I’ll try to keep this one short. I was starting a post on another topic when Donald Trump distracted me… again. This time it was the $2,000 per person “tariff dividend” he’s proposed. This would be paid to all low- and middle-income Americans starting in mid-2026. As if the federal government was a profitable enterprise. Obviously that’s the wrong model! This is either sheer stupidity or willful government failure. Sure, the Fed can just print money, so why not? Who knew Trump was a closet modern monetary theorist?

It’s such a bad idea…. Tariffs themselves are bad enough. They are taxes, of course, a truth about which Trump and his central trade planners have denied since the beginning of the escapade. Tariffs hurt consumers and businesses who import inputs. Tariffs retard growth by increasing input costs, disrupting supply chains, and raising the prices of not only imports, but also domestically-produced goods that compete with imports. Surely Trump knows all this and the implications for his political capital: he’s already backtracking on tariffs for certain food items.

The tariff dividend is a transparent attempt to compensate consumers for the harms of taxation. It’s also a transparent attempt to buy or keep votes, much as he’s already sought to buy-off farmers harmed by tariffs. The income limit for the dividend hasn’t been announced, but make no mistake: this represents another form of redistribution.

It’s also striking that the tariffs won’t generate nearly as much revenue as will be required to begin paying the dividend by mid-2026. In fact, it could be short by as much as $300 million! Will the Treasury borrow the rest? More pressure on the bond market and interest rates.

Furthermore, the so-called dividend would be inflationary if the Federal Reserve fails to neutralize it. It would amount to another “helicopter drop” of cash, similar to the cash dump from Covid relief payments: money printing under the guise of fiscal policy.

To the extent that tariff revenue flows, it should be used to reduce the federal deficit or to pay down the gigantic government debt already outstanding ($38 trillion today not including the impending cost of funding entitlement programs). Instead, Trump is proudly following in the footsteps of generations of spendthrift politicians.

Keep in mind that the dividend is a promise Trump might not be able to keep. The Supreme Court will soon announce its decision on presidential power to impose tariffs. This decision will bear on the president’s authority under the International Emergency Economic Powers Act (IEEPA) — if and when an actual emergency is at hand, which it clearly is not. More broadly, the decision hinges on whether a “foreign facing” tax falls within the president’s Article II powers under the Constitution.

The proposed tariff dividend undermines the Administration’s argument before the Court that tariffs are primarily regulatory tools, and that any revenue from tariffs is merely incidental. Thank God the dividend would have to be authorized by Congress! I truly hope there are enough sensible legislators on the Hill to beat back this idiocy.

Tariffs have far-reaching effects that strike some as counter-intuitive, but they are real forces nevertheless. Much like any selective excise tax, tariffs reduce the quantity demanded of the taxed good; buyers (importers) pay more, but sellers of the good (foreign exporters) extract less revenue. Suppose those sellers happen to be the primary buyers of what you produce. Because they have less to spend, you also will earn less revenue.

The Lerner Effect

The imposition of tariffs by the U.S. means that foreigners have fewer dollars to spend on exports from the U.S. (as well as fewer dollars to invest in the U.S. assets like Treasury bonds, stocks, and physical capital). That much is true without any change in the exchange rate. However, lower imports also imply a stronger dollar, further eroding the ability of foreigners to purchase U.S. exports.

The implications of the import tariff for U.S. exports may be even more starkly negative. Scott Sumner discusses an economic principle called Lerner Symmetry: a tax on imports can be the exact equivalent of a tax on exports! That’s because two-directional trade flows rely on two-directional flows of income.

Note that this has nothing to do with foreign retaliation against U.S. trade policy, although that will also hurt U.S. exporters. Nor is it a consequence of the very real cost increase that tariffs impose on U.S. export manufacturers who require foreign inputs. That’s a separate issue. Lerner Symmetry is simply part of the mechanics of trade flows in response to a one-sided tariff shock.

Assumptions For Lerner Symmetry

Scott Sumner enumerated certain conditions that must be in place for full Lerner Symmetry. While they might seem strict, the Lerner effect is nevertheless powerful under relaxed assumptions (though somewhat weaker than full Lerner Symmetry).

As Sumner puts it, while full Lerner Symmetry requires perfect competition, nearly all markets are “workably competitive”. In the longer-run, assumptions of price flexibility and full employment are anything but outlandish. Complete non-retaliation is an unrealistic assumption, given the breadth and scale of the Trump tariffs. Some countries will retaliate, but not all, and it is certainly not in their best interests to do so. The assumption of balanced trade is one and the same as the assumption of no capital flows; a departure from these “two” assumptions weakens the symmetry between tariffs and export taxes because a reduction in capital flows takes up some of the slack from lower revenue earned by foreign producers.

Trump Tariff Impacts

So here we are, after large hikes in tariffs and perhaps more on the way. Or perhaps more exceptions will be carved out for favored supplicants in return for concessions of one kind or another. All that is economically and ethically foul.

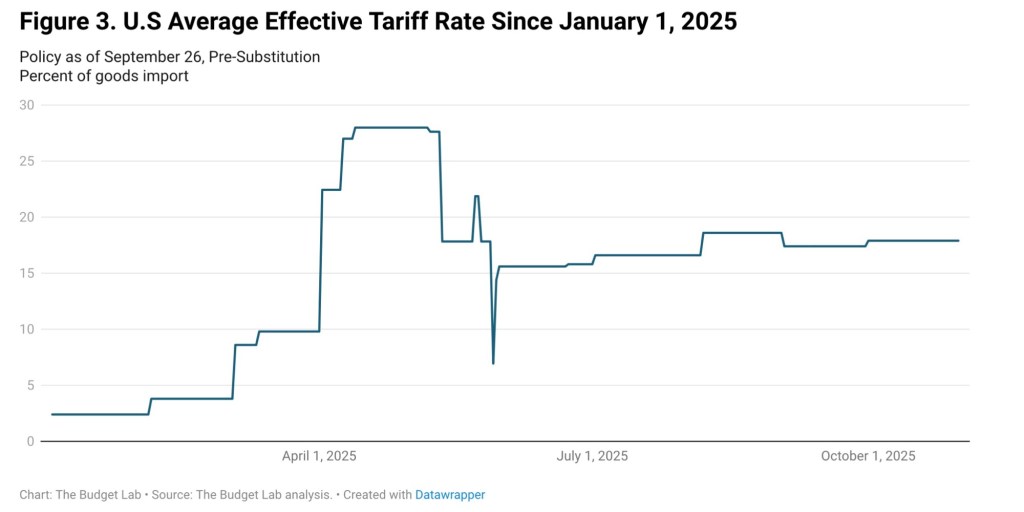

But how are imports and exports faring? Here I’ll quote the Yale Budget Lab’s (YBL) September 26th report on tariffs, which includes the chart shown at the top of this post:

“Consumers face an overall average effective tariff rate of 17.9%, the highest since 1934. After consumption shifts, the average tariff rate will be 16.7%, the highest since 1936. …

The post-substitution price increase settles at 1.4%, a $1,900 loss per household.“

The “post-substitution” modifier refers to the fact that price increases caused by tariffs would be somewhat larger but for consumers’ attempts to find lower-priced domestic substitutes. Suppose the PCE deflator ends 2025 with a 2.8% annual increase. The YBL’s price estimate implies that absent the Trump tariffs, the PCE would have increased 1.4%. If that seems small to you (and the tariff effect seems large to you), recall that monetary policy has been and remains moderately restrictive, so we might have expected some tapering in the PCE without tariffs.

