A lot has changed since Kevin Warsh was nominated by President Trump to replace Jerome Powell as chairman of the Federal Reserve Board. Most notably that includes the war in Iran, the run-up in oil prices, and a bond market increasingly nervous about inflation as it attempts to digest massive supplies of new Treasury debt. Tariffs have also contributed to the updraft in measured inflation since then, which (in addition to oil prices) represents another impingement on the economy’s supply side.

Change and Change Itself

By the time Warsh was sworn in as chairman, expectations for Fed rate cuts had swung to expectations of a quarter-point increase in the federal funds rate target, if not at the mid-June meeting of the Federal Open Market Committee (FOMC) then in July. It’s not clear that Warsh is on board with that, and the status of the Iranian conflict, oil supplies, and the bond market could change dramatically before the June meeting.

Short-term inflation expectations have risen, so a rate hike by the Fed might seem reasonable if not for the possibility that current inflation is transitory (but I use that term guardedly). In terms of money growth, policy seems roughly neutral to slightly restrictive. M2 growth from a year earlier was 4.7% in April. Nominal (current dollar) GDP grew at a slightly faster 5.1% clip in the first quarter, and it might accelerate in Q2. Real GDP advanced 1.6% from a year ago in the first quarter, but the Atlanta Fed’s forecast for real GDP in Q2 is a stronger 3.2%. Meanwhile, core PCE inflation (the Fed’s preferred gauge) was 3.1% in the first quarter and 3.3% in April. If the numbers roughly follow the same track going forward, nominal GDP in Q2 could be up by about 6% – 6.5% from a year ago. Slowing the rate of M2 growth much from its recent pace might be an overreaction.

Moreover, it might be premature to raise the funds rate when a peaceful resolution to the Iran conflict is still possible. Again, we might know by the time the FOMC convenes in June. In that case, market rates could ease quickly. I am skeptical, however, that Iran will prove to be a reliable partner to any peace agreement. I’ll be surprised if the blockade on the Strait of Hormuz ends any time soon, and a few air strikes have already been renewed. Still, I expect the FOMC to defer any rate hike until at least the July meeting. In fact, I’ll be surprised to see one at all.

Sound Money or Monetary Madness

Many describe Warsh as a “sound money” guy, having been greatly influenced by Milton Friedman. He’s been critical of quantitative easing (QE): the Fed’s purchases of securities for its own balance sheet to provide liquidity to the markets and banking system. If the hostilities continue in Iran, Warsh is more likely to favor quantitative tightening (QT) in the short-term than rate hikes. QT would involve reductions holdings of securities on the Fed’s balance sheet, which Warsh has long advocated.

On the other hand, Warsh has been undaunted in insisting that the AI revolution will be a dramatic deflationary force. That’s a longer-term proposition, but it reinforces his preference for lower rates. So Warsh is for “sound money” and would like to see QT, but he also prefers lower rates and apparently believes that AI might justify a more expansionary monetary posture. So where does that leave us?

Squaring the Circle

A few months ago I described a coherent policy agenda for the Fed under Kevin Warsh, given his policy preferences. It might have lacked realism in terms of Fed politics, but it was motivated by the question of whether lower rates are compatible with QT. The discussion did not anticipate the Iran conflict and its economic and financial consequences.

Lower rates and QT would be compatible if the Fed enables and incentivizes commercial banks to hold more securities and lend more aggressively. This would require regulatory changes as well as reductions in interest on bank reserves (IOR) held at the Fed.

Judy Shelton in the Wall Street Journal has made the same point, characterizing such a policy shift as “pro-market”. That’s because it would allow banks to invest in relatively safe assets, would eliminate a subsidy masquerading as a price (IOR – though fully administered), and would mean a transition from the Fed’s emphasis on maintaining ample bank reserves to scarce bank reserves. The latter would restore activity in the market for overnight loans of reserves (federal funds), which would then trade at a price corresponding to their degree of scarcity. That would provide an important signal to other markets, not to mention the Fed itself. Today, that signal is distorted by the Fed’s provision of ample reserves (repo rates notwithstanding). Jai Kadia and Norbert Michel have madea similar argument, along with advocating for rules-based monetary policy, rather than frequently destabilizing discretionary actions.

Momentum

In April, David Beckworth noted that momentum is buildingin influential circles for this change, which he describes as a “demand driven” approach, as opposed to the “supply driven”, ample reserve operating procedure now in force. This is the more common at many foreign central banks, and it has received prominent mention in recent speeches and statements by Fed officials. As Beckworth puts it in the title of his post, “The Fed’s Overton Window Is Shifting”.

Beckworth also mentions Warsh’s desire to establish a new Treasury-Fed Accord. The original 1951 Accord established the Fed’s independence from Treasury financing operations. Today’s ample reserves approach has made it far too easy for the Fed to succumb to pressures to monetize deficits and intervene in capital markets to manipulate longer rates. Warsh would surely like to re-establish the Fed’s monetary authority as a separate and independent function from Treasury financing.

The Fed Board of Governors (BoG) must approve changes in interest on reserves (IOR). (Better yet, an act of Congress would be required to prohibit IOR.) But Warsh, who is said to have good relations with the Fed staff and other Fed governors, is less likely to get a majority on the BoG than even the FOMC. For now, he’ll have to be persuasive to gain the support of a majority of either body.

Summary

Kevin Warsh is likely to argue strenuously for reductions in the size of the Fed’s balance sheet, and would almost certainly be happy for the FOMC to defer any rate hikes pending more clarity on a resolution to the Iran conflict. He will also argue for creating greater incentives for banks themselves to invest in Treasury debt, including reformed regulations on bank asset holdings and reduced interest on reserves held at the Fed. Ultimately, that would pave the way for lower rates on a variety of assets. But the Fed should be probably be cautious and gradual in the implementation: the changes to IOR and bank regulations must be well coordinated with QT and money growth must be calibrated to meet the Fed’s inflation target (or better yet, a nominal GDP target — see Part 2 of this post).

