Donald Trump’s latest volley against the Federal Reserve accuses the central bank of fixing interest rates at artificially high levels compared to rates in other developed countries. He repeatedly demands that the Fed make a large cut to its federal funds rate target, in the apparent belief that other rates will immediately fall with it. While a highly imperfect analogy, that’s a bit like saying that long-term parking in New York City would be cheaper if only hourly rates were cut to what’s charged in Omaha, and with only favorable consequences. Don’t tell Mamdani!

Trump believes the Fed’s restrictive monetary policy is preventing the economy from achieving its potential under his policies. He also argues that the Fed’s “high-rate” policy is costing the federal government and taxpayers hundreds of billions in excessive interest on federal debt. High rates can certainly impede growth and raise the cost of debt service. The question is whether there is a policy that can facilitate growth and reduce borrowing costs without risking other objectives, most notably price stability.

Delusions of Control

The financial community understands that the Fed does not directly control rates paid by the Treasury on federal debt. The Fed has its most influence on rates at the short end of the maturity spectrum. Rates on longer-term Treasury notes and bonds are subject to a variety of market forces, including expected inflation, the expected future path of federal deficits, and the perceived direction of the economy, to name a few. The Fed simply cannot dictate investor sentiments and expectations, and the ongoing flood of new Treasury debt complicates matters.

Another fundamental lesson for Trump is that cross-country comparisons of interest rates are meaningless outside the context of differing economic conditions. Market interest rates are driven by things that vary from one country to another, such as expected inflation rates, economic policies, currency values, and the strength of the home economy. Differences in rates are always the result of combinations of circumstances and expectations, which can be highly varied.

A Few Comparisons

A few examples will help reinforce this point. Below, I compare the U.S. to a few other countries in terms of recent short-term central bank rate targets and long-term market interest rates. Then we can ask what conditions explain these divergencies. For reference, the current fed funds rate target range is 4.25 – 4.5%, while 10-year Treasury bonds have traded recently at yields in the same range. Current U.S. inflation is roughly 2.5%.

It’s important to remember that markets attempt to price bonds to compensate buyers for expected future inflation. Currently, the10-year “breakeven” inflation implied by indexed Treasury bonds is about 2.35% (but it is closer to 3% at short durations). That means unindexed Treasury bonds yielding 4.4% offer an expected real yield just above 2%. Accounting for expected inflation often narrows the gap between U.S. interest rates and foreign rates, but not always.

Switzerland: The Swiss National Bank maintains a policy rate of 0%; the rate on 10-year Swiss government bonds has been in the 0.5 – 0.7% range. Why can’t we have Swiss-like interest rates in the U.S.? Is it merely intransigence on the part of the Fed, as Trump would have us believe?

No. Inflation in Switzerland is near zero, so in terms of real yields, the gap between U.S. and Swiss rates is closer to 1.4%, rather than 3.8%. But what of the remaining difference? Swiss government debt, even more than U.S. Treasury debt, attracts investors due to the nation’s “safe-haven” status. Also, U.S. yields are elevated by our ballooning federal debt and uncertainties related to trade policy. Economic growth is also somewhat stronger in the U.S., which tends to elevate yields.

These factors give the Fed reason to be cautious about cutting its target rate. It needs evidence that inflation will continue to trend down, and that policy uncertainties can be resolved without reigniting inflation.

Euro Area: The European Central Bank’s (ECB) refinancing rate is now 2.15%. Meanwhile, the 10-year German Bund is yielding around 2.6%, so both short-term and long-term rates in the Euro area are lower than in the U.S. In this case, the difference relative to U.S. rates is not large, nor is it likely attributable to lower expected inflation. Instead, sluggish growth in the EU helps explain the gap. Federal deficits and the ongoing issuance of new Treasury debt also keep U.S. yields higher. Treasury yields may also reflect a premium for volatility due to heavier reliance on foreign investors and private funds, who tend to be price sensitive.

Japan: The Bank of Japan’s (BOJ) policy rate is currently 0.5%. Yields on Japanese 10-year government bonds have recently traded just below 1.5%. Expected inflation in Japan has been around 2.5% this year, which means that real yields are sharply negative. The BOJ has tightened policy to bring inflation down. The nearly 3% gap between U.S. and Japanese bond yields reflects very weak economic growth in Japan. In addition, despite a very high debt to GDP ratio, the depressed value of the yen discourages investment abroad, helping to sustain heavy domestic holdings of government debt.

Blame and Backfire

Trump might well understand the limits of the Fed’s control over interest rates, but if he does, then this is exclusively a case of scapegoating. Cross-country differences in interest rates represent equilibria that balance an array of complex conditions. These range from disparate rates of inflation, the strength of economic growth, currency values, fiscal imbalances, and the character of the investor base. .

Investor expectations obviously play a huge role in all this. A central bank like the Fed cannot dictate long-term yields, and it can do much more harm than good by attempting to push the market where it does not want to go. That type of aggressiveness can spark changes in expectations that undermine policy objectives. It’s childish and destructive to insist that interest rates can and should be as low in the U.S. as in countries facing much different circumstances.