We also know that the early effects of the tariffs have been dominated by thinner margins earned by businesses on imported goods. Those firms have been swallowing a large portion of the tariff burden, but they will increasingly attempt to pass the added costs into prices.

But back to the main topic … what about exports? Unfortunately, the data is subject to lags and revisions, so it’s too early to say much. However, we know exports won’t decline as much as imports, given the lack of complete Lerner symmetry. YBL predicts a drop in exports of 14%, but that includes retaliatory effects. In August the WTO predicted only about a 4% decline, which would be about half the decline in imports.

Seeking Compensatory Rents

More telling perhaps, and it may or may not be a better indicator of the Lerner effect, is the clamoring for relief by American farmers who face diminished export opportunities. As Tyler Cowen says, “Lerner Symmetry Bites”. Other industries will feel the pinch, but many are likely preoccupied with the more immediate problem of increases in the direct cost of imported materials and components.

The farm lobby is certainly on its toes. The Trump Administration is now asking U.S. taxpayers to subsidize soybean producers to the tune of $15 billion. Those exporting farmers are undoubtedly victimized by tariffs. But so much for deficit reduction! More from Cowen:

“Using tariff revenue to subsidize the losses of exporters is a textbook illustration of Lerner Symmetry because the export losses flow directly from the tax on imports! The irony is that President Trump parades the subsidies as a victory while in fact they are simply damage control for a policy he created.“

A List of Harms

Tariffs are as distortionary as any other selective excise tax. They restrict choice and penalize domestic consumers and businesses, whose judgement of cost and quality happen to favor goods from abroad. Tariffs create cost and price pressures in some industries that both erode profit margins and reduce real incomes. For consumers, a tariff is a regressive tax, harming the poor disproportionately.

Tariffs also diminish foreign flows of capital to the U.S., slowing the long-term growth of the economy as well as productivity growth and real wages. And the Lerner effect implies that tariffs harm U.S. exporters by reducing the dollars available to foreigners for purchasing goods from the U.S. In these several ways, Americans are made worse off by tariffs.

We now see attempts to cover for the damage done by tariffs by subsidizing the victims. A “tariff dividend” to consumers? Subsidies to exporters harmed by the Lerner effect? In both cases, we would forego the opportunity to pay down the bloated public debt. Thus, the American taxpayer will be penalized as well.

The world doesn’t ordinarily revolve around tariffs, but so much has happened to make tariffs into an economic and political linchpin of the moment. Donald Trump put them in the spotlight, of course, and while he’s still seeing roses, things won’t turn out entirely the way he hopes. At the tariff levels he’s instituted, this shouldn’t be too surprising.

While tariff revenue is helping to shave the federal budget deficit, the tax falls largely on the backs of American consumers and businesses with all the attending distortions that entails. Sadly, the extra revenue also seems to have offered a handy excuse to put spending cuts on the back burner. Tariffs and tariff uncertainty have businesses attempting to compromise between reduced margins and price hikes. Thinning margins due to tariffs have played a role in the weak employment numbers we’ve seen over the past few months. And tariffs, at least until now, have quite rightly reinforced the Federal Reserve’s cautious stance toward easing policy. However, the weak labor market has likely convinced the Fed to cut its short-term interest rate target, despite inflation stubbornly remaining well above the Fed’s 2% objective. That upward price pressure will remain.

Now, the legal battle over Trump’s tariff authority is about to reach a climax. That’s what I’ll focus on here. The Supreme Court has agreed to fast track the challenge to the President’s discretion to impose retaliatory tariffs unilaterally. There are two cases at hand: V.O.S. Selections, Inc. v. Trump, and Learning Resources, Inc., et al. v. Donald Trump et al. In both cases, small business plaintiffs contend that Trump’s invocation of the International Emergency Economic Powers Act (IEEPA) is unwarranted, and that “most” of the tariff actions taken by Trump have usurped Congress’ power of the purse under Article I of the Constitution. Here’s Ilya Somin, who is a Volokh Conspiracy regular and one of the attorneys representing the plaintiffs:

“… IEEPA doesn’t even mention tariffs and has never previously been used to impose them, that there is no ‘unusual and extraordinary threat’ of the kind required to invoke IEEPA, the major questions doctrine, the constitutional nondelegation doctrine, and more.“

This isn’t the first time a U.S. president has imposed tariffs unilaterally, but it is easily the most drastic such action. Historically, nearly all tariffs were levied by acts of Congress. Prior to Trump II, perhaps the broadest tariff imposed by a President was Richard Nixon’s brief 10% surcharge on all imports, but that was lifted quickly. Presidents Johnson and Obama imposed some selective tariffs. All of these episodes seem piddling compared to Trump’s tariffs, which are both sweeping and in many cases painfully selective.

Eric Boehm notes that when it comes to major constitutional questions, the Court has taken the position that

“… executive power should be construed narrowly, not broadly …. Rather than tying itself into knots to affirm nearly unlimited executive powers over commerce, the Supreme Court should tell the Trump administration to get permission from Congress before imposing new tariffs.“

I believe that will be the general shape of the outcome here. Maybe there’s a way for the Court to allow the tariffs to stand until Congress decides to “man up”, acting one way or the other. SCOTUS would probably like to do just that! Or maybe the Court could stay the lower court’s injunction until the case is heard by the Court in full on the regular docket, or until Congress acts.

There’s a decent chance, however, that Trump’s tariffs will be struck down, leaving it up to tariff supporters in Congress to lay down statutory rules rather than put up with the impulsive craziness we’ve witnessed thus far. If the Court lets the tariffs stand, it leaves the door open for new tests on the limits of executive discretion. Here is Greg Ip at the link:

“There would also be no end to uncertainty. ‘Unlike most other tariff authorities, these tariffs are not enshrined in statute, there’s no process to change them, and they can change very rapidly, in a day, without much notice, as we’ve seen,’ said Greta Peisch, a trade attorney at Wiley Rein and former general counsel for the U.S. trade representative.“

We’ve already seen strong hints that the Administration would like to force businesses to eat the cost of the tariffs rather than pass them along to consumers in higher prices. There hasn’t been any formal action of this kind by the Administration, at least not yet. Still, one can hardly blame businesses who might perceive an implicit threat if they fail to comply. That kind of bullying represents an a massive abuse of power. The Court could do everyone a big favor by clarifying that the authority to impose tariffs rests with Congress.

An opinion piece caught my eye written by one Chad Wolf. It’s entitled: “Retailers caught red-handed using Trump’s tariffs as cover for price gouging”. A good rule is to approach allegations of “price gouging” with a strong suspicion of economic buffoonery. You tend to hear such gripes just when prices should rise to discourage over-consumption and encourage production. The Wolf article, however, typifies the kind of attack on capitalism we hear increasingly from the “new right” (and see this).

Wolf, a former Homeland Security official in the first Trump Administration, says that large retailers like Walmart and Target are ripping off American consumers by raising prices on goods that are, in his judgement, “unaffected” by tariffs.

We’ll get into that, but first a quick disclaimer: I have no connection to Walmart or Target. Sure, I’ve shopped at those stores and I’ve filled a few prescriptions at a Walmart pharmacy. Maybe I have an ETF with an interest, but I have no idea.

Competition and Consumer Choice

Of course, no one forces consumers to shop at Walmart or Target. Those stores compete with a wide variety of outlets, including Costco and Amazon, the latter just a few clicks away. In a market, sellers price goods at what the market will bear, which ultimately serves to signal scarcity: a balancing between the cost of required resources and the value assigned by buyers. Unfortunately, in the case of tariffs, buyers and sellers of imports must deal with an artificial form of scarcity designed to extract revenue while benefitting other interests.

