Tags

Cash Offer, CATO Institute, COLA Indexing, Covid-19, David Beckworth, Donald Trump, Equity Returns, Eric Leeper, FICA Taxes, Fiscal Theory of Price Level, Francesco Bianchi, Government Budget Constraint, Heritability, John Cochrane, Means Testing, Michael Woodford, NBER, Old Age and Survivors Insuurance, Privatization, Sebastian Merkel, Social Security Administration, Spousal Benefits, TrumpIRA, Trust Fund

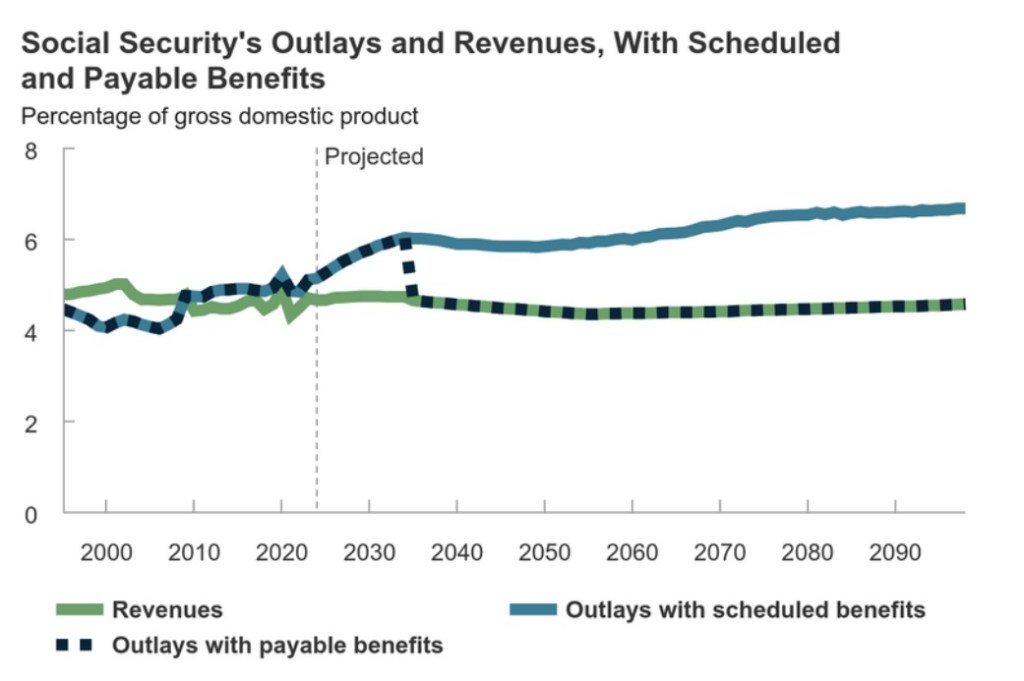

The 2026 report of the Board of Trustees of the Social Security Administration (SSA) says the retirement system’s official insolvency’s will occur in 2032Q4. This is the time at which the Old Age and Survivors Insurance (OASI) trust fund will be depleted, and it is a year earlier than SSA last projected. The disability income (DI) trust fund will last until 2034. The chart at the top combines the OASI and DI programs, so it shows a slightly later overall insolvency than OASI alone. Likewise, the theoretical benefit cuts shown in the chart are at the time of the combined insolvency, and they differ from mandated reductions in retirement benefits alone (22%).

Of course, the OASI and DI trust funds don’t really hold true “assets” for the federal government. Holdings consist of government bonds, which the SSA redeems with the Treasury Department to meet benefit obligations. In turn, Treasury must sell new bonds (borrow) to cover the SSA’s redemption. So the trust funds really only constitute additional Treasury “borrowing authority” on behalf of SSA.

Do Something!

Again, by law, depletion of the OASI trust fund will trigger an automatic 22% reduction in benefits. Needless to say, no one wants to see that happen, but no one wants to face up to the problem through reforms, either. Still, the issue will have to be confronted soon enough. By then, of course, President Trump will be off the hook. However, it would certainly be better to get the ball rolling sooner rather than later. An earlier fix would probably require somewhat less draconian reforms. It also would avoid a last-minute, heated political debate, the outcome of which is likely to be a bad policy choice.

