As of February 2026, I’m adding this short preamble to a few older posts on the subject of AI and future prospects for human labor. In the original post below (and a few others), I overstated the case that the law of comparative advantage would assure a continued role for humans in production. I still think the case is strong, mind you, but now I’m convinced that the outcome depends on elasticities of input substitution and how those elasticities might shift given the advent of AI-augmented capital. You can read my most recent thoughts on the matter here.

____________________________________________

Every now and then I grind my axe against the proposition that AI will put humans out of work. It’s a very fashionable view, along with the presumed need for government to impose “robot taxes” and provide everyone with a universal basic income for life. The thing is, I sense that my explanations for rejecting this kind of narrative have been a little abstruse, so I’m taking another crack at it now.

Will Human Workers Be Obsolete?

The popular account envisions a world in which AI replaces not just white-collar technocrats, but by pairing AI with advanced robotics, it replaces workers in the trades as well as manual laborers. We’ll have machines that cure, litigate, calculate, forecast, design, build, fight wars, make art, fix your plumbing, prune your roses, and replicate. They’ll be highly dextrous, strong, and smart, capable of solving problems both practical and abstract. In short, AI capital will be able to do everything better and faster than humans! The obvious fear is that we’ll all be out of work.

I’m here to tell you it will not happen that way. There will be disruptions to the labor market, extended periods of joblessness for some individuals, and ultimately different patterns of employment. However, the chief problem with the popular narrative is that AI capital will require massive quantities of resources to produce, train, and operate.

Even without robotics, today’s AIs require vast flows of energy and other resources, and that includes a tremendous amount of expensive compute. The needed resources are scarce and highly valued in a variety of other uses. We’ll face tradeoffs as a society and as individuals in allocating resources both to AI and across various AI applications. Those applications will have to compete broadly and amongst themselves for priority.

AI Use Cases

There are many high-value opportunities for AI and robotics, such as industrial automation, customer service, data processing, and supply chain optimization, to name a few. These are already underway to a significant extent. To that, however, we can add medical research, materials research, development of better power technologies and energy storage, and broad deployment in delivering services to consumers and businesses.

In the future, with advanced robotics, AI capital could be deployed in domains that carry high risks for human labor, such as construction of high rise buildings, underwater structures, and rescue operations. This might include such things as construction of solar platforms and large transports in space, or the preparation of space habitats for humans on other worlds.

Scarcity

There is no end to the list of potential applications of AI, but neither is there an end to the list of potential wants and aspirations of humanity. Human wants are insatiable, which sometimes provokes ham-fisted efforts by many governments to curtail growth. We have a long way to go before everyone on the planet lives comfortably. But even then, peoples’ needs and desires will evolve once previous needs are satisfied, or as technology changes lifestyles and practices. New approaches and styles drive fashions and aesthetics generally. There are always individuals who will compete for resources to experiment and to try new things. And the insatiability of human wants extends beyond the strictly private level. Everyone has an opinion about unsatisfied needs in the public sphere, such as infrastructure, maintenance, the environment, defense, space travel, and other dimensions of public activity.

Futurists have predicted that the human race will seek to become a so-called Type I civilization, capable of harnessing all of the energy on our planet. Then there will be the quest to harness all the energy within our solar system (a Type II civilization). Ultimately, we’ll seek to go beyond that by attempting to exploit all the energy in the Milky Way galaxy. Such an expansion of our energy demands would demonstrate how our wants always exceed the resources we have the ability to exploit.

In other words, scarcity will always be with us. The necessity of facing tradeoffs won’t ever be obviated, and prices will always remain positive. The question of dedicating resources to any particular application of AI will bring tradeoffs into sharper relief. The opportunity cost of many “lesser” AI and robotics applications will be quite high relative to their value to investors. Simply put, many of those applications will be rejected because there will be better uses for the requisite energy and other resources.

Tradeoffs

Again, it will be impossible for humans to accomplish many of the tasks that AI’s will perform, or to match the sheer productivity of AIs in doing so. Therefore, AI will have an absolute advantage over humans in all of those tasks.

However, there are many potential applications of AI that are of comparatively low value. These include a variety of low-skill tasks, but also tasks that require some dexterity or continuous judgement and adjustment. Operationalizing AI and robots to perform all these tasks, and diverting the necessary capital and energy away from other uses, would have a tremendously high opportunity cost. Human opportunity costs will not be so high. Thus, people will have a comparative advantage in performing the bulk if not all of these tasks.

Sure, there will be novelty efforts and test cases to train robots to do plumbing or install burglar alarm systems, and at some point buyers might wish to have robots prune their roses. Some people are already amenable to having humanoid robots perform sex work. Nevertheless, humans will remain competitive at these tasks due to the comparatively high opportunity costs faced by AI capital.

There will be many other domains in which humans will remain competitive. Once more, that’s because the opportunity costs for AI capital and other resources will be high. This includes many of the skilled trades, caregivers, and a great many management functions, especially at small companies. Their productivity will be enhanced by AI tools, but those jobs will not be decimated.

The key here is understanding that 1) capital and resources generally are scarce; 2) high value opportunities for AI are plentiful; and 3) the opportunity cost of funding AI in many applications will be very high. Humans will still have a comparative advantage in many areas.

Who’s the Boss?

There are still other ways in which human labor will always be required. One in particular involves the often complementary nature of AI and human inputs. People will have roles in instructing and supervising AIs, especially in tasks requiring customization and feedback. A key to assuring AI alignment with the objectives of almost any pursuit is human review. These kinds of roles are likely to be compensated in line with the complexity of the task. This extends to the necessity of human leadership of any organization.

That brings me to the subject of agentic and fully autonomous AI. No matter how sophisticated they get, AIs will always be the product of machines. They’ll be a kind of capital for which ownership should be confined to humans or organizations representing humans. We must be their masters. Disclaiming ownership and control of AIs, and granting agentic AIs the same rights and freedoms as people (as many have imagined) is unnecessary and possibly dangerous. AIs will do much productive work, but that work should be on behalf of human owners, and human labor will be deployed to direct and assess that work.

AIs (and People) Needing People

The collaboration between AIs and humans described above will manifest more broadly than anything task-specific, or anything we can imagine today. This is typical of technological advance. First-order effects often include job losses as new innovations enhance productivity or replace workers outright, but typically new jobs are created as innovations generate new opportunities for complementary products and services both upstream in production or downstream among ultimate users. In the case of AI, while much of this work might be performed by other AIs, at a minimum these changes will require guidance and supervision by humans.

In addition, consumers tend to have an aesthetic preference for goods and services produced by humans: craftsmen, artists, and entertainers. For example, if you’ve ever shopped for an oriental rug, you know that hand-knotted rugs are more expensive than machine-weaved rugs. Durability is a factor as well as uniqueness, the latter being a hallmark of human craftspeople. AI might narrow these differences over time, but the “human touch” will always have value relative to “comparable” AI output, even at a significant disadvantage in terms of speed and uncertainty regarding performance. The same is true of many other forms, such as sports, dance, music, and the visual arts. People prefer to be entertained by talented people, rather than highly-engineered machines. The “human touch” also has advantages in customer-facing transactions, including most forms of service and high-level sales/financial negotiations.

Owning the Machines

Finally, another word about AI ownership. An extension of the fashionable narrative that AIs will wholly replace human workers is that government will be called upon to tax AI and provide individuals with a universal basic income (UBI). Even if human labor were to be replaced by AIs, I believe that a “classic” UBI would be the wrong approach. Instead, all humans should have an ownership stake in the capital stock. This is wealth that yields compound growth over time and produces returns that make humans less reliant on streams of labor income.