Wolf touts the “gift” of a free market for American businesses, as if private rights flow from government beneficence. He then decries a so-called betrayal by large retailers who would “price gouge” the American consumer in an effort to protect their profit margins. The free market is indeed a great thing! But his indignance is highly ironic as a pretext for defending tariffs and protectionism, given their destructive effect on the free operation of markets.

Broader Impacts

Wolf might be unaware that tariffs have an impact on a large number of domestically-produced goods that are not imported, but nevertheless compete with imports. When a tariff is charged to buyers of imports, producers of domestic substitutes experience greater demand for their products. That means the prices of these import-competing goods must rise. Furthermore, the effect can manifest even before tariffs go into effect, as consumers begin to seek out substitutes and as producers anticipate higher input costs.

Obviously, tariffs also impinge on producers who rely on imports as inputs to production. It’s not clear that Wolf understands how much tariffs, which represent a direct increase in costs, hurt these firms and their competitive positions.

“Expected” Does Not Mean “Unaffected”

Wolf cites the Federal Reserve’s Beige Book report (which he calls a “study”) to support his claim that businesses are gouging buyers for goods “unaffected” by tariffs. Here is one quote he employs:

“A heavy construction equipment supplier said they raised prices on goods unaffected by tariffs to enjoy the extra margin before tariffs increased their costs,” the Beige Book report said.“

Read that again carefully! Apparently Wolf, and whoever added this to the Fed’s Beige Book, thinks that being “unaffected by tariffs” includes firms whose future costs, including replacement of inventories, will be affected by tariffs! He goes on to say:

“… Walmart has already issued price hikes under the guise of tariff costs.“

The examples at his “price hikes” link were for Chinese goods in April and May, after Trump announced 145% tariffs on China in April. In mid-May, Trump said China would face a lower 30% tariff rate during a 90-day “pause” while a trade agreement was negotiated. It is now 55%, but the point is that retailers were forced to play a guessing game with respect to inventory replacement costs due to uncertainty imposed by Trump. They had a sound reason for marking up those items.

Fibbing on the Margin

Here’s an excerpt from Wolf’s diatribe that demonstrates his cluelessness even more convincingly:

“We all know many of these large retailers are sitting on comfortable, even expanded, profit margins because of the price hikes from COVID-19 that never came down. But it’s not enough for them. They want to fleece the American consumer and blame it on President Trump’s America First agenda.“

So let’s take a look at those profit margins that “never came down” after the pandemic, but in a longer historical context. Here are gross margins for Walmart since 2010:

Walmart’s margin today is about the same as the average for discount stores, and it is lower than for department stores, retailers of household and personal products, groceries, and footwear. Furthermore, it is lower today than it was ten years ago. While the margin increased a little during the pandemic, it fell in its aftermath, contrary to Wolf’s assertion. That the company has rebuilt margins steadily since 2023 should be viewed not as an indictment, but perhaps as a testament to improved managerial performance.

Wolf goes on to quote a former Walmart CEO who says that the 25 basis point increase in the gross margin in the latest quarter (from ~24.7% to 24.94%) indicates that the chain can “manage” the tariff impact. Of course it can, but that would not constitute “price gouging”.

A Trump Lackey

Of course, Wolf is taking his cues from Donald Trump, who has been bullying American businesses to “eat” the cost of his tariff onslaught, rather than passing them along to the ultimate buyers of imported goods. However, private businesses should not be expected to take orders from the President. This is not Mussolini’s Italy. Moreover, anyone familiar with tax incidence will understand that sellers are likely to eat some portion of a tariff (sharing the burden with buyers) without jawboning from the executive branch. That’s because buyers demand less at higher prices and sellers wish to avoid losing profitable sales, to the extent they can. But the dynamics of this adjustment process might take time to play out.

It’s also worth noting that a retailer might attempt to hold the line on certain prices in an uncertain cost environment. This uncertainty is a real cost inflicted by Trump. Meanwhile, pointing to increased prices for domestic goods, even if they are truly unaffected by tariffs, proves nothing without knowledge of the relevant cost and market conditions for those goods. It certainly doesn’t prove an “unpatriotic” attempt to cross subsidize imported goods.

In fact, one might say it’s unpatriotic for the federal government to restrict the market choices faced by American consumers and businesses, and for the President to tell American sellers that they better “eat” the cost of tariffs (or else?). And say, what happened to the contention that tariffs aren’t taxes?

Conclusion

Attacks on sellers attempting to recoup tariff costs are unfair and anti-capitalist. They are also somewhat disdainful of the economic sovereignty of American consumers, though not as much as the tariffs themselves. In the case described above, Chad Wolf would have us believe that sellers should not act on their expectations of near-term tariff increases. He also fails to recognize the impact of tariffs on import-competing goods and the cost of tariffs borne by producers who must rely on imported goods as inputs to production. Even worse, Wolf misrepresents some of the evidence he uses to make his case.

More generally, American businesses should not be bullied into taking a hit just because they serve customers who wish to buy imported goods. There is nothing unpatriotic about the freedom to choose what to goods to buy, what goods to stock, and how to maintain profitability in the face of government interference.

The federal government ran a budget surplus of $27 billion in June, much to the surprise of nearly everyone. The Trump Administration and MAGA-friendly media were eager to credit a big revenue boost from higher tariffs, which… ahem … they have assured us are notreally taxes. In any case, to attribute the June surplus to tariffs is flatly ridiculous. The truth is these “non-tax” magic revenue generators made a relatively small contribution to the apparent shift in the government’s fiscal position in June. And I say “apparent” because the surplus itself was something of a mirage.

Yes, tariffs brought in a total of almost $27B during June, which is about the same as the surplus recorded, but that was purely coincidental. It does not imply that tariffs “created” a surplus. Nor does it suggest that tariffs might just be able to balance the federal budget. Not a chance!

Here is one of two other sides of the story: the Treasury reported that the budget balance this June improved from a year ago by a total of $89 billion, from a deficit of $72B in June of 2024 to the aforementioned surplus of $27B in June 2025. Outlays were lower by about $38B this June, accounting for almost 43% of the improvement. Receipts were about $59B higher, with tariffs increasing by $20B relative to June 2024. So tariffs contributed just over a third of the boost in receipts. Altogether then, tariffs accounted for 22.5% of the improvement in the June budget balance between 2024 and 2025. That version of the story, as far as it goes, does not support the contention that tariffs “caused” the budget surplus in June, only that tariff revenue was a contributing factor.

Let’s dig a little deeper, however. Were it not for so-called “calendar adjustments” made by the Treasury, it would have reported a deficit of $70B in June. The reason? The first day of June fell on a Sunday this year, socertain payments were shifted to the last prior business day: Friday, May 30. That reduced June outlays substantially. Moreover, an extra business day in June 2025 added revenue. So the surplus in June was, in essence, an artifact of the calendar and had little to do with tariff revenue.

Incidentally, no one should be surprised by the growth of tariff revenue collected in June. When a tax rate more than triples (from a pre-Trump average of about 3% to 10% plus in June — net of tariff exclusions), one should expect revenue from that tax to increase substantially (and it was probably exaggerated by the extra business day).

Oh wait! Did I say tax?

With time, buyers will adjust and scale back their import purchases, reducing the revenue impact of the tariff hikes. However, we still don’t know how high tariffs will go. That means we could see substantially higher tariff revenue, though the demand response and a likely negative impact on incomes will cut into those gains. Either way, the revenue potential of tariffs is limited. Some estimates put the revenue impact of Trump’s tariffs at less than $250B annually. That seems conservative, but it’s significant revenue if it holds up. Still, it won’t come close to balancing a federal budget that’s almost $2 trillion in the hole. It certainly doesn’t justify a headlong dive into protectionism, which amounts to taking a crap on the economic freedom and prosperity of the American public.

