Tariffs have far-reaching effects that strike some as counter-intuitive, but they are real forces nevertheless. Much like any selective excise tax, tariffs reduce the quantity demanded of the taxed good; buyers (importers) pay more, but sellers of the good (foreign exporters) extract less revenue. Suppose those sellers happen to be the primary buyers of what you produce. Because they have less to spend, you also will earn less revenue.

The Lerner Effect

The imposition of tariffs by the U.S. means that foreigners have fewer dollars to spend on exports from the U.S. (as well as fewer dollars to invest in the U.S. assets like Treasury bonds, stocks, and physical capital). That much is true without any change in the exchange rate. However, lower imports also imply a stronger dollar, further eroding the ability of foreigners to purchase U.S. exports.

The implications of the import tariff for U.S. exports may be even more starkly negative. Scott Sumner discusses an economic principle called Lerner Symmetry: a tax on imports can be the exact equivalent of a tax on exports! That’s because two-directional trade flows rely on two-directional flows of income.

Note that this has nothing to do with foreign retaliation against U.S. trade policy, although that will also hurt U.S. exporters. Nor is it a consequence of the very real cost increase that tariffs impose on U.S. export manufacturers who require foreign inputs. That’s a separate issue. Lerner Symmetry is simply part of the mechanics of trade flows in response to a one-sided tariff shock.

Assumptions For Lerner Symmetry

Scott Sumner enumerated certain conditions that must be in place for full Lerner Symmetry. While they might seem strict, the Lerner effect is nevertheless powerful under relaxed assumptions (though somewhat weaker than full Lerner Symmetry).

As Sumner puts it, while full Lerner Symmetry requires perfect competition, nearly all markets are “workably competitive”. In the longer-run, assumptions of price flexibility and full employment are anything but outlandish. Complete non-retaliation is an unrealistic assumption, given the breadth and scale of the Trump tariffs. Some countries will retaliate, but not all, and it is certainly not in their best interests to do so. The assumption of balanced trade is one and the same as the assumption of no capital flows; a departure from these “two” assumptions weakens the symmetry between tariffs and export taxes because a reduction in capital flows takes up some of the slack from lower revenue earned by foreign producers.

Trump Tariff Impacts

So here we are, after large hikes in tariffs and perhaps more on the way. Or perhaps more exceptions will be carved out for favored supplicants in return for concessions of one kind or another. All that is economically and ethically foul.

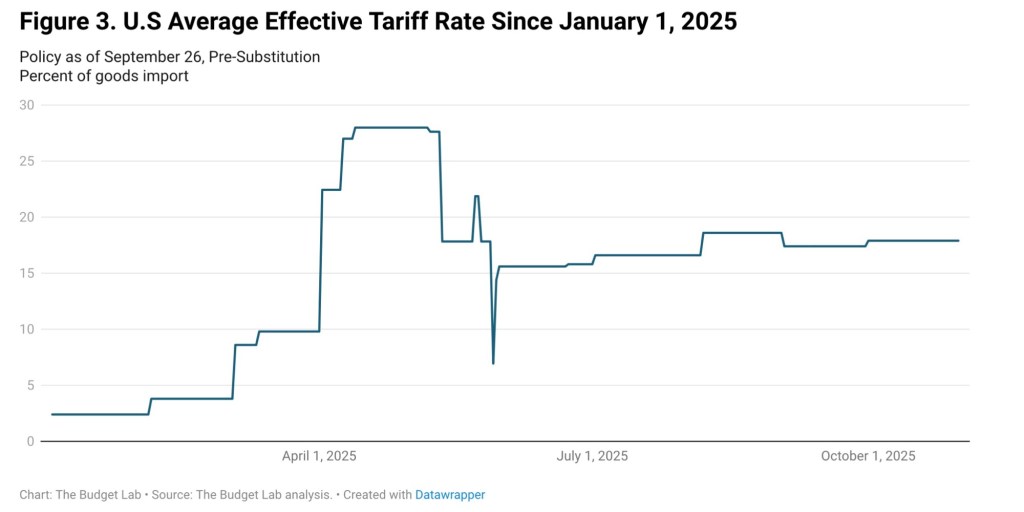

But how are imports and exports faring? Here I’ll quote the Yale Budget Lab’s (YBL) September 26th report on tariffs, which includes the chart shown at the top of this post:

“Consumers face an overall average effective tariff rate of 17.9%, the highest since 1934. After consumption shifts, the average tariff rate will be 16.7%, the highest since 1936. …

The post-substitution price increase settles at 1.4%, a $1,900 loss per household.“

The “post-substitution” modifier refers to the fact that price increases caused by tariffs would be somewhat larger but for consumers’ attempts to find lower-priced domestic substitutes. Suppose the PCE deflator ends 2025 with a 2.8% annual increase. The YBL’s price estimate implies that absent the Trump tariffs, the PCE would have increased 1.4%. If that seems small to you (and the tariff effect seems large to you), recall that monetary policy has been and remains moderately restrictive, so we might have expected some tapering in the PCE without tariffs.

We also know that the early effects of the tariffs have been dominated by thinner margins earned by businesses on imported goods. Those firms have been swallowing a large portion of the tariff burden, but they will increasingly attempt to pass the added costs into prices.

But back to the main topic … what about exports? Unfortunately, the data is subject to lags and revisions, so it’s too early to say much. However, we know exports won’t decline as much as imports, given the lack of complete Lerner symmetry. YBL predicts a drop in exports of 14%, but that includes retaliatory effects. In August the WTO predicted only about a 4% decline, which would be about half the decline in imports.

Seeking Compensatory Rents

More telling perhaps, and it may or may not be a better indicator of the Lerner effect, is the clamoring for relief by American farmers who face diminished export opportunities. As Tyler Cowen says, “Lerner Symmetry Bites”. Other industries will feel the pinch, but many are likely preoccupied with the more immediate problem of increases in the direct cost of imported materials and components.

The farm lobby is certainly on its toes. The Trump Administration is now asking U.S. taxpayers to subsidize soybean producers to the tune of $15 billion. Those exporting farmers are undoubtedly victimized by tariffs. But so much for deficit reduction! More from Cowen:

“Using tariff revenue to subsidize the losses of exporters is a textbook illustration of Lerner Symmetry because the export losses flow directly from the tax on imports! The irony is that President Trump parades the subsidies as a victory while in fact they are simply damage control for a policy he created.“

A List of Harms

Tariffs are as distortionary as any other selective excise tax. They restrict choice and penalize domestic consumers and businesses, whose judgement of cost and quality happen to favor goods from abroad. Tariffs create cost and price pressures in some industries that both erode profit margins and reduce real incomes. For consumers, a tariff is a regressive tax, harming the poor disproportionately.

Tariffs also diminish foreign flows of capital to the U.S., slowing the long-term growth of the economy as well as productivity growth and real wages. And the Lerner effect implies that tariffs harm U.S. exporters by reducing the dollars available to foreigners for purchasing goods from the U.S. In these several ways, Americans are made worse off by tariffs.

We now see attempts to cover for the damage done by tariffs by subsidizing the victims. A “tariff dividend” to consumers? Subsidies to exporters harmed by the Lerner effect? In both cases, we would forego the opportunity to pay down the bloated public debt. Thus, the American taxpayer will be penalized as well.

There’s a hopeful narrative making the rounds that artificial intelligence will prove to be such a boon to the economy that we need not worry about high levels of government debt. AI investment is already having a substantial economic impact. Jason Thomas of Carlyle says that AI capital expenditures on such things as data centers, hardware, and supporting infrastructure account for about a third of second quarter GDP growth (preliminarily a 3% annual rate). Furthermore, he says relevant orders are growing at an annual rate of about 40%. The capex boom may continue for a number of years before leveling off. In the meantime, we’ll begin to see whether AI is capable of boosting productivity more broadly.

Unfortunately, even with this kind of investment stimulus, there’s no assurance that AI will create adequate economic growth and tax revenue to end federal deficits, let alone pay down the $37 trillion public debt. That thinking puts too much faith in a technology that is unproven as a long-term economic engine. It would also be a naive attitude toward managing debt that now carries an annual interest cost of almost $1 trillion, accounting for about half of the federal budget deficit.

Boom Times?

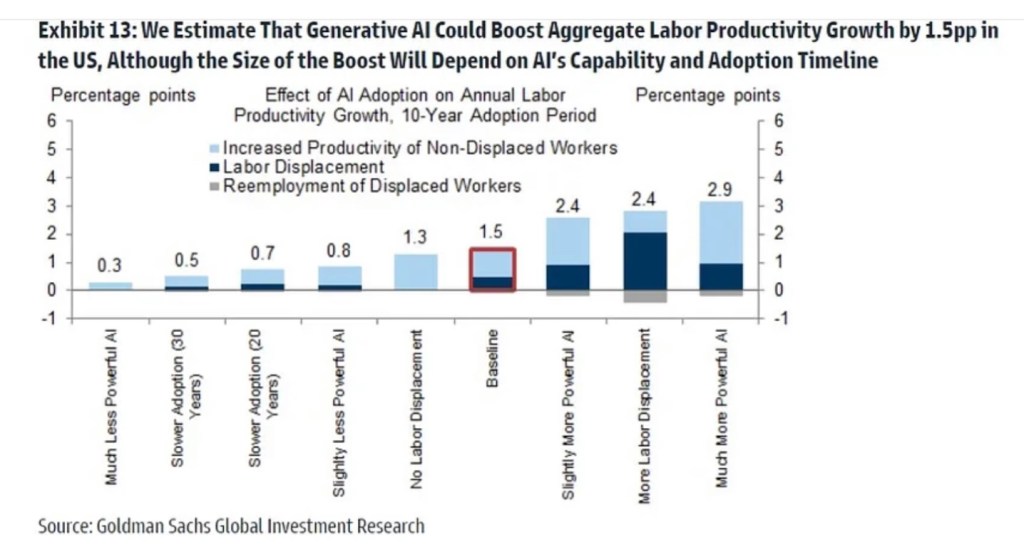

Predictions of AI’s long-term macro impact are all over the map. Goldman Sachs estimates a boost in global GDP of 7% over 10 years, which is not exactly aggressive. Daren Acemoglu has beenevenmore conservative, estimating a gain of 0.7% in total factor productivity over 10 years. Tyler Cowen has been skeptical about the impact of AI on economic growth. For an even more pessimistic take see these comments.

