The world doesn’t ordinarily revolve around tariffs, but so much has happened to make tariffs into an economic and political linchpin of the moment. Donald Trump put them in the spotlight, of course, and while he’s still seeing roses, things won’t turn out entirely the way he hopes. At the tariff levels he’s instituted, this shouldn’t be too surprising.

While tariff revenue is helping to shave the federal budget deficit, the tax falls largely on the backs of American consumers and businesses with all the attending distortions that entails. Sadly, the extra revenue also seems to have offered a handy excuse to put spending cuts on the back burner. Tariffs and tariff uncertainty have businesses attempting to compromise between reduced margins and price hikes. Thinning margins due to tariffs have played a role in the weak employment numbers we’ve seen over the past few months. And tariffs, at least until now, have quite rightly reinforced the Federal Reserve’s cautious stance toward easing policy. However, the weak labor market has likely convinced the Fed to cut its short-term interest rate target, despite inflation stubbornly remaining well above the Fed’s 2% objective. That upward price pressure will remain.

Now, the legal battle over Trump’s tariff authority is about to reach a climax. That’s what I’ll focus on here. The Supreme Court has agreed to fast track the challenge to the President’s discretion to impose retaliatory tariffs unilaterally. There are two cases at hand: V.O.S. Selections, Inc. v. Trump, and Learning Resources, Inc., et al. v. Donald Trump et al. In both cases, small business plaintiffs contend that Trump’s invocation of the International Emergency Economic Powers Act (IEEPA) is unwarranted, and that “most” of the tariff actions taken by Trump have usurped Congress’ power of the purse under Article I of the Constitution. Here’s Ilya Somin, who is a Volokh Conspiracy regular and one of the attorneys representing the plaintiffs:

“… IEEPA doesn’t even mention tariffs and has never previously been used to impose them, that there is no ‘unusual and extraordinary threat’ of the kind required to invoke IEEPA, the major questions doctrine, the constitutional nondelegation doctrine, and more.“

This isn’t the first time a U.S. president has imposed tariffs unilaterally, but it is easily the most drastic such action. Historically, nearly all tariffs were levied by acts of Congress. Prior to Trump II, perhaps the broadest tariff imposed by a President was Richard Nixon’s brief 10% surcharge on all imports, but that was lifted quickly. Presidents Johnson and Obama imposed some selective tariffs. All of these episodes seem piddling compared to Trump’s tariffs, which are both sweeping and in many cases painfully selective.

Eric Boehm notes that when it comes to major constitutional questions, the Court has taken the position that

“… executive power should be construed narrowly, not broadly …. Rather than tying itself into knots to affirm nearly unlimited executive powers over commerce, the Supreme Court should tell the Trump administration to get permission from Congress before imposing new tariffs.“

I believe that will be the general shape of the outcome here. Maybe there’s a way for the Court to allow the tariffs to stand until Congress decides to “man up”, acting one way or the other. SCOTUS would probably like to do just that! Or maybe the Court could stay the lower court’s injunction until the case is heard by the Court in full on the regular docket, or until Congress acts.

There’s a decent chance, however, that Trump’s tariffs will be struck down, leaving it up to tariff supporters in Congress to lay down statutory rules rather than put up with the impulsive craziness we’ve witnessed thus far. If the Court lets the tariffs stand, it leaves the door open for new tests on the limits of executive discretion. Here is Greg Ip at the link:

“There would also be no end to uncertainty. ‘Unlike most other tariff authorities, these tariffs are not enshrined in statute, there’s no process to change them, and they can change very rapidly, in a day, without much notice, as we’ve seen,’ said Greta Peisch, a trade attorney at Wiley Rein and former general counsel for the U.S. trade representative.“

We’ve already seen strong hints that the Administration would like to force businesses to eat the cost of the tariffs rather than pass them along to consumers in higher prices. There hasn’t been any formal action of this kind by the Administration, at least not yet. Still, one can hardly blame businesses who might perceive an implicit threat if they fail to comply. That kind of bullying represents an a massive abuse of power. The Court could do everyone a big favor by clarifying that the authority to impose tariffs rests with Congress.

Since his inauguration, Donald Trump has been busy finding ways for the government to extort payments and ownership shares from private companies. This has taken a variety of forms. Tad DeHaven summarizes the major pieces of booty extracted thus far in the following bullet points (skipping the quote marks here):

June 13: Trump issues an executive order allowing the Nippon Steel-US Steel deal contingent on giving the government a “golden share” that enables the president to exert extensive control over US Steel’s operations.

July 10: The Department of Defense (DoD) unveils a multi-part package with convertible preferred stock, warrants, and loan guarantees, making it the top shareholder of rare earth metals producer MP Materials.

July 23: The White House claims an agreement with Japan to reduce the president’s so-called reciprocal tariff rate on Japanese imports comes with a $550 billion Japanese “investment fund” that Trump will control.

July 31: Trump claims an agreement with South Korea to reduce the so-called reciprocal tariff on South Korean imports comes with a $350 billion South Korean-financed investment in projects “owned and controlled by the United States” that he will select.

August 12: In a Fox Business interview, Bessent points to the alleged investments from Japan, South Korea, and the EU “to some extent” and says, “Other countries, in essence, are providing us with a sovereign wealth fund.”

August 22: Fifteen days after calling for Intel CEO Lip-Bu Tan to resign, Trump announces that the US will take a 10 percent equity stake in Intel using the CHIPS Act and DoD funds, becoming Intel’s largest single shareholder.

Each of these “deals” has a slightly different back story, but national security is a common theme. And Trump says they’ll all make America great again. They are touted as a way for American taxpayers to benefit from the investment he claims his policies are attracting to the U.S. However, all of these are ill-advised for several reasons, some of which are common to all. That includes the extortionary nature of each and every one of them.

Short Background On “Deals”

The June 13 deal (Nippon/US Steel), the July 10 deal (MP Materials), and the August 22 deal (Intel) all involve U.S. government equity stakes in private companies. The August 11 deal (NVIDIA/AMD) diverts a stream of private revenue to the government. The July 23 and July 31 deals (Japan and South Korea) both involve “investment funds” that Trump will control to one extent or another.

The August 12 entry adds “expected” EU investments with some qualification, but that bullet quotes Treasury Secretary Bessent referring to these investments as part of a sovereign wealth fund (SWF). Secretary of Commerce Lutnick now denies that an SWF will exist. My objections might be tempered slightly (but only slightly) by an SWF because it would probably need to place constraints on an Administation’s control. That might give you a hint as to why Lutnick is now downplaying the creation of an SWF.

I object to the Nippon/US Steel “deal” in part (and only in part) because it was extortion on its face. There is no valid anti-trust argument against the deal (US Steel is the nation’s third largest steelmaker and is broke), and the national security concerns that were voiced (Japan! for one thing) were completely bogus. Even worse, the “Golden Share” would give the federal government authority, if it chose to exercise it, over a variety of the company’s decisions.

The Intel “deal” is another highly questionable transaction. Intel was to receive $11 billion under the CHIPS Act, a fine example of corporate welfare, as Veronique de Rugy once described the law. However, Intel was to receive its grants only if it stood up four fabrication facilities. But it did not. Now, instead of demanding reimbursement of amounts already paid, the government offered to pay the remainder in exchange for a 9.9% stake in the company. And there is no apparent requirement that Intel meet the original committment! This could turn out a bust!

The MP Materials transaction with the Department of Defense has also been rationalized on national security grounds. This excuse comes a little closer to passing the smell test, but the equity stake is objectionable for other reasons (to follow).

The Nvidia/AMD deal has been justified as compensation for allowing the companies to sell chips to China, which is competing with the U.S. to lead the world in AI development. This is another form of selective treatment, here applied to an export license. The chips in question do not have the same advanced specifications as those sold by the companies in the U.S., but let’s not let that get in the way of a revenue opportunity.

While nothing about TikTok appears on the list above, I fear that a resolution of its operational status in the U.S. presents another opportunity for extortion by the Trump Administration. I’m sure there will be many other cases.

Root Cause: Protectionism

The so-called investment funds described in the timeline above are nearly all the result of trade terms negotiated by a dominant and belligerent trading partner: the U.S. My objections to tariffs are one thing, but here we are extorting investment pledges for reductions in the taxes we’ll impose on our own citizens! Additionally, the belief that these investments will somehow prevent a general withdrawal of foreign investment in the U.S. is misguided. In fact, a smaller trade deficit dictates less foreign investment. The difference here is that the government will wrest ownership control over a greater share of less foreign investment.

Trump the Socialist?

