Donald Trump’s latest volley against the Federal Reserve accuses the central bank of fixing interest rates at artificially high levels compared to rates in other developed countries. He repeatedly demands that the Fed make a large cut to its federal funds rate target, in the apparent belief that other rates will immediately fall with it. While a highly imperfect analogy, that’s a bit like saying that long-term parking in New York City would be cheaper if only hourly rates were cut to what’s charged in Omaha, and with only favorable consequences. Don’t tell Mamdani!

Trump believes the Fed’s restrictive monetary policy is preventing the economy from achieving its potential under his policies. He also argues that the Fed’s “high-rate” policy is costing the federal government and taxpayers hundreds of billions in excessive interest on federal debt. High rates can certainly impede growth and raise the cost of debt service. The question is whether there is a policy that can facilitate growth and reduce borrowing costs without risking other objectives, most notably price stability.

Delusions of Control

The financial community understands that the Fed does not directly control rates paid by the Treasury on federal debt. The Fed has its most influence on rates at the short end of the maturity spectrum. Rates on longer-term Treasury notes and bonds are subject to a variety of market forces, including expected inflation, the expected future path of federal deficits, and the perceived direction of the economy, to name a few. The Fed simply cannot dictate investor sentiments and expectations, and the ongoing flood of new Treasury debt complicates matters.

Another fundamental lesson for Trump is that cross-country comparisons of interest rates are meaningless outside the context of differing economic conditions. Market interest rates are driven by things that vary from one country to another, such as expected inflation rates, economic policies, currency values, and the strength of the home economy. Differences in rates are always the result of combinations of circumstances and expectations, which can be highly varied.

A Few Comparisons

A few examples will help reinforce this point. Below, I compare the U.S. to a few other countries in terms of recent short-term central bank rate targets and long-term market interest rates. Then we can ask what conditions explain these divergencies. For reference, the current fed funds rate target range is 4.25 – 4.5%, while 10-year Treasury bonds have traded recently at yields in the same range. Current U.S. inflation is roughly 2.5%.

It’s important to remember that markets attempt to price bonds to compensate buyers for expected future inflation. Currently, the10-year “breakeven” inflation implied by indexed Treasury bonds is about 2.35% (but it is closer to 3% at short durations). That means unindexed Treasury bonds yielding 4.4% offer an expected real yield just above 2%. Accounting for expected inflation often narrows the gap between U.S. interest rates and foreign rates, but not always.

Switzerland: The Swiss National Bank maintains a policy rate of 0%; the rate on 10-year Swiss government bonds has been in the 0.5 – 0.7% range. Why can’t we have Swiss-like interest rates in the U.S.? Is it merely intransigence on the part of the Fed, as Trump would have us believe?

No. Inflation in Switzerland is near zero, so in terms of real yields, the gap between U.S. and Swiss rates is closer to 1.4%, rather than 3.8%. But what of the remaining difference? Swiss government debt, even more than U.S. Treasury debt, attracts investors due to the nation’s “safe-haven” status. Also, U.S. yields are elevated by our ballooning federal debt and uncertainties related to trade policy. Economic growth is also somewhat stronger in the U.S., which tends to elevate yields.

These factors give the Fed reason to be cautious about cutting its target rate. It needs evidence that inflation will continue to trend down, and that policy uncertainties can be resolved without reigniting inflation.

Euro Area: The European Central Bank’s (ECB) refinancing rate is now 2.15%. Meanwhile, the 10-year German Bund is yielding around 2.6%, so both short-term and long-term rates in the Euro area are lower than in the U.S. In this case, the difference relative to U.S. rates is not large, nor is it likely attributable to lower expected inflation. Instead, sluggish growth in the EU helps explain the gap. Federal deficits and the ongoing issuance of new Treasury debt also keep U.S. yields higher. Treasury yields may also reflect a premium for volatility due to heavier reliance on foreign investors and private funds, who tend to be price sensitive.

Japan: The Bank of Japan’s (BOJ) policy rate is currently 0.5%. Yields on Japanese 10-year government bonds have recently traded just below 1.5%. Expected inflation in Japan has been around 2.5% this year, which means that real yields are sharply negative. The BOJ has tightened policy to bring inflation down. The nearly 3% gap between U.S. and Japanese bond yields reflects very weak economic growth in Japan. In addition, despite a very high debt to GDP ratio, the depressed value of the yen discourages investment abroad, helping to sustain heavy domestic holdings of government debt.

Blame and Backfire

Trump might well understand the limits of the Fed’s control over interest rates, but if he does, then this is exclusively a case of scapegoating. Cross-country differences in interest rates represent equilibria that balance an array of complex conditions. These range from disparate rates of inflation, the strength of economic growth, currency values, fiscal imbalances, and the character of the investor base. .

Investor expectations obviously play a huge role in all this. A central bank like the Fed cannot dictate long-term yields, and it can do much more harm than good by attempting to push the market where it does not want to go. That type of aggressiveness can spark changes in expectations that undermine policy objectives. It’s childish and destructive to insist that interest rates can and should be as low in the U.S. as in countries facing much different circumstances.

Seemingly everyone wants to know: where is this tariff inflation you economists speak of? Even my pool guy asked me! We haven’t seen it yet, despite the substantial tariffs imposed by the Trump Administration. The press has been wondering about this for almost two months, and some of the MAGA faithful are celebrating the resounding success of the tariffs in this and other respects. Not so fast, grasshoppers!

There are a couple of aspects to the question of tariff inflation. One has to do with the meaning of inflation itself. Strictly speaking, inflation is a continuing positive rate of increase in the price level. Certain purists say it is a continuous positive rate of increase in the money supply, which I grant is least a step beyond what most people understand as inflation. Rising prices over any duration is a good enough definition for now, but I’ll return to this question below in the context of tariffs.

There is near-unanimity among economists that higher tariffs will increase the prices of imports, import-competing goods, and goods requiring imported materials as inputs. Domestic importers pay the tariffs, so they face pressure on their profit margins unless they can pass the cost onto their customers. But so far, since Donald Trump made his “Liberation Day” tariff announcement, we’ve seen very little price pressure. What explains this stability, and will it last?

Several factors have limited the price response to tariffs thus far:

— Some importers are “eating” the tariffs themselves, at least for now, and they might continue to pay a share of the tariffs with smaller margins.

“… cargo loaded onto ships in Asia on April 4 was not subject to the reciprocal tariffs, while cargo loaded April 5 was. Cargo coming from Asia can take up to 45 days to make it to U.S. ports and then must be transported to distribution centers and then on to customers. It is possible that goods from Asia subjected to high tariffs are only now making their way to customers. These two factors suggest the economic effects of increased tariffs could merely be delayed.“

— Data on prices is reported with a lag. We won’t know the June CPI and PPI until July 15, and the PCE price index (and its core measure, of most importance to the Fed) won’t be reported until July 31, and will be subject to revisions in subsequent months.

— Importers stocked up on inventories before tariffs took effect, and even before Trump took office. Once these are depleted, new supplies will carry a higher cost. That’s likely over the next few months.

— Uncertainty about the magnitude of the new tariffs. Trump has zig-zagged a number of times on the tariff rates he’ll impose on various countries, and real trade agreements have been slow in coming. This makes planning difficult. Nevertheless, inventories are likely to carry a higher replacement cost, but adjusting price creates a danger of putting oneself at a competitive disadvantage and alienating customers. Many businesses would prefer to wait for a clearer read on the situation before committing to a substantial price hike.

— Tariff exemptions have reduced the average tariffs assessed thus far to about 10%, well below the 15% official average. This will reduce the impact on prices and margins, but it is still a huge increase in tariffs and another source of uncertainty that should give importers pause in any effort to recoup tariffs by repricing.

— Importers are storing goods in “bonded warehouse“ to delay the payment of tariffs. This helps importers buy time before committing to pricing decisions.

— Kashkari notes that businesses can find ways to alter trade routes so as to lower the tariffs they pay. For example, he says some goods are being routed to take advantage of the relatively favorable terms of the free trade agreement between the U.S., Mexico, and Canada.

So it’s still too early to have seen much evidence of price pressure from Trump’s tariffs. However, that pressure is likely to become more obvious over the summer months. The expectation that tariffs should have already shown up in prices is just one of several errors of those critical of the Federal Reserve’s patience in easing policy.

Is there a sound reason to expect higher tariffs to produce a continuing inflation? Or instead, should we expect a “one-time” increase in the price level without further complications? Tariffs could generate an ongoing inflation if accompanied by an increase in the rate of money growth, or at least enough money growth to create expectations of higher inflation. Thus, if the Federal Reserve seeks to “accommodate” tariffs by easing monetary policy, that might lead to more widespread inflation. That could be difficult to rein-in, to the extent that higher inflation gets embedded into expectations.

Tariffs are excise taxes, and while they put upward pressure on the prices of imports and import-competing goods, they may have a contractionary effect on economic activity. Tighter budgets might lead to softer prices in other sectors of the economy and moderate the impact of tariffs on the overall price level.

The Fed’s reluctance to ease policy has been reinforced by another development. It’s usually argued that tariffs will strengthen the domestic currency due to the induced reduction in demand for foreign goods (and thus the need for foreign currency). Instead, the dollar has declined more than 9% against the Euro since “Liberation Day”, and the overall U.S. dollar index experienced its steepest first-half decline in 50 years. A lower dollar stimulates exports and depresses imports, but it also can lead to “imported” inflation (in this case, apart from the direct impact of tariffs). Uncertainty regarding tariffs deserves some of the blame for the dollar sell-off, but the fiscal outlook and rising debt levels have also done their part.