Matt Yglesias tweeted on X that “the bond market does not appear to believe in DOGE”. He included a chart much like the updated one above to “prove” his point. Tyler Cowen posted a link to the tweet on Marginal Revolution, without comment … Cowen surely must know that any such conclusion is premature, especially based on the movement of Treasury yields over the past month (or more, since the market’s evaluation of the DOGE agenda preceded Trump’s inauguration).

Of course, there is a difference between “believing” in DOGE and being convinced that its efforts should have succeeded in reducing interest rates immediately amidst waves of background noise from budget and tax legislation, court challenges, Federal Reserve missteps (this time cutting rates too soon), and the direction of the economy in general.

In this case, perhaps a better way to define success for DOGE is a meaningfully negative impact on the future supply of Treasury debt. Even that would not guarantee a decline in Treasury rates, so the premise of Yglesias’ tweet is somewhat shaky to begin with. Still, all else equal, we’d expect to see some downward pressure on yields if DOGE succeeds in this sense. But we must go further by recognizing that DOGE savings could well be reallocated to other spending initiatives. Then, the savings would not translate into lower supplies of Treasury debt after all.

Certainly, the DOGE team has made progress in identifying wasteful expenditures, inefficiencies, and poor controls on spending. But even if the $55 billion of estimated savings to date is reliable, DOGE has a long way to go to reach Musk’s stated objective of $2 trillion. There are some juicy targets, but it will be tough to get there in 17 more months, when DOGE is to stand down. Still, it’s not unreasonable to think DOGE might succeed in accomplishing meaningful deficit reduction.

But if bond traders have doubts about DOGE, it’s partly because Donald Trump and Elon Musk themselves keep giving them reasons. In my view, Musk and Trump have made a major misstep in toying with the idea of using prospective DOGE savings to fund “dividend checks” of $5,000 for all Americans. These would be paid by taking 20% of the guesstimated $2 trillion of DOGE savings. Musk’s expression of interest in the idea was followed by a bit of clusterfuckery, as Musk walked back his proposal the next day even as Trump jumped on board. PLEASE Elon, don’t give the Donald any crowd-pleasing ideas! And don’t lose sight of the underlying objective to reduce the burden of government and the public debt.

Now, Trump proposes that 60% of the savings accomplished by DOGE be put toward paying for outlays in future years. Sure, that’s deficit reduction, but it may serve to dull the sense that shrinking the federal government is an imperative. The mechanics of this are unclear, but as a first pass, I’d say the gain from investing DOGE savings for a year in low-risk instruments is unlikely to outweigh the foregone savings in interest costs from paying off debt today! Of course, that also depends on the future direction of interest rates, but it’s not a good bet to make with public funds.

Nor can the bond market be comforted by uncertainty surrounding legislation that would not only extend the Trump tax cuts, but will probably include various spending provisions, both cuts and increases. As of now, the mix of provisions that might accompany a deal among GOP factions is very much up in the air.

There is also trepidation about Trump’s aggressive stance toward the Federal Reserve. He promises to replace Jerome Powell as Fed Chairman, but with God knows whom? And Trump jawbones aggressively for lower rates. The Fed’s ill-advised rate cuts in the fall might have been motivated in part by an attempt to capitulate to the then-President Elect.

Trump’s Executive Order to create a sovereign wealth fund (SWF), which I recently discussed here, is probably not the most welcome news to bond investors. All else equal, placing tax or tariff revenue into such a fund would reduce the potential for deficit reduction, to say nothing of the idiocy of additional borrowing to purchase assets.

Finally, Trump has proposed what might later prove to be massive foreign policy trial balloons. Some of these are bound up with the creation of the SWF. They might generate revenue for the government without borrowing (mineral rights in Ukraine? Or Greenland?), but at this point there’s also a chance they’ll create massive funding needs (Gaza development?). Again, Trump seems to be prodding or testing counterparties to various negotiations… prodding diplomacy. It’s unlikely that anything too drastic will come of it from a fiscal perspective, but it probably doesn’t leave bond traders feeling easy.

At this stage, it’s pretty rash to conclude that the bond market “doesn’t believe in DOGE”. In fact, there is no doubt that DOGE is making some progress in identifying potential fraud and inefficiencies. However, bond traders must weigh a wide range of considerations, and Donald Trump has a tendency to kick up dust. Indeed, the so-called DOGE dividend will undermine confidence in debt reduction and bond prices.

The chart above makes a convincing case that we have a spending problem at the federal level. Really, we’ve had a spending problem for a long time. But at least tax revenue today remains reasonably well-aligned with its 50-year historical average as a share of GDP. Not spending. Even larger deficits opened up during the pandemic and they haven’t returned to pre-pandemic levels.

We’ve seen Joe Biden break spending records. His initiatives, often with questionable merit, have included the $1.8 trillion American Rescue Plan and the nearly $0.8 trillion Infrastructure Investment and Jobs Act, along with several other significant spending initiatives such as the Promise to Address Comprehensive Toxics Act and the subsidy-laden CHIPS Act. Meanwhile, emergency spending has become a regular occurrence on Biden’s watch. More recently, he’s made repeated efforts to forgive massive amounts of student loans despite the Supreme Court’s clear ruling that such gifts are unconstitutional.

