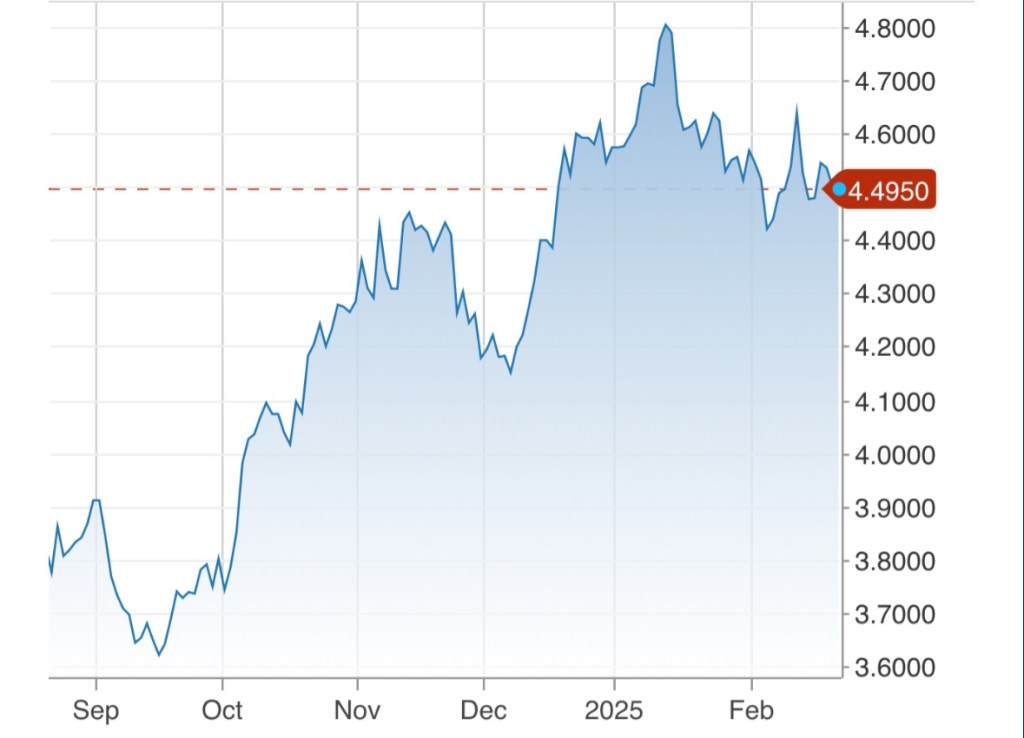

Matt Yglesias tweeted on X that “the bond market does not appear to believe in DOGE”. He included a chart much like the updated one above to “prove” his point. Tyler Cowen posted a link to the tweet on Marginal Revolution, without comment … Cowen surely must know that any such conclusion is premature, especially based on the movement of Treasury yields over the past month (or more, since the market’s evaluation of the DOGE agenda preceded Trump’s inauguration).

Of course, there is a difference between “believing” in DOGE and being convinced that its efforts should have succeeded in reducing interest rates immediately amidst waves of background noise from budget and tax legislation, court challenges, Federal Reserve missteps (this time cutting rates too soon), and the direction of the economy in general.

In this case, perhaps a better way to define success for DOGE is a meaningfully negative impact on the future supply of Treasury debt. Even that would not guarantee a decline in Treasury rates, so the premise of Yglesias’ tweet is somewhat shaky to begin with. Still, all else equal, we’d expect to see some downward pressure on yields if DOGE succeeds in this sense. But we must go further by recognizing that DOGE savings could well be reallocated to other spending initiatives. Then, the savings would not translate into lower supplies of Treasury debt after all.

Certainly, the DOGE team has made progress in identifying wasteful expenditures, inefficiencies, and poor controls on spending. But even if the $55 billion of estimated savings to date is reliable, DOGE has a long way to go to reach Musk’s stated objective of $2 trillion. There are some juicy targets, but it will be tough to get there in 17 more months, when DOGE is to stand down. Still, it’s not unreasonable to think DOGE might succeed in accomplishing meaningful deficit reduction.

