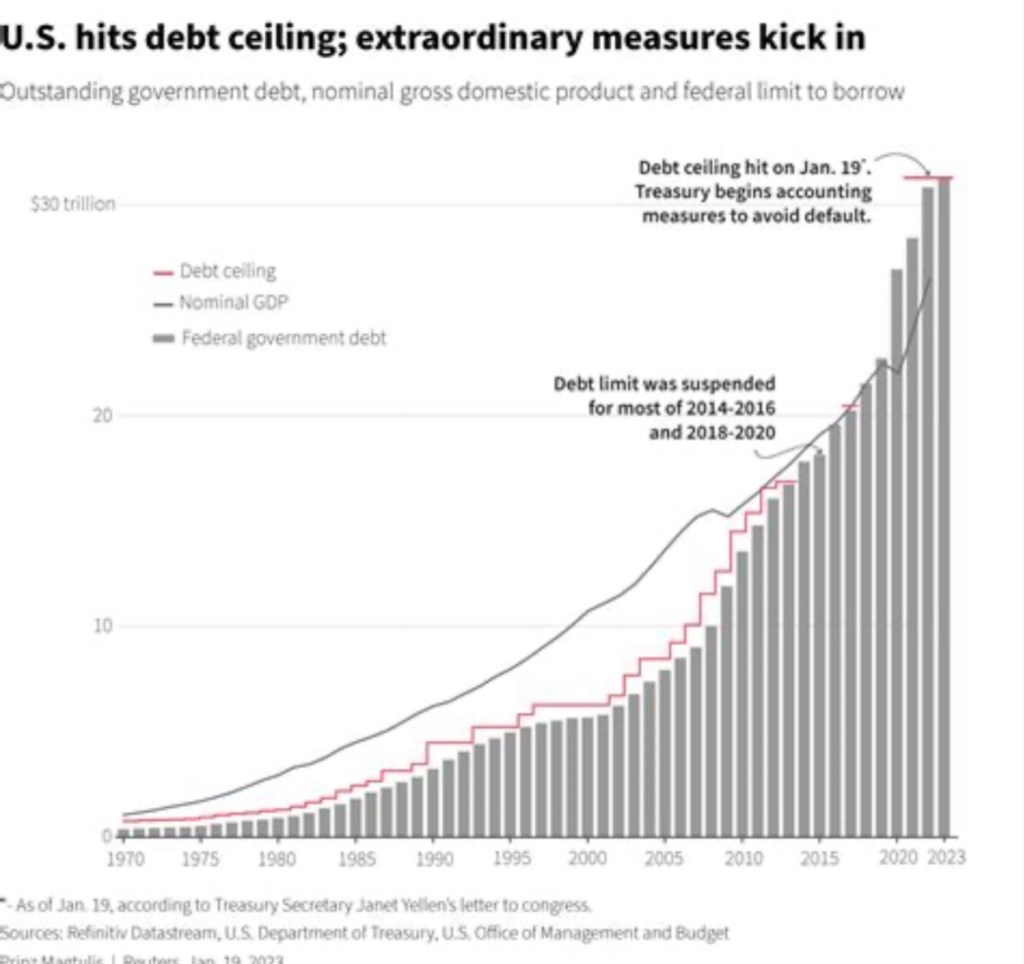

Long-awaited developments in the federal debt limit standoff shook loose in late April when Republicans passed a debt limit bill in the House of Representatives. Were it signed into law, the bill would extend the debt ceiling by about $1.5 trillion while incorporating elements of spending restraint. That approach is highly unpopular with democrats, but the zero-hour looms: Treasury Secretary Janet Yellen says the Treasury will run out of funds to pay all of the government’s obligations in early June. Soon we’ll have a better fix on President Biden’s response to the republicans, as he’s invited congressional leaders to the White House this Tuesday, May 8th to discuss the issue.

Biden wants a “clean” debt limit bill without changes impacting the budget path or existing appropriations. Senate Majority Leader Chuck Schumer would like to see a “clean” suspension of the debt limit. Republicans would like to use a debt limit extension to impose some spending restraint. They’ve focused only on the discretionary side of the budget, however, while much-needed reforms of mandatory programs like Social Security and Medicare were left aside. In fairness, both political parties have made massive contributions over the years to the burgeoning public debt, so not many are free of blame. But any time is a good time to try to enforce some fiscal discipline.

The Extraordinary Has Its Limits

Three months ago I wrote that the Treasury’s “extraordinary measures” to avoid breaching the debt limit would probably allow adequate time to break the impasse. In other words, accounting maneuvers allowed spending to continue without the sale of new debt. That bought some time, but perhaps not as much as hoped … tax filing season has revealed that revenue is coming in short of expectations, probably because weak asset markets have not generated anticipated levels of taxable capital gains income. In any case, very little progress was made over the past three months on settling the debt limit issue until the House passed the plan pushed by McCarthy. So we await the results of the pow-wow at the White House this week.

A Legislative Trick?

There’s been talk that House democrats will try to push through a “clean” debt limit bill of one sort or another by using a so-called discharge petition. They conveniently snuck this measure into an unrelated piece of legislation back in January. The upshot is that a bill meeting certain conditions must go to the floor for a vote if the discharge petition on the issue has at least 218 signatures. That means at least five republicans must join the democrats to force a vote and then join them again to pass a clean debt limit bill. That’s a long shot for democrats. Given the odds, will Biden deign to negotiate with House Speaker Kevin McCarthy? Even if he does, Biden will probably stall a while longer to extend the game of chicken. His hope would be for a few House republicans to lose their resolve for budget discipline in the face of looming default.

An Aside On Some Falsehoods

There’s a good measure of jingoistic BS surrounding the public debt. For example, you’ve probably heard from prominent voices in the debate that the U.S. has never defaulted on its debt and dad-gummit, it won’t start now!But the federal government has defaulted on its debt four times in the past! In three of those cases, the government reneged on commitments to convert bills or certificates into precious metals. The first default occurred during the Civil War, however, when the Union was unable to pay its war costs and subsequently went on a money printing binge. Unfortunately, we’re now engaged in a civil war of public versus private claims on resources, but the government can’t pay its bills without piling on debt. The statist forces now in control of the executive branch continue to insist that every American should demand more federal borrowing.

Here’s more BS in the form of linguistics that seemingly pervade all budget discussions these days: the House bill includes modest spending restraints, but mostly these are reductions in the growth of spending. Yet these are routinely described by democrats and the media as spending cuts. We could use another bill in the House demanding clear language that abides by the commonly accepted meaning of words. Fat chance!

The Trillion Dollar Coin

In my earlier debt limit post, I discussed two unconventional solutions to the Treasury’s financing dilemma. Both are conceived as short-term workarounds.

One is the minting of a $1 trillion platinum coin by the Treasury, which would deposit the coin at the Federal Reserve. The Fed would then sell back to the public (banks) existing Treasury bonds out of its massive holdings (> $8 trillion). The Treasury could then use the proceeds to pay the government’s bills. Thus, the Fed would do what the Treasury is prohibited from doing under the debt ceiling: selling debt.

When the debt ceiling is ultimately lifted, the “coin” process would be reversed (and the coin melted) without any impact on the money supply. As described, this is wholly different from earlier proposals to mint coins that would feed growth in the stock of money. Those were the brainchildren of so-called Modern Monetary Theorists and a few left-wing members of Congress.

There hasn’t been much discussion of “the coin” in recent months. In any case, the Fed would not be obligated to cooperate with the Treasury on this kind of workaround. The Fed has urged fiscal discipline, and it could simply refuse to take the coin if it felt that debt limit negotiations should be settled between Congress and the President.

Premium Bonds

The other workaround I discussed earlier is the sale by the Treasury of premium bonds or even perpetuities. This involves a little definitional trickery, as the debt limit is expressed in terms of the par value of debt. An example of premium bonds is given at the link above. High interest, low par bonds could be issued by the Treasury with the proceeds used to pay off older discounted bonds and pay the government’s bills. Perpetuities are an extreme case of premium bonds because they have zero par value and would not count against the debt limit at all. They simply pay interest forever with no return of principle. Paradoxically, perpetuities might also be less controversial because they would not involve payments to retire older debt.

Constitutional Challenge

The Biden Administration has pondered another way out of the jam, one that is perhaps more radical than either premium bonds or minting a big coin: challenge the debt ceiling on constitutional grounds. The idea is based on a clause in the Fourteenth Amendment stating that the: “validity of the public debt of the United States… shall not be questioned.” That’s an extremely vague provision. Presumably, as an amendment to the Constitution, this “rule” applies to the federal government itself, not to anyone dumping Treasury debt because its value is at risk. Any fair interpretation would dictate that the government should do nothing to undermine the value of outstanding public debt.

Let’s put aside the significant degree to which the real value of the public debt has been eroded historically by inflationary fiscal and monetary policy. That leaves us with the following questions:

Does a legislated debt limit (in and of itself) undermine the value of the public debt? Why would restraining the growth of debt or setting a limit on its quantity do such a thing?

Would a refusal to legislate an increase in the debt limit undermine or “question” the debt’s value? No, because belt-tightening is always a valid alternative to default. The Fourteenth Amendment is not a rationale for fiscal over-extension.

If we frame this as a question of default vs. fiscal restraint, only the former undermines the value of the debt.

From here, it looks like the blame for bringing the value of the public debt into question is squarely on the spendthrifts. Profligacy undermines the value of one’s commitments, so one can hardly blame those wishing to use the debt ceiling to promote fiscal responsibility. Any challenge to the debt ceiling based on the Fourteenth Amendment is likely to be guffawed out of court.