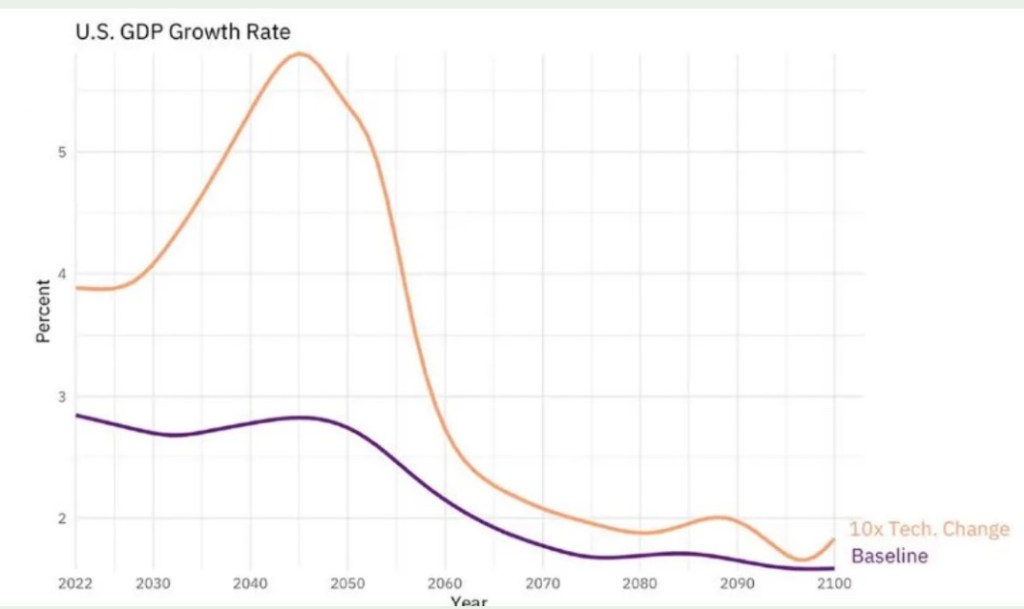

In July, however, Seth Benzell of the Stanford Digital Economy Lab discussed some simulations showing impressive AI-induced growth (see chart at top). The simulations project additional U.S. GDP growth of between 1% – 3% annually over the next 75 years! The largest boost in growth occurs now through the 2050s. This would produce a major advance in living standards. It would also eliminate the federal deficit and cure our massive entitlement insolvency, but the result comes with heavy qualifications. In fact, Benzell ultimately throws cold water on the notion that AI growth will be strong enough to reduce or even stabilize the public debt to GDP ratio.

The Scarcity Spoiler

The big hitch has to do with the scarcity of capital, which I’ve described asanimpediment to widespread AI application. Competition for capital will drive interest rates up (3% – 4%, according to Benzell’s model). Ongoing needs for federal financing intensify that effect. But it might not be so bad, according to Benzell, if climbing rates are accompanied by heightened productivity powered by AI. Then, tax receipts just might keep-up with or exceed the explosion in the government’s interest obligations.

A further complication cited by Benzell lurks in insatiable demands for public spending, and politicians who simply can’t resist the temptation to buy votes via public largesse. Indeed, as we’ve already seen, government will try to get in on the AI action, channeling taxpayer funds into projects deemed to be in the public interest. And if there are segments of the work force whose jobs are eliminated by AI, there will be pressure for public support. So even if AI succeeds in generating large gains in productivity and tax revenue, there’s very little chance we’ll see a contagion of fiscal discipline in Washington DC. This will put more upward pressure on interest rates, giving rise to the typical crowding out phenomenon, curtailing private investment in AI.

Playing Catch-Up

The capex boom must precede much of the hoped-for growth in productivity from AI. Financing comes first, which means that rates are likely to rise sooner than productivity gains can be expected. And again, competition from government borrowing will crowd out some private AI investment, slowing potential AI-induced increases in tax revenue.

There’s no chance of the converse: that AI investment will crowd out government borrowing! That kind of responsiveness is not what we typically see from politicians. It’s more likely that ballooning interest costs and deficits generally will provoke even more undesirable policy moves, such as money printing or rate ceilings.

The upshot is that higher interest rates will cause deficits to balloon before tax receipts can catch up. And as for tax receipts, the intangibility of AI will create opportunities for tax flight to more favorable jurisdictions, a point well understood by Benzell. As attorneys Bradford S. Cohen and Megan Jones put it:

“Digital assets can be harder to find and more easily shifted offshore, limiting the tax reach of the U.S. government.”

AI Growth Realism

Benzell’s trepidation about our future fiscal imbalances is well founded. However, I also think Benzell’s modeled results, which represent a starting point in his analysis of AI and the public debt, are too optimistic an assessment of AI’s potential to boost growth. As he says himself,

“… many of the benefits from AI may come in the form of intangible improvements in digital consumption goods. … This might be real growth, that really raises welfare, but will be hard to tax or even measure.”

This is unlikely to register as an enhancement to productivity. Yet Benzell somehow buys into the argument that AI will lead to high levels of unemployment. That’s one of his reasons for expecting higher deficits.

My view is that AI will displace workers in some occupations, but it is unlikely to put large numbers of humans permanently out of work and into state support. That’s because the opportunity cost of many AI applications is and will remain quite high. It will have to compete for financing not only with government and more traditional capex projects, but with various forms of itself. This will limit both the growth we are likely to reap from AI and losses of human jobs.

Sovereign Wealth Fund

I have one other bone to pick with Benzell’s post. That’s in regard to his eagerness to see the government create a sovereign wealth fund. Here is his concluding paragraph:

“Instead of contemplating a larger debt, we should instead be talking about a national sovereign wealth fund, that could ‘own the robots on behalf of the people’. This would both boost output and welfare, and put the welfare system on an indefinitely sustainable path.”

Whether the government sells federal assets or collects booty from other kinds of “deals”, the very idea of accumulating risk assets in a sovereign wealth fund undermines the objective to reduce debt. It will be a struggle for a sovereign wealth fund to consistently earn cash returns to compensate for interest costs and pay down the debt. This is especially unwise given the risk of rising rates. Furthermore, government interests in otherwise private concerns will bring cronyism, displacement of market forces by central planning, and a politicization of economic affairs. Just pay off the debt with whatever receipts become available. This will free up savings for investment in AI capital and hasten the hoped-for boom in productivity.

Summary

AI’s contribution to economic growth probably will be inadequate and come too late to end government budget deficits and reduce our burgeoning public debt. To think otherwise seems far fetched in light of our historical inability to restrain the growth of federal spending. Interest on the federal debt already accounts for about half of the annual budget deficit. Refinancing the existing public debt will entail much higher costs if AI capex continues to grow aggressively, pushing interest rates higher. These dynamics make it pretty clear that AI won’t provide an easy fix for federal deficits and debt. In fact, ongoing federal borrowing needs will sop up savings needed for AI development and diffusion, even as the capital needed for AI drives up the cost of funds to the government. It’s a shame that AI won’t be able to crowd out government.

As a long-time user of macroeconomic statistics, I admit to longstanding doubts about their accuracy and usefulness for policymaking. Almost any economist would admit to the former, not to mention the many well known conceptual shortcomings in government economic statistics. However, few dare question the use of most macro aggregates in the modeling and discussion of policy actions. One might think conceptual soundness and a reasonable degree of accuracy would be requirements for serious policy deliberation, but uncertainties are almost exclusively couched in terms of future macro developments; they seldom address variances around measures of the present state of affairs. In many respects, we don’t even know where we are, let alone where we’re going!

Early and Latter Day Admonitions

In the first of a pair of articles, Reuven Brenner discusses the hazards of basing policy decisions on economic aggregates, including critiques of these statistics by a few esteemed economists of the past. The most celebrated developer of national income accounting, Simon Kuznets, was clear in expressing his reservations about the continuity of the U.S. National Income and Product Accounts during the transition to a peacetime economy after World War II. The government controlled a large share of economic activity and prices during the war, largely suspending the market mechanism. After the war, market pricing and private decision-making quickly replaced government and military planners. Thus, the national accounts began to reflect values of production inherent in market prices. That didn’t necessarily imply accuracy, however, as the accounts relied (and still do) on survey information and a raft of assumptions.

The point is that the post-war economic results were not remotely comparable to the data from a wartime economy. Comparisons and growth rates over this span are essentially meaningless. As Brenner notes, the same can be said of the period during and after the pandemic in 2020-21. Activity in many sectors completely shut down. In many cases prices were simply not calculable, and yet the government published aggregates throughout as if everything was business as usual.

More than a decade after Kuznets, the game theorists Oskar Morgenstern and John von Neumann both argued that the calculations of economic aggregates are subject to huge degrees of error. They insisted that the government should never publish such data without also providing broad error bands.