Indeed, while Biden keeps pretty busy spinning tales of his days driving an 18-wheeler, cannibals devouring his Uncle Bosie Finnegan, his upbringing in black churches, synagogues, or in the Puerto Rican community, he still finds time to dream up ways for the government to spend money it doesn’t have. Or his kindly puppeteers do.

Biden’s New Budget

Eric Boehm expressed wonderment at Biden’s fiscal 2025 budget not long after its release in March. He was also mystified by the gall it took to produce a “fact sheet” in which the White House congratulated itself on fiscal responsibility. That’s how this Administration characterizes deficits projected at $16 trillion over the next ten years. No joke!

Furthermore, the Administration says the record spending will be “paid for”. Well, yes, with tax increases and lots of borrowing! There are a great many fabulist claims made by the White House about the budget. This link from the Office of Management and Budget includes a handy list of propaganda sheets they’ve managed to produce on the virtues of their proposal.

The Congressional Budget Office (CBO) projects ten-year deficits under current law that are $3 trillion higher than Biden’s proposed budget. That’s the basis of the White House’s boast of fiscal restraint. But the difference is basically paid for with a couple of accounting tricks (see below). More charitably, one could say it’s paid for with higher taxes, aided by the assumption of slightly faster economic growth. The latter will be a good trick while undercutting incentives and wages with a big boost to the corporate tax rate.

The revenue projected by the While House from those taxes does not come anywhere close to eliminating the gap shown in the CBO’s chart above. Federal spending under Biden’s budget grows at about 4% annually, just a bit slower than nominal GDP. Thus, the federal share of GDP remains roughly constant and only slightly higher than the CBO’s current projection for 2034. Nevertheless, spending relative to GDP would continue at an historically high rate. Over the next decade, it would average more than 3% higher than its 50-year average. That would be about $1.3 trillion in 2034!

Meanwhile, the ratio of tax revenue to GDP under Biden’s proposal, as they project it, would average slightly higher than its 50-year average, reaching a full percentage point above by 2034 (and higher than the CBO baseline). That’s probably optimistic.

There is little real effort in this budget to reduce federal deficits, with Treasury borrowing rates now near 15-year highs. Interest expense has grown to an alarming share of spending. In fact, it’s expected to exceed spending on defense in 2024! Perhaps not coincidentally, the White House assumes a greater decline in interest rates than CBO over the next 10 years.

Treats or Tricks?

The situation is likely worse than the White House depicts, given that its budget incorporates assumptions that look generous to their claim of fiscal restraint. First, they frontload nondefense discretionary spending, allowing Biden to make extravagant promises for the near-term while pushing off steep declines in budget commitments to the out-years. The sharp reductions in this category of spending pares more than $2 trillion from the 10-year deficit. From the link above:

Biden also proposes to restore the expanded the child tax credit — for one year! How handy from a budget perspective: heroically call for an expanded credit (for a year) while avoiding, for the time being, the addition of a couple of trillion to the 10-year deficit.

Code Red

So where does this end? The ratio of federal debt to GDP will resume its ascent after a slight decline from the pandemic high. Here is the CBO’s projection:

The Biden budget shows a relatively stable debt to GDP ratio through 2034 due to the assumptions of slightly faster GDP growth, lower Treasury borrowing rates, and the aforementioned “fiscal restraint”. But don’t count on it!

The government’s growing dominance over real resources will have negative consequences for growth in the long-term. Purely as a fiscal matter, however, it must be paid for in one of three ways: revenue from explicit taxes, federal borrowing, or an implicit tax on the public more commonly known as the inflation tax. The last two are intimately related.

Bond investors always face at least a small measure of default risk even when lending to the U.S. Treasury. There is almost no chance the government would ever default outright by failing to pay interest or principal when due. However, investors hold an expectation that the value of their bonds will erode in real terms due to inflation. To compensate, they demand an “inflation premium” in the interest rate they earn on Treasury bonds. But an upside surprise to inflation would constitute a “soft default” on the real value of their bonds. This occurred during and after the pandemic, and it was triggered by a burgeoning federal deficit.

Brief Mechanics

John Cochrane has explained the mechanism by which acts of fiscal profligacy can be transmitted to the price of goods. The real value of outstanding federal debt cannot exceed the expected real value of future surpluses (a present value summed across positive and negative surpluses). If expected surpluses are reduced via some emergency or shock such that repayment in real terms is less likely, then the real value of government debt must fall. That means either interest rates or the price level must rise, or some combination of the two.

The Federal Reserve can prevent interest rates from rising (by purchasing bonds and increasing the money supply), but that leaves a higher price level as the only way the real value of debt can come into line. In other words, an unexpected increase in the path of federal deficits would be financed by money printing and an inflation tax. The incidence of this unexpected “implicit” tax falls not only to bondholders, but also on the public at large, who suffer an unexpected decline in the purchasing power of their nominal assets and incomes. This in turn tends to free-up real resources for government absorption.

