About a year ago I wrote about the sketchy nature of carbon credits (or “offsets”), which are purchased by people or entities whose actions generate CO2 emissions they’d like to offset. Those actions would include Taylor Swift’s private air travel, electric power generation, and many other activities whose participants wish to have “greenwashed”.

One short digression before I get started: see those black clouds of CO2 in the image above? Well, carbon dioxide doesn’t really look like that. In fact, CO2 is transparent. Trees breathe it! Visually, it’s less obvious than the greenhouse gas known as water vapor in those puffy white clouds, but virtually every image you’ll ever see on-line depicting CO2 emissions shows dark, roiling smoke. I just hate to spoil the scary effect, but there it is.

Back to carbon credits, which help fund projects that offset CO2 emissions (at least theoretically), such as planting new forest acreage (which would absorb CO2 … someday) or preventing deforestation. Other types of offset activities include investment in renewable energy projects and carbon capture technology. So, for example, if a utility’s power generation emits CO2, the creation or preservation of some amount of forested acreage can serve as a carbon sink adequate to offset the utility’s emissions. Net zero! Or so the utility might claim.

If only it were that simple! Paul Mueller explains that the incentive structure of these arrangements is perverse. What if credits are sold on the basis of supposed efforts to preserve forests that were never at risk to begin with? In fact, the promise of revenue from the sale of credits may be a powerful incentive to falsely present forested lands as targets for development. For that matter, cutting forestland for lumber makes more sense if it can be replanted immediately in exchange for revenue from the sale of carbon credits. And newly planted acreage won’t lead to absorption of much CO2 for many years, until the trees begin to mature. Then there are the risks of forest fires or disease that could compromise a forest’s ultimate value as a carbon sink.

Whether through fraud, calamity, or mismanagement, the sad truth is that projects serving as a basis for credits have done far less to reduce deforestation than promised. On top of that, another issue plaguing carbon markets for some time has been double counting of offsets, which can occur under several circumstances. Ultimately, CO2 emissions themselves may have done more to promote the growth of forests than purchases of carbon credits, because CO2 gives life to vegetation!

Obviously, the purchase of offsets raises the incremental cost of any project having CO2 emissions. The incidence of this added cost is borne to a large extent by consumers, especially because power demand is fairly inelastic. The craziness of offset logic may even dictate the purchase of offsets when a plant emitting more CO2 (e.g., coal) is replaced by a plant emitting less (natural gas), because the replacement would still emit carbon!

Some carbon offsets help pay for the construction of renewable power facilities like wind and solar farms. These renewable power facilities contribute to the power supply, of course, but wind turbines and solar farms typically operate at a small fraction of nameplate capacity due to the intermittency of wind and sunshine. Thus, these offsets are far less than complete. And from that low rate of renewable utilization we can deduct another fraction: periods of actual utilization often occur when no one wants the power, and while utilities can sell that excess power into the grid, it doesn’t replace other power at those times and it therefore doesn’t contribute to reductions in CO2 emissions.

Claims of achieving net zero are very much in vogue in the corporate world, and for a few related reasons. One is that they help keep activists and protesters away from the gates. There are, however, plenty of activists serving on corporate boards, in the executive suite, and among regulators.

The purchase of carbon offsets by “socially responsible corporations” might put stakeholder pressure on competitors who are “insufficiently green”. That would help to compensate for the higher costs imposed by offsets. After all, carbon credits are not cheap. In fact, smaller competitors might struggle to fund additional outlays for the credits.

Finally, claims of carbon neutrality also help with another constituency: “woke” investors. “Achieving” net zero boosts a firm’s so-called ESG score, presumed to reflect soundness in terms of environmental (E) and social (S) responsibility, as well as the quality of internal governance (G). With firms jockeying for ESG improvements, they help keep the offset charade going.

There is no common standard for calculating ESG, and there is considerable variance in ESG scores across rating firms. This should be cause for great skepticism, but too many investors are vulnerable to suggestions that screening on ESGs can enable both social responsibility and better returns. Sadly, they are sometimes paying higher fees for the privilege. The ESG fad among these investors might have helped fulfill hopes of greater returns for a while, but the imagined ESG advantage may have faded.

Carbon credits or offsets are plagued by bad incentives that often lead to wasteful outlays if not outright fraud. At present, they generally fail to reduce atmospheric CO2 as promised and they contribute to higher costs, which are passed on to consumers. They also serve as an unworthy basis for higher ESG scores, which are something of a sham in any case.

There have been efforts underwayto improve the quality and legitimacy of carbon offsets. Some of this is voluntary due diligence on the part of purchasers. The effort also includes various NGOs and regulators. Ultimately, the push for quality is likely to push the price of offsets upward dramatically. Perhaps offsets will become more credible, but they won’t come cheap. The cost of achieving net zero targets will largely come out of consumers’ pockets, and those net zeros will still be nominal at best.

First, a preliminary issue: many resources qualify as commons in the very broadest sense, yet free societies have learned over time that many resources are used much more productively when property rights are assigned to individuals. For example, modern agriculture owes much to defining exclusive property rights to land so that conflicting interests don’t have to compete (e.g,, the farmer and the cowman). Federal land is treated as a commons, however. There is a rich history on the establishment of property rights, but within limits, the legal framework in place can define whether a resource is treated as a commons, a club good, or private property. The point here is that there are substantial economic advantages to preserving strong property rights, rather than treating all resources as communal.

The authors of the planetary commons (PC) paper present a rough sketch for governance over use of the planet’s resources, given their belief that a planetary crisis is unfolding before our eyes. The paper has two main thrusts as I see it. One is to broadly redefine virtually all physical resources as common pool interests because their use, in the authors’ view, may entail some degree of external cost involving degradation of the biosphere. The second is to propose centralized, “planetary” rule-making over the amounts and ways in which those resources are used.

It’s an Opinion Piece

The PC paper is billed as the work product of a “collaborative team of 22 leading international researchers”. This group includes four attorneys (one of whom was a lead author) and one philosopher. Climate impact researchers are represented, who undoubtedly helped shape assumptions about climate change and its causes that drive the PC’s theses. (More on those assumptions in a section below.) There are a few social scientists of various stripes among the credited authors, one meteorologist, and a few “sustainability”, “resilience”, and health researchers. It’s quite a collection of signees, er… “research collaborators”.

Grabby Interventionists

The reasoning underlying a “planetary commons” (PC) is that the planet’s biosphere qualifies as a commons. The biosphere must include virtually any public good like air and sunshine, any common good like waterways, or any private good or club good. After all, any object can play host to tiny microbes regardless of ownership status. So the PC authors characterization of the planet’s biosphere as a commons is quite broad in terms of conventional notions of resource attributes.

We usually think of spillover or external costs as arising from some use of a private resource that imposes costs on others, such as air or water pollution. However, mere survival requires that mankind exploit both public and non-public resources, acts that can always be said to impact the biosphere in some way. Efforts to secure shelter, food, and water all impinge on the earth’s resources. To some extent, mankind must use and shape the biosphere to succeed, and it’s our natural prerogative to do so, just like any other creature in the food chain.

Even if we are to accept the PC paper’s premise that the entire biosphere should be treated is a commons, most spillovers are de minimus. From a public policy perspective, it makes little sense to attempt to govern over such minor externalities. Monitoring behavior would be costly, if not impossible, at such an atomistic level. Instead, free and civil societies rely on a high degree of self-governance and informal enforcement of ethical standards to keep small harms to a minimum.

Unfortunately, the identification and quantification of meaningful spillover costs is not always clear-cut. This has led to an increasingly complex regulatory environment, an increasingly litigious business environment, and efforts by policymakers to manage the detailed inputs and outputs of the industrial economy.

All of that is costly in its own right, especially because the activities giving rise to those spillovers often enable large welfare enhancements. Regulators and planners face great difficulties in estimating the costs and benefits of various “correctives”. The very undertaking creates risk that often exceeds the cost of the original spillover. Nevertheless, the PC paper expands on the murkiest aspects of spillover governance by including “… all critical biophysical Earth-regulating systems and their functions, irrespective of where they are located…” as part of a commons requiring “… additional governance arrangements….”

Adoption of the PC framework would authorize global interventions (and ultimately local interventions, including surveillance) on a massive scale based on guesswork by bureaucrats regarding the evolution of the biosphere.

Ostrom Upside Down

Not only would the PC framework represent an expansion of the grounds for intervention by public authorities, it seeks to establish international authority for intervention into public and private affairs within sovereign states. The authors attempt to rationalize such far-reaching intrusions in a rather curious way:

“Drawing on the legacy of Elinor Ostrom’s foundational research, which validated the need for and effectiveness of polycentric approaches to commons governance (e.g., ref. 35, p. 528, ref. 36, p. 1910), we propose that a nested Earth system governance approach be followed, which will entail the creation of additional governance arrangements for those planetary commons that are not yet adequately governed.”

Anyone having a passing familiarity with Elinor Ostrom’s work knows that she focused on the identification of collaborative solutions to common goods problems. She studied voluntary and often strictly private efforts among groups or communities to conserve common pool resources, as opposed to state-imposed solutions. Ostrom accepted assigned rights and pricing solutions to managing common resources, but she counseled against sole reliance on market-based tools.

Surely the PC authors know they aren’t exactly channeling Ostrom:

“An earth system governance approach will require an overarching global institution that is responsible for the entire Earth system, built around high-level principles and broad oversight and reporting provisions. This institution would serve as a universal point of aggregation for the governance of individual planetary commons, where oversight and monitoring of all commons come together, including annual reporting on the state of the planetary commons.”

Polycentricity was used by Ostrom to describe the involvement of different, overlapping “centers of authority”, such as individual consumers and producers, cooperatives formed among consumers and producers, other community organizations, local jurisdictions, and even state or federal regulators. Some of these centers of authority supersede others in various ways. For example, solutions developed by cooperatives or lower centers of authority must align with the legal framework within various government jurisdictions. However, as David Henderson has noted, Ostrom observed that management of pooled resources at lower levels of authority was generally superior to centralized control. Henderson quotes Ostrom and a co-author on this point:

“When users are genuinely engaged in decisions regarding rules affecting their use, the likelihood of them following the rules and monitoring others is much greater than when an authority simply imposes rules.”