The upshot is that Trump’s tariffs are likely to cause a one-time increase in the price level with possibly a mild contractionary effect on the real economy. So it’s a somewhat stagflationary effect. It won’t be disastrous, but the tariffs can be made more inflationary than they “need be”. That’s why Trump is foolish to persist in haranguing the Fed for not rushing to ease policy.

President Trump engaged in one of his favorite pastimes on June 18 while the Federal Reserve Open Market Committee (FOMC) was concluding its meeting on the direction of monetary policy. He publicly called Fed Chairman Jerome Powell “stupid” for not having cut rates already, and later said the Fed’s board was “complicit”.

“”I don’t know why the Board doesn’t override this Total and Complete Moron!“

Trump also tagged Powell with one of his trademark appellations: “Too Late”. Yep, that’s how Trump says he refers to Powell.

Later that day, the Fed once again announced that it had decided to leave unchanged its target range for the interest rate on federal funds. Powell described the overall tenor of current Fed policy as mildly restrictive, but FOMC members still “expect” (loosely speaking) two quarter-point cuts in the funds rate by year end.

Of course, Powell and the FOMC really were far too late in recognizing that inflation was more than transitory in 2021-22. Now, with inflation measures tapering but still higher than the Fed’s 2% target, Trump says “Too Late” Powell and the Fed are again behind the curve. Of course, because the central bank is outside the President’s direct control, it makes a convenient scapegoat for whatever might ail the Trump economy, and Trump frets that unnecessarily high rates will cost the U.S. Treasury hundreds of billions in interest on new and refinanced federal debt.

The President has no appreciation for the value of an independent central bank, as opposed to one captive to the fiscal whims of Presidents and Congress. Despite his frequent criticism of inflationary sins of the past, Trump doesn’t understand the dangers of a central bank that could be bullied into inflating away government debt.

The day after the Fed’s meeting, Trump said rates should be cut immediately by a huge 2.5%! As the Donald might say, no one’s ever seen anything like it!

Trump, however, is delusional to think the Fed can engineer reductions in the spectrum of interest rates by aggressively slashing its fed funds target. The Fed does not control long-term interest rates, nor is that part of the Fed’s formal mandate. In fact, an aggressively large reduction in the fed funds rate is likely to backfire, feeding expectations of higher inflation and a selloff in credit markets.

Let me reiterate: the Fed does not control long-term interest rates. Short-term rates are more heavily influenced by the Fed’s rate actions, and by expectations of Fed policy, but the Fed is likewise influenced by those very expectations. In fact, the Fed often follows market rates rather than leading them. In any case, a general truth is that long-term interest rates go where market forces direct them, not where the Fed might try to push them.

Today the Fed is attempting to walk a line between precipitating divergent and potentially negative outcomes. It wants to see clear evidence that inflation is settling down at roughly the 2% target. Also, the Fed is wary that Trump’s tariffs might generate a near-term spike in prices. Under those circumstances, prematurely easing policy could rekindle more permanent inflationary pressures. It seems clear that the Fed currently judges inflation as the dominant risk.

At the same time, the real economy shows mixed signals. Clear signs of a downturn would likely prompt the Fed to cut its fed funds target sooner. After the latest meeting, the Fed announced that it had reduced its own forecast for real GDP growth in 2025 to just 1.4%. Recent employment gains have been moderate, but jobless claims are trending up. The unemployment rate is low, but the labor force has declined over the past few months, which incidentally might be putting upward pressure on wages.

Policy uncertainty was a major theme in the Fed’s June rate decision. Tariffs loom large and would be a threat to continued growth if producers, facing weak demand, were unable to pass the cost of tariffs through to customers, undermining their profit margins. Prospects for passage of the budget reconciliation bill create more uncertainty, providing another rationale to stand pat without cutting the funds rate.

Again, Jerome Powell says that Fed policy is “modestly restrictive” at present. In fact, estimates of the “policy neutral” Fed funds rate are in the vicinity of 2.75%, well below the current target range of 4.25-4.50. However, the money supply (M2) has drifted up over the past year and by May was up 4.4% from a year earlier. That would be consistent with 2% inflation and better than 2% real growth, the latter being higher than the FOMC’s expectation.

Another consideration is that the Fed has nearly ended its quantitative tightening (QT) program, having recently trimmed the passive runoff of maturing securities in its portfolio to just $5 billion per month. This leads to less downward pressure on bank reserves and less upward pressure on the fed funds rate. In other words, policy has already shifted toward greater support for money growth. But out of caution, the Fed wants to defer reductions in the funds rate to avoid undermining the central bank’s inflation-fighting credibility.

Jerome Powell and the FOMC probably could not care less about Trump’s exhortations to reduce interest rates. For one thing, it is beyond the Fed’s power to force down rates that could spur housing and other economic activity. And Trump should be grateful: such a reckless attempt would risk great harm to markets and the economy, not to mention Trump’s economic agenda. Better to wait until near-term inflation risks and policy uncertainty clear up.

Trump can jawbone as aggressively as he wants. He cannot fire Powell, though he keeps saying he “should”. However, no matter what actions the Fed takes, he will almost certainly not reappoint Powell to lead the Fed when Powell’s term expires next May. Sadly, Trump will try to appoint a replacement he can rely upon to do his bidding. Let’s hope the Senate stands in his way to preserve Fed independence.

Wow! We’re less than a week from Election Day! I’d hoped to write a few more detailed posts about the platforms and policies of Kamala Harris and Donald Trump, but I was waylaid by Hurricane Milton. It sent us scrambling into prep mode, then we evacuated to the Florida Panhandle. The drive there and back took much longer than expected due to the mass exodus. On our return we found the house was fine, but there was significant damage to an exterior structure and a mess in the yard. We also had to “de-prep” the house, and we’ve been dealing with contractors ever since. It was an exhausting episode, but we feel like we were very lucky.

Now, with less than a week left till the election, I’ll limit myself to a summary of the positions of the candidates in a number of areas, mostly but not all directly related to policy. I assign “grades” in each area and calculate an equally-weighted “GPA” for each candidate. My summaries (and “grades”) are pretty off-the-cuff and not adequate treatments on their own. Some of these areas are more general than others, and I readily admit that a GPA taken from my grade assignments is subject to a bit of double counting. Oh well!

Role of Government: Kamala Harris is a statist through and through. No mystery there. Trump is more selective in his statist tendencies. He’ll often favor government action if it’s politically advantageous. However, in general I think he is amenable to a smaller role for the public than the private sector. Harris: F; Trump: C

Regulation: There is no question that Trump stands for badly needed federal regulatory reform. This spans a wide range of areas, and it extends to a light approach to crypto and AI regulation. Trump plans to appoint Elon Musk as his “Secretary of Cost Cutting”. Harris, on the other hand, seems to favor a continuation of the Biden Administration’s heavy regulatory oversight. This encourages a bloated federal bureaucracy, inflicts high compliance costs on the private sector, stifles innovation, and tends to concentrate industrial power. Harris: F; Trump: A

Border Policy: Trump wants to close the borders (complete the wall) and deport illegal immigrants. Both are easier said than done. Except for criminal elements, the latter will be especially controversial. I’d feel better about Trump’s position if it were accompanied by a commitment to expanded legal immigration. We need more legal immigrants, especially the highly skilled. For her part, Harris would offer mass amnesty to illegals. She’d continue an open border policy, though she claims to want certain limits on illegal border crossings going forward. She also claims to favor more funds for border control. However, it is not clear how well this would translate into thorough vetting of illegal entrants, drug interdiction at the border, or sex trafficking. Harris: D; Trump: B-

Antitrust: Accusations of price gouging by American businesses? Harris! Forty three corporations in the S&P 500 under investigation by the DOJ? The Biden-Harris Administration. This reflects an aggressively hostile and manipulative attitude toward the business community. Trump, meanwhile, might wheedle corporations to act on behalf of certain of his agendas, but he is unlikely to take such a broadly punitive approach. Harris: F; Trump: B-

Foreign Policy: Harris is likely to continue the Biden Administration’s conciliatory approach to dealing with America’s adversaries. The other side of that coin is an often tepid commitment to longtime allies like Israel. Trump believes that dealing from a position of strength is imperative, and he’s willing to challenge enemies with an array of economic and political sticks and carrots. He had success during his first term in office promoting peace in the Middle East. A renewed version of the Abraham Accords that strengthened economic ties across the region would do just that. Ideally, he would like to restore the strength of America’s military, about which Harris has less interest. Trump has also shown a willingness to challenge our NATO partners in order to get them to “pay their fair share” toward the alliance’s shared defense. My major qualification here has to do with the candidates’ positions with respect to supporting Ukraine in its war against Putin’s mad aggression. Harris seems more likely than Trump to continue America’s support for Ukraine. Harris: D+; Trump: B-

Trade: Nations who trade with one another tend to be more prosperous and at peace. Unfortunately, neither candidate has much recognition of these facts. Harris is willing to extend the tariffs enforced during the Biden Administration. Trump, however, is under the delusion that tariffs can solve almost anything that ails the country. Of course, tariffs are a destructive tax on American consumers and businesses. Part of this owes to the direct effects of the tax. Part owes to the pricing power tariffs grant to domestic producers. Tariffs harm incentives for efficiency and the competitiveness of American industry. Retaliatory action by foreign governments is a likely response, which magnifies the harm.