Government Debt Is Risky

It appears that investors expect the future deficits now projected by the CBO (and the White House) to be paid down someday, to some extent, by future surpluses. That might seem preposterous, but markets apparently aren’t surprised by the projected deficits. After all, fiscal policy decisions can change tremendously over the course of a few years. But it still feels like excessive optimism. Whatever the case, Cochrane cautions that the next fiscal emergency, be it a new pandemic, a war, a recession, or some other crisis, is likely to create another huge expansion in debt and a substantial increase price level. Joe Biden doesn’t seem inclined to put us in a position to deal with that risk very effectively. Unfortunately, it’s not clear that Donald Trump will either. And neither seems inclined to seriously address the insolvencies of Social Security and Medicare. If unaddressed, those mandatory obligations will become real crises over the next decade.

We’re told again and again that government must take action to correct “market failures”. Economists are largely responsible for this widespread view. Our standard textbook treatments of external costs and benefits are constructed to demonstrate departures from the ideal of perfectly competitive market equilibria. This posits an absurdly unrealistic standard and diminishes the power and dramatic success of real-world markets in processing highly dispersed information, allocating resources based on voluntary behavior, and raising human living standards. It also takes for granted the underlying institutional foundations that lead to well-functioning markets and presumes that government possesses the knowledge and ability to rectify various departures from an ideal. Finally, “corrective” interventions are usually exposited in economics classes as if they are costless!

Failed Disgnoses

This brings into focus the worst presumption of all: that government solutions to social and economic problems never fail to achieve their intended aims. Of course that’s nonsense. If defined on an equivalent basis, government failure is vastly more endemic and destructive than market failure.

“According to ancient legend, a Roman emperor was asked to judge a singing contest between two participants. After hearing the first contestant, the emperor gave the prize to the second on the assumption that the second could be no worse than the first. Of course, this assumption could have been wrong; the second singer might have been worse. The theory of market failure committed the same mistake as the emperor. Demonstrating that the market economy failed to live up to the ideals of general competitive equilibrium was one thing, but to gleefully assert that public action could costlessly correct the failure was quite another matter. Unfortunately, much analytical work proceeded in such a manner. Many scholars burst the bubble of this romantic vision of the political sector during the 1960s. But it was [James] Buchanan and Gordon Tullock who deserve the credit for shifting scholarly focus.”

John Cochrane sums up the whole case succinctly in the “punchline” of a recent post:

“The case for free markets never was their perfection. The case for free markets always was centuries of experience with the failures of the only alternative, state control. Free markets are, as the saying goes, the worst system; except for all the others.”

Tracing Failures

We can view the relation between market failure and government failure in two ways. First, we can try to identify market failures and root causes. For example, external costs like pollution cause harm to innocent third parties. This failure might be solely attributable to transactions between private parties, but there are cases in which government engages as one of those parties, such as defense contracting. In other cases government effectively subsidizes toxic waste, like the eventual disposal of solar panels. Another kind of market failure occurs when firms wield monopoly power, but that is often abetted by costly regulations that deliver fatal blows to small competitors.

The second way to analyze the nexus between government and market failures is to first examine the taxonomy of government failure and identify the various damages inflicted upon the operation of private markets. That’s the course I’ll follow below, though by no means is the discussion here exhaustive.

Failures In and Out of Scope

An extensive treatment of government failure was offered eight years ago by William R. Keech and Michael Munger. To start, they point out what everyone knows: governments occasionally perpetrate monstrous acts like genocide and the instigation of war. That helps illustrate a basic dichotomy in government failures:

“… government may fail to do things it should do, or government may do things it should not do.’

Both parts of that statement have numerous dimensions. Failures at what government should do run the gamut from poor service at the DMV, to failure to enforce rights, to corrupt bureaucrats and politicians skimming off the public purse in the execution of their duties. These failures of government are all too common.

What government should and should not do, however, is usually a matter of political opinion. Thomas Jefferson’s axioms appear in a single sentence at the beginning of the Declaration of Independence; they are a tremendous guide to the first principles of a benevolent state. However, those axioms don’t go far in determining the range of specific legal protections and services that should and shouldn’t be provided by government.

Pareto Superiority

Keech and Munger engage in an analytical exercise in which the “should and shouldn’t” question is determined under the standard of Pareto superiority. A state of the world is Pareto superior if at least one person prefers it to the current state (and no one else is averse to it). Coincidentally, voluntary trades in private markets always exploit Pareto superior opportunities, absent legitimate external costs and benefits.

The set of Pareto superior states available to government can be expanded by allowing for side payments or compensation to those who would have preferred the current state. Still, those side payments are limited by the magnitude of the gains flowing to those who prefer the alternative (and if those gains can be redistributed monetarily).

Keech and Munger define government failure as the unexploited existence of Pareto superior states. Of course, by this definition, only a benevolent, omniscient, and omnipotent dictator could hope to avoid government failure. But this is no more unrealistic than the assumptions underlying perfectly competitive market equilibrium from which departure are deemed “market failures” that government should correct. Thus, Keech and Munger say:

“The concept of government failure has been trapped in the cocoon of the theory of perfect markets. … Government failure in the contemporary context means failing to resolve a classic market failure.”

