There’s a hopeful narrative making the rounds that artificial intelligence will prove to be such a boon to the economy that we need not worry about high levels of government debt. AI investment is already having a substantial economic impact. Jason Thomas of Carlyle says that AI capital expenditures on such things as data centers, hardware, and supporting infrastructure account for about a third of second quarter GDP growth (preliminarily a 3% annual rate). Furthermore, he says relevant orders are growing at an annual rate of about 40%. The capex boom may continue for a number of years before leveling off. In the meantime, we’ll begin to see whether AI is capable of boosting productivity more broadly.

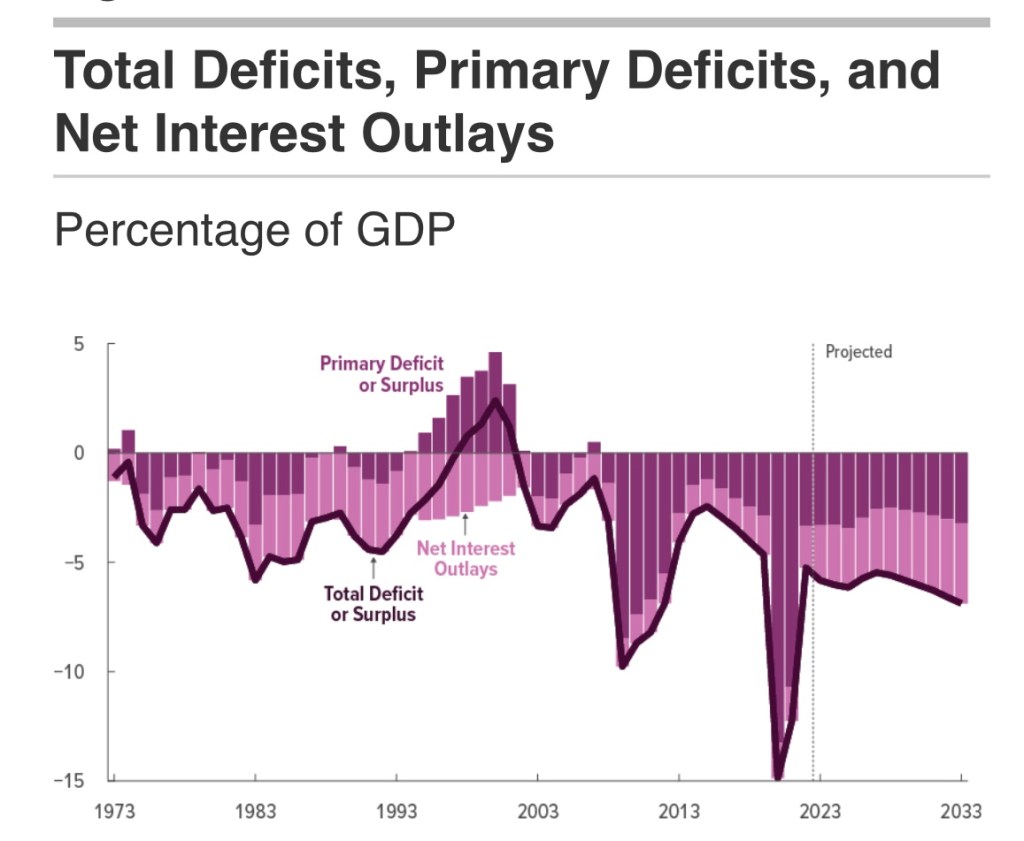

Unfortunately, even with this kind of investment stimulus, there’s no assurance that AI will create adequate economic growth and tax revenue to end federal deficits, let alone pay down the $37 trillion public debt. That thinking puts too much faith in a technology that is unproven as a long-term economic engine. It would also be a naive attitude toward managing debt that now carries an annual interest cost of almost $1 trillion, accounting for about half of the federal budget deficit.

Boom Times?

Predictions of AI’s long-term macro impact are all over the map. Goldman Sachs estimates a boost in global GDP of 7% over 10 years, which is not exactly aggressive. Daren Acemoglu has beenevenmore conservative, estimating a gain of 0.7% in total factor productivity over 10 years. Tyler Cowen has been skeptical about the impact of AI on economic growth. For an even more pessimistic take see these comments.

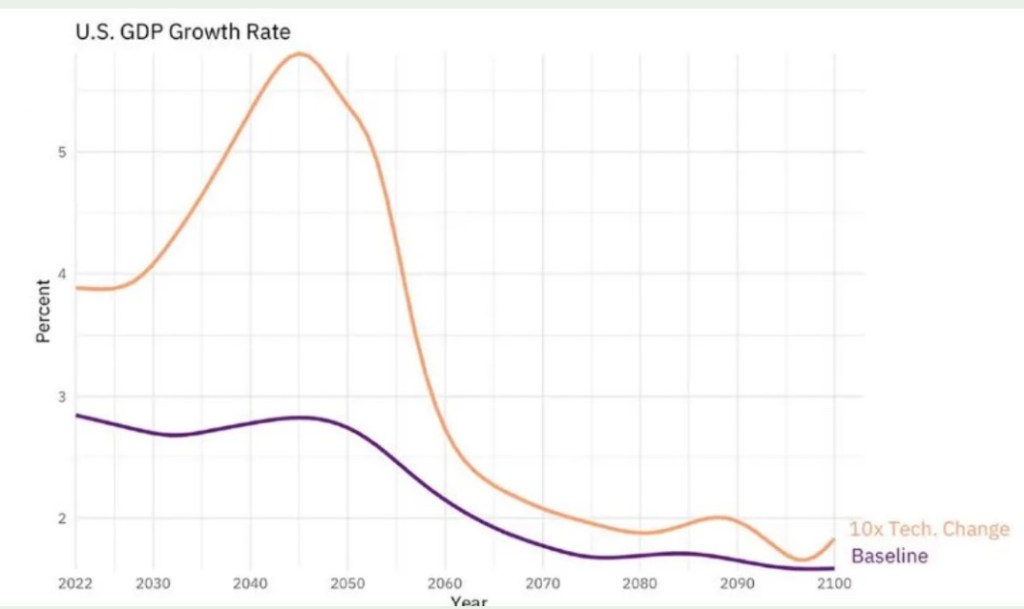

In July, however, Seth Benzell of the Stanford Digital Economy Lab discussed some simulations showing impressive AI-induced growth (see chart at top). The simulations project additional U.S. GDP growth of between 1% – 3% annually over the next 75 years! The largest boost in growth occurs now through the 2050s. This would produce a major advance in living standards. It would also eliminate the federal deficit and cure our massive entitlement insolvency, but the result comes with heavy qualifications. In fact, Benzell ultimately throws cold water on the notion that AI growth will be strong enough to reduce or even stabilize the public debt to GDP ratio.

The Scarcity Spoiler

The big hitch has to do with the scarcity of capital, which I’ve described asanimpediment to widespread AI application. Competition for capital will drive interest rates up (3% – 4%, according to Benzell’s model). Ongoing needs for federal financing intensify that effect. But it might not be so bad, according to Benzell, if climbing rates are accompanied by heightened productivity powered by AI. Then, tax receipts just might keep-up with or exceed the explosion in the government’s interest obligations.

A further complication cited by Benzell lurks in insatiable demands for public spending, and politicians who simply can’t resist the temptation to buy votes via public largesse. Indeed, as we’ve already seen, government will try to get in on the AI action, channeling taxpayer funds into projects deemed to be in the public interest. And if there are segments of the work force whose jobs are eliminated by AI, there will be pressure for public support. So even if AI succeeds in generating large gains in productivity and tax revenue, there’s very little chance we’ll see a contagion of fiscal discipline in Washington DC. This will put more upward pressure on interest rates, giving rise to the typical crowding out phenomenon, curtailing private investment in AI.

Playing Catch-Up

The capex boom must precede much of the hoped-for growth in productivity from AI. Financing comes first, which means that rates are likely to rise sooner than productivity gains can be expected. And again, competition from government borrowing will crowd out some private AI investment, slowing potential AI-induced increases in tax revenue.

There’s no chance of the converse: that AI investment will crowd out government borrowing! That kind of responsiveness is not what we typically see from politicians. It’s more likely that ballooning interest costs and deficits generally will provoke even more undesirable policy moves, such as money printing or rate ceilings.

The upshot is that higher interest rates will cause deficits to balloon before tax receipts can catch up. And as for tax receipts, the intangibility of AI will create opportunities for tax flight to more favorable jurisdictions, a point well understood by Benzell. As attorneys Bradford S. Cohen and Megan Jones put it:

“Digital assets can be harder to find and more easily shifted offshore, limiting the tax reach of the U.S. government.”