The authors of the PC have something else in mind, and they bastardize the spirit of Ostrom’s legacy in the process. For example, the next sentence is critical for understanding the authors’ intent:

“If excessive emissions and harmful activities in some countries affect planetary commons in other areas—for example, the melting of polar ice—strong political and legal restrictions for such localized activities would be needed.”

Of course, there are obvious difficulties in measuring impacts of various actions on polar ice, assigning responsibility, and determining the appropriate “restrictions”. But in essence, the PC paper advocates for a top-down model of governance. Polycentrism is thus reduced to “you do as we say”, which is not in the spirit of Ostrom’s research.

Planetary Governance

Transcending national sovereignty on questions of the biosphere is key to the authors’ ambitions. At a bare minimum, the authors desire legally-binding commitments to international agreements on environmental governance, unlike the unenforceable promises made for the Paris Climate Accords:

“At present, the United Nations General Assembly, or a more specialized body mandated by the Assembly, could be the starting point for such an overarching body, even though the General Assembly, with its state-based approach that grants equal voting rights to both large countries and micronations, represents outdated traditions of an old European political order.”

But the votes of various “micronations” count for zilch when it comes to real “claims” on the resources of other sovereign nations! Otherwise, there is nothing “voluntary” about the regime proposed in the PC paper.

“A challenge for such regimes is to duly adapt and adjust notions of state sovereignty and self-determination, and to define obligations and reciprocal support and compensation schemes to ensure protection of the Earth system, while including comprehensive stewardship obligations and mandates aimed at protecting Earth-regulating systems in a just and inclusive way.”

So there! The way forward is to adopt the broadest possible definition of market failure and global regulation of any and all private activity touching on nature in any way. And note here a similarity to the Paris Accords: achieving commitments would fall to national governments whose elites often demonstrate a preference for top-down solutions.

Ah Yes, Redistribution

It should be apparent by now that the PC paper follows a now well-established tradition in multi-national climate “negotiations” to serve as subterfuge for redistribution (which, incidentally, includes the achievement of interspecies justice):

“For instance, a more equal sharing of the burdens of climate stabilization would require significant multilateral financial and technology transfers in order not to harm the poorest globally (116).”

The authors insist that participation in this governance would be “voluntary”, but the following sentence seems inconsistent with that assurance:

“… considering that any move to strengthen planetary commons governance would likely be voluntarily entered into, the burdens of conservation must be shared fairly (115).”

Wait, what? “Voluntary” at what level? Who defines “fairness”? The authors approvingly offer this paraphrase of the words of Brazilian President Lula da Silva,

“… who affirmed the Amazon rainforest as a collective responsibility which Brazil is committed to protect on behalf of all citizens around the world, and that deserves and justifies compensation from other nations (117).”

Let Them Eat Cake

Furthermore, PC would require de-growth and so-called “sufficiency” for thee (i.e., be happy with less), if not for those who’ll design and administer the regime.

“… new principles that align with novel Anthropocene dynamics and that could reverse the path-dependent course of current governance. These new principles are captured under a new legal paradigm designed for the Anthropocene called earth system law and include, among others, the principles of differentiated degrowth and sufficiency, the principle of interconnectivity, and a new planetary ethic (e.g., principle of ecological sustainability) (134).”

If we’re to take the PC super-regulators at their word, the regulatory regime wouldimpinge on fertility decisions as well. Just who might we trust to govern humanity thusly? If we’re wise enough to applythe Munger Test, we wouldn’t grant that kind of power to our worst enemy!

Global Warmism

The underlying premise of the PC proposal is that a global crisis is now unfolding before our eyes: anthropomorphic global warming (AGW). The authors maintain that emissions of carbon dioxide are the cause of rising temperatures, rapidly rising sea levels, more violent weather, and other imminent disasters.

“It is now well established that human actions have pushed the Earth outside of the window of favorable environmental conditions experienced during the Holocene…”

“Earth system science now shows that there are biophysical limits to what existing organized human political, economic, and other social systems can appropriate from the planet.”

For a variety of reasons, both of these claims are more dubious than one might suppose based on popular narratives. As for the second of these, mankind’s limitless capacity for innovation is a more powerful force for sustainability than the authors would seem to allow. On the first claim, it’s important to note that the PC paper’s forebodings are primarily based on modeled, prospective outcomes, not historical data. The models are drastically oversimplified representations of the earth’s climate dynamics driven by exogenous carbon forcing assumptions. Their outputs have proven to be highly unreliable, overestimating warming trends almost without exception. These models exaggerate climate sensitivity to carbon forcings, and they largely ignore powerful natural forcings such as variations in solar irradiance, geological heating, and even geological carbon forcings. The models are also notorious for their inadequate treatment of feedback effects from cloud cover. Their predictions of key variables like water vapor are wildly in error.

The measurement of the so-called “global temperature” is itself subject to tremendous uncertainty. Weather stations come and go. They are distributed very unevenly across land masses, and measurement at sea is even sketchier. Averaging all these temperatures would be problematic even if there were no other issues… but there are. Individual stations are often sited poorly, including distortions from heat island effects. Aging of equipment creates a systematic upward bias, but correcting for that bias (via so-called homogenization) causes a “cooling the past” bias. It’s also instructive to note that the increase in global temperature from pre-industrial times actually began about 80 years prior to the onset of more intense carbon emissions in the 20th century.

Climate alarmists often speak in terms of temperature anomalies, rather than temperature levels. In other words, to what extent do temperatures differ from long-term averages? The magnitude of these anomalies, using the past several decades as a base, tend to be anywhere from zero degrees to well above one degree Celsius, depending on the year. Relative to temperature levels, the anomalies are a small fraction. Given the uncertainty in temperature levels, the anomalies themselves are dwarfed by the noise in the original series!

Pick Your Own Tipping Point

It seems that“tipping point” scares are heavily in vogue at the moment, and the PC proposal asks us to quaff deeply of these narratives. Everything is said to be at a tipping point into irrecoverable disaster that can be forestalled only by reforms to mankind’s unsustainable ways. To speak of the possibility of other causal forces would be a sacrilege. There are supposed tipping points for the global climate itself as well as tipping points for the polar ice sheets, the world’s forests, sea levels and coastal environments, severe weather, and wildlife populations. But none of this is based on objective science.

For example, the 1.5 degree limit on global warming is a wholly arbitrary figure invented by the IPCC for the Paris Climate Accords, yet the authors of the PC proposal would have us believe that it was some sort of scientific determination. And it does not represent a tipping point. Cliff Mass explains that climate models do not behave as if irreversible tipping points exist.

Likewise, the rise of sea levels has not accelerated from prior trends, so it has nothing to do with carbon forcing.

One thing carbon forcings have accomplished is a significant greening of the planet, which if anything bodes well for the biosphere

What about the disappearance of the polar ice sheets? On this point, Cliff Mass quotes Chapter 3 of the IPCC’s Special Report on the implications of 1.5C or more warming:

“there is little evidence for a tipping point in the transition from perennial to seasonal ice cover. No evidence has been found for irreversibility or tipping points, suggesting that year-round sea ice will return given a suitable climate.”

The PC paper also attempts to connect global warming to increases in forest fires, but that’s incorrect: there has been no increasing trend in forest fires or annual burned acreage. If anything, trends in measures of forest fire activity have been negative over the past 80 years.

Concluding Thoughts

The alarmist propaganda contained in the PC proposal is intended to convince opinion leaders and the public that they’d better get on board with draconian and coercive steps to curtail economic activity. They appeal to the sense of virtue that must always accompany consent to authoritarian action, and that means vouching for sacrifice in the interests of environmental and climate equity. All the while, the authors hide behind a misleading version of Elinor Ostrom’s insights into the voluntary and cooperative husbandry of common pool resources.

One day we’ll be able to produce enough carbon-free energy to accommodate high standards of living worldwide and growth beyond that point. In fact, we already possess the technological know-how to substantially reduce our reliance on fossil fuels, but we lack the political will to avail ourselves of nuclear energy. With any luck, that will soften with installations of modular nuclear units.

Ultimately, we’ll see advances in fusion technology, beamed non-intermittent solar power from orbital collection platforms, advances in geothermal power, and effective carbon capture. Developing these technologies and implementing them at global scales will require massive investments that can be made possible only through economic growth, even if that means additional carbon emissions in the interim. We must unleash the private sector to conduct research and development without the meddling and clumsy efforts at top-down planning that typify governmental efforts (including an end to mandates, subsidies, and taxes). We must also reject ill-advised attempts at geoengineered cooling that are seemingly flying under the regulatory radar. Meanwhile, let’s save ourselves a lot of trouble by dismissing the interventionists in the planetary commons crowd.

The interchange above is just a few miles from my new home. It’s the world’s largest “diverging diamond” design and it usually works quite well, so I was interested to see this video discussing both its benefits and the conditions under which it hasn’t performed well.

Unfortunately, the video maintains a dubious focus on car dependence in most urban areas. The tale it tells is daunting… and if the reaction on Reddit is any indication, it seems to excite the populist mind. The narrator blames car dependence and sprawl on poor urban planning. I agree in a sense, and I’ll even stipulate that our car dependence is often excessive, but not because anyone could have “planned” better. Top-down planning is notoriously failure-prone. Rather, the corrective is something the creators of the video never contemplate: effective pricing for the use of roads.

There is deserved emphasis near the end of the video on the cost of building and maintaining roads and interchanges. For example, the cost of the interchange above was $74.5 million when it was built about 15 years ago. That sounds exorbitant, and it’s natural for people (and especially urban planners) to question the necessity of building an interchange of that magnitude in what many feel “should be” an outlying district. Did sprawl make it necessary? Can that be avoided in a growing region? What can or should be done?