But markets must operate within a setting defined by culture and institutions. The establishment of a social order under which individuals have enforceable rights must come prior to well-functioning markets, and that requires a certain level of state capacity. Keech and Munger are correct that market failure is often a manifestation of government failure in setting and/or enforcing these “rules of the game”.

“The real question is … how the rules of the game should be structured in terms of incentives, property rights, and constraints.”

The Regulatory State and Market Failures

Government can do too little in defining and enforcing rights, and that’s undoubtedly a cause of failure in markets in even the most advanced economies. At the same time there is an undeniable tendency for mission creep: governments often try to do too much. Overregulation in the U.S. and other developed nations creates a variety of market failures. This includes the waste inherent in compliance costs that far exceed benefits; welfare losses from price controls, licensing, and quotas; diversion of otherwise productive resources into rent seeking activity, anti-competitive effects from “regulatory capture”; Chevron-like distortions endemic to the administrative judicial process; unnecessary interference in almost any aspect of private business; and outright corruption and bribe-taking.

Central Planning and Market Failures

Another category of government attempting to “do too much” is the misallocation of resources that inevitably accompanies efforts to pick “winners and losers”. The massive subsidies flowing to investors in various technologies are often misdirected. Many of these expenditures end up as losses for taxpayers, and this is not the only form in which failed industrial planning takes place. A related evil occurs when steps are taken to penalize and destroy industries in political disfavor with thin economic justification.

Other clear examples of government “planning” failure are protectionist laws. These are a net drain on our wealth as a society, denying consumers of free choice and saddling the country with the necessity to produce restricted products at high cost relative to erstwhile trading partners.

There are, of course, failures lurking within many other large government spending programs in areas such as national defense, transportation, education, and agriculture. Many of these programs can be characterized as centrally planning. Not only are some of these expenditures ineffectual, but massive procurement spending seems to invite waste and graft. After all, it’s somebody else’s money.

Redistribution and Market Failures

One might regard redistribution programs as vehicles for the kinds of side payments described by Keech and Munger. Some might even say these are the side payments necessary to overcome resistance from those unable to thrive in a market economy. That reverses the historical sequence of events, however, since the dominant economic role of markets preceded the advent of massive redistribution schemes. Unfortunately, redistribution programs have been plagued by poor design, such as the actuarial nightmare inherent in Social Security and the destructive work incentives embedded in other parts of the social safety net. These are rightly viewed as government failures, and their distortionary effects spill variously into capital markets, labor markets and ultimately product markets.

Taxation and Market Failures

All these public initiatives under which government failures precipitate assorted market failures must be paid for by taxpayers. Therefore, we must also consider the additional effects of taxation on markets and market failures. The income tax system is rife with economic distortions. Not only does it inflict huge compliance costs, but it alters incentives in ways that inhibit capital formation and labor supply. That hampers the ability of input markets to efficiently meet the needs of producers, inhibiting the economy’s productive capacity. In turn, these effects spill into output market failures, with consequent losses in .social welfare. Distortionary taxes are a form of government failure that leads to broad market failures.

Deficits and Market Failure

More often than not, of course, tax revenue is inadequate to fund the entire government budget. Deficit spending and borrowing can make sense when public outlays truly produce long-term benefits. In fact, the mere existence of “risk-free” assets (Treasury debt) across the maturity spectrum might enhance social welfare if it enables improvements in portfolio diversification that outweigh the cost of the government’s interest obligations. (Treasury securities do bear interest-rate risk and, if unindexed, they bear inflation risk.)

Nevertheless, borrowing can reflect and magnify deleterious government efforts to “do too much”, ultimately leading to market failures. Government borrowing may “crowd out” private capital formation, harming economy-wide productivity. It might also inhibit the ability of households to borrow at affordable rates. Interest costs of the public debt may become explosive as they rise relative to GDP, limiting the ability of the public sector to perform tasks that it should *actually* do, with negative implications for market performance.

Inflation and Market Failure

Deficit spending promotes inflation as well. This is more readily enabled when government debt is monetized, but absent fiscal discipline, the escalation of goods prices is the only remaining force capable of controlling the real value of the debt. This is essentially the inflation tax.

Inflation is a destructive force. It distorts the meaning of prices, causes the market to misallocate resources due to uncertainty, and inflicts costs on those with fixed incomes or whose incomes cannot keep up with inflation. Sadly, the latter are usually in lower socioeconomic strata. These are symptoms of market failure prompted by government failure to control spending and maintain a stable medium of exchange.

Conclusion

Markets may fail, but when they do it’s very often rooted in one form of government failure or another. Sometimes it’s an inadequacy in the establishment or enforcement of property rights. It could be a case of overzealous regulation. Or government may encroach on, impede, or distort decisions regarding the provision of goods or services best left to the market. More broadly, redistribution and taxation, including the inflation tax, distort labor and capital markets. The variety of distortions created when government fails at what it should do, or does what it shouldn’t do, is truly daunting. Yet it’s difficult to find leaders willing to face up to all this. Statism has a powerful allure, and too many elites are in thrall to the technocratic scientism of government solutions to social problems and central planning in the allocation of resources.

