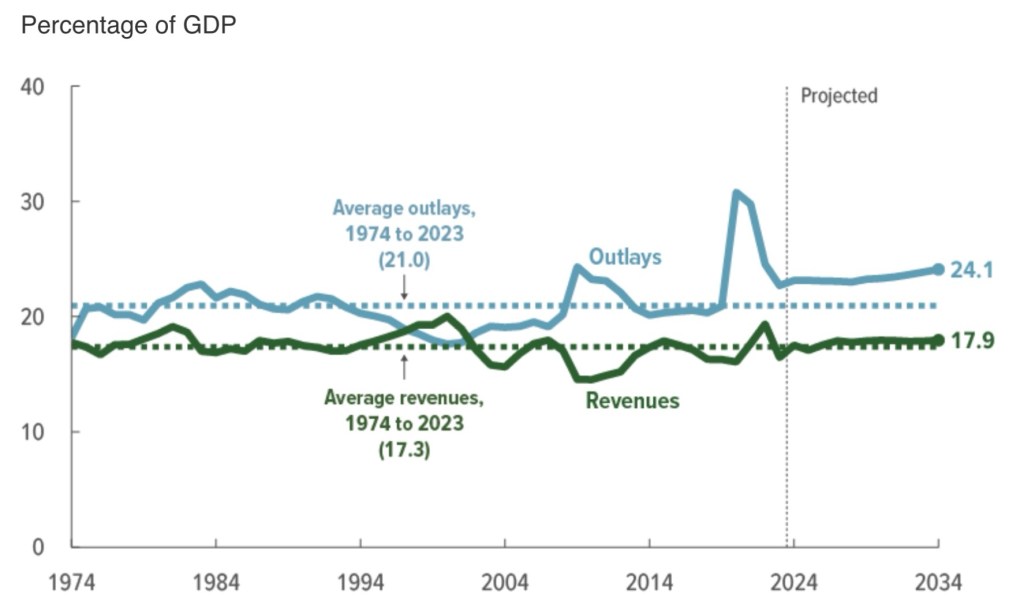

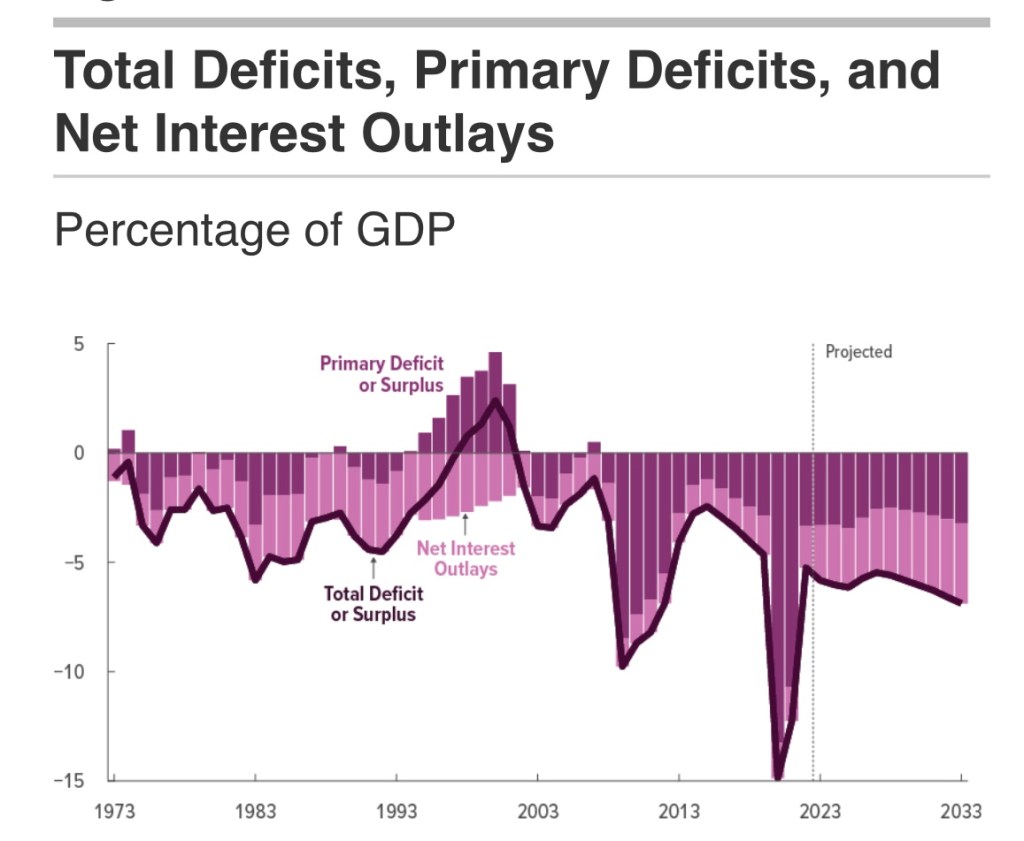

The chart above makes a convincing case that we have a spending problem at the federal level. Really, we’ve had a spending problem for a long time. But at least tax revenue today remains reasonably well-aligned with its 50-year historical average as a share of GDP. Not spending. Even larger deficits opened up during the pandemic and they haven’t returned to pre-pandemic levels.

We’ve seen Joe Biden break spending records. His initiatives, often with questionable merit, have included the $1.8 trillion American Rescue Plan and the nearly $0.8 trillion Infrastructure Investment and Jobs Act, along with several other significant spending initiatives such as the Promise to Address Comprehensive Toxics Act and the subsidy-laden CHIPS Act. Meanwhile, emergency spending has become a regular occurrence on Biden’s watch. More recently, he’s made repeated efforts to forgive massive amounts of student loans despite the Supreme Court’s clear ruling that such gifts are unconstitutional.

Indeed, while Biden keeps pretty busy spinning tales of his days driving an 18-wheeler, cannibals devouring his Uncle Bosie Finnegan, his upbringing in black churches, synagogues, or in the Puerto Rican community, he still finds time to dream up ways for the government to spend money it doesn’t have. Or his kindly puppeteers do.

Biden’s New Budget

Eric Boehm expressed wonderment at Biden’s fiscal 2025 budget not long after its release in March. He was also mystified by the gall it took to produce a “fact sheet” in which the White House congratulated itself on fiscal responsibility. That’s how this Administration characterizes deficits projected at $16 trillion over the next ten years. No joke!

Furthermore, the Administration says the record spending will be “paid for”. Well, yes, with tax increases and lots of borrowing! There are a great many fabulist claims made by the White House about the budget. This link from the Office of Management and Budget includes a handy list of propaganda sheets they’ve managed to produce on the virtues of their proposal.