AI Growth Realism

Benzell’s trepidation about our future fiscal imbalances is well founded. However, I also think Benzell’s modeled results, which represent a starting point in his analysis of AI and the public debt, are too optimistic an assessment of AI’s potential to boost growth. As he says himself,

“… many of the benefits from AI may come in the form of intangible improvements in digital consumption goods. … This might be real growth, that really raises welfare, but will be hard to tax or even measure.”

This is unlikely to register as an enhancement to productivity. Yet Benzell somehow buys into the argument that AI will lead to high levels of unemployment. That’s one of his reasons for expecting higher deficits.

My view is that AI will displace workers in some occupations, but it is unlikely to put large numbers of humans permanently out of work and into state support. That’s because the opportunity cost of many AI applications is and will remain quite high. It will have to compete for financing not only with government and more traditional capex projects, but with various forms of itself. This will limit both the growth we are likely to reap from AI and losses of human jobs.

Sovereign Wealth Fund

I have one other bone to pick with Benzell’s post. That’s in regard to his eagerness to see the government create a sovereign wealth fund. Here is his concluding paragraph:

“Instead of contemplating a larger debt, we should instead be talking about a national sovereign wealth fund, that could ‘own the robots on behalf of the people’. This would both boost output and welfare, and put the welfare system on an indefinitely sustainable path.”

Whether the government sells federal assets or collects booty from other kinds of “deals”, the very idea of accumulating risk assets in a sovereign wealth fund undermines the objective to reduce debt. It will be a struggle for a sovereign wealth fund to consistently earn cash returns to compensate for interest costs and pay down the debt. This is especially unwise given the risk of rising rates. Furthermore, government interests in otherwise private concerns will bring cronyism, displacement of market forces by central planning, and a politicization of economic affairs. Just pay off the debt with whatever receipts become available. This will free up savings for investment in AI capital and hasten the hoped-for boom in productivity.

Summary

AI’s contribution to economic growth probably will be inadequate and come too late to end government budget deficits and reduce our burgeoning public debt. To think otherwise seems far fetched in light of our historical inability to restrain the growth of federal spending. Interest on the federal debt already accounts for about half of the annual budget deficit. Refinancing the existing public debt will entail much higher costs if AI capex continues to grow aggressively, pushing interest rates higher. These dynamics make it pretty clear that AI won’t provide an easy fix for federal deficits and debt. In fact, ongoing federal borrowing needs will sop up savings needed for AI development and diffusion, even as the capital needed for AI drives up the cost of funds to the government. It’s a shame that AI won’t be able to crowd out government.

In a post a few years ago entitled “The National Endowment for Rich Farts”, I discussed a point that should be rather obvious: federal funding of the arts too often subsidizes the upper class, catering to their artistic tastes and underwriting a means through which they conduct social and professional networking. The topic is back in the news, with reports that the incoming Trump Administration, at the recommendation of the Department of Government Efficiency (DOGE), will attempt to eliminate funding for the Corporation for Public Broadcasting.

Great Big Stuff and Crowding Out

To opponents of federal arts funding, public radio is probably the bête noire of arts organizations due to its left-wing political orientation and the general affluence of its subscriber base. However, public arts funding goes way beyond subsidies for public radio.

Large nonprofits receive the bulk of government arts funding. Despite claims to the contrary, these organizations won’t go broke without the gravy provided by public funding. The federal government contributes about 3% of the revenue taken in by non-profit arts organizations, according to Americans For the Arts. These organizations are already heavily subsidized: their surpluses are tax exempt and private contributions are tax deductible. Tax deductions are worth more to those in high income-tax brackets, and involvement in such visible organizations is highly prized by elites.

It’s often argued that government should subsidize the arts because art has the qualities of a public good, but that’s a false premise. A good can be classified as “public” only when its consumption is non-exclusive and non-rivalrous. Can individuals be excluded from enjoying music? Of course. Can they be excluded from viewing a theatrical performance, a film, or any other piece of visual art? Generally yes, and art exhibitions and artistic performances are nearly always subject to paid and limited attendance.

In some contexts art is, or can be made, less excludable. Architecture can be admired (or detested) by anyone on the street. So can public monuments and street art. A concert or play can be performed free of charge, perhaps at a large, outdoor venue. Amplification and large video monitors can make a big difference in terms of non-exclusion. Museums can offer admission to the general public at no charge. And we can broaden the definition of a work to include copies or reproductions that might be available via public display or broadcast (on NPR!).

All these steps will help increase exposure to the arts. But you can’t make it mandatory. People will always self-exclude because they can. So, in which cases should taxpayers bear the costs of art, and of making it less exclusive? On the spectrum of legitimate functions of government, it’s hard to rank this sort of activity highly.

A claim less absurd than the public goods argument is that art has some positive spillover effects, or externalities. It should therefore be subsidized or underwritten with public funds lest it be underprovided. Unfortunately, the spillover effects of a piece of art (where relevant) are not always positive. After all, tastes vary considerably. One man’s art can be another man’s annoyance orprovocation. This undermines the case for public funding, at least for art that is controversial in nature.

Perhaps a better interpretation of art externalities is that exposure to the arts has positive spillover effects. Thus, additional art confers benefits to society above and beyond the edification of those exposed to it. Perhaps it makes us nicer and more interesting, but that’s a highly speculative rationale for public funding.

Less questionably, more art and more exposure to the arts does enrich society in ways that have nothing to do with external benefits. Culture and arts are by-products of normal social interactions between private individuals. The benefits of art exposure (and art education) are largely accrued privately. When artistic knowledge is shared to nourish or broaden one’s network, the benefits flow from private social interactions that arise naturally, rather than as a consequence of phantom external benefits.

The same danger looms when government provides a venue or manages aspects of a presentation of art, including curation of content. It’s an avenue through which art can become politicized. The problem, however, is not so much that a particular work might have political implications. As Samuel Andreyev, a Canadian composer says:

“Like any other subject, it is possible for political subjects to be handled sensitively by an artist, provided there is a strong enough element of abstraction and symbolism so that the work does not become merely journalistic.”

Andreyev makes a good point, but government funding and direction can create incentives to politicize art, encouraging more blatant expressions of political viewpoints at the expense of taxpayers.

I’ve certainly admired art despite subtle political implications with which I differed. One can hardly imagine a treatment of the human condition that would not invite tangential political commentary. Still, politicization of art should always be left as a private exercise, not one over which the government of a free society wields influence.

Do Markets Undervalue Art?

What about the artists themselves? The premise that artists deserve subsidies relies on the questionable presumption that the value of their work exceeds its commercial or market value. Thus, taxpayers are asked to pay handsomely for art that is not valued as highly by private buyers.

Artists who benefit from government arts funding are often well established professionally. Less fortunate artists scrape by, finding what market they can while working side gigs. In fact, many less celebrated artists work at their craft on a part-time basis while earning most of their income from day jobs. Should the government support these artists, or artists having few opportunities to promote their work?

It’s not clear that public funding should override the private market’s basis of valuation for established or unestablished artists. However, some government funding finds its way into less celebrated corners of the art world.This report uses data at the census tract level to show that arts organizations located in low income tracts, while receiving less, still get a disproportionate share of federal grant dollars relative to their share of the population. This finding should be viewed cautiously, as data at this level of aggregation has limitations. The findings do not imply that “starving artists” receive a disproportionate share of those dollars. Nor do they prove that federal grants benefit low-income individuals disproportionately via improved access to the arts. Again, the findings are based on the location of organizations. And again, large organizations receive the bulk of these grants.

Drawing the Line

So where do we draw the line on taxpayer subsidies for the arts? The standard, public-goods justification is false. While externalities may exist, they are not always positive, and it is hardly the state’s proper role to fund art that “challenges” notions about good and bad art. In that vein, just as law tends to be ineffective when it lacks consensus, public arts funding breeds dissent when the art is controversial.

The legitimacy of public arts funding ultimately depends on whether the art itself has a true public purpose. To varying degrees, this might include the architecture and interior design of public buildings, landscaping of parks, as well as certain monuments and statuary. Even within these disciplines, the selection of form, content, and the artists who will execute the work can be controversial. That might be unavoidable, though controversy will be minimized when the content of publicly-funded art remains within cultural norms.