Morgenstern delineated several reasons for the inaccuracies inherent in aggregate economic data. These include sampling errors, both private and political incentives to misreport, systematic biases introduced by interview processes, and inherent difficulties in classifying components of production. Also, myriad assumptions must be fed into the calculation of most economic aggregates. A classic example is the thorny imputation of services provided by owner-occupied homes (akin to the value of services generated by rental units to their occupants). More recently. Charles Manski reemphasized Morganstern’s concerns about the aggregates, reaching similar conclusions as to the wisdom of publishing wide ranges of uncertainty.

Real or Unreal?

Estimates of real spending and production are subject to even larger errors than estimates of nominal values. The latter are far simpler to measure, to the extent that they represent a simple adding up of current amounts spent (or income earned) over the course of a given time period. In other words, nominal aggregates represent the sum of prices times quantities. To estimate real quantities, nominal values must be adjusted (deflated) by price aggregates, the measurement of which are fraught with difficulties. Spending patterns change dramatically over time as preferences shift; technology advances, new goods and services replace others, and the qualities of goods and services evolve. A “unit of output” today is usually far different than what it was in the past, and adjusting prices for those changes is a notorious challenge.

This difficulty offers a strong rationale for relying on nominal quantities, rather than real quantities, in crafting certain kinds of policy. Perhaps the best example of the former is so-calledmarket monetarism and monetary policy guided by nominal GDP-level targeting, as championed by Scott Sumner.

Government’s Contribution

Another fundamental qualm is the inconsistency between data on government’s contribution to aggregate production versus private sector contributions. This is similar in spirit to Kuznets’ original critique. Private spending is valued at market prices of final output, whereas government spending is often valued at administered prices or at input cost.

An even deeper objection is that much of the value of government output is already subsumed in the value of private production. Kuznets himself thought so! For example, to choose two examples, public infrastructure and law enforcement contribute services which enhance the private sector’s ability to reliably produce and deliver goods to market. To add the government’s “output” of these services separately to the aggregate value of private production is to double count in a very real sense. Even Tyler Cowen is willing to entertain the notion that including defense spending in GDP is double counting. The article to which he links goes further than that.

Nevertheless, our aggregate measures allow for government spending to drive fluctuations in our estimates of GDP growth from one period to another. It’s reasonable to argue that government spending should be reported as a separate measure from private GDP.

But what about the well known Keynesian assertion that an increase in government spending will lift output by some multiple of the change? That proposition is considered valid (by Keynesians) only when resources are idle. Of course, today we see steady growth of government even at full employment, so the government’s effort to commandeer resources creates scarcity that crowds out private activity.

Measurement and Policy Uncertainty

Acting on published estimates of economic aggregates is hazardous for a number of other reasons. Perhaps the most basic is that these aggregates are backward-looking. A policy activist would surely agree that interventions should be crafted in recognition of concurrent data (were it available) or, even better, on the basis of reliable predictions of the future. Financial market prices are probably the best source of such forward-looking information.

In addition, revising the estimates of aggregates and their underlying data is an ongoing process. Initial published estimates are almost always based on incomplete data. Then the estimates can change substantially over subsequent months, underscoring uncertainty about the state of the economy. It is not uncommon to witness consistent biases over time in initial estimates, further undermining the credibility of the effort.

Even worse, substantial annual revisions and so-called “benchmark revisions” are made to aggregates like GDP, inflation, and employment data. Sometimes these revisions alter economic history substantially, such as the occurrence and timing of recessions. All this implies that decisions made on the basis of initial or interim estimates are potentially counterproductive (and on a long enough timeline, every aggregate is an “interim” estimate). At a minimum, the variable nature of revisions, which is an unavoidable aspect of publishing aggregate statistics, magnifies policy uncertainty.

Case Studies?

Brenner cites two historical episodes as support for his argument that aggregates are best ignored by policymakers. They are interesting anecdotes, but he gives few details and they hardly constitute proof of his thesis. In 1961, Hong Kong’s financial secretary stopped publishing all but “the most rudimentary statistics”. Combined with essentially non-interventionist policy including low tax rates, Hong Kong ran off three decades of impressive growth. On the other hand, Argentina’s long economic slide is intended by Brenner to show the downside of relying on economic aggregates and interventionism.

Bad Models, Bad Policy

It’s easy to see that economic aggregates have numerous flaws, rendering them unreliable guides for monetary and fiscal policy. Nevertheless, their publication has tended to encourage the adoption of policy interventions. This points to another issue lurking in the background: the role of economic aggregates in shaping the theory and practice of macroeconomics and the models on which policy recommendations are based. The conceptual difficulties surrounding aggregates, and the errors embedded within measured aggregates, have helped to foster questionable model treatments from a scientific perspective. For example, Paul Romer has said:

“Macroeconomists got comfortable with the idea that fluctuations in macroeconomic aggregates are caused by imaginary shocks, instead of actions that people take, after Kydland and Prescott (1982) launched the real business cycle (RBC) model. … [which] explains recessions as exogenous decreases in phlogiston.”

This is highly reminiscent of a quip by Brenner that macroeconomics has become a bit like astrology. A succession of macro models after the RBC model inherited the dependence on phlogiston. Romer goes on to note that model dependence on “imaginary” forces has aggravated the longstanding problem of statistically identifying individual effects. He also debunks the notion that adding expectations to models helps solve the identification problem. In fact, Romer insists that it makes it worse. He goes on to paint a depressing picture of the state of macroeconomics, one to which its reliance on faulty aggregates has surely contributed.

Aggregates also mask the detailed, real-world impacts of policies that invariably accompany changes in spending and taxes. While a given fiscal policy initiative might appear to be neutral in aggregate terms, it is almost always distortionary. For example, spending and tax programs always entail a redirection of resources, whether a consequence of redistribution, large-scale construction, procurement, or efforts to shape the industrial economy. These are usually accompanied by changes in the structure of incentives, regulatory requirements, and considerable rent seeking activity. Too often, outlays are dedicated to shoring up weak sectors of the economy, short-circuiting the process of creative destruction that serves to foster economic growth. Yet the macro models gloss over all the messy details that can negate the efficacy of activist fiscal policies.

Conclusion

The reliance of macroeconomic policy on aggregates like GDP, employment, and inflation statistics certainly has its dangers. These measures all suffer from theoretical problems, and they simply cannot be calculated without errors. They are backward-looking, and the necessity of making ongoing revisions leads to greater uncertainty. But compared to what? There are ways of shifting the focus to measures subject to less uncertainty, such as nominal income rather than real income. A number of theorists have proposed market-based methods of guiding policy, including Fischer Black. This deserves broader discussion.

The problems of aggregates are not solely confined to measurement. For example, national income accounting, along with the Keynesian focus on “underconsumption” during recessions, led to the fallacious view that spending decisions drive the economy. This became macroeconomic orthodoxy, driving macro mismanagement for decades and leading to inexorable growth in the dominance of government. Furthermore, macroeconomic models themselves have been corrupted by the effort to explain away impossibly error-prone measurements of aggregate activity.

Brenner has a point: it might be more productive to ignore the economic aggregates and institute stable policies which reinforce the efficacy of private markets in allocating resources. If nothing else, it makes sense to feature the government and private components separately.

Supporters of President Trump’s hard line on trade make so many false assertions that it’s hard to keep up. I’ve addressed several of these in earlier posts and I’ll address two more fallacies here: 1) that the U.S. manufacturing sector is in a state of crisis; and 2) that tariffs played a key role in promoting economic growth in the U.S. during the so-called gilded age of the late 19th and early 20th centuries.

Security

First, let’s revisit one tenet of protectionism: national security demands self-sufficiency. This undergirds the story that we must produce physical “things”, in addition to often higher-valued services, to be a great nation, or even to survive!

Of course, protecting industries critical to national security might seems like a natural concession to make, even for those supportive of liberalized trade. Ross Douthat says this:

“I think trying to reshore some manufacturing and decouple more from China makes sense from a national security standpoint, even if it costs something to G.D.P. and the stock market.“

Unfortunately, this kind of rationale is far too malleable. There is never a clearly defined limiting principle. Someone decides which goods are “critical” to national security, and this deliberation becomes the subject of much political jockeying and favor-seeking. But wait! Economic security is also cited as an adequate excuse for trade protections! And how about data security? Health security? Job security? Always there is insistence that “security” of one sort or another demands that we provide for our own needs. For definitive proof, take a look at this nonsense! Give them an inch and they’ll take a mile.

Pretty soon you “protect” such a wide swath of industries in a quest for self-sufficiency that the entire economy is unmoored from opportunity costs, comparative advantages, and the information about scarcities provided by market prices. Absolute “security” comes at the cost of transforming the economy’s productive machinery into a complacent hulk rivaling the inefficiency of Soviet industrial planning. Competition is the solution, but not limited to firms under the same set of protective trade barriers.