The Congressional Budget Office (CBO) projects ten-year deficits under current law that are $3 trillion higher than Biden’s proposed budget. That’s the basis of the White House’s boast of fiscal restraint. But the difference is basically paid for with a couple of accounting tricks (see below). More charitably, one could say it’s paid for with higher taxes, aided by the assumption of slightly faster economic growth. The latter will be a good trick while undercutting incentives and wages with a big boost to the corporate tax rate.

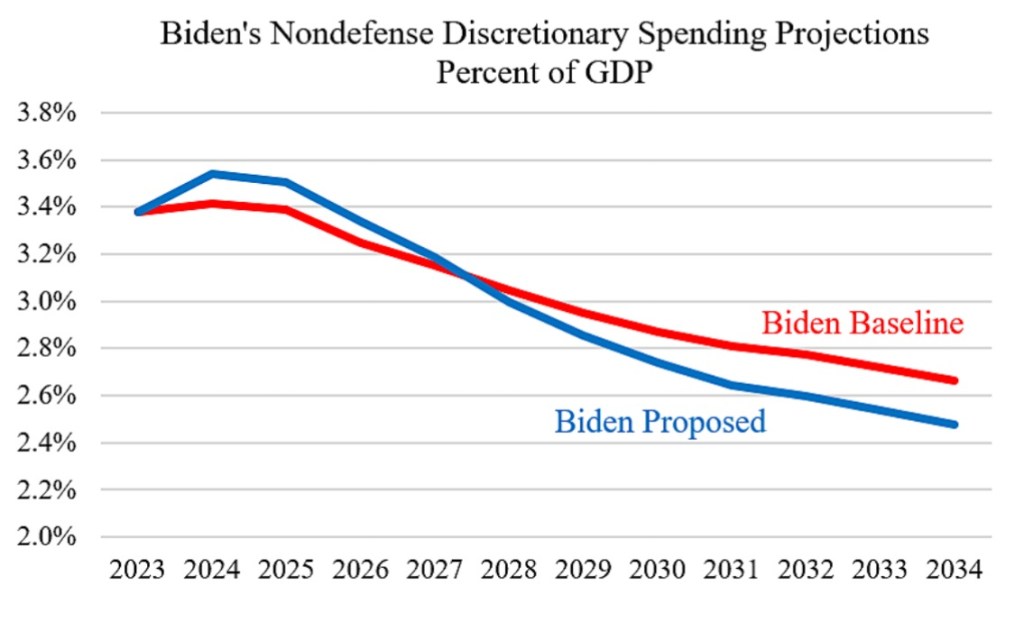

The revenue projected by the While House from those taxes does not come anywhere close to eliminating the gap shown in the CBO’s chart above. Federal spending under Biden’s budget grows at about 4% annually, just a bit slower than nominal GDP. Thus, the federal share of GDP remains roughly constant and only slightly higher than the CBO’s current projection for 2034. Nevertheless, spending relative to GDP would continue at an historically high rate. Over the next decade, it would average more than 3% higher than its 50-year average. That would be about $1.3 trillion in 2034!

Meanwhile, the ratio of tax revenue to GDP under Biden’s proposal, as they project it, would average slightly higher than its 50-year average, reaching a full percentage point above by 2034 (and higher than the CBO baseline). That’s probably optimistic.

There is little real effort in this budget to reduce federal deficits, with Treasury borrowing rates now near 15-year highs. Interest expense has grown to an alarming share of spending. In fact, it’s expected to exceed spending on defense in 2024! Perhaps not coincidentally, the White House assumes a greater decline in interest rates than CBO over the next 10 years.

Treats or Tricks?

The situation is likely worse than the White House depicts, given that its budget incorporates assumptions that look generous to their claim of fiscal restraint. First, they frontload nondefense discretionary spending, allowing Biden to make extravagant promises for the near-term while pushing off steep declines in budget commitments to the out-years. The sharp reductions in this category of spending pares more than $2 trillion from the 10-year deficit. From the link above:

Biden also proposes to restore the expanded the child tax credit — for one year! How handy from a budget perspective: heroically call for an expanded credit (for a year) while avoiding, for the time being, the addition of a couple of trillion to the 10-year deficit.

Code Red

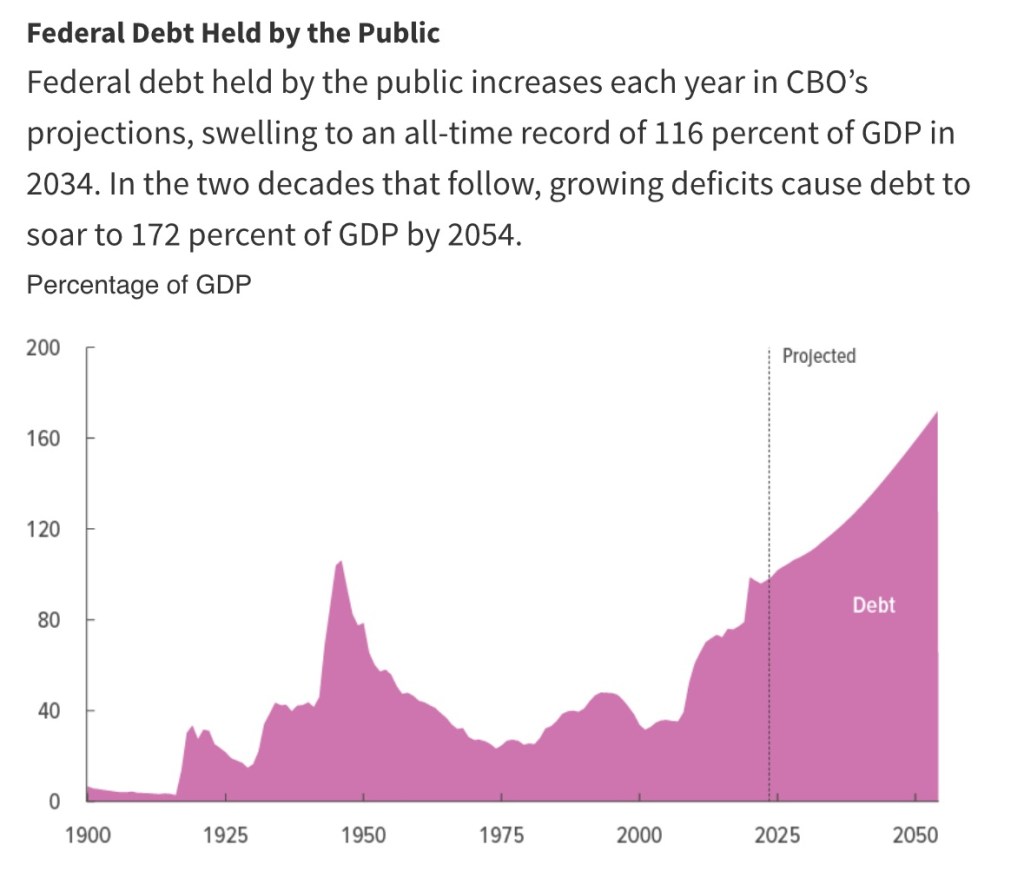

So where does this end? The ratio of federal debt to GDP will resume its ascent after a slight decline from the pandemic high. Here is the CBO’s projection:

The Biden budget shows a relatively stable debt to GDP ratio through 2034 due to the assumptions of slightly faster GDP growth, lower Treasury borrowing rates, and the aforementioned “fiscal restraint”. But don’t count on it!