Beyond those limited purposes, funding art at the federal level is difficult to justify. That role simply does not fall within the constitutionally-enumerated powers of the federal government. The tenuous rationale for subsidies implies that art is undervalued, despite the existence of a vibrant private ecosystem for art, including private support foundations and markets. To the extent that public subsidies line the pockets of elites or support art that would otherwise fail a market test, they represent a wasteful misallocation of resources.

Funding art might seem less troublesome at lower levels of government, where elected representatives and policymakers are in more intimate contact with voters and taxpayers. Still, the same economic reservations apply. At local levels, institutions like community orchestras and concerts series might be broadly supported. Publicly-funded museums, theatrical venues, and other facilities might be accepted by voters as well. If parents have educational choices and expect schools to teach art, it should be funded at public schools, so long as the content stays within cultural norms and is age-appropriate. Of course, all of these matters are up to local voters.

The greatest danger of public funding for the arts is that it tends to be utilized as a tool of political propaganda. Having the state select winners and losers in the arts invites politicization, undermining freedom and our system of government. On that point, Thomas Jefferson once made this observation:

“To compel a man to furnish contributions of money for the propagations of opinions which he disbelieves and abhors, is sinful and tyrannical.“

A week ago I posted about electrification and particularly EV mandates, one strand of government industrial policy under which non-favored sectors of the economy must labor. This post examines a related industrial policy: manipulation of power generation by government policymakers in favor of renewable energy technologies, while fossil fuels are targeted for oblivion. These interventions are a reaction to an overwrought climate crisis narrative, but they present many obstacles, oversights and risks of their own. Chief among them is whether the power grid will be capable of meeting current and future demand for power while relying heavily on variable resources: wind and sunshine.

Like almost everything I write, this post is too long! Here is a guide to what follows. Scroll down to whatever sections might be of interest:

Malinvestment: Idle capital

Key Considerations to chew on

False Premises: zero CO2? Low cost?

Imposed Cost: what and how much?

Supporting Growth: with renewables?

Resource Constraints: they’re tight!

Technological Advance: patience!

The Presumed Elephant: CO2 costs

Conclusion

Malinvestment

The intermittency of wind and solar power creates a fundamental problem of physically idle capital, which leaves the economy short of its production possibilities. To clarify, capital invested in wind and solar facilities is often idle in two critical ways. First, wind and solar assets have relatively low rates of utilization because of their variability, or intermittency. Second, neither provides “dispatchable” power: it is not “on call” in any sense during those idle periods, which are not entirely predictable. Wind and solar assets therefore contribute less value to the electric grid than dispatchable sources of power having equivalent capacity and utilization.

Is “idle capital” a reasonable characterization? Consider the shipping concerns that are now experimenting with sails on cargo ships. What is the economic value of such a ship without back-up power? Can you imagine them drifting in the equatorial calms for days on end? Even light winds would slow the transport of goods significantly. Idle capital might be bad enough, but a degree of idleness allows flexibility and risk mitigation in many applications. Idle, non–dispatchable capital, however, is unproductive capital.

Likewise, solar-powered signage can underperform or fail over the course of several dark, wintry days, even with battery backup. The signage is more reliable and valuable when it is backed-up by another power source. Again, idle, non-dispatchable capital is unproductive capital.

The pursuit of net-zero carbon emissions via wind and solar power creates idle capital, which increasingly lacks adequate backup power. That should be a priority, but it’s not. This misguided effort is funded from both private investment and public subsidies, but the former is very much contingent on the latter. That’s because the flood of subsidies is what allows private investors to profit from idle capital. Rent-enabled investments like these crowd out genuinely productive capital formation, which is not limited to power plants that might otherwise use fossil fuels.

Creating idle or unemployed physical capital is malinvestment, and it diminishes future economic growth. The surge in this activity began in earnest during the era of negative real interest rates. Today, in an era of higher rates, taxpayers can expect an even greater burden, as can ratepayers whose power providers are guaranteed returns on their regulated rate bases.

Key Consideration

The forced transition to net zero will be futile, but especially if wind and solar energy are the primary focus. Keep the following in mind:

The demand for electricity is expected to soar, and soon! Policymakers have high hopes for EVs, and while adoption rates might fall well short of their goals, they’re doing their clumsy best to force EVs down our throats with mandates. But facilitating EV charging presents difficulties. Lionel Shriver states the obvious: “Going Electric Requires Electricity”. Reliable electricity!

Perhaps more impressive than prospects for EVs is the expected growth in power demand from data centers required by the explosion of artificial intelligence applications across many industries. It’s happening now! This will be magnified with the advent of artificial general intelligence (AGI).

Dispatchable power sources are needed to back-up unreliable wind and solar power to ensure service continuity. Maintaining backup power carries a huge “imposed cost” at the margin for wind and solar. At present, that would entail CO2 emissions, violating the net zero dictum.

Perhaps worse than the cost of backup power would be the cost borne by users under the complete elimination of certain dispatchable power sources. An imposed cost then takes the form of outages. Users are placed at risk of losing power at home, at the office and factories, at stores, in transit, and at hospitals at peak hours or under potentially dangerous circumstances like frigid or hot weather.

Historically, dispatchable power has allowed utilities to provide reliable electricity on-demand. Just flip the switch! This may become a thing of the past.

Wind and solar power are sometimes available when they’re not needed, in which case the power goes unused because we lack effective power storage technology.

Wind and solar power facilities operate at low rates of utilization, yet new facilities are always touted at their full nameplate capacity. Capacity factors for wind turbines averaged almost 36% in the U.S. in 2022, while solar facilities averaged only about 24%. This compared with nuclear power at almost 93%, natural gas (66%), and coal (48%). Obviously, the low capacity factors for wind and solar reflect their variable nature, rather than dispatchable responses to fluctuations in power demand.

Low utilization and variability are underemphasized or omitted by those promoting wind and solar plant in the media and often in discussions of public policy, and no wonder! We hear a great deal about “additions to capacity”, which overstate the actual power-generating potential by factors of three to four times. Here is a typical example.

Wind and solar power are far more heavily subsidized than fossil fuels. This is true in absolute terms and especially on the basis of actual power output, which reveals their overwhelmingly uneconomic nature. From the link above, here are Mitch Rolling and Isaac Orr on this point:

“In 2022, wind and solar generators received three and eighteen times more subsidies per MWh, respectively, than natural gas, coal, and nuclear generators combined. Solar is the clear leader, receiving anywhere from $50 to $80 per MWh over the last five years, whereas wind is a distant second at $8 to $10 per MWh …. Renewable energy sources like wind and solar are largely dependent on these subsidies, which have been ongoing for 30 years with no end in sight.”

The first-order burden of subsidies falls on taxpayers. The second-order burdens manifest in an unstable grid and higher power costs. But just to be clear, subsidies are paid by governments to producers or consumers to reduce the cost of activity favored by policymakers. However, the International Monetary Fund frequently cites “subsidy” figures that include staff estimates of unaddressed externalities. These are based on highly-simplified models and subject to great uncertainty, of course, especially when dollar values are assigned to categories like “climate change”. Despite what alarmists would have us believe, the extent and consequences of climate change are not settled scientific issues, let alone the dollar cost.

Wind and solar power are extremely land- and/or sea-intensive. For example, Casey Handmer estimates that a one-Gigawatt data center, if powered by solar panels, would need a footprint of 20,000 acres.

Solar installations are associated with a significant heat island effect: “We found temperatures over a PV plant were regularly 3–4 °C warmer than wildlands at night….”

In addition to the destruction of habitat both on- and offshore, turbine blades create noise, electromagnetism, and migration barriers. Wind farms have been associated with significant bird and bat fatalities. Collisions with moving blades are one thing, but changes to the winds and air pressure around turbines are also a danger to avian species.

Solar farms present dangers to waterfowl. These creatures are tricked into diving toward what they believe to be bodies of water, only to crash into the panels.

The production of wind and solar equipment requires the intensive use of scarce resources, including environmentally-sensitive materials. Extracting these materials often requires the excavation of massive amounts of rock subject to extensive processing. Mining and processing rely heavily on diesel fuel. Net zero? No.

Wind and solar facilities often present major threats of toxicity at disposal, or even sooner. A recent hail storm in Texas literally destroyed a solar farm, and the smashed panels have prompted concerns not only about solar “sustainability”, but also that harsh chemicals may be leaking into the local environment.

The transmission of power is costly, but that cost is magnified by the broad spatial distribution of wind and solar generating units. Transmission from offshore facilities is particularly complex. And high voltage lines run into tremendous local opposition and regulatory scrutiny.