Manufacturing Is Mostly Fine

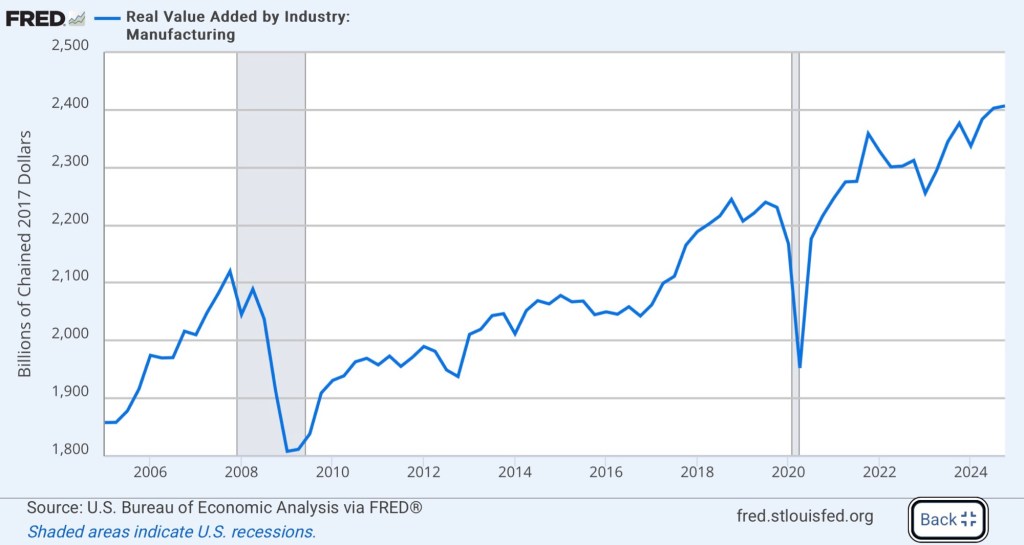

Trade warriors, including members of Trump’s team, insist that our decline as a nation is being hastened by a crisis in manufacturing. However, value added in U.S. manufacturing is at an all-time high.

There has been a long-term decline in manufacturing employment, but not manufacturing output. In fact, manufacturing output has doubled since 1980. As Jeff Jacoby notes, “the purpose of manufacturing is to make things, not jobs.” If our overarching social goal was job security, we’d have revolted long ago against the tremendous reduction in agricultural employment experienced over the past century. We’d rely on switchboard operators to load web pages, and we’d dig trenches and tunnels with spoons (to paraphrase Milton Friedman).

The secular decline in manufacturing employment is a consequence of growth in manufacturing productivity. Economy-wide, this phenomenon allows real income and our standard of living to grow.

Take That Job and …

It’s also significant that few Americans have much interest in factory work. It’s typically less dangerous than in times past, but many of today’s factory jobs are still physically challenging and relatively risky. Perhaps that helps explain why nearly half-a-million jobs in manufacturing are unfilled.

Jacoby describes the transition that has changed the face of American manufacturing:

“… US plants have largely turned away from making many of the low-tech, labor-intensive consumer items they once specialized in — sneakers, T-shirts, small appliances, toys. Those jobs have mostly gone overseas, and trying to bring them back by means of a trade war would be ruinous. Yet America remains a global manufacturing powerhouse — highly skilled, highly innovative, and highly efficient.“

And yet, even as wages in manufacturing have grown, many factory jobs do not pay as well as positions requiring far less strenuous toil in the services sector. It’s also true that the best manufacturing jobs in the U.S. today require high-level skills, which are in short supply. These factors help explain why manufacturers believe finding qualified workers is one of their biggest challenges.

Isolating Weak Sectors

There are specific sectors within manufacturing that have fared poorly, including textiles, furniture, metals, and low-end electronics. The loss of competitiveness that drove those sectoral declines is not a new development. It has, however, devastated communities in the U.S. that were heavily dependent on these industries. These misfortunes are regrettable, but trade barriers are not an effective prescription for revitalizing depressed areas.

Meanwhile, other manufacturing sectors have enjoyed growth, such as computers, aerospace, and EVs. While we’ve seen a decline in the number of manufacturing firms, theperformance of U.S. manufacturing in the 21st century can be described as mixed at the very worst.

The author of this piece seems to accept the false notion that U.S. manufacturing is moribund, but he knows tariffs aren’t an effective way to strengthen domestic goods production. He has a number of better suggestions, including a commitment to infrastructure investment, reforms to education and health, and reconfiguring certain corporate income tax policies. Unfortunately, his ideas on tariffs are sometimes as mistaken as Trump’s,

The Gilded Age

Finally, the other false assertion noted in the opening paragraph is that tariffs somehow spurred economic growth in the late 19th and early 20th centuries. Brian Albrecht corrects this protectionist fallacy, which lies at the root of many defenses of Trump’s tariffs. Albrecht cites favorable conditions for growth that were sufficient to overwhelm the negative effects of tariffs, including:

“… explosive population growth, mass European immigration, rapid technological innovation, westward expansion, abundant natural resources, high literacy rates, and stable property rights.”

While cross-country comparisons indicate a positive correlation between tariffs and growth during the 1870 – 1920 period, those differences were caused by other forces that dominated tariffs. Cross-industry research discussed by Albrecht indicates that tariffs on manufactured goods during the gilded era reduced labor productivity and stimulated the entry of smaller, less productive firms. Likewise, natural experiments find that tariffs allowed inefficient firms to survive and discouraged innovation.

Conclusion

The U.S. manufacturing sector is not in any sort of crisis, and its future growth won’t be powered by attempts to restore the sort of low-value production offshored over the past several decades. What protectionists interpret as failure is the natural progression of a technically advanced market-based civilization, where high-value services account for greater shares of growing total output. Of course, low-value production is sometimes “crowded out” in this process, depending on its trade-ability and comparative advantages. The logic of the process is encapsulated by Veronique de Rugy’s recent discussion of iPhone production (HT: Don Boudreaux):

“Then there’s [Commerce Secretary Howard] Lutnick, pining for a world where Americans flood back into massive factories to assemble iPhones. This is nostalgic industrial cosplay masquerading as economic strategy. Yes, iPhones aren’t assembled by Americans. But this isn’t a failure; it’s a feature of smart economic specialization. We design the iPhone here. That’s the high-value, high-margin part. The sophisticated chips, software, architecture, and intellectual property are all created in the U.S. The marketing is done here, too. That’s most of the value of the iPhone. The lower-value labor-intensive assembly work is done abroad because those tasks are more efficiently performed abroad.“

There is certainly no crisis in U.S. manufacturing. That narrative is driven by a combination of politics, rent seeking, and misplaced nostalgia.

Matt Yglesias tweeted on X that “the bond market does not appear to believe in DOGE”. He included a chart much like the updated one above to “prove” his point. Tyler Cowen posted a link to the tweet on Marginal Revolution, without comment … Cowen surely must know that any such conclusion is premature, especially based on the movement of Treasury yields over the past month (or more, since the market’s evaluation of the DOGE agenda preceded Trump’s inauguration).

Of course, there is a difference between “believing” in DOGE and being convinced that its efforts should have succeeded in reducing interest rates immediately amidst waves of background noise from budget and tax legislation, court challenges, Federal Reserve missteps (this time cutting rates too soon), and the direction of the economy in general.

In this case, perhaps a better way to define success for DOGE is a meaningfully negative impact on the future supply of Treasury debt. Even that would not guarantee a decline in Treasury rates, so the premise of Yglesias’ tweet is somewhat shaky to begin with. Still, all else equal, we’d expect to see some downward pressure on yields if DOGE succeeds in this sense. But we must go further by recognizing that DOGE savings could well be reallocated to other spending initiatives. Then, the savings would not translate into lower supplies of Treasury debt after all.

Certainly, the DOGE team has made progress in identifying wasteful expenditures, inefficiencies, and poor controls on spending. But even if the $55 billion of estimated savings to date is reliable, DOGE has a long way to go to reach Musk’s stated objective of $2 trillion. There are some juicy targets, but it will be tough to get there in 17 more months, when DOGE is to stand down. Still, it’s not unreasonable to think DOGE might succeed in accomplishing meaningful deficit reduction.

But if bond traders have doubts about DOGE, it’s partly because Donald Trump and Elon Musk themselves keep giving them reasons. In my view, Musk and Trump have made a major misstep in toying with the idea of using prospective DOGE savings to fund “dividend checks” of $5,000 for all Americans. These would be paid by taking 20% of the guesstimated $2 trillion of DOGE savings. Musk’s expression of interest in the idea was followed by a bit of clusterfuckery, as Musk walked back his proposal the next day even as Trump jumped on board. PLEASE Elon, don’t give the Donald any crowd-pleasing ideas! And don’t lose sight of the underlying objective to reduce the burden of government and the public debt.

Now, Trump proposes that 60% of the savings accomplished by DOGE be put toward paying for outlays in future years. Sure, that’s deficit reduction, but it may serve to dull the sense that shrinking the federal government is an imperative. The mechanics of this are unclear, but as a first pass, I’d say the gain from investing DOGE savings for a year in low-risk instruments is unlikely to outweigh the foregone savings in interest costs from paying off debt today! Of course, that also depends on the future direction of interest rates, but it’s not a good bet to make with public funds.

Nor can the bond market be comforted by uncertainty surrounding legislation that would not only extend the Trump tax cuts, but will probably include various spending provisions, both cuts and increases. As of now, the mix of provisions that might accompany a deal among GOP factions is very much up in the air.

There is also trepidation about Trump’s aggressive stance toward the Federal Reserve. He promises to replace Jerome Powell as Fed Chairman, but with God knows whom? And Trump jawbones aggressively for lower rates. The Fed’s ill-advised rate cuts in the fall might have been motivated in part by an attempt to capitulate to the then-President Elect.

Trump’s Executive Order to create a sovereign wealth fund (SWF), which I recently discussed here, is probably not the most welcome news to bond investors. All else equal, placing tax or tariff revenue into such a fund would reduce the potential for deficit reduction, to say nothing of the idiocy of additional borrowing to purchase assets.

Finally, Trump has proposed what might later prove to be massive foreign policy trial balloons. Some of these are bound up with the creation of the SWF. They might generate revenue for the government without borrowing (mineral rights in Ukraine? Or Greenland?), but at this point there’s also a chance they’ll create massive funding needs (Gaza development?). Again, Trump seems to be prodding or testing counterparties to various negotiations… prodding diplomacy. It’s unlikely that anything too drastic will come of it from a fiscal perspective, but it probably doesn’t leave bond traders feeling easy.