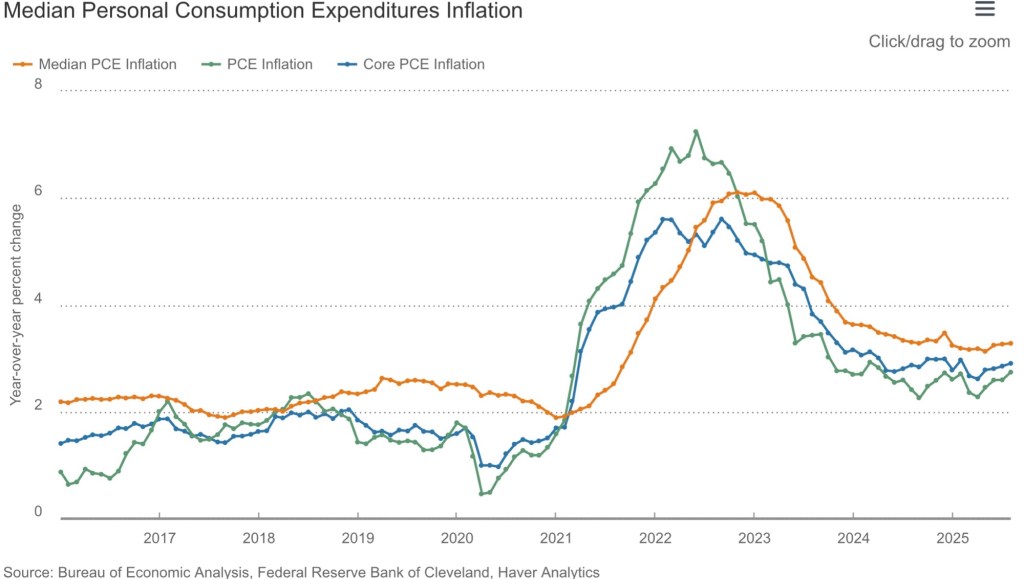

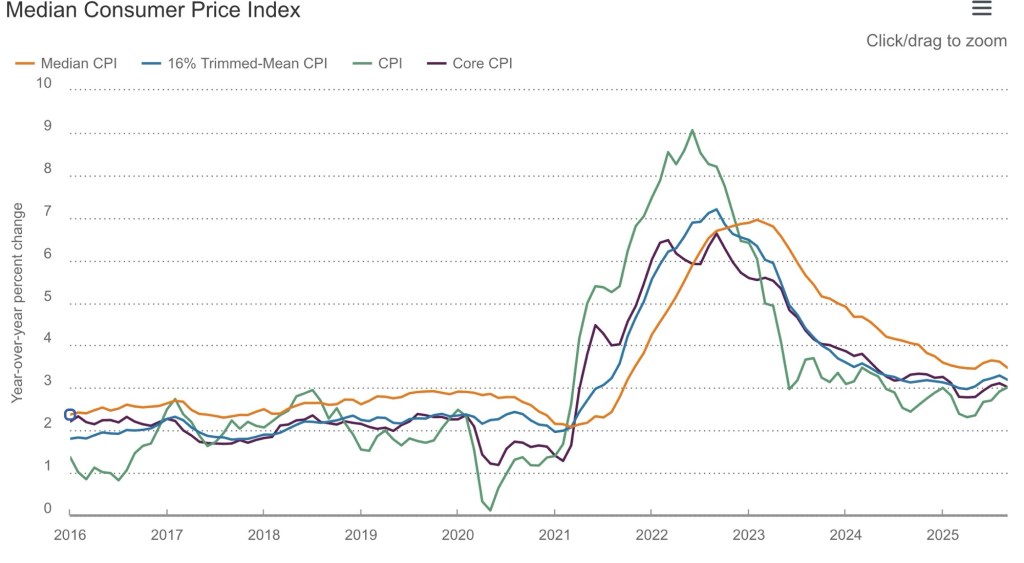

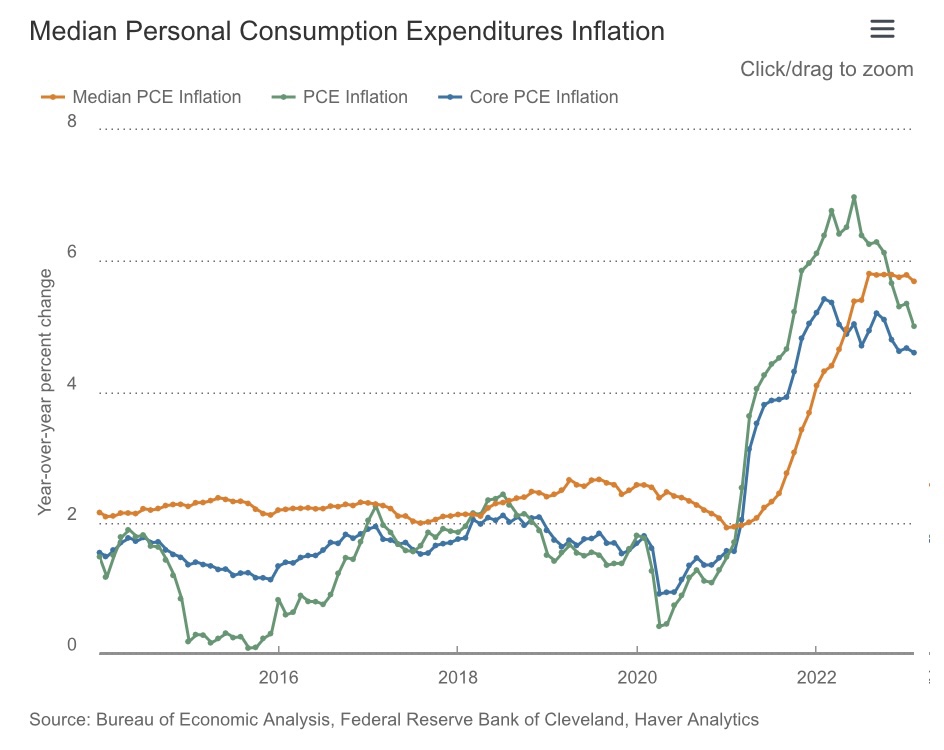

Inflation leveled off below 3% in 2024 and has drifted around the 3% level in 2025. The rate of increase in the core PCE (Personal Consumption Deflator) is the inflation measure of most interest to the Federal Reserve as a policy reference, but advances in the core CPI (Consumer Price Index) have settled at about the same level. The core inflation rates exclude food and energy prices due to the volatility of those components, but even with food and energy, inflation in the PCE and the CPI have been running near 3%.

It’s a 2% Target… Or Is It?

The Fed continues to maintain that its “official” inflation target is 2% for the core PCE. However, the central bank is now easing policy despite inflation running a full percentage point faster than the target. The rationale turns on the Fed’s dual mandate to maintain both “price stability” and full employment, goals that are not always compatible.

Currently, the labor market is showing signs of weakness, so the Fed has elected to ease policy by guiding the federal funds rate downward, and by putting a stop to run-off in its balance sheet holdings of securities. The latter ends a brief period of so-called quantitative tightening.

Just a couple of months ago, the central bank announced a new emphasis on targeting 2% inflation in the long run, with notable differences from the “flexible average inflation targeting” (FAIT) that it claimed to have adopted in 2020. In some respects, the Fed appeared to be giving more primacy to the “2%” definition of price stability than to the full employment mandate. Yet the “new approach” still allows plenty of wiggle room and might not differ much from the approach followed prior to FAIT.

“… an asymmetric approach to the dual mandate: It would implement makeup policy on misses below the inflation target, and it would respond to shortfalls from maximum employment. These asymmetries, while well- intended, created an inflationary bias that caused FAIT to fail the ‘stress test’ of the 2021–22 inflation surge. This failure caused the Fed to effectively abandon FAIT in early 2022 and become a single-mandate central bank focused on price stability.“

Scott Sumner says the Fed never really really practiced FAIT to begin with. It should have been a symmetric policy, but it wasn’t. During 2021-22, the Fed did not attempt to correct for rising inflation. Instead, it focused on the recessionary effects of Covid and the impingements of Covid-era restrictions on employment.

Clearly, Covid was a shock that monetary policy was ill-suited to address without reinforcing inflation. Furthermore, the pandemic inflation was thought by the Fed to be transitory, but easing policy was a critical error. Stimulating demand via monetary accommodation gave inflation more permanence than the Fed apparently expected.

Lost In the Tea Leaves Again

While a strong commitment to price stability is welcome, it’s not clear that is what’s guiding the Fed’s decisions at the moment. Again, the Fed’s preferred inflation gauge has flattened out at around 3%. However, with uncertainty about tariffs and tariff pass throughs in 2026, the weak dollar, and unrelenting Treasury borrowing, easier monetary conditions could well set the stage for persistent inflation above 3%, despite the official 2% target. That might help explain the failure of longer-term interest rates to decline in the wake of the Fed’s latest quarter-point cut in the federal funds target in October.

Suspicious Minds

Speculation that the Fed is allowing its true inflation target to creep upward is hardly new. Back in June, former New York Fed economist Robert Brusca noted the following:

“A Cleveland Fed survey already has the business community thinking that the REAL target for inflation is 2.5%.”

More recently, Mark Sobel of the Official Monetary and Fiscal Institutions Forum stated that the real target, for now, is probably 3%:

“But could the Fed stealthily and unintentionally end up near 3%? Even apart from above-target inflation in recent years, short- and longer-term structural forces are at play that could usher in slightly higher inflation, notwithstanding Fed speeches on the sanctity of the 2% inflation target.“

Chewing On Data

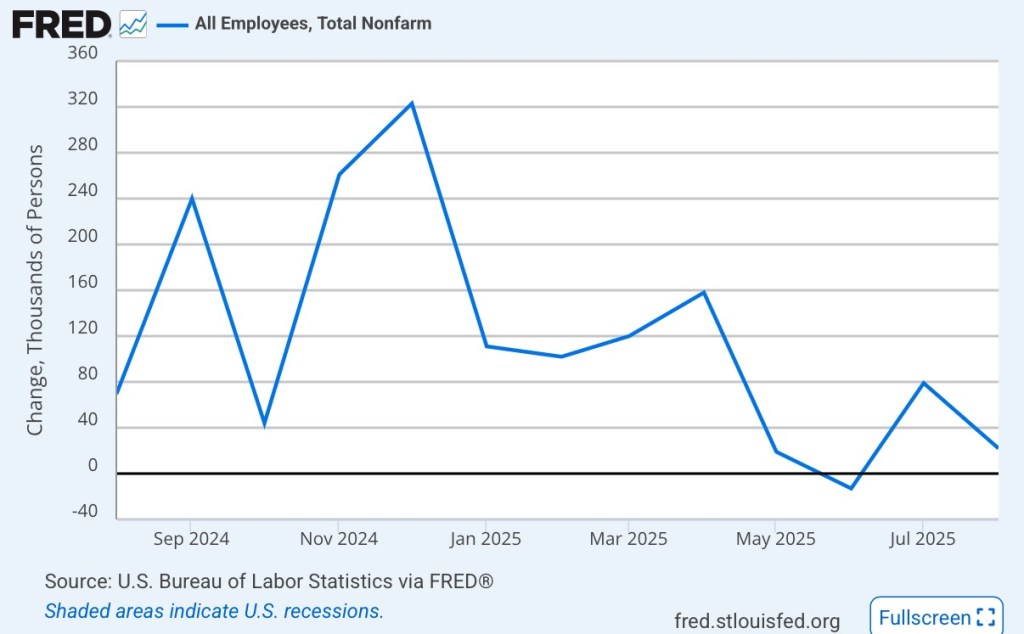

It’s pretty clear that the Fed has become a skittish about the pace of the real economy, lending more weight to the full employment part of its dual mandate. Employment growth slowed over the past year, partly due to government employee buy-outs and separations of illegal immigrants from their employers. The last official employment report was in early September, however, so the nonfarm payroll data is two months out-of-date:

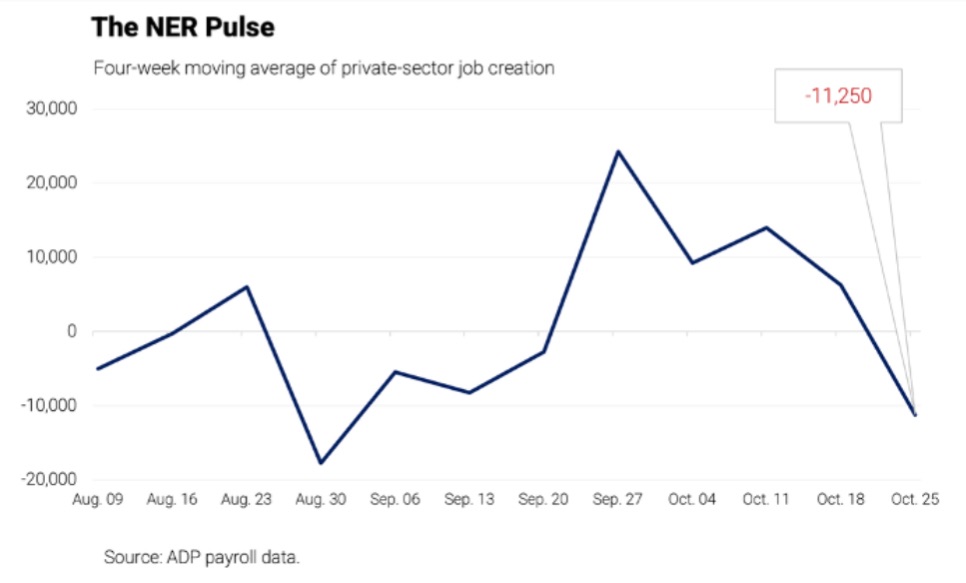

Private payroll growth from ADP over the past two months has not looked especially encouraging:

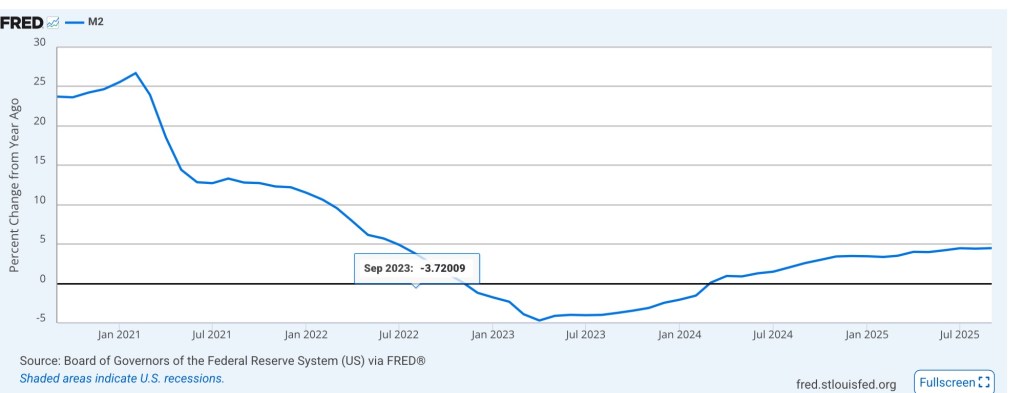

Tariffs and weakened profit margins have likely had a contractionary effect, and the six-week government shutdown just ended will shave 0.5% or more off fourth quarter GDP growth. Furthermore, while money (M2) growth has accelerated over the past year, it remains fairly restrained.

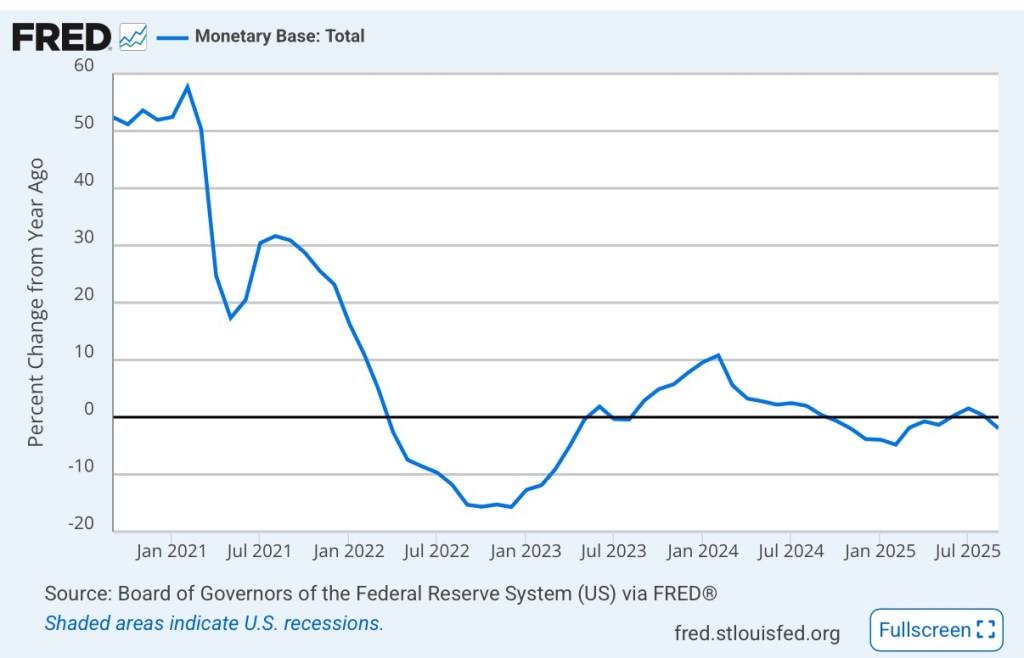

And the monetary base has been pretty flat for most of 2025:

We’ll see where these aggregates go from here. The extended “restraint” might now be of some concern to the Fed, given recent doubts about employment and economic growth. Still, in October, Fed Chairman Jerome Powell said that another quarter-point cut in the federal funds rate target in December was not a foregone conclusion. That statement seems to have worried equity investors while offering little solace to bond investors.

Aborted Landing

If (and as long as) the Fed gives primacy or greater weight in its policy deliberations to employment than inflation, it might as well have adopted an inflation target of 3% or more. The additional erosion in purchasing power wrought by that leniency is bad enough, but the effect of monetary policy on the real side of the economy is more poorly understood than its effect on nominal variables. The Fed’s shift in priorities is both unreliable on the real side and dangerous in terms of price stability. These concerns are even more salient given the upcoming appointment (in May) of a new Fed Chairman by President Trump, who seems eager for easy money.

Policy activists have long maintained that manipulating government policy can stabilize the economy. In other words, big spending initiatives, tax cuts, and money growth can lift the economy out of recessions, or budget cuts and monetary contraction can prevent overheating and inflation. However, this activist mirage burned away under the light of experience. It’s not that fiscal and monetary policy are powerless. It’s a matter of practical limitations that often cause these tools to be either impotent or destabilizing to the economy, rather than smoothing fluctuations in the business cycle.

The macroeconomics classes seem like yesterday: Keynesian professors lauded the promise of wise government stabilization efforts: policymakers could, at least in principle, counter economic shocks, particularly on the demand side. That optimistic narrative didn’t end after my grad school days. I endured many client meetings sponsored by macro forecasters touting the fine-tuning of fiscal and monetary policy actions. Some of those economists were working with (and collecting revenue from) government policymakers, who are always eager to validate their pretensions as planners (and saviors). However, seldom if ever do forecasters conduct ex post reviews of their model-spun policy scenarios. In fairness, that might be hard to do because all sorts of things change from initial conditions, but it definitely would not be in their interests to emphasize the record.