When wind turbines and solar panels are idle, so are the transmission facilities needed to reach them. Thus, low utilization and the variability of those units drives up the capital needed for power and power transmission.

There is also an acute shortage of transformers, which presents a major bottleneck to grid development and stability.

While zero carbon is the ostensible goal, zero carbon nuclear power has been neglected by our industrial planners. That neglect plays off exaggerated fears about safety. Fortunately, there is a growing realization that nuclear power may be surest way to carbon reductions while meeting growth in power demand. In fact, new data centers will go off-grid with their own modular reactors.

At the Shriver link, he notes the smothering nature of power regulation, which obstructs the objective of providing reliable power and any hope of achieving net zero.

The Biden administration has resisted the substitution of low CO2 emitting power sources for high CO2 emitting sources. For example, natural gas is more energy efficient in a variety of applications than other fuel sources. Yet policymakers seem determined to discourage the production and use of natural gas.

False Premises

Wind and solar energy are touted by the federal government as zero carbon and low-cost technologies, but both claims are false. Extracting the needed resources, fabricating, installing, connecting, and ultimately disposing of these facilities is high in carbon emissions.

The claim that wind and solar have a cost advantage over traditional power sources is based on misleading comparisons. First, putting claims about the cost of carbon aside, it goes without saying that the cost of replacing already operational coal or natural gas generating capacity with new wind and solar facilities is greater than doing nothing.

The hope among net zero advocates is that existing fossil fuel generating plant can be decommissioned as more renewables come on-line. Again, this thinking ignores the variable nature of renewable power. Dispatchable backup power is required to reliably meet power demand. Otherwise, fluctuating power supplies undermine the economy’s productive capacity, leading to declines in output, income, health, and well being. That is costly, but so is maintaining and adding back-up capacity. Costs of wind and solar should account for this necessity. It implies that wind and solar generating units carry a high cost at the margin.

Imposed Costs

A “grid report card” from the Mackinac Center for Public Policy notes the conceptual flaw in comparing the levelized cost (à la Lazard) of a variable resource with one capable of steady and dispatchable performance. From the report, here is the crux of the imposed-cost problem:

“… the more renewable generation facilities you build, the more it costs the system to make up for their variability, and the less value they provide to electricity markets.”

A committment to variable wind and solar power along with back-up capacity also implies that some capital will be idle regardless of wind and solar conditions. This is part of the imposed cost of wind and solar built into the accounting below. But while back-up power facilities will have idle periods, it is dispatchable and serves an insurance function, so it has value even when idle in preserving the stability of the grid. For that matter, sole reliance on dispatchable power sources requires excess capacity to serve an insurance function of a similar kind.

The Mackinac report card uses estimates of imposed cost from an Institute for Energy Research to construct the following comparison (expand the view or try clicking the image for a better view):

The figures shown in this table are somewhat dated, but the Mackinac authors use updated costs for Michigan from the Center of the American Experiment. These are shown below in terms of average costs per MWh through 2050, but the labels require some additional explanation.

The two bars on the left show costs for existing coal ($33/MWh) and gas-powered ($22) plants. The third and fourth bars are for new wind ($180) and solar ($278) installations. The fifth and sixth bars are for new nuclear reactors (a light water reactor ($74) and a small modular reactor($185)). Finally, the last two bars are for a new coal plant ($106) and a natural gas plant ($64), both with carbon capture and storage (CCS). It’s no surprise that existing coal and gas facilities are the most cost effective. Natural gas is by far the least costly of the new installations, followed by the light water reactor and coal.

The Mackinac “report card” is instructive in several ways. It provides a detailed analysis of different types of power generation across five dimensions, including reliability, cost, cleanliness, and market feasibility (the latter because some types of power (hydro, geothermal) have geographic limits. Natural gas comes out the clear winner on the report card because it is plentiful, energy dense, dispatchable, clean burning, and low-cost.

Supporting Growth

Growth in the demand for power cannot be met with variable resources without dispatchable backup or intolerable service interruptions. Unreliable power would seriously undermine the case for EVs, which is already tenuous at best. Data centers and other large users will go off-grid before they stand for it. This would represent a flat-out market rejection of renewable investments, ESGs be damned!

Casey Handmer makes some interesting projections of the power requirements of data centers supporting not just AI, but AGI, which he discusses in “How To Feed the AIs”. Here is his darkly humorous closing paragraph, predicated on meeting power demands from AGI via solar:

“It seems that AGI will create an irresistibly strong economic forcing function to pave the entire world with solar panels – including the oceans. We should probably think about how we want this to play out. At current rates of progress, we have about 20 years before paving is complete.”

Resource Constraints

Efforts to force a transition to wind and solar power will lead to more dramatic cost disadvantages than shown in the Mackinac report. By “forcing” a transition, I mean aggressive policies of mandates and subsidies favoring these renewables. These policies would effectuate a gross misallocation of resources. Many of the commodities needed to fabricate the components of wind and solar installations are already quite scarce, particularly on the domestic U.S. front. Inflating the demand for these commodities will result in shortages and escalating costs, magnifying the disadvantages of wind and solar power in real economic terms.

To put a finer point on the infeasibility of the net zero effort, Simon P. Michaux produced a comparative analysis in 2022 of the existing power mix versus a hypothetical power mix of renewable energy sources performing an equal amount of work, but at net-zero carbon emissions (the link is a PowerPoint summary). In the renewable energy scenario, he calculated the total quantities of various resources needed to achieve the objective over one generation of the “new” grid (to last 20 -30 years). He then calculated the numbers of years of mining or extraction needed to produce those quantities based on 2019 rates of production. Take a look at the results in the right-most column:

Those are sobering numbers. Granted, they are based on 2019 wind and solar technology. However, it’s clear that phasing out fossil fuels using today’s wind and solar technology would be out of the question within the lifetime of anyone currently living on the planet. Michaux seems to have a talent for understatement:

“Current thinking has seriously underestimated the scale of the task ahead.”

He also emphasizes the upward price pressure we’re likely to witness in the years ahead across a range of commodities.

Technological Breakthroughs

Michaux’s analysis assumes static technology, but there may come a time in the not-too-distant future when advances in wind and solar power and battery storage allow them to compete with hydrocarbons and nuclear power on a true economic basis. The best way to enable real energy breakthroughs is through market-driven economic growth. Energy production and growth is hampered, however, when governments strong-arm taxpayers, electricity buyers, and traditional energy producers while rewarding renewable developers with subsidies.

We know that improvements will come across a range of technologies. We’ve already seen reductions in the costs of solar panels themselves. Battery technology has a long way to go, but it has improved and might some day be capable of substantial smoothing in the delivery of renewable power. Collection of solar power in space is another possibility, as the feasibility of beaming power to earth has been demonstrated. This solution might also have advantages in terms of transmission depending on the locations and dispersion of collection points on earth, and it would certainly be less land intensive than solar power is today. Carbon capture and carbon conversion are advancing technologies, making net zero a more feasible possibility for traditional sources of power. Nuclear power is zero carbon, but like almost everything else, constructing plants is not. Nevertheless, fission reactors have made great strides in terms of safety and efficiency. Nuclear fusion development is still in its infancy, but there have been notable advances of late.

Some or all of these technologies will experience breakthroughs that could lead to a true, zero-carbon energy future. The timeline is highly uncertain, but it’s likely to be faster than anything like the estimates in Michaux’s analysis. Who knows? Perhaps AI will help lead us to the answers.

A Presumed Elephant

This post and my previous post have emphasized two glaring instances of government failure on their own terms: a headlong plunge into unreliable renewable energy, and forced electrification done prematurely and wrong. Some would protest that I left the veritable “elephant in the room”: the presumed external or spillover costs associated with CO2 emissions from burning fossil fuels. Renewables and electrification are both intended to prevent those costs.

External costs were not ignored, of course. Externalities were discussed explicitly in several different contexts such as the mining of new materials, EV tire wear, the substitution of “cleaner” fuels for others, toxicity at disposal, and the exaggerated reductions in CO2 from EVs when the “long tailpipe” problem is ignored. However, I noted explicitly that estimates of unaddressed externalities are often highly speculative and uncertain, and especially the costs of CO2 emissions. They should not be included in comparisons of subsidies.

Therefore, the costs of various power generating technologies shown above do not account for estimates of externalities. If you’re inclined, other SCC posts on the CO2 “elephant” can be found here.

Conclusion

Power demand is expected to soar given the coming explosion in AI applications, and especially if the heavily-subsidized and mandated transition to EVs comes to pass. But that growth in demand will not and cannot be met by relying on renewable energy sources. Their variability implies substantial idle capacity, higher costs, and service interruptions. Such a massive deployment of idle capital would represents an enormous waste of resources, but the sad fact is it’s been underway for some time.