But if bond traders have doubts about DOGE, it’s partly because Donald Trump and Elon Musk themselves keep giving them reasons. In my view, Musk and Trump have made a major misstep in toying with the idea of using prospective DOGE savings to fund “dividend checks” of $5,000 for all Americans. These would be paid by taking 20% of the guesstimated $2 trillion of DOGE savings. Musk’s expression of interest in the idea was followed by a bit of clusterfuckery, as Musk walked back his proposal the next day even as Trump jumped on board. PLEASE Elon, don’t give the Donald any crowd-pleasing ideas! And don’t lose sight of the underlying objective to reduce the burden of government and the public debt.

Now, Trump proposes that 60% of the savings accomplished by DOGE be put toward paying for outlays in future years. Sure, that’s deficit reduction, but it may serve to dull the sense that shrinking the federal government is an imperative. The mechanics of this are unclear, but as a first pass, I’d say the gain from investing DOGE savings for a year in low-risk instruments is unlikely to outweigh the foregone savings in interest costs from paying off debt today! Of course, that also depends on the future direction of interest rates, but it’s not a good bet to make with public funds.

Nor can the bond market be comforted by uncertainty surrounding legislation that would not only extend the Trump tax cuts, but will probably include various spending provisions, both cuts and increases. As of now, the mix of provisions that might accompany a deal among GOP factions is very much up in the air.

There is also trepidation about Trump’s aggressive stance toward the Federal Reserve. He promises to replace Jerome Powell as Fed Chairman, but with God knows whom? And Trump jawbones aggressively for lower rates. The Fed’s ill-advised rate cuts in the fall might have been motivated in part by an attempt to capitulate to the then-President Elect.

Trump’s Executive Order to create a sovereign wealth fund (SWF), which I recently discussed here, is probably not the most welcome news to bond investors. All else equal, placing tax or tariff revenue into such a fund would reduce the potential for deficit reduction, to say nothing of the idiocy of additional borrowing to purchase assets.

Finally, Trump has proposed what might later prove to be massive foreign policy trial balloons. Some of these are bound up with the creation of the SWF. They might generate revenue for the government without borrowing (mineral rights in Ukraine? Or Greenland?), but at this point there’s also a chance they’ll create massive funding needs (Gaza development?). Again, Trump seems to be prodding or testing counterparties to various negotiations… prodding diplomacy. It’s unlikely that anything too drastic will come of it from a fiscal perspective, but it probably doesn’t leave bond traders feeling easy.

At this stage, it’s pretty rash to conclude that the bond market “doesn’t believe in DOGE”. In fact, there is no doubt that DOGE is making some progress in identifying potential fraud and inefficiencies. However, bond traders must weigh a wide range of considerations, and Donald Trump has a tendency to kick up dust. Indeed, the so-called DOGE dividend will undermine confidence in debt reduction and bond prices.

If you want to induce a shortage, a price ceiling is a reliable way to do it. Usury laws are no exception to this rule. Private credit can be supplied plentifully to borrowers only when lenders are able to charge rates commensurate with other uses of their funds. Importantly, the rate charged must include a premium for the perceived risk of nonpayment. That’s critical when extending credit to financially-challenged applicants, who are often deserving but may be less stable or unproven.

No doubt certain lenders will seek to exploit vulnerable borrowers, but those borrowers are made less vulnerable when formal, mainstream sources of credit are available. A legal ceiling on the price of credit short-circuits this mechanism by restricting the supply to low-income borrowers, many of whom rely on credit cards as a source of emergency funds.

A couple of odd bedfellows, Senators Josh Hawley (R-MO) and Bernie Sanders (D-CT), are cosponsoring a bill to impose a cap of 10% on credit card interest rates. Sanders is an economic illiterate, so his involvement is no surprise. Hawley is otherwise a small government conservative, but in this effort he reveals a deep ignorance. Unfortunately, President Trump would be happy to sign their bill into law if it gets through Congress, having made a similar promise last fall during the campaign. Unfortunately, this is a typically populist stance for Trump; as a businessman he should know better.