In this post I attempt to explain why you should be skeptical of government stabilization efforts. It’s sort of a lengthy post, so I’ve listed section headings below in case readers wish to scroll to points of most interest. Pick and choose, if necessary, though some context might get lost in the process.

Expectations Change the World

Fiscal Extravagance

Multipliers In the Real World

Delays

Crowding Out

Other Peoples’ Money

Tax Policy

Monetary Policy

Boom and Bust

Inflation Targeting

Via Rate Targeting

Policy Coordination

Who Calls the Tune?

Stable Policy, Stable Economy

Expectations Change the World

There were always some realists in the economics community. In May we saw the passing of one such individual: Robert Lucas was a giant intellect within the economics community, and one from whom I had the pleasure of taking a class as a graduate student. He was awarded the Nobel Prize in Economic Science in 1995 for his applications of rational expectations theory and completely transforming macro research. As Tyler Cowen notes, Keynesians were often hostile to Lucas’ ideas. I remember a smug classmate, in class, telling the esteemed Lucas that an important assumption was “fatuous”. Lucas fired back, “You bastard!”, but proceeded to explain the underlying logic. Cowen uses the word “charming” to describe the way Lucas disarmed his critics, but he could react strongly to rude ignorance.

Lucas gained professional fame in the 1970s for identifying a significant vulnerability of activist macro policy. David Henderson explains the famous “Lucas Critique” in the Wall Street Journal:

“… because these models were from periods when people had one set of expectations, the models would be useless for later periods when expectations had changed. While this might sound disheartening for policy makers, there was a silver lining. It meant, as Lucas’s colleague Thomas Sargent pointed out, that if a government could credibly commit to cutting inflation, it could do so without a large increase in unemployment. Why? Because people would quickly adjust their expectations to match the promised lower inflation rate. To be sure, the key is government credibility, often in short supply.”

Non-credibility is a major pitfall of activist macro stabilization policies that renders them unreliable and frequently counterproductive. And there are a number of elements that go toward establishing non-credibility. We’ll distinguish here between fiscal and monetary policy, focusing on the fiscal side in the next several sections.

Fiscal Extravagance

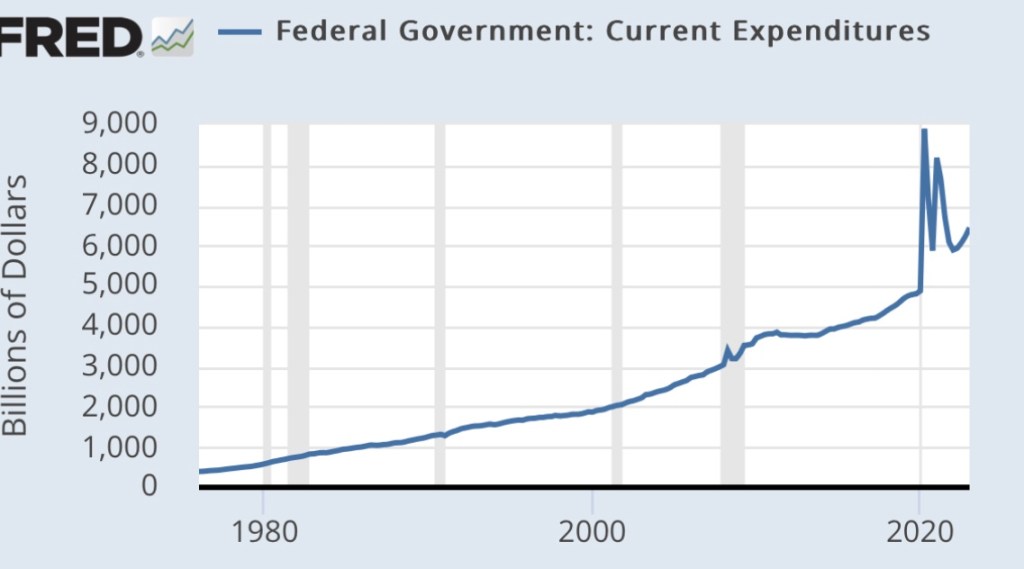

We’ve seen federal spending and budget deficits balloon in recent years. Chronic and growing budget deficits make it difficult to deliver meaningful stimulus, both practically and politically.

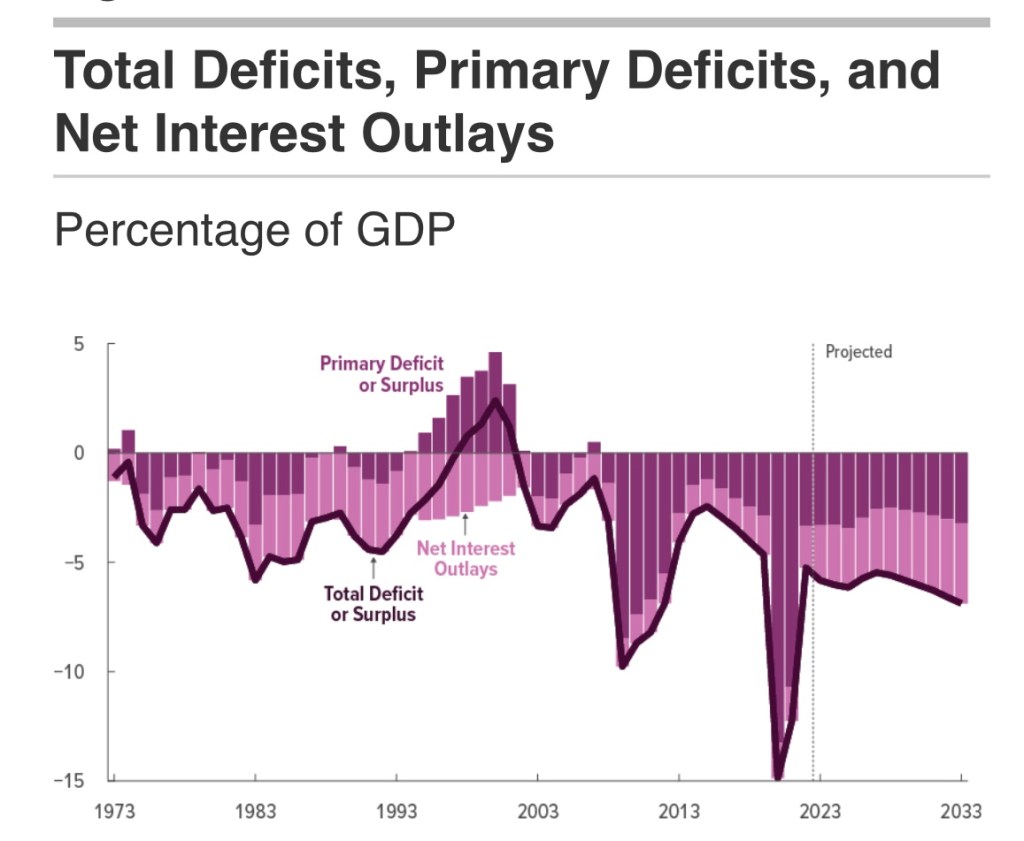

The next chart is from the most recent Congressional Budget Office (CBO) report. It shows the growing contribution of interest payments to deficit spending. Ever-larger deficits mean ever-larger amounts of debt on which interest is owed, putting an ever-greater squeeze on government finances going forward. This is particularly onerous when interest rates rise, as they have over the past few years. Both new debt is issued and existing debt is rolled over at higher cost.

Relief payments made a large contribution to the deficits during the pandemic, but more recent legislation (like the deceitfully-named Inflation Reduction Act) piled-on billions of new subsidies for private investments of questionable value, not to mention outright handouts. These expenditures had nothing to do with economic stabilization and no prayer of reducing inflation. Pissing away money and resources only hastens the debt and interest-cost squeeze that is ultimately unsustainable without massive inflation.

Hardly anyone with future political ambitions wants to address the growing entitlements deficit … but it will catch up with them. Social Security and Medicare are projected to exhaust their respective trust funds in the early- to mid-2030s, which will lead to mandatory benefit cuts in the absence of reform.

If it still isn’t obvious, the real problem driving the budget imbalance is spending, not revenue, as the next CBO chart demonstrates. The “emergency” pandemic measures helped precipitate our current stabilization dilemma. David Beckworth tweets that the relief measures “spurred a rapid recovery”, though I’d hasten to add that a wave of private and public rejection of extreme precautions in some regions helped as well. And after all, the pandemic downturn was exaggerated by misdirected policies including closures and lockdowns that constrained both the demand and supply sides. Beckworth acknowledges the relief measures “propelled inflation”, but the pandemic also seemed to leave us on a permanently higher spending path. Again, see the first chart below.