In the years ahead, the net-zero objective will prove representative of a bumbling effort at industrial planning. Costs will be driven higher, including the cost inflicted by outages and environmental damage. Ratepayers, taxpayers, and innocents will share these burdens. Travis Fisher is spot on when he says the grid is becoming a “dangerous liability” thanks to wounds inflicted by subsidies, regulations, and mandates.

“The National Electrical Grid is teetering on collapse. The shift away from full-time available power (like fossil fuels, LNG, etc.) to so-called ‘green’ sources has deeply impacted reliability.”

“Also, as more whale-killing off-shore wind farms are planned, the Biden administration forgot to plan for the thousands of miles of transmission lines that will be needed. And in a perfect example of leftist autophagy, there is considerable opposition from enviro-groups who will tie up the construction of wind farms and transmission lines in court for decades.”

Meanwhile, better alternatives to wind and solar have been routinely discouraged. The substantial reductions in carbon emissions achieved in the U.S. over the past 15 years were caused primarily by the substitution of natural gas for coal in power generation. Much more of that is possible. The Biden Administration, however, wishes to prevent that substitution in favor of greater reliance on high-cost, unreliable renewables. And the Administration wishes to do so without adequately backing up those variable power sources with dispatchable capacity. Likewise, nuclear power has been shunted aside, despite its safety, low risk, and dispatchability. However, there are signs of progress in attitudes toward bringing more nuclear power on-line.

Industrial policy usually meets with failure, and net zero via wind and solar power will be no exception. Like forced electrification, unreliable power fails on its own terms. Net zero ain’t gonna happen any time soon, and not even by 2050. That is, it won’t happen unless net zero is faked through mechanisms like fraudulent carbon credits (and there might not be adequate faking capacity for that!). Full-scale net-zero investment in wind and solar power, battery capacity, and incremental transmission facilities will drive the cost of power upward, undermining economic growth. Finally, wind and solar are not the environmental panacea so often promised. Quite the contrary: mining of the necessary minerals, component fabrication, installation, and even operation all have negative environmental impacts. Disposal at the end of their useful lives might be even worse. And the presumed environmental gains … reduced atmospheric carbon concentrations and lower temperatures, are more scare story than science.

Postscript: here’s where climate alarmism has left us, and this is from a candidate for the U.S. Senate (she deleted the tweet after an avalanche of well-deserved ridicule):

We’re told again and again that government must take action to correct “market failures”. Economists are largely responsible for this widespread view. Our standard textbook treatments of external costs and benefits are constructed to demonstrate departures from the ideal of perfectly competitive market equilibria. This posits an absurdly unrealistic standard and diminishes the power and dramatic success of real-world markets in processing highly dispersed information, allocating resources based on voluntary behavior, and raising human living standards. It also takes for granted the underlying institutional foundations that lead to well-functioning markets and presumes that government possesses the knowledge and ability to rectify various departures from an ideal. Finally, “corrective” interventions are usually exposited in economics classes as if they are costless!

Failed Disgnoses

This brings into focus the worst presumption of all: that government solutions to social and economic problems never fail to achieve their intended aims. Of course that’s nonsense. If defined on an equivalent basis, government failure is vastly more endemic and destructive than market failure.

“According to ancient legend, a Roman emperor was asked to judge a singing contest between two participants. After hearing the first contestant, the emperor gave the prize to the second on the assumption that the second could be no worse than the first. Of course, this assumption could have been wrong; the second singer might have been worse. The theory of market failure committed the same mistake as the emperor. Demonstrating that the market economy failed to live up to the ideals of general competitive equilibrium was one thing, but to gleefully assert that public action could costlessly correct the failure was quite another matter. Unfortunately, much analytical work proceeded in such a manner. Many scholars burst the bubble of this romantic vision of the political sector during the 1960s. But it was [James] Buchanan and Gordon Tullock who deserve the credit for shifting scholarly focus.”

John Cochrane sums up the whole case succinctly in the “punchline” of a recent post:

“The case for free markets never was their perfection. The case for free markets always was centuries of experience with the failures of the only alternative, state control. Free markets are, as the saying goes, the worst system; except for all the others.”

Tracing Failures

We can view the relation between market failure and government failure in two ways. First, we can try to identify market failures and root causes. For example, external costs like pollution cause harm to innocent third parties. This failure might be solely attributable to transactions between private parties, but there are cases in which government engages as one of those parties, such as defense contracting. In other cases government effectively subsidizes toxic waste, like the eventual disposal of solar panels. Another kind of market failure occurs when firms wield monopoly power, but that is often abetted by costly regulations that deliver fatal blows to small competitors.

The second way to analyze the nexus between government and market failures is to first examine the taxonomy of government failure and identify the various damages inflicted upon the operation of private markets. That’s the course I’ll follow below, though by no means is the discussion here exhaustive.

Failures In and Out of Scope

An extensive treatment of government failure was offered eight years ago by William R. Keech and Michael Munger. To start, they point out what everyone knows: governments occasionally perpetrate monstrous acts like genocide and the instigation of war. That helps illustrate a basic dichotomy in government failures:

“… government may fail to do things it should do, or government may do things it should not do.’

Both parts of that statement have numerous dimensions. Failures at what government should do run the gamut from poor service at the DMV, to failure to enforce rights, to corrupt bureaucrats and politicians skimming off the public purse in the execution of their duties. These failures of government are all too common.

What government should and should not do, however, is usually a matter of political opinion. Thomas Jefferson’s axioms appear in a single sentence at the beginning of the Declaration of Independence; they are a tremendous guide to the first principles of a benevolent state. However, those axioms don’t go far in determining the range of specific legal protections and services that should and shouldn’t be provided by government.

Pareto Superiority

Keech and Munger engage in an analytical exercise in which the “should and shouldn’t” question is determined under the standard of Pareto superiority. A state of the world is Pareto superior if at least one person prefers it to the current state (and no one else is averse to it). Coincidentally, voluntary trades in private markets always exploit Pareto superior opportunities, absent legitimate external costs and benefits.

The set of Pareto superior states available to government can be expanded by allowing for side payments or compensation to those who would have preferred the current state. Still, those side payments are limited by the magnitude of the gains flowing to those who prefer the alternative (and if those gains can be redistributed monetarily).

Keech and Munger define government failure as the unexploited existence of Pareto superior states. Of course, by this definition, only a benevolent, omniscient, and omnipotent dictator could hope to avoid government failure. But this is no more unrealistic than the assumptions underlying perfectly competitive market equilibrium from which departure are deemed “market failures” that government should correct. Thus, Keech and Munger say:

“The concept of government failure has been trapped in the cocoon of the theory of perfect markets. … Government failure in the contemporary context means failing to resolve a classic market failure.”

But markets must operate within a setting defined by culture and institutions. The establishment of a social order under which individuals have enforceable rights must come prior to well-functioning markets, and that requires a certain level of state capacity. Keech and Munger are correct that market failure is often a manifestation of government failure in setting and/or enforcing these “rules of the game”.

“The real question is … how the rules of the game should be structured in terms of incentives, property rights, and constraints.”

The Regulatory State and Market Failures

Government can do too little in defining and enforcing rights, and that’s undoubtedly a cause of failure in markets in even the most advanced economies. At the same time there is an undeniable tendency for mission creep: governments often try to do too much. Overregulation in the U.S. and other developed nations creates a variety of market failures. This includes the waste inherent in compliance costs that far exceed benefits; welfare losses from price controls, licensing, and quotas; diversion of otherwise productive resources into rent seeking activity, anti-competitive effects from “regulatory capture”; Chevron-like distortions endemic to the administrative judicial process; unnecessary interference in almost any aspect of private business; and outright corruption and bribe-taking.

Central Planning and Market Failures

Another category of government attempting to “do too much” is the misallocation of resources that inevitably accompanies efforts to pick “winners and losers”. The massive subsidies flowing to investors in various technologies are often misdirected. Many of these expenditures end up as losses for taxpayers, and this is not the only form in which failed industrial planning takes place. A related evil occurs when steps are taken to penalize and destroy industries in political disfavor with thin economic justification.

Other clear examples of government “planning” failure are protectionist laws. These are a net drain on our wealth as a society, denying consumers of free choice and saddling the country with the necessity to produce restricted products at high cost relative to erstwhile trading partners.