The government’s growing dominance over real resources will have negative consequences for growth in the long-term. Purely as a fiscal matter, however, it must be paid for in one of three ways: revenue from explicit taxes, federal borrowing, or an implicit tax on the public more commonly known as the inflation tax. The last two are intimately related.

Bond investors always face at least a small measure of default risk even when lending to the U.S. Treasury. There is almost no chance the government would ever default outright by failing to pay interest or principal when due. However, investors hold an expectation that the value of their bonds will erode in real terms due to inflation. To compensate, they demand an “inflation premium” in the interest rate they earn on Treasury bonds. But an upside surprise to inflation would constitute a “soft default” on the real value of their bonds. This occurred during and after the pandemic, and it was triggered by a burgeoning federal deficit.

Brief Mechanics

John Cochrane has explained the mechanism by which acts of fiscal profligacy can be transmitted to the price of goods. The real value of outstanding federal debt cannot exceed the expected real value of future surpluses (a present value summed across positive and negative surpluses). If expected surpluses are reduced via some emergency or shock such that repayment in real terms is less likely, then the real value of government debt must fall. That means either interest rates or the price level must rise, or some combination of the two.

The Federal Reserve can prevent interest rates from rising (by purchasing bonds and increasing the money supply), but that leaves a higher price level as the only way the real value of debt can come into line. In other words, an unexpected increase in the path of federal deficits would be financed by money printing and an inflation tax. The incidence of this unexpected “implicit” tax falls not only to bondholders, but also on the public at large, who suffer an unexpected decline in the purchasing power of their nominal assets and incomes. This in turn tends to free-up real resources for government absorption.

Government Debt Is Risky

It appears that investors expect the future deficits now projected by the CBO (and the White House) to be paid down someday, to some extent, by future surpluses. That might seem preposterous, but markets apparently aren’t surprised by the projected deficits. After all, fiscal policy decisions can change tremendously over the course of a few years. But it still feels like excessive optimism. Whatever the case, Cochrane cautions that the next fiscal emergency, be it a new pandemic, a war, a recession, or some other crisis, is likely to create another huge expansion in debt and a substantial increase price level. Joe Biden doesn’t seem inclined to put us in a position to deal with that risk very effectively. Unfortunately, it’s not clear that Donald Trump will either. And neither seems inclined to seriously address the insolvencies of Social Security and Medicare. If unaddressed, those mandatory obligations will become real crises over the next decade.

Policy activists have long maintained that manipulating government policy can stabilize the economy. In other words, big spending initiatives, tax cuts, and money growth can lift the economy out of recessions, or budget cuts and monetary contraction can prevent overheating and inflation. However, this activist mirage burned away under the light of experience. It’s not that fiscal and monetary policy are powerless. It’s a matter of practical limitations that often cause these tools to be either impotent or destabilizing to the economy, rather than smoothing fluctuations in the business cycle.

The macroeconomics classes seem like yesterday: Keynesian professors lauded the promise of wise government stabilization efforts: policymakers could, at least in principle, counter economic shocks, particularly on the demand side. That optimistic narrative didn’t end after my grad school days. I endured many client meetings sponsored by macro forecasters touting the fine-tuning of fiscal and monetary policy actions. Some of those economists were working with (and collecting revenue from) government policymakers, who are always eager to validate their pretensions as planners (and saviors). However, seldom if ever do forecasters conduct ex post reviews of their model-spun policy scenarios. In fairness, that might be hard to do because all sorts of things change from initial conditions, but it definitely would not be in their interests to emphasize the record.

In this post I attempt to explain why you should be skeptical of government stabilization efforts. It’s sort of a lengthy post, so I’ve listed section headings below in case readers wish to scroll to points of most interest. Pick and choose, if necessary, though some context might get lost in the process.

Expectations Change the World

Fiscal Extravagance

Multipliers In the Real World

Delays

Crowding Out

Other Peoples’ Money

Tax Policy

Monetary Policy

Boom and Bust

Inflation Targeting

Via Rate Targeting

Policy Coordination

Who Calls the Tune?

Stable Policy, Stable Economy

Expectations Change the World

There were always some realists in the economics community. In May we saw the passing of one such individual: Robert Lucas was a giant intellect within the economics community, and one from whom I had the pleasure of taking a class as a graduate student. He was awarded the Nobel Prize in Economic Science in 1995 for his applications of rational expectations theory and completely transforming macro research. As Tyler Cowen notes, Keynesians were often hostile to Lucas’ ideas. I remember a smug classmate, in class, telling the esteemed Lucas that an important assumption was “fatuous”. Lucas fired back, “You bastard!”, but proceeded to explain the underlying logic. Cowen uses the word “charming” to describe the way Lucas disarmed his critics, but he could react strongly to rude ignorance.

Lucas gained professional fame in the 1970s for identifying a significant vulnerability of activist macro policy. David Henderson explains the famous “Lucas Critique” in the Wall Street Journal:

“… because these models were from periods when people had one set of expectations, the models would be useless for later periods when expectations had changed. While this might sound disheartening for policy makers, there was a silver lining. It meant, as Lucas’s colleague Thomas Sargent pointed out, that if a government could credibly commit to cutting inflation, it could do so without a large increase in unemployment. Why? Because people would quickly adjust their expectations to match the promised lower inflation rate. To be sure, the key is government credibility, often in short supply.”

Non-credibility is a major pitfall of activist macro stabilization policies that renders them unreliable and frequently counterproductive. And there are a number of elements that go toward establishing non-credibility. We’ll distinguish here between fiscal and monetary policy, focusing on the fiscal side in the next several sections.