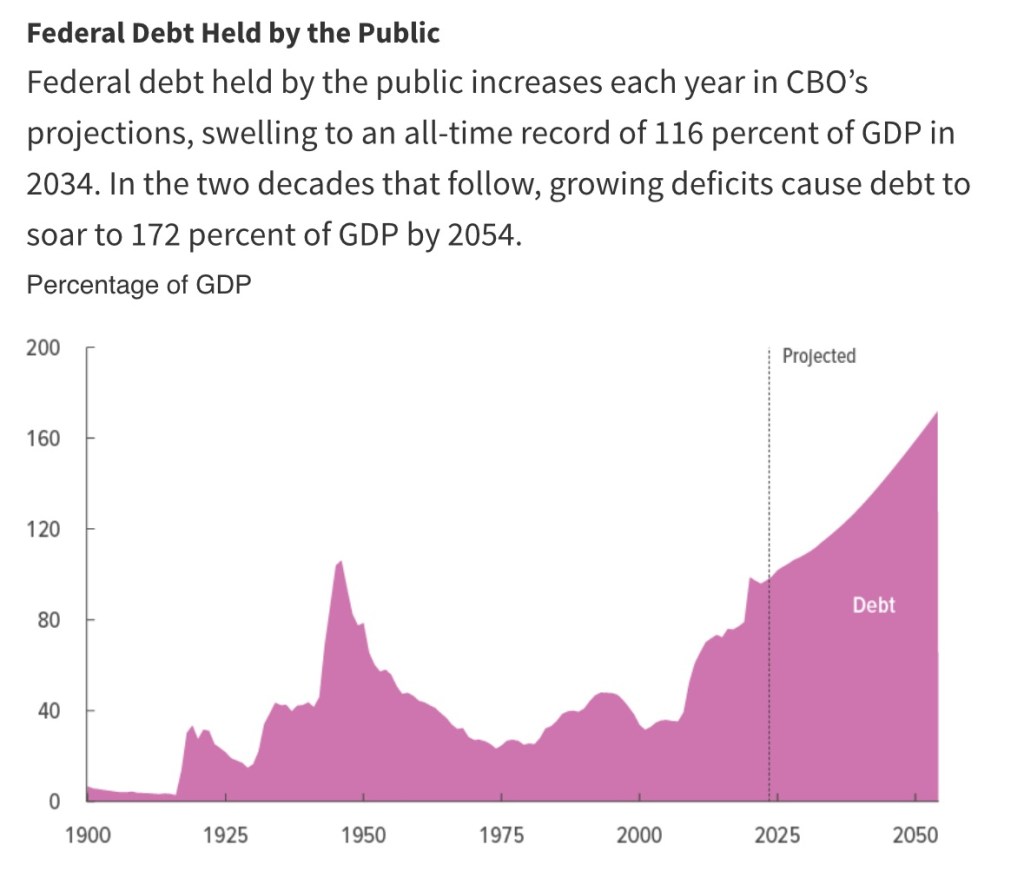

It’s as if people view the debt limit controversy as a political nuisance rather than the stopgap enforcement mechanism for fiscal sanity that it’s intended to be. That’s a lesson in how far we’ve gone toward an unhealthy acceptance of permanent federal deficits. Oh, most people seem to realize the the government’s spending is prodigious and beyond our capacity to collect taxes, but many don’t grasp the recklessness of the ongoing blowout. Federal deficits are expected to average $1.6 trillion per year over the next decade, versus less than $0.9 trillion and $1.25 trillion over the two previous decades, respectively. That $1.25 trillion includes the massive (and excessive) transfers that took place during the pandemic, which is why we’ve bumped up against the debt limit earlier than had been expected. The trend isn’t abating, despite the fact that the pandemic is behind us. And keep in mind that the Congressional Budget Office has been too optimistic for the past 20 years or so. Take a look at federal debt relative to GDP:

Unpleasant Arithmetic

With federal debt growing faster than GDP, the burden of servicing the debt mounts. This creates a strain in the coordination of fiscal and monetary policy, as described by David Andolfatto, who last year reviewed the implications of “Some Unpleasant Monetarist Arithmetic” for current policy. His title was taken from a seminal paper written by Thomas Sargent and Neil Wallace in 1981. Andolfatto says that:

“… attempting to monetize a smaller fraction of outstanding Treasury securities has the effect of increasing the rate of inflation. A tighter monetary policy ends up increasing the interest expense of debt issuance. And if the fiscal authority is unwilling to curtail the rate of debt issuance, the added interest expense must be monetized—at least if outright default is to be avoided.

