I’ll try to keep this one short. I was starting a post on another topic when Donald Trump distracted me… again. This time it was the $2,000 per person “tariff dividend” he’s proposed. This would be paid to all low- and middle-income Americans starting in mid-2026. As if the federal government was a profitable enterprise. Obviously that’s the wrong model! This is either sheer stupidity or willful government failure. Sure, the Fed can just print money, so why not? Who knew Trump was a closet modern monetary theorist?

It’s such a bad idea…. Tariffs themselves are bad enough. They are taxes, of course, a truth about which Trump and his central trade planners have denied since the beginning of the escapade. Tariffs hurt consumers and businesses who import inputs. Tariffs retard growth by increasing input costs, disrupting supply chains, and raising the prices of not only imports, but also domestically-produced goods that compete with imports. Surely Trump knows all this and the implications for his political capital: he’s already backtracking on tariffs for certain food items.

The tariff dividend is a transparent attempt to compensate consumers for the harms of taxation. It’s also a transparent attempt to buy or keep votes, much as he’s already sought to buy-off farmers harmed by tariffs. The income limit for the dividend hasn’t been announced, but make no mistake: this represents another form of redistribution.

It’s also striking that the tariffs won’t generate nearly as much revenue as will be required to begin paying the dividend by mid-2026. In fact, it could be short by as much as $300 million! Will the Treasury borrow the rest? More pressure on the bond market and interest rates.

Furthermore, the so-called dividend would be inflationary if the Federal Reserve fails to neutralize it. It would amount to another “helicopter drop” of cash, similar to the cash dump from Covid relief payments: money printing under the guise of fiscal policy.

To the extent that tariff revenue flows, it should be used to reduce the federal deficit or to pay down the gigantic government debt already outstanding ($38 trillion today not including the impending cost of funding entitlement programs). Instead, Trump is proudly following in the footsteps of generations of spendthrift politicians.

Keep in mind that the dividend is a promise Trump might not be able to keep. The Supreme Court will soon announce its decision on presidential power to impose tariffs. This decision will bear on the president’s authority under the International Emergency Economic Powers Act (IEEPA) — if and when an actual emergency is at hand, which it clearly is not. More broadly, the decision hinges on whether a “foreign facing” tax falls within the president’s Article II powers under the Constitution.

The proposed tariff dividend undermines the Administration’s argument before the Court that tariffs are primarily regulatory tools, and that any revenue from tariffs is merely incidental. Thank God the dividend would have to be authorized by Congress! I truly hope there are enough sensible legislators on the Hill to beat back this idiocy.

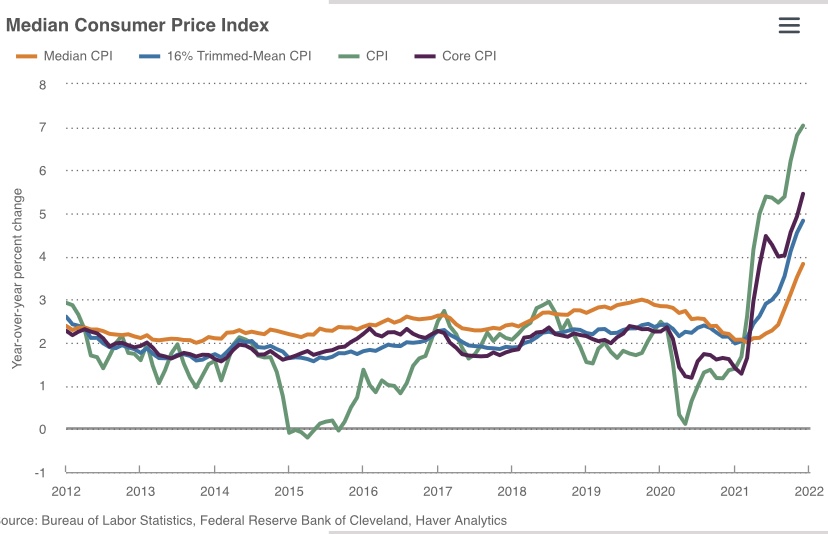

The Fed’s “higher for longer” path for short-term interest rates lingers on, and so does inflation in excess of the Fed’s 2% target. No one should be surprised that rate cuts aren’t yet on the table, but the markets freaked out a little with the release of the February CPI numbers last week, which were higher than expected. For now, it only means the Fed will remain patient with the degree of monetary restraint already achieved.