Good Interchange Design

The interchange in question is at I-75 and University Parkway in Sarasota, FL. It’s used by many drivers to access a large shopping mall, other commercial centers, and nearby residential areas. The video stresses the diverging diamond’s effectiveness and safety in handling high flows of traffic. The design reduces the number of conflict points relative to conventional diamond interchanges, especially for crossing traffic.

Both diverging diamonds and conventional diamond interchanges have advantages over cloverleaf designs. While the latter have no crossover conflict points, they require more land use. They also create additional complexities for grading and drainage, and they are often constrained in the length of space available for left-turn merges. Furthermore, a cloverleaf places more severe limits on traffic flow. Flyover ramps are another alternative that can save space but entail greater expense.

The interchange in question serves an area of rapid growth. Residents increasingly complain about traffic, especially when “snow birds” are in town during the winter months. The video shows that even the diverging diamond has problems once traffic reaches a certain volume. But new residential communities and commercial areas continue to come on-line, adding to traffic flows and requiring additional roads and infrastructure. Again, the narrator believes the resulting traffic and sprawl could have been avoided, and he’s partly correct as far as that goes.

Sprawl Reflects Preferences

The video fails to consider important qualifications to the “car dependence” critique of suburban sprawl. For example, many people like to use their cars and enjoy the freedom of mobility their cars confer. More importantly, most people prefer to live in low-density residential environments rather than dense urban neighborhoods, or even the kinds of communities depicted as ideal in the video. I’m one of those people. More space, more privacy, and more greenery (though I grant that sprawling mall parking lots are not my favorite aesthetic).

Joel Kotkin presents data along those lines, quoting research by Jessica Trounstine, who says, “preferences for single-family development are ubiquitous.” And low-density communities have broad appeal across demographics, as noted by Kotkin:

“Even in blue states, the majority of ethnic minorities live in suburbs, who have accounted for virtually all the suburban growth over the past decade. William Frey of the Brookings Institution notes that in 1990 roughly 20 percent of suburbanites were non-white. That rose to 30 percent in 2000 and 45 percent in 2020.”

Urban Planning Myopia

As to the video’s emphasis on car dependence, its most serious omission is a failure to recognize the economics of pricing. Road use comes with various costs, but the key here is the zero price at the margin for using specific routes, interchanges, bridges, and suburban parking lots. There are many exceptions to be sure, but the video makes no mention of road pricing as a development tool. Nor does it consider “socialized roads” as the chief cause of ever-expanding demands for roads, parking, and the all-too-typical failure of these ersatz “commons”.

The federal government is complicit in this. After all, the interstate highway system was a federal initiative, and interchanges (along with concomitant commercial development) are integral to its success. Interstate highways often supplemented regional efforts to facilitate commuting to cities from distant suburbs. More recently, Joe Biden’s Infrastructure Investment and Jobs Act of 2021 added $110 billion a year from the government’s general fund to subsidize highways and bridges. It should be no surprise that federal gas taxes don’t fund these subsidies. (Gas taxes are user fees only in a vague sense, as they don’t price specific routes at the margin).

More Roads, Trains, Buses?

There are two knee-jerk reactions to congested roads. The first is a tendency to double-down on invested plant, building more, bigger, and wider roads in the hope that they can handle the growing traffic load. Presumably this must be funded by taxpayers, as in the past, and seldom if ever by charging per marginal use of these facilities. This “solution” basically calls for more socialized roads.

The second knee-jerk reaction to congestion, and it is also a reaction to the real or presumed shortcomings of a “paved paradise”, is to call for more buses, streetcars, or light rail. But mass transit systems seldom pay for their operating costs let alone their capital costs. One of the reasons, of course, is that they must compete with free roads!

What else might the urban planners have us do? We can’t just tear down the sprawling developments and road infrastructure and start over. However, we can accomplish a few other things like: 1) raise revenue from users to make the upkeep of road infrastructure self-funding; 2) minimize congestion, emissions, and time-use while improving safety; and 3) stem growth in demand that eventually would require more lanes, more parking, and other measures to maximize traffic flow. Pricing the actual use of roads would do all these things in greater or lesser degree, and it would more effectively balance development preferences with costs. In turn, positive road-use prices would incentivize other development models such as the “human-centric” communities the video’s narrator finds so attractive.

Those Who Benefit Shall Pay

Tolls for the use of roads and bridges (and paid parking) are hardly new ideas. Tolls on bridges were a natural continuation of fees charged by operators of ferry boats. Tolling was instituted by large landholders to extract rents from anyone wishing to traverse their property, and only later was used as a mechanism for funding road construction and maintenance. But like any price, tolls serve to ration the availability of a resource.

Today, tolling in the U.S. is an increasingly important source of funding for highways and bridges. This importance is growing due to a less sanguine outlook for gas tax collections. In any case, tolls are often more advantageous politically than taxes. Technological advance has allowed tolling to become more cost effective as well. In Florida, for example, the SunPass system allows drivers to cruise through toll collection points at moderate speeds. It’s also used for parking at certain facilities like airports. SunPass holders are required to set up automatic “recharge” of their available balance for toll payments. Similar systems are in place in other states.

Technology has enabled dynamic congestion pricing to be implemented by commercial interests like Uber and Lyft. This means that price responds to demand and supply conditions in real time. In coming years, congestion pricing is likely to be instituted by jurisdictions experiencing heavy traffic volumes. New York City’s congestion pricing plan has stalled, but it would charge a toll on vehicles using Manhattan streets below Central Park.

Law of Demand

Tolls at interchanges like the one at I-75 and University Parkway would help to allocate resources more efficiently. First, the mechanics could be simple enough in concept, but toll booths are probably out of the question, and toll authorities would have to sort through various administrative issues.

Let’s suppose SunPass was put to use here, with the revenue distributed to several jurisdictions or agencies responsible for maintaining the interchange and a defined set of connecting streets. When a driver exits I-75 to University, enters I-75 from University, or uses the through lanes on University, the SunPass transponder in their vehicle would communicate with the toll system to record their passage, and their account would be charged the appropriate toll. The charge might differ for through lanes versus I-75 entry or exit. Over the course of a month, tolls on various roads and interchanges would accumulate and be summarized by road or interchange on a statement for the driver.

Vehicles without SunPass (or another toll system partnering with SunPass) would have to be charged via photo identification of tags with billing by mail once a month. This is already a feature of toll roads in Florida (and other states) when vehicles without a SunPass use the SunPass lanes. The volume of mail billing would increase substantially, but that is not an obstacle in principle.

One other wrinkle would allow existing residents of neighborhoods with street entrances within one or two miles of the interchange to receive discounted tolls. That seems fair, but the danger is that discounts of this kind, if extended too far, would blunt incentives that otherwise discourage overuse and underpriced road sprawl. It would also add another layer of complexity to the tolling system.

The behavior of drivers will change in response to tolls. They derive benefits from using particular interchanges which depend upon the importance of errands or appointments in each vicinity, the distance and convenience of other shopping areas, the time of day, and the time saved by using any one route instead of alternates. The toll paid for using an interchange might depend on the size of vehicle, the time of day, or some measure of average congestion at that time of day. A higher toll prompts drivers to consider other routes, other shopping areas (including on-line shopping), or different times of day for those errands. Thus, tolls will redistribute traffic across space and time and are likely to reduce overall traffic at the most congested interchanges, at least at peak hours when tolls are highest.

Smart Pricing

The advent and installation of more sophisticated tolling infrastructure will enable “smart roads”, time-of-day pricing, or even dynamic congestion pricing on some routes. Integrating dynamic pricing with information systems guiding driver decisions about route choice and timing would be another major step. Implementing sophisticated route pricing systems like this will take time, but ultimately the technology will allow tolls to be applied broadly and efficiently… if we allow it to happen.

Private Vs. Public

The private sector is likely to play a greater role in a world of more widespread tolling. To some extent this will take the form of more privately-owned roads. Short of that, many toll roads and smart roads will be privately administered and operated. Private concerns will also play a major role in provisioning infrastructure and systems for more widespread and sophisticated toll roads.

There is a long history of private roads in the U.S. Robert P. Murphy offers a brief summary:

“… many analysts simply assume, because currently the government virtually monopolizes the production and administration of roads, that it must always have done so. And yet, from the 1790s through the 1830s, the private sector was responsible for the creation and operation of many turnpikes. According to economist Daniel Klein, ‘The turnpike companies were legally organized like corporate businesses of the day. The first, connecting Philadelphia and Lancaster, was chartered in 1792, opened in 1794, and proved significant in the competition for trade.’3 ‘By 1800,’ Klein reports, ‘sixty-nine companies had been chartered’ in New England and the Middle Atlantic states. Merchants would often underwrite the expense of building a turnpike, knowing that it would bring in extra traffic to their businesses.”

In Norway and Sweden, most roads are owned and operated privately, though most of the private roads are local. The funding is generally provided by property owners along those routes. Private roads are increasingly common in the U.S., but they are mostly confined to private communities funded by residents. Broader private ownership of roads, and tolling, is likely to occur in the U.S. as governments at all levels struggle with issues of funding, maintenance, traffic control, and growth.

Pricing For Scarcity

There will be political obstacles to widespread tolling and road congestion pricing. Questions of equity and privacy will be raised, but pricing may hold the key to achieving more equitable outcomes. Greater reliance on tolls would avoid regressive tax increases, and selective tolls themselves might well have a progressive incidence, to the extent that congestion tends to be high in prosperous commercial districts. It would make alternatives like mass transit more competitive and viable as well. Furthermore, price signals will cause geographic patterns of commerce and development to shift, potentially encouraging the kinds of high-density, pedestrian communities long-favored by urban planners.