Many consumers in the low-income segment of the market for credit have thin credit reports, a few delinquencies, or even defaults. Most of these potential borrowers struggle with expenses but generally meet their obligations. But even a few with the best intentions and work ethic will be unable to pay their debts. The segment is risky for lenders.

Card issuers might be able to compensate along a variety of margins. These include high minimum payments, stiff fees for late payments, tight credit limits (on lines, individual purchases, or revolving balances), deep relationship requirements, and limits on rewards. However, the most straightforward option for covering the risk of default is to charge a higher interest rate on revolving balances.

The total return on assets of credit-card issuing banks in 2023 was 3.33%, more than twice the 1.35% earned at non-issuing banks, asreported by the Federal Reserve. But that difference in profitability is well aligned with the incremental risk of unsecured credit card lending. According to BBVA Research:

“… studies confirm that higher interest rates on credit cards are not related to limited market competition but to greater levels of risk relative to other banking activities backed or secured by collateral. … In fact, an investigation into the risk-adjusted returns of credit cards banks versus all commercial banks suggests that over the long term, credit cards banks do not enjoy a significant advantage. … the market is characterized by participants that operate a high-risk business that requires elevated risk premiums.”

So card issuers are not monopolists. They face competition from other banks, often on the basis of non-rate product features, as well as “down-market” lenders who “specialize” in serving high-risk borrowers. These include payday lenders, pawn shop operators, vehicle title lenders, refund anticipation lenders, and informal loan sharks, all of whom tend to demand stringent terms. People turn to these alternatives and other informal sources when they lack better options. Hawley, Sanders, and Trump would unwittingly throw more credit-challenged consumers into this tough corner of the credit market if the proposed legislation becomes law.

Much of this was discussed recently by J.D. Tuccille, who writes that many consumers:

“… find banks, credit card companies, and other mainstream institutions rigid, uninterested in their business, and too closely aligned with snoopy government officials. Often, the costs and requirements imposed by government regulations make doing business with higher-risk, lower-income customers unattractive to mainstream finance.

‘The regulators are causing the opposite of the desired effect by making it so dangerous now to serve a lower-income segment,’ JoAnn Barefoot, a former federal official, including a stint as deputy controller of the currency, told the book’s author. She emphasized red tape that makes serving many potential customers a legal minefield“

Tuccille offers a revealing quote attributed to a bank official from a 2015 article in the Albuquerque Journal:

“‘Banking regulations stemming from the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 and the Patriot Act of 2001 have created an almost adversarial credit environment for people whose finances are in cash.‘“

In other words, for some time the government has been doing its damnedest to choke off bank-supplied credit to low-income and risky borrowers, many of whom are deserving. It’s tempting to say this was well-intentioned, but the truth might be more sinister. Onerous regulation of lending practices at mainstream financial institutions, including caps on credit card interest rates, is political gold for politicians hoping to exploit populist sentiment. “Good” politics often hold sway over predictable but unintended consequences, which later can be blamed on the very same financial institutions.

I want a federal government with a less pervasive presence in the private sphere. That’s why I oppose a U.S. sovereign wealth fund (SWF), but President Trump issued an executive order (EO) on February 3 setting in motion the creation of an SWF. It would hold various assets with the ostensible intent to earn a return benefiting American taxpayers.

Here are a few comments on the form an SWF might take:

1) How would the SWF be funded?

—Sales of federal assets like federal land, buildings, and the sale of extraction rights? These are probably the least offensive possibilities for funding an SWF, but the proceeds, if and when they materialize, should be used to pay off our massive federal debt, not to fund a governmental piggy bank.

—Taxes/Tariffs? Funding an SWF via taxes or tariffs would be contrary to the EO’s stated objective to “lessen the burden of taxes on American families and small businesses”. Moreover, it would be contrary to a pro-growth agenda, undermining any gains an SWF might produce.

—Borrowing? Another contradiction of a basic rationale for the SWF, which is “to promote fiscal sustainability”. It would mean more debt on top of a mountain of debt that is already growing at an unsustainable rate.