To be fair, Trump believes he can use tariffs as a negotiating tool in nearly all international matters, whether economic, political, or military. This might work to achieve some objectives, but at the cost of damaging relations more broadly and undermining the U.S. economy. Trump is an advocate for not just selective, punitive tariffs, but for broad application of tariffs. Someone needs to disabuse him of the notion that tariffs have great revenue-raising potential. They don’t. And Trump is seemingly unaware of another basic fact: the trade deficit is mirrored by foreign investment in the U.S. economy, which spurs domestic economic growth. Quashing imports via tariffs will also quash that source of growth. I’ll add one other qualification below in the section on taxes, but I’m not sure it has a meaningful chance.

Harris: C-; Trump: F

Inflation: This is a tough one to grade. The President has no direct control over inflation. Harris wants to challenge “price gougers”, which has little to do with actual inflation. I expect both candidates to tolerate large deficits in order to fulfill campaign promises and other objectives. That will put pressure on credit markets and is likely to be inflationary if bond investors are surprised by the higher trajectory of permanent government indebtedness, or if the Federal Reserve monetizes increasing amounts of federal debt. Deficits are likely to be larger under Trump than Harris due in large part to differences in their tax plans, but I’m skeptical that Harris will hold spending in check. Trump’s policies are more growth oriented, and these along with his energy policies and deregulatory actions could limit the inflationary consequences of his spending and tax policies. Higher tariffs will not be of much help in funding larger deficits, and in fact they will be inflationary. Harris: C; Trump: C

Federal Reserve Independence: Harris would undoubtedly like to have the Fed partner closely with the Treasury in funding federal spending. Her appointments to the Board would almost certainly lead to a more activist Fed with a willingness to tolerate rapid monetary expansion and inflation. Trump might be even worse. He has signaled disdain for the Fed’s independence, and he would be happy to lean on the Fed to ease his efforts to fulfill promises to special interests. Harris: D; Trump: F

Entitlement Reform: Social Security and Medicare are both insolvent and benefits will be cut in 2035 without reforms. Harris would certainly be willing to tax the benefits of higher-income retirees more heavily, and she would likely be willing to impose FICA and Medicare taxes on incomes above current earning limits. These are not my favorite reform proposals. Trump has been silent on the issue except to promise no cuts in benefits. Harris: C-; Trump: F

Health Care: Harris is an Obamacare supporter and an advocate of expanded Medicaid. She favors policies that would short-circuit consumer discipline for health care spending and hasten the depletion of the already insolvent Medicare and Medicaid trust funds. These include a $2,000 cap on health care spending for Americans on Medicare, having Medicare cover in-home care, and extending tax credits for health insurance premia. She supports funding to address presumed health care disparities faced by black men. She also promises efforts to discipline or supplant pharmacy benefit managers. Trump, for his part, has said little about his plans for health care policy. He is not a fan of Obamacare and he has promised to take on Big Pharma, whatever that might mean. I fear that both candidates would happily place additional controls of the pricing of pharmaceuticals, a sure prescription for curtailed research and development and higher mortality. Harris: F; Trump: D+

Abortion: The Supreme Court’s 2022 decision in Dobbs v. Jackson essentially relegated abortion law to individual states. That’s consistent with federalist principles, leaving the controversial balancing of abortion vs. the unborn child’s rights up to state voters. Geographic differences of opinion on this question are dramatic, and Dobbs respects those differences. Trump is content with it. Meanwhile, Harris advocates for the establishment of expanded abortion rights at the federal level, including authorization of third trimester abortions by “care providers”. And Harris does not believe there should be religious exemptions for providers who do not wish to offer abortion services. No doubt she also approves of federally funded abortions. Harris: F; Trump: A

Housing: The nation faces an acute housing shortage owing to excessive regulation that limits construction of new or revitalized housing. These excessive rules are primarily imposed at the state and local level. While the federal government has little direct control over many of these decisions, it has abetted this regulatory onslaught in a variety of ways, especially in the environmental arena. Harris is offering stimulus to the demand side through a $25,000 housing tax credit for first-time home buyers. This will succeed in raising the cost of housing. She has also called for heavier subsidies for developers of low-income housing. If past is prologue, this might do more to line the pockets of developers than add meaningfully to the stock of affordable housing. Harris also favors rent controls, a sure prescription for deterioration in the housing stock, and she would prohibit software allowing landlords to determine competitive neighborhood rents. Trump has called for deregulation generally and would not favor rent controls. Harris: F; Trump B

Taxes: Harris has broached several wildly destructive tax proposals. Perhaps the worst of these is to tax unrealized capital gains, and while she promises it would apply only to extremely wealthy taxpayers, it would constitute a wealth tax. Once that line is crossed, the threat of widening the base becomes a very slippery slope. It would also be a strong detriment to domestic capital investment and economic growth. Harris would increase the top marginal personal tax rate and the corporate tax rate, which would discourage investment and undermine real wage growth. She’d also increase estate tax rates. As discussed above, she unwisely calls for a $25,000 tax credit for first-time homebuyers. She also wants to expand the child care tax credit to $6,000 for families with newborns. A proposed $50,000 small business tax credit would allow the federal government to subsidize and encourage risky entrepreneurial activity at taxpayers’ expense. I’m all for small business, but this style of industrial planning is bonkers. She would sunset the Trump (TCJA) tax cuts in 2026.

Finally, Harris has mimicked Trump in calling for no taxes on tips. Treating certain forms of income more favorably than others is a recipe for distortions in economic activity. Employers of tip-earning workers will find ways to shift employees’ income to tips that are mandatory for patrons. It will also skew labor supply decisions toward occupations that would otherwise have less economic value. But Trump managed to find an idea so politically seductive that Harris couldn’t resist.

Trump’s tax plans are a mixed bag of good and bad ideas. They include extending his earlier tax cuts (TCJA) and restoring the SALT deduction. The latter is an alluring campaign tidbit for voters in high-tax states. He would reduce the corporate tax rate, which I strongly favor. Corporate income is double-taxed, which is a detriment to growth as well as a weight on real wages. He would eliminate taxes on overtime income, another example of favoring a particular form of income over others. Wage earners would gain at the expense of salaried employees, so one could expect a transition in the form employees are paid over time. Otherwise, the classification of hours as “overtime” would have to be standardized. One could expect existing employees to work longer hours, but at the expense of new jobs. Finally, Trump says Social Security benefits should not be taxed, another kind of special treatment by form of income. This might encourage early retirement and become an additional drain on the Social Security Trust Fund.

The higher tariffs promised by Trump would collect some revenue. I’d be more supportive of this plank if the tariffs were part of a larger transition from income taxes to consumption taxes. However, Trump would still like to see large differentials between tariffs and taxes imposed on the consumption of domestically-produced goods and services.

Harris: F; Trump C+

Climate Policy: This topic has undergone a steep decline in relative importance to voters. Harris favors more drastic climate interventions than Trump, including steep renewable subsidies, EV mandates, and a panoply of other initiatives, many of which would carry over from the Biden Administration. Harris: F; Trump: B

Energy: Low-cost energy encourages economic growth. Just ask the Germans! Consistent with the climate change narrative, Harris wishes to discourage the use of fossil fuels, their domestic production, and even their export. She has been very dodgy with respect to restrictions on fracking. Her apparent stance on energy policy would be an obvious detriment to growth and price stability (or I should say a continuing detriment). Trump wishes to encourage fossil fuel production. Harris: F; Trump: A

Constitutional Integrity: Harris has supported the idea of packing the Supreme Court, which would lead to an escalating competition to appoint more and more justices with every shift in political power. She’s also disparaged the Electoral College, without which many states would never have agreed to join the Union. Under the questionable pretense of “protecting voting rights”, she has opposed steps to improve election integrity, such voter ID laws. And operatives within her party have done everything possible to register non-citizens as voters. Harris: F; Trump: A

First Amendment Rights: Harris has called for regulation and oversight of social media content and moderation. A more descriptive word for this is censorship. Trump is generally a free speech advocate. Harris: F; Trump A-

Second Amendment Rights: Harris would like to ban so-called “assault weapons” and high-capacity magazines, and she backs universal background checks for gun purchases. Trump has not called for any new restrictions on gun rights. Harris: F; Trump: A

DEI: Harris is strongly supportive of diversity and equity initiatives, which have undermined social cohesion and the economy. That necessarily makes her an enemy of merit-based rewards. Trump has no such confusion. Harris: F; Trump: A

Hysteria: The Harris campaign has embraced a strategy of demonizing Donald Trump. Of course, that’s not a new approach among Democrats, who have fabricated bizarre stories about Trump escapades in Russia, Trump as a pawn of Vladimir Putin, and Russian manipulation of the 2016 Trump campaign. Congressional democrats spent nearly all of Trump’s first term in office trying to find grounds for impeachment. Concurrently, there were a number of other crazy and false stories about Trump. The current variation on “Orange Man Bad” is that Trump is a fascist and a Nazi, and that all of his supporters are Nazis. And that Trump will use the military against his domestic political opponents, the so-called “enemy within”. And that Trump will send half the country’s populace to labor camps. The nonsense never ends, but could anything more powerfully ignite the passions of violent extremists than this sort of hateful rhetoric? Would it not be surprising if at least a few leftists weren’t interested in assassinating “Hitler” himself. This is hysteria, and one has to wonder if that is not, in fact, the intent.