Here’s a good summary of possible reforms from the CATO Institute. These options could shore-up the social security system. They span raising the retirement age, tax increases, cuts to benefits/spousal benefits, adjusted benefit “bend points”, adjustments to COLA indexing, means testing, and even flat benefit levels. But even CATO doesn’t broach the topic of the deeper reform required by privatization or even self-directed investment choices.

Make Me An Offer

In this section I discuss the potential willingness of current and future beneficiaries to accept a lump sum cash offer. I’ll defer discussion of how those cash offers might be funded until a section below. In late 2024, I argued that many future beneficiaries would willingly accept a cash deposit today, all tax-deferred, of less than the actuarial value of their future benefits earned to-date (as calculated by SSA):

“Given that the balance remaining at death would be heritable, some individuals might be willing to accept an initial deposit less than the actuarial PV of the future SS benefits they’ve accumulated to-date (discounted at an internal rate of return equating future benefits “earned” to-date and contributions to-date). I also believe many individuals would willingly accept a lower initial deposit because they would gain some control over investment direction.

There is a long history of economic research investigating the reasons for low demand for annuities (akin to OASI benefits). Control over investment direction brings the opportunity to earn greater returns on “contributions” (FICA payroll taxes). While equity returns have their ups and downs, they generally exceed the returns “earned” by workers on Social Security. It’s pretty much a given that most people investing in 401(k)s would rather have their savings there than governed by SSA benefit formulas!

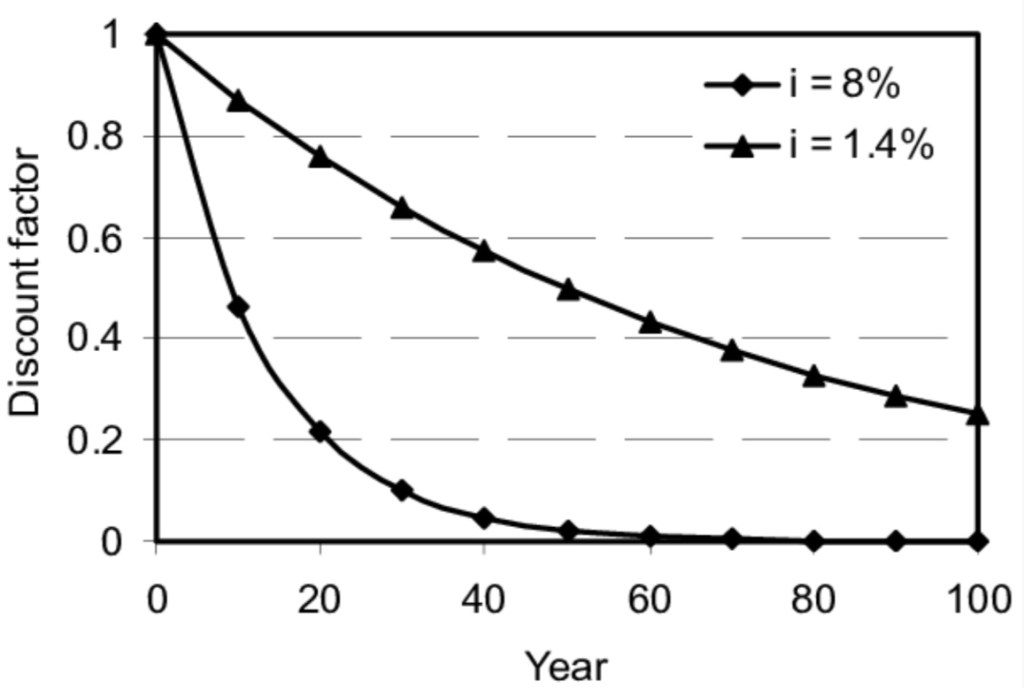

How can such a discounted cash offer be estimated? The actuarial PV of benefits at an appropriate discount rate geared to equity returns would be straightforward to calculate. Alternatively, trials on sample populations of retirees and active workers could be used to gauge uptake at various discounts. Later, trial participants could be given the option to keep their choice, to opt into whatever structure is finally adopted, or to revert to traditional benefits. The cash offer would almost certainly be worth more to future retirees, who have more time to earn superior returns at lower risk, than to current retirees.