Needless to say, I don’t favor government ownership of the means of production. That’s socialism, but do matters of national security offer a rationale for public ownership? For example, rare earth minerals are important to national defense. Therefore, it’s said that we must ensure a domestic supply of those minerals. I’m not convinced that’s true, but in any case, fat defense contracts should create fat profit opportunities in mining rare earths (enter MP Materials). None of that means public ownership is necessary or a good idea.

All of these federal investments are construed, to one extent or another, as matters of national security, but that argument for market intervention is much too malleable. Must we ensure a domestic supply of semiconductors for national security reasons? And public ownership? Is the same true of steel? Is the same true of our “manufacturing security”? It can go on and on. The next thing you know, someone will argue that grocery stores should be owned by the government in the name of “food security”! Oh, wait…

Trump the Central Planner

Government ownership takes the notion of industrial planning a huge step beyond the usual conception of that term. Ordinarily, when government takes the role of encouraging or discouraging activity in particular industries or technologies, it attempts to select winners and losers. The very idea presumes that the market is not allocating resources in an optimal way, as if the government is in any position to gainsay the decisions of private market participants who have skin in the game. This is a foolhardy position with predictably negative consequences. (For some examples, see the first, second, and fourth articles linked here by Don Boudreaux.) The fundamental flaw in central planning always comes down to the inability of planners to collect, process, and act on the information that the market handles with marvelous efficiency.

When government invests taxpayer funds in exchange for ownership positions in private concerns, the potential levers of control are multiplied. One danger is that political guidance will replace normal market incentives. And as de Rugy points out, the government’s potential role as a regulator creates a clear conflict of interest. In a strong sense, a government ownership stake is worse for private owners than a mere dilution of their interests. It looms as a possible taking, as private owners and managers surrender to creeping government extortion.

Financial Malfeasance

In addition to the objections above, I maintain that these investments represent poor stewardship of public funds. The U.S. public debt currently stands at $37 trillion with an entitlement disaster still to come. In fact, according to one estimate, the federal government’s total unfunded obligations amount to additional $121 trillion! Putting aside the extortion we’re witnessing, any spare dollar should be put toward retiring debt, rather than allowing its upward progression.

As I’ve noted before, paying off a dollar of debt entails a risk-free “return” in the form of interest cost avoidance, let’s say 3.5% for the sake of argument. If instead the dollar is “invested” in risk assets by the government, the interest cost is still incurred. To earn a net return as high as the that foregone from interest avoidance, the government must consistently earn at least 7% on its invested dollar. But of course that return is not risk-free!

A continuing failure to pay down the public debt will ultimately poison the debt market’s assessment of the government’s will to stay within its long-run budget constraint. That would ultimately manifest in an inflation, shrinking the real value of the public debt even as it undermines the living standards of many Americans.

One final thought: Though few MAGA enthusiasts would admit it even if they understood, we’re witnessing a bridging of two ends of the idealogical “horseshoe”. Right-wing populism and protectionism meet the left-wing ideal of central planning and public ownership. There is a name for this particular form of corporatist state, and it is fascism.

I’ve noted a number of policy moves by Donald Trump that I find aggravating (scroll my home page), but I still applaud his administration’s agenda to downsize government, promote operational efficiency, and deregulate the private economy. It’s just too bad that Trump demonstrates a penchant for expanding government authority in significant ways, which makes it harder to celebrate successes of the former variety. Beyond that, there have been huge obstacles to rationalizing the administrative state. We’ve seen progress in some areas, but the budgetary impact has been disappointing.

Grinding On

The Department of Government Efficiency (DOGE) was to play a large role in the effort to reduce fraud and inefficiency at the federal level. On the surface, it’s easy to surmise that DOGE has failed in its mission to root out government waste. After seven months, DOGE touts that it has saved taxpayers $205 billion thus far. That is well short of the original $2 trillion objective (subsequently talked down by Elon Musk), but it was expected to take 18 months to reach that goal. Still, the momentum has slowed considerably.

Moreover, the $205 billion figure does not represent recurring budgetary savings. Some of it is one-time proceeds from property sales or grant cancellations. Some of it ($30 billion) seems to represent savings in regulatory compliance costs to Americans, but that’s not clear as the DOGE website is lightly documented, to put it charitably. A recent analysis reached the conclusion that DOGE had exaggerated the savings it has claimed for taxpayers, which seems plausible.

But DOGE is still plugging away, reviewing federal contracts, programs, regulations, payments, grants, workforce deployment, and accounting systems. The work is desperately needed given the fraud that’s been exposed among the agency workforce, which seemed to escalate following the advent of massive Covid benefit payments during the pandemic. Some details of an investigation by the Senate DOGE Caucus, discussed at this link, are truly astonishing. Employees at multiple state and federal agencies have been collecting food stamps, survivor benefits, and even unemployment benefits while employed by government. Apparently, this was made possible by the lack of list de-duplication by the federal agencies that dole out these benefits. This might be a pretty good explanation for the lawsuits filed by federal employee unions attempting to prevent DOGE from accessing agency records. Congratulations to Senator Joni Ernst, Chairman of the Caucus, for her leadership in exposing this graft.

False Aspersions

Shortly after DOGE was constituted, most of its employees were assigned to individual agencies to identify opportunities to reduce waste and promote efficiency. This has led to confusion about the extent to which DOGE should take credit for certain savings maneuvers. However, contrary to some allegations, no DOGE employees have been “embedded” as career civil servants.

Since almost the start of Trump’s second term, DOGE has been blamed for workforce reductions that some deemed reckless and arbitrary. There were indeed some early mistakes, most notably at HHS, but a number of those key workers were rehired. Many of the force reductions were instigated by individual agencies themselves, and many of those were voluntary separations with generous severance packages.

As to the “arbitrary” nature of the force reductions, one former DOGE staffer described the difficulty of making sensible cuts at the Veterans Administration under agency rules:

“Then came a reality check about RIF rules, which turned out to be brutally deterministic:

Tenure matters most—new hires were cut first

Veterans’ preference comes next; vets are protected over non-vets

Length of service trumps performance—seniority beats skill

Performance ratings break any remaining ties

“These reduction-in-force rules–which stem from the Veterans’ Preference Act of 1944–surprised me and many others. Unlike private industry layoffs that target middle management bloat and low performers, the government cuts its newest people first, regardless of performance. Anyone promoted within the last two years was also considered probationary—first in line to go.“

It would be hard to be less arbitrary than these rules. Other agencies are subject to similar strictures on reductions in force. No wonder the Administration relied heavily on a buyout offer (“deferred resignation”) with broad eligibility in its attempt to downsize government. Furthermore, the elimination of positions was largely targeted functions that were wasteful of taxpayer resources, such as promoting DEI objectives and administering grants to NGOs driven by ideological motives.

Of course, the buyouts come with a cost to taxpayers. In fact, one report asserted that DOGE’s efforts themselves cost taxpayers $135 billion or more. Of course, buyouts carry a one-time cost. However, that figure also includes a questionable estimate of lost productivity caused by turmoil at federal agencies. I’m just a little skeptical when it comes to claims about the productivity of the federal workforce.

Obstacles

DOGE has had to grapple with other severe limitations, as Dan Mitchell has commented. These are primarily rooted in the spending authority of Congress. Only one rescission bill reflecting DOGE cuts, totaling just $9 billion, has made it to Trump’s desk. Another “untouchable” for DOGE is interest on the federal debt, which has become a huge portion of the federal budget.

Furthermore, DOGE is guilty of one self-imposed obstacle: the main driver of ongoing deficits is entitlement spending, While the Big Beautiful Bill included Medicaid reforms, the Trump Administration and Congress have shown little interest in shoring up Social Security and Medicare, both of which are technically insolvent. While DOGE would seem to have limited authority over entitlements, as opposed to the discretionary budget, some charge that DOGE made a critical error in failing to address entitlement fraud. According to Veronique de Rugy:

“It is insane not to have started there. Given DOGE’s comparative advantage in data analytics and [information technology], this is where it can have the greatest impact… Cracking down on this waste isn’t just about saving money; it’s about restoring integrity to safety-net programs and protecting taxpayers. And if fixing this problem is not quintessential ‘efficiency,’ what is?“

On the Bright Side

Michael Reitz offered a different perspective. He cited the difficulty of reforming an entrenched bureaucracy. He also noted the following, however, as a kind of hidden success of DOGE and Elon Musk:

“But others I spoke with thought Musk’s four months in government were both substantive and symbolic. He changed the conversation about waste and grift. Musk made cuts cool again, especially for Republican politicians who have forgotten fiscal restraint. He highlighted the need to follow the data and oppose bureaucrats who impede reform by controlling the flow of information.“

Of course, DOGE has been instrumental in identifying absurdly wasteful federal contracts, even if they are “small change” relative to the size of the federal budget. This includes grants to NGOs that appear to have functioned primarily as partisan slush funds. DOGE has also helped identify deregulatory actions to eliminate duplicative or contradictory agency rules on industry, reducing costly economic burdens on the private sector. The DOGE website claims (preliminarily) that it has deleted 1.9 million words of regulation, but doesn’t provide a total number of rules eliminated.