The second chart below shows that non-discretionary spending (largely entitlements) and interest outlays are how we got on that path. The only avenue for countercyclical spending is discretionary expenditures, which constitute an ever-smaller share of the overall budget.

We’ve had chronic deficits for years, but we’ve shifted to a much larger and continuing imbalance. With more deficits come higher interest costs, especially when interest rates follow a typical upward cyclical pattern. This creates a potentially explosive situation that is best avoided via fiscal restraint.

Putting other doubts about fiscal efficacy aside, it’s all but impossible to stimulate real economic activity when you’ve already tapped yourself out and overshot in the midst of a post-pandemic economic expansion.

Multipliers In the Real World

So-called spending multipliers are deeply beloved by Keynesians and pork-barrel spenders. These multipliers tell us that every dollar of extra spending ultimately raises income by some multiple of that dollar. This assumes that a portion of every dollar spent by government is re-spent by the recipient, and a portion of that is re-spent again by another recipient. But spending multipliers are never what they’re cracked up to be for a variety of reasons. (I covered these in“Multipliers Are For Politicians”, and also see this post.) There are leakages out of the re-spending process (income taxes, saving, imports), which trim the ultimate impact of new spending on income. When supply constraints bind on economic activity, fiscal stimulus will be of limited power in real terms.

If stimulus is truly expected to be counter-cyclical and transitory, as is generally claimed, then much of each dollar of extra government spending will be saved rather than spent. This is the lesson of the permanent income hypothesis. It means greater leakages from the re-spending stream and a lower multiplier. We saw this with the bulge in personal savings in the aftermath of pandemic relief payments.

Another side of this coin, however, is that cutting checks might be the government’s single-most efficient activity in execution, but it can create massive incentive problems. Some recipients are happy to forego labor market participation as long as the government keeps sending them checks, but at least they spend some of the income.

Delays

Another unappreciated and destabilizing downside of fiscal stimulus is that it often comes too late, just when the economy doesn’t need stimulus. That’s because a variety of delays are inherent in many spending initiatives: legislative, regulatory, legal challenges, planning and design, distribution to various spending authorities, and final disbursement. As I noted here:

“Even government infrastructure projects, heralded as great enhancers of American productivity, are often subject to lengthy delays and cost overruns due to regulatory and environmental rules. Is there any such thing as a federal ‘shovel-ready’ infrastructure project?”

Crowding Out

The supply of savings is limited, but when government borrows to fund deficits, it directly competes with private industry for those savings. Thus, funds that might otherwise pay for new plant, equipment, and even R&D are diverted to uses that should qualify as government consumption rather than long-term investment. Government competition for funds “crowds-out” private activity and impedes growth in the economy’s productive capacity. Thus, the effort to stimulate economic activity is self-defeating in some respects.

Other Peoples’ Money

Government doesn’t respond to price signals the way self-interested private actors do. This indifference leads to mis-allocated resources and waste. It extends to the creation of opportunities for graft and corruption, typically involving diversion of resources into uses that are of questionable productivity (corn ethanol, solar and wind subsidies).

Consider one other type of policy action perceived as counter-cyclical: federal bailouts of failing financial institutions or other troubled businesses. These rescues prop up unproductive enterprises rather than allowing waste to be flushed from the system, which should be viewed as a beneficial aspect of recession. The upshot is that too many efforts at economic stabilization are misdirected, wasteful, ill-timed, and pro-cyclical in impact.

Tax Policy

Like stabilization efforts on the spending side, tax changes may be badly timed. Tax legislation is often complex and can take time for consumers and businesses to adjust. In terms of traditional multiplier analysis, the initial impact of a tax change on spending is smaller than for expenditures, so tax multipliers are smaller. And to the extent that a tax change is perceived as temporary, it is made less effective. Thus, while changes in tax policy can have powerful real effects, they suffer from some of the same practical shortcomings for stabilization as changes in spending.

However, stimulative tax cuts, if well crafted, can boost disposable incomes and improve investment and work incentives. As temporary measures, that might mean an acceleration of certain kinds of activity. Tax increases reduce disposable incomes and may blunt incentives, or prompt delays in planned activities. Thus, tax policy may bear on the demand side as well as the timing of shifts in the economy’s productive potential or supply side.

Monetary Policy

Monetary policy is subject to problems of its own. Again, I refer to practical issues that are seemingly impossible for policy activists to overcome. Monetary policy is conducted by the nation’s central bank, the Federal Reserve (aka, the Fed). It is theoretically independent of the federal government, but the Fed operates under a dual mandate established by Congress to maintain price stability and full employment. Therein lies a basic problem: trying to achieve two goals that are often in conflict with a single policy tool.

Make no mistake: variations in money supply growth can have powerful effects. Nevertheless, they are difficult to calibrate due to “long and variable lags” as well as changes in money “velocity” (or turnover) often prompted by interest rate movements. Excessively loose money can lead to economic excesses and an overshooting of capacity constraints, malinvestment, and inflation. Swinging to a tight policy stance in order to correct excesses often leads to “hard landings”, or recession.

Boom and Bust

The Fed fumbled its way into engineering the Great Depression via excessively tight monetary policy. “Stop and go” policies in the 1970s led to recurring economic instability. Loose policy contributed to the housing bubble in the 2000s, and subsequent maladjustments led to a mortgage crisis (also see here). Don’t look now, but the inflationary consequences of the Fed’s profligacy during the pandemic prompted it to raise short-term interest rates in the spring of 2022. It then acted with unprecedented speed in raising rates over the past year. While raising rates is not always synonymous with tightening monetary conditions, money growth has slowed sharply. These changes might well lead to recession. Thus, the Fed seems given to a pathology of policy shifts that lead to unintentional booms and busts.

Inflation Targeting

The Fed claims to follow a so-called flexible inflation targeting policy. In reality, it has reacted asymmetrically to departures from its inflation targets. It took way too long for the Fed to react to the post-pandemic surge in inflation, dithering for months over whether the surge was “transitory”. It wasn’t, but the Fed was reluctant to raise its target rates in response to supply disruptions. At the same time, the Fed’s own policy actions contributed massively to demand-side price pressures. Also neglected is the reality that higher inflation expectations propel inflation on the demand side, even when it originates on the supply side.

Via Rate Targeting

At a more nuts and bolts level, today the Fed’s operating approach is to control money growth by setting target levels for several key short-term interest rates (eschewing a more direct approach to the problem). This relies on price controls (short-term interest rates being the price of liquidity) rather than allowing market participants to determine the rates at which available liquidity is allocated. Thus, in the short run, the Fed puts itself into the position of supplying whatever liquidity is demanded at the rates it targets. The Fed makes periodic adjustments to these rate targets in an effort to loosen or tighten money, but it can be misdirected in a world of high debt ratios in which rates themselves drive the growth of government borrowing. For example, if higher rates are intended to reduce money growth and inflation, but also force greater debt issuance by the Treasury, the approach might backfire.

Policy Coordination

While nominally independent, the Fed knows that a particular monetary policy stance is more likely to achieve its objectives if fiscal policy is not working at cross purposes. For example, tight monetary policy is more likely to succeed in slowing inflation if the federal government avoids adding to budget deficits. Bond investors know that explosive increases in federal debt are unlikely to be repaid out of future surpluses, so some other mechanism must come into play to achieve real long-term balance in the valuation of debt with debt payments. Only inflation can bring the real value of outstanding Treasury debt into line. Continuing to pile on new debt simply makes the Fed’s mandate for price stability harder to achieve.

Who Calls the Tune?

The Fed has often succumbed to pressure to monetize federal deficits in order to keep interest rates from rising. This obviously undermines perceptions of Fed independence. A willingness to purchase large amounts of Treasury bills and bonds from the public while fiscal deficits run rampant gives every appearance that the Fed simply serves as the Treasury’s printing press, monetizing government deficits. A central bank that is a slave to the spending proclivities of politicians cannot make credible inflation commitments, and cannot effectively conduct counter-cyclical policy.

Stable Policy, Stable Economy

Activist policies for economic stabilization are often perversely destabilizing for a variety of reasons. Good timing requires good forecasts, but economic forecasting is notoriously difficult. The magnitude and timing of fiscal initiatives are usually wrong, and this is compounded by wasteful planning, allocative dysfunction, and a general absence of restraint among political leaders as well as the federal bureaucracy..

Predicting the effects of monetary policy is equally difficult and, more often than not, leads to episodes of over- and under-adjustment. In addition, the wrong targets, the wrong operating approach, and occasional displays of subservience to fiscal pressure undermine successful stabilization. All of these issues lead to doubts about the credibility of policy commitments. Stated intentions are looked upon with doubt, increasing uncertainty and setting in motion behaviors that lead to undesirable economic consequences.