—“Deals” that might place assets under government ownership? Already, potential buyers of TikTok are singing the praises of a partnership with the SWF. Trump seems to think the government can acquire interests in certain enterprises in exchange for allowing them to operate in the U.S. He also believes that federal dollars can be used for development in order to acquire ownership capital. The federal government should not engage in the development of private resources. Business enterprises should remain private or be privatized, to the extent that their ownership has nothing to do with the provision of public goods.

2) What kinds of investments would be held in the SWF? Stocks and bonds? TikTok shares? Private equity? Crypto? The Gaza Riviera REIT?

These are all terrible ideas. Government ownership of the means of production, or socialism, virtually guarantees underperformance and subservience to political objectives. Federal acquisition of private businesses is not a legitimate function of the state.

There is no point in having the government hold a Bitcoin or crypto reserve. First, giving the U.S. government an interest in the private blockchain undermines the very purpose that most users feel gives the blockchain value. Second, the return on crypto depends only on price changes, and most forms of crypto are volatile. It is a stretch to believe that crypto assets have value in promoting “fiscal sustainability” or national security.

3) How would the SWF’s assets and earnings ultimately be used?

The EO plainly states that earnings in the SWF are to be used to promote fiscal sustainability and benefit taxpayers. In the presence of a large and growing national debt, the best path toward those objectives would be to use any and all spare funds to pay off debt and limit the explosive interest burden it imposes. This puts the funds back into hands of private investors, who will respond to market incentives by deploying the capital as they see fit. Does anyone truly think government planners know better how to put those funds to use?

SWF and Future Debt Service

Just to clarify matters, let’s quantify two alternatives: 1) pay off debt immediately; 2) create an SWF to invest funds and pay off debt later. Suppose the government stumbles upon a spare $100. It can immediately pay off $100 of debt and avoid a certain $3.50 in interest expense in year one. If instead an SWF invests the funds at an expected (but uncertain) return of 7%, then perhaps a greater reduction in the debt can be made a year later. How much? Not $107, but only $103.50 (assuming the 7% return is realized) because the $3.50 interest expense on the debt was not avoided in year one. The SWF must earn twice the interest cost on debt to break even on the proposition. That might be possible for an average return over many years, but the returns will vary and the government is likely to botch the job in any case.

An Itch For Intervention

The SWF is subject to dangers inherent in many government activities. One is that the funds held in reserve might be used as a tool of market intervention and/or political mischief, much as Joe Biden attempted to tamp down oil prices by releasing millions of barrels from the Strategic Petroleum Reserve. An administration having available a large pool of financial assets might be tempted to use it to intervene in various markets to manipulate asset prices. And even if you happen to like the interventions of one administration, you might hate the interventions of another.

The Scratch That Corrupts

In testament to the inefficacy and corruption inherent in government intervention in private markets, Peter Earle offers a number of examples of government planning gone awry. It’s not difficult to understand the dysfunction:

“A sovereign wealth fund would not, whatever the intentions of its government administrators, be guided purely by market signals but rather by political interests. That virtually ensures poor investment choices, investments in politically favored industries, and/or wasteful subsidies tending to yield subpar returns.

“Government officials will not have the same rigorous concern for opportunity costs that drives private investors and for-profit managers, as bureaucratic decision-making is often guided by political priorities and budget cycles rather than the disciplined allocation of capital to its most productive use. The Knowledge Problem is real — and ignoring it is expensive.“

“…there are systemic governance issues and regulatory gaps that can enable SWFs to act as conduits of corruption, money laundering, and other illicit activities.“

Therefore, the management and operations of an SWF require great transparency as well as strong governance and oversight. This obviously adds a layer of cost as well.

Sound Planning

There is an economic rationale for holding funds in reserve for certain, earmarked purposes. For example, private businesses usually maintain reserves for the upkeep or replacement of physical capital. Shouldn’t the government do the same for public infrastructure such as highways or harbors? Public investments in physical capital should be planned such that the flow of tax revenue is adequate to replenish infrastructure from wear and tear. To the extent that the necessary expenditures are “lumpy”, however, a maintenance reserve fund is sound practice, as long as its management is transparent and accountable, and its holdings represent prudent risks.