Savings incentives (and negative consumption incentives) are a big step in encouraging more widespread ownership of capital. However, if direct intervention is necessary, early endowments of capital would be far preferable to a UBI because they will largely be saved, fostering economic growth, and they would create better incentives than a UBI. Along those lines, President Trump’s Big Beautiful Bill, which is now law, has established “Baby Bonds” for all American children born in 2025 – 2028, initially funded by the federal government with $1,000. Of course, this is another unfunded federal obligation on top of the existing burden of a huge public debt and ongoing deficits. Given my doubts about the persistence of AI-induced job losses, I reject government establishment of both a UBI and universal endowments of capital.

Summary

Capital and energy are scarce, so the tremendous resource requirements of AI and robotics means that the real world opportunity costs of many AI applications will remain impractically high. The tradeoffs will be so steep that they’ll leave humans with comparative advantages in many traditional areas of employment. Partly, these will come down to a difference in perceived quality owing to a preference for human interaction and human performance in a variety of economic interactions, including patronization of the art and athleticism of human beings. In addition, AIs will open up new occupations never before contemplated. We won’t be out of work. Nevertheless, it’s always a good idea to accumulate ownership in productive assets, including AI capital, and public policy should do a better job of supporting the private initiative to do so.

Artificial intelligence (AI) has become a very hot topic with incredible recent advances in AI performance. It’s very promising technology, and the expectations shown in thechart above illustrate what would be a profound economic impact. Like many new technologies, however, many find it threatening and are reacting with great alarm, There’s a movement within the tech industry itself, partly motivated by competitive self-interest, calling for a “pause”, or a six-month moratorium on certain development activities. Politicians in Washington are beginning to clamor for legislation that would subject AI to regulation. However, neither a voluntary pause nor regulatory action are likely to be successful. In fact, either would likely do more harm than good.

Leaps and Bounds

The pace of advance in AI has been breathtaking. From ChatGPT 3.5 to ChatGPT 4, in a matter of just a few months, the tool went from relatively poor performance on tests like professional and graduate entrance exams (e.g., bar exams, LSAT, GRE) to very high scores. Using these tools can be a rather startling experience, as I learned for myself recently when I allowed one to write the first draft of a post. (Despite my initial surprise, my experience with ChatGPT 3.5 was somewhat underwhelming after careful review, but I’ve seen more impressive results with ChatGPT 4). They seem to know so much and produce it almost instantly, though it’s true they sometimes “hallucinate”, reflect bias, or invent sources, so thorough review is a must.

Nevertheless, AIs can write essays and computer code, solve complex problems, create or interpret images, sounds and music, simulate speech, diagnose illnesses, render investment advice, and many other things. They can create subroutines to help themselves solve problems. And they can replicate!

As a gauge of the effectiveness of models like ChatGPT, consider that today AI is helping promote “over-employment”. That is, there are a number of ambitious individuals who, working from home, are holding down several different jobs with the help of AI models. In fact, some of these folks say AIs are doing 80% of their work. They are the best “assistants” one could possibly hire, according to a man who has four different jobs.

Economist Bryan Caplan is an inveterate skeptic of almost all claims that smack of hyperbole, and he’s won a series of bets he’s solicited against others willing to take sides in support of such claims. However, Caplan thinks he’s probably lost his bet on the speed of progress on AI development. Needless to say, it has far exceeded his expectations.

Naturally, the rapid progress has rattled lots of people, including many experts in the AI field. Already, we’re witnessing the emergence of “agency” on the part of AI Learning Language Models (LLMs), or so called “agentic” behavior. Here’s an interesting thread on agentic AI behavior. Certain models are capable of teaching themselves in pursuit of a specified goal, gathering new information and recursively optimizing their performance toward that goal. Continued gains may lead to an AI model having artificial generative intelligence (AGI), a superhuman level of intelligence that would go beyond acting upon an initial set of instructions. Some believe this will occur suddenly, which is often described as the “foom” event.

Team Uh-Oh

Concern about where this will lead runs so deep that a letter was recently signed by thousands of tech industry employees, AI experts, and other interested parties calling for a six-month worldwide pause in AI development activity so that safety protocols can be developed. One prominent researcher in machine intelligence, Eliezer Yudkowsky, goes much further: he believes that avoiding human extinction requires immediate worldwide limits on resources dedicated to AI development. Is this a severely overwrought application of the precautionary principle? That’s a matter I’ll consider at greater length below, but like Caplan, I’m congenitally skeptical of claims of impending doom, whether from the mouth of Yudkowsky, Greta Thunberg, Paul Ehrlich, or Nassim Taleb.

As I mentioned at the top, I suspect competition among AI developers played a role in motivating some of the signatories of the “AI pause” letter, and some of the non-signatories as well. Robin Hanson points out that Sam Altman, the CEO of OpenAI, did not sign the letter. OpenAI (controlled by a nonprofit foundation) owns ChatGPT and is the current leader in rolling out AI tools to the public. ChatGPT 4 can be used with the Microsoft search engine Bing, and Microsoft’s Bill Gates also did not sign the letter. Meanwhile, Google was caught flat-footed by the ChatGPT rollout, and its CEO signed. Elon Musk (who signed) wants to jump in with his own AI development: TruthGPT. Of course, the pause letter stirred up a number of members of Congress, which I suspect was the real intent. It’s reasonable to view the letter as a means of leveling the competitive landscape. Thus, it looks something like a classic rent-seeking maneuver, buttressed by the inevitable calls for regulation of AIs. However, I certainly don’t doubt that a number of signatories did so out of a sincere belief that the risks of AI must be dealt with before further development takes place.

The vast dimensions of the supposed AI “threat” may have some libertarians questioning their unequivocal opposition to public intervention. If so, they might just as well fear the potential that AI already holds for manipulation and control by central authorities in concert with their tech and media industry proxies. But realistically, broad compliance with any precautionary agreement between countries or institutions, should one ever be reached, is pretty unlikely. On that basis, a “scout’s honor” temporary moratorium or set of permanent restrictions might be comparable to something like the Paris Climate Accord. China and a few other nations are unlikely to honor the agreement, and we really won’t know whether they’re going along with it except for any traceable artifacts their models might leave in their wake. So we’ll have to hope that safeguards can be identified and implemented broadly.

Likewise, efforts to regulate by individual nations are likely to fail, and for similar reasons. One cannot count on other powers to enforce the same kinds of rules, or any rules at all. Putting our faith in that kind of cooperation with countries who are otherwise hostile is a prescription for ceding them an advantage in AI development and deployment. Regulation of the evolution of AI will likely fail. As Robert Louis Stevenson once wrote, “Thus paternal laws are made, thus they are evaded”. And if it “succeeds, it will leave us with a technology that will fall short of its potential to benefit consumers and society at large. That, unfortunately, is usually the nature of state intrusion into a process of innovation, especially when devised by a cadre of politicians with little expertise in the area.

Again, according to experts like Yudkowsky, AGI would pose serious risks. He thinks the AI Pause letter falls far short of what’s needed. For this reason, there’s been much discussion of somehow achieving an alignment between the interests of humanity and the objectives of AIs. Here is a good discussion by Seth Herd on the LessWrong blog about the difficulties of alignment issues.

Some experts feel that alignment is an impossibility, and that there are ways to “live and thrive” with unalignment (and see here). Alignment might also be achieved through incentives for AIs. Those are all hopeful opinions. Others insist that these models still have a long way to go before they become a serious threat. More on that below. Of course, the models do have their shortcomings, and current models get easily off-track into indeterminacy when attempting to optimize toward an objective.

But there’s an obvious question that hasn’t been answered in full: what exactly are all these risks?As Tyler Cowen has said, it appears that no one has comprehensively catalogued the risks or specified precise mechanisms through which those risks would present. In fact, AGI is such a conundrum that it might be impossible to know precisely what threats we’ll face. But even now, with deployment of AIs still in its infancy, it’s easy to see a few transition problems on the horizon.

