A plethora of regulations and subsidies established by governments at all levels is making it more difficult for Americans to move, especially from one state to another. Yale Law Professor David Schleicher identifies these barriers to mobility and writes that they compromise the nation’s ability to match jobs with workers. Thus, these laws beget economic immobility as well. His paper, “Stuck in Place: Law and the Economic Consequences of Residential Stability“, describes a number of the barriers:

“Land-use laws and occupational licensing regimes limit entry into local and state labor markets; differing eligibility standards for public benefits, public employee pension policies, homeownership subsidies, state and local tax regimes, and even basic property law rules reduce exit from states and cities with less opportunity; and building codes, mobile home bans, federal location-based subsidies, legal constraints on knocking down houses and the problematic structure of Chapter 9 municipal bankruptcy all limit the capacity of failing cities to ‘shrink’ gracefully, directly reducing exit among some populations and increasing the economic and social costs of entry limits elsewhere.“

To get a sense of the magnitude of declines in mobility over the past three decades, see Figure 3 in this discussion about mobility by Richard Florida at CityLab. The percentage of homeowners who move declined from almost 10% annually in the late 1980s to about 5% in 2016. The biggest declines occurred during the periods of economic weakness in 2001 and 2008. For renters, the percentage of movers declined from just above 35% in 1988 to less than 24% in 2016.

Workers who might otherwise migrate to jurisdictions with better economic opportunities often cannot do so. Schleicher notes that low-income workers suffer the most from these obstacles, which he divides into entry and exit barriers. Most of the obstacles he cites are compelling, though at times his emphasis veers toward enabling more effective government management of the macroeconomy, which is very unappealing to my libertarian instincts.

Entry Barriers

Schleicher emphasizes two major ways in which entry barriers are created. One is the spread and severity of land use restrictions such as zoning and construction laws, which have become so severe in some areas of the country that they have led to drastic inflation in housing prices. In a review of Schliecher’s paper, Ronald Bailey at Reason.com illustrates the disparities created by this process:

“According to the Trulia real estate market analysis, the median house price in San Francisco is $1.2 million, with a median rent of $4,100 a month; in Youngstown it’s $93,000, with a median rent of $650. In other words, a Youngstown worker who sold his home for full price would receive enough money to rent a place in San Francisco for 22 months.“

The contrast in the economies of these two cities is stark. The San Francisco Bay Area has experienced vibrant job growth over the past several years, while Youngstown has been struggling for decades. Given the difference in housing prices and rents, it would be almost impossible for a worker from Youngstown to pursue an opportunity in the Bay Area without a accepting a severe decline in their standard of living. Joel Kotkin makes a similar point in discussing the high cost of housing in some areas, but his focus is on the difficult prospects for economic mobility and homeownership among Millennials.

The second major entry barrier discussed by Schleicher takes the form of occupational licensing laws. They differ across states but have multiplied since the 1950s. According to Richard Florida (linked above), the share of American workers subject to some form of licensing requirement rose from just 5% in the 1950s to 25% by 2008. Schleicher cites low rates of interstate mobility among professions that typically require a license to practice. Veterans of those occupations tend to have an established book of business, however, so it’s reasonable to expect fewer distant moves. Nevertheless, the cost of obtaining a license in a new state and differing licensure requirements are likely to inhibit the mobility of licensed professionals.

Exit Barriers

One of the most interesting sections in Schleicher’s paper is on exit barriers. Locations are always “sticky” to the extent that local ties exist or develop over time, both between people and between people and local institutions. But some institutions create ties that are severely binding. For example, state and local government employees are often enrolled in defined benefit plans with lengthy vesting periods. Remaining in one system throughout a career can be a huge advantage. Other exit barriers involve differences in eligibility and levels of aid under federal programs managed by states such as Medicaid, Temporary Assistance to Needy Families (TANF), and the Supplemental Nutrition Assistance Program (SNAP — food stamps). Beyond the actual benefits at stake, administrative costs and delays in re-enrollment might hinder a needy family’s attempt to make an interstate move.

Local and state law on property transfers can also impinge on mobility. Real estate transfer taxes in some states certainly create an incentive to stay put. Also, while tax reassessments occur with regularity in most jurisdictions, some impose limits on the amount of the annual change in valuation, requiring a full tax revaluation on resale, so a seller must forego such a tax discount. Rent controls reward renters who stay in place, creating another exit barrier. And rent controls prevent entry as well, as they invariably reduce the supply of quality housing, thereby inflating the rents of vacated apartments available to new residents.