Another example is the maintenance of a reserve fund for pension payments. This is a reasonable and even necessary practice under traditional defined benefit plans, but those plans have often fallen short of their obligations in practice. The private sector stayed ahead of this risk by shifting overwhelmingly to defined contribution plans. As part of this shift, the existing pension obligations of many private entities were converted to vested “cash value” balances. The public sector should do the same, putting employees in charge of their own retirement savings.

Countries with SWFs tend to be small and also tend to run budget surpluses. Very often, they are funded with revenue earned from abundant natural resources. But even those governments short-change their citizens by failing to reduce tax rates, which would promote growth.

Nonsensical Appeal to Nationalism

Why does the creation of an SWF sound so good to people who should know better? I think it has something to do with the nationalist urge to embrace symbols of patriotic strength. An SWF might evoke the emotive impact of phrases like “sound money” or “a strong dollar”. But in the presence of a large public debt and large, continuing budget deficits, the kind of SWF envisioned by Trump would be counterproductive. Future obligations to pay down the public debt are better addressed in the present, to the extent possible. The government has no business hoarding private financial assets as a means of outrunning debt. Sure, the return on equity usually exceeds the interest rate on public debt, but private investors are better at allocating capital than government, so government should not attempt to take on that role.

Ongoing increases in the resources dedicated to health care in the U.S., and their prices, are driven primarily by the abandonment of market forces. We have largely eliminated the incentives that markets create for all buyers and sellers of health care services as well as insurers. Consumers bear little responsibility for the cost of health care decisions when third parties like insurers and government are the payers. A range of government interventions have pushed health care spending upward, including regulation of insurers, consumer subsidies, perverse incentives for consolidation among health care providers, and a mechanism by which pharmaceutical companies negotiate side payments to insurers willing to cover their drugs.

It’s not yet clear whether the Trump Administration and its “Make America Healthy Again” agenda will serve to liberate market forces in any way. Skeptics can be forgiven for worrying that MAHA will be no more than a cover for even more centrally-planned health care, price controls, and regulation of the pharmaceutical and food industries, not to mention consumer choices. Robert F. Kennedy Jr., who is likely to be confirmed by the Senate as Donald Trump’s Secretary of Health and Human Services, has strong and sometimes defensible opinions about nutrition and public health policies. He is, however, an inveterate left-winger and is not an advocate for market solutions. Trump himself has offered only vague assurances on the order of “You won’t lose your coverage”.

Government Control

The updraft in health care inflation coincided with government dominance of the sector. Steven Hayward points out that the cost pressure began at about the same time as Medicare came into existence in 1965. This significantly pre-dates the trend toward aging of the population, which will surely exacerbate cost pressures as greater concentrations of baby boomers approach or exceed life expectancy over the next decade.

Government now controls or impinges on about 84% of health care spending in the U.S., as noted by Michael F. Cannon. The tax deductibility of employer-provided health insurance is a massive example of federal manipulation and one that is highly distortionary. It reinforces the prevalence of third-party payments, which takes decision-making out of consumers’ hands. Equalizing the tax treatment of employer-provided health coverage would obviously promote tax equity. Just as importantly, however, tax-subsidized premiums create demand for inflated coverage levels, which raise prices and quantities. And today, the federal government requires coverages for routine care, going beyond the basic function of insurance and driving the cost of care and insurance upward.

The traditional non-portability of employer-provided coverage causes workers with uninsurable pre-existing conditions to lose coverage when they leave a job. Thus, Cannon states that the tax exclusion for employer coverage penalizes workers who instead might have chosen portable individual coverage in a market setting without tax distortions. Cannon proposes a reform whereby employer coverage would be replaced with deposits into tax-free Universal Health Accounts owned by workers, who could then purchase their own insurance.