Fiscal Extravagance

We’ve seen federal spending and budget deficits balloon in recent years. Chronic and growing budget deficits make it difficult to deliver meaningful stimulus, both practically and politically.

The next chart is from the most recent Congressional Budget Office (CBO) report. It shows the growing contribution of interest payments to deficit spending. Ever-larger deficits mean ever-larger amounts of debt on which interest is owed, putting an ever-greater squeeze on government finances going forward. This is particularly onerous when interest rates rise, as they have over the past few years. Both new debt is issued and existing debt is rolled over at higher cost.

Relief payments made a large contribution to the deficits during the pandemic, but more recent legislation (like the deceitfully-named Inflation Reduction Act) piled-on billions of new subsidies for private investments of questionable value, not to mention outright handouts. These expenditures had nothing to do with economic stabilization and no prayer of reducing inflation. Pissing away money and resources only hastens the debt and interest-cost squeeze that is ultimately unsustainable without massive inflation.

Hardly anyone with future political ambitions wants to address the growing entitlements deficit … but it will catch up with them. Social Security and Medicare are projected to exhaust their respective trust funds in the early- to mid-2030s, which will lead to mandatory benefit cuts in the absence of reform.

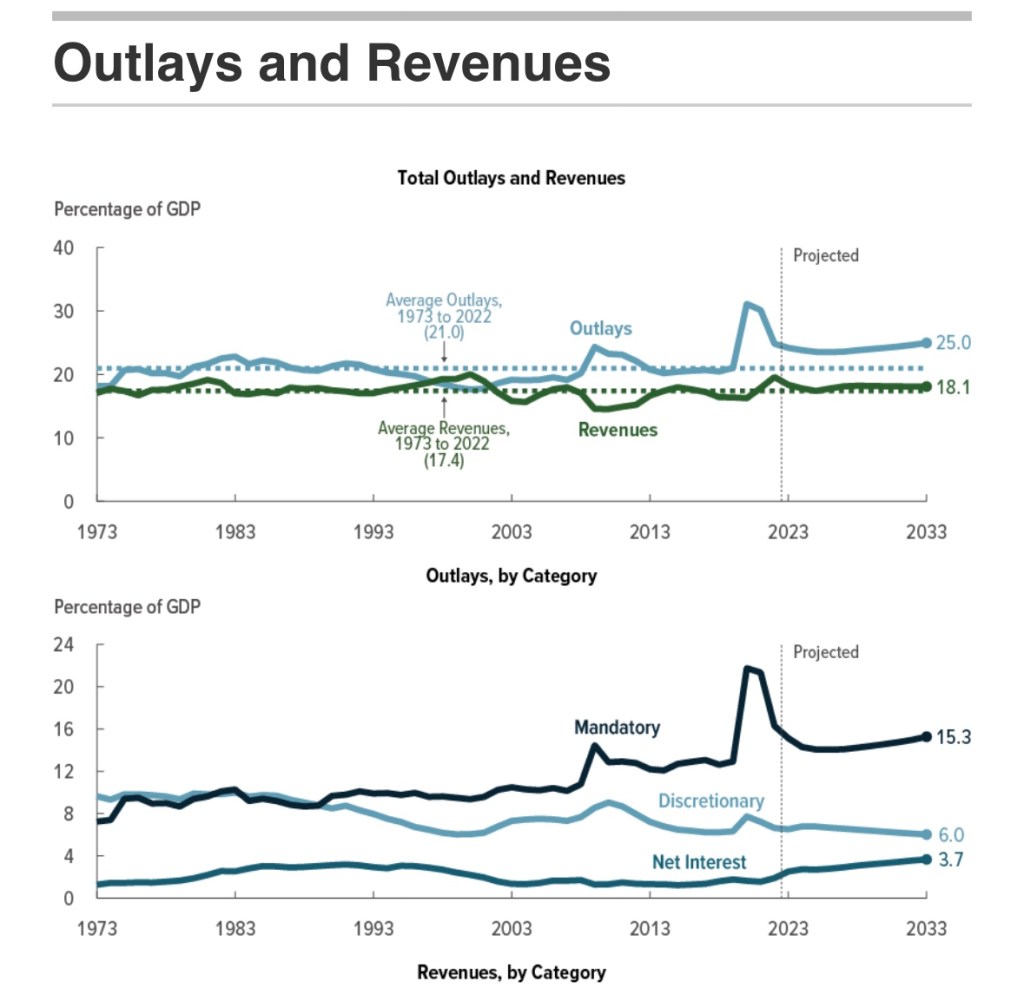

If it still isn’t obvious, the real problem driving the budget imbalance is spending, not revenue, as the next CBO chart demonstrates. The “emergency” pandemic measures helped precipitate our current stabilization dilemma. David Beckworth tweets that the relief measures “spurred a rapid recovery”, though I’d hasten to add that a wave of private and public rejection of extreme precautions in some regions helped as well. And after all, the pandemic downturn was exaggerated by misdirected policies including closures and lockdowns that constrained both the demand and supply sides. Beckworth acknowledges the relief measures “propelled inflation”, but the pandemic also seemed to leave us on a permanently higher spending path. Again, see the first chart below.

The second chart below shows that non-discretionary spending (largely entitlements) and interest outlays are how we got on that path. The only avenue for countercyclical spending is discretionary expenditures, which constitute an ever-smaller share of the overall budget.

We’ve had chronic deficits for years, but we’ve shifted to a much larger and continuing imbalance. With more deficits come higher interest costs, especially when interest rates follow a typical upward cyclical pattern. This creates a potentially explosive situation that is best avoided via fiscal restraint.

Putting other doubts about fiscal efficacy aside, it’s all but impossible to stimulate real economic activity when you’ve already tapped yourself out and overshot in the midst of a post-pandemic economic expansion.

Multipliers In the Real World

So-called spending multipliers are deeply beloved by Keynesians and pork-barrel spenders. These multipliers tell us that every dollar of extra spending ultimately raises income by some multiple of that dollar. This assumes that a portion of every dollar spent by government is re-spent by the recipient, and a portion of that is re-spent again by another recipient. But spending multipliers are never what they’re cracked up to be for a variety of reasons. (I covered these in“Multipliers Are For Politicians”, and also see this post.) There are leakages out of the re-spending process (income taxes, saving, imports), which trim the ultimate impact of new spending on income. When supply constraints bind on economic activity, fiscal stimulus will be of limited power in real terms.

If stimulus is truly expected to be counter-cyclical and transitory, as is generally claimed, then much of each dollar of extra government spending will be saved rather than spent. This is the lesson of the permanent income hypothesis. It means greater leakages from the re-spending stream and a lower multiplier. We saw this with the bulge in personal savings in the aftermath of pandemic relief payments.