An important part of DOGE’s mission was to modernize technology, software, and accounting systems at federal agencies. This included centralization of these systems with improved tracking of payments and a written justification for each payment. These efforts were met with hostility from some quarters, including lawsuits to limit or prevent DOGE personnel from accessing agency data. Nevertheless, DOGE has pushed ahead with the initiative. This is a laudable attempt to not only modernize systems, but to encourage transparency, accountability, and efficiency.

In a related development, this week DOGE was blamed by a whistleblower for uploading a file from Social Security containing sensitive information to an unsecured cloud environment. However, a spokesperson for the Social Security Administration stated that the data was secure and that the SSA had no indication that it had been breached. We shall see.

AI Scrutiny

Now, DOGE is recommending the use of an AI tool to cut federal regulations. According to Newsweek:

“The ‘DOGE AI Deregulation Decision Tool,’ developed by engineers brought into government under Elon Musk’s DOGE initiative, is programmed to scan about 200,000 existing federal rules and flag those that are either outdated or not legally required.“

Critics are concerned about accuracy and legal complexities, but the regulations flagged by the AI tool will be reviewed by attorneys and other agency personnel, and there will be an opportunity for public comment. The process could make deregulatory progress well beyond what would be possible under purely human review. DOGE believes that up to 100,000 rules could be eliminated, saving trillions of dollars in compliance costs. If successful, this might well turn out to be DOGE’s signal accomplishment.

Conclusion

I’m disappointed at the flagging momentum of DOGE’s quest to eliminate inefficiencies in the executive branch. I’m also frustrated by the limited progress in translating DOGE’s work into ongoing deficit reduction. In addition, it was a mistake to leave aside any scrutiny of improper entitlement payments. Nevertheless, DOGE has has some significant wins and the effort continues. Also, it must be acknowledged that DOGE has faced tremendous obstacles. For too long, government itself has metastasized along with bureaucratic inefficiencies and graft. That is the rotten fruit of the symbiosis between rent seeking behavior and a bloated public sector. We should applaud the spirit motivating DOGE and encourage greater progress.

There’s a hopeful narrative making the rounds that artificial intelligence will prove to be such a boon to the economy that we need not worry about high levels of government debt. AI investment is already having a substantial economic impact. Jason Thomas of Carlyle says that AI capital expenditures on such things as data centers, hardware, and supporting infrastructure account for about a third of second quarter GDP growth (preliminarily a 3% annual rate). Furthermore, he says relevant orders are growing at an annual rate of about 40%. The capex boom may continue for a number of years before leveling off. In the meantime, we’ll begin to see whether AI is capable of boosting productivity more broadly.

Unfortunately, even with this kind of investment stimulus, there’s no assurance that AI will create adequate economic growth and tax revenue to end federal deficits, let alone pay down the $37 trillion public debt. That thinking puts too much faith in a technology that is unproven as a long-term economic engine. It would also be a naive attitude toward managing debt that now carries an annual interest cost of almost $1 trillion, accounting for about half of the federal budget deficit.

Boom Times?

Predictions of AI’s long-term macro impact are all over the map. Goldman Sachs estimates a boost in global GDP of 7% over 10 years, which is not exactly aggressive. Daren Acemoglu has beenevenmore conservative, estimating a gain of 0.7% in total factor productivity over 10 years. Tyler Cowen has been skeptical about the impact of AI on economic growth. For an even more pessimistic take see these comments.

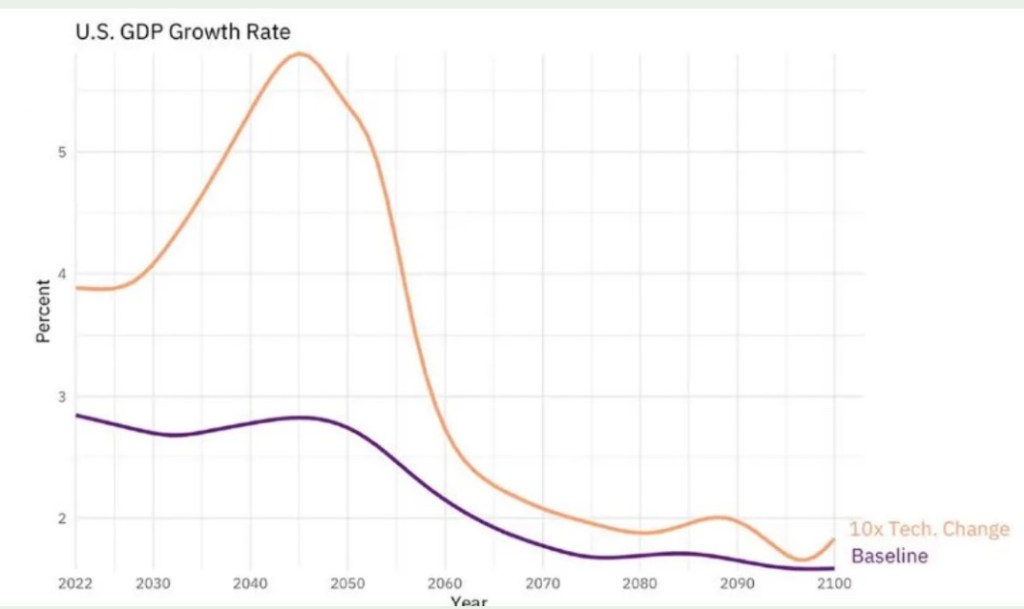

In July, however, Seth Benzell of the Stanford Digital Economy Lab discussed some simulations showing impressive AI-induced growth (see chart at top). The simulations project additional U.S. GDP growth of between 1% – 3% annually over the next 75 years! The largest boost in growth occurs now through the 2050s. This would produce a major advance in living standards. It would also eliminate the federal deficit and cure our massive entitlement insolvency, but the result comes with heavy qualifications. In fact, Benzell ultimately throws cold water on the notion that AI growth will be strong enough to reduce or even stabilize the public debt to GDP ratio.

The Scarcity Spoiler

The big hitch has to do with the scarcity of capital, which I’ve described asanimpediment to widespread AI application. Competition for capital will drive interest rates up (3% – 4%, according to Benzell’s model). Ongoing needs for federal financing intensify that effect. But it might not be so bad, according to Benzell, if climbing rates are accompanied by heightened productivity powered by AI. Then, tax receipts just might keep-up with or exceed the explosion in the government’s interest obligations.

A further complication cited by Benzell lurks in insatiable demands for public spending, and politicians who simply can’t resist the temptation to buy votes via public largesse. Indeed, as we’ve already seen, government will try to get in on the AI action, channeling taxpayer funds into projects deemed to be in the public interest. And if there are segments of the work force whose jobs are eliminated by AI, there will be pressure for public support. So even if AI succeeds in generating large gains in productivity and tax revenue, there’s very little chance we’ll see a contagion of fiscal discipline in Washington DC. This will put more upward pressure on interest rates, giving rise to the typical crowding out phenomenon, curtailing private investment in AI.

Playing Catch-Up

The capex boom must precede much of the hoped-for growth in productivity from AI. Financing comes first, which means that rates are likely to rise sooner than productivity gains can be expected. And again, competition from government borrowing will crowd out some private AI investment, slowing potential AI-induced increases in tax revenue.

There’s no chance of the converse: that AI investment will crowd out government borrowing! That kind of responsiveness is not what we typically see from politicians. It’s more likely that ballooning interest costs and deficits generally will provoke even more undesirable policy moves, such as money printing or rate ceilings.

The upshot is that higher interest rates will cause deficits to balloon before tax receipts can catch up. And as for tax receipts, the intangibility of AI will create opportunities for tax flight to more favorable jurisdictions, a point well understood by Benzell. As attorneys Bradford S. Cohen and Megan Jones put it:

“Digital assets can be harder to find and more easily shifted offshore, limiting the tax reach of the U.S. government.”