White Collar Wipeout

Job losses seem like a rather mundane outcome relative to extinction. Those losses might come quickly, particularly among white collar workers like programmers, attorneys, accountants, and a variety of administrative staffers. According to a survey of 1,000 businesses conducted in February:

“Forty-eight percent of companies have replaced workers with ChatGPT since it became available in November of last year. … When asked if ChatGPT will lead to any workers being laid off by the end of 2023, 33% of business leaders say ‘definitely,’ while 26% say ‘probably.’ … Within 5 years, 63% of business leaders say ChatGPT will ‘definitely’ (32%) or ‘probably’ (31%) lead to workers being laid off.”

A rapid rate of adoption could well lead to widespread unemployment and even social upheaval. For perspective, that implies a much more rapid rate of technological diffusion than we’ve ever witnessed, so this outcome is viewed with skepticism in some quarters. But in fact, the early adoption phase of AI models is proceeding rather quickly. You can use ChatGPT 4 easily enough on the Bing platform right now!

Contrary to the doomsayers, AI will not just enhance human productivity. Like all new technologies, it will lead to opportunities for human actors that are as yet unforeseen. AI is likely to identify better ways for humans to do many things, or do wonderful things that are now unimagined. At a minimum, however, the transition will be disruptive for a large number of workers, and it will take some time for new opportunities and roles for humans to come to fruition.

Robin Hanson has a unique proposal for meeting the kind of challenge faced by white collar workers vulnerable to displacement by AI, or for blue collar workers who are vulnerable to displacement by robots (the deployment of which has been hastened by minimum wage and living wage activism). This treatment of Hanson’s idea will be inadequate, but he suggests a kind of insurance or contract sold to both workers and investors by owners of assets likely to be insensitive to AI risks. The underlying assets are paid out to workers if automation causes some defined aggregate level of job loss. Otherwise, the assets are paid out to investors taking the other side of the bet. Workers could buy these contracts themselves, or employers could do so on their workers’ behalf. The prices of the contracts would be determined by a market assessment of the probability of the defined job loss “event”. Governmental units could buy the assets for their citizens, for that matter. The “worker contracts” would be cheap if the probability of the job-loss event is low. Sounds far-fetched, but perhaps the idea is itself an entrepreneurial opportunity for creative players in the financial industry.

The threat of job losses to AI has also given new energy to advocates of widespread adoption of universal basic income payments by government. Hanson’s solution is far preferable to government dependence, but perhaps the state could serve as an enabler or conduit through which workers could acquire AI and non-AI capital.

Human Capital

Current incarnations of AI are not just a threat to employment. One might add the prospect that heavy reliance on AI could undermine the future education and critical thinking skills of the general population. Essentially allowing machines to do all the thinking, research, and planning won’t inure to the cognitive strength of the human race, especially over several generations. Already people suffer from an inability to perform what were once considered basic life skills, to say nothing of tasks that were fundamental to survival in the not too distant past. In other words, AI could exaggerate a process of “dumbing down” the populace, a rather undesirable prospect.

Fraud and Privacy

AI is responsible for still more disruptions already taking place, in particular violations of privacy, security, and trust. For example, a company called Clearview AI has scraped 30 billion photos from social media and used them to create what its CEO proudly calls a “perpetual police lineup”, which it has provided for the convenience of law enforcement and security agencies.

AI is also a threat to encryption in securing data and systems. Conceivably, AI could be of value in perpetrating identity theft and other kinds of fraud, but it can also be of value in preventing them. AI is also a potential source of misleading information. It is often biased, reflecting specific portions of the on-line terrain upon which it is trained, including skewed model weights applied to information reflecting particular points of view. Furthermore, misinformation can be spread by AIs via “synthetic media” and the propagation of “fake news”. These are fairly clear and present threats of social, economic, and political manipulation. They are all foreseeable dangers posed by AI in the hands of bad actors, and I would include certain nudge-happy and politically-motivated players in that last category.

The Sky-Already-Fell Crowd

Certain ethicists with extensive experience in AI have condemned the signatories of the “Pause Letter” for a focus on “longtermism”, or risks as yet hypothetical, rather than the dangers and wrongs attributable to AIs that are already extant:TechCrunch quotes a rebuke penned by some of these dissenting ethicists to supporters of the “Pause Letter”:

“‘Those hypothetical risks are the focus of a dangerous ideology called longtermism that ignores the actual harms resulting from the deployment of AI systems today,’ they wrote, citing worker exploitation, data theft, synthetic media that props up existing power structures and the further concentration of those power structures in fewer hands.”

So these ethicists bemoan AI’s presumed contribution to the strength and concentration of “existing power structures”. In that, I detect just a whiff of distaste for private initiative and private rewards, or perhaps against the sovereign power of states to allow a laissez faire approach to AI development (or to actively sponsor it). I have trouble taking this “rebuke” too seriously, but it will be fruitless in any case. Some form of cooperation between AI developers on safety protocols might be well advised, but competing interests also serve as a check on bad actors, and it could bring us better solutions as other dilemmas posed by AI reveal themselves.

ImaginingAI Catastrophes

What are the more consequential (and completely hypothetical) risks feared by the “pausers” and “stoppers”. Some might have to do with the possibility of widespread social upheaval and ultimately mayhem caused by some of the “mundane” risks described above. But the most noteworthy warnings are existential: the end of the human race! How might this occur when AGI is something confined to computers? Just how does the supposed destructive power of AGIs get “outside the box”? It must do so either by tricking us into doing something stupid, hacking into dangerous systems (including AI weapons systems or other robotics), and/or through the direction and assistance of bad human actors. Perhaps all three!

The first question is this: why would an AGI do anything so destructive? No matter how much we might like to anthropomorphize an “intelligent” machine, it would still be a machine. It really wouldn’t like or dislike humanity. What it would do, however, is act on its objectives. It would seek to optimize a series of objective functions toward achieving a goal or a set of goals it is given. Hence the role for bad actors. Let’s face it, there are suicidal people who might like nothing more than to take the whole world with them.

Otherwise, if humanity happens to be an obstruction to solving an AGI’s objective, then we’d have a very big problem. Humanity could be an aid to solving an AGI’s optimization problem in ways that are dangerous. As Yudkowsky says, we might represent mere “atoms it could use somewhere else.” And if an autonomous AGI were capable of setting it’s own objectives, without alignment, the danger would be greatly magnified. An example might be the goal of reducing carbon emissions to pre-industrial levels. How aggressively would an AGI act in pursuit of that goal? Would killing most humans contribute to the achievement of that goal?

Here’s one that might seem far-fetched, but the imagination runs wild: some individuals might be so taken with the power of vastly intelligent AGI as to make it an object of worship. Such an “AGI God” might be able to convert a sufficient number of human disciples to perpetrate deadly mischief on its behalf. Metaphorically speaking, the disciples might be persuaded to deliver poison kool-aid worldwide before gulping it down themselves in a Jim Jones style mass suicide. Or perhaps the devoted will survive to live in a new world mono-theocracy. Of course, these human disciples would be able to assist the “AGI God” in any number of destructive ways. And when brain-wave translation comes to fruition, they better watch out. Only the truly devoted will survive.

An AGI would be able to create the illusion of emergency, such as a nuclear launch by an adversary nation. In fact, two or many adversary nations might each be fooled into taking actions that would assure mutual destruction and a nuclear winter. If safeguards such as human intermediaries were required to authorize strikes, it might still be possible for an AGI to fool those humans. And there is no guarantee that all parties to such a manufactured conflict could be counted upon to have adequate safeguards, even if some did.

Yudkowsky offers at least one fairly concrete example of existential AGI risk:

“A sufficiently intelligent AI won’t stay confined to computers for long. In today’s world you can email DNA strings to laboratories that will produce proteins on demand, allowing an AI initially confined to the internet to build artificial life forms or bootstrap straight to postbiological molecular manufacturing.”

There are many types of physical infrastructure or systems that an AGI could conceivably compromise, especially with the aid of machinery like robots or drones to which it could pass instructions. Safeguards at nuclear power plants could be disabled before steps to trigger melt down. Water systems, rivers, and bodies of water could be poisoned. The same is true of food sources, or even the air we breathe. In any case, complete social disarray might lead to a situation in which food supply chains become completely dysfunctional. So, a super-intelligence could probably devise plenty of “imaginative” ways to rid the earth of human beings.