There are, of course, failures lurking within many other large government spending programs in areas such as national defense, transportation, education, and agriculture. Many of these programs can be characterized as centrally planning. Not only are some of these expenditures ineffectual, but massive procurement spending seems to invite waste and graft. After all, it’s somebody else’s money.

Redistribution and Market Failures

One might regard redistribution programs as vehicles for the kinds of side payments described by Keech and Munger. Some might even say these are the side payments necessary to overcome resistance from those unable to thrive in a market economy. That reverses the historical sequence of events, however, since the dominant economic role of markets preceded the advent of massive redistribution schemes. Unfortunately, redistribution programs have been plagued by poor design, such as the actuarial nightmare inherent in Social Security and the destructive work incentives embedded in other parts of the social safety net. These are rightly viewed as government failures, and their distortionary effects spill variously into capital markets, labor markets and ultimately product markets.

Taxation and Market Failures

All these public initiatives under which government failures precipitate assorted market failures must be paid for by taxpayers. Therefore, we must also consider the additional effects of taxation on markets and market failures. The income tax system is rife with economic distortions. Not only does it inflict huge compliance costs, but it alters incentives in ways that inhibit capital formation and labor supply. That hampers the ability of input markets to efficiently meet the needs of producers, inhibiting the economy’s productive capacity. In turn, these effects spill into output market failures, with consequent losses in .social welfare. Distortionary taxes are a form of government failure that leads to broad market failures.

Deficits and Market Failure

More often than not, of course, tax revenue is inadequate to fund the entire government budget. Deficit spending and borrowing can make sense when public outlays truly produce long-term benefits. In fact, the mere existence of “risk-free” assets (Treasury debt) across the maturity spectrum might enhance social welfare if it enables improvements in portfolio diversification that outweigh the cost of the government’s interest obligations. (Treasury securities do bear interest-rate risk and, if unindexed, they bear inflation risk.)

Nevertheless, borrowing can reflect and magnify deleterious government efforts to “do too much”, ultimately leading to market failures. Government borrowing may “crowd out” private capital formation, harming economy-wide productivity. It might also inhibit the ability of households to borrow at affordable rates. Interest costs of the public debt may become explosive as they rise relative to GDP, limiting the ability of the public sector to perform tasks that it should *actually* do, with negative implications for market performance.

Inflation and Market Failure

Deficit spending promotes inflation as well. This is more readily enabled when government debt is monetized, but absent fiscal discipline, the escalation of goods prices is the only remaining force capable of controlling the real value of the debt. This is essentially the inflation tax.

Inflation is a destructive force. It distorts the meaning of prices, causes the market to misallocate resources due to uncertainty, and inflicts costs on those with fixed incomes or whose incomes cannot keep up with inflation. Sadly, the latter are usually in lower socioeconomic strata. These are symptoms of market failure prompted by government failure to control spending and maintain a stable medium of exchange.

Conclusion

Markets may fail, but when they do it’s very often rooted in one form of government failure or another. Sometimes it’s an inadequacy in the establishment or enforcement of property rights. It could be a case of overzealous regulation. Or government may encroach on, impede, or distort decisions regarding the provision of goods or services best left to the market. More broadly, redistribution and taxation, including the inflation tax, distort labor and capital markets. The variety of distortions created when government fails at what it should do, or does what it shouldn’t do, is truly daunting. Yet it’s difficult to find leaders willing to face up to all this. Statism has a powerful allure, and too many elites are in thrall to the technocratic scientism of government solutions to social problems and central planning in the allocation of resources.

Policy activists have long maintained that manipulating government policy can stabilize the economy. In other words, big spending initiatives, tax cuts, and money growth can lift the economy out of recessions, or budget cuts and monetary contraction can prevent overheating and inflation. However, this activist mirage burned away under the light of experience. It’s not that fiscal and monetary policy are powerless. It’s a matter of practical limitations that often cause these tools to be either impotent or destabilizing to the economy, rather than smoothing fluctuations in the business cycle.

The macroeconomics classes seem like yesterday: Keynesian professors lauded the promise of wise government stabilization efforts: policymakers could, at least in principle, counter economic shocks, particularly on the demand side. That optimistic narrative didn’t end after my grad school days. I endured many client meetings sponsored by macro forecasters touting the fine-tuning of fiscal and monetary policy actions. Some of those economists were working with (and collecting revenue from) government policymakers, who are always eager to validate their pretensions as planners (and saviors). However, seldom if ever do forecasters conduct ex post reviews of their model-spun policy scenarios. In fairness, that might be hard to do because all sorts of things change from initial conditions, but it definitely would not be in their interests to emphasize the record.

In this post I attempt to explain why you should be skeptical of government stabilization efforts. It’s sort of a lengthy post, so I’ve listed section headings below in case readers wish to scroll to points of most interest. Pick and choose, if necessary, though some context might get lost in the process.

Expectations Change the World

Fiscal Extravagance

Multipliers In the Real World

Delays

Crowding Out

Other Peoples’ Money

Tax Policy

Monetary Policy

Boom and Bust

Inflation Targeting

Via Rate Targeting

Policy Coordination

Who Calls the Tune?

Stable Policy, Stable Economy

Expectations Change the World

There were always some realists in the economics community. In May we saw the passing of one such individual: Robert Lucas was a giant intellect within the economics community, and one from whom I had the pleasure of taking a class as a graduate student. He was awarded the Nobel Prize in Economic Science in 1995 for his applications of rational expectations theory and completely transforming macro research. As Tyler Cowen notes, Keynesians were often hostile to Lucas’ ideas. I remember a smug classmate, in class, telling the esteemed Lucas that an important assumption was “fatuous”. Lucas fired back, “You bastard!”, but proceeded to explain the underlying logic. Cowen uses the word “charming” to describe the way Lucas disarmed his critics, but he could react strongly to rude ignorance.

Lucas gained professional fame in the 1970s for identifying a significant vulnerability of activist macro policy. David Henderson explains the famous “Lucas Critique” in the Wall Street Journal:

“… because these models were from periods when people had one set of expectations, the models would be useless for later periods when expectations had changed. While this might sound disheartening for policy makers, there was a silver lining. It meant, as Lucas’s colleague Thomas Sargent pointed out, that if a government could credibly commit to cutting inflation, it could do so without a large increase in unemployment. Why? Because people would quickly adjust their expectations to match the promised lower inflation rate. To be sure, the key is government credibility, often in short supply.”

Non-credibility is a major pitfall of activist macro stabilization policies that renders them unreliable and frequently counterproductive. And there are a number of elements that go toward establishing non-credibility. We’ll distinguish here between fiscal and monetary policy, focusing on the fiscal side in the next several sections.

Fiscal Extravagance

We’ve seen federal spending and budget deficits balloon in recent years. Chronic and growing budget deficits make it difficult to deliver meaningful stimulus, both practically and politically.

The next chart is from the most recent Congressional Budget Office (CBO) report. It shows the growing contribution of interest payments to deficit spending. Ever-larger deficits mean ever-larger amounts of debt on which interest is owed, putting an ever-greater squeeze on government finances going forward. This is particularly onerous when interest rates rise, as they have over the past few years. Both new debt is issued and existing debt is rolled over at higher cost.

Relief payments made a large contribution to the deficits during the pandemic, but more recent legislation (like the deceitfully-named Inflation Reduction Act) piled-on billions of new subsidies for private investments of questionable value, not to mention outright handouts. These expenditures had nothing to do with economic stabilization and no prayer of reducing inflation. Pissing away money and resources only hastens the debt and interest-cost squeeze that is ultimately unsustainable without massive inflation.

Hardly anyone with future political ambitions wants to address the growing entitlements deficit … but it will catch up with them. Social Security and Medicare are projected to exhaust their respective trust funds in the early- to mid-2030s, which will lead to mandatory benefit cuts in the absence of reform.