Can any of these people actually define the term fascist? Most fundamentally, a fascist desires the use of government coercion for private gain (of wealth or power) for oneself and/or one’s circle of allies. By that definition, we could probably categorize a great many American politicians as fascists, including Barack Obama, Joe Biden, Donald Trump, and a majority of both houses of Congress. That only demonstrates that corporatism is fundamental to fascist politics. Less-informed definitions of fascism conflate it with everything from racism (certainly can play a part) and homophobia (certainly can play a part) to mere capitalism. But take a look at the demographics of Trump’s supporters and you can see that most of these definitions are inapt.

Is the Trump campaign suffering from any form of hysteria? It’s shown great talent at poking fun at the left. Of course, Trump’s reactions to illegal immigration, crime, and third-trimester abortions are construed by leftists to be hysterical. I mean, why would anyone get upset about those kinds of things?

Harris: F; Trump: A

“Grade Point Average”

I’m sure I forgot an area or two I should have covered. Anyway, the following are four-point “GPAs” calculated over 20 categories. I’m deducting a quarter point for a “minus” grade and adding a quarter point for a “plus” grade. Here’s what I get:

Economic ignorance and campaign politics seem to go hand-in-hand, especially when it comes to the rhetoric of avowed interventionists. They love “easy” answers. If they get their way, negative but predictable consequences are always “unintended” and/or someone else’s fault. Unfortunately, too many journalists and voters like “easy” answers, and they repeatedly fall for the ploy.

This post highlights one of many bad ideas coming out of the Kamala Harris campaign. I probably won’t have time to cover all of her bad ideas before the election. There are just too many! I hope to highlight a few from the Trump campaign as well. Unfortunately, the two candidates have more than one bad idea in common.

Price Gouging

Here I’ll focus on Harris’ destructive proposal for a federal ban on “price gouging”. Unfortunately, she has yet to define precisely what she means by that term. On its face, she’d apparently support legislation authorizing the DOJ to go after grocers, gas stations, or other sellers in visible industries charging prices deemed excessive by the federal bureaucracy. This is a form of price control and well in keeping with the interventionist mindset.

As Michael Munger has said, when you charge “too much” you are “gouging”; when you charge “too little” you are “predatory”; and when you charge the same price as competitors you’ve engaged in a price fixing conspiracy. The fact that Harris’ proposal is deliberately vague is an even more dangerous invitation to arbitrary caprice by federal enforcers. It might be hard to price a ham sandwich without breaking such a law.

The great advantage of the price system is its impersonal coordination of the actions of disparate agents, creating incentives for both buyers and sellers to direct resources toward their most valued uses. Price controls of any kind short circuit that coordination, inevitably leading to shortages (or surpluses), misallocations, and diminished well being.

Inflation As Aggregate Macro Gouging

Aside from vote buying, Harris has broader objectives than the usual “anti-gouging” sentiment that accompanies negative supply shocks. She’s faced mounting pressure to address prices that have soared during the Biden Administration. The inflation during and after the COVID pandemic was induced by supply shortfalls first and then a spending/money-printing binge by the federal government. The pandemic induced shortages in some key areas, but the Treasury and the Fed together engineered a gigantic cash dump to accommodate that shock. This stimulated demand and turned temporary dislocations into permanently higher prices.

There were howls from the Left that greed in the private sector was to blame, despite plentiful evidence to the contrary. Blaming “price gouging” for inflated prices dovetails with Harris’ proclivity to inveigh against “corporate greed”. It’s typical leftist blather intended to appeal to anyone harboring suspicions of private property and the profit motive.

The profit motive is a compelling force for social good, motivating the performance of large corporations and small businesses alike. Diatribes against “greed” coming from the likes of a career politician with no private sector experience are not only unconvincing. They reveal childlike misapprehensions regarding economic phenomena.

More substantively, some have noted that mark-ups rose during and after the pandemic, but these markups are explained by normal cyclical fluctuations and the growing dominance of services in the spending mix. High margins are difficult to sustain without persistently high levels of demand. The Fed’s shift toward monetary restraint has dissipated much of that excessive demand pressure, but certainly not enough to bring prices back to pre-pandemic levels, which would require a severe economic contraction.

Claims that concentration among sellers has risen in some markets are also cited as evidence that greedy, price-gouging corporations are fueling inflation. If that is a real concern, then we might expect Harris to lean more heavily on antitrust policy. She should be circumspect in that regard: antitrust enforcement is too often used for terrible reasons (and also see here). In any case, rising market concentration does not necessarily imply a reduction in competitive pressures. Indeed, it might reflect the successful efforts of a strong competitor to please customers, delivering better value via quality and price. Moreover, mergers and acquisitions often result in stronger challenges to dominant players, energizing innovation, improved quality, and price competition.

If Harris is serious about minimizing inflation she should advocate for fiscal and monetary restraint. We’ve heard nothing of that from her campaign, however. No credible plans other than vaguely-defined price controls and promises to tax and spend our way to a joyful “opportunity economy”.

Disaster Supply Gouging

There is already a federal law against hoarding “scarce items” in times of war or national crisis and reselling at more than the (undefined) “prevailing market price”. There are also laws in 34 states with varying “anti-gouging” provisions, mostly applicable during emergencies only. These laws are counterproductive as they tend to “gouge” the flow of supplies.

In the aftermath of terrible storms or earthquakes, there are almost always shortages of critical goods like food, water, and fuel, not to mention specialized manpower, machinery, and materials needed for cleanup and restoration. As I pointed out some time ago, retailers often fail to adjust their prices under these circumstances, even as shelves are rapidly emptied. They are sometimes prohibited from repricing aggressively. If not, they are conflicted by the predictable hoarding that empties shelves, the higher costs of replenishing inventory, and the knowledge that price rationing creates undeservedly bad public relations. So retailers typically act with restraint to avoid any hint of “gouging” during crises.

Disasters often disrupt production and create physical barriers that hinder the very movement of goods. When prices are flexible and can respond to scarcity on the ground, suppliers can be very creative in finding ways to deliver badly needed supplies, despite the high costs those are likely to entail. Private sellers can do all this more nimbly and with greater efficiency than government, but they need price incentives to cover the costs and various risks. Price controls prevent that from happening, prolonging shortages at the worst possible time.

The chief complaint of those who oppose this natural corrective mechanism is that higher prices are “unfair”. And it is true that some cannot afford to pay higher prices induced by severe scarcity. The answer here is that government can write checks or even distribute cash, much as the government did nationwide during the pandemic. That’s about the only thing at which the state excels. Then people can afford to pay prices that reflect true levels of scarcity. If done selectively and confined to a regional level, the broader inflationary consequences are easily neutralized.

Instead, the knee-jerk reaction is to short-circuit the price mechanism and insist that available supplies be rationed equally. That might be a fine way for retailers to respond in the short run. Share the misery and prevent hoarding. But supplies will run low. When the shelves are empty, the price is infinite! That’s why sellers must have flexibility, not prohibitions.

Blame Game

Harris is engaged in a facile blame game at both the macro and micro level. She claims that inflation could be controlled if only corporations weren’t so greedy. Forget that they must cover their own rising costs, including the costs of compensating risk-averse investors. For that matter, she probably hasn’t gathered that a return to capital is a legitimate cost. Like many others, Harris seems ignorant of the elevated costs of bringing goods to market following either unpredictable disasters or during a general inflation. She also lacks any understanding of the benefits of relying on unfettered markets to bridge short-term gaps in supply. But none of this is surprising. She follows in a long tradition of ignorant interventionism. Let’s hope we have enough voters who aren’t that gullible.

When Federal Reserve Chairman Jerome Powell said “higher for longer” last year, it wasn’t about the Grateful Dead concerts he’s attended over the years. No, he meant the Fed might need to raise its short-term interest rate target and/or keep it elevated for an extended period to squeeze inflation out of the economy. As late as December, Powell said that additional rate hikes remain on the table. But short of that, the Fed might keep its current target rate steady until inflation is solidly in-line with its 2% objective. The obvious risk is that tight monetary policy might tip the economy into recession. The market, for its part, is pricing in several rate cuts this year.

Thus far, the release of key economic data for December 2023 has not settled the debate as to whether disinflation has truly paused short of the Fed’s goal. There were inauspicious signs from the labor market in December as well. These data releases don’t rule out a “soft landing”, but they indicate that recession risks are still with us in 2024. The Fed will face a dilemma if the economy weakens but inflation fails to abate, either due to residual stickiness or new supply shocks. The latter are unfolding even now with the shut down of Red Sea shipping.