Back To Earth

Is all this concern overblown? Many think so. Bryan Caplan now has a $500 bet with Eliezer Yudkowsky that AI will not exterminate the human race by 2030. He’s already paid Yudkowsky, who will pay him $1,000 if we survive. Robin Hanson says “Most AI Fear Is Future Fear”, and I’m inclined to agree with that assessment. In a way, I’m inclined to view the AI doomsters as highly sophisticated, change-fearing Luddites, but Luddites nevertheless.

Ben Hayum is very concerned about the dangers of AI, butwriting at LessWrong, he recognizes some real technical barriers that must be overcome for recursive optimization to be successful. He also notes that the big AI developers are all highly focused on safety. Nevertheless, he says it might not take long before independent users are able to bootstrap their own plug-ins or modules on top of AI models to successfully optimize without running off the rails. Depending on the specified goals, he thinks that will be a scary development.

James Pethokoukis raises a point that hasn’t had enough recognition: successful innovations are usually dependent on other enablers, such as appropriate infrastructure and process adaptations. What this means is that AI, while making spectacular progress thus far, won’t have a tremendous impact on productivity for at least several years, nor will it pose a truly existential threat. The lag in the response of productivity growth would also limit the destructive potential of AGI in the near term, since installation of the “social plant” that a destructive AGI would require will take time. This also buys time for attempting to solve the AI alignment problem.

In another Robin Hanson piece, he expresses the view that the large institutions developing AI have a reputational Al stake and are liable for damages their AI’s might cause. He notes that they are monitoring and testing AIs in great detail, so he thinks the dangers are overblown.:

“So, the most likely AI scenario looks like lawful capitalism…. Many organizations supply many AIs and they are pushed by law and competition to get their AIs to behave in civil, lawful ways that give customers more of what they want compared to alternatives.”

In the longer term, the chief focus of the AI doomsters, Hanson is truly an AI optimist. He thinks AGIs will be “designed and evolved to think and act roughly like humans, in order to fit smoothly into our many roughly-human-shaped social roles.” Furthermore, he notes that AI owners will have strong incentives to monitor and “delimit” AI behavior that runs contrary to its intended purpose. Thus, a form of alignment is achieved by virtue of economic and legal incentives. In fact, Hanson believes the “foom” scenario is implausible because:

“… it stacks up too many unlikely assumptions in terms of our prior experiences with related systems. Very lumpy tech advances, techs that broadly improve abilities, and powerful techs that are long kept secret within one project are each quite rare. Making techs that meet all three criteria even more rare. In addition, it isn’t at all obvious that capable AIs naturally turn into agents, or that their values typically change radically as they grow. Finally, it seems quite unlikely that owners who heavily test and monitor their very profitable but powerful AIs would not even notice such radical changes.”

As smart as AGIs would be, Hanson asserts that the problem of AGI coordination with other AIs, robots, and systems would present insurmountable obstacles to a bloody “AI revolution”. This is broadly similar to Pethokoukis’ theme. Other AIs or AGIs are likely to have competing goals and “interests”. Conflicting objectives and competition of this kind will do much to keep AGIs honest and foil malign AGI behavior.

The kill switch is a favorite response of those who think AGI fears are exaggerated. Just shut down an AI if its behavior is at all aberrant, or if a user attempts to pair an AI model with instructions or code that might lead to a radical alteration in an AI’s level of agency. Kill switches would indeed be effective at heading off disaster if monitoring and control is incorruptible. This is the sort of idea that begs for a general solution, and one hopes that any advance of that nature will be shared broadly.

One final point about AI agency is whether autonomous AGIs might ever be treated as independent factors of production. Could they be imbued with self-ownership?Tyler Cowen asks whether an AGI created by a “parent” AGI could legitimately be considered an independent entity in law, economics, and society. And how should income “earned” by such an AGI be treated for tax purposes. I suspect it will be some time before AIs, including AIs in a lineage, are treated separately from their “controlling” human or corporate entities. Nevertheless, as Cowen says, the design of incentives and tax treatment of AI’s might hold some promise for achieving a form of alignment.

Letting It Roll

There’s plenty of time for solutions to the AGI threat to be worked out. As I write this, the consensus forecast for the advent of real AGI on the Metaculus online prediction platform is July 27, 2031. Granted, that’s more than a year sooner than it was 11 days ago, but it still allows plenty of time for advances in controlling and bounding agentic AI behavior. In the meantime, AI is presenting opportunities to enhance well being through areas like medicine, nutrition, farming practices, industrial practices, and productivity enhancement across a range of processes. Let’s not forego these opportunities. AI technology is far too promising to hamstring with a pause, moratoria, or ill-devised regulations. It’s also simply impossible to stop development work on a global scale.

Nevertheless, AI issues are complex for all private and public institutions. Without doubt, it will change our world. This AI Policy Guide from Mercatus is a helpful effort to lay out issues at a high-level.

Government budget negotiations never fail to frustrate anyone of a small-government persuasion. We have a huge, ongoing federal budget deficit. Spending’s gone bat-shit out of control over the past several years and too few in Congress are willing to do anything about it. Democrats would rather see politically-targeted tax increases. While some Republicans advocate spending cuts, the focus is almost entirely on discretionary spending. Meanwhile, the entitlement state is off the table, including Social Security reform.

Fiscal Indiscretion

Sadly, non-discretionary outlays (entitlements) today make a much larger contribution to the deficit than discretionary spending. That includes the programs like Social Security (SS) and Medicare, in which spending levels are programmatic and not subject to annual appropriations by Congress. When these programs were instituted there were a large number of workers relative to retirees, so tax contributions exceeded benefit levels for many decades. The revenue excesses were placed into “trust funds” and invested in Treasury debt. In other words, surpluses under non-discretionary SS and Medicare programs were used to finance discretionary spending!

The aging of Baby Boomers ultimately led to a reversal in the condition of the trust funds. Fewer workers relative to retirees meant that annual payroll tax collections were not adequate to cover annual benefits, and that meant drawing down the trust funds. Current projections by the system trustees call for the SS Trust Fund to be exhausted by 2035. Once that occurs, benefits will automatically be reduced by roughly 20% unless Congress acts to shore up the system before then.

A Few Proposals

I’ve written about the need for SS reform on several occasions (though the first article at that link is not germane here). It seems imperative for Congress and the President to address these shortfalls. By all appearances, however, many Republicans have put the issue aside. For his part, Joe Biden has apparently accepted the prospect of an automatic reduction in benefits in 2035, or at least he’s willing to kick that can down the road. He has, however, endorsed taxes on high earners to fund Medicare. Senator John Kennedy (R-LA) suggests raising the retirement age, or at least raise the minimum age at which one may claim benefits (now 62). Senators Bill Cassidy (R-La.) and Angus King (I-Maine) were working on a compromise that would create an investment fund to fortify the system, but the specifics are unclear, as well as how much that would accomplish.

Meanwhile, Senator Bernie Sanders (S-VT) proposes to expand SS benefits by $2,400 a year and add funding by extending payroll taxes to earners above the current limit of $160,000. Senator Joe Manchin (D-WV) has endorsed the latter as a “quick fix”.

There is also at least oneproposal in Congress to end the practice of taxing a portion of SS benefits as income. I have trouble believing it will gain wide support, despite the clear double-taxation involved.

Then there are always discussions of reducing benefits at higher income levels or even means-testing benefits. In fact, it would be interesting to know what proportion of current benefits actually function as social insurance, as opposed to a universal entitlement. The answer, at least, could serve as a baseline for more fundamental reforms, including changes in the structure of payroll taxes, voluntary lump-sum payouts, and private accounts.