AI Growth Realism

Benzell’s trepidation about our future fiscal imbalances is well founded. However, I also think Benzell’s modeled results, which represent a starting point in his analysis of AI and the public debt, are too optimistic an assessment of AI’s potential to boost growth. As he says himself,

“… many of the benefits from AI may come in the form of intangible improvements in digital consumption goods. … This might be real growth, that really raises welfare, but will be hard to tax or even measure.”

This is unlikely to register as an enhancement to productivity. Yet Benzell somehow buys into the argument that AI will lead to high levels of unemployment. That’s one of his reasons for expecting higher deficits.

My view is that AI will displace workers in some occupations, but it is unlikely to put large numbers of humans permanently out of work and into state support. That’s because the opportunity cost of many AI applications is and will remain quite high. It will have to compete for financing not only with government and more traditional capex projects, but with various forms of itself. This will limit both the growth we are likely to reap from AI and losses of human jobs.

Sovereign Wealth Fund

I have one other bone to pick with Benzell’s post. That’s in regard to his eagerness to see the government create a sovereign wealth fund. Here is his concluding paragraph:

“Instead of contemplating a larger debt, we should instead be talking about a national sovereign wealth fund, that could ‘own the robots on behalf of the people’. This would both boost output and welfare, and put the welfare system on an indefinitely sustainable path.”

Whether the government sells federal assets or collects booty from other kinds of “deals”, the very idea of accumulating risk assets in a sovereign wealth fund undermines the objective to reduce debt. It will be a struggle for a sovereign wealth fund to consistently earn cash returns to compensate for interest costs and pay down the debt. This is especially unwise given the risk of rising rates. Furthermore, government interests in otherwise private concerns will bring cronyism, displacement of market forces by central planning, and a politicization of economic affairs. Just pay off the debt with whatever receipts become available. This will free up savings for investment in AI capital and hasten the hoped-for boom in productivity.

Summary

AI’s contribution to economic growth probably will be inadequate and come too late to end government budget deficits and reduce our burgeoning public debt. To think otherwise seems far fetched in light of our historical inability to restrain the growth of federal spending. Interest on the federal debt already accounts for about half of the annual budget deficit. Refinancing the existing public debt will entail much higher costs if AI capex continues to grow aggressively, pushing interest rates higher. These dynamics make it pretty clear that AI won’t provide an easy fix for federal deficits and debt. In fact, ongoing federal borrowing needs will sop up savings needed for AI development and diffusion, even as the capital needed for AI drives up the cost of funds to the government. It’s a shame that AI won’t be able to crowd out government.

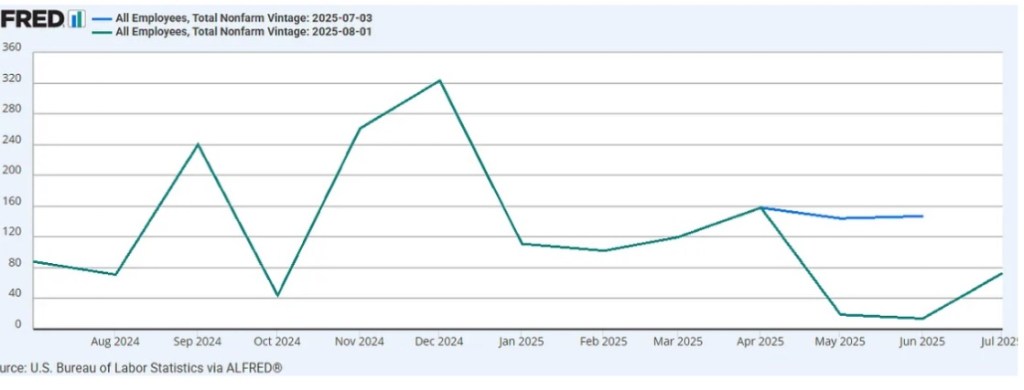

The dismissal of the Bureau of Labor Statistics (BLS) commissioner Erika McEntarfer by President Trump was regrettable and a dumb move besides. It was undeserved, and its timing made Trump look like the authoritarian buffoon of his enemies’ worst nightmares.

Trump believed the weak employment report for July made him “look bad”. He was particularly enraged by the downward revisions in nonfarm payrolls for the months of May and June (see chart above). Of course, he would not have liked the estimates to begin with, had they been in line the ultimate revisions — he just doesn’t like “bad” numbers on his watch. Trump stated his conviction that the weak report was “politically motivated”, and even “rigged” by McEntarfer, which is absurd. To anyone who knows anything about how these numbers are produced, this makes Trump look like a guy who is willing to manipulate economic data to his advantage. Only good numbers, please!

As I’ve said before, the mere availability of aggregate economic statistics seems to encourage activist policy. This is made worse by the unreliability and mis-measurement of these aggregates, which compounds policy failures. Like other parts of the federal statistical system, BLS reporting has shortcomings, some of them severe and getting worse. But that’s not McEntarfer’s doing. The numbers, for all their faults, are generated by a highly standardized process. Reforming that process will not be cheap.

One compelling take on the negative revisions is that they are really Trump’s very own fault. In an excellent post describing some of the technicalities that drive revisions, Claudia Sahm says:

“This is a policy problem, not a measurement problem. … Large, unpredictable shifts in economic policy are placing unusual strains on our measurement apparatus because they are causing large, unpredictable changes in the behavior of consumers and businesses. These changes are difficult to measure in real time. The GDP statistics this year have struggled to isolate massive swings in imported goods around the start of tariffs from its measure of domestic production. The initial estimates of payrolls didn’t capture the slowdown in employment, but that’s more a reflection of how sharp the jobs slowdown is, rather than a limitation of the surveys.“

The key lesson here is that shifts in the policy landscape can make economic activity more difficult to measure. And of course, policy uncertainty has contractionary effects on top of the stagflationary effects of higher taxes (i.e., tariffs). But I’m not holding out hope that Trump will engage in any introspection on the point.

As Sahm explains, the sharp slowing of job growth serves to highlight one of the difficulties inherent in survey-based measures of economic performance: not all responses are timely, and that is likely aggravated when underlying changes in activity are dramatic. In fact, she says, the June revision was driven largely by late reporting. Furthermore, the May and June revisions to payrolls were also partly driven by a change in seasonal adjustment factors based on new data (BLS uses a concurrent seasonal adjustment methodology).

In terms of industries, half of the June revision to payrolls came from state and local education, erasing an initial estimate showing that public education jobs had increased in June, which perplexed analysts at the time. The other half of the revision was spread broadly across the private sector.

In addition to the changeable nature of survey data and seasonal variability, BLS reports suffer because they often involve shaky assumptions made necessary by the limits of survey coverage. Perhaps the most controversial of these comes from the so-called birth/death (b/d) model of business formation/closure. This model is used by the BLS to estimate the net jobs created by new businesses that cannot be covered by the monthly Establishment Survey. Month-to-month, that can be a large gap to fill. Unfortunately, the b/d model can be extremely inaccurate, especially at turning points. In July 2025, the b/d model added about 257,000 jobs to total new jobs (prior to seasonal adjustment). Thus, the b/d assumption was 3.5 times the seasonally adjusted total gain of 73,000!

“It is inexcusable for the BLS to not incorporate QCEW data as soon as possible.

“Instead, it relies on poor sampling of a small subset. On that poor sample, the response rate is pathetic.

“In addition, there is survival bias. In recognition of survival bias, the BLS concocted its absurd birth-death model.

“And on top that that, struggling businesses have no incentive to respond. In contrast, large corporations likely have someone dedicated to filling out government surveys.”

I’ve been critical of large BLS revisions in the past, as well as glaring inconsistencies between estimates of payroll jobs from the Establishment Survey and total civilian employment from the BLS Household Survey. Of course, they are different surveys designed to estimate different things with different samples, different coverage, geared toward counting jobs in one case and people employed and unemployed in the other. The two are benchmarked differently and at different frequencies. Still, it’s unsettling to see the two surveys diverge sharply in terms of monthly changes or trends, or to see consistently one-directional revisions. John Podhoretz states that the number of new nonfarm payroll jobs has been revised down in 25 of the past 30 months!

As Veronique de Rugy says, flaws are not the same as bad faith. Surely improvements can be made to both BLS surveys, their benchmarking, and to other adjustments and assumptions made for reporting. However, it’s pretty clear that BLS has not had the staffing and resources necessary to address these shortcomings. Over the ten years ending in 2024, inflation-adjusted BLS funding declined by more than 20%. At the same time, response rates on the Household survey have declined from 89% to less than 70%. The Establishment Survey of nonfarm businesses has also been plagued by deteriorating response rates, which fell from 61% to less than 43% over the past 10 years. And now, the Trump Administration has proposed an additional budget cut for the BLS of 8% in 2026.