Realistic Offers

A discount averaging 22% is well within the range of possibility in the aggregate, which would match the benefit cuts due in 2032 barring reform. This NBER paper found that many participants would accept a lump-sum at a 25% discount from actuarial value, while this paper found that non-retirees value their future benefits at a discount of 30%.

It’s likely that a number of beneficiaries will decline the cash offer out of conservatism, fear, or ignorance. Perhaps some will opt-in over time. But all indications are, from the annuity research, that most future retirees would accept an offer. So too might a significant number of current retirees, perhaps early in their retirement years, or who might highly value a chance to leave a bequest, or who might fear that poor health will limit the value of taking traditional SS benefits.

How To Fund Up-Front Payments

The upshot is that the availability of such a cash option would sharply reduce future benefit outlays. The rub is that the cash must be funded up-front. It would represent a huge addition to the government’s current borrowing needs, which sounds like an insurmountable obstacle to the success of the initiative. The fear is that immediate pressure on capital markets and interest rates could create an economic upheaval the likes of which we’ve never seen. More than anything else, the funding problem has led many to dismiss the possibility of privatization.

There is, however, an alternative view: the very reduction in the flow of future benefit obligations makes the plan more than feasible. That is because, in present value terms, the value of the reduction in future benefits would exceed the immediate borrowing necessary to pay the cash offers.

This reasoning is based on the government’s long-term budget constraint, which forces equality between the real value of government debt outstanding and the real present value of expected future government surpluses. Capital markets must value government debt on that basis, lest the debt’s value must be justified by a fiction.

The long-term budget constraint is central to the fiscal theory of the price level (FTPL). John Cochrane has written extensively on FTPL, and its adherents range from Eric Leeper, Michael Woodford, Sebastian Merkel, Francesco Bianchi, and to some degree David Beckworth.

Under the government budget constraint, a large increase in borrowing unaccompanied by any increase in future surpluses must leave the real value of debt outstanding unchanged. This happens because the real amount of debt is inflated away sufficiently or revalued as interest rates are bid upward.

In the case of a Social Security cash offer at a discount from actuarial present value, immediate borrowing should be more than offset by reductions in future SS benefit obligations. If financial markets find the future benefit reductions credible, there should be no upward pressure on interest rates or the price level. In fact, perhaps the opposite.

Of course, all this assumes that politicians possess fiscal discipline. Assuming they understand the gain in the government’s fiscal position, they cannot rush to commit to new programs, spending initiatives, or tax cuts that would sop up the increase in future surpluses (reduction in future deficits).

Trump Accounts

The Trump Administration has assiduously avoided serious discussion of SS reform. Instead, never missing a chance to stamp the Trump brand everywhere, the president has championed a “new” saving vehicle called TrumpIRA. It allows private workers without an employer-sponsored savings plan to establish an IRA account through the TrumpIRA web site. Qualified savers who establish such an account will be eligible for a $1,000 government matching contribution. So Trump has found another way to commit taxpayer resources that do not exist. Given our ongoing massive fiscal imbalance, you’d think his economic team might clue him in on a key lever that should be employed to increase national savings: deficit reduction! Instead, he’s busy subsidizing TrumpIRAs, Trump Baby Bonds, and plowing billions into government stakes in private companies.

The SS system itself, as it now exists, represents a huge disincentive to save. Privatization would sweep away those bad incentives, especially if the private accounts could be used for additional savings beyond existing FICA “contributions”. And access to those additional amounts saved should be open at any time, subject to a normal tax on withdrawal.

Summary

My earlier post on this topic contains much more detail on a voluntary privatization plan for Social Security, including potential risks. This is the sort of initiative that should be under discussion in policy-making circles. Sadly, the Administration doesn’t see any advantage in addressing SS reform at all, and other parties have dismissed privatization as a fiscal boondoggle. However, a substantial reduction in future benefit obligations would be more than sufficient to offset the short-term borrowing needed to offer cash to fund heritable, self-directed, private accounts at a discount from the actuarial present value of future benefits.