More Radical Views

There are a few prominent voices who claim that SS is sustainable in its current form, but perhaps with a few “no big deal” tax increases. Oh, that’s only about a $1 trillion “deal”, at least for both Medicare and SS. More offensive still are the scare tactics used by opponents of SS reform any time the subject comes up. I’m not aware of any serious reform proposal made over the past two decades that would have affected the benefits of anyone over the age of 55, and certainly no one then-eligible for benefits. Yet that charge is always made: they want to cut your SS benefits! The Democrats made that claim against George W. Bush, torpedoing what might have been a great accomplishment for all. And now, apparently Donald Trump is willing to use such accusations to damage any rival who has ever mentioned reform, including Mike Pence. Will you please cut the crap?

The System

The thing to remember about SS is that it is currently structured as a pay-as-you-go (PAYGO) system, despite the fact that benefits are defined like many creaky private pensions of old. SS benefits in each period are paid out of current “contributions” (i.e., FICO payroll taxes) plus redemptions of government bonds held in the Trust Fund. Contributions today are not “invested” anywhere because they are not enough to pay for current benefits under PAYGO.

The Trust Fund was accumulated during the years when favorable demographics led to greater FICO contributions than benefit payouts. The excess revenue was “invested” in Treasury bonds, which meant it was used to fund deficits in the general budget. It’s been about 15 years since the Trust Fund entered a “draw-down” status, and again, it will be exhausted by 2035.

SSA Says It’s a Good Deal

A participant’s expected “rate of return” on lifetime payroll tax payments depends on several things: lifetime earnings, age at which benefits are first claimed, life expectancy at that time, marital status, relative earning levels within two-earner couples, and the “full retirement age” for the individual’s birth year. Payroll tax payments, by the way, include the employer’s share because that is one of the terms of a hire. A high rate of return is not the same as a high level of benefits, however. In fact, relative to career income, SS has a great deal of progressivity in terms of rates of return, but not much in terms of benefit levels.

The Social Security Administration (SSA) has calculated illustrative real internal rates of return (IRR) for many categories of earners given certain assumptions. (An IRR is a discount rate that equalizes the present value (PV) of a stream of payments and the PV of a stream of payoffs.) The SSA’s most recent update of this exercise was in April 2022. The report references Old Age, Survivors, and Disability Insurance (OASDI), but the focus is exclusively on seniors.

Three basic scenarios were considered: 1) current law, as scheduled, despite its unsustainability; 2) a payroll tax increase from 12.4% (not including the Medicare tax) to 15.96% starting in 2035, when the Trust Fund is exhausted; and 3) a reduction in benefits of 22% starting in 2035.

The authors of the report concludethat “… the real value of OASDI benefits is extraordinarily high.” This theme has been echoed by several other writers, such as here and here. This conclusion is based on a comparison to returns earned by investments that SSA judges to have comparably low risk.

I note here that I’ve made assertions in the past about relative SS returns based on nominal benefits, rather than inflation-adjusted values. Those comparisons to private returns might have seemed drastic because they were expressed in terms of hypothetical future nominal values at the point of retirement. The gaps are not as large in real terms or if we consider SS returns broadly to include those accruing to low career earners. Medium and high earners tend to earn lower hypothetical returns from SS.

A Mixed Bag

SSA’s calculated IRRs are highest for one-earner couples followed by two-earner couples. Single males do relatively poorly due to their higher mortality rates. Low earners do very well relative to higher earners. Earlier birth years are associated with higher IRRs, but these are not as impressive for cohorts who have not yet claimed benefits. The ranges of birth years provided in the report make this a little imprecise, but I’ll focus on those born in 1955 and later.

Of course the returns are highest under the current law hypothetical than for the scenarios involving a benefit reduction or a payroll tax hike. The current law IRRs can be viewed as baselines for other calculations, but otherwise they are irrelevant. The system is technically insolvent and the scheduled benefits under current law can’t be maintained beyond 2034 without steps to generate more revenue or cut benefits. Those steps will reduce IRRs earned by hypothetical SS “assets” whether they take the form of higher payroll taxes, lower benefits, a greater full retirement age, or other measures.

The tax hike doesn’t have much impact on the IRRs of near-term retirees. It falls instead on younger cohorts with some years of employment (and payroll tax payments) remaining. The effect of a cut in benefits is spread more evenly across age cohorts and the reductions in IRRs is somewhat larger.

With higher payroll taxes after 2034, the average IRRs for birth years of 1955+ range from about 0.5% up to about 6.25%. The returns for single females and two-earner couples are roughly similar and fall between those for single males on the low end and one-earner couples on the high end. In all cases, low earners have much higher IRRs than others.

The reduction in benefits produces returns for the 1955+ age cohorts averaging small, negative values for high-earning single men up to 5.5% to 6% for low-earning, one-earner couples.

But On the Whole…

The IRR values reported by SSA are quite variable across cohorts. Individuals or couples with low earnings can usually expect to “earn” real IRRs on their contributions of better than 3% (and above 5% in a few cases). Medium earners can expect real returns from 1% to 3% (and in some cases above 4%). Many of the returns are quite good for a safe “asset”, but not for high earners.

Again, SSA states that these are real returns, though they provide no detail on the ways in which they adjust the components used in their IRR formula to arrive at real returns. Granting the benefit of the doubt, we saw persistently negative real returns on a range of safe assets in the not-very-distant past, so the IRRs are respectable by comparison.

Qualifications

There are many assumptions in the SSA’s analysis that might be construed as drastic simplifications, such as no divorce and remarriage, uniform career duration, and no relationship between earnings and mortality. But it’s easy to be picky. Many of the assumptions discernible from the report seem to be reasonable simplifications in what could otherwise be an unruly analysis. Nonetheless, there are a few assumptions that I believe bias the IRRs upward (and perhaps a few in the other direction).

In fact, SSA is remarkably non-transparent in their explanation of the details. Repeated checking of SSA’s document for clear answers is mostly futile. Be that as it may, I’m forced to give SSA the benefit of the doubt in several respects. One is the reinvestment of cumulative remaining contributions at the IRR throughout the earning career and retirement. A detailed formula with all components and time subscripts would have been nice.

… And Major Doubts

As to my misgivings, first, the IRRs reported by SSA are based on earners who all reach the age of 65. However, roughly 14% – 15% of individuals who live to be of working age die before they reach the age of 65. Most of those deaths occur in the latter part of that range, after many years of contributions and hypothetical compounding. That means the dollar impact of contributions forfeited at death before age 65 is probably larger than the unweighted share of individuals. These individuals pay-in but receive no retirement benefit in SSA’s IRR framework, although some receive disability benefits for a period of time prior to death. It wouldn’t bother my conscience to knock off at least a tenth of the quoted returns for this consideration alone.

A second major concern surrounds the method of calculating benefits and discounted benefits. SSA assumes that benefits continue for the expected life of the claimant as of age 65. If life expectancy is 19 years at age 65, then “expected” benefits are a flat stream of benefit payments for 19 years. Discounting each payment back to age 65 at the IRR yields one side of the present value equality. This constant cash flow (CCF) treatment is likely to overstate the present value of benefits. Instead of CCFs, each payment should be weighted by the probability that the claimant will be alive to receive it with a limit at some advanced age like 100. CCF overcounts present values up to the expected life, but it undercounts present values beyond the expected life because the assumed CCF benefits then are zero!! Weighting benefit payments by the probability of survival to each age produces continuing additions to the PV, but increasing mortality and decaying discount factors become quite substantial beyond expected life, leading to relatively minor additions to PV over that range. The upshot is that the CCFs employed by SSA overstate PVs by front-loading all benefits earlier in retirement. For a given PV of contributions, an overstated PV of benefits requires a higher (and overstated) IRR to restore the PV equality, and this might be a substantial source of upward bias in SSA’s calculations.