The Market’s Likely Rebuke

The market will probably react harshly if the debt ceiling impasse continues. That would bring higher yields on outstanding Treasury debt and a sharp worsening of the liquidity crisis for banks holding devalued Treasury debt. Naturally, Biden will attempt to blame the GOP for any bad outcome. His Treasury could attempt to buy more time by announcing the minting of a large coin or the sale of premium bonds, including perpetuities. Ultimately, neither of those moves would do much to stem the damage. The real problem is fiscal incontinence.

It’s long past time for me to revisit a few key issues surrounding gun rights, as well as a few sacred cows accepted uncritically by the press and nurtured by interventionists. Tragic gun violence and mass shootings have given rise to strong public reaction, but one undeniable result is that gun purchases have surged, bringing household gun ownership rates up sharply to levels of the 1980s and 1990s. This owes in part to the growing reality that police in many communities are under-resourced, unable to respond effectively to crimes and disorder in the wake of defunding and activist sentiment opposing police use of force. Under these circumstances, many private citizens believe they must be ready to defend themselves. And after all, even under better circumstances, counting on the ability of police to arrive and act promptly at a time of extreme need is a crap shoot.

As a preview, here’s a list of the sections/topics addressed below. You can skip what might not interest you, though earlier sections might provide more context.

What’s An “Assault Weapon”?

Deadlier Gun Modifications

Homicide Data

Crime and Gun Violence

Lone Wolf Psychopaths

Private Intervention and Reporting

Red Flag Laws

Defensive Gun Uses

Invitations To Kill

Second Amendment Protections

Modern Sporting Rifles

Not many politicians or people can define exactly what they mean by “assault weapons”, even those strongly opposed to … whatever they are. Scary looking things. Contrary to the implication promoted by the anti-gun lobby, what they call “assault rifles” today are not machine guns. Those have been heavily regulated since 1934, must be registered, and are now illegal for civilians to own if produced after May 19, 1986. In other words, what are frequently called “assault rifles” are not fully automatic weapons that fire a continuous stream of bullets. Rather, they are semiautomatic, which means they load the next bullet automatically but do not fire multiple bullets with a single pull of the trigger. You have to pull the trigger each time you fire a bullet. There are many semiautomatic handguns as well. Here’s a little history on semi-automatics:

“Semi-automatic, magazine-fed rifles were introduced to the civilian market here in the US in 1905. The US military adopted them about three decades later for use in World War II. … The civilian version of the modern sporting rifle, the AR-15, was introduced in 1956 so it has been with us for over six decades.”

So… it’s also misleading to call semiautomatics “military rifles” because they were originally produced for the civilian market. By the way, “AR” stands for ArmaLite Rifle, NOT “assault rifle”.

It’s more accurate to use the term “modern sporting rifle” for a semiautomatic today, rather than “assault rifle”. The vast bulk of the 15 million semiautomatic rifles held by the public were purchased for sport shooting, and people actually think they’re a lot of fun to shoot. Of course, they are also kept as a defensive weapons. By defensive, I include their use as a weapon against predators or invasive species on farms and ranches. If you don’t think that kind of weapon is especially useful for that purpose, remember that the task often involves firing with accuracy over a significant range. A modern sporting rifle is far superior to alternatives under those circumstances, especially when multiple shots at a moving target are likely to be necessary.

Obviously, a semiautomatic rifle is advantageous if there are multiple intruders. I was reminded of this by a recent article about feral hogs and the destruction they’re causing in the south, and especially in Texas. They breed fast and are so numerous that they are wreaking unprecedented damage to farms, ranches, and even suburban lawns and gardens. A handgun, shotgun, or a bolt action rifle won’t be nearly as effective against these beastsbecause theytravel in groups of two to 30+.

Deadly Modifications

An accessory called an “auto sears” or “auto switch”can transforma semiautomatic pistol or rifle into a fully automatic weapon, but it’s a felony to possess an unregistered auto sears. Bump stocks allow semiautomatic rifles to fire more rapidly, sort of like machine guns, but they sacrifice accuracy. Bump stocks were outlawed a few years ago under an ATF rule, but their legality is still pending in court. These modifications do have legitimate uses, but I won’t argue the soundness of these bans other than to note their consistency with prior restrictions on machine guns. However, illegal bump stocks and auto sears circulate and they are easy to produce, so it’s not clear that these laws can ever produce their hoped-for result.

There are restrictions on magazine capacity in 13 states. The biggest problem with these restrictions is that they limit the effectiveness of defensive gun use. People miss their targets in high-pressure situations… a lot. Furthermore, dangerous confrontations often involve more than one attacker to defend against. Changing a magazine in the middle of all that presents a challenge that should be unnecessary. It’s no coincidence that 15+ bullet magazines are standard issue with some of the most popular guns on the market.

Homicide Data

It’s difficult to get refined data on the use of sporting rifles in gun homicides because reported categories of weapons are too broad. Nevertheless, we know semiautomatic rifles are not commonly used in violent crimes. There were 20,138 firearm deaths in the U.S. in 2022 excluding suicides, which is obviously tragic. In 2020, handguns were used in 59% of all gun homicides, while rifles (including semiautomatics) were used in just 3%. It’s possible these percentages undercount, as there is a sizable category labeled as “Type Not Stated”.

Mass shootings, defined by the FBI as four or more people killed, accounted for 3.2% of firearm deaths, for a total of 648 including deaths of shooters themselves. Rifles were used in about 30% of the mass shootings. That’s roughly consistent with the range of estimates shown in this 2021 report from the RAND Corporation.

It’s important to note that internationally, the U.S. has not been the outlier in mass public shootings that many believe it to be. In any case, you’ll hope in vain if you think a ban on sporting rifles will put a stop to mass shootings. In addition to interfering with the rights of millions of law-abiding gun owners, the decade-long ban on so-called assault weapons ending in 2004 had no impact on mass public shootings or any other type of crime (also see this post). Of course, there are plenty of other available means of committing mass murder, and there are plenty of illegal guns on the street, so this shouldn’t be a surprise.

One more important fact to bear in mind: despite efforts to convince us otherwise, gun violence is not the leading cause of death among children. By that I mean real children, not 18 – 19 year-old gang members. Kids age 12 and under die in car crashes at double the rate of gun deaths, for example.

Crime and Gun Violence

Gun violence has many causes, and criminal activity is foremost. According to this analysis, arguments or gang-related incidents accounted for 57% of 303 mass shooting deaths over a six-month period in 2021, while also accounting for more than 75% of the injuries. Much of this mayhem is black-on-black violence, and it’s odd that few seem willing to admit it. Law-abiding inner-city households and minorities just might have the most to gain from gun ownership.

A poorly conceived and politically motivated article in Politico claimed that gun violence was heavily concentrated in southern “red states”. The author’s heavy-handed attempt to focus on state-level statistics blurred more relevant distinctions. For example, he failed to emphasize the heavy concentration of gun violence in urban areas (which are heavily “blue”) and crime-ridden neighborhoods populated by those at the lowest rungs of the socioeconomic ladder.

The predominance of criminal and gang-related shootings suggests that major solutions to gun violence can be found within the criminal justice system: stiff bail, aggressive prosecution, and long sentences for criminal actions, whether gang-related or otherwise. Lately, we’ve been veering in the other direction.

On the other hand, gangs would be far less active and deadly if black market opportunities were minimized. Those tend to be created by government when it interferes with otherwise voluntary transactions. Most conspicuous in this regard is the prosecution of the drug war. This creates risk-fueled profits for dealing and trafficking that are highly enticing to hard-luck gang members. Unfortunately, competitive pressure on the black market often takes violent forms. Legalization or even decriminalization of a wider assortment of drugs would undercut black market profitability, however. This approach would be far more effective if governments avoid imposing high taxes on newly-legalized drugs, because taxes simply recreate black-market opportunities.

Psychopathic Homicide

It’s no secret that severe mental illness can lead to acts of violence, including mass shootings. One analysis found that so-called “lone wolf” attacks accounted for 15% of mass shooting deaths and less than 5% of injuries during the first half of 2021.

We can probably all agree that anyone in the grips of a severe psychosis should not be in possession of guns. The obvious problem is that we can’t easily identify such persons without severe infringements on constitutional rights. Furthermore, we won’t always accurately identify true threats and we’ll mistakenly finger some harmless individuals. So how do we decide who’s really and legally crazy? Can we agree on some threshold of craziness and who meets it? Respect for civil liberties demands restraint in limiting individual rights without just cause. The revocation of a person’s Second Amendment rights should require a high degree of certainty that the individual is a threat.

Not all disturbed individuals seek or ever receive care, and not all disturbed individuals are dangerous, so attempting to identifying them through their utilization of mental health care is imperfect at best. Indeed, most mass shooters are thought to have had an undiagnosed disorder. Should a therapist be required to report to authorities a patient whom they’ve diagnosed as psychotic or dangerous? Would that be sufficient cause to confiscate a patient’s guns? That is not as straightforward for therapists as it might seem:

“Mandatory reporting of persons believed to be at imminent risk for committing violence or attempting suicide can pose an ethical dilemma for physicians, who might find themselves struggling to balance various conflicting interests. Legal statutes dictate general scenarios that require mandatory reporting to supersede confidentiality requirements, but physicians must use clinical judgment to determine whether and when a particular case meets the requirement. In situations in which it is not clear whether reporting is legally required, the situation should be analyzed for its benefit to the patient and to public safety. Access to firearms can complicate these situations, as firearms are a well-established risk factor for violence and suicide yet also a sensitive topic about which physicians and patients might have strong personal beliefs.”