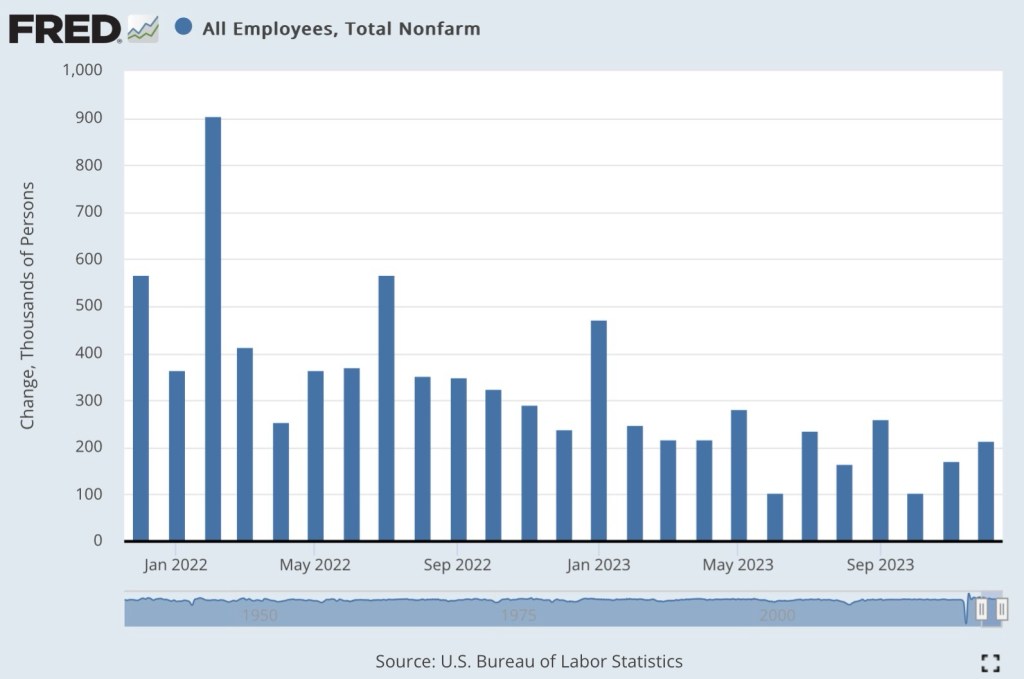

Bad Employment Report

On the surface, the employment report from the Bureau of Labor Statistics (BLS) was strong relative to expectations, and the media reported it on that superficial level: nonfarm payrolls increased by 216,000 jobs, about 45,000 more than expected; unemployment was unchanged from November at 3.7%.

Unfortunately, the report contained several ominous signs:

1) Employment from the BLS Household Survey declined by 683,000 in December and is essentially flat since July. This discrepancy should be rather unsettling to anyone waving off the possibility of a recession.

2) The number of full-time workers decreased by 1.53 million in December, and the number of part-time workers increased by 762,000 as the holidays approached. Retail employment was not particularly strong however, and the big loss of full-time work stands in contrast to the “strong-report” narrative.

3) The number of multiple jobholders hit a record and increased by 556,000 over the past year. This might indicate trouble for some workers making ends meet.

5) The civilian labor force declined by 676,000. What accounts for the change in status among these former workers or job seekers?

6) From the BLS Establishment Survey, government hiring accounted for 24% of the nonfarm jobs filled in December. Social Services accounted for 10% of the new hiring and health care for 18%, both of which are heavily dependent on government.

7) Nonfarm payrolls were revised downward by a total of 71,000 for October and November. We’ve seen downward revisions for 10 of the past 11 months.

8) In total, initial monthly job reports in 2023 overstated the full-year gain in nonfarm employment after available revisions by 439,000.

Those are big qualifiers on the “stronger than expected” jobs report. Furthermore, I tend to discount new government jobs as a real engine of production possibilities, so the report didn’t offer much assurance about the economy’s momentum. In addition, there are estimates that the payroll gain was due to better weather than the seasonal adjustment factors indicate.

Fictional Payroll Gains?

Still other issues cast doubt on the BLS payroll numbers. First, they are based on a survey of employers that is not complete by the time of each month’s initial report. Second, the survey is heavily skewed toward employees of government and large corporations; the sample of small employers is light by comparison. Third, seasonal adjustments often swamp the unadjusted changes in payrolls.

Finally, the BLS uses a statistical model of business births/deaths to adjust the figures. This is intended to correct for a lag in survey coverage as new businesses are formed and others close. The net effect on the payroll estimate can be positive or negative. Unfortunately, it’s difficult for even the BLS to tell how much the birth/death model affects the headline nonfarm jobs figure in any particular month. Therefore, it’s tough to put much faith in the monthly reports, but we watch them anyway.

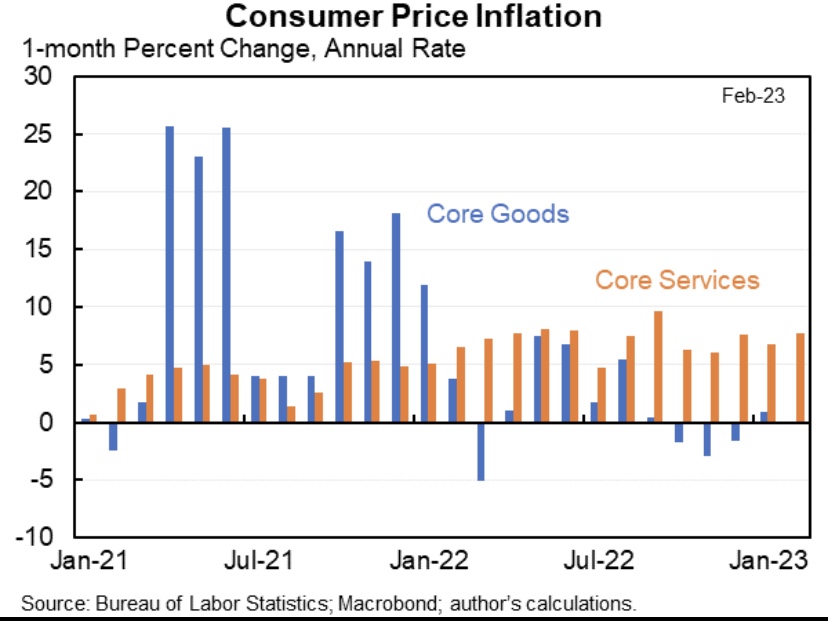

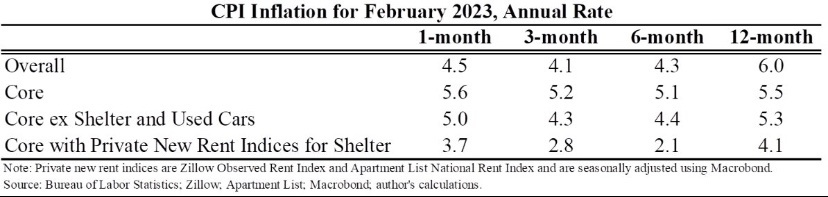

Stubborn Inflation

The Consumer Price Index (CPI) for December increased 0.3% over November and 3.4% year-over-year, slightly more than expectations of 0.2% and 3.2%, respectively. The “core” CPI (excluding food and energy prices) rose 3.9% year-over-year, more than the 3.8% expected. The core rate declined on a one-month and year-over-year basis, however, as did the median item in the CPI.

All CPI measures in the chart declined during 2023, though the core and median lagged the headline CPI (green line), which “flattened” somewhat during the last half of the year. So there appears to be some stickiness hindering disinflation in the CPI at this point, but the apparent “stickiness” has been confined to lagging declines in housing costs (also see here).

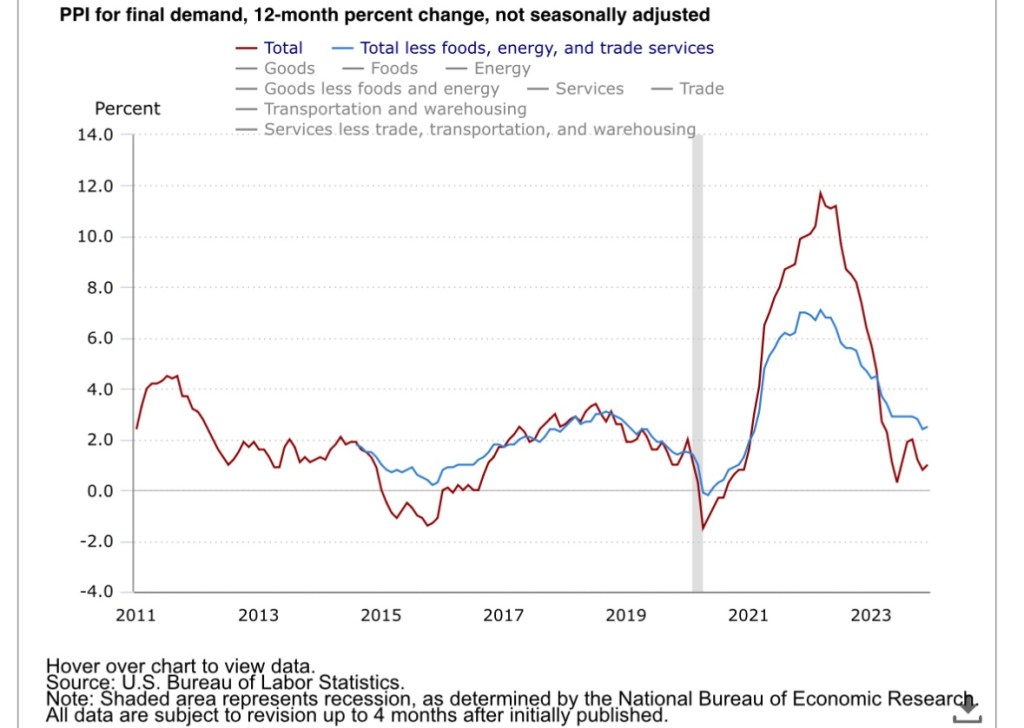

The Producer Price Index (PPI) reported a day later was thought to be benign. Like the CPI, disinflation in the core PPI has tapered:

In this context, it should be noted that declines in the Fed’s preferred inflation gauge, the PCE deflator, have also undergone something of a pause, and the PCE weights housing costs much less heavily than the CPI.