At this stage, it’s pretty rash to conclude that the bond market “doesn’t believe in DOGE”. In fact, there is no doubt that DOGE is making some progress in identifying potential fraud and inefficiencies. However, bond traders must weigh a wide range of considerations, and Donald Trump has a tendency to kick up dust. Indeed, the so-called DOGE dividend will undermine confidence in debt reduction and bond prices.

Kamala Harris’ campaign platform lifts several tax provisions from Joe Biden’s ill-fated campaign. The most pernicious of these are lauded by observers on the Left for their “fairness”, but they dismiss some rather obvious economic damage these provisions would inflict. Here, I’ll cover Harris’ proposal to tax unrealized capital gains of the rich in two different ways:

A minimum 25% “billionaire tax” on the “incomes” of taxpayers with net worth exceeding $100 million. This definition of income would include unrealized capital gains.

A tax of 28% at the time of death on unrealized capital gains in excess of $5 million ($10 million for joint returns).

Why Bother?

To get a whiff of the complexity involved, take a look at the description on pp. 79 – 85 of this document, to which the Harris proposal seems to correspond. It’s not fully fleshed out, but it’s easy to imagine the lucrative opportunities this would create for tax attorneys and accountants, to say nothing of job openings at the IRS!

On the other hand, there’s little chance these proposals would be approved by Congress, no matter which party holds a majority. Harris knows that, or at least her advisors do. That taxation of unrealized gains is even part of the conversation in a presidential election year tells us how normalized the idea has become within the Democrat Party, which seems to have lost all regard for private property rights. These are classist proposals designed to garner the votes of the “tax-the-rich” crowd, who either aren’t aware or haven’t come to grips with the fact that the U.S. already has a very progressive income tax system. “The rich” already pay a disproportionately high share of taxes.

Taxable Income

These provisions would complicate and corrupt the income tax code by distorting the definition of income for tax purposes. The Internal Revenue Code has always been consistent in defining taxable income as realized income. One might use the expression “mark-to-market taxation” to characterize a tax on unrealized gains from tradable assets. It’s much more difficult to estimate unrealized gains on non-tradable or infrequently traded investments, for which there is no ready market value.

There is one type of income that some believe to be taxed as unrealized. A few weeks ago, in a post about Sam Altman’s infatuation with a wealth tax, I cited a recent Supreme Court decision that has been mistakenly interpreted as favoring income taxation of unrealized gains or a wealth tax. In fact, Moore v. United States involved the undistributed profits of a foreign pass-through entity (i.e., not a C corporation) for purposes of the mandatory repatriation tax. The foreign firm’s profits were realized, and its pass-through status meant that the U.S. owners had also, by definition, realized the profits. So this case did not set a precedent or create an exception to the rule that income taxation applies only to realized income.

Forced Sales

Tradable assets with easily recorded market values will often have unrealized gains in a given year. While tax payments might be spread over the current and future tax years, these taxes could necessitate asset sales to pay the taxes owed. If unrealized losses are treated symmetrically, they would require either future deductions or possibly credits for prior tax payments.

Estimates of unrealized gains on illiquid or private investments like closely-held business interests, artwork, or real estate are highly uncertain and subject to dispute. A large tax liability on such an asset could be especially burdensome. Cash must be raised, which might require a forced sale of other assets. And again, these valuations often come with great complexity and exorbitant administrative costs, not just for the IRS, but especially for taxpayers.

Economic Downsides

As I noted above, additional taxes on unrealized gains would create an obvious need for liquidity, if not immediately then at death. With or without careful planning, sales of assets by wealthy investors to pay the tax would undermine market values of equity (and other assets), producing a broader loss of wealth economy-wide.

Avoidance schemes would be heavily utilized. For example, a wealthy investor could borrow heavily against assets so as to offset unrealized gains with deductible debt-service costs.

Capital flight is likely to be intense if a Harris tax regime began to take shape in Congress. This might be the best avoidance scheme of all. The U.S. is likely to experience massive capital outflows. Furthermore, investment in new physical capital will decline, ultimately leading to lower productivity and real wages.

Entrepreneurial activity would also take a hit. In a critique of Jason Furman’s effort to justify Harris’ proposal, Tyler Cowen asks why we should be so eager to “whack” venture capital. He also quotes an email from Alex Tabarrok on the detrimental policy effects on rapidly growing start-ups:

“What’s really going on is that you are divorcing the entrepreneur from their capital at precisely the moment that the team is likely most productive. Separation of capital from entrepreneur could negatively impact the company’s growth or the entrepreneur’s ability to manage effectively. The entrepreneur could lose control, for example. If you wait until the entrepreneur realizes the gain that’s the time that the entrepreneur wants out and is ready to consume so it’s closer to taxing consumption and better timed in the entrepreneurial growth process.“

Or the entrepreneur might just decide that a startup would be more rewarding in a tax-friendly environment, perhaps somewhere overseas.

Interest Rates and Tax Receipts

Tabarrok notes in a separate post that much of the variation in stock prices is caused by changes in interest rates. Investors use market rates to determine discount rates at which a firm’s future cash flows can be valued. Thus, changes in rates engender changes in stock prices, capital gains, and capital losses.

A decline in interest rates can raise market valuations without any change in dividends. However, a long-term investor would see no change in pre-tax income or consumption, so the tax could force a series of premature sales. A change in a firm’s expected growth rate would also create an unrealized gain (or loss), but the tax would undermine U.S. equity values. Taxing an actual increase in the dividend is one thing, but taxing a change in expectations of future dividends is another. As Tabarrok puts it, “It’s taxing the chickens before the eggs have hatched.“

Dangerous Narrative, Dangerous Policy

A final objection to taxing unrealized capital gains is that it would cross the line into a form of wealth taxation. Assets come in many forms, but the only time realized values can be discerned are when they are traded. That goes for collectibles, homes, boats, and the full array of financial assets. A corollary is that a very large percentage of wealth is unrealized.

A tax on unrealized gains would be the proverbial camel’s nose under the tent and another incursion into the private realm. So often in the history of taxation we’ve seen narrow taxes expand into broad taxes. This is one more opportunity for the state to extend its dominance and control.

I’ve written in the past about the economic dangers of a wealth tax. First, every dollar of income used to purchase capital is already taxed once. In that sense, the cost basis of wealth would be double taxed under a wealth tax. Second, the supply of capital is highly elastic. This implies a high propensity for capital flight, shallowing of productive physical capital, and reduced productivity and real wages. Avoidance schemes would rapidly be put into play. Given these limitations, the revenue raising potential of a wealth tax is unlikely to live up to expectations. Finally, a wealth tax is unconstitutional, but that won’t stop the Left from pushing for one, especially if they first get a tax on unrealized gains. Even if they are unsuccessful now, the conversation tends to normalize the idea of a wealth tax among low-information voters, and that is a shame.

As of February 2026, I’m adding this short preamble to a few older posts on the subject of AI and future prospects for human labor. In the original post below (and a few others), I overstated the case that the law of comparative advantage would assure a continued role for humans in production. I still think the case is strong, mind you, but now I’m convinced that the outcome depends on elasticities of input substitution and how those elasticities might shift given the advent of AI-augmented capital. You can read my most recent thoughts on the matter here.

____________________________________________

I was happy to see Noah Smith’s recent post on the graces of comparative advantage and the way it should mediate the long-run impact of AI on job prospects for humans. However, I’m embarrassed to have missed his post when it was published in March (and I also missed a New York Timespiece about Smith’s position).

I said much the same thing as Smith in my post two weeks ago about the persistence of a human comparative advantage, but I wondered why the argument hadn’t been made prominently by economists.I discussed it myself about seven years ago. But alas, I didn’t see Smith’s post until last week!

I highly recommend it, though I quibble on one or two issues. Primarily, I think Smith qualifies his position based on a faulty historical comparison. Later, he doubles back to offer a kind of guarantee after all. Relatedly, I think Smith mischaracterizes the impact of energy costs on comparative advantages, and more generally the impact of the resources necessary to support a human population.

We Specialize Because…

Smith encapsulates the underlying phenomenon that will provide jobs for humans in a world of high automation and generative AI: “… everyone — every single person, every single AI, everyone — always has a comparative advantage at something!” He tells technologists “… it’s very possible that regular humans will have plentiful, high-paying jobs in the age of AI dominance — often doing much the same kind of work that they’re doing right now …”

… often, but probably transformed in fundamental ways by AI, and also doing many other new kinds of work that can’t be foreseen at present. Tyler Cowen believes themost important macro effects of AI will be from “new” outputs, not improvements in existing outputs. That emphasis doesn’t necessarily conflict with Smith’s narrative, but again, Smith thinks people will do many of the same jobs as today in a world with advanced AI.

Smith’s Non-Guarantee

Smith hedges, however, in a section of his post entitled “‘Possible’ doesn’t mean guaranteed”. This despite his later assertion that superabundance would not eliminate jobs for humans. That might seem like a separate issue, but it’s strongly intertwined with the declining AI cost argument at the basis of his hedge. More on that below.

On his reluctance to “guarantee” that humans will have jobs in an AI world, Smith links to a 2013 Tyler Cowen post on“Why the theory of comparative advantage is overrated”. For example, Cowen says, why do we ever observe long-term unemployment if comparative advantage rules the day? Of course there are many reasons why we observe departures from the predicted results of comparative advantage. Incentives are often manipulated by governments and people differ drastically in their capacities and motivation.