If physicians or therapists approach these questions with the greatest deference to public safety, we’re liable to see a lot fewer people seeking therapy. I would not rule out, however, that such deference might be the best for society.

Private Intervention and Reporting

Less formal mechanisms to promote public safety require vigilance by private individuals, families, and other groups. A large number of perpetrators of mass killings were known to be deeply troubled well beforehand by family and/or acquaintances. Signs of maladjustment in loved ones are easily dismissed or forgiven, but families must take great responsibility for the potential actions of their own. Seeking therapeutic help is one thing, but when a family member shows more obvious signs of psychosis, then it might be time for contact with authorities and possibly institutionalization.

There have also been many cases in which mass killers have previewed their violent thoughts on-line. Anyone connected with such an individual on social media or witnessing deranged behavior should not hesitate to contact police to intervene. Of course, things aren’t always clear cut, but it’s important to be attentive and take responsible action when an individual’s behavior appears to take an ominous turn. This too can be abused, and authorities must be fair-minded about reviewing reports of threats to be sure they aren’t motivated by petty differences, whether personal, business, or political. This is at the heart of the right to due process of law under the Fifth and Fourteenth Amendments of the Constitution.

Red Flag Laws

Among the proposals for reducing gun violence are additional measures for controlling ownership and access to guns. Red flag laws are intended to restrict more formally and comprehensively the ability of persons at risk of harming themselves or others from owning or acquiring guns. At present, 19 states and DC have some form of red flag law(s), while one state (OK) has enacted an anti-red flag law.

Broadly, restrictions on gun possession, whether technically part of a red flag law or otherwise, can be invoked on account of age (< 21), a federal or state criminal record, a documented alcohol or drug addiction, a formally diagnosed mental illness, or a pattern of threatening or suicidal behavior. The latter may include threats arising from domestic disputes. All of these possibilities are potentially troublesome from the perspective of civil liberty, but under red flag laws, usually a court order is required to enforce the restriction. The key point is that the individual in question must have due process rights before restrictions are imposed or guns are confiscated. Otherwise, as Rep. Dan Crenshaw (TX)objects:

“What you’re essentially trying to do with the red flag law is enforce the law before the law has been broken. And it’s a really difficult thing to do, it’s difficult to assess whether somebody is a threat. Now if they are such a threat that they’re threatening somebody with a weapon already, well, then they’ve already broken the law. So why do you need this other law?”

The answer to Crenshaw’s question is that mere threats are difficult to prosecute. Likewise, it should be difficult to revoke anyone’s Second Amendment rights. Red flag laws should ensure that anyone whose gun rights are under review will receive due process. A huge difficulty is that such reviews must be speedy. If a real danger is convincingly shown to exist, then guns are confiscated and/or the individual is placed on a red flag list, at least temporarily.

Defensive Gun Use

One of the most under-reported phenomena in the gun debate is that of defensive gun uses (DGUs), which are hard to count because they often go unreported. One component of DGUs is so-called justifiable homicide by police and private citizens, which (when reported) typically contribute 700 – 800 deaths to total homicides each year. However, a DGU does not imply that a shot is fired or that a gun is pointed in the direction of a criminal threat. At a minimum, it means a threat was deterred by the presence of an armed defender.

The 2021 Georgetown National Firearms Survey reported an estimated 1.67 million DGUs per year. Of these, 25% occur inside the gun owner’s home and another 54% on their property. There is no question that DGUs save lives, and probably many thousands of lives every year. There is also no doubt that the prospect of an armed defender inside a home or business deters criminals.

Killing Zones

As one might gather from the evidence on DGUs, one of the most misguided efforts to promote safety within environments like schools and churches is their designation as “gun-free zones”. This is an invitation to anyone crazy enough to perpetrate deadly violence against large numbers of innocents, as we learned once more in the recent Nashville school shooting. Someone on staff should be trained and always armed with a gun, whether that be a resource officer, another employee, or a volunteer. Preferably several designated individuals would be armed in buildings such as large schools, or perhaps one or two trusted and designated volunteers at gatherings in houses of worship.

Second Amendment Protections

Second Amendment rights are critical to effective self-defense, which is usually a matter of protecting one’s life and property from thieves, home invaders, and predatory or destructive beasts. Anti-gun radicals find even this rationale objectionable, demonstrating no regard for gun rights whatsoever. Another claim is that the right to bear arms was given specific purpose only by the need to maintain “a well-regulated militia”, and it is further asserted that this need is out-dated.

Despite those objections, a right’s stated purpose in the text of the Constitution does not by itself define any limit on its applicability. The fact that the Second Amendment recognizes and enumerates gun rights gives emphasis to the founders’ awareness that gun-grabbers might push any advantage were that right to be left unenumerated. Furthermore, a civilian militia, whether formal or informal, might well be needed to defend against any tyrannical force as might arise in the event of a breakdown of the constitutional order.

I’m willing to stipulate that there is no immediate threat today of physical coercion by government intended to subjugate classes of individuals, or of any federal military aggression against the sovereignty of any state. That may owe in part to private gun ownership, however, which deters against open acts of tyranny. It also tends to foster a preference for more nuanced applications of government power. There’s no need for privately-owned tanks, fighter aircraft, and missiles to offer meaningful deterrence. Direct, bloody confrontations are a bad look and no way to gain broad support for other forms of coercion by government.

A better alternative for regimes or political movements who wish to radically change the social order is to offer subtle and plausibly deniable encouragement of destructive or coercive acts by proxy forces (e.g., Brownshirts, Antifa, BLM, KKK). While possession of guns by these proxies can make them more dangerous, a general public under arms is not as vulnerable as an unarmed population. Private gun owners can defend themselves more effectively and represent a significant and healthy impediment to extensions of political power of this nature.

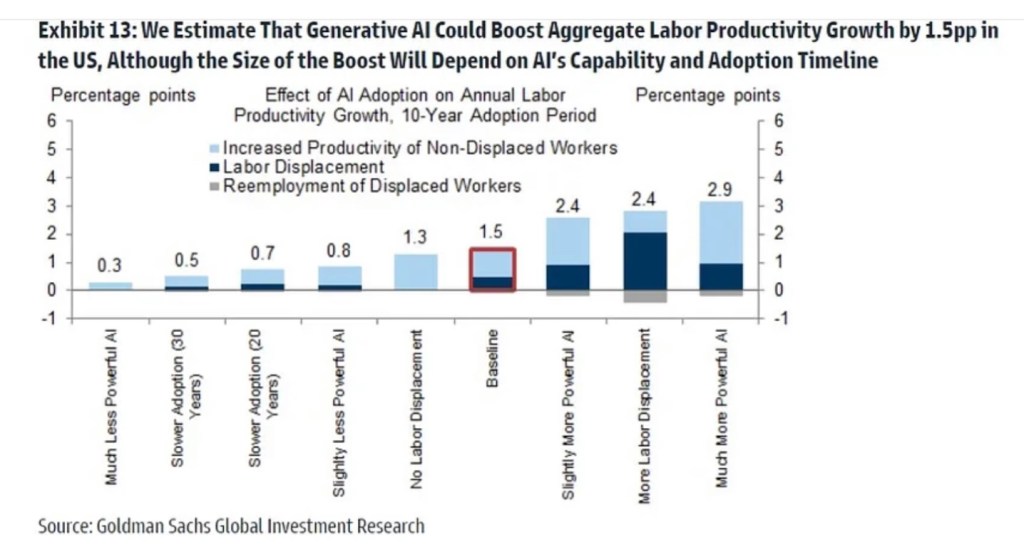

Artificial intelligence (AI) has become a very hot topic with incredible recent advances in AI performance. It’s very promising technology, and the expectations shown in thechart above illustrate what would be a profound economic impact. Like many new technologies, however, many find it threatening and are reacting with great alarm, There’s a movement within the tech industry itself, partly motivated by competitive self-interest, calling for a “pause”, or a six-month moratorium on certain development activities. Politicians in Washington are beginning to clamor for legislation that would subject AI to regulation. However, neither a voluntary pause nor regulatory action are likely to be successful. In fact, either would likely do more harm than good.

Leaps and Bounds

The pace of advance in AI has been breathtaking. From ChatGPT 3.5 to ChatGPT 4, in a matter of just a few months, the tool went from relatively poor performance on tests like professional and graduate entrance exams (e.g., bar exams, LSAT, GRE) to very high scores. Using these tools can be a rather startling experience, as I learned for myself recently when I allowed one to write the first draft of a post. (Despite my initial surprise, my experience with ChatGPT 3.5 was somewhat underwhelming after careful review, but I’ve seen more impressive results with ChatGPT 4). They seem to know so much and produce it almost instantly, though it’s true they sometimes “hallucinate”, reflect bias, or invent sources, so thorough review is a must.

Nevertheless, AIs can write essays and computer code, solve complex problems, create or interpret images, sounds and music, simulate speech, diagnose illnesses, render investment advice, and many other things. They can create subroutines to help themselves solve problems. And they can replicate!

As a gauge of the effectiveness of models like ChatGPT, consider that today AI is helping promote “over-employment”. That is, there are a number of ambitious individuals who, working from home, are holding down several different jobs with the help of AI models. In fact, some of these folks say AIs are doing 80% of their work. They are the best “assistants” one could possibly hire, according to a man who has four different jobs.