Urban sprawl and auto dependence are old targets of the urban planning community, not to mention the populist left. But those critics rely on a stylized characterization of geographic and social arrangements that happen to be preferred by masses of individuals. As an economist, I sympathize with the critics because those preferences are revealed under incentives that do not reflect the scarcity and real costs of roads and driving. However, in the absence of adequate price incentives, solutions offered by critics of sprawl and autos are at worst brutally intrusive and at best ineffectual. More efficient pricing of roads can be achieved with the installation of tolling solutions that are now technologically feasible. Optimizing tolls over specific roads, bridges, blocks, intersections, and interchanges will require more sophisticated systems, but for now, let’s at least get road-use prices going in the right direction!

When Federal Reserve Chairman Jerome Powell said “higher for longer” last year, it wasn’t about the Grateful Dead concerts he’s attended over the years. No, he meant the Fed might need to raise its short-term interest rate target and/or keep it elevated for an extended period to squeeze inflation out of the economy. As late as December, Powell said that additional rate hikes remain on the table. But short of that, the Fed might keep its current target rate steady until inflation is solidly in-line with its 2% objective. The obvious risk is that tight monetary policy might tip the economy into recession. The market, for its part, is pricing in several rate cuts this year.

Thus far, the release of key economic data for December 2023 has not settled the debate as to whether disinflation has truly paused short of the Fed’s goal. There were inauspicious signs from the labor market in December as well. These data releases don’t rule out a “soft landing”, but they indicate that recession risks are still with us in 2024. The Fed will face a dilemma if the economy weakens but inflation fails to abate, either due to residual stickiness or new supply shocks. The latter are unfolding even now with the shut down of Red Sea shipping.

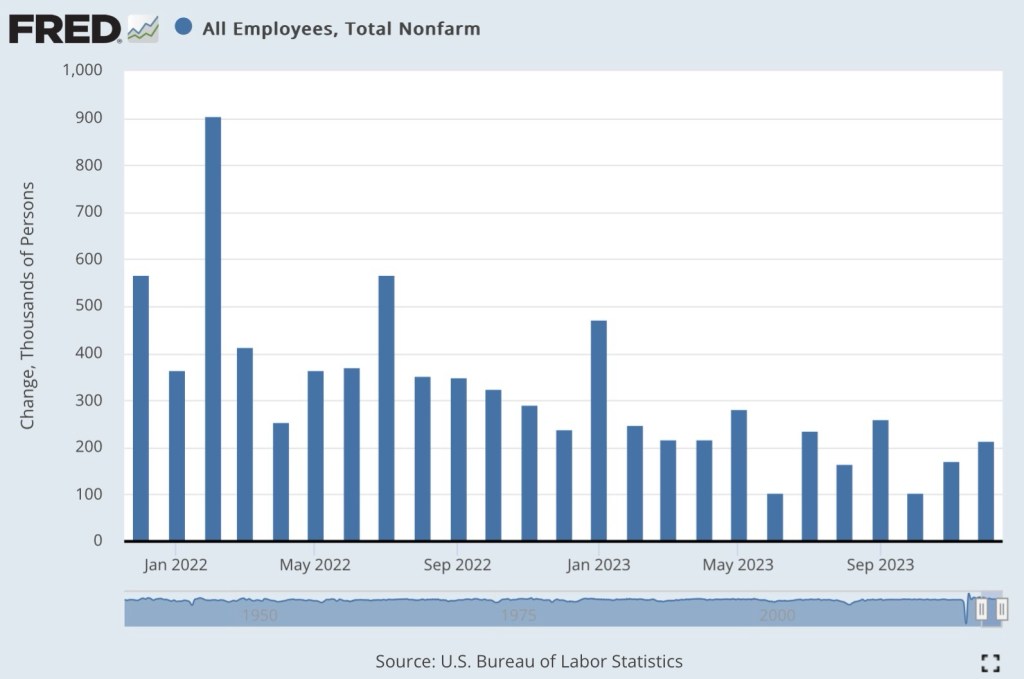

Bad Employment Report

On the surface, the employment report from the Bureau of Labor Statistics (BLS) was strong relative to expectations, and the media reported it on that superficial level: nonfarm payrolls increased by 216,000 jobs, about 45,000 more than expected; unemployment was unchanged from November at 3.7%.

Unfortunately, the report contained several ominous signs:

1) Employment from the BLS Household Survey declined by 683,000 in December and is essentially flat since July. This discrepancy should be rather unsettling to anyone waving off the possibility of a recession.

2) The number of full-time workers decreased by 1.53 million in December, and the number of part-time workers increased by 762,000 as the holidays approached. Retail employment was not particularly strong however, and the big loss of full-time work stands in contrast to the “strong-report” narrative.

3) The number of multiple jobholders hit a record and increased by 556,000 over the past year. This might indicate trouble for some workers making ends meet.

5) The civilian labor force declined by 676,000. What accounts for the change in status among these former workers or job seekers?

6) From the BLS Establishment Survey, government hiring accounted for 24% of the nonfarm jobs filled in December. Social Services accounted for 10% of the new hiring and health care for 18%, both of which are heavily dependent on government.

7) Nonfarm payrolls were revised downward by a total of 71,000 for October and November. We’ve seen downward revisions for 10 of the past 11 months.

8) In total, initial monthly job reports in 2023 overstated the full-year gain in nonfarm employment after available revisions by 439,000.

Those are big qualifiers on the “stronger than expected” jobs report. Furthermore, I tend to discount new government jobs as a real engine of production possibilities, so the report didn’t offer much assurance about the economy’s momentum. In addition, there are estimates that the payroll gain was due to better weather than the seasonal adjustment factors indicate.

Fictional Payroll Gains?

Still other issues cast doubt on the BLS payroll numbers. First, they are based on a survey of employers that is not complete by the time of each month’s initial report. Second, the survey is heavily skewed toward employees of government and large corporations; the sample of small employers is light by comparison. Third, seasonal adjustments often swamp the unadjusted changes in payrolls.

Finally, the BLS uses a statistical model of business births/deaths to adjust the figures. This is intended to correct for a lag in survey coverage as new businesses are formed and others close. The net effect on the payroll estimate can be positive or negative. Unfortunately, it’s difficult for even the BLS to tell how much the birth/death model affects the headline nonfarm jobs figure in any particular month. Therefore, it’s tough to put much faith in the monthly reports, but we watch them anyway.

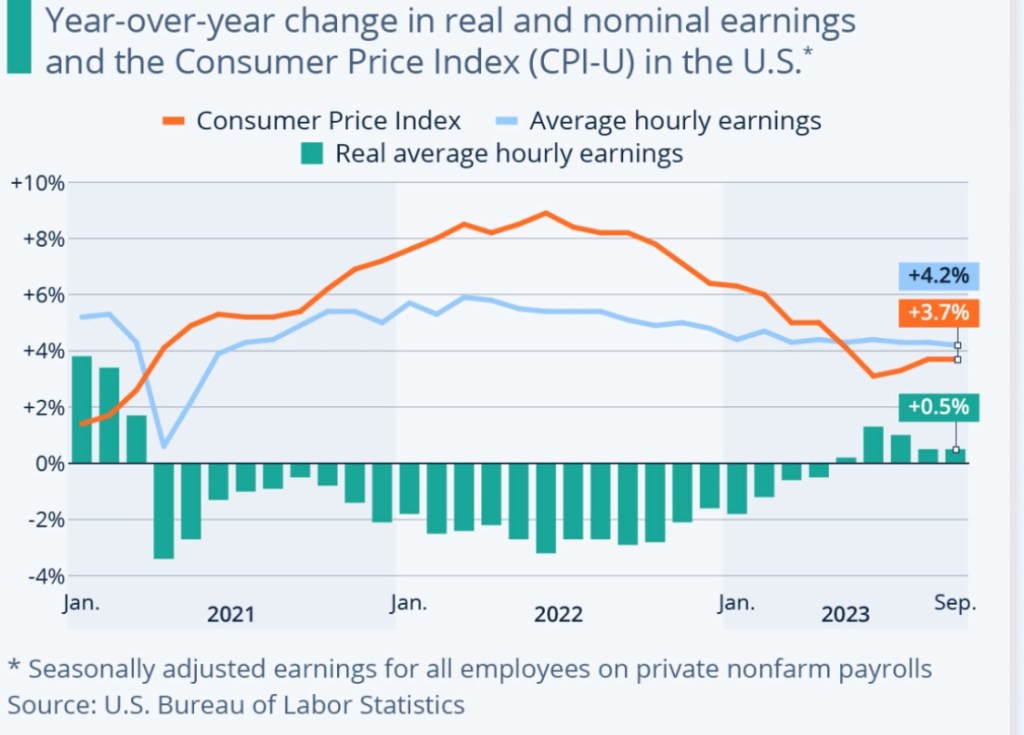

Stubborn Inflation

The Consumer Price Index (CPI) for December increased 0.3% over November and 3.4% year-over-year, slightly more than expectations of 0.2% and 3.2%, respectively. The “core” CPI (excluding food and energy prices) rose 3.9% year-over-year, more than the 3.8% expected. The core rate declined on a one-month and year-over-year basis, however, as did the median item in the CPI.

All CPI measures in the chart declined during 2023, though the core and median lagged the headline CPI (green line), which “flattened” somewhat during the last half of the year. So there appears to be some stickiness hindering disinflation in the CPI at this point, but the apparent “stickiness” has been confined to lagging declines in housing costs (also see here).