The CPI and PPI reports don’t offer any reason for the Fed to reduce its target federal funds rate over the next couple of Federal Open Market Committee (FOMC) meetings. There are two more sets of monthly inflation reports before the meeting in late March, so things could change. But again, the Fed has given ample guidance that it might have to leave its target rate at the current level for an extended period.

The Market View

Markets had priced-in six cuts in the Fed funds rate target in 2024 prior to the CPI report, but traders began to discount that possibility in its immediate aftermath. However, members of the FOMC expected an average of three cuts in 2024, with more to come in 2025, whether or not that’s consistent with “higher for longer”. Inflation is hovering somewhat above the Fed’s goal, but getting the rest of the job done might be tough, and indeed, might imply “longer” if not “higher”.

But why did the market ever hold the expectation of six cuts this year? Traders must have anticipated an economic contraction, which would kick the Fed into rapid response mode. The employment report offered no assurance that such a “hard landing” will be avoided. A few more negative signals on the real economy without further progress on prices would provide quite a test of the Fed’s inflation-fighting resolve.

The joke’s on me, but my “out” on the question above is “long and variable lags” in the impact of monetary policy, a description that goes back to the work of Milton Friedman. If you call me out on my earlier forebodings of a hard landing or recession, I’ll plead that I repeatedly quoted Friedman on this point as a caveat! That is, the economic impact of a monetary tightening will be lagged by anywhere from 9 to 24 months. So maybe we’re just not there yet.

Of course, maybe I’m wrong and we won’t have to get “there”: the rate of inflation has indeed tapered over the past year. A soft landing now seems like a more realistic possibility. Still, there’s a ways to go, and as Scott Sumner says, when it comes to squeezing inflation out of the system, “It’s the final percentage point that’s the toughest.” One might say the Federal Reserve is hedging its bets, avoiding further increases in its target federal funds rate absent evidence of resurging price pressures.

Strong Growth or Mirage?

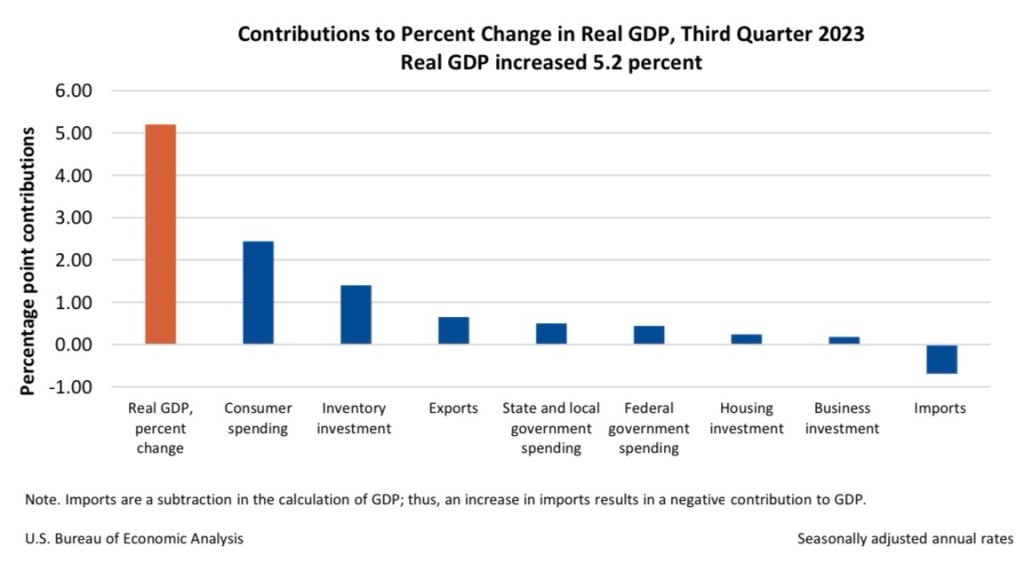

Economic growth is still strong. Real GDP in the third quarter grew at an astonishing 5.2% annual rate. A bulge in inventories accounted for about a quarter of the gain, which might lead to some retrenchment in production plans. Government spending also accounted for roughly a quarter, which corresponds to a literal liability as much as a dubious gain in real output. Unfortunately, fiscal policy is working at cross purposes to the current thrust of monetary policy. Profligate spending and burgeoning budget deficits might artificially prop up the economy for a time, but it adds to risks going forward, not to mention uncertainty surrounding the strength and timing in the effects of tight money.

Consumers accounted for almost half of the third quarter growth despite a slim 0.1% increase in real personal disposable income. That reinforces the argument that consumers are depleting their pandemic savings and becoming more deeply indebted heading into the holidays.

The economy continues to produce jobs at a respectable pace. The November employment report was slightly better than expected, but it was buttressed by the return of striking workers, and retail and manufacturing jobs declined. Still, the unemployment rate fell slightly, so the labor market has remained stronger than expected by most economists.

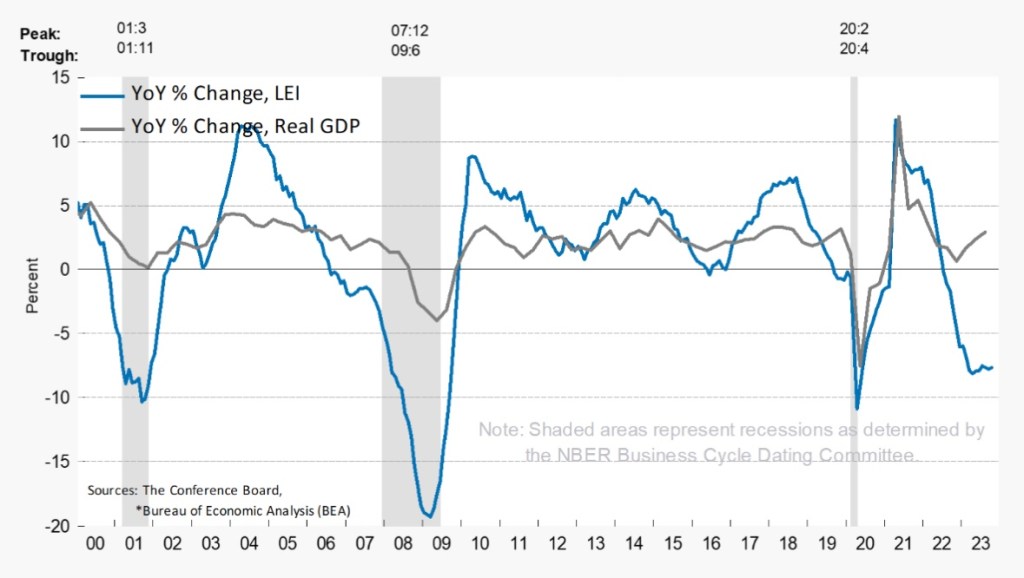

Consumer sentiment had been in the dumps until the University of Michigan report for December, which erased four months of declines. The expectations index is one component of the leading economic indicators, which has been at levels strongly suggesting a recession ahead for well over a year now. See the chart below:

But expectations improved sharply in November, and that included a decline in inflation expectations.

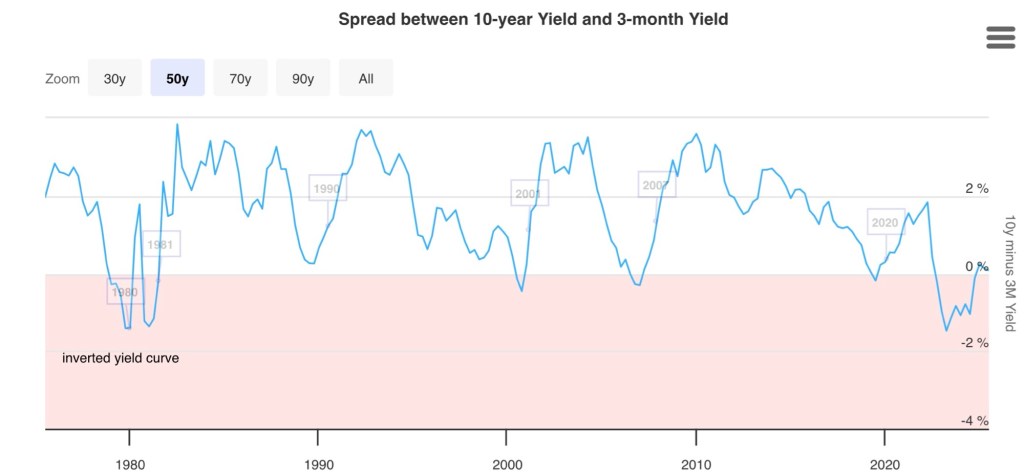

Another component of the LEI is the slope of the yield curve (measured by the difference between the 10-year Treasury bond yield and the federal funds rate). This spread has been a reliable predictor of recessions historically. The 10-year bond yield has declined by over 90 basis points since mid-October, a sign that bond investors think the inflation threat is subsiding. However, that drop steepened the negative slope of the yield curve, meaning that the recession signal has strengthened.