Economist Bryan Caplan is an inveterate skeptic of almost all claims that smack of hyperbole, and he’s won a series of bets he’s solicited against others willing to take sides in support of such claims. However, Caplan thinks he’s probably lost his bet on the speed of progress on AI development. Needless to say, it has far exceeded his expectations.

Naturally, the rapid progress has rattled lots of people, including many experts in the AI field. Already, we’re witnessing the emergence of “agency” on the part of AI Learning Language Models (LLMs), or so called “agentic” behavior. Here’s an interesting thread on agentic AI behavior. Certain models are capable of teaching themselves in pursuit of a specified goal, gathering new information and recursively optimizing their performance toward that goal. Continued gains may lead to an AI model having artificial generative intelligence (AGI), a superhuman level of intelligence that would go beyond acting upon an initial set of instructions. Some believe this will occur suddenly, which is often described as the “foom” event.

Team Uh-Oh

Concern about where this will lead runs so deep that a letter was recently signed by thousands of tech industry employees, AI experts, and other interested parties calling for a six-month worldwide pause in AI development activity so that safety protocols can be developed. One prominent researcher in machine intelligence, Eliezer Yudkowsky, goes much further: he believes that avoiding human extinction requires immediate worldwide limits on resources dedicated to AI development. Is this a severely overwrought application of the precautionary principle? That’s a matter I’ll consider at greater length below, but like Caplan, I’m congenitally skeptical of claims of impending doom, whether from the mouth of Yudkowsky, Greta Thunberg, Paul Ehrlich, or Nassim Taleb.

As I mentioned at the top, I suspect competition among AI developers played a role in motivating some of the signatories of the “AI pause” letter, and some of the non-signatories as well. Robin Hanson points out that Sam Altman, the CEO of OpenAI, did not sign the letter. OpenAI (controlled by a nonprofit foundation) owns ChatGPT and is the current leader in rolling out AI tools to the public. ChatGPT 4 can be used with the Microsoft search engine Bing, and Microsoft’s Bill Gates also did not sign the letter. Meanwhile, Google was caught flat-footed by the ChatGPT rollout, and its CEO signed. Elon Musk (who signed) wants to jump in with his own AI development: TruthGPT. Of course, the pause letter stirred up a number of members of Congress, which I suspect was the real intent. It’s reasonable to view the letter as a means of leveling the competitive landscape. Thus, it looks something like a classic rent-seeking maneuver, buttressed by the inevitable calls for regulation of AIs. However, I certainly don’t doubt that a number of signatories did so out of a sincere belief that the risks of AI must be dealt with before further development takes place.

The vast dimensions of the supposed AI “threat” may have some libertarians questioning their unequivocal opposition to public intervention. If so, they might just as well fear the potential that AI already holds for manipulation and control by central authorities in concert with their tech and media industry proxies. But realistically, broad compliance with any precautionary agreement between countries or institutions, should one ever be reached, is pretty unlikely. On that basis, a “scout’s honor” temporary moratorium or set of permanent restrictions might be comparable to something like the Paris Climate Accord. China and a few other nations are unlikely to honor the agreement, and we really won’t know whether they’re going along with it except for any traceable artifacts their models might leave in their wake. So we’ll have to hope that safeguards can be identified and implemented broadly.

Likewise, efforts to regulate by individual nations are likely to fail, and for similar reasons. One cannot count on other powers to enforce the same kinds of rules, or any rules at all. Putting our faith in that kind of cooperation with countries who are otherwise hostile is a prescription for ceding them an advantage in AI development and deployment. Regulation of the evolution of AI will likely fail. As Robert Louis Stevenson once wrote, “Thus paternal laws are made, thus they are evaded”. And if it “succeeds, it will leave us with a technology that will fall short of its potential to benefit consumers and society at large. That, unfortunately, is usually the nature of state intrusion into a process of innovation, especially when devised by a cadre of politicians with little expertise in the area.

Again, according to experts like Yudkowsky, AGI would pose serious risks. He thinks the AI Pause letter falls far short of what’s needed. For this reason, there’s been much discussion of somehow achieving an alignment between the interests of humanity and the objectives of AIs. Here is a good discussion by Seth Herd on the LessWrong blog about the difficulties of alignment issues.

Some experts feel that alignment is an impossibility, and that there are ways to “live and thrive” with unalignment (and see here). Alignment might also be achieved through incentives for AIs. Those are all hopeful opinions. Others insist that these models still have a long way to go before they become a serious threat. More on that below. Of course, the models do have their shortcomings, and current models get easily off-track into indeterminacy when attempting to optimize toward an objective.

But there’s an obvious question that hasn’t been answered in full: what exactly are all these risks?As Tyler Cowen has said, it appears that no one has comprehensively catalogued the risks or specified precise mechanisms through which those risks would present. In fact, AGI is such a conundrum that it might be impossible to know precisely what threats we’ll face. But even now, with deployment of AIs still in its infancy, it’s easy to see a few transition problems on the horizon.

White Collar Wipeout

Job losses seem like a rather mundane outcome relative to extinction. Those losses might come quickly, particularly among white collar workers like programmers, attorneys, accountants, and a variety of administrative staffers. According to a survey of 1,000 businesses conducted in February:

“Forty-eight percent of companies have replaced workers with ChatGPT since it became available in November of last year. … When asked if ChatGPT will lead to any workers being laid off by the end of 2023, 33% of business leaders say ‘definitely,’ while 26% say ‘probably.’ … Within 5 years, 63% of business leaders say ChatGPT will ‘definitely’ (32%) or ‘probably’ (31%) lead to workers being laid off.”

A rapid rate of adoption could well lead to widespread unemployment and even social upheaval. For perspective, that implies a much more rapid rate of technological diffusion than we’ve ever witnessed, so this outcome is viewed with skepticism in some quarters. But in fact, the early adoption phase of AI models is proceeding rather quickly. You can use ChatGPT 4 easily enough on the Bing platform right now!

Contrary to the doomsayers, AI will not just enhance human productivity. Like all new technologies, it will lead to opportunities for human actors that are as yet unforeseen. AI is likely to identify better ways for humans to do many things, or do wonderful things that are now unimagined. At a minimum, however, the transition will be disruptive for a large number of workers, and it will take some time for new opportunities and roles for humans to come to fruition.

Robin Hanson has a unique proposal for meeting the kind of challenge faced by white collar workers vulnerable to displacement by AI, or for blue collar workers who are vulnerable to displacement by robots (the deployment of which has been hastened by minimum wage and living wage activism). This treatment of Hanson’s idea will be inadequate, but he suggests a kind of insurance or contract sold to both workers and investors by owners of assets likely to be insensitive to AI risks. The underlying assets are paid out to workers if automation causes some defined aggregate level of job loss. Otherwise, the assets are paid out to investors taking the other side of the bet. Workers could buy these contracts themselves, or employers could do so on their workers’ behalf. The prices of the contracts would be determined by a market assessment of the probability of the defined job loss “event”. Governmental units could buy the assets for their citizens, for that matter. The “worker contracts” would be cheap if the probability of the job-loss event is low. Sounds far-fetched, but perhaps the idea is itself an entrepreneurial opportunity for creative players in the financial industry.

The threat of job losses to AI has also given new energy to advocates of widespread adoption of universal basic income payments by government. Hanson’s solution is far preferable to government dependence, but perhaps the state could serve as an enabler or conduit through which workers could acquire AI and non-AI capital.

Human Capital

Current incarnations of AI are not just a threat to employment. One might add the prospect that heavy reliance on AI could undermine the future education and critical thinking skills of the general population. Essentially allowing machines to do all the thinking, research, and planning won’t inure to the cognitive strength of the human race, especially over several generations. Already people suffer from an inability to perform what were once considered basic life skills, to say nothing of tasks that were fundamental to survival in the not too distant past. In other words, AI could exaggerate a process of “dumbing down” the populace, a rather undesirable prospect.

Fraud and Privacy

AI is responsible for still more disruptions already taking place, in particular violations of privacy, security, and trust. For example, a company called Clearview AI has scraped 30 billion photos from social media and used them to create what its CEO proudly calls a “perpetual police lineup”, which it has provided for the convenience of law enforcement and security agencies.

AI is also a threat to encryption in securing data and systems. Conceivably, AI could be of value in perpetrating identity theft and other kinds of fraud, but it can also be of value in preventing them. AI is also a potential source of misleading information. It is often biased, reflecting specific portions of the on-line terrain upon which it is trained, including skewed model weights applied to information reflecting particular points of view. Furthermore, misinformation can be spread by AIs via “synthetic media” and the propagation of “fake news”. These are fairly clear and present threats of social, economic, and political manipulation. They are all foreseeable dangers posed by AI in the hands of bad actors, and I would include certain nudge-happy and politically-motivated players in that last category.

The Sky-Already-Fell Crowd

Certain ethicists with extensive experience in AI have condemned the signatories of the “Pause Letter” for a focus on “longtermism”, or risks as yet hypothetical, rather than the dangers and wrongs attributable to AIs that are already extant:TechCrunch quotes a rebuke penned by some of these dissenting ethicists to supporters of the “Pause Letter”:

“‘Those hypothetical risks are the focus of a dangerous ideology called longtermism that ignores the actual harms resulting from the deployment of AI systems today,’ they wrote, citing worker exploitation, data theft, synthetic media that props up existing power structures and the further concentration of those power structures in fewer hands.”