Third, when comparing an SS “asset” to private returns, a big difference is that private balances remaining at death become assets of the earner’s estate. Meanwhile, a single beneficiary forfeits their SS benefits at death (except for a small death benefit), while a surviving spouse having lower benefits receives ongoing payments of the decedent’s benefits for life. This consideration, however, in and of itself, means that private plans have a substantial advantage: the “expected” residual at death can be “optimized” at zero or some higher balance, depending on the strength of the earner’s bequest motive.

Finally, in a footnote, the SSA report notes that their treatment of income taxes on Social Security benefits for claimants with higher incomes might bias some of the IRRs upward. That seems quite likely.

It would be difficult to recast SSA’s report based on adjustments for all of these qualifications. However, it’s likely that the IRRs in the SSA report are sharply overstated. That means many more beneficiaries with medium and higher earnings records would have returns in the 0% to 2% range, with more IRRs in the negative range for singles. Low earners, however, might still get returns in a range of 3% to 5%.

The SSA analysis attempts to demonstrate some limits to the risks faced by participants, given the scenarios involving a payroll tax increase or a benefits reduction in 2035. Nevertheless, there are additional political risks to the returns of certain classes of current and future retirees. For example, payroll taxes could be made much more progressive, benefits could be made subject to means testing, or indexing of benefits could be reduced. In fact, there are additional demographic risks that might confront retirees several decades ahead. Continued declines in fertility could further undermine the system’s solvency, requiring more drastic steps to shore up the system. As a hypothetical asset, by no means is SS “risk-free”.

Better Returns

Now let’s consider returns earned by private assets, which represent investments in productive capital. For stocks, these include the sum of all dividends and capital gains (growth in value). For compounding purposes, we assume that all returns are reinvested until retirement. Remember that private returns are much less variable over spans of decades than over durations of a few years. Over the course of 40 year spans (SSA’s career assumption), private returns have been fairly stable historically, and have been high enough to cushion investors from setbacks. Here is Seeking Alpha on annualized returns on the basket of stocks in the S&P 500:

“… the return on the S&P 500 since the beginning of valuation in 1928, is 10.22%, whereas the inflation-adjusted return on the market since that time is 7.01%…”

That real return would generate benefits far in excess of SS for most participants, but it’s not an adequate historical perspective on market performance. A more complete picture of real returns on the S&P, though one that is still potentially flawed, emerges from this calculator, which relies on data from Robert Shiller. The returns extend back to 1871, but the index as we know it today has existed only since 1957. The earlier returns tend to be lower, so these values may be biased:

Real stock market returns over rolling 40-year time spans varied considerably over this longer period. Still, those kind of stock returns would be superior to the IRRs in the SSA report going forward in all but a few cases (and then only for low and very low earners).

Most workers facing a choice between investing at these rates for 40 years, with market risk, and accepting standard SS benefits, uncertain as they are, couldn’t be blamed for choosing stocks. In fact, if we think of contributions to either type of plan as compounding to a hypothetical sum at retirement, the stock investments would produce a “pot of gold” several times greater in magnitude than SS.

However, we still don’t have a fair comparison because workers choosing a stock plan would essentially engage in a kind of dollar-cost averaging over 40 years, meaning that investments would be made in relatively small amounts over time, rather than investing a lump-sum at the beginning. This helps to smooth returns because purchases are made throughout the range of market prices over time, but it also means that returns tend to be lower than the 40-year rolling returns shown above. That’s because the average contribution is invested for only half the time.

To be very conservative, if we assume that real stock returns average between 5% and 6% annually, $1 invested every year would grow to between $131 – $155 after 40 years in constant dollars. At returns of 1% to 2% from SS, which I believe are typical of the IRRs for many medium earners, the cumulative “pot” would grow to $49 – $60. Assuming that the tax treatment of the stock plan was the same as contributions and benefits under SS, the stock plan almost triples your money.

Dealing With the Transition

Privatization covers a range of possible alternatives, all of which would require federal borrowing to pay transition costs. Unfortunately, the Achilles heel in all this is that now is a bad time to propose more federal borrowing, even if it has clear long-term benefits to future retirees.

Todd Henderson in the Wall Street Journal suggests a seeding of capital provided by government at birth along with an insurance program to smooth returns. Another idea is to offer an inducement to delay retirement claims by allowing at least a portion of future benefits to be taken as a lump sum. If retirees can privately invest at a more advantageous return, they might be willing to accept a substantial discount on the actuarial value of their benefits.

In fact, there is evidence that a majority of participants seem to prefer distributions of lump sums because they don’t value their future benefits at anything like that suggested by the SSA analysis. In fact, many participants would defer retirement by 1 – 2 years given a lump sum payment. Discounts and/or delayed claims would reduce the ultimate funding shortfall, but it would require substantial federal borrowing up front.

Additional federal borrowing would also be required under a private option for investing one’s own contributions for future dispersal. The impact of this change on the system’s long-term imbalances would depend on the share of earners willing to opt-out of the traditional SS program in whole or in part. More opt-outs would mean a smaller long-term obligations for the traditional system, but it would be hampered by a costly transition over a number of years. Starting from today’s PAYGO system, someone still has to pay the benefits of current retirees. This would almost certainly mean federal borrowing. Spreading the transition over a lengthy period of time would reduce the impact on credit markets, but the borrowing would still be substantial.

For example, perhaps earners under 35 years of age could begin opting out of a portion or all of the traditional program at their discretion, investing contributions for their own future use. Thus, only a small portion of contributions would be diverted in the beginning, and amounts diverted would contribute to the nation’s available pool of saving, helping to keep borrowing costs in check. By the time these younger earners reach retirement age, nearly all of today’s retirees will have passed on. Ultimately, the average retiree will benefit from higher returns than under the traditional program, but since they won’t be (fully) paying the benefits of current or near-term retirees, the public must come to grips with the bad promises of the past and fund those obligations in some other way: reduced benefits, taxes, or borrowing.

Another objection to privatization is financial risk, particularly for lower-income beneficiaries. Limiting opt-outs to younger earners with adequate time for growth would mitigate this risk, along with a reversion to the traditional program after age 45, for example. Some have proposed limiting opt-outs to higher earners. Bear in mind, however, that the financial risk of private accounts should be weighed against the political and demographic risk already inherent in the existing system.

One more possibility for bridging the transition to private, individually-controlled accounts is to sell federal assets. I have discussed this before in the context of funding a universal basic income (which I oppose). The proceeds of such sales could be used to pay the benefits of current and near-term retirees so as to allow the opt-out for younger workers. Or it could be used to pay off federal debt accumulated in the process. The asset sales would have to proceed at a careful and deliberate pace, perhaps stretching over several decades, but those sales could include everything from the huge number of unoccupied federal buildings to vast tracts of public lands in the west, student loans, oil and gas reserves, and airports and infrastructure such as interstate highways and bridges. Of course, these assets would be more productive in private hands anyway.

The Likely Outcome

Will any such privatization plan ever see the light of day? Probably not, and it’s hard to guess when anything will be done in Washington to address the insolvency we already face. Instead, we’ll see some combination of higher payroll taxes, higher payroll taxes on high earners through graduated payroll tax rates or by lifting the earnings cap, reduced benefits on further retirees, limits on COLAs to low career earners, and means-tested benefits. Some have mentioned funding Social Security shortfalls with income taxes. All of these proposals, with the exception of automatic benefit cuts in 2035, would require acts of Congress.

I’ll get to the weird trick right off the bat. Then you can read on if you want. The trick really is perverse if you believe in principles of sound credit and financial stability. To levy a fiscal inflation tax, all the government need do is spend like a drunken sailor and undermine its own credibility as a trustworthy borrower. One way to do that: adopt the policy prescriptions of Modern Monetary Theory (MMT).

A Theory of Deadbeat Government

That’s right! Run budget deficits and convince investors the debt you float will never be repaid with future real surpluses. That doesn’t mean the government would literally default (though that is never outside the realm of possibility). However, given such a loss of faith, something else must give, because the real value government debt outstanding will exceed the real value of expected future surpluses from which to pay that debt. The debt might be in the form of interest-bearing government bonds or printed money: it’s all government debt. Ultimately, under these circumstances, there will be a revised expectation that the value of that debt (bonds and dollars) will be eroded by an inflation tax.