The best policies are those that can be relied upon by private actors, both as a matter of fulfilling expectations and avoiding destabilization. Federal budget policy should promote stability, but that’s not achievable institutions unable to constrain growth in spending and deficits. Budget balance would promote stability and should be the norm over business cycles, or perhaps over periods as long as typical 10-year budget horizons. Stimulus and restraint on the fiscal side should be limited to the effects of so-called automatic stabilizers, such as tax rates and unemployment compensation. On the monetary side, the Fed would do more to stabilize the economy by adopting formal rules, whether a constant rate of money growth or symmetric targeting of nominal GDP.

To the great chagrin of some market watchers, the Federal Reserve Open Market Committee (FOMC) increased its target for the federal funds rate in March by 0.25 points, to range of 4.75 – 5%. This was pretty much in line with plans the FOMC made plain in the fall. The “surprise” was that this increase took place against a backdrop of liquidity shortfalls in the banking system, which also had taken many by surprise. Perhaps a further surprise was that after a few days of reflection, the market didn’t seem to mind the rate hike all that much.

Switchman Sleeping

There’s plenty of blame to go around for bank liquidity problems. Certain banks and their regulators (including the Fed) somehow failed to anticipate that carrying large, unhedged positions in low-rate, long-term bonds might at some point alarm large depositors as interest rates rose. Those banks found themselves way short of funds needed to satisfy justifiably skittish account holders. A couple of banks were closed, but the FDIC agreed to insure all of their depositors. As the lender of last resort, the Fed provided banks with “credit facilities” to ease the liquidity crunch. In a matter of days, the fresh credit expanded the Fed’s balance sheet, offsetting months of “quantitative tightening” that had taken place since last June.

Of course, the Fed is no stranger to dozing at the switch. Historically, the central bank has failed to anticipate changes wrought by its own policy actions. Today’s inflation is a prime example. That kind of difficulty is to be expected given the “long and variable lags” in the effects of monetary policy on the economy. It makes activist policy all the more hazardous, leading to the kinds of “boom and bust” cycles described in Austrian business cycle theory.

Persistent Inflation

When the Fed went forward with the 25 basis point hike in the funds rate target in March, it was greeted with dismay by those still hopeful for a “soft landing”. In the Fed’s defense, one could say the continued effort to tighten policy is an attempt to make up for past sins, namely the Fed’s monetary profligacy during the pandemic.

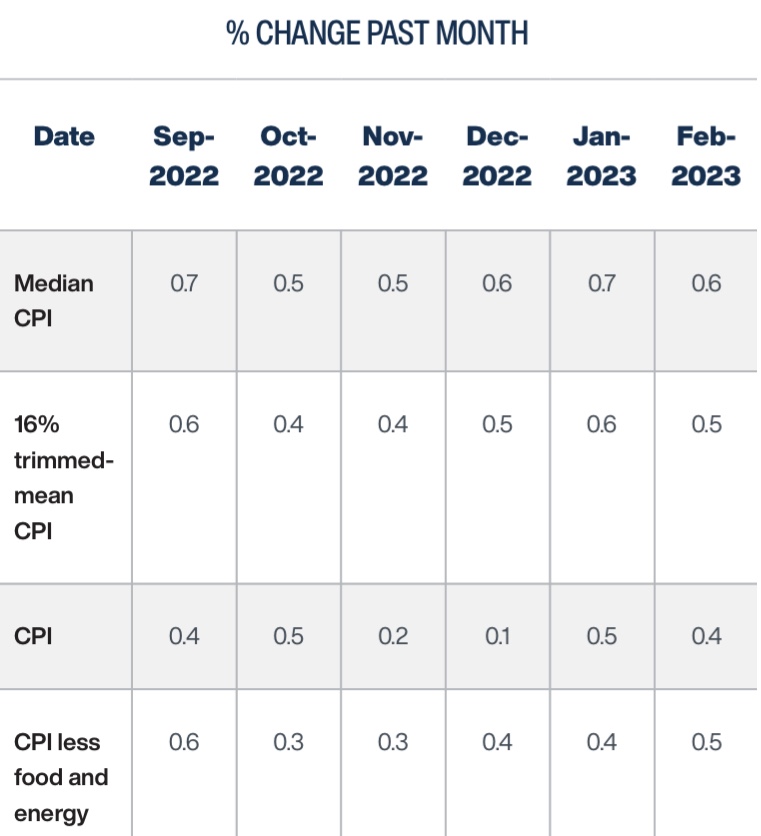

The Fed’s rationale for this latest rate hike was that inflation remains persistent. Here are four CPI measures from the Cleveland Fed, which show some recent tapering of price pressures. Perhaps “flattening” would be a better description, at least for the median CPI:

Those are 12-month changes, and just in case you’ve heard that month-to-month changes have tapered more sharply, that really wasn’t the case in January and February:

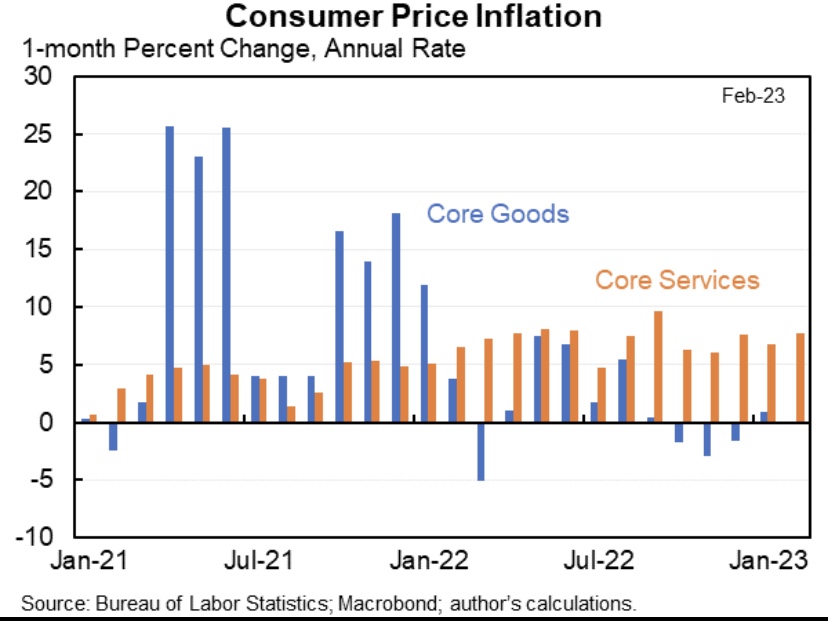

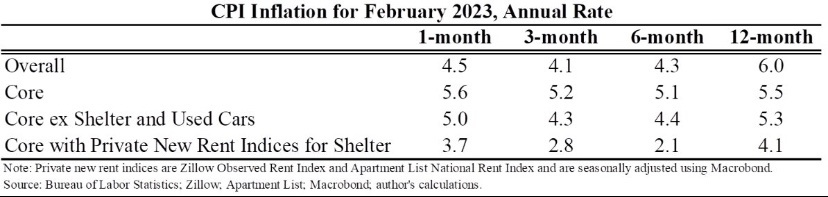

Jason Furman notedin a series of tweets that the prices of services are driving recent inflation, while goods prices have been flat:

A compelling argument is that the shelter component of the CPI is overstating services inflation, and it’s weighted at more than one-third of the overall index. CPI shelter costs are known as “owner’s equivalent rent” (OER), which is based on a survey question of homeowners as to the rents they think they could command, and it is subject to a fairly long lag. Actual rent inflation has slowed sharply since last summer, so the shelter component is likely to relieve pressure on CPI inflation (and the Fed) in coming months. Nevertheless, Furman points out that CPI inflation over the past 3 -4 months was up even when housing is excluded. Substituting a private “new rent” measure of housing costs for OER would bring measured inflation in services closer the Fed’s comfort zone, however.

The Fed’s preferred measure of inflation, the deflator for personal consumption expenditures (PCE), uses a much lower weight on housing costs, though it might also overstate inflation within that component. Here’s another chart from the Cleveland Fed:

Inflation in the Core PCE deflator, which excludes food and energy prices, looks as if it’s “flattened” as well. This persistence is worrisome because inflation is difficult to stop once it becomes embedded in expectations. That’s exactly what the Fed says it’s trying to prevent.

Rate Targets and Money Growth

Targeting the federal funds rate (FFR) is the Fed’s primary operational method of conducting monetary policy. The FFR is the rate at which banks borrow from one another overnight to meet short-term needs for reserves. In order to achieve price stability, the Fed would do better to focus directly on controlling the money supply. Nevertheless, it has successfully engineered a decline in the money supply beginning last April, and recently the money supply posted year-over-year negative growth.