Trump would have done better to ask the BLS commissioner what resources were needed to revamp its processes. Instead, his approach was to create a public spectacle by firing the head of the agency. One has to wonder how Trump might find a well-trained economist or statistician who will take the job if the numbers must always reflect well on the boss.

As of February 2026, I’m adding this short preamble to a few older posts on the subject of AI and future prospects for human labor. In the original post below (and a few others), I overstated the case that the law of comparative advantage would assure a continued role for humans in production. I still think the case is strong, mind you, but now I’m convinced that the outcome depends on elasticities of input substitution and how those elasticities might shift given the advent of AI-augmented capital. You can read my most recent thoughts on the matter here.

____________________________________________

Every now and then I grind my axe against the proposition that AI will put humans out of work. It’s a very fashionable view, along with the presumed need for government to impose “robot taxes” and provide everyone with a universal basic income for life. The thing is, I sense that my explanations for rejecting this kind of narrative have been a little abstruse, so I’m taking another crack at it now.

Will Human Workers Be Obsolete?

The popular account envisions a world in which AI replaces not just white-collar technocrats, but by pairing AI with advanced robotics, it replaces workers in the trades as well as manual laborers. We’ll have machines that cure, litigate, calculate, forecast, design, build, fight wars, make art, fix your plumbing, prune your roses, and replicate. They’ll be highly dextrous, strong, and smart, capable of solving problems both practical and abstract. In short, AI capital will be able to do everything better and faster than humans! The obvious fear is that we’ll all be out of work.

I’m here to tell you it will not happen that way. There will be disruptions to the labor market, extended periods of joblessness for some individuals, and ultimately different patterns of employment. However, the chief problem with the popular narrative is that AI capital will require massive quantities of resources to produce, train, and operate.

Even without robotics, today’s AIs require vast flows of energy and other resources, and that includes a tremendous amount of expensive compute. The needed resources are scarce and highly valued in a variety of other uses. We’ll face tradeoffs as a society and as individuals in allocating resources both to AI and across various AI applications. Those applications will have to compete broadly and amongst themselves for priority.

AI Use Cases

There are many high-value opportunities for AI and robotics, such as industrial automation, customer service, data processing, and supply chain optimization, to name a few. These are already underway to a significant extent. To that, however, we can add medical research, materials research, development of better power technologies and energy storage, and broad deployment in delivering services to consumers and businesses.

In the future, with advanced robotics, AI capital could be deployed in domains that carry high risks for human labor, such as construction of high rise buildings, underwater structures, and rescue operations. This might include such things as construction of solar platforms and large transports in space, or the preparation of space habitats for humans on other worlds.

Scarcity

There is no end to the list of potential applications of AI, but neither is there an end to the list of potential wants and aspirations of humanity. Human wants are insatiable, which sometimes provokes ham-fisted efforts by many governments to curtail growth. We have a long way to go before everyone on the planet lives comfortably. But even then, peoples’ needs and desires will evolve once previous needs are satisfied, or as technology changes lifestyles and practices. New approaches and styles drive fashions and aesthetics generally. There are always individuals who will compete for resources to experiment and to try new things. And the insatiability of human wants extends beyond the strictly private level. Everyone has an opinion about unsatisfied needs in the public sphere, such as infrastructure, maintenance, the environment, defense, space travel, and other dimensions of public activity.

Futurists have predicted that the human race will seek to become a so-called Type I civilization, capable of harnessing all of the energy on our planet. Then there will be the quest to harness all the energy within our solar system (a Type II civilization). Ultimately, we’ll seek to go beyond that by attempting to exploit all the energy in the Milky Way galaxy. Such an expansion of our energy demands would demonstrate how our wants always exceed the resources we have the ability to exploit.

In other words, scarcity will always be with us. The necessity of facing tradeoffs won’t ever be obviated, and prices will always remain positive. The question of dedicating resources to any particular application of AI will bring tradeoffs into sharper relief. The opportunity cost of many “lesser” AI and robotics applications will be quite high relative to their value to investors. Simply put, many of those applications will be rejected because there will be better uses for the requisite energy and other resources.

Tradeoffs

Again, it will be impossible for humans to accomplish many of the tasks that AI’s will perform, or to match the sheer productivity of AIs in doing so. Therefore, AI will have an absolute advantage over humans in all of those tasks.

However, there are many potential applications of AI that are of comparatively low value. These include a variety of low-skill tasks, but also tasks that require some dexterity or continuous judgement and adjustment. Operationalizing AI and robots to perform all these tasks, and diverting the necessary capital and energy away from other uses, would have a tremendously high opportunity cost. Human opportunity costs will not be so high. Thus, people will have a comparative advantage in performing the bulk if not all of these tasks.

Sure, there will be novelty efforts and test cases to train robots to do plumbing or install burglar alarm systems, and at some point buyers might wish to have robots prune their roses. Some people are already amenable to having humanoid robots perform sex work. Nevertheless, humans will remain competitive at these tasks due to the comparatively high opportunity costs faced by AI capital.

There will be many other domains in which humans will remain competitive. Once more, that’s because the opportunity costs for AI capital and other resources will be high. This includes many of the skilled trades, caregivers, and a great many management functions, especially at small companies. Their productivity will be enhanced by AI tools, but those jobs will not be decimated.

The key here is understanding that 1) capital and resources generally are scarce; 2) high value opportunities for AI are plentiful; and 3) the opportunity cost of funding AI in many applications will be very high. Humans will still have a comparative advantage in many areas.

Who’s the Boss?

There are still other ways in which human labor will always be required. One in particular involves the often complementary nature of AI and human inputs. People will have roles in instructing and supervising AIs, especially in tasks requiring customization and feedback. A key to assuring AI alignment with the objectives of almost any pursuit is human review. These kinds of roles are likely to be compensated in line with the complexity of the task. This extends to the necessity of human leadership of any organization.

That brings me to the subject of agentic and fully autonomous AI. No matter how sophisticated they get, AIs will always be the product of machines. They’ll be a kind of capital for which ownership should be confined to humans or organizations representing humans. We must be their masters. Disclaiming ownership and control of AIs, and granting agentic AIs the same rights and freedoms as people (as many have imagined) is unnecessary and possibly dangerous. AIs will do much productive work, but that work should be on behalf of human owners, and human labor will be deployed to direct and assess that work.

AIs (and People) Needing People

The collaboration between AIs and humans described above will manifest more broadly than anything task-specific, or anything we can imagine today. This is typical of technological advance. First-order effects often include job losses as new innovations enhance productivity or replace workers outright, but typically new jobs are created as innovations generate new opportunities for complementary products and services both upstream in production or downstream among ultimate users. In the case of AI, while much of this work might be performed by other AIs, at a minimum these changes will require guidance and supervision by humans.

In addition, consumers tend to have an aesthetic preference for goods and services produced by humans: craftsmen, artists, and entertainers. For example, if you’ve ever shopped for an oriental rug, you know that hand-knotted rugs are more expensive than machine-weaved rugs. Durability is a factor as well as uniqueness, the latter being a hallmark of human craftspeople. AI might narrow these differences over time, but the “human touch” will always have value relative to “comparable” AI output, even at a significant disadvantage in terms of speed and uncertainty regarding performance. The same is true of many other forms, such as sports, dance, music, and the visual arts. People prefer to be entertained by talented people, rather than highly-engineered machines. The “human touch” also has advantages in customer-facing transactions, including most forms of service and high-level sales/financial negotiations.

Owning the Machines

Finally, another word about AI ownership. An extension of the fashionable narrative that AIs will wholly replace human workers is that government will be called upon to tax AI and provide individuals with a universal basic income (UBI). Even if human labor were to be replaced by AIs, I believe that a “classic” UBI would be the wrong approach. Instead, all humans should have an ownership stake in the capital stock. This is wealth that yields compound growth over time and produces returns that make humans less reliant on streams of labor income.

Savings incentives (and negative consumption incentives) are a big step in encouraging more widespread ownership of capital. However, if direct intervention is necessary, early endowments of capital would be far preferable to a UBI because they will largely be saved, fostering economic growth, and they would create better incentives than a UBI. Along those lines, President Trump’s Big Beautiful Bill, which is now law, has established “Baby Bonds” for all American children born in 2025 – 2028, initially funded by the federal government with $1,000. Of course, this is another unfunded federal obligation on top of the existing burden of a huge public debt and ongoing deficits. Given my doubts about the persistence of AI-induced job losses, I reject government establishment of both a UBI and universal endowments of capital.