Dashed Hopes

As I’ve said before, there was little reason for the market to have expected the Fed to cut rates aggressively this year. Just a couple of months ago, the market expected as many as six quarter-point cuts in the Fed’s target for the federal funds rate. The only rationale for that reaction would have been faster disinflation or the possibility of an economic “hard landing”. A downturn is not out of the question, especially if the Fed feels compelled to raise its rate target again in an effort to stem a resurgence in inflation. Maybe some traders felt the Fed would act politically, cutting rates aggressively as the presidential election approaches. Not yet anyway, and it seems highly unlikely.

There is no assurance that the Fed can succeed in engineering a “soft landing”, i.e., disinflation to its 2% goal without a recession. No one can claim any certainty on that point — it’s too early to call, though the odds have improved somewhat. As Scott Sumner succinctly puts it, a soft landing basically depends on whether the Fed can disinflate gradually enough.

It’s a Demand-Side Inflation

I’d like to focus a little more on Sumner’s perspective on Fed policy because it has important implications for the outlook. Sumner is a so-called market monetarist and a leading proponent of nominal GDP level targeting by the Fed. He takes issue with those ascribing the worst of the pandemic inflation to supply shocks. There’s no question that disruptions occurred on the supply side, but the Fed did more than accommodate those shocks in attempting to minimize their impact on real output and jobs. In fact, it can fairly be said that a Fed / Treasury collaboration managed to execute the biggest “helicopter drop” of money in the history of the world, by far!

That “helicopter drop” consisted of pandemic relief payments, a fiscal maneuver amounting to a gigantic monetary expansion and stimulus to demand. The profligacy has continued on the fiscal side since then, with annual deficits well in excess of $1 trillion and no end in sight. This reflects government demand against which the Fed can’t easily act to countervail, making the job of achieving a soft landing that much more difficult.

The Treasury, however, is finding a more limited appetite among investors for the flood of bonds it must regularly sell to fund the deficit. Recent increases in long-term Treasury rates reflect these large funding needs as well as the “higher-for-longer” outlook for short-term rates, inflation expectations, and of course better perceived investment alternatives.

The Nominal GDP Proof

There should be no controversy that inflation is a demand-side problem. As Summer says, supply shocks tend to reverse themselves over time, and that was largely the case as the pandemic wore on in 2021. Furthermore, advances in both real and nominal GDP have continued since then. The difference between the two is inflation, which again, has remained above the Fed’s target.

So let’s see… output and prices both growing? That combination of gains demonstrates that demand has been the primary driver of inflation for three-plus years. Restrictive monetary policy is the right prescription for taming excessive demand growth and inflation.

Here’s Sumner from early March (emphasis his), where he references flexible average inflation targeting (FAIT), a policy the Fed claims to be following, and nominal GDP level targeting (NGDPLT):

“Over the past 4 years, the PCE price index is up 16.7%. Under FAIT it should have risen by 8.2% (i.e., 2%/year). Thus we’ve had roughly 8.5% excess inflation (a bit less due to compounding.)

Aggregate demand (NGDP) is up by 27.6%. Under FAIT targeting (which is similar to NGDPLT) it should have been up by about 17% (i.e., 4%/year). So we’ve had a bit less than 10.6% extra demand growth. That explains all of the extra inflation.”

Is Money “Tight”?

The Fed got around to tightening policy in the spring of 2022, but that doesn’t necessarily mean that policy ever advanced to the “tight” stage. Sumner has been vocal in asserting that the Fed’s policy hasn’t looked especially restrictive. Money growth feeds demand and ultimately translates into nominal GDP growth (aggregate demand). The latter is growing too rapidly to bring inflation into line with the 2% target. But wait! Money growth has been moderately negative since the Fed began tightening. How does that square with Sumner’s view?

In fact, the M2 money supply is still approximately 35% greater than at the start of the pandemic. There’s still a lot of M2 sloshing around out there, and the Fed’s portfolio of securities acquired during the pandemic via “quantitative easing” remains quite large ($7.5 trillion). Does this sound like tight money?

Again, Sumner would say that with nominal GDP ripping ahead at 5.7%, the Fed can’t be credibly targeting 2% inflation given an allowance for real GDP growth at trend of around 1.8% (or even somewhat greater than that). It’s an even bigger stretch if M2 velocity (V — turnover) continues to rebound with higher interest rates.

Wage growth also exceeds a level consistent with the Fed’s target. The chart below shows the gap between price inflation and wage inflation that left real wages well below pre-pandemic levels. Since early 2023, wages have made up part of that decline, but stubborn wage inflation can impede progress against price inflation.

Just Tight Enough?