In 2024, federal subsidies for health insurance coverage were about $2 trillion, according to the Congressional Budget Office (CBO). Those subsidies are projected to grow to $3.5 trillion by 2034 (8.5% of GDP). Joel Zinberg and Liam Sigaud emphasize the wasteful nature of premium subsidiesfor exchange plans mandated by the Affordable Care Act (ACA), better known as Obamacare. Subsidies were temporarily expanded in 2021, but only until 2026. They should be allowed to expire. These subsidies increase the demand for health care, but they are costly to taxpayers and are offered to individuals far above the poverty line. Furthermore, as Zinberg and Sigaud discuss, subsidized coverage for the previously uninsured does very little to improve health outcomes. That’s because almost all of the health care needs of the formerly uninsured were met via uncompensated care at emergency rooms, clinics, medical schools, and physician offices.

Proportionate Consumption

Perhaps surprisingly, and contrary to popular narratives, health care spending in the U.S. is not really out-of-line with other developed countries relative to personal income and consumption expenditures (as opposed to GDP). We spend more on health care because we earn and consume more of everything. This shouldn’t allay concern over health care spending because our economic success has not been matched by health outcomes, which have lagged or deteriorated relative to peer nations. Better health might well have allowed us to spend proportionately less on health care, but this has not been the case. There are explanations based on obesity levels and diet, but important parts of the explanation can be found elsewhere.

It should also be noted that a significant share of our decades-long increases in health care spending can be attributed to quantities, not just prices, as explained at the last link above.

Health Consequences

The ACAdid nothing to slow the rise in the cost of health care coverage. In fact, if anything, the ACA cemented government dominance in a variety of ways, reinforcing tendencies for cost escalation. Even worse, the ACA had negative consequences for patient care. David Chavous posted a good X thread in December on some of the health consequences of Obamacare:

1) The ACA imposed penalties on certain hospital readmissions, which literally abandoned people at death’s door.

2) It encouraged consolidation among providers in an attempt to streamline care and reduce prices. This reduced competitive pressures, however, which had the “unforeseen” consequence of raising prices and discouraging second opinions. The former goes against all economic logic while the latter goes against sound medical decision-making.

3) The ACA forced insurers to offer fewer options, increasing the cost of insurance by encouraging patients to wait until they had a pre-existing condition to buy coverage. Care was almost certainly deferred as well. Ultimately, that drove up premiums for healthy people and worsened outcomes for those falling ill.

4) It forced drug companies to negotiate with Pharmacy Benefit Managers (PBMs) to get their products into formularies. The PBMs have acted as classic middlemen, accomplishing little more than driving up drug prices and too often forcing patients to skimp on their prescribed dosage, or worse yet, increasing their vulnerability to lower-priced quackery.

The Insurers

So the ACA drastically increased the insured population (including the new burden of covering pre-existing conditions). It also forced insurers to meet draconian cost-control thresholds. Little wonder that claim rejection increased, a phenomenon often at the root of public animosity toward health insurers. Peter Earle cites several reasons for the increase in denial rates while noting that claim rejection has made little difference in insurer profit margins.

Matt Margolis points out that under the ACA, we’ve managed to worsen coverage in exchange for higher premiums and deductibles. All while profits have been capped. Claim denials or delays due to pre-authorization rules (which delay care) have become routine following the implementation of Obamacare.

Perhaps the biggest mistake was forcing insurers to cover pre-existing conditions without allowing them to price for risk. Rather than forcing healthy individuals to pay for risks they don’t face, it would be more economically sensible to directly subsidize coverage for those in high-risk pools.

Noah Smith also defends the health insurers. For example, while UnitedHealth Group has the largest market share in the industry, its net profit margin of 6.1% is only about half of the average for the S&P 500. Other major insurers earn even less by this metric. Profits just don’t explain why American health care spending is so high. Ultimately, the services delivered and charges assessed by providers explain high U.S. health care spending, not insurer profits or administrative costs.

