Tags

Cleveland Fed, Consumer Price Index, Consumer Sentiment, David Beckworth, infrastructure, Joe Biden, Joe Manchin, Median CPI, Pandemic Emergency Powers, Price Controls, Trimmed CPI, Vladimir Putin, Wholesale Price Index

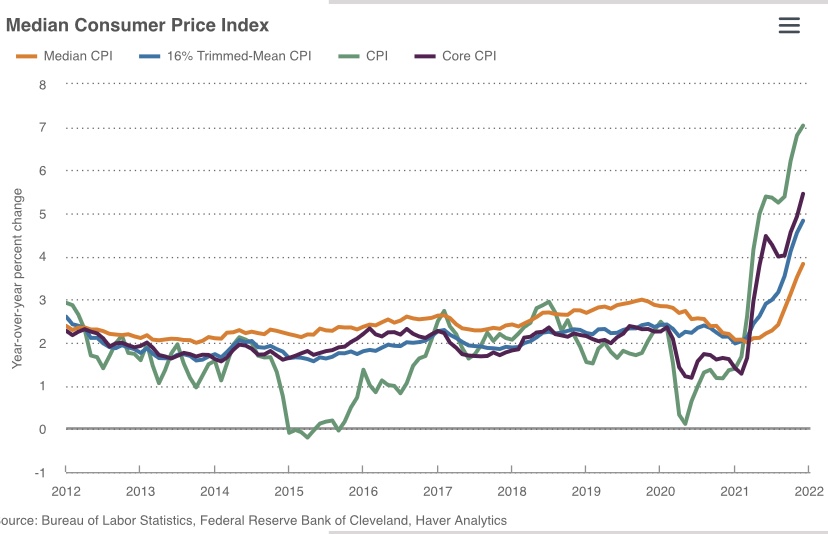

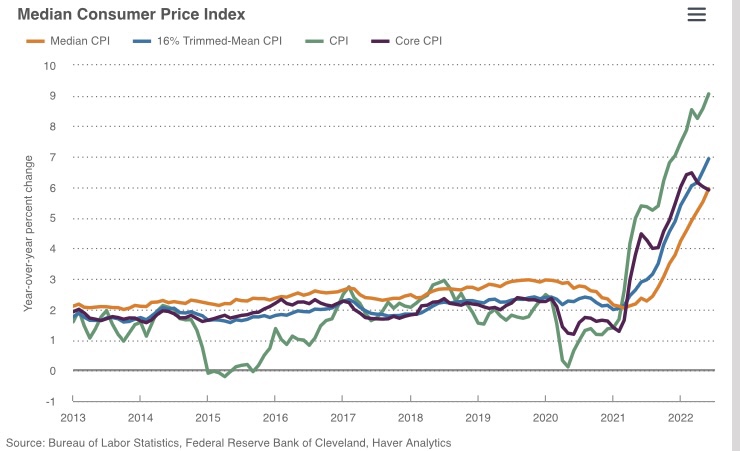

Inflation accelerated at the consumer level in June and the advances continued to broaden. That’s confirmed by the median item in the Consumer Price Index (CPI) and a measure of the CPI that “trims” out items with the largest and smallest price hikes (see chart above from the Cleveland Fed). Wholesale inflation also picked up in June. At this point, there’s a very real danger that increasing expectations of future inflation are getting embedded into current pricing decisions. Once that happens, the cycle is very hard to break. And wage rates are not keeping pace, so inflation is reducing real incomes for many workers. The sad fact is that inflation takes its greatest toll on the well being of low income earners.

And why did inflation accelerate from 1.4% in January 2021 to 9.2% in June? Don’t ask Joe Biden, at least not if you want a straight answer. He’s been changing his tune almost every month, with a rotating cast of the characters coming in for blame. First, the story was that higher inflation was just transitory; then too, the Administration said it only hurt the rich, a wholly preposterous assertion; the blame then shifted to the oil companies; then to Putin; and then big corporations generally; more recently, it’s independent gas retailers! Nothing is said about Biden’s early pledge to shut down fossil fuels. Nothing is said about the federal government’s profligate spending and the money printing that paid for it. Nothing is said about the extended payment of unemployment benefits, which pinched labor supply. More generally, nothing is said about the extension of Biden’s pandemic emergency powers, which allows continued Medicaid and food stamp benefits to many who are otherwise ineligible. The federal spigot has been wide open!