Andolfatto wrote that last spring, before the Federal Reserve began its ongoing campaign to tighten monetary policy by raising short-term interest rates. But he went on to say:

“Deficit and debt levels are elevated relative to their historical norms, and the current administration seems poised to embark on an ambitious public spending program. … In the event that inflation rises and then remains intolerably above target, the Federal Reserve is expected to raise its policy rate. … if the fiscal authority is determined to pursue its deficit policy into the indefinite future, raising the policy rate may only keep a lid on inflation temporarily and possibly only at the expense of a recession. In the longer run, an aggressive interest rate policy may contribute to inflationary pressure—at least until the fiscal regime changes.”

So it is with a spendthrift government: escalating debt and interest expense must ultimately be dealt with via higher taxes or inflation, despite the best intentions of a monetary authority.

Fiscal Wrasslin’

Some people think the debt limit debate is all a big fake. Maybe … there are spendthrifts on both sides of the aisle. Still, the current debt limit impasse could serve a useful purpose if fiscal conservatives succeed in efforts to restrain spending. There is, however, an exaggerated uproar over the possibility of default, meaning a failure to make scheduled payments on Treasury securities. The capital markets aren’t especially worried because an outright default is very unlikely. Establishment Republicans may well resort to their usual cowardice and accept compromise without holding out for better controls on spending. Already, in a politically defensive gesture, House Speaker Kevin McCarthy has said the GOP wishes to strengthen certain entitlement programs. Let’s hope he really means restoring solvency to the Social Security and Medicare Trust Funds via fundamental reforms. And if the GOP rules out cuts to any program, let’s hope they don’t rule out cuts in the growth of these programs, or privatization. For their part, of course, Democrats would like to eliminate the debt ceiling entirely.

One of the demands made by Republicans is a transformation of the federal tax system. They would like to eliminate the income tax and substitute a tax on consumption. Economists have long favored the latter because it would eliminate incentives that penalize saving, which undermine economic growth. Unfortunately, this is almost dead in the water as a political matter, but the GOP further sabotaged their own proposal in their zeal to abolish the IRS. Their consumption tax would be implemented as a national sales tax applied at the point of sale, complete with a new Treasury agency to administer the tax. They’d have done better to propose a value added tax (VAT) or a tax on a simple base of income less saving (and other allowances).

Gimmicks and Measures

We’ve seen proposals for various accounting tricks to allow the government to avoid a technical default and buy time for an agreement to be reached on the debt limit. Treasury Secretary Janet Yellen already has implemented “extraordinary measures” to stay under the debt limit until June, she estimates. The Treasury is drawing down cash, skipping additional investments in government retirement accounts (which can be made up later without any postponement of benefits), plus a few other creative accounting maneuvers.

Payment prioritization, whereby the Treasury makes payments on debt and critical programs such as Social Security and Medicare, but defers a variety of other payments, has also been considered. Those deferrals could include amounts owed to contractors or even government salaries. However, a deferral of payments owed to anyone represents a de facto default. Thus, payment prioritization is not a popular idea, but if push comes to shove, it might be viewed as the lesser of two evils. Missing payments on government bonds could precipitate a financial crisis, but no one believes it will come to that.

Two other ideas for avoiding a breach of the debt ceiling are rather audacious. One involves raising new cash via the sale of premium bonds by the Treasury, as described here by Josh Barro (and here by Matt Levine). The other idea is to mint a large denomination ($1 trillion) platinum, “commemorative” coin, which the Treasury would deposit at the Federal Reserve, enabling it to conduct business as usual until the debt limit impasse is resolved. I’ll briefly describe each of these ideas in more detail below.

Premium Bonds

Premium bonds would offer a solution to the debt limit controversy because the debt ceiling is defined in terms of the par value of Treasury debt outstanding, as opposed to the amount actually raised from selling bonds at auction. For example, a note that promises to pay $100 in one year has a par value of $100. If it also promises to pay $100 in interest, it will sell at a steep premium. Thus, the Treasury collects, say, $185 at auction, and it could use the proceeds to pay off $100 of maturing debt and fund $85 of federal spending. That would almost certainly require a “market test” by the Treasury on a limited scale, and the very idea might reveal any distaste the market might have for obviating the debt limit in this fashion. But distaste is probably too mild a word.

An extreme example of this idea is for the Treasury to sell perpetuities, which have a zero par value but pay interest forever, or at least until redeemed beyond some minimum (but lengthy) term. John Cochrane has made this suggestion, though mainly just “for fun”. The British government sold perpetuities called consols for many years. Such bonds would completely circumvent the debt limit, at least without legislation to redefine the limit, which really is long overdue.

The $1 Trillion Coin

Minting a trillion dollar coin is another thing entirely. Barro has a separate discussion of this option, as does Cochrane. The idea was originally proposed and rejected during an earlier debt-limit controversy in 2011. Keep in mind, in what follows, that the Fed does not follow Generally Accepted Accounting Principles (GAAP).