This is a sketch of “The Fiscal Theory of the Price Level” (FTPL). The link goes to a draft of a paper by John Cochrane, which he intends as an introduction and summary of the theory. He has been discussing and refining this theory for many years. In fairness to him, it’s a draft. There are a few passages that could be written more clearly, but on the whole, FTPL is a useful way of thinking about fiscal issues that may give rise to inflation.

Fiscal Helicopters

Cochrane discusses the old allegory about how an economy responds to dollar bills dropped from a helicopter — free money floating into everyone’s yard! The result is the classic “too much money chasing too few goods” problem, so dollar prices of goods must rise. We tend to think of the helicopter drop as a monetary policy experiment, but as Cochrane asserts, it is fiscal policy.

We have experienced something very much like the classic helicopter drop in the past two years. The federal government has effectively given money away in a variety of pandemic relief efforts. Our central bank, the Federal Reserve, has monetized much of the debt the Treasury issued as it “loaded the helicopter”.

In effect, this wasn’t an act of monetary policy at all, because the Fed does not have the authority to simply issue new government debt. The Fed can buy other assets (like government bonds) by issuing dollars (as bank reserves). That’s how it engineers increases in the money supply. It can also “lend” to the U.S. Treasury, crediting the Treasury’s checking account. Presto! Stimulus payments are in the mail!

This is classic monetary seigniorage, or in more familiar language, an inflation tax. Here is Cochrane description of the recent helicopter drop:

“The Fed and Treasury together sent people about $6 trillion, financed by new Treasury debt and new reserves. This cumulative expansion was about 30% of GDP ($21,481) or 38% of outstanding debt ($16,924). If people do not expect that any of that new debt will be repaid, it suggests a 38% price-level rise. If people expect Treasury debt to be repaid by surpluses but not reserves, then we still expect $2,506 / $16,924 = 15% cumulative inflation.”

FTPL, May I Introduce You To MMT

Another trend in thought seems to have dovetailed with the helicopter drop , and it may have influenced investor sentiment regarding the government’s ever-weakening commitment to future surpluses: that would be the growing interest in MMT. This “theory” says, sure, go ahead! Print the money government “must” spend. The state simply fesses-up, right off the bat, that it has no intention of running future surpluses.

To be clear, and perhaps more fair, economists who subscribe to MMT believe that deficits financed with money printing are acceptable when inflation and interest rates are very low. However, expecting stability under those circumstances requires a certain level of investor confidence in the government fisc. Read this for Cochrane’s view of MMT.

Statists like Bernie Sanders, Alexandria Ocasio-Cortez, and seemingly Joe Biden are delighted to adopt a more general application of MMT as intellectual cover for their grandiose plans to remake the economy, fix the climate, and expand the welfare state. But generalizing MMT is a dangerous flirtation with inflation denialism and invites economic disaster.

If This Goes On…

Amid this lunacy we have Joe Biden and his party hoping to find avenues for “Build Back Better”. Fortunately, it’s looking dead at this point. The bill considered in the fall would have amounted to an additional $2 trillion of “infrastructure” spending, mostly not for physical infrastructure. Moreover, according to the Congressional Budget Office, that bill’s cost would have far exceeded $2 trillion by the time all was said and done. There are ongoing hopes for separate passage of free community college, an extended child tax credit for all families, a higher cap for state and local income tax deductions, and a host of other social and climate initiatives. The latter, relegated to a separate bill, is said to carry a price tag of over $550 billion. In addition, the Left would still love to see complete forgiveness of all student debt and institute some form of universal basic income. Hey, just print the money, right? Warm up the chopper! But rest easy, cause all this appears less likely by the day.

Are there possible non-inflationary outcomes from ongoing helicopter drops that are contingent on behavior? What if people save the fresh cash because it’s viewed as a one-time windfall (i.e., not a permanent increase in income)? If you sit on such a windfall it will erode as prices rise, and the change in expectations about government finance won’t be too comforting on that score.

There are many aspects of FTPL worth pondering, such as whether bond investors would be very troubled by yawning deficits with MMT noisemakers in Congress IF the Fed refused to go along with it. That is, no money printing or debt monetization. The burgeoning supply of debt would weigh heavily on the market, forcing rates up. Government keeps spending and interest costs balloon. It is here where Cochrane and critics of FTPL have a sharp disagreement. Does this engender inflation in the absence of debt monetization? Cochrane says yes if investors have faith in the unfaithfulness of fiscal policymakers. Excessive debt is then every bit as inflationary as printing money.

Real Shocks and FTPL

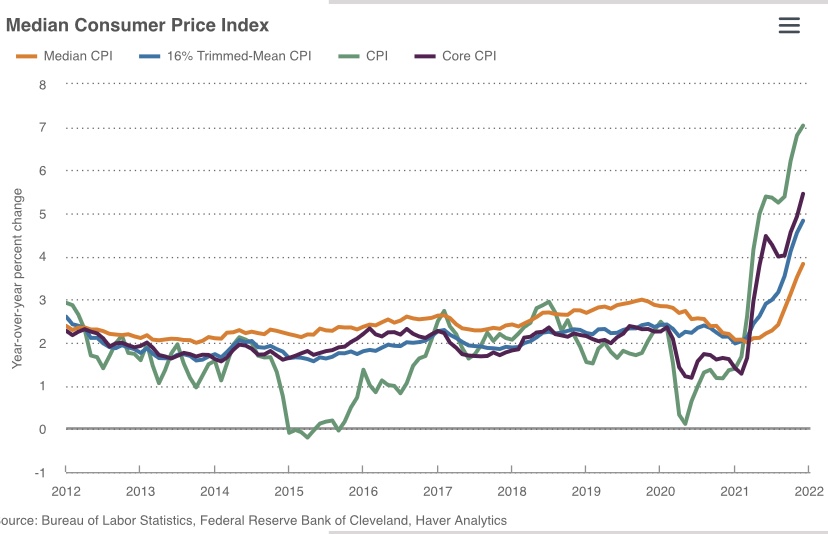

It’s natural to think supply disruptions are primarily responsible for the recent acceleration of inflation, rather than the helicopter drop. There’s no question about those price pressures in certain markets, much of it inflected by wayward policymakers, and some of those markets involve key inputs like energy and labor. Even the median component of the CPI has escalated sharply, though it has lagged broader measures a bit.

Broad price pressures cannot be sustained indefinitely without accommodating changes in the supply of money, which is the so-called “numeraire” in which all goods are priced. What does this have to do with FTPL or the government’s long-term budget constraint? The helicopter drop certainly led to additional money growth and spending, but again, FTPL would say that inflation follows from the expectation that government will not produce future surpluses needed for long-term budget balance. The creation of either new money or government debt, loaded the chopper as it were, is sufficient to accommodate broad price pressures over some duration.

Conclusion

Whether or not FTPL is a fully accurate description of fiscal and monetary phenomena, few would argue that a truly deadbeat government is a prescription for hyperinflation. That’s an extreme, but the motivation for FTPL is the potential abandonment of good and honest governing principles. Pledging an inflation tax is not exactly what anyone means by the full faith and credit of the U.S. government.

Mark Judge says he understands the real importance of #WeAreClosed, a hashtag that’s attained some popularity on Twitter in support of those having to choose between a return to low-paying jobs or continued unemployment benefits. Judge is a conservative author and an old high school friend of Supreme Court Justice Brett Kavanaugh. His notoriety soared in 2018 during Kavanaugh’s confirmation hearings. Christine Blasey Ford, who alleged that Kavanaugh sexually assaulted her more than 30 years before, said Judge had been in the room at the time. Judge offered to cooperate with investigators but denied any memory of the incident, and he was never compelled to testify before the Senate Judiciary Committee.