So these ethicists bemoan AI’s presumed contribution to the strength and concentration of “existing power structures”. In that, I detect just a whiff of distaste for private initiative and private rewards, or perhaps against the sovereign power of states to allow a laissez faire approach to AI development (or to actively sponsor it). I have trouble taking this “rebuke” too seriously, but it will be fruitless in any case. Some form of cooperation between AI developers on safety protocols might be well advised, but competing interests also serve as a check on bad actors, and it could bring us better solutions as other dilemmas posed by AI reveal themselves.

ImaginingAI Catastrophes

What are the more consequential (and completely hypothetical) risks feared by the “pausers” and “stoppers”. Some might have to do with the possibility of widespread social upheaval and ultimately mayhem caused by some of the “mundane” risks described above. But the most noteworthy warnings are existential: the end of the human race! How might this occur when AGI is something confined to computers? Just how does the supposed destructive power of AGIs get “outside the box”? It must do so either by tricking us into doing something stupid, hacking into dangerous systems (including AI weapons systems or other robotics), and/or through the direction and assistance of bad human actors. Perhaps all three!

The first question is this: why would an AGI do anything so destructive? No matter how much we might like to anthropomorphize an “intelligent” machine, it would still be a machine. It really wouldn’t like or dislike humanity. What it would do, however, is act on its objectives. It would seek to optimize a series of objective functions toward achieving a goal or a set of goals it is given. Hence the role for bad actors. Let’s face it, there are suicidal people who might like nothing more than to take the whole world with them.

Otherwise, if humanity happens to be an obstruction to solving an AGI’s objective, then we’d have a very big problem. Humanity could be an aid to solving an AGI’s optimization problem in ways that are dangerous. As Yudkowsky says, we might represent mere “atoms it could use somewhere else.” And if an autonomous AGI were capable of setting it’s own objectives, without alignment, the danger would be greatly magnified. An example might be the goal of reducing carbon emissions to pre-industrial levels. How aggressively would an AGI act in pursuit of that goal? Would killing most humans contribute to the achievement of that goal?

Here’s one that might seem far-fetched, but the imagination runs wild: some individuals might be so taken with the power of vastly intelligent AGI as to make it an object of worship. Such an “AGI God” might be able to convert a sufficient number of human disciples to perpetrate deadly mischief on its behalf. Metaphorically speaking, the disciples might be persuaded to deliver poison kool-aid worldwide before gulping it down themselves in a Jim Jones style mass suicide. Or perhaps the devoted will survive to live in a new world mono-theocracy. Of course, these human disciples would be able to assist the “AGI God” in any number of destructive ways. And when brain-wave translation comes to fruition, they better watch out. Only the truly devoted will survive.

An AGI would be able to create the illusion of emergency, such as a nuclear launch by an adversary nation. In fact, two or many adversary nations might each be fooled into taking actions that would assure mutual destruction and a nuclear winter. If safeguards such as human intermediaries were required to authorize strikes, it might still be possible for an AGI to fool those humans. And there is no guarantee that all parties to such a manufactured conflict could be counted upon to have adequate safeguards, even if some did.

Yudkowsky offers at least one fairly concrete example of existential AGI risk:

“A sufficiently intelligent AI won’t stay confined to computers for long. In today’s world you can email DNA strings to laboratories that will produce proteins on demand, allowing an AI initially confined to the internet to build artificial life forms or bootstrap straight to postbiological molecular manufacturing.”

There are many types of physical infrastructure or systems that an AGI could conceivably compromise, especially with the aid of machinery like robots or drones to which it could pass instructions. Safeguards at nuclear power plants could be disabled before steps to trigger melt down. Water systems, rivers, and bodies of water could be poisoned. The same is true of food sources, or even the air we breathe. In any case, complete social disarray might lead to a situation in which food supply chains become completely dysfunctional. So, a super-intelligence could probably devise plenty of “imaginative” ways to rid the earth of human beings.

Back To Earth

Is all this concern overblown? Many think so. Bryan Caplan now has a $500 bet with Eliezer Yudkowsky that AI will not exterminate the human race by 2030. He’s already paid Yudkowsky, who will pay him $1,000 if we survive. Robin Hanson says “Most AI Fear Is Future Fear”, and I’m inclined to agree with that assessment. In a way, I’m inclined to view the AI doomsters as highly sophisticated, change-fearing Luddites, but Luddites nevertheless.

Ben Hayum is very concerned about the dangers of AI, butwriting at LessWrong, he recognizes some real technical barriers that must be overcome for recursive optimization to be successful. He also notes that the big AI developers are all highly focused on safety. Nevertheless, he says it might not take long before independent users are able to bootstrap their own plug-ins or modules on top of AI models to successfully optimize without running off the rails. Depending on the specified goals, he thinks that will be a scary development.

James Pethokoukis raises a point that hasn’t had enough recognition: successful innovations are usually dependent on other enablers, such as appropriate infrastructure and process adaptations. What this means is that AI, while making spectacular progress thus far, won’t have a tremendous impact on productivity for at least several years, nor will it pose a truly existential threat. The lag in the response of productivity growth would also limit the destructive potential of AGI in the near term, since installation of the “social plant” that a destructive AGI would require will take time. This also buys time for attempting to solve the AI alignment problem.

In another Robin Hanson piece, he expresses the view that the large institutions developing AI have a reputational Al stake and are liable for damages their AI’s might cause. He notes that they are monitoring and testing AIs in great detail, so he thinks the dangers are overblown.:

“So, the most likely AI scenario looks like lawful capitalism…. Many organizations supply many AIs and they are pushed by law and competition to get their AIs to behave in civil, lawful ways that give customers more of what they want compared to alternatives.”

In the longer term, the chief focus of the AI doomsters, Hanson is truly an AI optimist. He thinks AGIs will be “designed and evolved to think and act roughly like humans, in order to fit smoothly into our many roughly-human-shaped social roles.” Furthermore, he notes that AI owners will have strong incentives to monitor and “delimit” AI behavior that runs contrary to its intended purpose. Thus, a form of alignment is achieved by virtue of economic and legal incentives. In fact, Hanson believes the “foom” scenario is implausible because:

“… it stacks up too many unlikely assumptions in terms of our prior experiences with related systems. Very lumpy tech advances, techs that broadly improve abilities, and powerful techs that are long kept secret within one project are each quite rare. Making techs that meet all three criteria even more rare. In addition, it isn’t at all obvious that capable AIs naturally turn into agents, or that their values typically change radically as they grow. Finally, it seems quite unlikely that owners who heavily test and monitor their very profitable but powerful AIs would not even notice such radical changes.”

As smart as AGIs would be, Hanson asserts that the problem of AGI coordination with other AIs, robots, and systems would present insurmountable obstacles to a bloody “AI revolution”. This is broadly similar to Pethokoukis’ theme. Other AIs or AGIs are likely to have competing goals and “interests”. Conflicting objectives and competition of this kind will do much to keep AGIs honest and foil malign AGI behavior.

The kill switch is a favorite response of those who think AGI fears are exaggerated. Just shut down an AI if its behavior is at all aberrant, or if a user attempts to pair an AI model with instructions or code that might lead to a radical alteration in an AI’s level of agency. Kill switches would indeed be effective at heading off disaster if monitoring and control is incorruptible. This is the sort of idea that begs for a general solution, and one hopes that any advance of that nature will be shared broadly.

One final point about AI agency is whether autonomous AGIs might ever be treated as independent factors of production. Could they be imbued with self-ownership?Tyler Cowen asks whether an AGI created by a “parent” AGI could legitimately be considered an independent entity in law, economics, and society. And how should income “earned” by such an AGI be treated for tax purposes. I suspect it will be some time before AIs, including AIs in a lineage, are treated separately from their “controlling” human or corporate entities. Nevertheless, as Cowen says, the design of incentives and tax treatment of AI’s might hold some promise for achieving a form of alignment.

Letting It Roll

There’s plenty of time for solutions to the AGI threat to be worked out. As I write this, the consensus forecast for the advent of real AGI on the Metaculus online prediction platform is July 27, 2031. Granted, that’s more than a year sooner than it was 11 days ago, but it still allows plenty of time for advances in controlling and bounding agentic AI behavior. In the meantime, AI is presenting opportunities to enhance well being through areas like medicine, nutrition, farming practices, industrial practices, and productivity enhancement across a range of processes. Let’s not forego these opportunities. AI technology is far too promising to hamstring with a pause, moratoria, or ill-devised regulations. It’s also simply impossible to stop development work on a global scale.

Nevertheless, AI issues are complex for all private and public institutions. Without doubt, it will change our world. This AI Policy Guide from Mercatus is a helpful effort to lay out issues at a high-level.

There’s justifiable controversy surrounding TikTok, the social media app. I find much to dislike about TikTok but also much to dislike about the solutions some have proposed, such as a complete ban on the app in the United States. Such proposals would grant the federal executive branch powers that most of us wouldn’t grant to our worst enemy (i.e., they fail the “Munger test”).

Congressional Activity

The proposed RESTRICT Act (Restricting the Emergence of Security Threats that Risk Information and Communications Technology) is a bipartisan effort to eliminate the perceived threats to national security posed by technologies like TikTok. That would include a ban on the app. Proponents of a ban go further than national security concerns, arguing that TikTok represents a threat to the health and productivity of users. However, an outright ban on the app would be a drastic abridgment of free speech rights, and it would limit Americans’ access to a popular platform for creativity and entertainment. In addition, the proposed legislation would authorize intrusions into the privacy of Americans and extend new executive authority into the private sphere, such as tampering with trade and commerce in ways that could facilitate protectionist actions. In fact, so intrusive is the RESTRICT Act that it’s been called a “Patriot Act for the digital age.” From Scott Lincicome and several coauthors at CATO:

“… the proposal—at least as currently written—raises troubling and far‐reaching concerns for the First Amendment, international commerce, technology, privacy, and separation of powers.”