Skeptics might be tempted to conclude that the “coin trick” is a ploy to engineer a huge increase the money supply to fund government expansion, but that’s not really the gist of this proposal. Instead, the Treasury would deposit the coin in its account at the Fed. The Fed would hold the coin and give the Treasury access to a like amount of cash. To raise that cash, the Fed would sell to the public $1 trillion out of its massive holdings of government securities. The Treasury would use that cash to meet its obligations without exceeding the debt ceiling. As Barro says, the Fed would essentially substitute sales of government bonds from its portfolio for bonds the Treasury is prohibited from selling under the debt limit. The effect on the supply of money is basically zero, and it is non-inflationary unless the approach has an unsettling impact on markets and inflation expectations (which of course is a distinct possibility).

When the debt ceiling is finally increased by Congress, the process is reversed. The Treasury can borrow again and redeem its coin from the Fed for $1 trillion, then “melt it down”, as Barro says. The Fed would repurchase from the public the government securities it had sold, adding them back to its portfolio (if that is consistent with its objectives at that time). Everything is a wash with respect to the “coin trick”, as long as the Treasury ultimately gets a higher debt limit.

Lust For the Coin

In fairness to skeptics, it’s easy to understand why the “coin trick” described above might be confused with another coin minting idea that arose from the collectivist vanguard during the pandemic. Representative Rashida Tlaib (D-MI) proposed minting coins to fund monthly relief payments of $1,000 – $2,000 for every American via electronic benefit cards. She was assisted in crafting this proposal by Rohan Grey, a prominent advocate of Modern Monetary Theory (MMT), the misguided idea that government can simply print money to pay for the resources it demands without inflationary consequences.

Tlaib’s plan would have required the Federal Reserve to accept the minted coins as deposits into the Treasury’s checking account. But then, rather than neutralizing the impact on the money supply by selling government bonds, the coin itself would be treated as base money. Cash balances would simply be made available in the Treasury’s checking account with the Fed. That’s money printing, pure and simple, but it’s not at all the mechanism under discussion with respect to short-term circumvention of the debt limit.

Fed Independence

The “coin trick” as a debt limit work-around is probably an impossibility, as Barro and others point out. First, the Fed would have to accept the coin as a deposit, and it is under no legal obligation to do so. Second, it obligates the Fed to closely coordinate monetary policy with the Treasury, effectively undermining its independence and its ability to pursue its legal mandates of high employment and low inflation. Depending on how badly markets react, it might even present the Fed with conflicting objectives.

Believe me, you might not like the Fed, but we certainly don’t want a Fed that is subservient to the Treasury… maintaining financial and economic stability in the presence of an irresponsible fiscal authority is bad enough without seating that authority at the table. As Barro says of the “coin trick”:

“These actions would politicize the Fed and undermine its independence. In order to stabilize expectations about inflation, the Fed would have to communicate very clearly about its intentions to coordinate its fiscal actions with Treasury — that is, it would have to tell the world that it’s going to act as Treasury’s surrogate in selling bonds when Treasury can’t. …

These actions would interfere with the Fed’s normal monetary operations. … the Fed is currently already reducing its holdings of bonds as part of its strategy to fight inflation. If economic conditions change (fairly likely, in the event of a near-default situation) that might change the Fed’s desired balance sheet strategy.”

On With The Show

Discussions about the debt limit continue between the White House and both parties in Congress. Kevin McCarthy met with President Biden today (2/1), but apparently nothing significant came it. Fiscal conservatives wonder whether McCarthy and other members of the GOP lack seriousness when it comes to fiscal restraint. But spending growth must slow to achieve deficit reduction, non-inflationary growth, and financial stability.

Meanwhile, even conservative media pundits seem to focus only on the negative politics of deficit reduction, ceding the advantage to Democrats and other fiscal expansionists. For those pundits, the economic reality pales in significance. That is a mistake. Market participants are increasingly skeptical that the federal government will ever pay down its debts out of future surpluses. This will undermine the real value of government debt, other nominal assets, incomes and buying power. That’s the inflation tax in action.

Unbridled growth of the government’s claims on resources at the expense of the private sector destroys the economy’s productive potential, to say nothing of growth. The same goes for government’s insatiable urge to regulate private activities and to direct patterns of private resource use. Unfortunately, so many policy areas are in need of reform that imposition of top-down controls on spending seems attractive as a stopgap. Concessions on the debt limit should only be granted in exchange for meaningful change: limits on spending growth, regulatory reforms, and tax simplification (perhaps replacing the income tax with a consumption tax) should all be priorities.

In the meantime, let’s avoid trillion dollar coins. As a debt limit work-around, premium bonds are more practical without requiring any compromise to the Fed’s independence. Other accounting gimmicks will be used to avoid missing payments, of course, but the fact that premium bonds and platinum coins are under discussion highlights the need to redefine the debt limit. When the eventual time of default draws near, fiscal conservatives must be prepared to stand up to their opponents’ convenient accusations of “brinksmanship”. The allegation is insincere and merely a cover for government expansionism.

In advanced civilizations the period loosely called Alexandrian is usually associated with flexible morals, perfunctory religion, populist standards and cosmopolitan tastes, feminism, exotic cults, and the rapid turnover of high and low fads---in short, a falling away (which is all that decadence means) from the strictness of traditional rules, embodied in character and inforced from within. -- Jacques Barzun