Another side of this coin, however, is that cutting checks might be the government’s single-most efficient activity in execution, but it can create massive incentive problems. Some recipients are happy to forego labor market participation as long as the government keeps sending them checks, but at least they spend some of the income.

Delays

Another unappreciated and destabilizing downside of fiscal stimulus is that it often comes too late, just when the economy doesn’t need stimulus. That’s because a variety of delays are inherent in many spending initiatives: legislative, regulatory, legal challenges, planning and design, distribution to various spending authorities, and final disbursement. As I noted here:

“Even government infrastructure projects, heralded as great enhancers of American productivity, are often subject to lengthy delays and cost overruns due to regulatory and environmental rules. Is there any such thing as a federal ‘shovel-ready’ infrastructure project?”

Crowding Out

The supply of savings is limited, but when government borrows to fund deficits, it directly competes with private industry for those savings. Thus, funds that might otherwise pay for new plant, equipment, and even R&D are diverted to uses that should qualify as government consumption rather than long-term investment. Government competition for funds “crowds-out” private activity and impedes growth in the economy’s productive capacity. Thus, the effort to stimulate economic activity is self-defeating in some respects.

Other Peoples’ Money

Government doesn’t respond to price signals the way self-interested private actors do. This indifference leads to mis-allocated resources and waste. It extends to the creation of opportunities for graft and corruption, typically involving diversion of resources into uses that are of questionable productivity (corn ethanol, solar and wind subsidies).

Consider one other type of policy action perceived as counter-cyclical: federal bailouts of failing financial institutions or other troubled businesses. These rescues prop up unproductive enterprises rather than allowing waste to be flushed from the system, which should be viewed as a beneficial aspect of recession. The upshot is that too many efforts at economic stabilization are misdirected, wasteful, ill-timed, and pro-cyclical in impact.

Tax Policy

Like stabilization efforts on the spending side, tax changes may be badly timed. Tax legislation is often complex and can take time for consumers and businesses to adjust. In terms of traditional multiplier analysis, the initial impact of a tax change on spending is smaller than for expenditures, so tax multipliers are smaller. And to the extent that a tax change is perceived as temporary, it is made less effective. Thus, while changes in tax policy can have powerful real effects, they suffer from some of the same practical shortcomings for stabilization as changes in spending.

However, stimulative tax cuts, if well crafted, can boost disposable incomes and improve investment and work incentives. As temporary measures, that might mean an acceleration of certain kinds of activity. Tax increases reduce disposable incomes and may blunt incentives, or prompt delays in planned activities. Thus, tax policy may bear on the demand side as well as the timing of shifts in the economy’s productive potential or supply side.

Monetary Policy

Monetary policy is subject to problems of its own. Again, I refer to practical issues that are seemingly impossible for policy activists to overcome. Monetary policy is conducted by the nation’s central bank, the Federal Reserve (aka, the Fed). It is theoretically independent of the federal government, but the Fed operates under a dual mandate established by Congress to maintain price stability and full employment. Therein lies a basic problem: trying to achieve two goals that are often in conflict with a single policy tool.

Make no mistake: variations in money supply growth can have powerful effects. Nevertheless, they are difficult to calibrate due to “long and variable lags” as well as changes in money “velocity” (or turnover) often prompted by interest rate movements. Excessively loose money can lead to economic excesses and an overshooting of capacity constraints, malinvestment, and inflation. Swinging to a tight policy stance in order to correct excesses often leads to “hard landings”, or recession.

Boom and Bust

The Fed fumbled its way into engineering the Great Depression via excessively tight monetary policy. “Stop and go” policies in the 1970s led to recurring economic instability. Loose policy contributed to the housing bubble in the 2000s, and subsequent maladjustments led to a mortgage crisis (also see here). Don’t look now, but the inflationary consequences of the Fed’s profligacy during the pandemic prompted it to raise short-term interest rates in the spring of 2022. It then acted with unprecedented speed in raising rates over the past year. While raising rates is not always synonymous with tightening monetary conditions, money growth has slowed sharply. These changes might well lead to recession. Thus, the Fed seems given to a pathology of policy shifts that lead to unintentional booms and busts.

Inflation Targeting

The Fed claims to follow a so-called flexible inflation targeting policy. In reality, it has reacted asymmetrically to departures from its inflation targets. It took way too long for the Fed to react to the post-pandemic surge in inflation, dithering for months over whether the surge was “transitory”. It wasn’t, but the Fed was reluctant to raise its target rates in response to supply disruptions. At the same time, the Fed’s own policy actions contributed massively to demand-side price pressures. Also neglected is the reality that higher inflation expectations propel inflation on the demand side, even when it originates on the supply side.

Via Rate Targeting

At a more nuts and bolts level, today the Fed’s operating approach is to control money growth by setting target levels for several key short-term interest rates (eschewing a more direct approach to the problem). This relies on price controls (short-term interest rates being the price of liquidity) rather than allowing market participants to determine the rates at which available liquidity is allocated. Thus, in the short run, the Fed puts itself into the position of supplying whatever liquidity is demanded at the rates it targets. The Fed makes periodic adjustments to these rate targets in an effort to loosen or tighten money, but it can be misdirected in a world of high debt ratios in which rates themselves drive the growth of government borrowing. For example, if higher rates are intended to reduce money growth and inflation, but also force greater debt issuance by the Treasury, the approach might backfire.

Policy Coordination

While nominally independent, the Fed knows that a particular monetary policy stance is more likely to achieve its objectives if fiscal policy is not working at cross purposes. For example, tight monetary policy is more likely to succeed in slowing inflation if the federal government avoids adding to budget deficits. Bond investors know that explosive increases in federal debt are unlikely to be repaid out of future surpluses, so some other mechanism must come into play to achieve real long-term balance in the valuation of debt with debt payments. Only inflation can bring the real value of outstanding Treasury debt into line. Continuing to pile on new debt simply makes the Fed’s mandate for price stability harder to achieve.

Who Calls the Tune?

The Fed has often succumbed to pressure to monetize federal deficits in order to keep interest rates from rising. This obviously undermines perceptions of Fed independence. A willingness to purchase large amounts of Treasury bills and bonds from the public while fiscal deficits run rampant gives every appearance that the Fed simply serves as the Treasury’s printing press, monetizing government deficits. A central bank that is a slave to the spending proclivities of politicians cannot make credible inflation commitments, and cannot effectively conduct counter-cyclical policy.