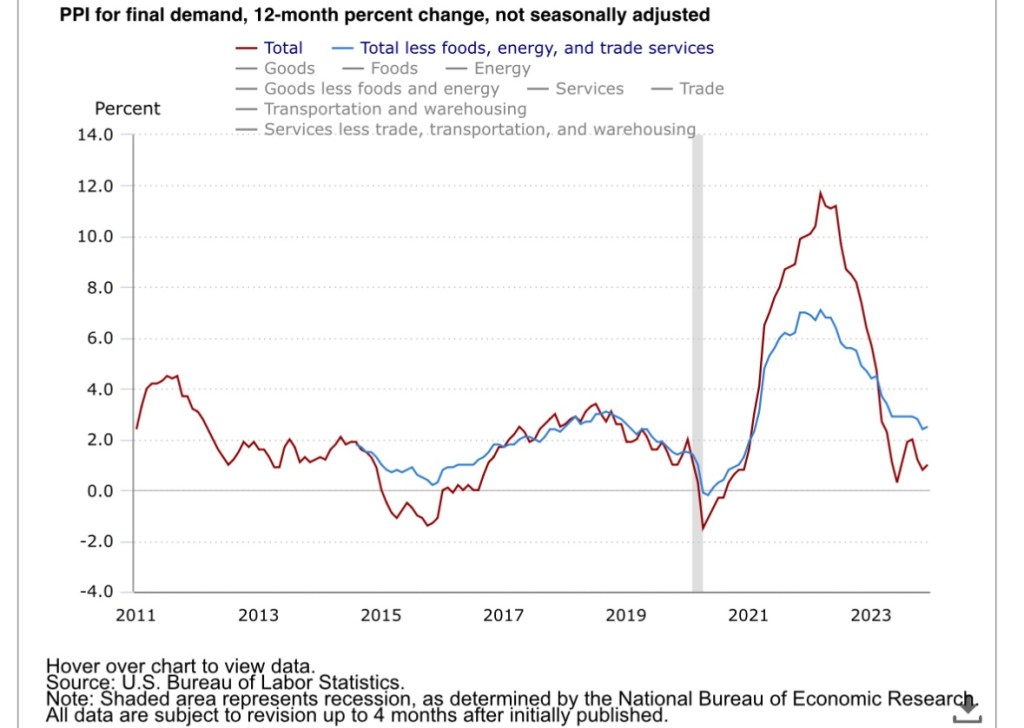

The Producer Price Index (PPI) reported a day later was thought to be benign. Like the CPI, disinflation in the core PPI has tapered:

In this context, it should be noted that declines in the Fed’s preferred inflation gauge, the PCE deflator, have also undergone something of a pause, and the PCE weights housing costs much less heavily than the CPI.

The CPI and PPI reports don’t offer any reason for the Fed to reduce its target federal funds rate over the next couple of Federal Open Market Committee (FOMC) meetings. There are two more sets of monthly inflation reports before the meeting in late March, so things could change. But again, the Fed has given ample guidance that it might have to leave its target rate at the current level for an extended period.

The Market View

Markets had priced-in six cuts in the Fed funds rate target in 2024 prior to the CPI report, but traders began to discount that possibility in its immediate aftermath. However, members of the FOMC expected an average of three cuts in 2024, with more to come in 2025, whether or not that’s consistent with “higher for longer”. Inflation is hovering somewhat above the Fed’s goal, but getting the rest of the job done might be tough, and indeed, might imply “longer” if not “higher”.

But why did the market ever hold the expectation of six cuts this year? Traders must have anticipated an economic contraction, which would kick the Fed into rapid response mode. The employment report offered no assurance that such a “hard landing” will be avoided. A few more negative signals on the real economy without further progress on prices would provide quite a test of the Fed’s inflation-fighting resolve.

Leftism has taken on new dimensions amid its preoccupation with identity politics, victimhood, and “wokeness”. Traditional socialists are still among us, of course, but “wokeists” and “identitarians” have been on the progressive vanguard of late, rooting for the deranged human butchers of Hamas and the dismantling of liberal institutions. This didn’t happen overnight, of course, and traditional socialists are mostly fine with it.

An older story is the rebranding of leftism that took place in the U.S. during the first half of the 20th century, when the word “liberal” was co-opted by leftists. Before that, a liberal orientationwas understood to be antithetical to the collectivist mindset long associated with the Left. Note also that liberalism retains its original meaning even today in much of Europe. Often we hear the term “classical liberal” to denote the “original” meaning of liberalism, but the modifier should be wholly unnecessary.

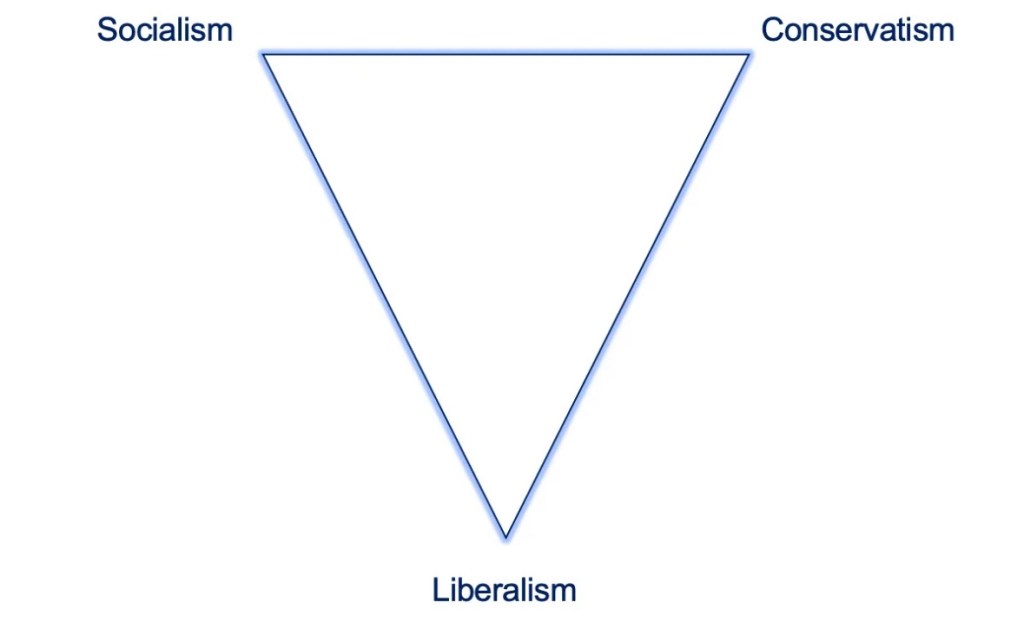

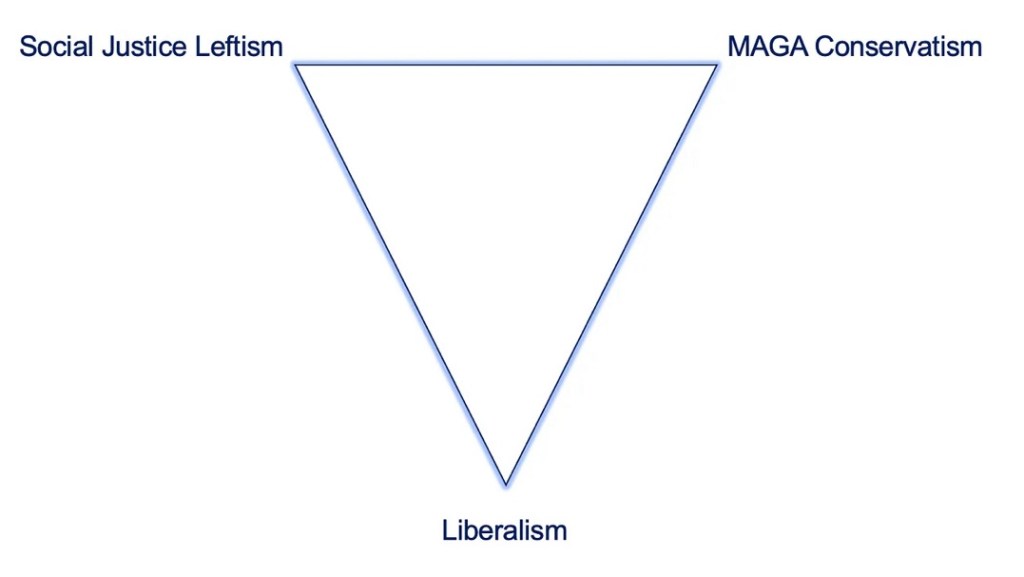

Liberalism Is Not “In-Betweenism”

In this vein, Nate Silver presents a basic taxonomy of political orientationin a recentSubstack post. It includes the diagram above, which distinguishes between socialism, conservatism, and liberalism. Silver draws on a classic essay written by Friedrich Hayek in 1945, “Why I am Not a Conservative”, in which Hayek discussed the meaning of the word “liberal” (and see here). Liberalism’s true emphasis is a tolerance for individual rights and freedoms, subject to varying articulations of the “nonaggression principle”. That is, “do as you like, but do no harm to others”.

We often see a linear representation distinguishing between so-called progressives on the left and conservatives on the right. Of course, a major hallmark of leftist thinking is extreme interventionism. Leftists or progressives are always keen to detect the slightest whiff of an externality or the slightest departure from the perfectly competitive market ideal. They seem eager to find a role for government in virtually every area of life. While it’s not a limiting case, we can substitute socialism or statism for progressivism on the far left, as Silver does, whereby the state takes primacy in economic and social affairs.

Conservatism, on the other hand, is a deep resistance to change, whether institutional, social, and sometimes economic. Conservatives too often demonstrate a willingness to use the coercive power of the state to prevent change. Hayek noted the willingness of both socialists and conservatives to invoke state power for their own ends.

Similarly, religious conservatives often demand state support beyond that afforded by the freedom to worship in the faith of one’s choice. They might strongly reject certain freedoms held to be fundamental by liberals. Meanwhile, socialists often view mere religious freedom as a threat to the power of the state, or at least they act like it (e.g. see here for an example).

Like conservatives, dedicated statists would doubtless resist change if it meant a loss of their own power. That is, they’d wish to preserve socialist institutions. On this point, witness the vitriol from the Left over what it perceives as threats to the public school monopoly. Witness also the fierce resistance among public employees to reducing the scale of the administrative state, and how advocates of entitlements fiercely resist decreases in the growth rate of those expenditures.

Silver, like Hayek, objects to the traditional, linear framework in which liberals are thought to occupy a range along a line between socialism and conservatism. He objects to that because real liberals value individual liberty as a natural human right, a viewpoint typically abhored by both socialists and conservatives. There is nothing “in between” about it! And of course, conservatives and progressives are equally guilty in their mistaken use of the word “liberal”.