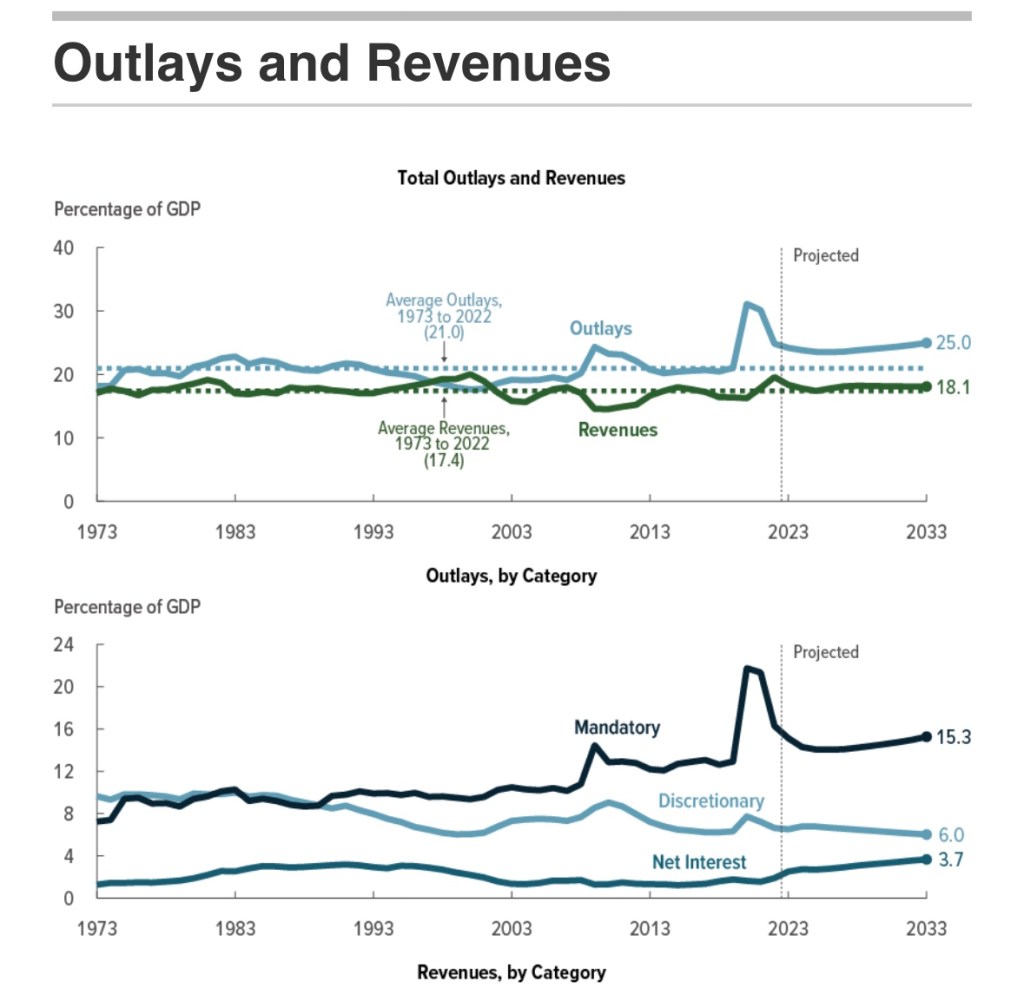

If it still isn’t obvious, the real problem driving the budget imbalance is spending, not revenue, as the next CBO chart demonstrates. The “emergency” pandemic measures helped precipitate our current stabilization dilemma. David Beckworth tweets that the relief measures “spurred a rapid recovery”, though I’d hasten to add that a wave of private and public rejection of extreme precautions in some regions helped as well. And after all, the pandemic downturn was exaggerated by misdirected policies including closures and lockdowns that constrained both the demand and supply sides. Beckworth acknowledges the relief measures “propelled inflation”, but the pandemic also seemed to leave us on a permanently higher spending path. Again, see the first chart below.

The second chart below shows that non-discretionary spending (largely entitlements) and interest outlays are how we got on that path. The only avenue for countercyclical spending is discretionary expenditures, which constitute an ever-smaller share of the overall budget.

We’ve had chronic deficits for years, but we’ve shifted to a much larger and continuing imbalance. With more deficits come higher interest costs, especially when interest rates follow a typical upward cyclical pattern. This creates a potentially explosive situation that is best avoided via fiscal restraint.

Putting other doubts about fiscal efficacy aside, it’s all but impossible to stimulate real economic activity when you’ve already tapped yourself out and overshot in the midst of a post-pandemic economic expansion.

Multipliers In the Real World

So-called spending multipliers are deeply beloved by Keynesians and pork-barrel spenders. These multipliers tell us that every dollar of extra spending ultimately raises income by some multiple of that dollar. This assumes that a portion of every dollar spent by government is re-spent by the recipient, and a portion of that is re-spent again by another recipient. But spending multipliers are never what they’re cracked up to be for a variety of reasons. (I covered these in“Multipliers Are For Politicians”, and also see this post.) There are leakages out of the re-spending process (income taxes, saving, imports), which trim the ultimate impact of new spending on income. When supply constraints bind on economic activity, fiscal stimulus will be of limited power in real terms.

If stimulus is truly expected to be counter-cyclical and transitory, as is generally claimed, then much of each dollar of extra government spending will be saved rather than spent. This is the lesson of the permanent income hypothesis. It means greater leakages from the re-spending stream and a lower multiplier. We saw this with the bulge in personal savings in the aftermath of pandemic relief payments.

Another side of this coin, however, is that cutting checks might be the government’s single-most efficient activity in execution, but it can create massive incentive problems. Some recipients are happy to forego labor market participation as long as the government keeps sending them checks, but at least they spend some of the income.

Delays

Another unappreciated and destabilizing downside of fiscal stimulus is that it often comes too late, just when the economy doesn’t need stimulus. That’s because a variety of delays are inherent in many spending initiatives: legislative, regulatory, legal challenges, planning and design, distribution to various spending authorities, and final disbursement. As I noted here:

“Even government infrastructure projects, heralded as great enhancers of American productivity, are often subject to lengthy delays and cost overruns due to regulatory and environmental rules. Is there any such thing as a federal ‘shovel-ready’ infrastructure project?”

Crowding Out

The supply of savings is limited, but when government borrows to fund deficits, it directly competes with private industry for those savings. Thus, funds that might otherwise pay for new plant, equipment, and even R&D are diverted to uses that should qualify as government consumption rather than long-term investment. Government competition for funds “crowds-out” private activity and impedes growth in the economy’s productive capacity. Thus, the effort to stimulate economic activity is self-defeating in some respects.

Other Peoples’ Money

Government doesn’t respond to price signals the way self-interested private actors do. This indifference leads to mis-allocated resources and waste. It extends to the creation of opportunities for graft and corruption, typically involving diversion of resources into uses that are of questionable productivity (corn ethanol, solar and wind subsidies).

Consider one other type of policy action perceived as counter-cyclical: federal bailouts of failing financial institutions or other troubled businesses. These rescues prop up unproductive enterprises rather than allowing waste to be flushed from the system, which should be viewed as a beneficial aspect of recession. The upshot is that too many efforts at economic stabilization are misdirected, wasteful, ill-timed, and pro-cyclical in impact.

Tax Policy

Like stabilization efforts on the spending side, tax changes may be badly timed. Tax legislation is often complex and can take time for consumers and businesses to adjust. In terms of traditional multiplier analysis, the initial impact of a tax change on spending is smaller than for expenditures, so tax multipliers are smaller. And to the extent that a tax change is perceived as temporary, it is made less effective. Thus, while changes in tax policy can have powerful real effects, they suffer from some of the same practical shortcomings for stabilization as changes in spending.

However, stimulative tax cuts, if well crafted, can boost disposable incomes and improve investment and work incentives. As temporary measures, that might mean an acceleration of certain kinds of activity. Tax increases reduce disposable incomes and may blunt incentives, or prompt delays in planned activities. Thus, tax policy may bear on the demand side as well as the timing of shifts in the economy’s productive potential or supply side.

Monetary Policy

Monetary policy is subject to problems of its own. Again, I refer to practical issues that are seemingly impossible for policy activists to overcome. Monetary policy is conducted by the nation’s central bank, the Federal Reserve (aka, the Fed). It is theoretically independent of the federal government, but the Fed operates under a dual mandate established by Congress to maintain price stability and full employment. Therein lies a basic problem: trying to achieve two goals that are often in conflict with a single policy tool.

Make no mistake: variations in money supply growth can have powerful effects. Nevertheless, they are difficult to calibrate due to “long and variable lags” as well as changes in money “velocity” (or turnover) often prompted by interest rate movements. Excessively loose money can lead to economic excesses and an overshooting of capacity constraints, malinvestment, and inflation. Swinging to a tight policy stance in order to correct excesses often leads to “hard landings”, or recession.

Boom and Bust

The Fed fumbled its way into engineering the Great Depression via excessively tight monetary policy. “Stop and go” policies in the 1970s led to recurring economic instability. Loose policy contributed to the housing bubble in the 2000s, and subsequent maladjustments led to a mortgage crisis (also see here). Don’t look now, but the inflationary consequences of the Fed’s profligacy during the pandemic prompted it to raise short-term interest rates in the spring of 2022. It then acted with unprecedented speed in raising rates over the past year. While raising rates is not always synonymous with tightening monetary conditions, money growth has slowed sharply. These changes might well lead to recession. Thus, the Fed seems given to a pathology of policy shifts that lead to unintentional booms and busts.