Disinflation, But Still Inflation

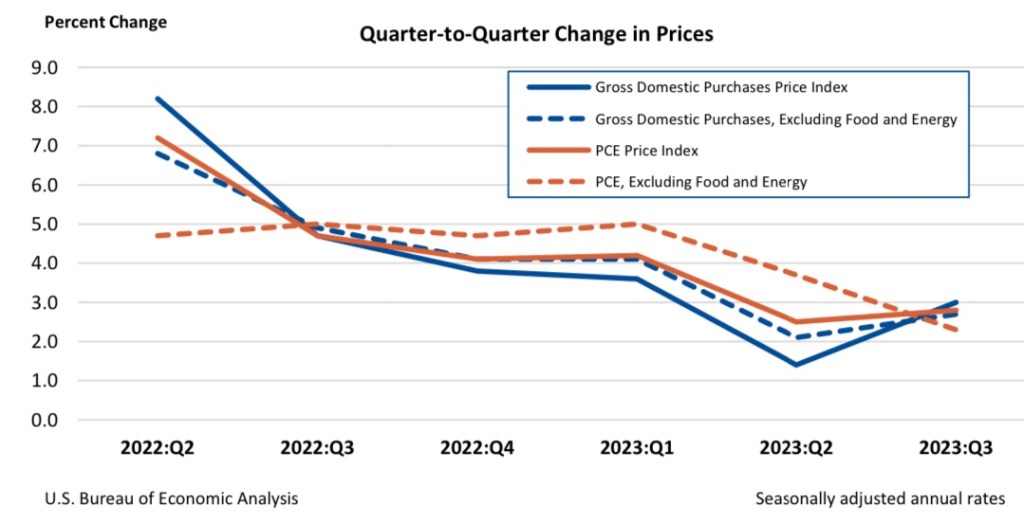

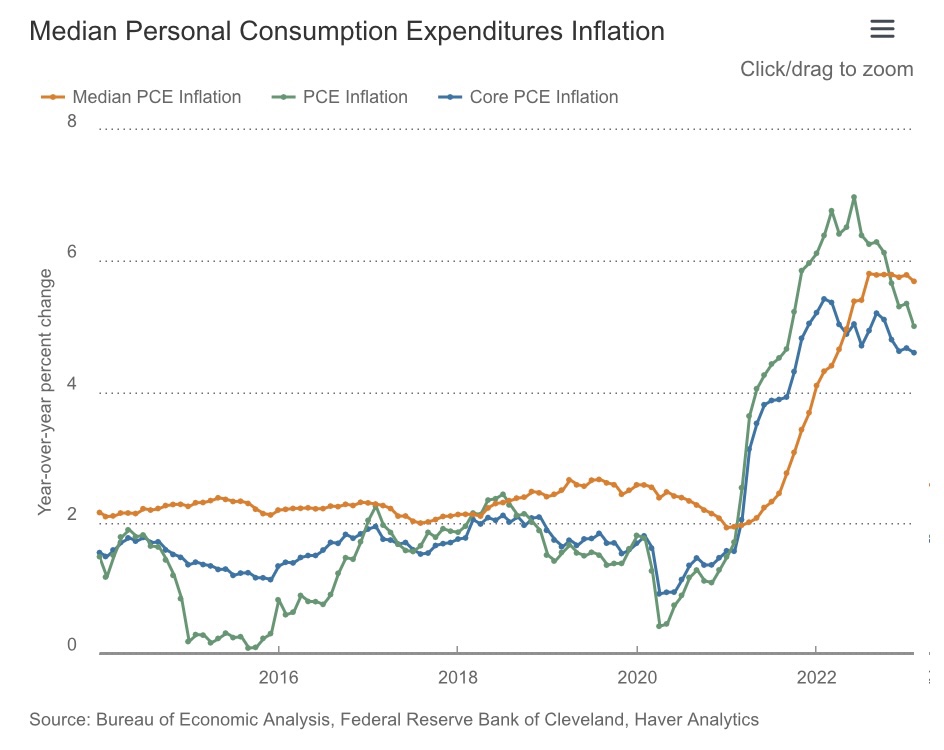

Inflation measures have been slowing, and the Fed’s “target” inflation rate of 2% appears within reach. In the Fed’s view, the most important inflation gauge is the personal consumption expenditures deflator excluding food and energy prices (the “core” PCE). The next chart shows the extent to which it has tapered over the past two quarters. While it’s encouraging that inflation has edged closer to the Fed’s target, it does not mean the inflation fight is over. Still, the decision taken at the December meeting of the Fed’s Open Market Committee (FOMC) to leave its interest rate target unchanged is probably wise.

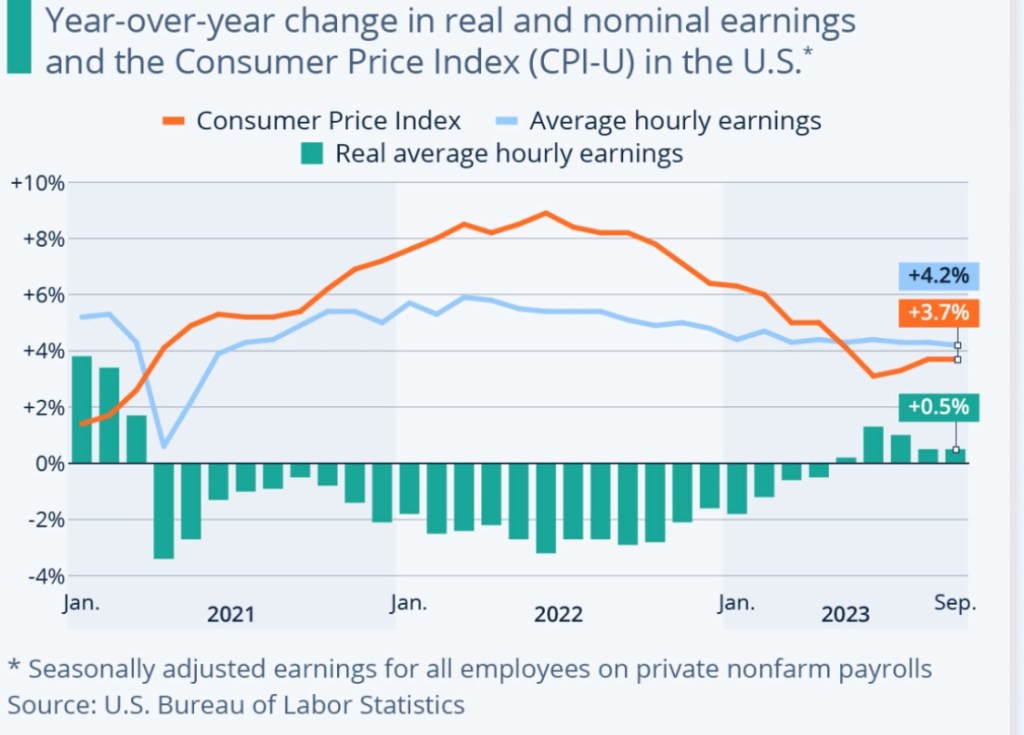

Real wages declined during most of the past three years with the surge in price inflation (see next chart). Some small gains occurred over the past few months, but the earlier declines reinforce the view that consumers need to tighten their belts to maintain savings or avoid excessive debt.

Has Policy Really Been “Tight“?

The prospect of a hard landing presupposes that policy is “tight” and has been tight for some months, but there is disagreement over whether that is, in fact, the case. Scott Sumner, at the link above in the second paragraph, is skeptical that policy is “tight” even now. That’s despite the fact that the Fed hiked its federal funds rate target 11 times between March 2022 and July 2023 (by a total of 5.25%). The Fed waited too long to get started on its upward rate moves, which helps explain the continuing strength of the economy right now.

The real fed funds rate turned positive (arguably) as early as last winter as the rate rose and as expected inflation began to decline. There is also solid evidence that real interest rates on the short-end of the maturity spectrum are higher than “neutral” real rates and have been for well over a year (see chart below). If the Fed leaves its rate target unchanged over the next few months, assuming expected inflation continues to taper, the real rate will rise passively and the Fed’s policy stance will have tightened further.

Another view is that the Fed’s policy became “tight” when the monetary aggregates began to decrease (April 2022 for M2). A few months later the Fed began so-called “quantitative tightening” (QT—selling securities to reduce its balance sheet). Thus far, QT has reversed only a portion of the vast liquidity provided by the Fed during the pandemic. However, markets do grow accustomed to generous ongoing flows of liquidity. Cutting them off creates financial tensions that have real economic effects. No doubt the Fed’s commitment to QT established some credibility that a real policy shift was underway. So it’s probably fair to say that policy became “tight” as this realization took hold, which might place the date demarcating “tight” policy around 15 – 18 months ago.

Back to the Lags

Again, changes in monetary policy have a discernible impact only with a lag. The broad range of timing discussed among monetary experts (again, going back to Milton Friedman) is 9 – 24 months. We’re right in there now, which adds to the conviction among many forecasters that the onset of recession is likely during the first half of 2024. That’s my position, and while the tapering of inflation we’ve witnessed thus far is quite encouraging, it might take sustained monetary restraint before we’re at or below the Fed’s 2% target. That also increases the risk that we’ll ultimately suffer through a hard landing. In fact, there are prominent voices like hedge fund boss Bill Ackman who predict the Fed must begin to cut the funds rate soon to avoid a hard landing. Jamie Diamond, CEO of JP Morgan, says the U.S. is headed for a hard landing in 2024.

Looking Forward

If new data over the next few months is consistent with a “soft landing” (and it would take much more than a few months to be conclusive), or especially if the data more strongly indicate an incipient recession, the Fed certainly won’t raise its target rate again. The Fed is likely to begin to cut the funds rate sometime next year, and sooner if a recession seems imminent. Otherwise, my guess is the Fed waits at least until well into the second quarter. The average of FOMC member forecasts at the December meeting works out to three quarter-point rate cuts by year-end 2024. When the Fed does cut its target rate, I hope it won’t at the same time abandon QT, the continuing sales of securities from its currently outsized portfolio. Reducing the Fed’s holdings of securities will restrain money growth and give the central bank more flexibility over future policy actions. QT will also put pressure on Congress and the President to reduce budget deficits.