Mapping Political Preferences

Liberty, statism, and conservatism are not exactly orthogonal political dimensions. Larger government almost always means less economic liberty. At a minimum, state dominance implies a social burden associated with public monopoly and monopsony power, as well as tax and welfare-state incentive problems. These features compromise or corrupt the exercise of basic rights. On the other hand, capitalism and its concomitant reliance on consumer sovereignty, individual initiative, free exchange and secure property rights is most in harmony with true liberalism.

For conservatives, resistance to change in support of a traditionally free market economy might offer something of a contradiction. In one sense, it corresponds to upholding market institutions. However, free markets allow new competitors and new technologies to undermine incumbents, who conservatives sometimes wish to defend through regulatory or protectionist measures. And conservatives are almost always too happy to join in the chorus of “price gouging” in response to the healthy operation of the free market in bringing forth supplies.

All that is to say that preferences involving liberty, statism, and traditionalism are not independent of one another. They cannot simply be mapped onto a three-dimensional space. At least the triangular representation gets liberalism out of the middle, but it’s difficult to visualize other ideological positions there. For example, “state religionism” could lie anywhere along the horizontal line at the top or even below it if certain basic liberties are preserved. Facism combines elements of socialism and a deformed version of capitalism that is properly called corporatism, but where would it fall within the triangle?

Big Government Liberalism?

Silver says he leans heavily toward a “big government” version of liberalism, but big government is hard to square with broad liberties. Granted, any well-functioning society must possess a certain level of “state capacity” to defend against private or public violations of individual rights, adjudicate disputes, and provide true public goods. It’s not clear whether Silver’s preferences lie within the bounds of those ambitions. Still, he deserves credit for his recognition that liberalism is wholly different from the progressive, socialist vision. It is the opposite.

The “New” Triangle

Silver attempts to gives the triangular framework a more contemporary spin by replacing conservatism with “MAGA Conservatism” and socialism with “Social Justice Leftism” (SJL), or “wokeism”. Here, I’m treating MAGA as a “brand”. Nothing below is intended to imply that America should not be a great nation.

The MAGA variant of conservatism emphasizes nationalism, though traditional conservatives have never been short on love of nation. For that matter, as a liberal American, it’s easier to forgive nationalist sentiments than it is the “Death to America” refrain we now hear from some SJLs.

The MAGA brand is also centered around a single individual, Donald Trump, whose rhetoric strikes many as nativistic. And Trump is a populistwhosepolicy proposals are often nakedly political and counterproductive.

SJL shares with socialism an emphasis on various forms of redistribution and social engineering, but with a new focus on victimhood based on classes of identity. Of SJL, Silver says:

“Proponents of SJL usually dislike variations on the term ‘woke’, but the problem is that they dislike almost every other term as well. And we need some term for this ideology, because it encompasses quite a few distinctive features that differentiate it both from liberalism and from traditional, socialist-inflected leftism. In particular, SJL is much less concerned with the material condition of the working class, or with class in general. Instead, it is concerned with identity — especially identity categories involving race, gender and sexuality, but sometimes also many others as part of a sort of intersectional kaleidoscope.”

The gulf between liberals and SJLs couldn’t be wider on issues like free speech and “equity”, and equality of opportunity. MAGAns, on the other hand, have some views on individual rights and responsibility that are largely consistent with liberals, but reflexive populism often leads them to advocate policies protecting rents, corporate welfare, and protectionism.

Divided Liberalism

Liberalism emphasizes limited government, individual autonomy, and free exchange. However, there are issues upon which true liberals are of divided opinion. For example, one such area of controversy is the conflict between a woman’s right to choose and the fetal right to life. Many true liberals disagree over whether the rights of a fetus outweigh its mother’s right to choose, but most would concede that the balance shifts to the fetus at some point well short of birth (putting aside potential dangers to the mother’s life). Open borders is another area that can divide true liberals. On one side, the right to unrestricted mobility is thought to supersede any public interest in enforcing borders and limiting the flow of immigrants. On the other side, questions of national sovereignty, national security, as well as social and state capacity to absorb immigrants take primacy.

Don’t Call Lefties “Liberal”… They’re Not!

True liberalism (including most strains of libertarianism) recognizes various roles that a well-functioning state should play, but it also recognizes the primacy of the individual and individual rights as a social underpinning. As Hayek noted, true liberals are not resistant to change per se, unlike conservatives. But modern progressives demand changes of the worst kind: that the state should intervene to pursue their favored objectives, laying claim to an ever-greater share of private resources. This requires government coercion on a massive scale, the antithesis of liberalism. It’s time to recognize that “progressives” aren’t liberals in any sense of the word. For that matter, they don’t even stand for progress.

I’ll close with a quote from Adam Smith that I cribbed from Scott Sumner. Unfortunately, Sumner does not give the full reference, but I’ll take his word that Smith wrote this 20 years before the publication of The Wealth of Nations:

“Little else is requisite to carry a state to the highest degree of opulence from the lowest barbarism, but peace, easy taxes, and a tolerable administration of justice; all the rest being brought about by the natural course of things. All governments which thwart this natural course, which force things into another channel, or which endeavour to arrest the progress of society at a particular point, are unnatural, and to support themselves are obliged to be oppressive and tyrannical.”

The joke’s on me, but my “out” on the question above is “long and variable lags” in the impact of monetary policy, a description that goes back to the work of Milton Friedman. If you call me out on my earlier forebodings of a hard landing or recession, I’ll plead that I repeatedly quoted Friedman on this point as a caveat! That is, the economic impact of a monetary tightening will be lagged by anywhere from 9 to 24 months. So maybe we’re just not there yet.

Of course, maybe I’m wrong and we won’t have to get “there”: the rate of inflation has indeed tapered over the past year. A soft landing now seems like a more realistic possibility. Still, there’s a ways to go, and as Scott Sumner says, when it comes to squeezing inflation out of the system, “It’s the final percentage point that’s the toughest.” One might say the Federal Reserve is hedging its bets, avoiding further increases in its target federal funds rate absent evidence of resurging price pressures.

Strong Growth or Mirage?

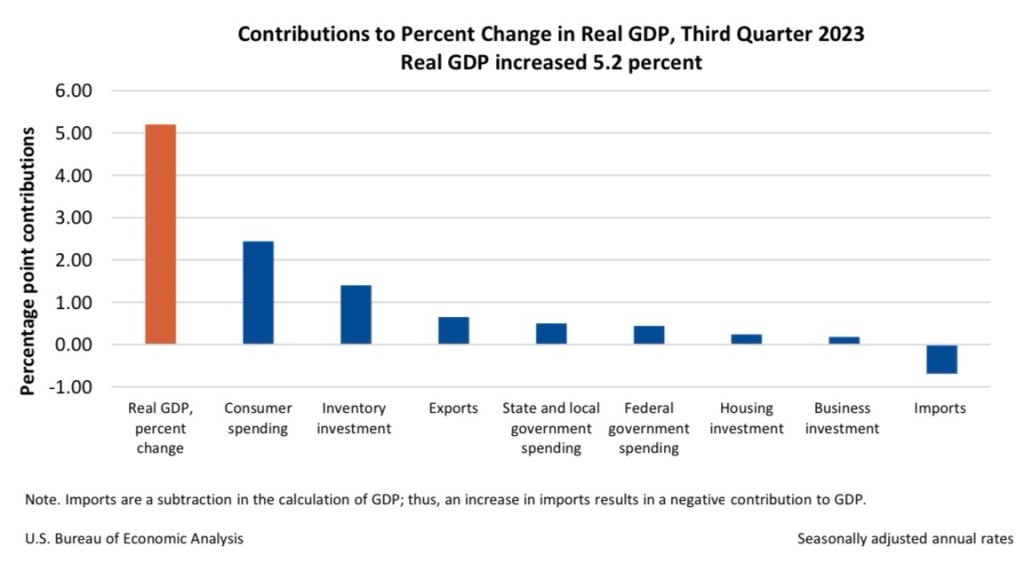

Economic growth is still strong. Real GDP in the third quarter grew at an astonishing 5.2% annual rate. A bulge in inventories accounted for about a quarter of the gain, which might lead to some retrenchment in production plans. Government spending also accounted for roughly a quarter, which corresponds to a literal liability as much as a dubious gain in real output. Unfortunately, fiscal policy is working at cross purposes to the current thrust of monetary policy. Profligate spending and burgeoning budget deficits might artificially prop up the economy for a time, but it adds to risks going forward, not to mention uncertainty surrounding the strength and timing in the effects of tight money.

Consumers accounted for almost half of the third quarter growth despite a slim 0.1% increase in real personal disposable income. That reinforces the argument that consumers are depleting their pandemic savings and becoming more deeply indebted heading into the holidays.

The economy continues to produce jobs at a respectable pace. The November employment report was slightly better than expected, but it was buttressed by the return of striking workers, and retail and manufacturing jobs declined. Still, the unemployment rate fell slightly, so the labor market has remained stronger than expected by most economists.