That doesn’t mean money growth has been “optimized” in any sense, but a slowdown in money growth was way overdue after the pandemic money creation binge. You might not like the way the Fed executed the reversal or its operating policy in general, and neither do I, but it did restrain money growth. In that sense, I applaud the Fed for exercising its independence, standing up to the Treasury rather than continuing to monetize yawning federal deficits. That’s encouraging, but at some point the Fed will reverse course and ease policy. We’ll probably hope in vain that the Fed can avoid sending us once again along the path of boom and bust cycles.

In effect, the FFR target is a price control with a dynamic element: the master fiddles with the target whenever economic conditions are deemed to suggest a change. This “controlled” rate has a strong influence on other short-term interest rates. The farther out one goes on the maturity spectrum, however, the weaker is the association between changes in the funds rate and other interest rates. The Fed doesn’t truly “control” those rates of most importance to consumers, corporate borrowers, government borrowers, and investors. It definitely influences those rates, but credit risk, business opportunities, and long-term expectations are often dominant.

The FOMC’s latest rate increase suggests its members don’t expect an immediate downturn in economic activity or a definitive near-term drop in inflation. The Committee may, however, be willing to pause for a period of several meeting cycles (every six weeks) to see whether the “long and variable lags” in the transmission of tighter monetary policy might begin to kick-in. As always, the FOMC’s next step will be “data dependent”, as Chairman Powell likes to say. In the meantime, the economic response to earlier tightening moves is likely to strengthen. Lenders are responding to the earlier rate hikes and reduced lending margins by curtailing credit and attempting to rebuild their own liquidity.

Is It Supply Or Demand?

There’s an ongoing debate about whether monetary policy is appropriate for fighting this episode of inflation. It’s true that monetary policy is ill-suited to addressing supply disruptions, though it can help to stem expectations that might cause supply-side price pressures to feed upon themselves (and prevent them from becoming demand-side pressures). However, profligate fiscal and monetary policy did much to create the current inflation, which is pressure on the demand-side. On that point, David Beckworth leaves little doubt as to where he stands:

“The real world is nominal. And nominal PCE was about $1.6 trillion above trend thru February. Unless one believes in immaculate above-trend spending, this huge surge could 𝙣𝙤𝙩 have happened without support from fiscal and monetary policy.”

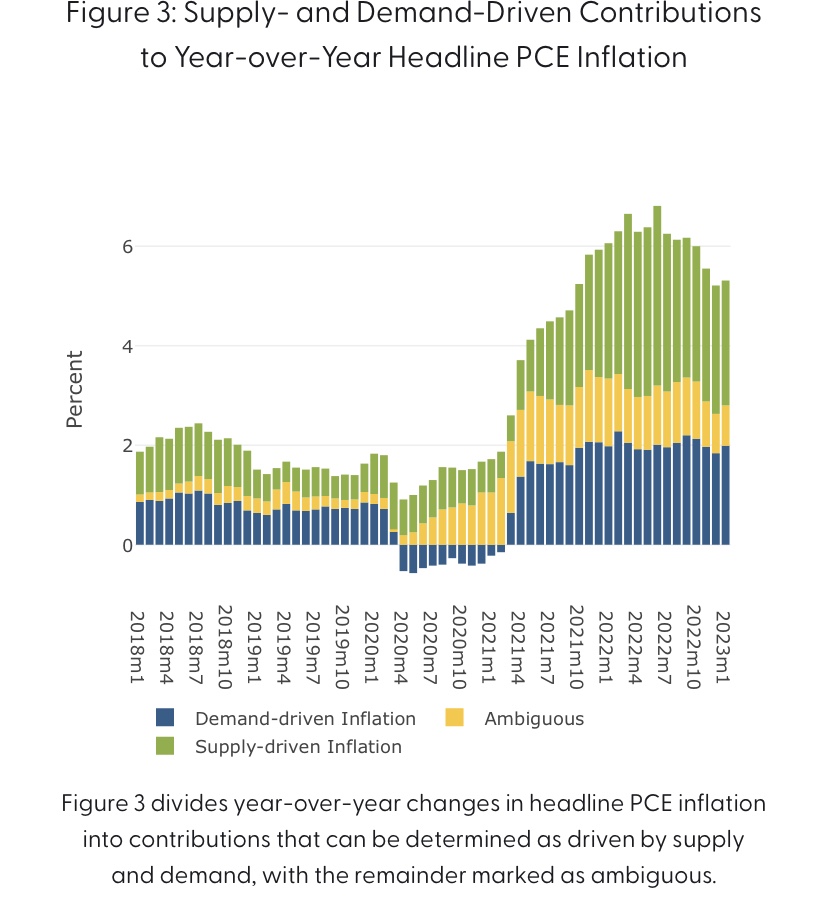

In reality, this inflationary episode was borne of a mix of demand and supply-side pressures, and policy either caused or accommodated all of it. Nevertheless, it’s interesting to consider efforts to decompose these forces. This NBER paper attributed about 2/3 of inflation from December 2019 – June 2022 to the demand-side. Given the ongoing tenor of fiscal policy and the typical policy lags, it’s likely that the effects of fiscal and monetary stimulus have persisted well beyond that point. Here is a page from the San Francisco Fed’s site that gives an edge to supply-side factors, as reflected in this breakdown of the Fed’s favorite inflation gauge:

Of course, all of these decompositions are based on assumptions and are, at best, model-based. Nevertheless, to the extent that we still face supply constraints, they would impose limits to the Fed’s ability to manage inflation downward without a “hard landing”.

There’s also no doubt that supply side policies would reduce the kinds of price pressures we’re now experiencing. Regulation and restrictive energy policies under the Biden Administration have eroded productive capacity. These policies could be reversed if political leaders were serious about improving the nation’s economic health.

The Dark Runway Ahead

Will we have a recession? And when? There are no definite signs of an approaching downturn in the real economy just yet. Inventories of goods did account for more than half of the fourth quarter gain in GDP, which may now be discouraging production. There are layoffs in some critical industries such as tech, but we’ll have to see whether there is new evidence of overall weakness in next Friday’s employment report. Real wages have been a little down to flat over the past year, while consumer debt is climbing and real retail sales have trended slightly downward since last spring. Many firms will experience higher debt servicing costs going forward. So it’s not clear that the onset of recession is close at hand, but the odds are good that we’ll see a downturn as the year wears on, especially with credit increasingly scarce in the wake of the liquidity pinch at banks. But no one knows for sure, including the Fed.

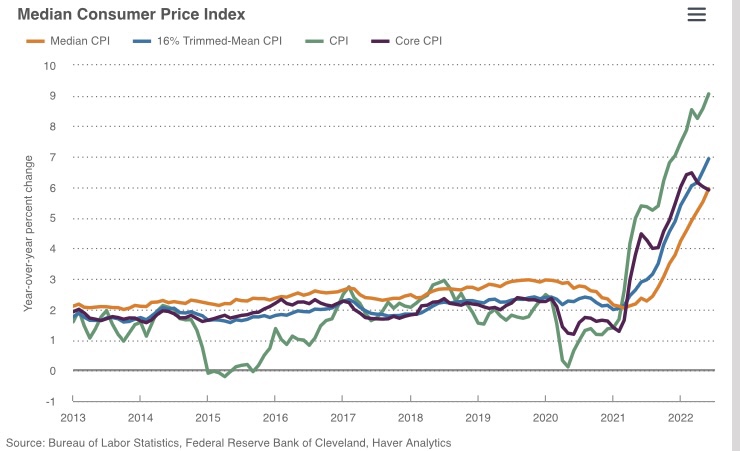

Inflation accelerated at the consumer level in June and the advances continued to broaden. That’s confirmed by the median item in the Consumer Price Index (CPI) and a measure of the CPI that “trims” out items with the largest and smallest price hikes (see chart above from the Cleveland Fed). Wholesale inflation also picked up in June. At this point, there’s a very real danger that increasing expectations of future inflation are getting embedded into current pricing decisions. Once that happens, the cycle is very hard to break. And wage rates are not keeping pace, so inflation is reducing real incomes for many workers. The sad fact is that inflation takes its greatest toll on the well being of low income earners.