But Cowen cites a theoretical weakness of comparative advantage: that inputs are substitutable (or complementary) by degrees, and the degree might change under different market conditions. An implication is that “comparative advantages are endogenous to trade”, specialization, and prices. Fair enough, but one could say the same thing about any supply curve. And if equilibria exist in input markets it means these endogenous forces tend toward comparative advantages and specializations balancing the costs and benefits of production and trade. These processes might be constrained by various frictions and interventions, and their dynamics might be complex and lengthy, but that doesn’t invalidate their role in establishing specializations and trade.

The Glue Factory

Smith concerns himself mainly with another one of Cowen’s “failings of comparative advantage”: “They do indeed send horses to the glue factory, so to speak.” The gist here is that when a new technology, motorized transportation, displaced draft horses, there was no “wage” low enough to save the jobs performed by horses. Smith says horses were too costly to support (feed, stables, etc…), so their comparative advantage at “pulling things” was essentially worthless.

True, but comparing outmoded draft horses to humans in a world of AI is not quite appropriate. First, feedstock to a “glue factory” better not be an alternative use for humans whose comparative advantages become worthless. We’ll have to leave that question as an imperative for the alignment community.

Second, horses do not have versatile skill sets, so the comparison here is inapt due to their lack of alternative uses as capital assets. Yes, horses can offer other services (racing, riding, nostalgic carriage rides), but sadly, the vast bulk of work horses were “one-trick ponies”. Most draft horses probably had an opportunity cost of less than zero, given the aforementioned costs of supporting them. And it should be obvious that a single-use input has a comparative advantage only in its single use, and only when that use happens to be the state-of-the-art, or at least opportunity-cost competitive.

The drivers, on the other hand, had alternatives, and saw their comparative advantage in horse-driving occupations plunge with the advent of motorized transport. With time it’s certain many of them found new jobs, perhaps some went on to drive motorized vehicles. The point is that humans have alternatives, the number depending only on their ability to learn a crafts and perhaps move to a new location. Thus, as Smith says, “… everyone — every single person, every single AI, everyone — always has a comparative advantage at something!” But not draft horses in a motorized world, and not square pegs in a world of round holes.

AI Producer Constraints

That brings us to the topic of what Smith calls producer-specific constraints, which place limits on the amount and scope of an input’s productivity. For example, in my last post, there was only one super-talented Harvey Specter, so he’s unlikely to replace you and keep doing his own job. Thus, time is a major constraint. For Harvey or anyone else, the time constraint affects the slope of the tradeoff (and opportunity costs) between one type of specialization versus another.

Draft horses operated under the constraints of land, stable, and feed requirements, which can all be viewed as long-run variable costs. The alternative use for horses at the glue factory did not have those costs.

Humans reliant on wages must feed and house themselves, so those costs also represent constraints, but they probably don’t change the shape of the tradeoff between one occupation and another. That is, they probably do not alter human comparative advantages. Granted, some occupations come with strong expectations among associates or clients regarding an individual’s lifestyle, but this usually represents much more than basic life support. In the other end of the spectrum, displaced workers will take actions along various margins: minimize living costs; rely on savings; avail themselves of charity or any social safety net as might exist; and ultimately they must find new positions at which they maintain comparative advantages.

The Compute Constraint

In the case of AI agents, the key constraint cited by Smith is “compute”, or computer resources like CPUs or GPUs. Advancements in compute have driven the AI revolution, allowing AI models to train on increasingly large data sets and levels of compute. In fact, by one measure of compute, floating point operations per second (FLOPs), compute has become drastically cheaper, with FLOPs per dollar almost doubling every two years. Perhaps I misunderstand him, but Smith seems to assert the opposite: that compute costs are increasing. Regardless, compute is scarce, and will always be scarce because advancements in AI will require vast increases in training. This author explains that while lower compute costs will be more than offset by exponential increases in training requirements, there nevertheless will be an increasing trend in capabilities per compute.

Every AI agent will require compute, and while advancements are enabling explosive growth in AI capabilities, scarce compute places constraints on the kinds of AI development and deployment that some see as a threat to human jobs. In other words, compute scarcity can change the shape of the tradeoffs between various AI applications and thus, comparative advantages.

The Energy Constraint

Another producer constraint on AI is energy. Certainly highly complex applications, perhaps requiring greater training, physical dexterity, manipulation of materials, and judgement, will require a greater compute and energy tradeoff against simpler applications. Smith, however, at one point dismisses energy as a differential producer constraint because “… humans also take energy to run.” That is a reference to absolute energy requirements across inputs (AI vs. human), not differential requirements for an input across different outputs. Only the latter impinge on tradeoffs or opportunity costs facing an inputs. Then, the input having the lowest opportunity cost for a particular output has a comparative advantage for that output. However, it’s not always clear whether an energy tradeoff across outputs for humans will be more or less skewed than for AI, so this might or might not influence a human comparative advantage.

Later, however, Smith speculates that AI might bid up the cost of energy so high that “humans would indeed be immiserated en masse.” That position seems inconsistent. In fact, if AI energy demands are so intensive, it’s more likely to dampen the growth in demand for AI agents as well as increase the human comparative advantage because the most energy-intensive AI applications will be disadvantaged.

And again, there is Smith’s caution regarding the energy required for human life support. Is that a valid long-run variable cost associated with comparative advantages possessed by humans? It’s not wrong to include fertility decisions in the long-run aggregate human labor supply function in some fashion, but it doesn’t imply that energy requirements will eliminate comparative advantages. Those will still exist.

Hype, Or Hyper-Growth?

AI has come a long way over the past two years, and while its prospective impact strikes some as hyped thus far, it has the potential to bring vast gains across a number of fields within just a few years. According to this study, explosive economic growth on the order of 30% annually is a real possibility within decades, as generative AI is embedded throughout the economy. “Unprecedented” is an understatement for that kind of expansive growth. Dylan Matthews in Vox surveys the arguments as to how AI will lead to super-exponential economic growth. This is the kind of scenario that would give rise to superabundance.

I noted above that Smith, despite his unwillingness to guarantee that human jobs will exist in a world of generative AI, asserts (in an update) at the bottom of his post that a superabundance of AI (and abundance generally) would not threaten human comparative advantages. This superabundance is a case of decreasing costs of compute and AI deployment. Here Smith says:

“The reason is that the more abundant AI gets, the more value society produces. The more value society produces, the more demand for AI goes up. The more demand goes up, the greater the opportunity cost of using AI for anything other than its most productive use.

“As long as you have to make a choice of where to allocate the AI, it doesn’t matter how much AI there is. A world where AI can do anything, and where there’s massively huge amounts of AI in the world, is a world that’s rich and prosperous to a degree that we can barely imagine. And all that fabulous prosperity has to get spent on something. That spending will drive up the price of AI’s most productive uses. That increased price, in turn, makes it uneconomical to use AI for its least productive uses, even if it’s far better than humans at its least productive uses.

“Simply put, AI’s opportunity cost does not go to zero when AI’s resource costs get astronomically cheap. AI’s opportunity cost continues to scale up and up and up, without limit, as AI produces more and more value.”

This seems as if Smith is backing off his earlier hedge. Some of that spending will be in the form of fabulous investment projects of the kinds I mentioned in my post, and smaller ones as well, all enabled by AI. But the key point is that comparative advantages will not go away, and that means human inputs will continue to be economically useful.

I referenced Andrew Mayne in my last post. He contends that the income growth made possible by AI will ensure that plenty of jobs are available for humans. He mentions comparative advantage in passing, but he centers his argument around applications in which human workers and AI will be strong complements in production, as will sometimes be the case.

A New Age of Worry

The economic success of AI is subject to a number of contingencies. Most important is that AI alignment issues are adequately addressed. That is, the “self-interest” of any agentic AI must align with the interests of human welfare. Do no harm!

The difficulty of universal alignment is illustrated by the inevitability of competition among national governments for AI supremacy, especially in the area of AI-enabled weaponry and espionage. The national security implications are staggering.

A couple of Smith‘s biggest concerns are the social costs of adjusting to the economic disruptions AI is sure to bring, as well as its implications for inequality. Humans will still have comparative advantages, but there will be massive changes in the labor market and transitions that are likely to involve spells of unemployment and interruptions to incomes for some. The speed and strength of the AI revolution may well create social upheaval. That will create incentives for politicians to restrain the development and adoption of AI, and indeed, we already see the stirrings of that today.

Finally, Smith worries that the transition to AI will bring massive gains in wealth to the owners of AI assets, while workers with few skills are likely to languish. I’m not sure that’s consistent with his optimism regarding income growth under AI, and inequality matters much less when incomes are rising generally. Still, the concern is worthy of a more detailed discussion, which I’ll defer to a later post.

I’ve taken an extended hiatus from blogging while moving to a different part of the country. I haven’t posted here in over 10 weeks, but a new post appears below. I’m still tying-up loose ends from the move, but I’ll be trying to get back to posting more regularly … trying!

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Absurd ideas about race and identity politics come from extreme elements on both the Left and the Right. Some leftists insist that race has no natural basis — that it’s simply a “social construct”. On the Right, a “racialist” contingent is promoting the “celebration of whiteness” and embracing racial preferences for whites. Treated as alternative pathways, I’d take “social construct”. It’s nonsense, of course, but the beautiful irony is that it provides a basis for stripping away from our institutions the entire diversity, equity, and inclusion (DEI) straightjacket. It’s almost as if those promoting race as a social construct wish to build a “colorblind” society. On the other hand, I suppose some think they can have their DEI cake along with a side of free choice to identify as anything they want: black, white, or furry.