Seemingly everyone wants to know: where is this tariff inflation you economists speak of? Even my pool guy asked me! We haven’t seen it yet, despite the substantial tariffs imposed by the Trump Administration. The press has been wondering about this for almost two months, and some of the MAGA faithful are celebrating the resounding success of the tariffs in this and other respects. Not so fast, grasshoppers!

There are a couple of aspects to the question of tariff inflation. One has to do with the meaning of inflation itself. Strictly speaking, inflation is a continuing positive rate of increase in the price level. Certain purists say it is a continuous positive rate of increase in the money supply, which I grant is least a step beyond what most people understand as inflation. Rising prices over any duration is a good enough definition for now, but I’ll return to this question below in the context of tariffs.

There is near-unanimity among economists that higher tariffs will increase the prices of imports, import-competing goods, and goods requiring imported materials as inputs. Domestic importers pay the tariffs, so they face pressure on their profit margins unless they can pass the cost onto their customers. But so far, since Donald Trump made his “Liberation Day” tariff announcement, we’ve seen very little price pressure. What explains this stability, and will it last?

Several factors have limited the price response to tariffs thus far:

— Some importers are “eating” the tariffs themselves, at least for now, and they might continue to pay a share of the tariffs with smaller margins.

“… cargo loaded onto ships in Asia on April 4 was not subject to the reciprocal tariffs, while cargo loaded April 5 was. Cargo coming from Asia can take up to 45 days to make it to U.S. ports and then must be transported to distribution centers and then on to customers. It is possible that goods from Asia subjected to high tariffs are only now making their way to customers. These two factors suggest the economic effects of increased tariffs could merely be delayed.“

— Data on prices is reported with a lag. We won’t know the June CPI and PPI until July 15, and the PCE price index (and its core measure, of most importance to the Fed) won’t be reported until July 31, and will be subject to revisions in subsequent months.

— Importers stocked up on inventories before tariffs took effect, and even before Trump took office. Once these are depleted, new supplies will carry a higher cost. That’s likely over the next few months.

— Uncertainty about the magnitude of the new tariffs. Trump has zig-zagged a number of times on the tariff rates he’ll impose on various countries, and real trade agreements have been slow in coming. This makes planning difficult. Nevertheless, inventories are likely to carry a higher replacement cost, but adjusting price creates a danger of putting oneself at a competitive disadvantage and alienating customers. Many businesses would prefer to wait for a clearer read on the situation before committing to a substantial price hike.

— Tariff exemptions have reduced the average tariffs assessed thus far to about 10%, well below the 15% official average. This will reduce the impact on prices and margins, but it is still a huge increase in tariffs and another source of uncertainty that should give importers pause in any effort to recoup tariffs by repricing.

— Importers are storing goods in “bonded warehouse“ to delay the payment of tariffs. This helps importers buy time before committing to pricing decisions.

— Kashkari notes that businesses can find ways to alter trade routes so as to lower the tariffs they pay. For example, he says some goods are being routed to take advantage of the relatively favorable terms of the free trade agreement between the U.S., Mexico, and Canada.

So it’s still too early to have seen much evidence of price pressure from Trump’s tariffs. However, that pressure is likely to become more obvious over the summer months. The expectation that tariffs should have already shown up in prices is just one of several errors of those critical of the Federal Reserve’s patience in easing policy.

Is there a sound reason to expect higher tariffs to produce a continuing inflation? Or instead, should we expect a “one-time” increase in the price level without further complications? Tariffs could generate an ongoing inflation if accompanied by an increase in the rate of money growth, or at least enough money growth to create expectations of higher inflation. Thus, if the Federal Reserve seeks to “accommodate” tariffs by easing monetary policy, that might lead to more widespread inflation. That could be difficult to rein-in, to the extent that higher inflation gets embedded into expectations.

Tariffs are excise taxes, and while they put upward pressure on the prices of imports and import-competing goods, they may have a contractionary effect on economic activity. Tighter budgets might lead to softer prices in other sectors of the economy and moderate the impact of tariffs on the overall price level.

The Fed’s reluctance to ease policy has been reinforced by another development. It’s usually argued that tariffs will strengthen the domestic currency due to the induced reduction in demand for foreign goods (and thus the need for foreign currency). Instead, the dollar has declined more than 9% against the Euro since “Liberation Day”, and the overall U.S. dollar index experienced its steepest first-half decline in 50 years. A lower dollar stimulates exports and depresses imports, but it also can lead to “imported” inflation (in this case, apart from the direct impact of tariffs). Uncertainty regarding tariffs deserves some of the blame for the dollar sell-off, but the fiscal outlook and rising debt levels have also done their part.

The upshot is that Trump’s tariffs are likely to cause a one-time increase in the price level with possibly a mild contractionary effect on the real economy. So it’s a somewhat stagflationary effect. It won’t be disastrous, but the tariffs can be made more inflationary than they “need be”. That’s why Trump is foolish to persist in haranguing the Fed for not rushing to ease policy.

First, a few more comments re: my speculative musings that Donald Trump’s tariff rampage could ultimately result in a regime with lower trade barriers, at least with a subset of trading partners. Arthur Laffer and Stephen Moore suggested last week that the White House should propose reciprocal free trade with zero barriers and zero subsidies for exports to any country that wishes to negotiate. A more cynical Ben Zycher scoffed at the very possibility, noting that Trump and his lieutenants view any trade deficit as evidence of cheating in one form or another. Zycher is convinced that Trump lacks a basic understanding of the (mostly) benign forces that drive trade imbalances.

I’ve said much the same. Trump’s crazy notions about trade could scuttle negotiations, or he might later accuse a trading partner of cheating on the pretext of a bilateral trade deficit (he’s done so already). And all this is to say nothing of the serious constitutional questions surrounding Trump’s tariff actions.

The mistaken focus on bilateral trade deficits also manifests in certain proposals made during trade negotiations: “Okay, but you’re gonna have to purchase vast quantities of our soybeans every year.” This sort of export promotion is a further drift into industrial planning, and it’s just too much for Trump’s trade negotiators to resist.

This might well turn out as an exercise in self-harm for Trump. However, I’ve also wondered whether his trade hokum is pure posturing, especially because he expressed support for a free trade regime in 2018. Let’s hope he meant it and that he’ll pursue that objective in trade talks. Please, just negotiate lower trade barriers on both sides without the mercantilist baggage.

Which brings me to the theme of this post: it would probably be simpler and more effective for the U.S. to simply drop all of its trade barriers unilaterally. There should be limited exceptions related to national security, but in general we should “turn the other cheek” and let recalcitrant trade partners engage in economic self-harm, if they must.

Okay, Wise Guy, What’s Your Plan?

I have a few friends who bemoan the lack of “fair play” against the U.S. in foreign trade. They have a point, but they also hold an unshakable belief that the U.S. can be just as efficient at producing anything as any other country. They are pretty much in denial that comparative advantages exist in the real world. They are seemingly oblivious to the critical role of specialization in unlocking gains from trade and lifting much of the world’s population out of penury over the past few centuries.

Furthermore, these friends believe that Trump is justified in “retaliating” against countries with whom the U.S. runs trade deficits. If tariffs are so bad, they ask, what would I do instead? Again, here’s my answer:

Eliminate (almost) all barriers to trade imposed by the U.S. Let protectionist nations choke themselves with tariffs/trade barriers.