So here’s a quick synopsis of events leading to our inflationary surge: demand strengthened as pandemic restrictions were lifted across the country. Unfortunately, businesses were not ready to meet that level of demand. Operations had been sharply curtailed during the pandemic all along business supply chains. Hiring staff was next to impossible for many firms, especially given the Biden Administration’s ineptitude with respect to labor incentives. The Administration also set out to starve the fossil fuel industry of capital and to shut down drilling and refining operations through restrictions and binding regulations. The price of oil began to soar early in the Administration, which has been working its way into the prices of other goods and services, including food and transportation. Reinforcing these ill effects was the broader regulatory onslaught instigated at many agencies by Biden, actions which tend to increase costs while limiting competition in many industries.

Most of the factors just listed were limitations on supply. However, the price pressure was accelerated on the demand side by government stimulus payments. And in fact, none of this inflation would be sustainable without easy monetary policy — and monetization of government debt.

Later, of course, Vladimir Putin’s invasion of Ukraine exacerbated worldwide energy and food shortages. Meanwhile, Democrat efforts to push through additional social spending, née “infrastructure”, were unrelenting. They are still pushing for more climate change regulation, not to mention funding “investments” intended to improve the “equity” of highways! Thank God for Joe Manchin for shutting it down, though even he seems intent on imposing drug price controls. Biden now says he’ll impose green energy policy via executive order.