Inflation Targeting

The Fed claims to follow a so-called flexible inflation targeting policy. In reality, it has reacted asymmetrically to departures from its inflation targets. It took way too long for the Fed to react to the post-pandemic surge in inflation, dithering for months over whether the surge was “transitory”. It wasn’t, but the Fed was reluctant to raise its target rates in response to supply disruptions. At the same time, the Fed’s own policy actions contributed massively to demand-side price pressures. Also neglected is the reality that higher inflation expectations propel inflation on the demand side, even when it originates on the supply side.

Via Rate Targeting

At a more nuts and bolts level, today the Fed’s operating approach is to control money growth by setting target levels for several key short-term interest rates (eschewing a more direct approach to the problem). This relies on price controls (short-term interest rates being the price of liquidity) rather than allowing market participants to determine the rates at which available liquidity is allocated. Thus, in the short run, the Fed puts itself into the position of supplying whatever liquidity is demanded at the rates it targets. The Fed makes periodic adjustments to these rate targets in an effort to loosen or tighten money, but it can be misdirected in a world of high debt ratios in which rates themselves drive the growth of government borrowing. For example, if higher rates are intended to reduce money growth and inflation, but also force greater debt issuance by the Treasury, the approach might backfire.

Policy Coordination

While nominally independent, the Fed knows that a particular monetary policy stance is more likely to achieve its objectives if fiscal policy is not working at cross purposes. For example, tight monetary policy is more likely to succeed in slowing inflation if the federal government avoids adding to budget deficits. Bond investors know that explosive increases in federal debt are unlikely to be repaid out of future surpluses, so some other mechanism must come into play to achieve real long-term balance in the valuation of debt with debt payments. Only inflation can bring the real value of outstanding Treasury debt into line. Continuing to pile on new debt simply makes the Fed’s mandate for price stability harder to achieve.

Who Calls the Tune?

The Fed has often succumbed to pressure to monetize federal deficits in order to keep interest rates from rising. This obviously undermines perceptions of Fed independence. A willingness to purchase large amounts of Treasury bills and bonds from the public while fiscal deficits run rampant gives every appearance that the Fed simply serves as the Treasury’s printing press, monetizing government deficits. A central bank that is a slave to the spending proclivities of politicians cannot make credible inflation commitments, and cannot effectively conduct counter-cyclical policy.

Stable Policy, Stable Economy

Activist policies for economic stabilization are often perversely destabilizing for a variety of reasons. Good timing requires good forecasts, but economic forecasting is notoriously difficult. The magnitude and timing of fiscal initiatives are usually wrong, and this is compounded by wasteful planning, allocative dysfunction, and a general absence of restraint among political leaders as well as the federal bureaucracy..

Predicting the effects of monetary policy is equally difficult and, more often than not, leads to episodes of over- and under-adjustment. In addition, the wrong targets, the wrong operating approach, and occasional displays of subservience to fiscal pressure undermine successful stabilization. All of these issues lead to doubts about the credibility of policy commitments. Stated intentions are looked upon with doubt, increasing uncertainty and setting in motion behaviors that lead to undesirable economic consequences.

The best policies are those that can be relied upon by private actors, both as a matter of fulfilling expectations and avoiding destabilization. Federal budget policy should promote stability, but that’s not achievable institutions unable to constrain growth in spending and deficits. Budget balance would promote stability and should be the norm over business cycles, or perhaps over periods as long as typical 10-year budget horizons. Stimulus and restraint on the fiscal side should be limited to the effects of so-called automatic stabilizers, such as tax rates and unemployment compensation. On the monetary side, the Fed would do more to stabilize the economy by adopting formal rules, whether a constant rate of money growth or symmetric targeting of nominal GDP.

The Federal Reserve just announced tighter monetary policy in an attempt to reduce inflationary pressures. First, it raised its target range for the federal funds rate (on overnight loans between banks) by 0.5%. The new range is 0.75% – 1%. Second, on June 1, the Fed will begin taking steps to reduce the size of its $9 trillion portfolio of securities. These holdings were acquired during periods of so-called quantitative easing (QE) beginning in 2008, including dramatic expansions in 2020-21. A shorthand reference for this portfolio is simply the Fed’s “balance sheet”. It includes government debt the Fed has purchased as well as privately-issued mortgage-backed securities (MBS).

What Is This Balance Sheet You Speak Of?

Talk of the Fed’s balance sheet seems to mystify lots of people. During the 2008 financial crisis, the Fed began to inject liquidity into the economy by purchasing large amounts of assets to be held on its balance sheet. This was QE. It’s scope was unprecedented and a departure from the Fed’s pre-crisis reliance on interest rate targeting. QE had the effect of increasing bank reserves, which raised the possibility of excessive money supply growth. That’s when the Fed began to pay interest to banks on reserves, so they might be content to simply hold some of the reserves over and above what they are required to hold, rather than using all of that excess to support new loans and deposits (and thus money growth). However, that interest won’t stop banks from lending excess reserves if better opportunities present themselves.

The Fed has talked about reducing, “normalizing”, or “tapering” its balance sheet for some time, but it only recently stopped adding to it. With inflation raging and monetary policy widely viewed as too “dovish”, analysts expected the Fed to stop reinvesting proceeds from maturing securities, which amounts to about $95 billion per month. That would shrink or “taper” the balance sheet at a rate of about $1.1 trillion per year. Last week the Fed decided to cap the “runoff” at $47.5 billion per month for the first three months, deferring the $95 billion pace until September. Monetary policy “hawks” were disappointed by this announcement.

Monetizing Government

So, one might ask, what’s the big deal? Why must the Fed taper its securities holdings? Well, first, the rate of inflation is far above the Fed’s target range, and it’s far above the “average Joe’s” comfort range. Inflation imposes significant costs on the economy and acts as a regressive form of taxation, harming the poor disproportionately. To the extent that the Fed’s huge balance sheet (and the corresponding bank reserves) are supporting incremental money growth and fueling inflation, the balance sheet must be reduced.

In that connection, the Fed’s investment in government debt represents monetized federal debt. That means the Fed is essentially printing money to meet the Treasury’s financing needs. Together with profligate spending by the federal government, nothing could do more to convince investors that government debt will never be repaid via future budget surpluses. This dereliction of the government’s “full faith and credit”, and the open-armed acceptance of the inflation tax as a financing mechanism (à la Modern Monetary Theory), is the key driver of fiscal inflation. Reducing the balance sheet would represent de-monetization, which might help to restore faith in the Fed’s ability to push back against fiscal recklessness.

Buyer of First Resort

Perhaps just as critically, the Fed’s heavy investment in government debt and MBS represents an ongoing distortion to the pricing of financial assets and the allocation of capital. Some call this interference in the “price discovery process”. That’s because the Fed has represented a market-altering presence, a willing and inelastic buyer of government debt and MBS. Given that presence, it’s difficult for buyers and sellers to discern the true values of alternative uses of capital, or to care.

QE was, among other things, a welcome institutional development for the U.S. Treasury and for those who fancy that fresh money printing is an ever-valid form of government payment for scarce resources. The Fed’s involvement also means that other potential buyers of Treasury debt need not worry about interest rate risk, making public debt relatively more attractive than private debt. This is a dimension of the “crowding out” phenomenon, whereby the allocation of capital and flows of real resources between public and private uses are distorted.

The Fed’s presence as a buyer of MBS depresses mortgage rates and makes mortgage lending less risky for lenders and investors. As a result, it encourages an over-investment in housing and escalating home prices. This too distorts the allocation of capital and real resources, at the margin, toward housing and away from uses with greater underlying value.

Conclusion

The magnitude of the Fed’s balance sheet is an ongoing testament to an increasingly dominant role of central authorities in the economy. In this case, the Fed has served as a conduit for the inflation tax. In addition, it has unwittingly facilitated crowding out of private capital investment. The Fed’s purchases of MBS have distorted the incentives (and demand) for residential investment. These are subtle effects that the average citizen might not notice, just as one might not notice the early symptoms of a debilitating disease. The long-term consequences of the Fed’s QE activities, including the inflation tax and distorted allocations of capital, are all too typical of failures of government intervention and attempts at central planning. But don’t expect anyone at the Fed to admit it.