Before getting into that, I’ll address one fact that is often denied by protectionists.

Yes, a Tariff Is a Tax!

Protectionists often claim that tariffs are not really taxes on U.S. buyers. However, tariffs are charged to buyers of imported goods (often businesses who sell imported goods to consumers or other businesses). In principle, tariffs operate just like a sales tax charged to retail buyers. Both raise government revenue, and they are both excise taxes.

In both cases, the buyer pays but generally bears less than the full burden of the tax. That’s because demand curves slope downward, so sellers (foreign exporters) try to avoid losing sales by moderating their prices in response to the tariff. In both cases, sellers end up shouldering part of the tax burden. How much depends on how buyers react to price: a steep (inelastic) demand curve implies that buyers bear the greater part of the burden of a tariff or sales tax.

People sometimes buy imports due to a lack of substitutes, which implies a steep demand curve. Consumer imports are often luxury items, and well-heeled buyers may be somewhat insensitive to price. Most imports, however, are inputs purchased by businesses, either capital goods or intermediate goods. In the face of higher tariffs, those businesses find it difficult and costly to arrange new suppliers, let alone domestic suppliers, who can deliver quickly and meet their specifications.

These considerations imply that the demand for imports is fairly inelastic (steeper), especially in the short run (when alternatives can’t easily be arranged). Thus, import buyers bear a large portion of the burden in the immediate aftermath of an increased tariff. By imposing tariffs we tax our own citizens and businesses, forcing them to incur higher costs. Correspondingly, if demand is inelastic, an importing country tends to gain more than its trading partners by unilaterally eliminating its own tariffs.

Tariffs on imports also trigger price hikes by import-competing producers. Sometimes this is opportunistic, but even these producers incur higher costs in attempting to meet new demand from buyers who formerly purchased imports. (See this post for an explanation of the costly transition, including a nice exposition of the waste of resources it entails.)

Other Forms of Blood Letting

Beyond tariffs, certain barriers to trade make it more difficult or impossible to purchase goods produced abroad. This includes import quotas and domestic content restrictions. These barriers are often as bad or worse than tariffs because they increase costs and encumber freedom of choice and consumer sovereignty.

Another kind of trade intervention, export subsidies, must be funded by taxpayers. Subsidies are too easily used to protect special interests who otherwise can’t compete. Currency manipulation can both subsidize exports and discourage imports, but it is often unsustainable. The common theme of these interventions is to undermine economic efficiency by shielding the domestic economy from real price signals.

Let Them Tax Themselves

Suppose the U.S. simply turns the other cheek, eliminating all of our own trade interventions with respect to country X despite X’s tariffs and other interventions.

To start with, the existence of barriers means that both countries are unable to exploit all of the benefits of specialization and mutually beneficial trade. Both countries must produce an excess of goods in which they lack a comparative advantage, and both countries produce too few goods in which they have a comparative advantage. Both incur extra costs and produce less output than they could in the absence of trade barriers.

Unilateral elimination of U.S. tariffs and other barriers would reduce high-cost domestic production of certain goods in favor of better substitutes from country X. But Country X gains as well, because it is now able to produce more goods and services for export in which it possesses a comparative advantage. Therefore, the unilateral move by the U.S. is beneficial to both countries.

On the other hand, U.S. export industries are still constrained by country X’s import tax or other restraints. These would-be exporters are no worse off than before, but they are worse off relative to a state in which buyers in country X could freely express their preferences in the marketplace.

What exactly does country X gain from tariffs and other trade burdens on its citizens? It denies them full access to what they deem to be superior goods and services at an acceptable price. It means that resources are misallocated, forcing abstention or the use of inferior or costlier domestic alternatives. Resources must be diverted to relatively inefficient firms. In short, the tariff makes country X less prosperous.

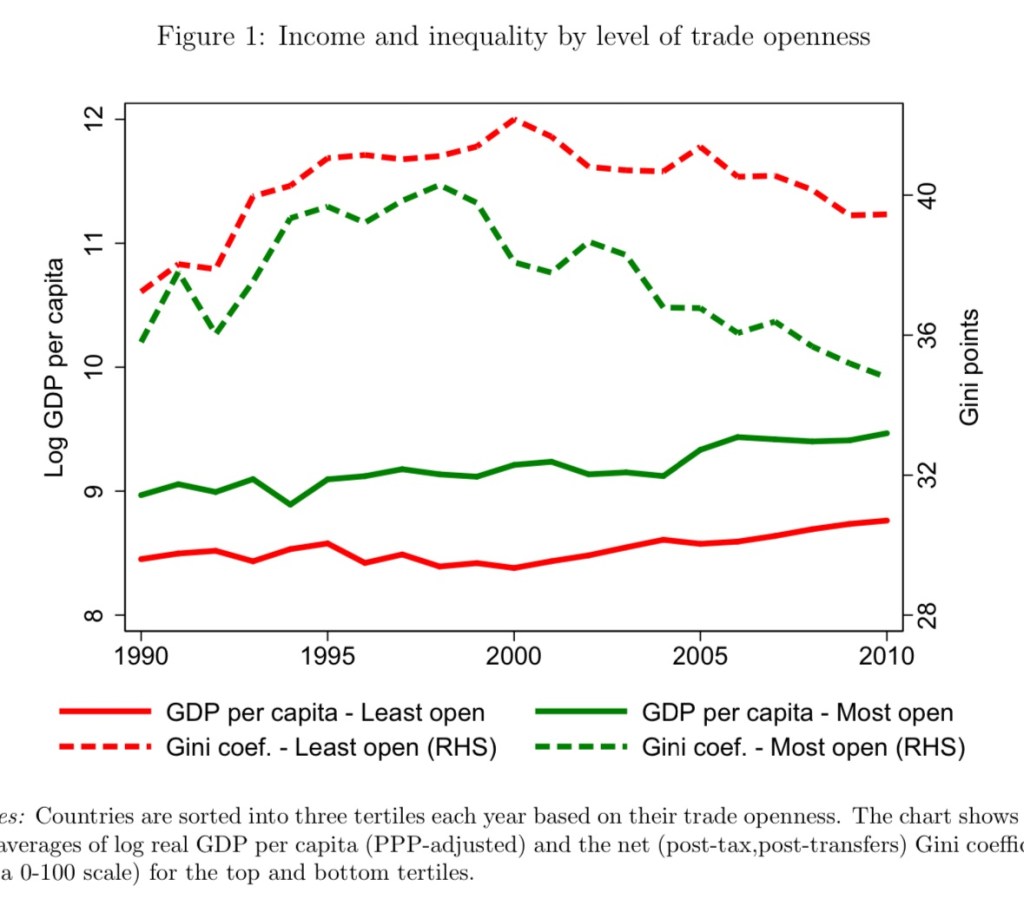

Empirical evidence shows that more open economies (with fewer trade barriers) enjoy greater income and productivity growth. This study found that “trade’s impact on real income [is] consistently positive and significant over time.”See this paper as well. Trade barriers tend to increase the income gap between rich and poor countries. The chart below (from this link) compares real GDP per capita from the top third and bottom third of the distribution of countries on a measure of trade “openness”. Converting logs to levels, the top third has more than twice the average real GDP per capita of the bottom third. And of course, the averaging process mutes differences between very open and very closed trade policies.

The chart also shows that countries more “open” to trade have more equal distributions of income, as measured by their Gini coefficients.