Summary

Capital and energy are scarce, so the tremendous resource requirements of AI and robotics means that the real world opportunity costs of many AI applications will remain impractically high. The tradeoffs will be so steep that they’ll leave humans with comparative advantages in many traditional areas of employment. Partly, these will come down to a difference in perceived quality owing to a preference for human interaction and human performance in a variety of economic interactions, including patronization of the art and athleticism of human beings. In addition, AIs will open up new occupations never before contemplated. We won’t be out of work. Nevertheless, it’s always a good idea to accumulate ownership in productive assets, including AI capital, and public policy should do a better job of supporting the private initiative to do so.

An opinion piece caught my eye written by one Chad Wolf. It’s entitled: “Retailers caught red-handed using Trump’s tariffs as cover for price gouging”. A good rule is to approach allegations of “price gouging” with a strong suspicion of economic buffoonery. You tend to hear such gripes just when prices should rise to discourage over-consumption and encourage production. The Wolf article, however, typifies the kind of attack on capitalism we hear increasingly from the “new right” (and see this).

Wolf, a former Homeland Security official in the first Trump Administration, says that large retailers like Walmart and Target are ripping off American consumers by raising prices on goods that are, in his judgement, “unaffected” by tariffs.

We’ll get into that, but first a quick disclaimer: I have no connection to Walmart or Target. Sure, I’ve shopped at those stores and I’ve filled a few prescriptions at a Walmart pharmacy. Maybe I have an ETF with an interest, but I have no idea.

Competition and Consumer Choice

Of course, no one forces consumers to shop at Walmart or Target. Those stores compete with a wide variety of outlets, including Costco and Amazon, the latter just a few clicks away. In a market, sellers price goods at what the market will bear, which ultimately serves to signal scarcity: a balancing between the cost of required resources and the value assigned by buyers. Unfortunately, in the case of tariffs, buyers and sellers of imports must deal with an artificial form of scarcity designed to extract revenue while benefitting other interests.

Wolf touts the “gift” of a free market for American businesses, as if private rights flow from government beneficence. He then decries a so-called betrayal by large retailers who would “price gouge” the American consumer in an effort to protect their profit margins. The free market is indeed a great thing! But his indignance is highly ironic as a pretext for defending tariffs and protectionism, given their destructive effect on the free operation of markets.

Broader Impacts

Wolf might be unaware that tariffs have an impact on a large number of domestically-produced goods that are not imported, but nevertheless compete with imports. When a tariff is charged to buyers of imports, producers of domestic substitutes experience greater demand for their products. That means the prices of these import-competing goods must rise. Furthermore, the effect can manifest even before tariffs go into effect, as consumers begin to seek out substitutes and as producers anticipate higher input costs.

Obviously, tariffs also impinge on producers who rely on imports as inputs to production. It’s not clear that Wolf understands how much tariffs, which represent a direct increase in costs, hurt these firms and their competitive positions.

“Expected” Does Not Mean “Unaffected”

Wolf cites the Federal Reserve’s Beige Book report (which he calls a “study”) to support his claim that businesses are gouging buyers for goods “unaffected” by tariffs. Here is one quote he employs:

“A heavy construction equipment supplier said they raised prices on goods unaffected by tariffs to enjoy the extra margin before tariffs increased their costs,” the Beige Book report said.“

Read that again carefully! Apparently Wolf, and whoever added this to the Fed’s Beige Book, thinks that being “unaffected by tariffs” includes firms whose future costs, including replacement of inventories, will be affected by tariffs! He goes on to say:

“… Walmart has already issued price hikes under the guise of tariff costs.“

The examples at his “price hikes” link were for Chinese goods in April and May, after Trump announced 145% tariffs on China in April. In mid-May, Trump said China would face a lower 30% tariff rate during a 90-day “pause” while a trade agreement was negotiated. It is now 55%, but the point is that retailers were forced to play a guessing game with respect to inventory replacement costs due to uncertainty imposed by Trump. They had a sound reason for marking up those items.

Fibbing on the Margin

Here’s an excerpt from Wolf’s diatribe that demonstrates his cluelessness even more convincingly:

“We all know many of these large retailers are sitting on comfortable, even expanded, profit margins because of the price hikes from COVID-19 that never came down. But it’s not enough for them. They want to fleece the American consumer and blame it on President Trump’s America First agenda.“

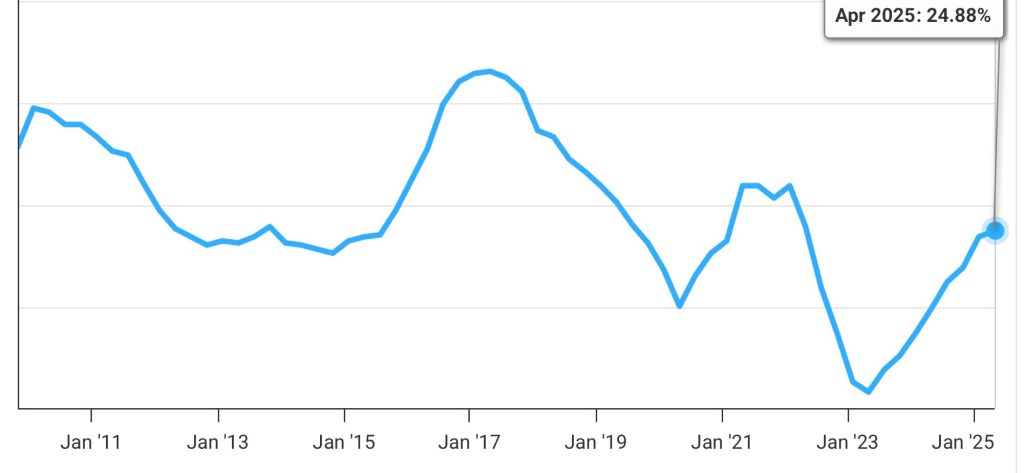

So let’s take a look at those profit margins that “never came down” after the pandemic, but in a longer historical context. Here are gross margins for Walmart since 2010:

Walmart’s margin today is about the same as the average for discount stores, and it is lower than for department stores, retailers of household and personal products, groceries, and footwear. Furthermore, it is lower today than it was ten years ago. While the margin increased a little during the pandemic, it fell in its aftermath, contrary to Wolf’s assertion. That the company has rebuilt margins steadily since 2023 should be viewed not as an indictment, but perhaps as a testament to improved managerial performance.

Wolf goes on to quote a former Walmart CEO who says that the 25 basis point increase in the gross margin in the latest quarter (from ~24.7% to 24.94%) indicates that the chain can “manage” the tariff impact. Of course it can, but that would not constitute “price gouging”.

A Trump Lackey

Of course, Wolf is taking his cues from Donald Trump, who has been bullying American businesses to “eat” the cost of his tariff onslaught, rather than passing them along to the ultimate buyers of imported goods. However, private businesses should not be expected to take orders from the President. This is not Mussolini’s Italy. Moreover, anyone familiar with tax incidence will understand that sellers are likely to eat some portion of a tariff (sharing the burden with buyers) without jawboning from the executive branch. That’s because buyers demand less at higher prices and sellers wish to avoid losing profitable sales, to the extent they can. But the dynamics of this adjustment process might take time to play out.

It’s also worth noting that a retailer might attempt to hold the line on certain prices in an uncertain cost environment. This uncertainty is a real cost inflicted by Trump. Meanwhile, pointing to increased prices for domestic goods, even if they are truly unaffected by tariffs, proves nothing without knowledge of the relevant cost and market conditions for those goods. It certainly doesn’t prove an “unpatriotic” attempt to cross subsidize imported goods.

In fact, one might say it’s unpatriotic for the federal government to restrict the market choices faced by American consumers and businesses, and for the President to tell American sellers that they better “eat” the cost of tariffs (or else?). And say, what happened to the contention that tariffs aren’t taxes?

Conclusion

Attacks on sellers attempting to recoup tariff costs are unfair and anti-capitalist. They are also somewhat disdainful of the economic sovereignty of American consumers, though not as much as the tariffs themselves. In the case described above, Chad Wolf would have us believe that sellers should not act on their expectations of near-term tariff increases. He also fails to recognize the impact of tariffs on import-competing goods and the cost of tariffs borne by producers who must rely on imported goods as inputs to production. Even worse, Wolf misrepresents some of the evidence he uses to make his case.

More generally, American businesses should not be bullied into taking a hit just because they serve customers who wish to buy imported goods. There is nothing unpatriotic about the freedom to choose what to goods to buy, what goods to stock, and how to maintain profitability in the face of government interference.