Despite Sumner’s doubts, there are arguments to be made that Fed policy qualifies as restrictive. Even moderate declines in liquidity can come as a shock to markets grown accustomed to torrents from the money supply firehose. And to the extent that inflation expectations have declined, real interest rates may be higher now than they were in early November. In any case, it’s clear the market was disappointed in the higher-than-expected CPI, and traders were not greatly assuaged by the moderate report on the PPI that followed.

However, the Fed pays closest attention to another price index: the core deflator for personal consumption expenditures (PCE). Inflation by this measure is trending much closer to the Fed’s target (see the second chart below). Still, from the viewpoint of traders, many of whom, not long ago, expected six rate cuts this year, the reality of “higher for longer” is a huge disappointment.

Danger Lurks

As I noted, many believe the odds of a soft landing have improved. However, the now-apparent “stickiness” of inflation and the knowledge that the Fed will standby or possibly hike rates again has rekindled fears that the economy could turn south before the Fed elects to cut its short-term interest rate target. That might surprise Sumner in the absence of more tightening, as his arguments are partly rooted in the continuing strength of aggregate demand and nominal GDP growth.

There’s a fair degree of consensus that the labor market remains strong, which underscores Sumner’s doubts as to the actual tenor of monetary policy. The March employment numbers were deceptive, however. The gain in civilian employment was just shy of 500,000, but that gain was entirely in part-time employment. Full-time employment actually declined slightly. In fact, the same is true over the prior 12 months. And over that period, the number of multiple jobholders increased by more than total employment. Increasing reliance on part-time work and multiple jobs is a sign of stress on household budgets and that firms may be reluctant to commit to full-time hires. From the establishment survey, the gain in nonfarm employment was dominated once again by government and health care. These numbers hardly support the notion that the economy is on solid footing.

There are other signs of stress: credit card delinquencies hit an all-time high in February. High interest rates are taking a toll on households and business borrowers. Retail sales were stronger than expected in March, but excess savings accumulated during the pandemic were nearly depleted as of February, so it’s not clear how long the spending can last. And while the index of leading indicators inched up in February, it was the first gain in two years and the index has shown year/over-year declines over that entire two-year period.

Conclusion

It feels a little hollow for me to list a series of economic red flags, having done so a few times over the past year or so. The risks of a hard landing are there, to be sure. The behavior of the core PCE deflator over the next few months will have much more influence on the Fed policy, as would any dramatic changes in the real economy. The “data dependence” of policy is almost a cliche at this point. The Fed will stand pat for now, and I doubt the Fed will raise its rate target without a dramatic upside surprise on the core deflator. Likewise, any downward rate moves won’t be forthcoming without more softening in the core deflator toward 2% or definitive signs of a recession. So rate cuts aren’t likely for some months to come.

I’ll get to the weird trick right off the bat. Then you can read on if you want. The trick really is perverse if you believe in principles of sound credit and financial stability. To levy a fiscal inflation tax, all the government need do is spend like a drunken sailor and undermine its own credibility as a trustworthy borrower. One way to do that: adopt the policy prescriptions of Modern Monetary Theory (MMT).

A Theory of Deadbeat Government

That’s right! Run budget deficits and convince investors the debt you float will never be repaid with future real surpluses. That doesn’t mean the government would literally default (though that is never outside the realm of possibility). However, given such a loss of faith, something else must give, because the real value government debt outstanding will exceed the real value of expected future surpluses from which to pay that debt. The debt might be in the form of interest-bearing government bonds or printed money: it’s all government debt. Ultimately, under these circumstances, there will be a revised expectation that the value of that debt (bonds and dollars) will be eroded by an inflation tax.

This is a sketch of “The Fiscal Theory of the Price Level” (FTPL). The link goes to a draft of a paper by John Cochrane, which he intends as an introduction and summary of the theory. He has been discussing and refining this theory for many years. In fairness to him, it’s a draft. There are a few passages that could be written more clearly, but on the whole, FTPL is a useful way of thinking about fiscal issues that may give rise to inflation.

Fiscal Helicopters

Cochrane discusses the old allegory about how an economy responds to dollar bills dropped from a helicopter — free money floating into everyone’s yard! The result is the classic “too much money chasing too few goods” problem, so dollar prices of goods must rise. We tend to think of the helicopter drop as a monetary policy experiment, but as Cochrane asserts, it is fiscal policy.

We have experienced something very much like the classic helicopter drop in the past two years. The federal government has effectively given money away in a variety of pandemic relief efforts. Our central bank, the Federal Reserve, has monetized much of the debt the Treasury issued as it “loaded the helicopter”.