An important qualification is that domestic production of certain goods and services might be critical to national security. We must be willing to tolerate some inefficiencies in that case. It would be foolish to depend on a hostile nation for those supplies, despite any comparative advantage they might possess. It’s reasonable to expect such a list of critical goods and services to evolve with technological developments and changing security threats. However, merely acknowledging this justification leaves the door open for excessively broad interpretations of “critical goods”, especially in times of crisis.

Setting a Good Policy and Example

Here’s an attempt to summarize:

Tariffs are taxes, and non-tariff barriers inflict costs by distorting prices or diminishing choice

Trade barriers reduce economic efficiency and produce welfare losses

Trade barriers deny the citizens of a country the benefits of specialization

Both countries gain when one trading partner eliminates tariffs on imports from the other

The demand for imports is fairly inelastic, at least in the short run. Thus, the gain from eliminating a tariff will be skewed toward the domestic importers

Both countries gain when they agree to eliminate any and all trade barriers

Across countries, trade barriers are associated with lower incomes, lower income growth, and more unequal distributions of income

The U.S. has a large number of trading partners. Every liberalization we initiate means a welfare gain for us and one trading partner, who would do well to follow our example and reciprocate in full. Not doing so foregoes welfare gains and leads to incremental losses in income relative to more trade-friendly nations. Across all of our trading relationships, a unilateral end to U.S. trade barriers would almost certainly convince some countries to reciprocate. Those that refuse would suffer. Let them self-flagulate. Let them tax themselves.

Donald Trump’s imposition of higher tariffs — much higher tariffs — on our trading partners carries tremendous risk. See this article for a good summary of the tariffs Trump levied (and now paused for 90 days) on imported goods from different countries. The President believes he can win major concessions from other nations in terms of trade barriers as well as foreign policy objectives. But he would also have us believe that we’ll be better off even if those concessions fall short of his hopes.

Perhaps he’s posturing, but Trump seems to thinks tariffs are some kind of elixir. That is nonsense for a variety of reasons. I’ve discussed several of those previously and I’ll add more in a subsequent post. Here, I’ll attempt to give Trump his due. I’m highly skeptical, but I’ll be happy to eat crow if he is successful in achieving a trade regime with lower tariffs and other barriers across many of our trading partners.

Markets

The tariff announcements last week on “Liberation Day” spooked markets, prompting a continuation of the classic flight to safety we’ve witnessed since Trump began to rattle his trade saber. This has driven bond prices up and long-term interest rates down, though now we’re seeing a partial reversal (if it holds). Will lower interest rates help save the day for Trump? It will bring lower borrowing costs to many borrowers, including the federal government, and it should help to buttress stock values, softening the blow to some extent.

The tariffs, should they remain in place, are likely to boost inflation temporarily (a one-time increase in the price level) and could very well tip the U.S. economy into recession. Depending on the severity, those developments would undercut the GOP’s hopes of maintaining a congressional majority in the 2026 mid-term elections. Then, he’d truly have managed to cut off his nose to spite his face. Still, Trump thinks he knows something about tariffs that markets don’t.

Dominoes

Bill Ackman has expressed a view of how markets are reacting and how they might evolve under Trump’s trade policy. He thinks markets would be fine had the President set tariffs at levels matching our trading partners (doubtful at best), but Trump went bigger in order to jolt other nations into negotiating. Ackman thinks there might be a “tipping point” when countries line up at the negotiating table. And indeed, as of April 7, the administration said “up to” 70 countries had reached out to enter new trade negotiations with the U.S. That probably helped bring investors out of their doldrums, pending actual deals.

Elon Musk states a desire to see tariffs eliminated between the U.S. and the EU, and the EU has made a limited offer along those lines. This might be indicative of similar thinking by others in the administration. But Trump insists he’ll always revisit tariffs wherever he sees a bilateral trade deficit. Contrary to all economic logic, he is convinced that trade deficits are harmful, when in fact they mainly reflect our relative prosperity.

Hard-Nosed, High Stakes

Economists have been almost uniform in their condemnation of Trump’s approach trade. To some extent, that’s a visceral reaction to Trump’s pro-tariff rhetoric and revulsion to his opening moves. But is there an economic rationale for this type of aggressive attempt to bargain for lower trade barriers? Yes, and it’s not a terribly deep insight, and it carries great risks in the real world.

From a game-theoretic perspective, it’s possible that a dominant trading partner, in repeated rounds, can ultimately achieve lower bilateral trade barriers through the threat or imposition of higher barriers to imports from a trading partner. The key is the difference in costs that barriers impose on the two nations. One is in a position to leverage its dominant position, inflicting greater costs on the other nation as an inducement to gain concessions and achieve improved conditions for mutual trade.

The U.S. is almost uniformly the dominant partner in bilateral trade relationships. That’s because U.S. GDP is so large and U.S. trade with any given country is a comparatively small fraction of GDP. But dominance can mean different things: there are countries that supply critical goods to the U.S., like oil, semiconductors, or rare earths, which may give certain countries disproportionate leverage in trade negotiation. Those products along with many others are exempted from Trump’s tariffs.

Other Cards

Nevertheless, the U.S. has economic leverage over individual trading partners in the vast majority of cases, which Trump certainly is willing to exploit. And Trump has another powerful tool with which to negotiate with some trading partners: U.S. military protection. Using it might expose the U.S. to strategic disadvantages, but don’t put it past Trump to bring this up in negotiations!

Trump is doing his best to prove a readiness to escalate. That might build his credibility except for a couple of critical facts: first, his actions have already violated at least 15 existing treaties. Why should they trust him? Second, some groups of nations are likely to present a united front, putting them on a more equal footing with the U.S. This makes a trade war between the U.S. and the rest of the world more likely.One nation in particular stands ready to capitalize on severed relations between other nations and “Donald Trump’s” America: Xi Jinping’s China. Bilateral trade with China might just be the Super Bowl of these tariff games. Unfortunately, it could be a Super Bowl where everyone loses!

An additional complication: while the U.S. has dominance in most of its trade relationships, the barriers to U.S. goods erected by other nations are often supported by powerful special interests. Trump’s ability to strike deals will be complicated where governments are captive to these interests, which might be concentrated among powerful elites or of a more diffuse, nationalist/populist nature.

Deep In the Woods

There is optimism in some quarters that a few successful trade deals will lead to a “tipping point” in the willingness of other nations to negotiate with Trump. Despite the sudden clamor among our trade partners to negotiate, we’re a long way from getting solid agreements. Investors still assess a greater risk of a world trade war than vanishing barriers to trade.