Who Are the Racists?

People of good faith don’t harbor or act on racist tendencies. The mere recognition of racial/ethnic/cultural differences is not evidence of racism and does not preclude the treatment of all with fairness and due respect. It’s possible to respect, value, or fall in love with someone outside one’s own racial, ethnic, or cultural group of origin, even while holding a general affinity for one’s own group, as nearly everyone does.

But a few real racists are sprinkled across all races, ethnicities, cultures, and the full political spectrum. The “popular” racist stereotype as white male has been kept alive by the lingering echos of slavery in America, which ended nearly 16 decades ago, and the long hangover that included Jim Crow laws and segregation. Today, however, “white society” or “whiteness” is hardly the sole domain of prejudice.

IsRacialism Different?

Now, a few whites are promoting the celebration of “white identity” as a counterbalance to identity politics among non-whites. Ostensibly, this “white racialism” might be similar to celebrations of identity often practiced by minorities, which are also forms of racialism. Should white racialism be viewed as less savory than racialism practiced by racial minorities?

For most Caucasians, “being white” does not have much salience relative to other affiliations defining identity. That’s why white racialism seems odd to me. Sure, when forced to check a box, whites will check “Caucasian”, but “white identity” seems overly broad. There are too many distinct cultures and subcultures that dominate self-identity, such as national ancestry, religion, and cultural membership.

The same could be said for many other racial categories, but minority status and historical events (e.g., American slavery) help explain why broad categories often form cohesive identity groups. And, as Christopher Rufo notes in his great discussion of the racialist viewpoint, broad categories tend to be the most closely associated with racialism:

“Yes, left-wing racialism is indeed now deeply embedded in America’s institutions, and the demographic balance of the country has shifted in recent decades. And yes, the basic racial classification system in the United States broadly delineates continental origin—Europe, Africa, Latin America, Asia—in a way that is not arbitrary or meaningless. Terms such as ‘white,’ ‘black,’ ‘Latino,’ and ‘Asian,’ while often obscuring important variations within such groupings, have become the lingua franca and are useful shorthand descriptors for many purposes.”

There are individuals from all groups or “classes”, including whites, who react critically to aggressive expressions of identity by members of other classes. Perhaps that’s excusable, depending on the degree of zealotry on either part. The line between pride in race/ancestry/culture and fractious racialism might be hard to discern in some cases, but the chief distinction is rooted in explicit, demeaning and/or envious comparisons to “out-groups”. This might be damaging enough, but from there it can be a very short step into outright racism.

A preoccupation with the historic disadvantages of one’s race can be disempowering to an individual and destructive in a social sense. I believe the white racialist phenomenon belongs in that category. The presumed “disadvantages” of whiteness are very contemporary, however, rooted in policies dating back only to the widespread adoption of racial preferences for non-white “protected classes” and DEI.

Preferences For All

Imagine the racialist policies now practiced widely in government, industry, and academia — particularly racial preferences on behalf of protected classes — but now applied on behalf of heretofore unprotected classes as well. For example, what if some proportion of jobs, admissions, or other coveted placements were set aside for whites? If whites represent 50% of the population, then 50% of hires or admissions would be reserved for whites.

Some might assume that this treatment is already implied by existing racial preferences, but that’s not the case. In the wake of George Floyd’s death, just 6% of new hires among S&P companies were white, according to Bloomberg News.

Nevertheless, such a white racialist turnabout would be a colossal mistake. Adding strict limits to the application of existing preferences might be a good thing, but white racial preferences would buttress the entire system of racial preferences as an institution and add more rigidity to the operation of labor markets. From an economic viewpoint, it would be just as pernicious as racial preferences generally.

Racial preferences of any kind freeze labor markets and impair the allocation of human resources to their most-valued uses. In fact, placing one individual into a position on any basis other than their qualifications implies that two individuals must be placed into positions in which they lack comparative advantage relative to each other. Little by little, that means lost output and upward price pressure. It is a mechanism that short circuits gains from trade, shriveling the benefits that the most and least talented confer on society at large. Extending preferences to whites would only serve to further institutionalize this damaging practice.

Adherence to numerical preferences is to pretend that people can be treated less as individuals and more like interchangeable parts… except with respect to their value as “class members”. Racial preferences are presumed to be a remedy for so-called structural racism, as opposed to racism by individuals. But they involve classification and favor the so-called “oppressed” at the expense of designated “oppressors”. The latter, almost without exception, had no role oppressive regimes of the past. Favoritism of this kind necessarily means reverse discrimination and fails to match individuals to roles in an optimal fashion.

Whether publicly or privately imposed, racial preferences often undermine those they are purported to help by placing individuals into positions for which they may not be competitive. This can sabotage an individual’s long-term success. It goes without saying that preferences build resentment among the “unprotected”, which goes to the impetus for “white racialism”. Indeed, preferences are not always popular with protected classes either. That’s because they interfere with merit-based decision-making and are perceived to stigmatize those presumed to benefit.

The Fixed Pie Is a Lie

Racialism reflects zero-sum thinking, a hallmark of DEI initiatives. Tyler Cowen quoted the abstract of a recent NBER working paper that found:

“… a more zero-sum mindset is strongly associated with more support for government redistribution, race- and gender-based affirmative action, and more restrictive immigration policies.”

Zero-sum thinking is fundamental to rent-seeking behavior, which is motivated by either malevolent greed or perceptions of victimhood. Victimhood and rent seeking is at the heart of calls for DEI, to say nothing of more radical proposals like reparation payments. White racialism attempts to get in on the action by positing that whites are oppressed under the current institutional dominance of DEI. But the misguided presumption that every identity group should have their own preferences or quotas broadens the emphasis on redressing perceived harms and redistributing rewards — zero-sum activities.

These zero-sum efforts waste energy and resources, harming our ability to produce things that enhance well being. Ultimately, they are actually negative-sum activities, and they also breed hatred.

Race is obviously determined by genetics, but I’d be happy to pretend it’s a mere social construct if that would help get us to a “colorblind” society.

Conclusion

There’s a huge irony in the racialism exercised by both traditional and “white racialist” DEI advocates: it neglects the most fundamental and just application of diversity: equality of opportunity. This principle incorporates the concept of diversity without sacrificing economic efficiency. We’ve largely abandoned it in favor of equality of outcomes via racial preferences, even at a time when society has become enlightened with respect to racial differences. In doing so, we’ve unintentionally chosen another form of explicit racial victimization.

To close, here’s a good summary of the dangers of racialism and identity politics offered by Victor Davis Hanson:

“Anytime one ethnic, racial, or religious group refuses to surrender its prime identity in exchange for a shared sense of self, other tribes for their own survival will do the same.

All then rebrand their superficial appearance as essential not incidental to whom they are.

And like nuclear proliferation that sees other nations go nuclear once a neighboring power gains the bomb, so too the tribalism of one group inevitably leads only to more tribalism of others. The result is endless Hobbesian strife.”

And that’s how white racialism fits right in with the pernicious politics of identity. When you can, vote for the elimination, or at least reform, of DEI policies and practices, not for a reinforcement of identity politics.

Policy activists have long maintained that manipulating government policy can stabilize the economy. In other words, big spending initiatives, tax cuts, and money growth can lift the economy out of recessions, or budget cuts and monetary contraction can prevent overheating and inflation. However, this activist mirage burned away under the light of experience. It’s not that fiscal and monetary policy are powerless. It’s a matter of practical limitations that often cause these tools to be either impotent or destabilizing to the economy, rather than smoothing fluctuations in the business cycle.

The macroeconomics classes seem like yesterday: Keynesian professors lauded the promise of wise government stabilization efforts: policymakers could, at least in principle, counter economic shocks, particularly on the demand side. That optimistic narrative didn’t end after my grad school days. I endured many client meetings sponsored by macro forecasters touting the fine-tuning of fiscal and monetary policy actions. Some of those economists were working with (and collecting revenue from) government policymakers, who are always eager to validate their pretensions as planners (and saviors). However, seldom if ever do forecasters conduct ex post reviews of their model-spun policy scenarios. In fairness, that might be hard to do because all sorts of things change from initial conditions, but it definitely would not be in their interests to emphasize the record.

In this post I attempt to explain why you should be skeptical of government stabilization efforts. It’s sort of a lengthy post, so I’ve listed section headings below in case readers wish to scroll to points of most interest. Pick and choose, if necessary, though some context might get lost in the process.

Expectations Change the World

Fiscal Extravagance

Multipliers In the Real World

Delays

Crowding Out

Other Peoples’ Money

Tax Policy

Monetary Policy

Boom and Bust

Inflation Targeting

Via Rate Targeting

Policy Coordination

Who Calls the Tune?

Stable Policy, Stable Economy

Expectations Change the World

There were always some realists in the economics community. In May we saw the passing of one such individual: Robert Lucas was a giant intellect within the economics community, and one from whom I had the pleasure of taking a class as a graduate student. He was awarded the Nobel Prize in Economic Science in 1995 for his applications of rational expectations theory and completely transforming macro research. As Tyler Cowen notes, Keynesians were often hostile to Lucas’ ideas. I remember a smug classmate, in class, telling the esteemed Lucas that an important assumption was “fatuous”. Lucas fired back, “You bastard!”, but proceeded to explain the underlying logic. Cowen uses the word “charming” to describe the way Lucas disarmed his critics, but he could react strongly to rude ignorance.