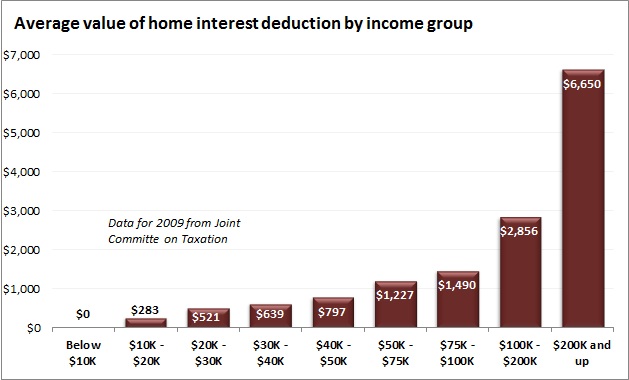

Finally, federal policies designed to encourage homeownership create exit barriers across the country. Ownership of a residence increases the “stickiness” of any locale, but the loss of a mortgage interest income-tax deduction adds to the sacrifice of a move to a rental unit in a more expensive location. So does the interest rate subsidy inherent in the implicit federal guarantee against default on mortgages securitized by Fannie Mae and Freddie Mac. Finally, when local economies are in a state of decline, home prices usually follow. Consequently, owners are likely to suffer reduced or negative equity in their homes and may be “locked in”, unable to pay off their mortgage on a sale, and therefore unable to leave their current residence.

Rent Seeking and Good Intentions

Some of the policies discussed above are the handiwork of those powerful enough to enlist government power in their own self-interest. That includes zoning laws, by which property owners can prevent land uses they deem undesirable. It also includes occupational licensing, a political avenue through which established business interests limit competition by new entrants. Of course, licensure is typically sold to voters as consumer protection, a claim that is often dubious.

Other policies that hinder mobility can be characterized as well-intentioned, like the old-style, defined benefit plans still in use by many state and local governments, or federal subsidies for homeownership. Many such policies are, or have been, promoted on the basis of the obvious gains they create for individuals, with little thought given to the “unseen” but damaging economic consequences. Rent controls fall into this category as well, but are very damaging in the long-term.

The Labor Market Ossified

All of the mobility-limiting policies discussed by Schleicher have a detrimental effect on the performance of labor markets. Workers tend to get stuck in depressed areas, where their value as human resources is diminished even while employers in other markets face limited supplies of qualified labor. This leads to higher structural unemployment, lower growth in output, and more difficulty for the private sector in meeting the needs of consumers than otherwise be possible.

I haven’t dealt with one other national policy dealing explicitly with geographic mobility: immigration. Restrictions on legal immigration and the issuance of green cards are often sought by interests hoping to protect Americans from competition for jobs. Suspending competition is never a good idea, however, as it leads to higher prices and undermines consumer interests. To the extent that businesses face a shortage of qualified talent to fill particular jobs, as is often the case, such restrictive policies are unequivocally damaging to the economy for the same reasons as barriers to interstate migration. Liberalized immigration allows more foreigners with peaceful, productive and often entrepreneurial intent to contribute to the country’s ability to create wealth.

Prescriptions

What can be done to promote interstate mobility? Here is a list that is undoubtedly incomplete: encourage state and local governments to end rent controls; liberalize zoning laws; reevaluate construction restrictions; liberalize occupational licensing; reduce real estate transfer taxes and smooth the timing of tax revaluations. Governments should also transition from defined benefit to defined contribution benefit plans, a step that would also allow them to avoid persistent overoptimism about their ability to meet future pension obligations. As long as states manage federal aid programs and have leeway in setting eligibility requirements and their share of benefits, there will be exit barriers to low-income recipients. Perhaps states should be required to coordinate benefits, with strict time limits, when recipients move interstate to pursue employment opportunities. Finally, subsidies encouraging homeownership should be phased out, including the federal tax deduction for mortgage interest and full privatization of Fannie Mae and Freddie Mac. A neutral stance with respect to homeownership would allow the market to seek an optimal balance in residential property ownership without creating excessive locational anchors.

Schleicher devotes a large part of his paper to the implications of reduced mobility for macroeconomic stabilization policy. In particular, he contends that measures intended to stimulate the economy cannot be as effective when labor supplies are inflexible. That might be true, but I’m loath to endorse Keynesian activism. Still, there is no doubt that geographic stasis of the kind described by Schleicher contributes to immobility in incomes as well. The main conclusion I draw from his paper is that governments ought to be very cautious about interfering in market transactions, even when convinced that their cause is noble. The law of unintended consequences has a way of foiling the best laid plans of social engineers.