Look I've been as critical of tariffs as anyone but if the long term vision is domestic Nike sweatshops filled with fired DC bureaucrats, I'm willing to listen https://t.co/CmsJ7bx5vk

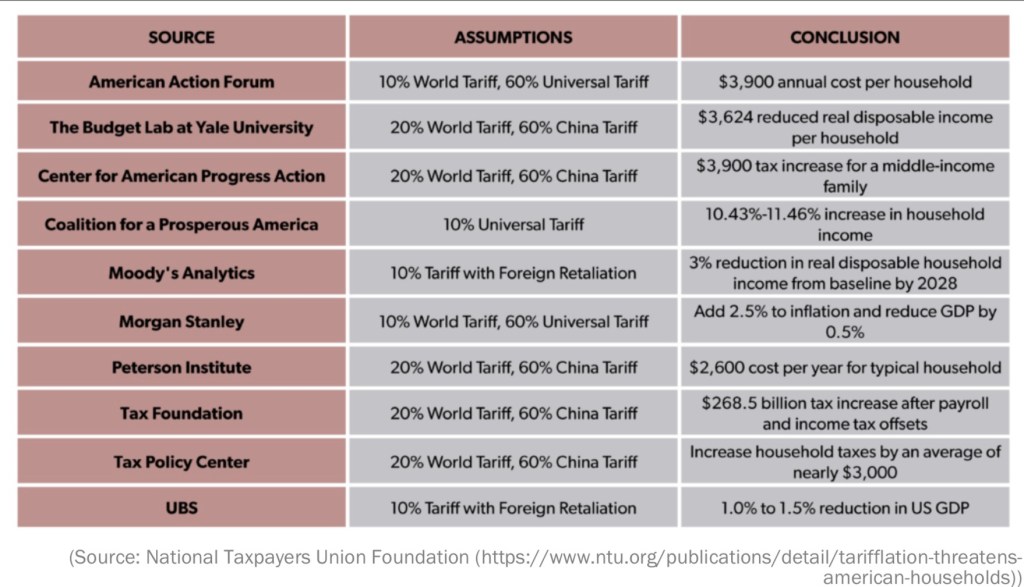

The table above is from Eric Boehm at Reason.com. It shows a variety of negative economic projections based on the likely imposition of tariffs by the incoming Trump Administration. Donald Trump’s protectionist agenda is motivated in large part by the notion that imports of foreign goods and services harm the U.S. economy. This misapprehension is common on both the populist left and the nationalist right, but it is also fueled by special interests averse to competition. Especially puzzling are those who extol the virtues of capitalism and free markets while claiming that free markets across borders are inimical to our nation’s economic interests.

Imports and Domestic Spending

Many assume that imports directly reduce GDP. In fact, on this point, some might be led astray by a superficial exposure to macroeconomics. As Noah Smith has noted, they might think back to the simple spending definition of GDP they learned as college freshmen:

GDP = C + I + G + (X – M),

where C is consumer spending on final goods and services, I is investment spending, G is government spending, X is foreign spending on U.S. exports, and M is U.S. spending on imports from abroad. So imports are subtracted! Doesn’t that mean imports directly reduce GDP?

The key here is to recognize that C, I, and G already include spending on imported goods. Therefore, imports must be subtracted from the spending totals to find the value spent on domestically-produced final goods and services. No, imports are not a direct, net subtraction from GDP.

Your Loathsome Foreign Car

Of course the domestic impact of imports goes deeper than this simple accounting framework. If someone decides to purchase an imported good instead of a close substitute produced domestically, what happens to GDP? If the decision has an immediate impact on production, then U.S. GDP declines. Otherwise, the domestic good is new inventory investment (part of I above), and there is no change. But if the import decision is repeated, the result is permanently lower U.S. GDP relative to the alternative, as producers won’t want to add to inventories indefinitely. The same is true if a domestic producer decides to purchase a component or raw material produced overseas rather than one produced at home.

The import decision causes a domestic producer to lose a sale along with the profit that sale would have earned. That puts pressure on the firm’s workers and wages as well. The firm still has the value of the unit in inventory, but if the import decision is repeated there will be more substantial follow-on effects on production, employment, spending, and saving.

Not So Fast

There is still more to the story, of course. By purchasing the foreign good,,which in the buyer’s estimation delivers greater value at that point in time, there is a gain in consumer surplus that is very real. To the buyer, that gain is perhaps equivalent to dollars in the bank. Their real wealth has increased relative to the surplus value of the foregone domestic purchase. This, too, will likely have follow-on effects in terms of spending and saving, but positive effects.

Therefore, to a first approximation, the immediate effects of an import purchase on total domestic welfare are ambiguous. Consumers of imports gain value; producers of import-competing goods lose value.

As to the loss of the domestic sale, competition is tough, but it greatly contributes to the efficiency of the free market system and to the well being of consumers. Let’s face it: ultimately, the whole point of economic activity is to enable consumption. Production has no other purpose. So producers must react to competition and strive to improve value for buyers along any margins they can. That, in turn, is unequivocally positive for potential buyers both here and abroad.

It’s also true that the purchase of foreign goods means that dollars must be sold in exchange for foreign currency. That weakens the dollar, but those “excess dollars” are generally used to purchase U.S. assets, including physical capital. That direct investment promotes economic growth.

Open Economy, Open Mind

No matter what you believe about the net benefits or costs of a single import transaction like the one described above, it is misleading to draw conclusions about the benefits of foreign trade based on a single transaction, or even a series of repeated transactions.

First, consumer sovereignty is based on freedom of choice, including the freedom to purchase from any seller, domestic or foreign. Consumers greatly benefit from that broad freedom. Add to that the benefit of producers who are free to purchase inputs from any source they believe to offer the greatest value (a benefit that ultimately flows through to consumers). These freedoms ultimately enhance productivity and well being.

Trade across borders leverages the same economic advantages as trade within borders. People tend to accept the latter as truth without giving it a thought, yet the former is often rejected reflexively. The question is inappropriately bound up in issues like patriotism and, over time, an excessive focus on high-visibility job losses in traditional industries.

Trade allows people and their countries to specialize in producing things at which they are comparatively efficient, i.e., in which they are lower-cost producers. This is at the very heart of mutually beneficial exchange: no party to a voluntary transaction expects to suffer a loss. And in trade, when an external, domestic party sustains a lost sale, for example, they have the opportunity to improve or reallocate their resources to endeavors to which they are better suited. So there are direct gains from trade and there are indirect gains via the discipline of competition, including the benefits of reallocating scarce resources from inefficient to efficient uses.

Tariff Gains

Now we shift gears to tariffs: interventions having benefits that are more concentrated than costs, and which tend to be more ephemeral:

— Domestic producers who compete with imports gain through the grant of additional market power, given the tax on foreign goods and services. These producers now have more pricing flexibility, and what is often more pertinent, survivability.

— Workers at domestic firms will benefit to the extent that their employers face reduced foreign competition. Some combination of employment, hours, and wages may rise.

— Some firms have mixed gains and losses, with more pricing power over final product but elevated costs due to the use of taxed foreign components.

Tariff Losses

Who pays when government succumbs to irrational protectionist pressure and attempts to restrict imports via tariffs?

— Domestic consumers suffer a loss of freedom and bear a large part of the burden of the tariff tax.

— Higher prices for imports lead to higher prices for competing domestic goods, causing consumers to experience a loss of purchasing power.

— Domestic businesses suffer a loss of control over input decisions. Those already utilizing foreign inputs (and their buyers downstream) bear some of the burden of the tariff tax. For example, tariffs could be quite damaging to the U.S. AI industry, a result that would run strongly contrary to Trump’s promise to promote American AI.

— The U.S. suffers a loss of foreign investment, which could engender higher interest rates, lower productivity growth, and lower real wages.

— As Tyler Cowen puts it in a review of this paper, “… lobbying, logrolling and political horse-trading were essential features of the shift toward higher US tariffs. A lot of the tariffs of the time [1870 -1909] depended on which party controlled Congress, rather than economic rationality.“

— Tariffs tend to reduce economic growth due to diminished productivity in tariff-protected industries, which also erodes real wages. Less productive firms capture a significant share of the benefits of tariffs, so that economic growth falls due to a compositional effect. Higher prices for imports and import-competing goods undermine the real gains of import-protected workers.

— Finally, tariffs invariably beget retaliatory tariffs by erstwhile friendly trading partners. Export industries and their employees take a direct hit. This retaliation damages the prospects of the most productive exporters, while weaker exporting firms might be forced to close shop unnecessarily.