And why did inflation accelerate from 1.4% in January 2021 to 9.2% in June? Don’t ask Joe Biden, at least not if you want a straight answer. He’s been changing his tune almost every month, with a rotating cast of the characters coming in for blame. First, the story was that higher inflation was just transitory; then too, the Administration said it only hurt the rich, a wholly preposterous assertion; the blame then shifted to the oil companies; then to Putin; and then big corporations generally; more recently, it’s independent gas retailers! Nothing is said about Biden’s early pledge to shut down fossil fuels. Nothing is said about the federal government’s profligate spending and the money printing that paid for it. Nothing is said about the extended payment of unemployment benefits, which pinched labor supply. More generally, nothing is said about the extension of Biden’s pandemic emergency powers, which allows continued Medicaid and food stamp benefits to many who are otherwise ineligible. The federal spigot has been wide open!

So here’s a quick synopsis of events leading to our inflationary surge: demand strengthened as pandemic restrictions were lifted across the country. Unfortunately, businesses were not ready to meet that level of demand. Operations had been sharply curtailed during the pandemic all along business supply chains. Hiring staff was next to impossible for many firms, especially given the Biden Administration’s ineptitude with respect to labor incentives. The Administration also set out to starve the fossil fuel industry of capital and to shut down drilling and refining operations through restrictions and binding regulations. The price of oil began to soar early in the Administration, which has been working its way into the prices of other goods and services, including food and transportation. Reinforcing these ill effects was the broader regulatory onslaught instigated at many agencies by Biden, actions which tend to increase costs while limiting competition in many industries.

Most of the factors just listed were limitations on supply. However, the price pressure was accelerated on the demand side by government stimulus payments. And in fact, none of this inflation would be sustainable without easy monetary policy — and monetization of government debt.

Later, of course, Vladimir Putin’s invasion of Ukraine exacerbated worldwide energy and food shortages. Meanwhile, Democrat efforts to push through additional social spending, née “infrastructure”, were unrelenting. They are still pushing for more climate change regulation, not to mention funding “investments” intended to improve the “equity” of highways! Thank God for Joe Manchin for shutting it down, though even he seems intent on imposing drug price controls. Biden now says he’ll impose green energy policy via executive order.

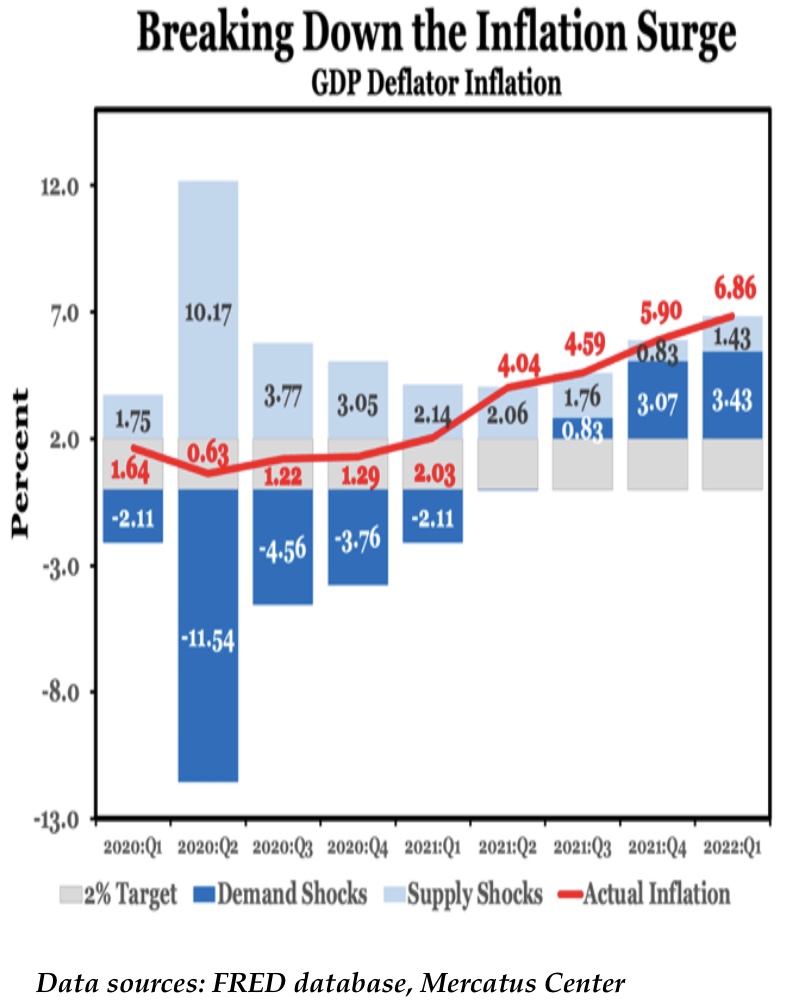

Until about March of this year, Federal Reserve policy remained extremely accommodative, despite the central bank having completely missed its so-called inflation target rate of 2% well before that. Take another look at the chart at the top of this post. CPI inflation shot above 2% in early 2021. The Fed did not really react until March 2022. The chart below shows that growth in the GDP deflator was slightly more muted than the CPI, but it too was above 2% in the first quarter of 2021 and accelerated from there. It’s as if there had been no Fed target at all!

The story, again, was “not to worry, it’s transitory”. Moreover, the Fed was convinced the inflation was driven entirely by supply problems. In fairness, it’s true that tighter monetary policy won’t stop inflation from supply shocks without great cost in terms of lost output. But monetary accommodation, which is what happened in 2021, simply validates inflation and runs the risk of allowing inflation expectations to become embedded in pricing. And again, that’s hard to undo.

Despite the dominance of supply-side inflation pressures early in 2021, it’s no wonder that a different kind of pressure has cropped up since then. The following chart from David Beckworth is helpful:

We now have primarily demand-side inflation fueled by the earlier accommodation of supply constraints and the monetization of government deficits. Sure, there remain significant supply constraints, whether induced by the actions of Russia, Biden, or lingering pandemic dysfunctions. But supply-side inflation cannot sustain without monetary accommodation. An early reading for the second-quarter GDP deflator will be available in late July, but it may well show accelerating pressures from both the demand side and the supply side.

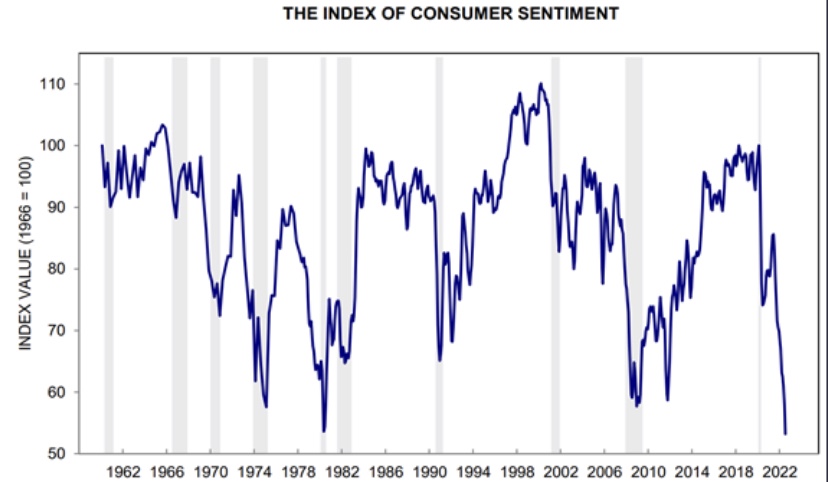

There is no way to eliminate the inflation surge without curtailing the growth of liquidity. Unfortunately, the risk that monetary tightening by the Fed will induce a recession is already very high, even a likelihood at this point. A fairly reliable signal of recession is an inversion of the yield curve, and we now see two-year Treasury debt yielding 15 – 20 basis points more than 10-year bonds. Again, real wages are declining. Real retail sales are down two months in a row and down from a year ago. Here’s a chart showing the most recent dismal reading on the index of consumer sentiment:

Whether a recession has already begun is not clear, but inflation certainly hasn’t abated, and the Fed is expected to continue tightening, albeit belatedly. Meanwhile, the Biden Administration and key Democrats don’t seem to want to make the Fed’s job any easier. They simply don’t comprehend the reality and their role in fostering the upward price trends we’re experiencing. They still cling to hopes of another big spending package that would add to deficits and the inflation tax, despite contemplating tax hikes on private employers, but so far Manchin has put the kabash on that. Still, we’re nowhere close to putting our fiscal and monetary houses in order.

In advanced civilizations the period loosely called Alexandrian is usually associated with flexible morals, perfunctory religion, populist standards and cosmopolitan tastes, feminism, exotic cults, and the rapid turnover of high and low fads---in short, a falling away (which is all that decadence means) from the strictness of traditional rules, embodied in character and inforced from within. -- Jacques Barzun