The Temptation of Joe Lunchpail

I often agree with Judge’s points of view, but not so much in the case of “We Are Closed”. I don’t think he’s identified the right problem or the right villain. He expresses sympathy for those who toil at jobs like dishwashing — and apparently he worked as a dishwasher in the not too distant past. I sympathize as well. It’s tough to make ends meet working a low-wage job. Judge views health insurance as indispensable, and that can take a big chunk out of a low earner’s paycheck. Child care can take another big chunk.

Of course, it’s easy to understand the dilemma faced by these potential re-entrants to the labor force. Under normal circumstances, a worker who is laid off or furloughed can expect to have 30% to 50% of their lost wages replaced by unemployment compensation, depending on the state. That’s somewhere between $500 to $850 a month for a worker earning $10 an hour. COVID assistance now adds another $300 a month, though a number of states will soon end those extended benefits. Still, for now, the extra $300 means the $10/hour worker can replace 50% to 70% of their income if they remain out of work. Rental assistance may also be available due to unemployment or a loss of income. Also, Obamacare premiums are subsidized at low income levels.

In addition to the incremental effect of a decision not to work, all those earning less than $75,000 a year are receiving checks for $1,400. It’s not dependent on being out of work, but it’s a cushion that might convince fence-sitters that marginal wages are not worthwhile for the time being. Any rational individual will weigh public aid against the prospect of a boring, physically demanding, low-wage position.

For the Intercession of Saintly Bosses

Judge cites Henry Ford as the kind of enlightened employer we need more of today. The story goes that Ford wanted his line workers to be able to afford the vehicles they produced, and he did pay his line workers more than the prevailing wage. After all, the technology he implemented made his workers highly productive. However, that he paid them enough to buy Model Ts is something of a myth. And paying employees on any basis other than their productivity is generally a bad business model.

Clearly Judge has large corporations in mind: “Companies that make millions in profit and have high-earning CEOs …” should pay their workers more, he says. It’s foolish to take the position that those “millions” represent some kind of fun money. While high profits surely reflect monopoly power or ill-gotten rents in some cases, my baseline assumption is that profits are necessary to attract the capital needed to maintain and grow a business. And CEO pay is a cheap target: high-level managerial talent is in very short supply. It’s an extremely competitive corner of the labor market, and one seldom gets there via shear nepotism, as Judge implies, or they won’t last long.

Large firms have traditionally paid premium wages. That might be a consequence of more rigorous screening of hires, and certainly large firms tend to have more productive capital per worker. There is some evidence that the large firm wage premium has diminished more recently. Still, if large firms made a regular practice of extracting excess profits by underpaying workers, that wage premium would be negative!

Recently we’ve seen several large corporations make waves by hiking wages in the relatively low-wage retail and food service industries. This includes Amazon, Costco (which has notoriously high labor productivity), Target, WalMart, and Chipotle. This is not so much a matter of enlightenment as it is a reaction to tight labor market conditions exacerbated by the #WeAreClosed” attitude.

Lucifer’s Leviathan

I’d like to cut Judge plenty of slack. He seems to understand work incentives, and he clearly believes work is more fulfilling and socially beneficial than life on the dole. He doesn’t advocate for a higher legal minimum or so-called “living wage”, at least not that I’m aware. Nevertheless, it’s important to note in this context that while a higher wage floor would help certain workers, it would harm the least productive and most needy, who are likely to lose hours or even their jobs if the pay rate threatens to exceed their contribution to output. Then there is the inevitable substitution of capital for labor, as automation becomes a more favorable alternative to higher wage payments. Those workers who keep their jobs may find deteriorated working conditions, as there are many margins along which employers are able to compensate for a higher wage. That includes the most obvious: higher customer prices. However, many small firms facing stiff competition might not be able to manage that. In the end, wage floors really don’t help the working poor, who pay higher prices and might well lose hours or their jobs.

Democrats have been unsuccessful in attaching a higher minimum wage to the Biden infrastructure bill, but they are using the post-pandemic labor shortage as a talking point in favor of putting it back in. It’s also being used in state-level negotiations over minimum wage legislation. Beefed-up COVID relief for workers, as well as the scare tactics regarding continuing COVID risks to workers, have helped to engineer tight labor market conditions and a higher reservation wage among potential workers. Firms are being forced to pay up or go without staff. The largest players with financial reserves may be only too willing to go along with it — we’ve already seen some evidence of that, which puts their smaller competitors in a real bind.

The conundrum faced by low-wage workers in the post-pandemic labor market just might offer a clue as to the impact of a universal basic income on labor force participation. That would bring us full circle to the point at which some will simply choose not to work. Unfortunately, politicians need only hear “Do Something!” to inspire incredibly crackpot policy initiatives. And that way lays the Beast!

The Final Judgement

I’m not sure Judge thought much about the market consequences of ongoing COVID relief or public aid in general. He’d like to see a higher equilibrium wage rate, but he’d surely have mixed feelings about the advantage it confers to large firms at the expense of small ones, given the strong sympathies and antipathies he expresses in his post.

Manual labor is hard! But in the end, low-wage earners who apply themselves and gain job experience can look forward to better things. It’s up to them to seek out the best employment relationship they can. Insisting that firms pay workers more than their productive value is not helpful. If anything, it may buttress political support for governments to impose wage mandates. Public efforts to “help” workers are at best uneven in their effects, helping some workers and harming others. That goes for minimum wages and many forms of public aid, especially the unconditional variety. Judge’s sympathies for those having to choose between returning to work and collecting aid are understandable, but they reflect the sad consequences of the knee-jerk temptation to offer public alms to those presently living and working below their aspirations.

Many jobs have been lost to technology over the last few centuries, yet more people are employed today than ever before. Despite this favorable experience, politicians can’t help the temptation to cast aspersions at certain production technologies, constantly advocating intervention in markets to “save jobs”. Today, some serious anti-tech policy proposals and legislative efforts are underway: regional bans on autonomous vehicles, “robot taxes” (advocated by Bill Gates!!), and even continuing legal resistance to technology-enabled services such as ride sharing and home sharing. At the link above, James Pethokoukas expresses trepidation about one legislative proposal taking shape, sponsored by Senator Maria Cantwell (D-WA), to create a federal review board with the potential to throttle innovation and the deployment of technology, particularly artificial intelligence.

Last week I mentioned the popular anxiety regarding automation and artificial intelligence in my post on the Universal Basic Income. This anxiety is based on an incomplete accounting of the “seen” and “unseen” effects of technological advance, to borrow the words of Frederic Bastiat, and of course it is unsupported by historical precedent. Dierdre McCloskey reviews the history of technological innovations and its positive impact on dynamic labor markets:

“In 1910, one out of 20 of the American workforce was on the railways. In the late 1940s, 350,000 manual telephone operators worked for AT&T alone. In the 1950s, elevator operators by the hundreds of thousands lost their jobs to passengers pushing buttons. Typists have vanished from offices. But if blacksmiths unemployed by cars or TV repairmen unemployed by printed circuits never got another job, unemployment would not be 5 percent, or 10 percent in a bad year. It would be 50 percent and climbing.

Each month in the United States—a place with about 160 million civilian jobs—1.7 million of them vanish. Every 30 days, in a perfectly normal manifestation of creative destruction, over 1 percent of the jobs go the way of the parlor maids of 1910. Not because people quit. The positions are no longer available. The companies go out of business, or get merged or downsized, or just decide the extra salesperson on the floor of the big-box store isn’t worth the costs of employment.“

Robert Samuelson discusses a recent study that found that technological advance consistently improves opportunities for labor income. This is caused by cost reductions in the innovating industries, which are subsequently passed through to consumers, business profits, and higher pay to retained workers whose productivity is enhanced by the improved technology inputs. These gains consistently outweigh losses to those who are displaced by the new capital. Ultimately, the gains diffuse throughout society, manifesting in an improved standard of living.