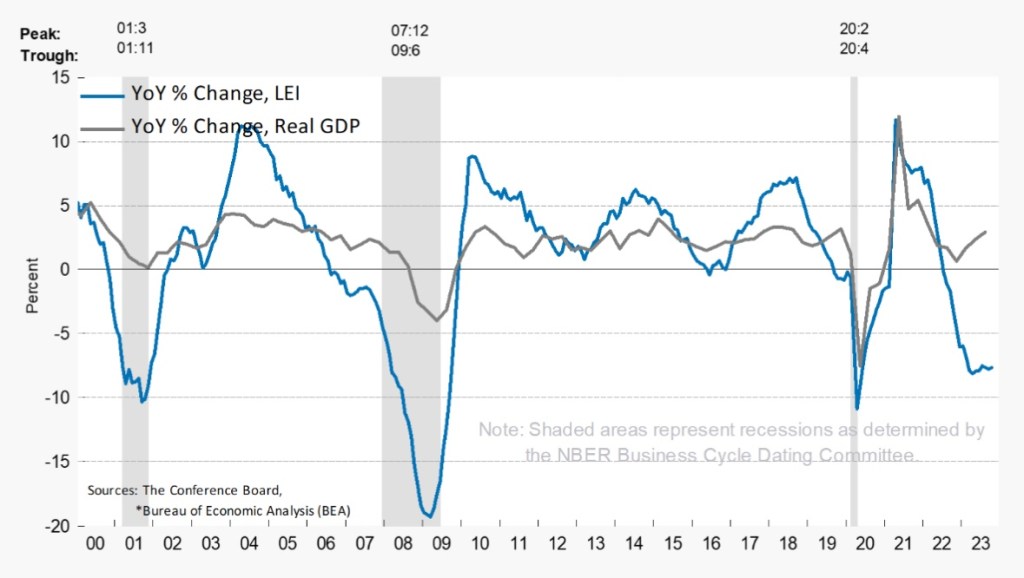

Consumer sentiment had been in the dumps until the University of Michigan report for December, which erased four months of declines. The expectations index is one component of the leading economic indicators, which has been at levels strongly suggesting a recession ahead for well over a year now. See the chart below:

But expectations improved sharply in November, and that included a decline in inflation expectations.

Another component of the LEI is the slope of the yield curve (measured by the difference between the 10-year Treasury bond yield and the federal funds rate). This spread has been a reliable predictor of recessions historically. The 10-year bond yield has declined by over 90 basis points since mid-October, a sign that bond investors think the inflation threat is subsiding. However, that drop steepened the negative slope of the yield curve, meaning that the recession signal has strengthened.

Disinflation, But Still Inflation

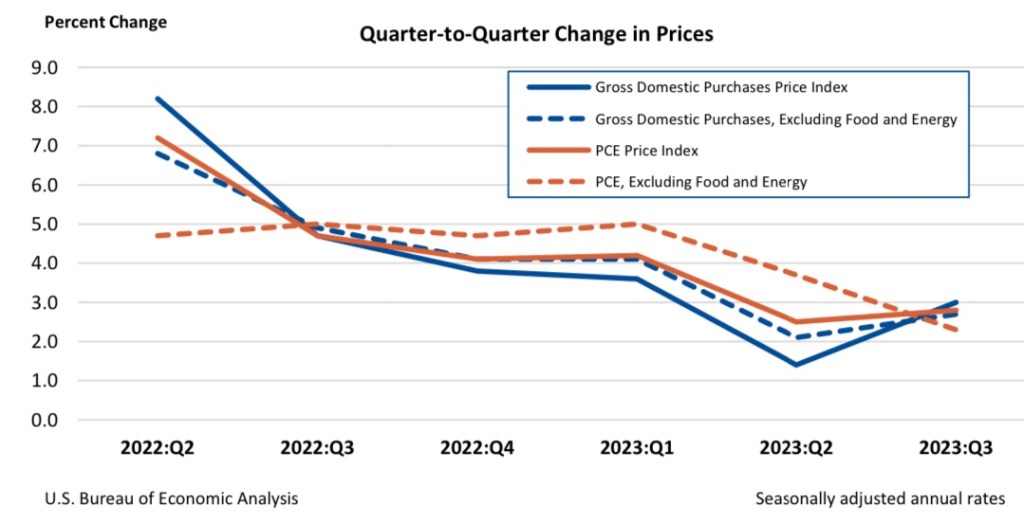

Inflation measures have been slowing, and the Fed’s “target” inflation rate of 2% appears within reach. In the Fed’s view, the most important inflation gauge is the personal consumption expenditures deflator excluding food and energy prices (the “core” PCE). The next chart shows the extent to which it has tapered over the past two quarters. While it’s encouraging that inflation has edged closer to the Fed’s target, it does not mean the inflation fight is over. Still, the decision taken at the December meeting of the Fed’s Open Market Committee (FOMC) to leave its interest rate target unchanged is probably wise.

Real wages declined during most of the past three years with the surge in price inflation (see next chart). Some small gains occurred over the past few months, but the earlier declines reinforce the view that consumers need to tighten their belts to maintain savings or avoid excessive debt.

Has Policy Really Been “Tight“?

The prospect of a hard landing presupposes that policy is “tight” and has been tight for some months, but there is disagreement over whether that is, in fact, the case. Scott Sumner, at the link above in the second paragraph, is skeptical that policy is “tight” even now. That’s despite the fact that the Fed hiked its federal funds rate target 11 times between March 2022 and July 2023 (by a total of 5.25%). The Fed waited too long to get started on its upward rate moves, which helps explain the continuing strength of the economy right now.

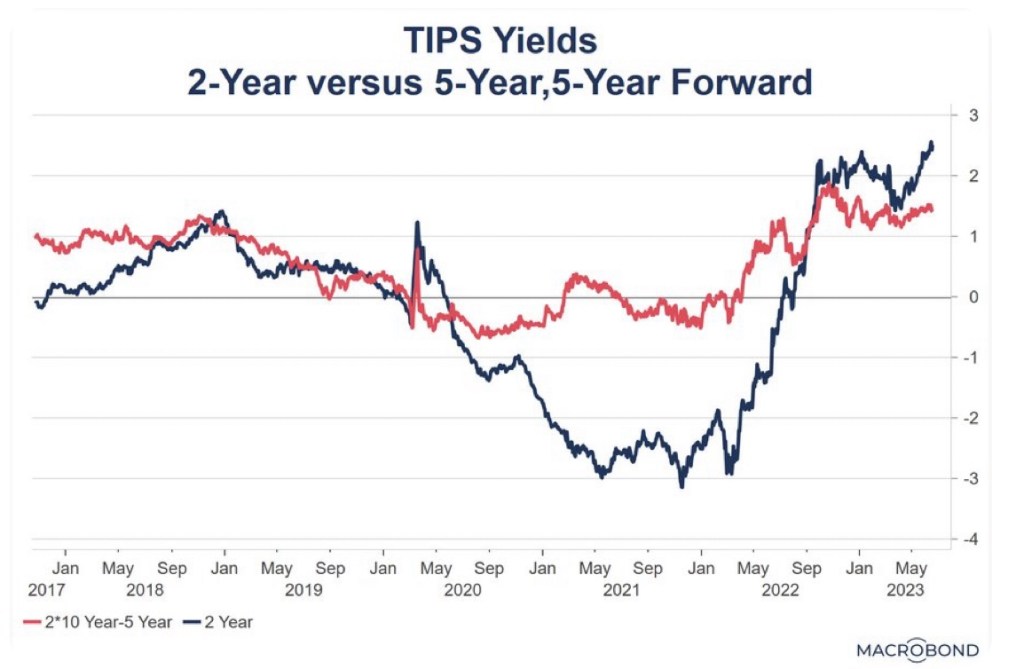

The real fed funds rate turned positive (arguably) as early as last winter as the rate rose and as expected inflation began to decline. There is also solid evidence that real interest rates on the short-end of the maturity spectrum are higher than “neutral” real rates and have been for well over a year (see chart below). If the Fed leaves its rate target unchanged over the next few months, assuming expected inflation continues to taper, the real rate will rise passively and the Fed’s policy stance will have tightened further.

Another view is that the Fed’s policy became “tight” when the monetary aggregates began to decrease (April 2022 for M2). A few months later the Fed began so-called “quantitative tightening” (QT—selling securities to reduce its balance sheet). Thus far, QT has reversed only a portion of the vast liquidity provided by the Fed during the pandemic. However, markets do grow accustomed to generous ongoing flows of liquidity. Cutting them off creates financial tensions that have real economic effects. No doubt the Fed’s commitment to QT established some credibility that a real policy shift was underway. So it’s probably fair to say that policy became “tight” as this realization took hold, which might place the date demarcating “tight” policy around 15 – 18 months ago.

Back to the Lags

Again, changes in monetary policy have a discernible impact only with a lag. The broad range of timing discussed among monetary experts (again, going back to Milton Friedman) is 9 – 24 months. We’re right in there now, which adds to the conviction among many forecasters that the onset of recession is likely during the first half of 2024. That’s my position, and while the tapering of inflation we’ve witnessed thus far is quite encouraging, it might take sustained monetary restraint before we’re at or below the Fed’s 2% target. That also increases the risk that we’ll ultimately suffer through a hard landing. In fact, there are prominent voices like hedge fund boss Bill Ackman who predict the Fed must begin to cut the funds rate soon to avoid a hard landing. Jamie Diamond, CEO of JP Morgan, says the U.S. is headed for a hard landing in 2024.

Looking Forward

If new data over the next few months is consistent with a “soft landing” (and it would take much more than a few months to be conclusive), or especially if the data more strongly indicate an incipient recession, the Fed certainly won’t raise its target rate again. The Fed is likely to begin to cut the funds rate sometime next year, and sooner if a recession seems imminent. Otherwise, my guess is the Fed waits at least until well into the second quarter. The average of FOMC member forecasts at the December meeting works out to three quarter-point rate cuts by year-end 2024. When the Fed does cut its target rate, I hope it won’t at the same time abandon QT, the continuing sales of securities from its currently outsized portfolio. Reducing the Fed’s holdings of securities will restrain money growth and give the central bank more flexibility over future policy actions. QT will also put pressure on Congress and the President to reduce budget deficits.

Germany’s inter-war descent into genocidal barbarism is perhaps the most horrifying episode of modern times. Seemingly normal, “nice people” in Germany were persuaded to go along with the murderous pogroms of the anti-Semitic National Socialists, giving truth to the “banality of evil”, as the famous expression goes. Of course, there were plenty of true believers, and multitudes bowed to the Nazis under fierce coercion, but many others went along just to “fit in”.

What could life have felt like in Weimar Germany in the late 1920s and early 1930s as the fascists accumulated power? Were normal people afraid? Well before Adolf Hitler’s rise to power he was known for his hatred of Jews, but German political leaders who enabled his ascent did not take his extreme prejudice as seriously as they should have, or they thought they could at least keep him and his followers in check. Surely there were people who foresaw the approaching cataclysm for what it would be.