The federal government ran a budget surplus of $27 billion in June, much to the surprise of nearly everyone. The Trump Administration and MAGA-friendly media were eager to credit a big revenue boost from higher tariffs, which… ahem … they have assured us are notreally taxes. In any case, to attribute the June surplus to tariffs is flatly ridiculous. The truth is these “non-tax” magic revenue generators made a relatively small contribution to the apparent shift in the government’s fiscal position in June. And I say “apparent” because the surplus itself was something of a mirage.

Yes, tariffs brought in a total of almost $27B during June, which is about the same as the surplus recorded, but that was purely coincidental. It does not imply that tariffs “created” a surplus. Nor does it suggest that tariffs might just be able to balance the federal budget. Not a chance!

Here is one of two other sides of the story: the Treasury reported that the budget balance this June improved from a year ago by a total of $89 billion, from a deficit of $72B in June of 2024 to the aforementioned surplus of $27B in June 2025. Outlays were lower by about $38B this June, accounting for almost 43% of the improvement. Receipts were about $59B higher, with tariffs increasing by $20B relative to June 2024. So tariffs contributed just over a third of the boost in receipts. Altogether then, tariffs accounted for 22.5% of the improvement in the June budget balance between 2024 and 2025. That version of the story, as far as it goes, does not support the contention that tariffs “caused” the budget surplus in June, only that tariff revenue was a contributing factor.

Let’s dig a little deeper, however. Were it not for so-called “calendar adjustments” made by the Treasury, it would have reported a deficit of $70B in June. The reason? The first day of June fell on a Sunday this year, socertain payments were shifted to the last prior business day: Friday, May 30. That reduced June outlays substantially. Moreover, an extra business day in June 2025 added revenue. So the surplus in June was, in essence, an artifact of the calendar and had little to do with tariff revenue.

Incidentally, no one should be surprised by the growth of tariff revenue collected in June. When a tax rate more than triples (from a pre-Trump average of about 3% to 10% plus in June — net of tariff exclusions), one should expect revenue from that tax to increase substantially (and it was probably exaggerated by the extra business day).

Oh wait! Did I say tax?

With time, buyers will adjust and scale back their import purchases, reducing the revenue impact of the tariff hikes. However, we still don’t know how high tariffs will go. That means we could see substantially higher tariff revenue, though the demand response and a likely negative impact on incomes will cut into those gains. Either way, the revenue potential of tariffs is limited. Some estimates put the revenue impact of Trump’s tariffs at less than $250B annually. That seems conservative, but it’s significant revenue if it holds up. Still, it won’t come close to balancing a federal budget that’s almost $2 trillion in the hole. It certainly doesn’t justify a headlong dive into protectionism, which amounts to taking a crap on the economic freedom and prosperity of the American public.

Stablecoins are a very hot topic, and not only among crypto enthusiasts. This is “Crypto Week” in Congress, but current activity in the stablecoin (SC) space ranges from an explosion of transactions and issuance by banks and other institutions, plans for issuance by other businesses like large retailers, the introduction of new embedded SC features, laws affirming the right of use in non-crypto transactions, regulatory maneuvers, and central bank scrutiny.

The Digital Money Realm

An SC is a digital asset convertible to currency at a value pegged to some other asset with a stable market value. SCs are almost all pegged to the dollar, but they can be algorythmically pegged to a basket of currencies, Treasury securities, gold, silver, or other commodities, or a combination of various kinds of assets. Still, it’s thought that the growth of SCs will reinforce the dollar’s position as the world’s dominant currency.

SCs had their genesis and are still primarily used for settlement of transaction involving crypto-currencies and cross-border transactions. They function as a store of value and provide investors exposure to the underlying asset(s), but they are increasingly seen as transactions media as well. They offer a direct channel to instant settlement without other intermediaries and with low transaction costs.

Unfortunately, the purported stability of SCs has not always held up. In 2022, the collapse of the SC Terra/Luna demonstrated that a run on an SC is a real risk. Pending legislation in the U.S. will attempt to address this risk (see below). Tether is the dominant SC on the market today, and its issuer, Tether Ltd., claims to back it with 100% fiat currency reserves. However, those claims have come under suspicion with concerns about the true liquidity of their backing. Tether has other problems, including money laundering allegations. The bills now under consideration in the Congress would require a major change in the way Tether and other SC issuers do business in the U.S.

Crypto-Week Pending Legislation

SC issuers hold levels of reserves against their outstanding value, but currently only under various state regulations. That’s likely to change soon. Bipartisan legislation is moving through Congress: the so-called GENIUS Act was approved by the Senate in June; the STABLE Act in the House has many similar provisions.

The GENIUS and STABLE bills would require public disclosure, frequent audits, and establish 100 percent reserve requirements for so-called “payment” SCs. The bills also stipulate that reserves must be held in highly liquid assets like U.S. dollars, money market fund shares, and Treasury securities maturing within 93 days. This is likely a disappointment to “hard money” partisans who’d like to see SCs backed by precious metals. Both bills would also prohibit interest-bearing SCs, obviously an impediment to risk-taking by issuers and also a nod to banks hoping to avoid new competitive pressures. Altogether, the bills would make SCs more currency-like and less vehicles for saving or speculation of any kind.

A third piece of federal legislation, the so-called CLARITY Act, would sort out the regulatory roles of different federal agencies pertaining to digital assets.

CBDC

Central banks like the Federal Reserve have taken a keen interest in SCs, which amount to an alternative monetary system. Advocates of a Central Bank Digital Currency (CBDC) maintain that it would have greater stability and public trust than privately-issued SCs. No doubt a CBDC would facilitate investigation of fraud and money laundering, and supporters say it would help preserve the sovereignty of the U.S. monetary system.

However, a CBDC is off the table in the U.S. for the foreseeable “political” future. President Trump has issued an executive order (EO) prohibiting the development or issuance of a CBDC in the U.S. The EO asserts that a CBDC would not promote stability and in fact would do the opposite.

Opposition to a CBDC revolves around several issues: 1) it would cause an atrophy in the private development of digital assets and SCs in the U.S.; 2) a CBDC would create grave concerns about surveillance and potential use of the CBDC as an input to a social credit tool; 3) the alleged risk of a CBDC to the stability of the banking system. #3 is apparently in reference to possible disintermediation when a CBDC is substituted for traditional bank deposits — but SCs have been noted for that same risk.

Neither the GENIUS Act nor the STABLE Act explicitly prohibits a CBDC, which has riled a few conservatives. However, there are provisions in the GENIUS Act that effectively rule a CBDC out at a “retail” and consumer level.

A fourth piece of legislation, the Anti-CBDC Surveillance State Act, would prohibit the Federal Reserve from “… testing, studying, developing, creating, or implementing a central bank digital currency and bar the banks from using such a currency to implement monetary policy.” The bill was passed by the House of Representatives in May, but it has yet to clear the Senate. Some House members might like to have its major provisions incorporated into the current SC legislation, but that remains to be seen, and if such a revision was passed by the House it would require another Senate vote in any case.

Not Quite Like Cash

As a “programmable” currency, a CBDC could be used to control transactions deemed impermissible by a future “regime”. This would be a manifestation of what Dave Friedman calls “The Convergence of AI and the State”. His concerns extend to privately-issued SC’s as well, inasfar as SCs and other payment systems have us “sleepwalking into a cashless society”.

Privacy has been a downside to SCs and all blockchain transactions from the start, but there are several technological extensions that could protect SC transactions and accounts from nosy governments or nefarious actors. Taurus, a crypto custodian, has launched a Stablecoin contract for businesses with privacy features using so-called zero knowledge proofs that would satisfy “Know Your Customer” requirements and anti-money laundering laws, but without revealing amounts paid or the recipient’s identity. Still, there are legitimate concerns regarding access by regulators, and law enforcement could ultimately gain access to account and transaction data given a reasonable suspicion of wrongdoing. This will almost certainly be addressed in any SC legislation that makes it to Trump’s desk.

Macro Policy Implications

Will broader adoption of SCs compromise the ability of central banks to conduct monetary policy? Scott Sumner says no:

“The Fed will still control the monetary base, and they have almost unlimited ability to adjust both the supply and the demand for base money. This means they will be able to react to the creation of money substitutes as required to prevent any impact on macroeconomic objectives such as employment and the price level.”

When Sumner’s says the Fed controls the demand for base money, he refers to the interest rate the Fed pays on bank reserves.