Bad Company

TikTok is owned by a Chinese company, ByteDance, and there is understandable concern about the app’s data collection practices and the potential for the Chinese government to access user data for nefarious purposes. The Trump administration cited these concerns when it attempted to ban TikTok in 2020, and while the ban was ultimately blocked by a federal judge, the Biden administration has also expressed concerns about the app’s data security.

TikTok has also been accused of promoting harmful content, including hate speech, misinformation, and sexually explicit material. Critics argue that the app’s algorithm rewards provocative and controversial content, which can lead to the spread of harmful messages and the normalization of inappropriate behavior. Of course, those are largely value judgements, including labels like “provocative”, “inappropriate”, and many interpretations of content as “hate speech”. With narrow exceptions, such content is protected under the First Amendment.

Unlike L. Frank Baum’s Tik-Tok machine in the land of Oz, the TikTok app might not always qualify as a “faithful servant”. There are some well-founded health and performance concerns related to TikTok, however. Some experts have expressed reservations about the effects of the app on attention span. The short-form videos typical of TikTok, and endless scrolling, suggest that the app is designed to be addictive, though I’m not aware of studies that purport to prove its “addictive nature. Of course, it can easily become a time sink for users, but so can almost all social media platforms. Nevertheless, some experts contend that heavy use of TikTok may lead to a decrease in attention span and an increase in distraction, which can have negative implications for productivity, learning, and mental health.

Bad Government

The RESTRICT Act, or a ban on TikTok, would drastically violate free speech rights and limit Americans’ access to a popular platform for creativity and self-expression. TikTok has become a cultural phenomenon, with millions of users creating and sharing content on the app every day. This is particularly true of more youthful individuals, who are less likely to be persuaded by their elders’ claims that the content available on TikTok is “inappropriate”. And they’re right! At the very least, “appropriateness” depends on an individual’s age, and it is generally not an area over which government should have censorship authority, “community standards” arguments notwithstanding. Furthermore, allowing access for children is a responsibility best left in the hands of parents, not government.

Likewise, businesses should be free to operate without undue interference from government. The RESTRICT Act would violate these principles, as it would limit individual choice and potentially harm innovation within the U.S. tech industry.

A less compelling argument against banning TikTok is that it could harm U.S.-China relations and have broader economic consequences. China has already warned that a TikTok ban could prompt retaliation, and such a move could escalate tensions between the two countries. That’s all true to one degree or another, but China has already demonstrated a willingness and intention to harm U.S.-China relations. As for economic repercussions, do business with China at your own risk. According to this piece, U.S. investment in the PRC’s tech industry has fallen by almost 80% since 2018, so the private sector is already taking strong steps to reduce that risk.

Like it or not, however, many software companies are subject to at least partial Chinese jurisdiction. The means the RESTRICT Act would do far more than simply banning TikTok in the U.S. First, it would subject on-line activity to much greater scrutiny. Second, it would threaten users of a variety of information or communications products and services with severe penalties for speech deemed to be “unsafe”. According to Columbia Law Professor Philip Hamburger:

“Under the proposed statute, the commerce secretary could therefore take ‘any mitigation measure to address any risk’ arising from the use of the relevant communications products or services, if the secretary determines there is an ‘undue or unacceptable risk to the national security of the United States or the safety of United States persons.’

We live in an era in which dissenting speech is said to be violence. In recent years, the Federal Bureau of Investigation has classified concerned parents and conservative Catholics as violent extremists. So when the TikTok bill authorizes the commerce secretary to mitigate communications risks to ‘national security’ or ‘safety,’ that means she can demand censorship.”

A Lighter Touch

The RESTRICT Act is unreasonably broad and intrusive and an outright ban of TikTok is unnecessarily extreme. There are less draconian alternatives, though all may involve some degree of intrusion. For example, TikTok could be compelled to allow users to opt out of certain types of data collection, and to allow independent audits of its data handling practices. TikTok could also be required to store user data within the U.S. or in other countries that have strong data privacy laws. While this option would represent stronger regulation of TikTok, it could also be construed as strengthening the property rights of users.

To address concerns about TikTok’s ownership by a Chinese company, its U.S. operations could be required to partner with a U.S. company. Perhaps this could satisfied by allowing a U.S. company to acquire a stake in TikTok, or by having TikTok spin off its U.S. operations into a separate company that is majority-owned by a U.S. entity.

Finally, perhaps political or regulatory pressure could persuade TikTok to switch to using open-source software, as Elon Musk has done with Twitter. Then, independent developers would have the ability to audit code and identify security vulnerabilities or suspicious data handling practices. From there, it’s a matter of caveat emptor.

Restrain the Restrictive Impulse

The TikTok debate raises important questions about the role of government in regulating technology and free speech. Rather than impulsively harsh legislation like the RESTRICT Act or an outright ban on TikTok, an enlightened approach would encourage transparency and competition in the tech industry. That, in turn, could help address concerns about data security and promote innovation. Additionally, individuals should take personal responsibility for their use of technology by being mindful of the content they consume and what they reveal about themselves on social media. That includes parental responsibility and supervision of the use of social media by children. Ultimately, the TikTok debate highlights tensions between national security, technological innovation, and individual liberty. and it’s important to find a balance that protects all three.

Note: The first draft of this post was written by ChatGPT, based on an initial prompt and sequential follow-ups. It was intended as an experiment in preparation for a future post on artificial intelligence (AI). While several vestiges of the first draft remain, what appears above bears little resemblance to what ChatGPT produced. There were many deletions, rewrites, and supplements in arriving at the final draft.

My first impression of the ChatGPT output was favorable. It delineated a few of the major issues surrounding a TikTok ban, but later I was struck by its repetition of bland generalities and its lack of information on more recent developments like the RESTRICT Act. The latter shortfall was probably due to my use of ChatGPT 3.5 rather than 4.0. On the whole, the exercise was fascinating, but I will limit my use of AI tools like ChatGPT to investigation of background on certain questions.

To the great chagrin of some market watchers, the Federal Reserve Open Market Committee (FOMC) increased its target for the federal funds rate in March by 0.25 points, to range of 4.75 – 5%. This was pretty much in line with plans the FOMC made plain in the fall. The “surprise” was that this increase took place against a backdrop of liquidity shortfalls in the banking system, which also had taken many by surprise. Perhaps a further surprise was that after a few days of reflection, the market didn’t seem to mind the rate hike all that much.

Switchman Sleeping

There’s plenty of blame to go around for bank liquidity problems. Certain banks and their regulators (including the Fed) somehow failed to anticipate that carrying large, unhedged positions in low-rate, long-term bonds might at some point alarm large depositors as interest rates rose. Those banks found themselves way short of funds needed to satisfy justifiably skittish account holders. A couple of banks were closed, but the FDIC agreed to insure all of their depositors. As the lender of last resort, the Fed provided banks with “credit facilities” to ease the liquidity crunch. In a matter of days, the fresh credit expanded the Fed’s balance sheet, offsetting months of “quantitative tightening” that had taken place since last June.

Of course, the Fed is no stranger to dozing at the switch. Historically, the central bank has failed to anticipate changes wrought by its own policy actions. Today’s inflation is a prime example. That kind of difficulty is to be expected given the “long and variable lags” in the effects of monetary policy on the economy. It makes activist policy all the more hazardous, leading to the kinds of “boom and bust” cycles described in Austrian business cycle theory.

Persistent Inflation

When the Fed went forward with the 25 basis point hike in the funds rate target in March, it was greeted with dismay by those still hopeful for a “soft landing”. In the Fed’s defense, one could say the continued effort to tighten policy is an attempt to make up for past sins, namely the Fed’s monetary profligacy during the pandemic.

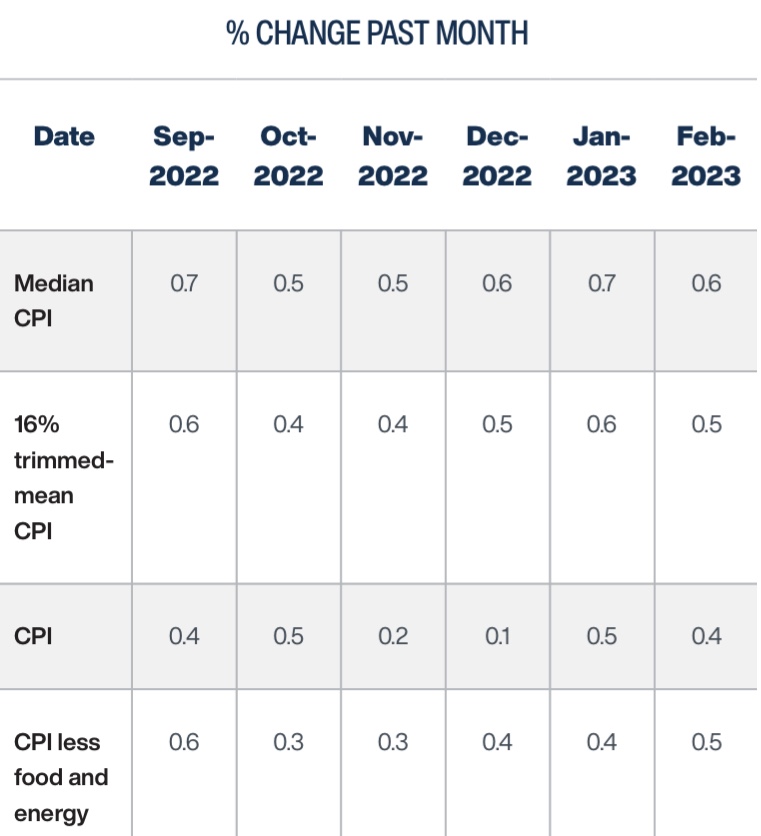

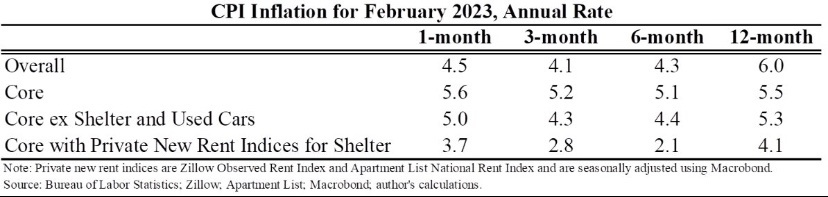

The Fed’s rationale for this latest rate hike was that inflation remains persistent. Here are four CPI measures from the Cleveland Fed, which show some recent tapering of price pressures. Perhaps “flattening” would be a better description, at least for the median CPI:

Those are 12-month changes, and just in case you’ve heard that month-to-month changes have tapered more sharply, that really wasn’t the case in January and February:

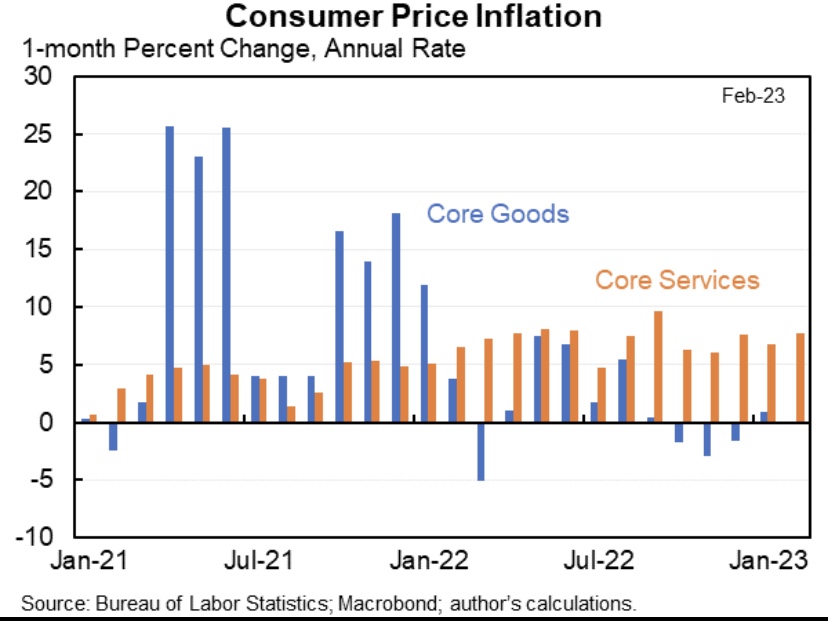

Jason Furman notedin a series of tweets that the prices of services are driving recent inflation, while goods prices have been flat:

A compelling argument is that the shelter component of the CPI is overstating services inflation, and it’s weighted at more than one-third of the overall index. CPI shelter costs are known as “owner’s equivalent rent” (OER), which is based on a survey question of homeowners as to the rents they think they could command, and it is subject to a fairly long lag. Actual rent inflation has slowed sharply since last summer, so the shelter component is likely to relieve pressure on CPI inflation (and the Fed) in coming months. Nevertheless, Furman points out that CPI inflation over the past 3 -4 months was up even when housing is excluded. Substituting a private “new rent” measure of housing costs for OER would bring measured inflation in services closer the Fed’s comfort zone, however.

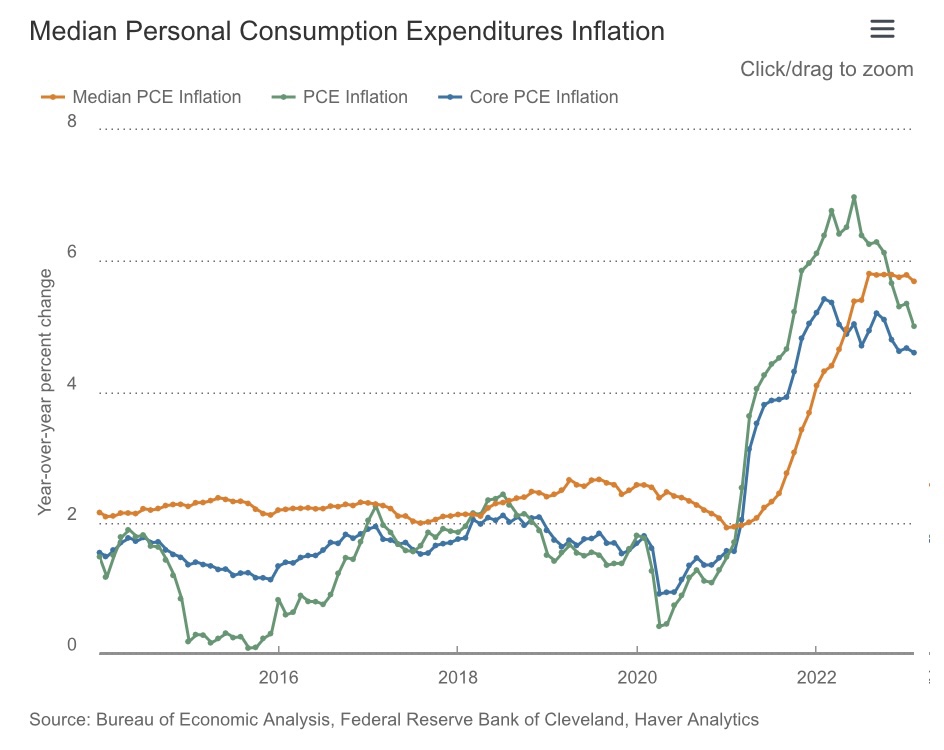

The Fed’s preferred measure of inflation, the deflator for personal consumption expenditures (PCE), uses a much lower weight on housing costs, though it might also overstate inflation within that component. Here’s another chart from the Cleveland Fed:

Inflation in the Core PCE deflator, which excludes food and energy prices, looks as if it’s “flattened” as well. This persistence is worrisome because inflation is difficult to stop once it becomes embedded in expectations. That’s exactly what the Fed says it’s trying to prevent.

Rate Targets and Money Growth

Targeting the federal funds rate (FFR) is the Fed’s primary operational method of conducting monetary policy. The FFR is the rate at which banks borrow from one another overnight to meet short-term needs for reserves. In order to achieve price stability, the Fed would do better to focus directly on controlling the money supply. Nevertheless, it has successfully engineered a decline in the money supply beginning last April, and recently the money supply posted year-over-year negative growth.

That doesn’t mean money growth has been “optimized” in any sense, but a slowdown in money growth was way overdue after the pandemic money creation binge. You might not like the way the Fed executed the reversal or its operating policy in general, and neither do I, but it did restrain money growth. In that sense, I applaud the Fed for exercising its independence, standing up to the Treasury rather than continuing to monetize yawning federal deficits. That’s encouraging, but at some point the Fed will reverse course and ease policy. We’ll probably hope in vain that the Fed can avoid sending us once again along the path of boom and bust cycles.

In effect, the FFR target is a price control with a dynamic element: the master fiddles with the target whenever economic conditions are deemed to suggest a change. This “controlled” rate has a strong influence on other short-term interest rates. The farther out one goes on the maturity spectrum, however, the weaker is the association between changes in the funds rate and other interest rates. The Fed doesn’t truly “control” those rates of most importance to consumers, corporate borrowers, government borrowers, and investors. It definitely influences those rates, but credit risk, business opportunities, and long-term expectations are often dominant.

The FOMC’s latest rate increase suggests its members don’t expect an immediate downturn in economic activity or a definitive near-term drop in inflation. The Committee may, however, be willing to pause for a period of several meeting cycles (every six weeks) to see whether the “long and variable lags” in the transmission of tighter monetary policy might begin to kick-in. As always, the FOMC’s next step will be “data dependent”, as Chairman Powell likes to say. In the meantime, the economic response to earlier tightening moves is likely to strengthen. Lenders are responding to the earlier rate hikes and reduced lending margins by curtailing credit and attempting to rebuild their own liquidity.

Is It Supply Or Demand?

There’s an ongoing debate about whether monetary policy is appropriate for fighting this episode of inflation. It’s true that monetary policy is ill-suited to addressing supply disruptions, though it can help to stem expectations that might cause supply-side price pressures to feed upon themselves (and prevent them from becoming demand-side pressures). However, profligate fiscal and monetary policy did much to create the current inflation, which is pressure on the demand-side. On that point, David Beckworth leaves little doubt as to where he stands:

“The real world is nominal. And nominal PCE was about $1.6 trillion above trend thru February. Unless one believes in immaculate above-trend spending, this huge surge could 𝙣𝙤𝙩 have happened without support from fiscal and monetary policy.”