One other note: the discussion of gains and losses above is essentially the same for policies that reward the use of American labor via tax breaks. This not only penalizes imports of final and intermediate foreign goods, it subsidizes high-cost domestic labor. Obviously, the upshot is a less competitive U.S. economy.

Tariff-Threat Policy

To be fair, Donald Trump has said he’d use the threat of tariffs strategically to achieve a variety of objectives, not all of which are directly related to trade. We can hope that many of those threats won’t be acted upon. On one hand, that’s more appealing than general tariffs, with potential foreign policy gains and less in the way of general damage to the economy. On the other hand, the discretionary application of tariffs could invite political favoritism and foster a corrupt rent-seeking environment.

Conclusion

Trade protectionism protects weak and strong producers alike. The weak should not be given artificial incentives to produce goods inefficiently. That’s simply a waste of resources. Protecting the strong is unnecessary and discourages the drive for efficiency as well as real value creation. It lends market power to already powerful firms, leading to higher prices and penalizing domestic consumers.

One last aside: tariffs cannot raise anywhere close to the revenue necessary to replace the income tax, an absurd claim made by Trump on the campaign trail.

Only free trade is consistent with the values of a free society. It enhances choice, makes markets more competitive, creates incentives for efficiency, and cultivates opportunities for economic growth, That would serve Trump and the nation much better than the fixation on tariffs.

As if you needed more evidence that governments are incompetent, look no further than trade policy: public officials the world over are almost universally ignorant regarding the effects of international trade and trade imbalances. In this sense, the Trump Administration’s new tariffs on imported steel and aluminum are in keeping with the long history of public sector foibles on trade. This phenomenon stems from an unhealthy and obsessive focus on the well-being of producers without regard to the implications of policy for consumers. Warren Meyer of Coyote Blog offers an evaluation of Chinese trade policy, which he mischievously (I believe) claims was written by a Chinese blogger on a “sister blog” called “Panda Blog“. Despite Meyer’s playfulness, the post is instructive:

“Our Chinese government continues to pursue a policy of export promotion, patting itself on the back for its trade surplus in manufactured goods with the United States. The Chinese government does so through a number of avenues, … each and every one of these government interventions subsidizes US citizens and consumers at the expense of Chinese citizens and consumers. A low yuan makes Chinese products cheap for Americans but makes imports relatively dear for Chinese. So-called ‘dumping’ represents an even clearer direct subsidy of American consumers over their Chinese counterparts. And limiting foreign exchange re-investments to low-yield government bonds has acted as a direct subsidy of American taxpayers and the American government, saddling China with extraordinarily low yields on our nearly $1 trillion in foreign exchange. Every single step China takes to promote exports is in effect a subsidy of American consumers by Chinese citizens.“

The very idea of a trade deficit is often used to intimate a threat to a nation’s economic health. Conversely, a trade surplus is used to suggest that a nation is achieving great economic success. Both contentions are nonsense. Here is more from “Panda Blog“:

“We at Panda Blog believe it is insane for our Chinese government to continue to chase the chimera of ever-growing foreign exchange and trade surpluses. These achieved nothing lasting for Japan and they will achieve nothing for China. In fact, the only thing that amazes us more than China’s subsidize-Americans strategy is that the Americans seem to complain about it so much. They complain about their trade deficits, which are nothing more than a reflection of their incredible wealth. … They complain about China buying their government bonds, which does nothing more than reduce the costs of their Congress’s insane deficit spending. They even complain about dumping, which is nothing more than a direct subsidy by China of lower prices for American consumers.

And, incredibly, the Americans complain that it is they that run a security risk with their current trade deficit with China! This claim is so crazy, we at Panda Blog have come to the conclusion that it must be the result of a misdirection campaign by CIA-controlled American media. After all, the fact that China exports more to the US than the US does to China means that by definition, more of China’s economic production is dependent on the well-being of the American economy than vice-versa.“

By the way, those “quotes” from “Panda Blog” appeared on Coyote Blog 12 years ago!

All nations tend to play these trade games to one extent or another. But protectionist actions always harm a nation’s consumers more than they help producers, a proposition that is easy to demonstrate using a simple supply and demand diagram. While the class of consumers is broader than the class of producers, ultimately “producer” and “consumer” are different roles played by the same individuals. So protectionism is always harmful to a nation, on balance. Furthermore, retaliation against another nation for its dim-witted trade barriers also harms the retaliating nation’s consumers more than it helps its producers, and that’s true regardless of whether retaliation begets reciprocal actions.

Of course, producers are generally in a better position than consumers to grease the political skids in their favor. In a separate post, Meyer notes that protectionist trade policies are rooted in cronyism. The costs to society are very real, but they tend to be diffuse and therefore less obvious to most consumers.

“A lot of the media seems to believe the biggest reason they are bad is that they will incite retaliatory tariffs from other countries, which they almost certainly will. But even if no one retaliated, even if the tariffs were purely unilateral, they would still be bad. In case after case, they are justified as increasing the welfare of a certain number of workers in targeted industries, but they hurt the welfare of perhaps 100x more people who consume or work for companies that consume the targeted products. Prices will rise for everyone and choices will be narrowed.“

A couple of points deserve emphasis in relation to my last post on Trump’s tariff action:

In terms of jobs, the tariffs announced by President Trump present a very poor risk-reward tradeoff (WSJ article is gated):

“The policy point is that Mr. Trump’s tariffs are trying to revive a world of steel production that no longer exists. He is taxing steel-consuming industries that employ 6.5 million and have the potential to grow more jobs to help a declining industry that employs only 140,000.“

Stephen Mihm discusses ways in which the U.S. steel industry squandered its superiority in the post-World War II era. Much of Mihm’s article is devoted to the industry’s failure to upgrade to new production technologies. Interestingly, however, it fails to mention the damaging role played by unions in the process. “Dumping” had very little to do with it.

Finally, Pierre Lemieux takes a closer look at the national security argument for trade barriers. He concludes that it is fallacious. Of course, it is an excuse for cronyism. Protectionism harms the competitiveness of the protected industries, which actually undermines national security. And protectionism is usually unnecessary on close examination. In the case of steel, for example, national defense and homeland security use only about 3% of American steel production. Beyond that simple fact, the argument is dangerously open-ended. Almost anything can be represented as critical to national security: steel, food, clothing, and many other categories. Even human resources.

Today, Trump announced that Canada and Mexico will be exempt from the new tariffs while a renegotiation of the North American Free Trade Agreement (NAFTA) is underway. That’s better, but this carve-out exempts only 25% of U.S. steel imports. Perhaps Australia will be granted an exemption as well, but additional carve-outs will prompt further increases in tariffs on non-exempt imports. Trump also said that U.S. flexibility in applying the new tariffs to allies will depend on their commitments for military spending!

Thus, rather than maintaining the pretense that trade relationships are about economics, the administration has conceded that the tariffs and the exemption process will be transparently political, never a prescription for efficient resource allocation. Moreover, U.S. trading partners are likely to be reluctant to test the politics of modifying their own trade manipulations at home. Indeed, the politics may dictate retaliation, rather than concessions. In any case, the governments of our trading partners are as clueless on trade as Trump, his Commerce Secretary Wilbur Ross, and his economic advisor Peter Navarro, or they would never intervene in private trade decisions to begin with.

In advanced civilizations the period loosely called Alexandrian is usually associated with flexible morals, perfunctory religion, populist standards and cosmopolitan tastes, feminism, exotic cults, and the rapid turnover of high and low fads---in short, a falling away (which is all that decadence means) from the strictness of traditional rules, embodied in character and inforced from within. -- Jacques Barzun

{kind=link}