As noted above, however, it’s widely feared that public substitution of SCs for bank deposits could drain bank reserves, adding variability to the broader demand for monetary assets, thus weakening the relationship between policy actions, the money stock, and other key variables.

Even if this is correct and Summer is wrong, the Federal Reserve should be treated as a special (but very important) case. That’s because the dollar is the dominant global currency, almost all SCs are backed by dollars, and essentially all SCs used in the U.S. will be backed by dollar-denominated assets should GENIUS-type legislation become law. That severely limits any potential disintermediation that SCs might otherwise cause. Control of bank reserves should be manageable, and therefore SCs will not meaningfully weaken the Fed’s controlof base money or the transmission of monetary policy.

Things are not so simple for countries having home currencies that play a minor role internationally. SC’s backed by other currencies or assets are then more likely to weaken the central bank’s control of domestic monetary assets. In fact, SCs might create greater vulnerability to “dollarization” in some countries, which would weaken the efficacy of domestic monetary control. If Sumner is correct, the existence of SCs would still add a layer of variability for these central banks, making policy adjustments more complex and error-prone.

Conclusion

Stablecoins are already huge in the crypto world and they are making inroads to the broader financial sector, factor payments, and everyday consumer decisions. Naturally they have attracted a great deal of interest in policy circles, both for their benefits and the risks they present. The purported liquidity and stability of SCs, together with a few prior missteps, make the legislation now before Congress a key to broader adoption, particularly the provisions on reserves and transparency. While not strictly a part of the legislation, the incorporation of privacy features will enhance the value of SCs to all users.

Conservatives and libertarians undoubtedly will welcome the proscription on development of a digital currency by the Fed. Private SCs backed by dollar reserves should allow the Fed to maintain ample control over the monetary base and the supply of monetary assets. Moreover, the growth of dollar-backed SCs will strengthen the dollar’s dominance in international trade and finance. However, while stablecoins can and do reduce transaction costs in a variety of circumstances, dollar-backed SCs cannot be better stores of value than the dollar itself, which we know has had its shortcomings over the years.

Donald Trump’s latest volley against the Federal Reserve accuses the central bank of fixing interest rates at artificially high levels compared to rates in other developed countries. He repeatedly demands that the Fed make a large cut to its federal funds rate target, in the apparent belief that other rates will immediately fall with it. While a highly imperfect analogy, that’s a bit like saying that long-term parking in New York City would be cheaper if only hourly rates were cut to what’s charged in Omaha, and with only favorable consequences. Don’t tell Mamdani!

Trump believes the Fed’s restrictive monetary policy is preventing the economy from achieving its potential under his policies. He also argues that the Fed’s “high-rate” policy is costing the federal government and taxpayers hundreds of billions in excessive interest on federal debt. High rates can certainly impede growth and raise the cost of debt service. The question is whether there is a policy that can facilitate growth and reduce borrowing costs without risking other objectives, most notably price stability.

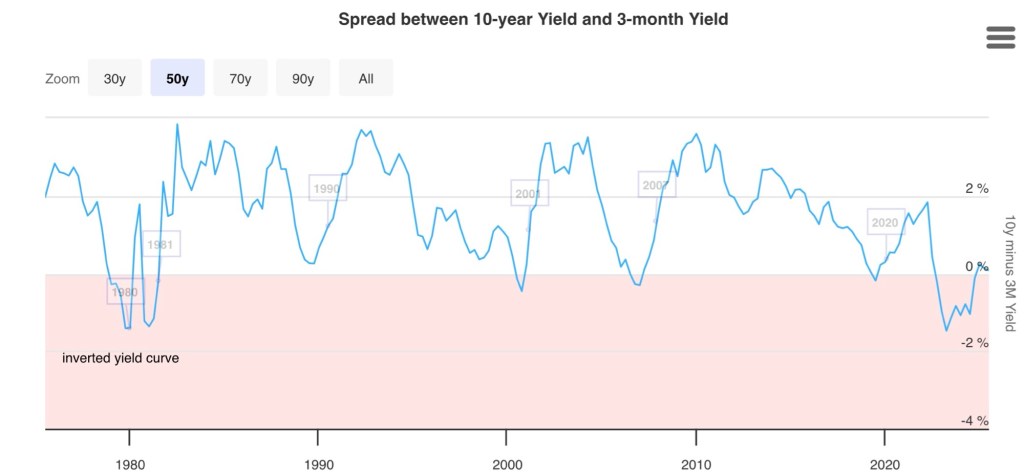

Delusions of Control

The financial community understands that the Fed does not directly control rates paid by the Treasury on federal debt. The Fed has its most influence on rates at the short end of the maturity spectrum. Rates on longer-term Treasury notes and bonds are subject to a variety of market forces, including expected inflation, the expected future path of federal deficits, and the perceived direction of the economy, to name a few. The Fed simply cannot dictate investor sentiments and expectations, and the ongoing flood of new Treasury debt complicates matters.

Another fundamental lesson for Trump is that cross-country comparisons of interest rates are meaningless outside the context of differing economic conditions. Market interest rates are driven by things that vary from one country to another, such as expected inflation rates, economic policies, currency values, and the strength of the home economy. Differences in rates are always the result of combinations of circumstances and expectations, which can be highly varied.

A Few Comparisons

A few examples will help reinforce this point. Below, I compare the U.S. to a few other countries in terms of recent short-term central bank rate targets and long-term market interest rates. Then we can ask what conditions explain these divergencies. For reference, the current fed funds rate target range is 4.25 – 4.5%, while 10-year Treasury bonds have traded recently at yields in the same range. Current U.S. inflation is roughly 2.5%.

It’s important to remember that markets attempt to price bonds to compensate buyers for expected future inflation. Currently, the10-year “breakeven” inflation implied by indexed Treasury bonds is about 2.35% (but it is closer to 3% at short durations). That means unindexed Treasury bonds yielding 4.4% offer an expected real yield just above 2%. Accounting for expected inflation often narrows the gap between U.S. interest rates and foreign rates, but not always.

Switzerland: The Swiss National Bank maintains a policy rate of 0%; the rate on 10-year Swiss government bonds has been in the 0.5 – 0.7% range. Why can’t we have Swiss-like interest rates in the U.S.? Is it merely intransigence on the part of the Fed, as Trump would have us believe?

No. Inflation in Switzerland is near zero, so in terms of real yields, the gap between U.S. and Swiss rates is closer to 1.4%, rather than 3.8%. But what of the remaining difference? Swiss government debt, even more than U.S. Treasury debt, attracts investors due to the nation’s “safe-haven” status. Also, U.S. yields are elevated by our ballooning federal debt and uncertainties related to trade policy. Economic growth is also somewhat stronger in the U.S., which tends to elevate yields.

These factors give the Fed reason to be cautious about cutting its target rate. It needs evidence that inflation will continue to trend down, and that policy uncertainties can be resolved without reigniting inflation.

Euro Area: The European Central Bank’s (ECB) refinancing rate is now 2.15%. Meanwhile, the 10-year German Bund is yielding around 2.6%, so both short-term and long-term rates in the Euro area are lower than in the U.S. In this case, the difference relative to U.S. rates is not large, nor is it likely attributable to lower expected inflation. Instead, sluggish growth in the EU helps explain the gap. Federal deficits and the ongoing issuance of new Treasury debt also keep U.S. yields higher. Treasury yields may also reflect a premium for volatility due to heavier reliance on foreign investors and private funds, who tend to be price sensitive.

Japan: The Bank of Japan’s (BOJ) policy rate is currently 0.5%. Yields on Japanese 10-year government bonds have recently traded just below 1.5%. Expected inflation in Japan has been around 2.5% this year, which means that real yields are sharply negative. The BOJ has tightened policy to bring inflation down. The nearly 3% gap between U.S. and Japanese bond yields reflects very weak economic growth in Japan. In addition, despite a very high debt to GDP ratio, the depressed value of the yen discourages investment abroad, helping to sustain heavy domestic holdings of government debt.

Blame and Backfire

Trump might well understand the limits of the Fed’s control over interest rates, but if he does, then this is exclusively a case of scapegoating. Cross-country differences in interest rates represent equilibria that balance an array of complex conditions. These range from disparate rates of inflation, the strength of economic growth, currency values, fiscal imbalances, and the character of the investor base. .

Investor expectations obviously play a huge role in all this. A central bank like the Fed cannot dictate long-term yields, and it can do much more harm than good by attempting to push the market where it does not want to go. That type of aggressiveness can spark changes in expectations that undermine policy objectives. It’s childish and destructive to insist that interest rates can and should be as low in the U.S. as in countries facing much different circumstances.