In effect, this wasn’t an act of monetary policy at all, because the Fed does not have the authority to simply issue new government debt. The Fed can buy other assets (like government bonds) by issuing dollars (as bank reserves). That’s how it engineers increases in the money supply. It can also “lend” to the U.S. Treasury, crediting the Treasury’s checking account. Presto! Stimulus payments are in the mail!

This is classic monetary seigniorage, or in more familiar language, an inflation tax. Here is Cochrane description of the recent helicopter drop:

“The Fed and Treasury together sent people about $6 trillion, financed by new Treasury debt and new reserves. This cumulative expansion was about 30% of GDP ($21,481) or 38% of outstanding debt ($16,924). If people do not expect that any of that new debt will be repaid, it suggests a 38% price-level rise. If people expect Treasury debt to be repaid by surpluses but not reserves, then we still expect $2,506 / $16,924 = 15% cumulative inflation.”

FTPL, May I Introduce You To MMT

Another trend in thought seems to have dovetailed with the helicopter drop , and it may have influenced investor sentiment regarding the government’s ever-weakening commitment to future surpluses: that would be the growing interest in MMT. This “theory” says, sure, go ahead! Print the money government “must” spend. The state simply fesses-up, right off the bat, that it has no intention of running future surpluses.

To be clear, and perhaps more fair, economists who subscribe to MMT believe that deficits financed with money printing are acceptable when inflation and interest rates are very low. However, expecting stability under those circumstances requires a certain level of investor confidence in the government fisc. Read this for Cochrane’s view of MMT.

Statists like Bernie Sanders, Alexandria Ocasio-Cortez, and seemingly Joe Biden are delighted to adopt a more general application of MMT as intellectual cover for their grandiose plans to remake the economy, fix the climate, and expand the welfare state. But generalizing MMT is a dangerous flirtation with inflation denialism and invites economic disaster.

If This Goes On…

Amid this lunacy we have Joe Biden and his party hoping to find avenues for “Build Back Better”. Fortunately, it’s looking dead at this point. The bill considered in the fall would have amounted to an additional $2 trillion of “infrastructure” spending, mostly not for physical infrastructure. Moreover, according to the Congressional Budget Office, that bill’s cost would have far exceeded $2 trillion by the time all was said and done. There are ongoing hopes for separate passage of free community college, an extended child tax credit for all families, a higher cap for state and local income tax deductions, and a host of other social and climate initiatives. The latter, relegated to a separate bill, is said to carry a price tag of over $550 billion. In addition, the Left would still love to see complete forgiveness of all student debt and institute some form of universal basic income. Hey, just print the money, right? Warm up the chopper! But rest easy, cause all this appears less likely by the day.

Are there possible non-inflationary outcomes from ongoing helicopter drops that are contingent on behavior? What if people save the fresh cash because it’s viewed as a one-time windfall (i.e., not a permanent increase in income)? If you sit on such a windfall it will erode as prices rise, and the change in expectations about government finance won’t be too comforting on that score.

There are many aspects of FTPL worth pondering, such as whether bond investors would be very troubled by yawning deficits with MMT noisemakers in Congress IF the Fed refused to go along with it. That is, no money printing or debt monetization. The burgeoning supply of debt would weigh heavily on the market, forcing rates up. Government keeps spending and interest costs balloon. It is here where Cochrane and critics of FTPL have a sharp disagreement. Does this engender inflation in the absence of debt monetization? Cochrane says yes if investors have faith in the unfaithfulness of fiscal policymakers. Excessive debt is then every bit as inflationary as printing money.

Real Shocks and FTPL

It’s natural to think supply disruptions are primarily responsible for the recent acceleration of inflation, rather than the helicopter drop. There’s no question about those price pressures in certain markets, much of it inflected by wayward policymakers, and some of those markets involve key inputs like energy and labor. Even the median component of the CPI has escalated sharply, though it has lagged broader measures a bit.

Broad price pressures cannot be sustained indefinitely without accommodating changes in the supply of money, which is the so-called “numeraire” in which all goods are priced. What does this have to do with FTPL or the government’s long-term budget constraint? The helicopter drop certainly led to additional money growth and spending, but again, FTPL would say that inflation follows from the expectation that government will not produce future surpluses needed for long-term budget balance. The creation of either new money or government debt, loaded the chopper as it were, is sufficient to accommodate broad price pressures over some duration.