Lucas gained professional fame in the 1970s for identifying a significant vulnerability of activist macro policy. David Henderson explains the famous “Lucas Critique” in the Wall Street Journal:

“… because these models were from periods when people had one set of expectations, the models would be useless for later periods when expectations had changed. While this might sound disheartening for policy makers, there was a silver lining. It meant, as Lucas’s colleague Thomas Sargent pointed out, that if a government could credibly commit to cutting inflation, it could do so without a large increase in unemployment. Why? Because people would quickly adjust their expectations to match the promised lower inflation rate. To be sure, the key is government credibility, often in short supply.”

Non-credibility is a major pitfall of activist macro stabilization policies that renders them unreliable and frequently counterproductive. And there are a number of elements that go toward establishing non-credibility. We’ll distinguish here between fiscal and monetary policy, focusing on the fiscal side in the next several sections.

Fiscal Extravagance

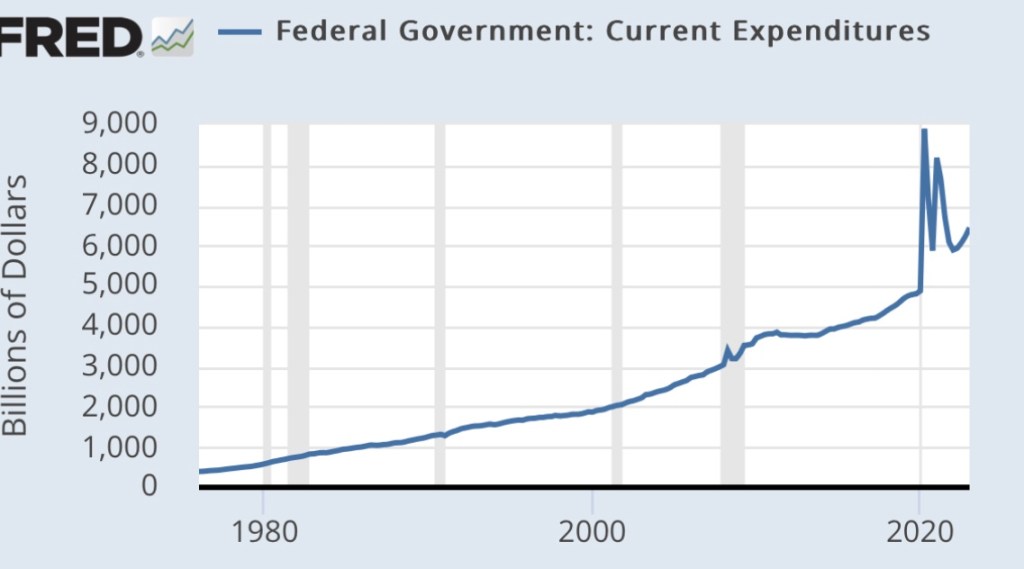

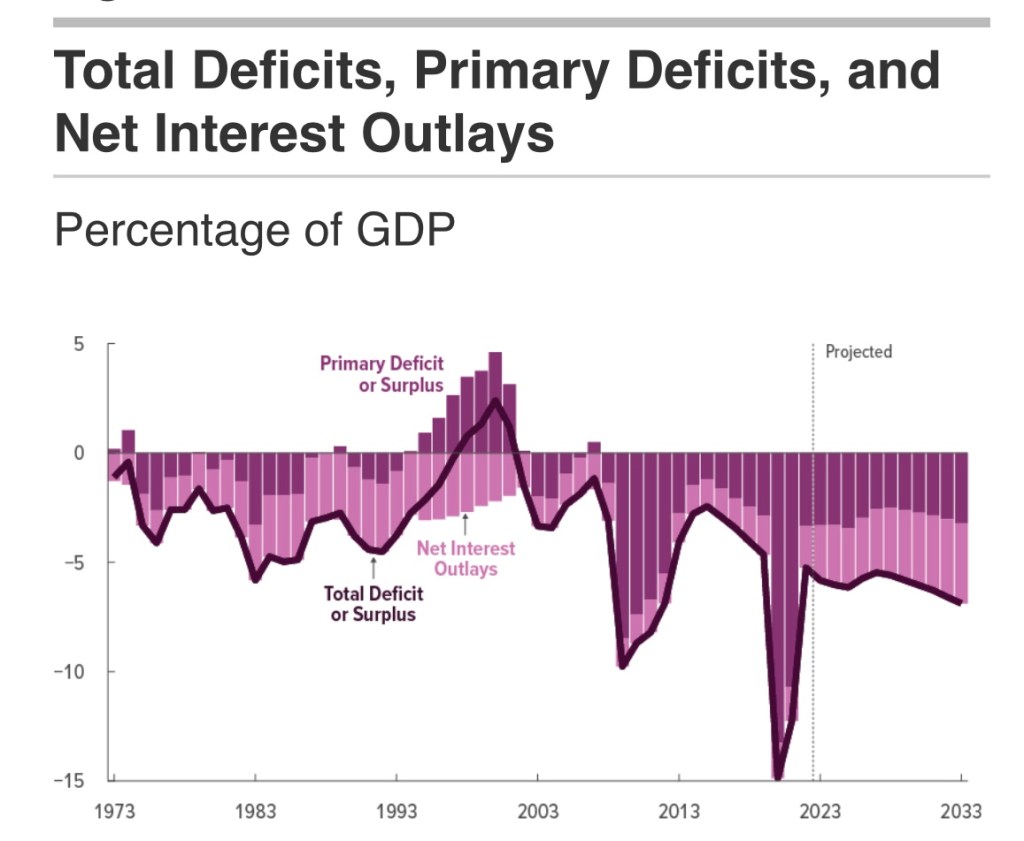

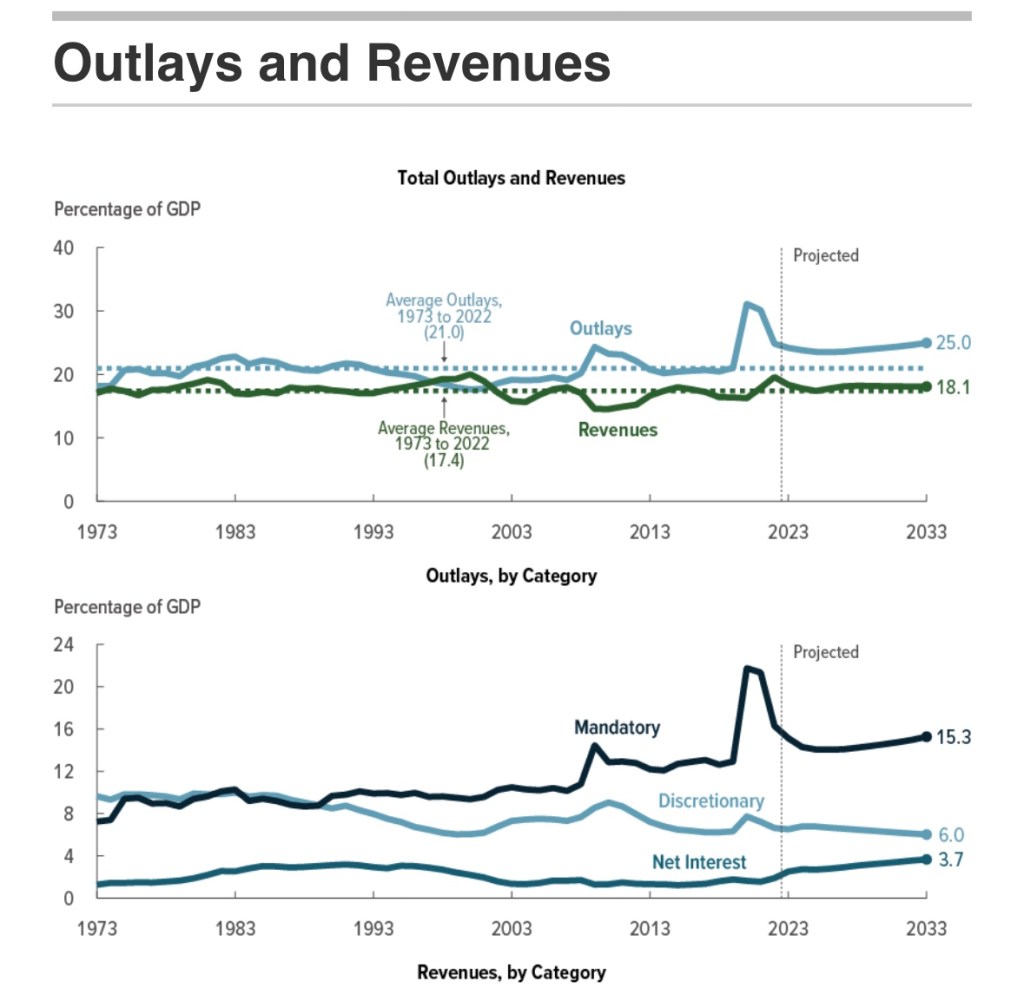

We’ve seen federal spending and budget deficits balloon in recent years. Chronic and growing budget deficits make it difficult to deliver meaningful stimulus, both practically and politically.

The next chart is from the most recent Congressional Budget Office (CBO) report. It shows the growing contribution of interest payments to deficit spending. Ever-larger deficits mean ever-larger amounts of debt on which interest is owed, putting an ever-greater squeeze on government finances going forward. This is particularly onerous when interest rates rise, as they have over the past few years. Both new debt is issued and existing debt is rolled over at higher cost.

Relief payments made a large contribution to the deficits during the pandemic, but more recent legislation (like the deceitfully-named Inflation Reduction Act) piled-on billions of new subsidies for private investments of questionable value, not to mention outright handouts. These expenditures had nothing to do with economic stabilization and no prayer of reducing inflation. Pissing away money and resources only hastens the debt and interest-cost squeeze that is ultimately unsustainable without massive inflation.