Current expressions of anti-Semitism might give us a sense of what life was like during the decline and fall of the Weimar Republic. Just ask Jewish students at NYU and Cornell if they’ve sensed a whiff of it in the wake of Hamas’ slaughter of civilians in southern Israel on October 7th. The harassment these students have endured was motivated in part by claims that Israeli retaliation is morally inferior to the barbarities committed by Hamas, which is preposterous.

Of course, unlike late Weimar Germany, when Jews were blamed for economic (and other) problems, the Jew hatred we’re witnessing in the U.S. today has little to do with the immediate state of the economy. Conditions now are nothing like what prevailed in Germany as the Great Depression took hold, despite current inflationary stresses on real household incomes.

And yet some hold Jews in contempt for their relative economic success, a fact that is bound up with the frequency with which Jews are placed at the center of economic conspiracy theories. One would think Jews to be the ultimate “white oppressors”. But it seems that much of the current wave of anti-Semitism comes from fairly elite quarters, ensconced within major institutions where its sympathizers are insulated from day-to-day economic pressures.

And that brings us to a frightening aspect of the current malaise: how heavily institutionalized the hatred for certain groups or “classes” has already become. This owes to the blame directed toward whites, men, Jews, and Asians presumed to have been endowed with an inside track on success at the expense of others. Success of any kind, in the narrative of “critical” social justice, is “oppressive”, as if success is a zero-sum game.

“The ‘social justice’ political analysis is founded on the Marxist conviction that society is divided into two classes: oppressors and victims. The corresponding ‘social justice’ ethic is that victims must be raised up and celebrated and that oppressors must be suppressed and eliminated.”

This thinking has been integrated into the policies, practices and rhetoric taught in schools at all levels, corporations andnonprofits, social and traditional media, and government (including intelligence agencies and the military). This level of integration gives diversity, equity, and inclusivity (DEI) policies coercive force on behalf of so-called “protected groups”, in the parlance of anti-discrimination law. When those practices are enforced by government in various ways, the private gains extracted from “unprotected” groups amount to fascism.

Bari Weiss wrote an article in Tablet last week entitled “End DEI” in which she describes her bemused reaction as a student in the early 2000s to nascent DEI rhetoric. (Also see her recent speech to the Federalist Society here.) It’s more obvious today, but even then she recognized the hate inherent in DEI doctrine. She crystallizes the dangers she saw in DEI ideology:

“What I saw was a worldview that replaced basic ideas of good and evil with a new rubric: the powerless (good) and the powerful (bad). It replaced lots of things. Colorblindness with race-obsession. Ideas with identity. Debate with denunciation. Persuasion with public shaming. The rule of law with the fury of the mob.

“People were to be given authority in this new order not in recognition of their gifts, hard work, accomplishments, or contributions to society, but in inverse proportion to the disadvantages their group had suffered, as defined by radical ideologues. According to them, as Jamie Kirchick concisely put it in these pages: ‘Muslim > gay, Black > female, and everybody > the Jews.’”

Weiss says Jewish leaders told her, at that time, not to be hysterical, that these perverse ideas would ultimately pass like any fad. That sounds so eerily familiar. Instead, we’ve witnessed a widespread ideological takeover.

“If underrepresentation is the inevitable outcome of systemic bias, then overrepresentation—and Jews are 2% of the American population—suggests not talent or hard work, but unearned privilege. This conspiratorial conclusion is not that far removed from the hateful portrait of a small group of Jews divvying up the ill-gotten spoils of an exploited world.

“It isn’t only Jews who suffer from the suggestion that merit and excellence are dirty words. It is strivers of every race, ethnicity, and class. That is why Asian American success, for example, is suspicious. The percentages are off. The scores are too high. From whom did you steal all that success?”

The whole DEI enterprise is corrupt and unethical. It denies the meritorious in favor of those having certain superficial characteristics like the “right” skin color. That is evil and economically demented besides. It also breeds hatred that often flows both ways between classes of people, creating an incendiary environment. That we’re talking about systemic, legalized discrimination against any group is disturbing enough, but when small minorities are “othered” in this way, the potential for violent action against them is magnified. But this is just where the DEI mindset leads its proponents and beneficiaries.

Our slide into this monstrous “social justice” regime mirrors the insanity and anger that was fomented against certain “out groups” when the Nazi’s accumulated power in the latter years of the Weimar Republic. Too many today have succumbed to this zero-sum psychology, young and old alike. Fortunately, they are beginning to face some fierce resistance, but those who extol the supposed righteousness of the class struggle via DEI won’t easily give up. Our institutions are infested with their kind.

As long as influential people preach the virtues of DEI and social justice, the danger of a headlong plunge into genocidal madness is possible. And the sad truth is that normal human beings are subject to social manipulation of the most evil kind.David Foster at Ricochet: quotes an address given by C.S. Lewis in which he emphasizes this point. His words are haunting:

“Of all the passions, the passion for the Inner Ring is most skillful in making a man who is not yet a very bad man do very bad things.”

Elsewhere in Lewis’ address, he says:

“And the prophecy I make is this. To nine out of ten of you the choice which could lead to scoundrelism will come, when it does come, in no very dramatic colours. Obviously bad men, obviously threatening or bribing, will almost certainly not appear. Over a drink, or a cup of coffee, disguised as triviality and sandwiched between two jokes, from the lips of a man, or woman, whom you have recently been getting to know rather better and whom you hope to know better still—just at the moment when you are most anxious not to appear crude, or naïf or a prig—the hint will come. It will be the hint of something which the public, the ignorant, romantic public, would never understand: something which even the outsiders in your own profession are apt to make a fuss about: but something, says your new friend, which ‘we’ — and at the word ‘we’ you try not to blush for mere pleasure—something ‘we’ always do.

“And you will be drawn in, if you are drawn in, not by desire for gain or ease, but simply because at that moment, when the cup was so near your lips, you cannot bear to be thrust back again into the cold outer world. It would be so terrible to see the other man’s face—that genial, confidential, delightfully sophisticated face—turn suddenly cold and contemptuous, to know that you had been tried for the Inner Ring and rejected. And then, if you are drawn in, next week it will be something a little further from the rules, and next year something further still, but all in the jolliest, friendliest spirit. It may end in a crash, a scandal, and penal servitude; it may end in millions, a peerage and giving the prizes at your old school. But you will be a scoundrel.”

I’ve taken an extended hiatus from blogging while moving to a different part of the country. I haven’t posted here in over 10 weeks, but a new post appears below. I’m still tying-up loose ends from the move, but I’ll be trying to get back to posting more regularly … trying!

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Absurd ideas about race and identity politics come from extreme elements on both the Left and the Right. Some leftists insist that race has no natural basis — that it’s simply a “social construct”. On the Right, a “racialist” contingent is promoting the “celebration of whiteness” and embracing racial preferences for whites. Treated as alternative pathways, I’d take “social construct”. It’s nonsense, of course, but the beautiful irony is that it provides a basis for stripping away from our institutions the entire diversity, equity, and inclusion (DEI) straightjacket. It’s almost as if those promoting race as a social construct wish to build a “colorblind” society. On the other hand, I suppose some think they can have their DEI cake along with a side of free choice to identify as anything they want: black, white, or furry.

Who Are the Racists?

People of good faith don’t harbor or act on racist tendencies. The mere recognition of racial/ethnic/cultural differences is not evidence of racism and does not preclude the treatment of all with fairness and due respect. It’s possible to respect, value, or fall in love with someone outside one’s own racial, ethnic, or cultural group of origin, even while holding a general affinity for one’s own group, as nearly everyone does.

But a few real racists are sprinkled across all races, ethnicities, cultures, and the full political spectrum. The “popular” racist stereotype as white male has been kept alive by the lingering echos of slavery in America, which ended nearly 16 decades ago, and the long hangover that included Jim Crow laws and segregation. Today, however, “white society” or “whiteness” is hardly the sole domain of prejudice.

IsRacialism Different?

Now, a few whites are promoting the celebration of “white identity” as a counterbalance to identity politics among non-whites. Ostensibly, this “white racialism” might be similar to celebrations of identity often practiced by minorities, which are also forms of racialism. Should white racialism be viewed as less savory than racialism practiced by racial minorities?

For most Caucasians, “being white” does not have much salience relative to other affiliations defining identity. That’s why white racialism seems odd to me. Sure, when forced to check a box, whites will check “Caucasian”, but “white identity” seems overly broad. There are too many distinct cultures and subcultures that dominate self-identity, such as national ancestry, religion, and cultural membership.

The same could be said for many other racial categories, but minority status and historical events (e.g., American slavery) help explain why broad categories often form cohesive identity groups. And, as Christopher Rufo notes in his great discussion of the racialist viewpoint, broad categories tend to be the most closely associated with racialism:

“Yes, left-wing racialism is indeed now deeply embedded in America’s institutions, and the demographic balance of the country has shifted in recent decades. And yes, the basic racial classification system in the United States broadly delineates continental origin—Europe, Africa, Latin America, Asia—in a way that is not arbitrary or meaningless. Terms such as ‘white,’ ‘black,’ ‘Latino,’ and ‘Asian,’ while often obscuring important variations within such groupings, have become the lingua franca and are useful shorthand descriptors for many purposes.”

There are individuals from all groups or “classes”, including whites, who react critically to aggressive expressions of identity by members of other classes. Perhaps that’s excusable, depending on the degree of zealotry on either part. The line between pride in race/ancestry/culture and fractious racialism might be hard to discern in some cases, but the chief distinction is rooted in explicit, demeaning and/or envious comparisons to “out-groups”. This might be damaging enough, but from there it can be a very short step into outright racism.

A preoccupation with the historic disadvantages of one’s race can be disempowering to an individual and destructive in a social sense. I believe the white racialist phenomenon belongs in that category. The presumed “disadvantages” of whiteness are very contemporary, however, rooted in policies dating back only to the widespread adoption of racial preferences for non-white “protected classes” and DEI.

Preferences For All