Under the ACA, insurance premiums pay the bulk of the cost of health care delivery, including the cost of services more reasonably categorized as routine health maintenance. The latter is like buying insurance for oil changes. Furthermore, there are no options to decline any of the ten so-called “essential benefits” under the ACA, thus increasing the cost of coverage.

Medical Records

Arnold Kling argues that the ACA’s emphasis on uniform, digitized medical records is not a productive avenue for achieving efficiencies in health care delivery. Moreover, it’s been a key factor driving the increasing concentration in the health care industry. Here is Kling:

“My point is that you cannot do this until you tighten up the health care delivery process, making it more rigid and uniform. And I would not try to do that. Health care does not necessarily lend itself to being commoditized. You risk making health care in America less open to innovation and less responsive to the needs of people.

“So far, all that has been accomplished by the electronic medical records drive has been to put small physician practices out of business. They have not been able to absorb the overhead involved in implementing these systems, so that they have been forced to lose their independence, primarily to hospital-owned conglomerates.”

Separating Health and State

The problem of rising health care costs in the U.S. is capsulized by Bryan Caplan in his call for the separation of health and state. The many policy-driven failures discussed above offer more than adequate rationale for reform. The alternative suggested by Caplan is to “pull the plug” on government involvement in health care, relying instead on the free market.

Caplan debunks a few popular notions regarding the appropriate role for markets in health care and health insurance. In particular, it’s often alleged that moral hazard and adverse selection would encourage unhealthy behaviors and encourage the worst risks to over-insure, causing insurance markets to fail. But these problems arise only when risk is not priced efficiently, precisely what the government has accomplished by attempting to equalizing rates.

Pulling the plug on government interference in health care would also mean deregulating both insurance offerings and pricing, encouraging the adoption of portable coverage, expediting drug approvals based on peer-country approvals, reforming pharmacy benefit management, ending deadly Medicare drug price controls, and encouraging competition among health care providers.

Value Vs. Volume

There are a host of other reforms that could bring more sanity to our health care system. Many of these are covered here by Sebastian Caliri, with some emphasis on the potential role of AI in improving health care. Some of these are at odds with Kling’s skepticism regarding digitized health records.

Perhaps the most fundamental reforms entertained by Caliri have to do with health care payments. One is to make payments dependent on outcomes rather than diagnostic codes established and priced by the American Medical Association. To paraphrase Caliri, it would be far better for Americans to pay for value rather than volume.

Another payment reform discussed by Caliri is expanding direct payments to providers such as capitation fees, whereby patients pay to subscribe to a bundle of services for a fixed fee. Finally, Caliri discusses the importance of achieving “site-neutral payments”, eliminating rules that allow health systems to charge a higher premium relative to independent providers for identical services.

For what it’s worth, Arnold Kling disagrees that changing payment metrics would be of much help because participants will learn to game a new system. Instead, he emphasizes the importance of reducing consumer incentives for costly treatments having little benefit. No dispute there!

Avoid the Single-Payer Calamity

I’ll close this jeremiad with a quote from Caliri’s piece in which he contrasts the knee-jerk, leftist solution to our nation’s health care dilemma with a more rational, market-oriented approach:

“Single payer solutions and government control favored by the left are no solutions at all. Moving to a monopsonist system like Canada is a recipe for strangling innovation and rationing access. Just ask our neighbors to the north who have to wait a year for orthopedic surgery. The UK’s National Health Service (NHS) is teetering on the brink of collapse. We need to sort out some other way forward.

“Other parts of the economy provide inspiration for what may actually work. In the realm of information technology, for example, fifty years has taken us from expensive four operation calculators to ubiquitous, free, artificial intelligence capable of passing the Turing Test. We can argue about the precise details but most of this miracle came from profit-seeking enterprises competing in a free market to deliver the best value for the buyer’s dollar.“

In advanced civilizations the period loosely called Alexandrian is usually associated with flexible morals, perfunctory religion, populist standards and cosmopolitan tastes, feminism, exotic cults, and the rapid turnover of high and low fads---in short, a falling away (which is all that decadence means) from the strictness of traditional rules, embodied in character and inforced from within. -- Jacques Barzun