Conclusion

Whether or not FTPL is a fully accurate description of fiscal and monetary phenomena, few would argue that a truly deadbeat government is a prescription for hyperinflation. That’s an extreme, but the motivation for FTPL is the potential abandonment of good and honest governing principles. Pledging an inflation tax is not exactly what anyone means by the full faith and credit of the U.S. government.

Should government actively manipulate asset prices in an effort to “manage ” economic growth? The world’s central bankers, otherwise at their wit’s end, are attempting just that. Hopes have been pinned on so-called quantitative easing (QE), which simply means that central banks like the U.S. Federal Reserve (the Fed) buy assets (government and private bonds) from the public to inject newly “printed” money into the economy. The Fed purchased $4.5 trillion of assets between the last financial crisis and late 2014, when it ended its QE. Other central banks are actively engaged in QE, however, and there are still calls from some quarters for the Fed to resume QE, despite modest but positive economic growth. The goals of QE are to drive asset prices up and interest rates down, ultimately stimulating demand for goods and economic growth. Short-term rates have been near zero in many countries (and in the U.S. until December), and negative short-term interest rates are a reality in the European Union, Japan and Sweden.

Does anyone really have to pay money to lend money, as indicated by a negative interest rate? Yes, if a bank “lends” to the Bank of Japan, for example, by holding reserves there. The BOJ is currently charging banks for the privilege. But does anyone really “earn” negative returns on short-term government or private debt? Not unless you buy a short-term bill and hold it till maturity. Central banks are buying those bills at a premium, usually from member banks, in order to execute QE, and that offsets a negative rate. But the notion is that when these “captive” member banks are penalized for holding reserves, they will be more eager to lend to private borrowers. That may be, but only if there are willing, credit-worthy borrowers; unfortunately, those are scarce.

Thus far, QE and zero or negative rates do not seem to be working effectively, and there are several reasons. First, QE has taken place against a backdrop of increasingly binding regulatory constraints. A private economy simply cannot flourish under such strictures, with or without QE. Moreover, government makes a habit of manipulating investment decisions, partly through regulatory mandates, but also by subsidizing politically-favored activities such as ethanol, wind energy, post-secondary education, and owner-occupied housing. This necessarily comes at the sacrifice of opportunities for physical investment that are superior on economic merits.

The most self-defeating consequence of QE and rate manipulation, be that zero interest rate policy (ZIRP) or negative interest rate policy (NIRP), is the distortion of inter-temporal tradeoffs that guide decisions to save and invest in productive assets. How, and how much, should individuals save when returns on relatively safe assets are very low? Most analysts would conclude that very low rates prompt a strong substitution effect toward consuming more today and less in the future. However, the situation may well engender a strong “income effect”, meaning that more must be saved (and less consumed in the present) in order to provide sufficient resources in the future. The paradox shouldn’t be lost on central bankers, and it may undermine the stimulative effects of ZIRP or NIRP. It might also lead to confusion in the allocation of productive capital, as low rates could create a mirage of viability for unworthy projects. Central bank intervention of this sort is disruptive to the healthy transformation of resources across time.

Savers might hoard cash to avoid a negative return, which would further undermine the efficacy of QE in creating monetary stimulus. This is at the root of central bank efforts to discourage the holding of currency outside of the banking system: the “war on cash“. (Also see here.) This policy is extremely offensive to anyone with a concern for protecting the privacy of individuals from government prying.

Another possible response for savers is to “reach for yield”, allocating more of their funds to high-risk assets than they would ordinarily prefer (e.g., growth funds, junk bonds, various “alternative” investments). So the supply of saving available for adding to the productive base in various sectors is twisted by central bank manipulation of interest rates. The availability of capital may be constrained for relatively safe sectors but available at a relative discount to risky sectors. This leads to classic malinvestment and ultimately business failures, displaced workers, and harsh adjustment costs.

With any luck, the Fed will continue to move away from this misguided path. Zero or negative interest rates imposed by central banks penalize savers by making the saving decision excessively complex and fraught with risk. Business investment is distorted by confusing signals as to risk preference and inflated asset prices. Central economic planning via industrial policy, regulation, and price controls, such as the manipulation of interest rates, always ends badly. Unfortunately, most governments are well-practiced at bungling in all of those areas.

In advanced civilizations the period loosely called Alexandrian is usually associated with flexible morals, perfunctory religion, populist standards and cosmopolitan tastes, feminism, exotic cults, and the rapid turnover of high and low fads---in short, a falling away (which is all that decadence means) from the strictness of traditional rules, embodied in character and inforced from within. -- Jacques Barzun

{kind=link}