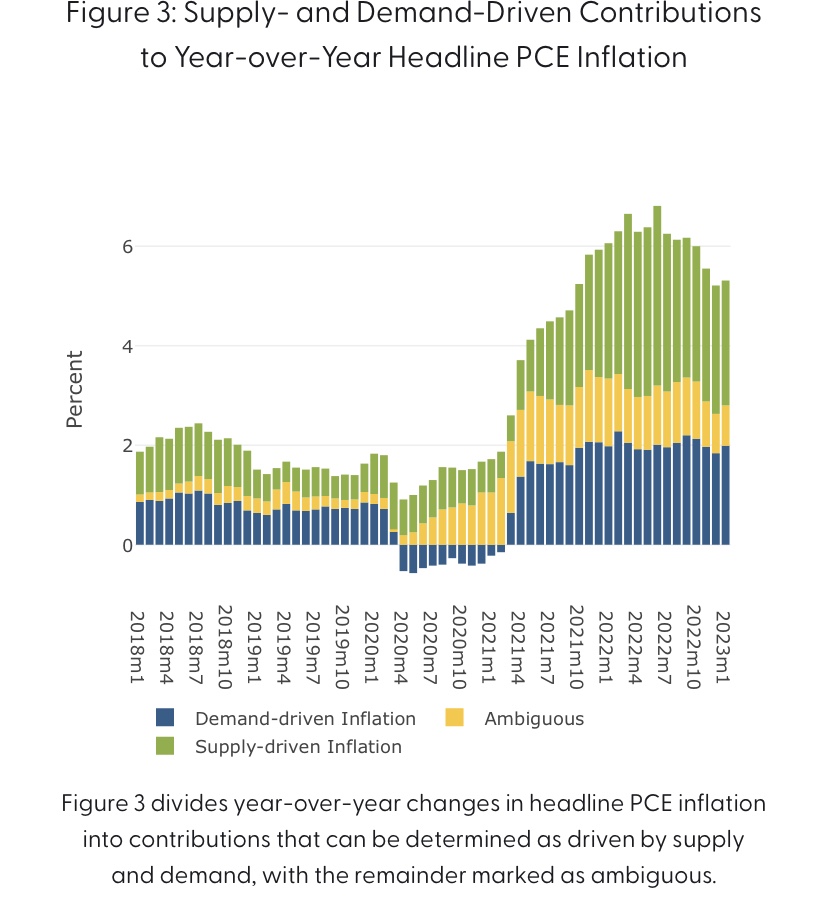

In reality, this inflationary episode was borne of a mix of demand and supply-side pressures, and policy either caused or accommodated all of it. Nevertheless, it’s interesting to consider efforts to decompose these forces. This NBER paper attributed about 2/3 of inflation from December 2019 – June 2022 to the demand-side. Given the ongoing tenor of fiscal policy and the typical policy lags, it’s likely that the effects of fiscal and monetary stimulus have persisted well beyond that point. Here is a page from the San Francisco Fed’s site that gives an edge to supply-side factors, as reflected in this breakdown of the Fed’s favorite inflation gauge:

Of course, all of these decompositions are based on assumptions and are, at best, model-based. Nevertheless, to the extent that we still face supply constraints, they would impose limits to the Fed’s ability to manage inflation downward without a “hard landing”.

There’s also no doubt that supply side policies would reduce the kinds of price pressures we’re now experiencing. Regulation and restrictive energy policies under the Biden Administration have eroded productive capacity. These policies could be reversed if political leaders were serious about improving the nation’s economic health.

The Dark Runway Ahead

Will we have a recession? And when? There are no definite signs of an approaching downturn in the real economy just yet. Inventories of goods did account for more than half of the fourth quarter gain in GDP, which may now be discouraging production. There are layoffs in some critical industries such as tech, but we’ll have to see whether there is new evidence of overall weakness in next Friday’s employment report. Real wages have been a little down to flat over the past year, while consumer debt is climbing and real retail sales have trended slightly downward since last spring. Many firms will experience higher debt servicing costs going forward. So it’s not clear that the onset of recession is close at hand, but the odds are good that we’ll see a downturn as the year wears on, especially with credit increasingly scarce in the wake of the liquidity pinch at banks. But no one knows for sure, including the Fed.

Government budget negotiations never fail to frustrate anyone of a small-government persuasion. We have a huge, ongoing federal budget deficit. Spending’s gone bat-shit out of control over the past several years and too few in Congress are willing to do anything about it. Democrats would rather see politically-targeted tax increases. While some Republicans advocate spending cuts, the focus is almost entirely on discretionary spending. Meanwhile, the entitlement state is off the table, including Social Security reform.

Fiscal Indiscretion

Sadly, non-discretionary outlays (entitlements) today make a much larger contribution to the deficit than discretionary spending. That includes the programs like Social Security (SS) and Medicare, in which spending levels are programmatic and not subject to annual appropriations by Congress. When these programs were instituted there were a large number of workers relative to retirees, so tax contributions exceeded benefit levels for many decades. The revenue excesses were placed into “trust funds” and invested in Treasury debt. In other words, surpluses under non-discretionary SS and Medicare programs were used to finance discretionary spending!

The aging of Baby Boomers ultimately led to a reversal in the condition of the trust funds. Fewer workers relative to retirees meant that annual payroll tax collections were not adequate to cover annual benefits, and that meant drawing down the trust funds. Current projections by the system trustees call for the SS Trust Fund to be exhausted by 2035. Once that occurs, benefits will automatically be reduced by roughly 20% unless Congress acts to shore up the system before then.

A Few Proposals

I’ve written about the need for SS reform on several occasions (though the first article at that link is not germane here). It seems imperative for Congress and the President to address these shortfalls. By all appearances, however, many Republicans have put the issue aside. For his part, Joe Biden has apparently accepted the prospect of an automatic reduction in benefits in 2035, or at least he’s willing to kick that can down the road. He has, however, endorsed taxes on high earners to fund Medicare. Senator John Kennedy (R-LA) suggests raising the retirement age, or at least raise the minimum age at which one may claim benefits (now 62). Senators Bill Cassidy (R-La.) and Angus King (I-Maine) were working on a compromise that would create an investment fund to fortify the system, but the specifics are unclear, as well as how much that would accomplish.

Meanwhile, Senator Bernie Sanders (S-VT) proposes to expand SS benefits by $2,400 a year and add funding by extending payroll taxes to earners above the current limit of $160,000. Senator Joe Manchin (D-WV) has endorsed the latter as a “quick fix”.

There is also at least oneproposal in Congress to end the practice of taxing a portion of SS benefits as income. I have trouble believing it will gain wide support, despite the clear double-taxation involved.

Then there are always discussions of reducing benefits at higher income levels or even means-testing benefits. In fact, it would be interesting to know what proportion of current benefits actually function as social insurance, as opposed to a universal entitlement. The answer, at least, could serve as a baseline for more fundamental reforms, including changes in the structure of payroll taxes, voluntary lump-sum payouts, and private accounts.

More Radical Views

There are a few prominent voices who claim that SS is sustainable in its current form, but perhaps with a few “no big deal” tax increases. Oh, that’s only about a $1 trillion “deal”, at least for both Medicare and SS. More offensive still are the scare tactics used by opponents of SS reform any time the subject comes up. I’m not aware of any serious reform proposal made over the past two decades that would have affected the benefits of anyone over the age of 55, and certainly no one then-eligible for benefits. Yet that charge is always made: they want to cut your SS benefits! The Democrats made that claim against George W. Bush, torpedoing what might have been a great accomplishment for all. And now, apparently Donald Trump is willing to use such accusations to damage any rival who has ever mentioned reform, including Mike Pence. Will you please cut the crap?

The System

The thing to remember about SS is that it is currently structured as a pay-as-you-go (PAYGO) system, despite the fact that benefits are defined like many creaky private pensions of old. SS benefits in each period are paid out of current “contributions” (i.e., FICO payroll taxes) plus redemptions of government bonds held in the Trust Fund. Contributions today are not “invested” anywhere because they are not enough to pay for current benefits under PAYGO.

The Trust Fund was accumulated during the years when favorable demographics led to greater FICO contributions than benefit payouts. The excess revenue was “invested” in Treasury bonds, which meant it was used to fund deficits in the general budget. It’s been about 15 years since the Trust Fund entered a “draw-down” status, and again, it will be exhausted by 2035.

SSA Says It’s a Good Deal

A participant’s expected “rate of return” on lifetime payroll tax payments depends on several things: lifetime earnings, age at which benefits are first claimed, life expectancy at that time, marital status, relative earning levels within two-earner couples, and the “full retirement age” for the individual’s birth year. Payroll tax payments, by the way, include the employer’s share because that is one of the terms of a hire. A high rate of return is not the same as a high level of benefits, however. In fact, relative to career income, SS has a great deal of progressivity in terms of rates of return, but not much in terms of benefit levels.

The Social Security Administration (SSA) has calculated illustrative real internal rates of return (IRR) for many categories of earners given certain assumptions. (An IRR is a discount rate that equalizes the present value (PV) of a stream of payments and the PV of a stream of payoffs.) The SSA’s most recent update of this exercise was in April 2022. The report references Old Age, Survivors, and Disability Insurance (OASDI), but the focus is exclusively on seniors.

Three basic scenarios were considered: 1) current law, as scheduled, despite its unsustainability; 2) a payroll tax increase from 12.4% (not including the Medicare tax) to 15.96% starting in 2035, when the Trust Fund is exhausted; and 3) a reduction in benefits of 22% starting in 2035.

The authors of the report concludethat “… the real value of OASDI benefits is extraordinarily high.” This theme has been echoed by several other writers, such as here and here. This conclusion is based on a comparison to returns earned by investments that SSA judges to have comparably low risk.