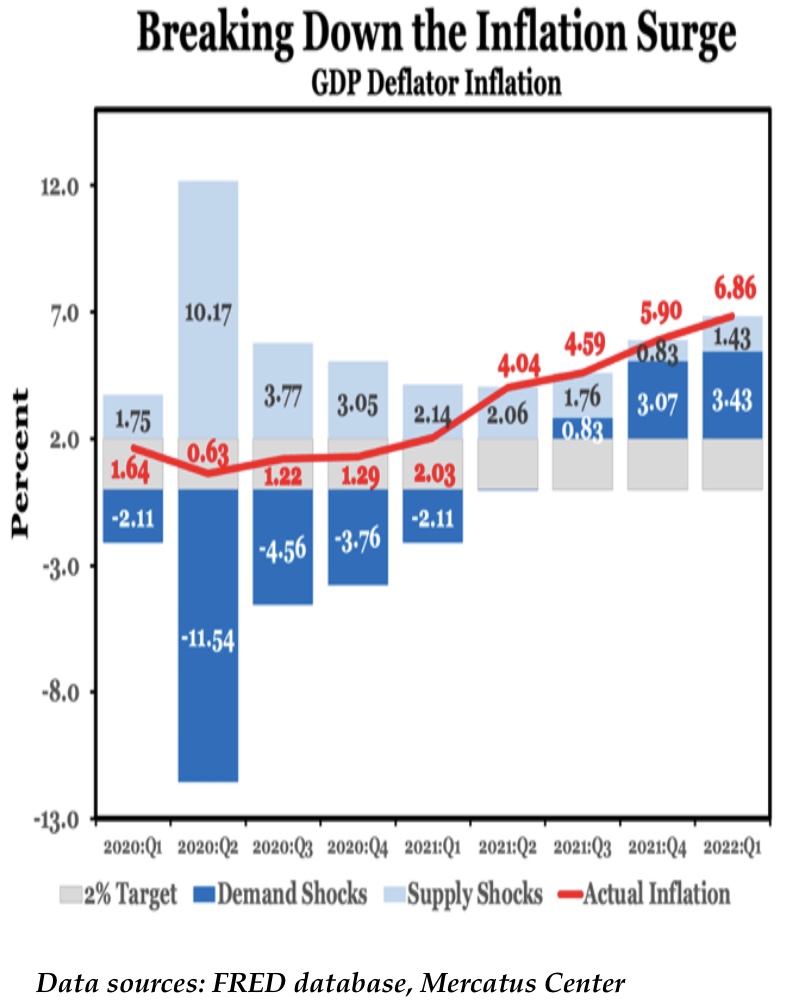

Until about March of this year, Federal Reserve policy remained extremely accommodative, despite the central bank having completely missed its so-called inflation target rate of 2% well before that. Take another look at the chart at the top of this post. CPI inflation shot above 2% in early 2021. The Fed did not really react until March 2022. The chart below shows that growth in the GDP deflator was slightly more muted than the CPI, but it too was above 2% in the first quarter of 2021 and accelerated from there. It’s as if there had been no Fed target at all!

The story, again, was “not to worry, it’s transitory”. Moreover, the Fed was convinced the inflation was driven entirely by supply problems. In fairness, it’s true that tighter monetary policy won’t stop inflation from supply shocks without great cost in terms of lost output. But monetary accommodation, which is what happened in 2021, simply validates inflation and runs the risk of allowing inflation expectations to become embedded in pricing. And again, that’s hard to undo.

Despite the dominance of supply-side inflation pressures early in 2021, it’s no wonder that a different kind of pressure has cropped up since then. The following chart from David Beckworth is helpful:

We now have primarily demand-side inflation fueled by the earlier accommodation of supply constraints and the monetization of government deficits. Sure, there remain significant supply constraints, whether induced by the actions of Russia, Biden, or lingering pandemic dysfunctions. But supply-side inflation cannot sustain without monetary accommodation. An early reading for the second-quarter GDP deflator will be available in late July, but it may well show accelerating pressures from both the demand side and the supply side.

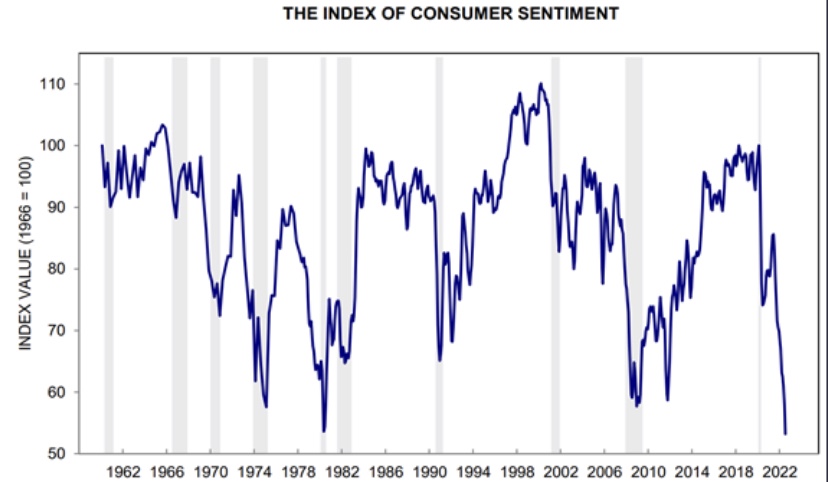

There is no way to eliminate the inflation surge without curtailing the growth of liquidity. Unfortunately, the risk that monetary tightening by the Fed will induce a recession is already very high, even a likelihood at this point. A fairly reliable signal of recession is an inversion of the yield curve, and we now see two-year Treasury debt yielding 15 – 20 basis points more than 10-year bonds. Again, real wages are declining. Real retail sales are down two months in a row and down from a year ago. Here’s a chart showing the most recent dismal reading on the index of consumer sentiment:

Whether a recession has already begun is not clear, but inflation certainly hasn’t abated, and the Fed is expected to continue tightening, albeit belatedly. Meanwhile, the Biden Administration and key Democrats don’t seem to want to make the Fed’s job any easier. They simply don’t comprehend the reality and their role in fostering the upward price trends we’re experiencing. They still cling to hopes of another big spending package that would add to deficits and the inflation tax, despite contemplating tax hikes on private employers, but so far Manchin has put the kabash on that. Still, we’re nowhere close to putting our fiscal and monetary houses in order.