Stable Policy, Stable Economy

Activist policies for economic stabilization are often perversely destabilizing for a variety of reasons. Good timing requires good forecasts, but economic forecasting is notoriously difficult. The magnitude and timing of fiscal initiatives are usually wrong, and this is compounded by wasteful planning, allocative dysfunction, and a general absence of restraint among political leaders as well as the federal bureaucracy..

Predicting the effects of monetary policy is equally difficult and, more often than not, leads to episodes of over- and under-adjustment. In addition, the wrong targets, the wrong operating approach, and occasional displays of subservience to fiscal pressure undermine successful stabilization. All of these issues lead to doubts about the credibility of policy commitments. Stated intentions are looked upon with doubt, increasing uncertainty and setting in motion behaviors that lead to undesirable economic consequences.

The best policies are those that can be relied upon by private actors, both as a matter of fulfilling expectations and avoiding destabilization. Federal budget policy should promote stability, but that’s not achievable institutions unable to constrain growth in spending and deficits. Budget balance would promote stability and should be the norm over business cycles, or perhaps over periods as long as typical 10-year budget horizons. Stimulus and restraint on the fiscal side should be limited to the effects of so-called automatic stabilizers, such as tax rates and unemployment compensation. On the monetary side, the Fed would do more to stabilize the economy by adopting formal rules, whether a constant rate of money growth or symmetric targeting of nominal GDP.

Government budget negotiations never fail to frustrate anyone of a small-government persuasion. We have a huge, ongoing federal budget deficit. Spending’s gone bat-shit out of control over the past several years and too few in Congress are willing to do anything about it. Democrats would rather see politically-targeted tax increases. While some Republicans advocate spending cuts, the focus is almost entirely on discretionary spending. Meanwhile, the entitlement state is off the table, including Social Security reform.

Fiscal Indiscretion

Sadly, non-discretionary outlays (entitlements) today make a much larger contribution to the deficit than discretionary spending. That includes the programs like Social Security (SS) and Medicare, in which spending levels are programmatic and not subject to annual appropriations by Congress. When these programs were instituted there were a large number of workers relative to retirees, so tax contributions exceeded benefit levels for many decades. The revenue excesses were placed into “trust funds” and invested in Treasury debt. In other words, surpluses under non-discretionary SS and Medicare programs were used to finance discretionary spending!

The aging of Baby Boomers ultimately led to a reversal in the condition of the trust funds. Fewer workers relative to retirees meant that annual payroll tax collections were not adequate to cover annual benefits, and that meant drawing down the trust funds. Current projections by the system trustees call for the SS Trust Fund to be exhausted by 2035. Once that occurs, benefits will automatically be reduced by roughly 20% unless Congress acts to shore up the system before then.

A Few Proposals

I’ve written about the need for SS reform on several occasions (though the first article at that link is not germane here). It seems imperative for Congress and the President to address these shortfalls. By all appearances, however, many Republicans have put the issue aside. For his part, Joe Biden has apparently accepted the prospect of an automatic reduction in benefits in 2035, or at least he’s willing to kick that can down the road. He has, however, endorsed taxes on high earners to fund Medicare. Senator John Kennedy (R-LA) suggests raising the retirement age, or at least raise the minimum age at which one may claim benefits (now 62). Senators Bill Cassidy (R-La.) and Angus King (I-Maine) were working on a compromise that would create an investment fund to fortify the system, but the specifics are unclear, as well as how much that would accomplish.

Meanwhile, Senator Bernie Sanders (S-VT) proposes to expand SS benefits by $2,400 a year and add funding by extending payroll taxes to earners above the current limit of $160,000. Senator Joe Manchin (D-WV) has endorsed the latter as a “quick fix”.

There is also at least oneproposal in Congress to end the practice of taxing a portion of SS benefits as income. I have trouble believing it will gain wide support, despite the clear double-taxation involved.

Then there are always discussions of reducing benefits at higher income levels or even means-testing benefits. In fact, it would be interesting to know what proportion of current benefits actually function as social insurance, as opposed to a universal entitlement. The answer, at least, could serve as a baseline for more fundamental reforms, including changes in the structure of payroll taxes, voluntary lump-sum payouts, and private accounts.

More Radical Views

There are a few prominent voices who claim that SS is sustainable in its current form, but perhaps with a few “no big deal” tax increases. Oh, that’s only about a $1 trillion “deal”, at least for both Medicare and SS. More offensive still are the scare tactics used by opponents of SS reform any time the subject comes up. I’m not aware of any serious reform proposal made over the past two decades that would have affected the benefits of anyone over the age of 55, and certainly no one then-eligible for benefits. Yet that charge is always made: they want to cut your SS benefits! The Democrats made that claim against George W. Bush, torpedoing what might have been a great accomplishment for all. And now, apparently Donald Trump is willing to use such accusations to damage any rival who has ever mentioned reform, including Mike Pence. Will you please cut the crap?

The System

The thing to remember about SS is that it is currently structured as a pay-as-you-go (PAYGO) system, despite the fact that benefits are defined like many creaky private pensions of old. SS benefits in each period are paid out of current “contributions” (i.e., FICO payroll taxes) plus redemptions of government bonds held in the Trust Fund. Contributions today are not “invested” anywhere because they are not enough to pay for current benefits under PAYGO.

The Trust Fund was accumulated during the years when favorable demographics led to greater FICO contributions than benefit payouts. The excess revenue was “invested” in Treasury bonds, which meant it was used to fund deficits in the general budget. It’s been about 15 years since the Trust Fund entered a “draw-down” status, and again, it will be exhausted by 2035.

SSA Says It’s a Good Deal

A participant’s expected “rate of return” on lifetime payroll tax payments depends on several things: lifetime earnings, age at which benefits are first claimed, life expectancy at that time, marital status, relative earning levels within two-earner couples, and the “full retirement age” for the individual’s birth year. Payroll tax payments, by the way, include the employer’s share because that is one of the terms of a hire. A high rate of return is not the same as a high level of benefits, however. In fact, relative to career income, SS has a great deal of progressivity in terms of rates of return, but not much in terms of benefit levels.

The Social Security Administration (SSA) has calculated illustrative real internal rates of return (IRR) for many categories of earners given certain assumptions. (An IRR is a discount rate that equalizes the present value (PV) of a stream of payments and the PV of a stream of payoffs.) The SSA’s most recent update of this exercise was in April 2022. The report references Old Age, Survivors, and Disability Insurance (OASDI), but the focus is exclusively on seniors.

Three basic scenarios were considered: 1) current law, as scheduled, despite its unsustainability; 2) a payroll tax increase from 12.4% (not including the Medicare tax) to 15.96% starting in 2035, when the Trust Fund is exhausted; and 3) a reduction in benefits of 22% starting in 2035.

