Chips

Pingback: Demand, Disinflation, and Fed Gradualism | Sacred Cow Chips