The authors of the report concludethat “… the real value of OASDI benefits is extraordinarily high.” This theme has been echoed by several other writers, such as here and here. This conclusion is based on a comparison to returns earned by investments that SSA judges to have comparably low risk.

I note here that I’ve made assertions in the past about relative SS returns based on nominal benefits, rather than inflation-adjusted values. Those comparisons to private returns might have seemed drastic because they were expressed in terms of hypothetical future nominal values at the point of retirement. The gaps are not as large in real terms or if we consider SS returns broadly to include those accruing to low career earners. Medium and high earners tend to earn lower hypothetical returns from SS.

A Mixed Bag

SSA’s calculated IRRs are highest for one-earner couples followed by two-earner couples. Single males do relatively poorly due to their higher mortality rates. Low earners do very well relative to higher earners. Earlier birth years are associated with higher IRRs, but these are not as impressive for cohorts who have not yet claimed benefits. The ranges of birth years provided in the report make this a little imprecise, but I’ll focus on those born in 1955 and later.

Of course the returns are highest under the current law hypothetical than for the scenarios involving a benefit reduction or a payroll tax hike. The current law IRRs can be viewed as baselines for other calculations, but otherwise they are irrelevant. The system is technically insolvent and the scheduled benefits under current law can’t be maintained beyond 2034 without steps to generate more revenue or cut benefits. Those steps will reduce IRRs earned by hypothetical SS “assets” whether they take the form of higher payroll taxes, lower benefits, a greater full retirement age, or other measures.

The tax hike doesn’t have much impact on the IRRs of near-term retirees. It falls instead on younger cohorts with some years of employment (and payroll tax payments) remaining. The effect of a cut in benefits is spread more evenly across age cohorts and the reductions in IRRs is somewhat larger.

With higher payroll taxes after 2034, the average IRRs for birth years of 1955+ range from about 0.5% up to about 6.25%. The returns for single females and two-earner couples are roughly similar and fall between those for single males on the low end and one-earner couples on the high end. In all cases, low earners have much higher IRRs than others.

The reduction in benefits produces returns for the 1955+ age cohorts averaging small, negative values for high-earning single men up to 5.5% to 6% for low-earning, one-earner couples.

But On the Whole…

The IRR values reported by SSA are quite variable across cohorts. Individuals or couples with low earnings can usually expect to “earn” real IRRs on their contributions of better than 3% (and above 5% in a few cases). Medium earners can expect real returns from 1% to 3% (and in some cases above 4%). Many of the returns are quite good for a safe “asset”, but not for high earners.

Again, SSA states that these are real returns, though they provide no detail on the ways in which they adjust the components used in their IRR formula to arrive at real returns. Granting the benefit of the doubt, we saw persistently negative real returns on a range of safe assets in the not-very-distant past, so the IRRs are respectable by comparison.

Qualifications

There are many assumptions in the SSA’s analysis that might be construed as drastic simplifications, such as no divorce and remarriage, uniform career duration, and no relationship between earnings and mortality. But it’s easy to be picky. Many of the assumptions discernible from the report seem to be reasonable simplifications in what could otherwise be an unruly analysis. Nonetheless, there are a few assumptions that I believe bias the IRRs upward (and perhaps a few in the other direction).

In fact, SSA is remarkably non-transparent in their explanation of the details. Repeated checking of SSA’s document for clear answers is mostly futile. Be that as it may, I’m forced to give SSA the benefit of the doubt in several respects. One is the reinvestment of cumulative remaining contributions at the IRR throughout the earning career and retirement. A detailed formula with all components and time subscripts would have been nice.

… And Major Doubts

As to my misgivings, first, the IRRs reported by SSA are based on earners who all reach the age of 65. However, roughly 14% – 15% of individuals who live to be of working age die before they reach the age of 65. Most of those deaths occur in the latter part of that range, after many years of contributions and hypothetical compounding. That means the dollar impact of contributions forfeited at death before age 65 is probably larger than the unweighted share of individuals. These individuals pay-in but receive no retirement benefit in SSA’s IRR framework, although some receive disability benefits for a period of time prior to death. It wouldn’t bother my conscience to knock off at least a tenth of the quoted returns for this consideration alone.

A second major concern surrounds the method of calculating benefits and discounted benefits. SSA assumes that benefits continue for the expected life of the claimant as of age 65. If life expectancy is 19 years at age 65, then “expected” benefits are a flat stream of benefit payments for 19 years. Discounting each payment back to age 65 at the IRR yields one side of the present value equality. This constant cash flow (CCF) treatment is likely to overstate the present value of benefits. Instead of CCFs, each payment should be weighted by the probability that the claimant will be alive to receive it with a limit at some advanced age like 100. CCF overcounts present values up to the expected life, but it undercounts present values beyond the expected life because the assumed CCF benefits then are zero!! Weighting benefit payments by the probability of survival to each age produces continuing additions to the PV, but increasing mortality and decaying discount factors become quite substantial beyond expected life, leading to relatively minor additions to PV over that range. The upshot is that the CCFs employed by SSA overstate PVs by front-loading all benefits earlier in retirement. For a given PV of contributions, an overstated PV of benefits requires a higher (and overstated) IRR to restore the PV equality, and this might be a substantial source of upward bias in SSA’s calculations.

Third, when comparing an SS “asset” to private returns, a big difference is that private balances remaining at death become assets of the earner’s estate. Meanwhile, a single beneficiary forfeits their SS benefits at death (except for a small death benefit), while a surviving spouse having lower benefits receives ongoing payments of the decedent’s benefits for life. This consideration, however, in and of itself, means that private plans have a substantial advantage: the “expected” residual at death can be “optimized” at zero or some higher balance, depending on the strength of the earner’s bequest motive.

Finally, in a footnote, the SSA report notes that their treatment of income taxes on Social Security benefits for claimants with higher incomes might bias some of the IRRs upward. That seems quite likely.

It would be difficult to recast SSA’s report based on adjustments for all of these qualifications. However, it’s likely that the IRRs in the SSA report are sharply overstated. That means many more beneficiaries with medium and higher earnings records would have returns in the 0% to 2% range, with more IRRs in the negative range for singles. Low earners, however, might still get returns in a range of 3% to 5%.

The SSA analysis attempts to demonstrate some limits to the risks faced by participants, given the scenarios involving a payroll tax increase or a benefits reduction in 2035. Nevertheless, there are additional political risks to the returns of certain classes of current and future retirees. For example, payroll taxes could be made much more progressive, benefits could be made subject to means testing, or indexing of benefits could be reduced. In fact, there are additional demographic risks that might confront retirees several decades ahead. Continued declines in fertility could further undermine the system’s solvency, requiring more drastic steps to shore up the system. As a hypothetical asset, by no means is SS “risk-free”.

Better Returns

Now let’s consider returns earned by private assets, which represent investments in productive capital. For stocks, these include the sum of all dividends and capital gains (growth in value). For compounding purposes, we assume that all returns are reinvested until retirement. Remember that private returns are much less variable over spans of decades than over durations of a few years. Over the course of 40 year spans (SSA’s career assumption), private returns have been fairly stable historically, and have been high enough to cushion investors from setbacks. Here is Seeking Alpha on annualized returns on the basket of stocks in the S&P 500:

“… the return on the S&P 500 since the beginning of valuation in 1928, is 10.22%, whereas the inflation-adjusted return on the market since that time is 7.01%…”

That real return would generate benefits far in excess of SS for most participants, but it’s not an adequate historical perspective on market performance. A more complete picture of real returns on the S&P, though one that is still potentially flawed, emerges from this calculator, which relies on data from Robert Shiller. The returns extend back to 1871, but the index as we know it today has existed only since 1957. The earlier returns tend to be lower, so these values may be biased:

Real stock market returns over rolling 40-year time spans varied considerably over this longer period. Still, those kind of stock returns would be superior to the IRRs in the SSA report going forward in all but a few cases (and then only for low and very low earners).

Most workers facing a choice between investing at these rates for 40 years, with market risk, and accepting standard SS benefits, uncertain as they are, couldn’t be blamed for choosing stocks. In fact, if we think of contributions to either type of plan as compounding to a hypothetical sum at retirement, the stock investments would produce a “pot of gold” several times greater in magnitude than SS.

However, we still don’t have a fair comparison because workers choosing a stock plan would essentially engage in a kind of dollar-cost averaging over 40 years, meaning that investments would be made in relatively small amounts over time, rather than investing a lump-sum at the beginning. This helps to smooth returns because purchases are made throughout the range of market prices over time, but it also means that returns tend to be lower than the 40-year rolling returns shown above. That’s because the average contribution is invested for only half the time.

To be very conservative, if we assume that real stock returns average between 5% and 6% annually, $1 invested every year would grow to between $131 – $155 after 40 years in constant dollars. At returns of 1% to 2% from SS, which I believe are typical of the IRRs for many medium earners, the cumulative “pot” would grow to $49 – $60. Assuming that the tax treatment of the stock plan was the same as contributions and benefits under SS, the stock plan almost triples your money.

Dealing With the Transition

Privatization covers a range of possible alternatives, all of which would require federal borrowing to pay transition costs. Unfortunately, the Achilles heel in all this is that now is a bad time to propose more federal borrowing, even if it has clear long-term benefits to future retirees.

Todd Henderson in the Wall Street Journal suggests a seeding of capital provided by government at birth along with an insurance program to smooth returns. Another idea is to offer an inducement to delay retirement claims by allowing at least a portion of future benefits to be taken as a lump sum. If retirees can privately invest at a more advantageous return, they might be willing to accept a substantial discount on the actuarial value of their benefits.

In fact, there is evidence that a majority of participants seem to prefer distributions of lump sums because they don’t value their future benefits at anything like that suggested by the SSA analysis. In fact, many participants would defer retirement by 1 – 2 years given a lump sum payment. Discounts and/or delayed claims would reduce the ultimate funding shortfall, but it would require substantial federal borrowing up front.

Additional federal borrowing would also be required under a private option for investing one’s own contributions for future dispersal. The impact of this change on the system’s long-term imbalances would depend on the share of earners willing to opt-out of the traditional SS program in whole or in part. More opt-outs would mean a smaller long-term obligations for the traditional system, but it would be hampered by a costly transition over a number of years. Starting from today’s PAYGO system, someone still has to pay the benefits of current retirees. This would almost certainly mean federal borrowing. Spreading the transition over a lengthy period of time would reduce the impact on credit markets, but the borrowing would still be substantial.

For example, perhaps earners under 35 years of age could begin opting out of a portion or all of the traditional program at their discretion, investing contributions for their own future use. Thus, only a small portion of contributions would be diverted in the beginning, and amounts diverted would contribute to the nation’s available pool of saving, helping to keep borrowing costs in check. By the time these younger earners reach retirement age, nearly all of today’s retirees will have passed on. Ultimately, the average retiree will benefit from higher returns than under the traditional program, but since they won’t be (fully) paying the benefits of current or near-term retirees, the public must come to grips with the bad promises of the past and fund those obligations in some other way: reduced benefits, taxes, or borrowing.

Another objection to privatization is financial risk, particularly for lower-income beneficiaries. Limiting opt-outs to younger earners with adequate time for growth would mitigate this risk, along with a reversion to the traditional program after age 45, for example. Some have proposed limiting opt-outs to higher earners. Bear in mind, however, that the financial risk of private accounts should be weighed against the political and demographic risk already inherent in the existing system.

One more possibility for bridging the transition to private, individually-controlled accounts is to sell federal assets. I have discussed this before in the context of funding a universal basic income (which I oppose). The proceeds of such sales could be used to pay the benefits of current and near-term retirees so as to allow the opt-out for younger workers. Or it could be used to pay off federal debt accumulated in the process. The asset sales would have to proceed at a careful and deliberate pace, perhaps stretching over several decades, but those sales could include everything from the huge number of unoccupied federal buildings to vast tracts of public lands in the west, student loans, oil and gas reserves, and airports and infrastructure such as interstate highways and bridges. Of course, these assets would be more productive in private hands anyway.

The Likely Outcome

Will any such privatization plan ever see the light of day? Probably not, and it’s hard to guess when anything will be done in Washington to address the insolvency we already face. Instead, we’ll see some combination of higher payroll taxes, higher payroll taxes on high earners through graduated payroll tax rates or by lifting the earnings cap, reduced benefits on further retirees, limits on COLAs to low career earners, and means-tested benefits. Some have mentioned funding Social Security shortfalls with income taxes. All of these proposals, with the exception of automatic benefit cuts in 2035, would require acts of Congress.

In advanced civilizations the period loosely called Alexandrian is usually associated with flexible morals, perfunctory religion, populist standards and cosmopolitan tastes, feminism, exotic cults, and the rapid turnover of high and low fads---in short, a falling away (which is all that decadence means) from the strictness of traditional rules, embodied in character and inforced from within. -- Jacques Barzun