We’re told again and again that government must take action to correct “market failures”. Economists are largely responsible for this widespread view. Our standard textbook treatments of external costs and benefits are constructed to demonstrate departures from the ideal of perfectly competitive market equilibria. This posits an absurdly unrealistic standard and diminishes the power and dramatic success of real-world markets in processing highly dispersed information, allocating resources based on voluntary behavior, and raising human living standards. It also takes for granted the underlying institutional foundations that lead to well-functioning markets and presumes that government possesses the knowledge and ability to rectify various departures from an ideal. Finally, “corrective” interventions are usually exposited in economics classes as if they are costless!

Failed Disgnoses

This brings into focus the worst presumption of all: that government solutions to social and economic problems never fail to achieve their intended aims. Of course that’s nonsense. If defined on an equivalent basis, government failure is vastly more endemic and destructive than market failure.

“According to ancient legend, a Roman emperor was asked to judge a singing contest between two participants. After hearing the first contestant, the emperor gave the prize to the second on the assumption that the second could be no worse than the first. Of course, this assumption could have been wrong; the second singer might have been worse. The theory of market failure committed the same mistake as the emperor. Demonstrating that the market economy failed to live up to the ideals of general competitive equilibrium was one thing, but to gleefully assert that public action could costlessly correct the failure was quite another matter. Unfortunately, much analytical work proceeded in such a manner. Many scholars burst the bubble of this romantic vision of the political sector during the 1960s. But it was [James] Buchanan and Gordon Tullock who deserve the credit for shifting scholarly focus.”

John Cochrane sums up the whole case succinctly in the “punchline” of a recent post:

“The case for free markets never was their perfection. The case for free markets always was centuries of experience with the failures of the only alternative, state control. Free markets are, as the saying goes, the worst system; except for all the others.”

Tracing Failures

We can view the relation between market failure and government failure in two ways. First, we can try to identify market failures and root causes. For example, external costs like pollution cause harm to innocent third parties. This failure might be solely attributable to transactions between private parties, but there are cases in which government engages as one of those parties, such as defense contracting. In other cases government effectively subsidizes toxic waste, like the eventual disposal of solar panels. Another kind of market failure occurs when firms wield monopoly power, but that is often abetted by costly regulations that deliver fatal blows to small competitors.

The second way to analyze the nexus between government and market failures is to first examine the taxonomy of government failure and identify the various damages inflicted upon the operation of private markets. That’s the course I’ll follow below, though by no means is the discussion here exhaustive.

Failures In and Out of Scope

An extensive treatment of government failure was offered eight years ago by William R. Keech and Michael Munger. To start, they point out what everyone knows: governments occasionally perpetrate monstrous acts like genocide and the instigation of war. That helps illustrate a basic dichotomy in government failures:

“… government may fail to do things it should do, or government may do things it should not do.’

Both parts of that statement have numerous dimensions. Failures at what government should do run the gamut from poor service at the DMV, to failure to enforce rights, to corrupt bureaucrats and politicians skimming off the public purse in the execution of their duties. These failures of government are all too common.

What government should and should not do, however, is usually a matter of political opinion. Thomas Jefferson’s axioms appear in a single sentence at the beginning of the Declaration of Independence; they are a tremendous guide to the first principles of a benevolent state. However, those axioms don’t go far in determining the range of specific legal protections and services that should and shouldn’t be provided by government.

Pareto Superiority

Keech and Munger engage in an analytical exercise in which the “should and shouldn’t” question is determined under the standard of Pareto superiority. A state of the world is Pareto superior if at least one person prefers it to the current state (and no one else is averse to it). Coincidentally, voluntary trades in private markets always exploit Pareto superior opportunities, absent legitimate external costs and benefits.

The set of Pareto superior states available to government can be expanded by allowing for side payments or compensation to those who would have preferred the current state. Still, those side payments are limited by the magnitude of the gains flowing to those who prefer the alternative (and if those gains can be redistributed monetarily).

Keech and Munger define government failure as the unexploited existence of Pareto superior states. Of course, by this definition, only a benevolent, omniscient, and omnipotent dictator could hope to avoid government failure. But this is no more unrealistic than the assumptions underlying perfectly competitive market equilibrium from which departure are deemed “market failures” that government should correct. Thus, Keech and Munger say:

“The concept of government failure has been trapped in the cocoon of the theory of perfect markets. … Government failure in the contemporary context means failing to resolve a classic market failure.”

But markets must operate within a setting defined by culture and institutions. The establishment of a social order under which individuals have enforceable rights must come prior to well-functioning markets, and that requires a certain level of state capacity. Keech and Munger are correct that market failure is often a manifestation of government failure in setting and/or enforcing these “rules of the game”.

“The real question is … how the rules of the game should be structured in terms of incentives, property rights, and constraints.”

The Regulatory State and Market Failures

Government can do too little in defining and enforcing rights, and that’s undoubtedly a cause of failure in markets in even the most advanced economies. At the same time there is an undeniable tendency for mission creep: governments often try to do too much. Overregulation in the U.S. and other developed nations creates a variety of market failures. This includes the waste inherent in compliance costs that far exceed benefits; welfare losses from price controls, licensing, and quotas; diversion of otherwise productive resources into rent seeking activity, anti-competitive effects from “regulatory capture”; Chevron-like distortions endemic to the administrative judicial process; unnecessary interference in almost any aspect of private business; and outright corruption and bribe-taking.

Central Planning and Market Failures

Another category of government attempting to “do too much” is the misallocation of resources that inevitably accompanies efforts to pick “winners and losers”. The massive subsidies flowing to investors in various technologies are often misdirected. Many of these expenditures end up as losses for taxpayers, and this is not the only form in which failed industrial planning takes place. A related evil occurs when steps are taken to penalize and destroy industries in political disfavor with thin economic justification.

Other clear examples of government “planning” failure are protectionist laws. These are a net drain on our wealth as a society, denying consumers of free choice and saddling the country with the necessity to produce restricted products at high cost relative to erstwhile trading partners.

There are, of course, failures lurking within many other large government spending programs in areas such as national defense, transportation, education, and agriculture. Many of these programs can be characterized as centrally planning. Not only are some of these expenditures ineffectual, but massive procurement spending seems to invite waste and graft. After all, it’s somebody else’s money.

Redistribution and Market Failures

One might regard redistribution programs as vehicles for the kinds of side payments described by Keech and Munger. Some might even say these are the side payments necessary to overcome resistance from those unable to thrive in a market economy. That reverses the historical sequence of events, however, since the dominant economic role of markets preceded the advent of massive redistribution schemes. Unfortunately, redistribution programs have been plagued by poor design, such as the actuarial nightmare inherent in Social Security and the destructive work incentives embedded in other parts of the social safety net. These are rightly viewed as government failures, and their distortionary effects spill variously into capital markets, labor markets and ultimately product markets.

Taxation and Market Failures

All these public initiatives under which government failures precipitate assorted market failures must be paid for by taxpayers. Therefore, we must also consider the additional effects of taxation on markets and market failures. The income tax system is rife with economic distortions. Not only does it inflict huge compliance costs, but it alters incentives in ways that inhibit capital formation and labor supply. That hampers the ability of input markets to efficiently meet the needs of producers, inhibiting the economy’s productive capacity. In turn, these effects spill into output market failures, with consequent losses in .social welfare. Distortionary taxes are a form of government failure that leads to broad market failures.

Deficits and Market Failure

More often than not, of course, tax revenue is inadequate to fund the entire government budget. Deficit spending and borrowing can make sense when public outlays truly produce long-term benefits. In fact, the mere existence of “risk-free” assets (Treasury debt) across the maturity spectrum might enhance social welfare if it enables improvements in portfolio diversification that outweigh the cost of the government’s interest obligations. (Treasury securities do bear interest-rate risk and, if unindexed, they bear inflation risk.)

Nevertheless, borrowing can reflect and magnify deleterious government efforts to “do too much”, ultimately leading to market failures. Government borrowing may “crowd out” private capital formation, harming economy-wide productivity. It might also inhibit the ability of households to borrow at affordable rates. Interest costs of the public debt may become explosive as they rise relative to GDP, limiting the ability of the public sector to perform tasks that it should *actually* do, with negative implications for market performance.

Inflation and Market Failure

Deficit spending promotes inflation as well. This is more readily enabled when government debt is monetized, but absent fiscal discipline, the escalation of goods prices is the only remaining force capable of controlling the real value of the debt. This is essentially the inflation tax.

Inflation is a destructive force. It distorts the meaning of prices, causes the market to misallocate resources due to uncertainty, and inflicts costs on those with fixed incomes or whose incomes cannot keep up with inflation. Sadly, the latter are usually in lower socioeconomic strata. These are symptoms of market failure prompted by government failure to control spending and maintain a stable medium of exchange.

Conclusion

Markets may fail, but when they do it’s very often rooted in one form of government failure or another. Sometimes it’s an inadequacy in the establishment or enforcement of property rights. It could be a case of overzealous regulation. Or government may encroach on, impede, or distort decisions regarding the provision of goods or services best left to the market. More broadly, redistribution and taxation, including the inflation tax, distort labor and capital markets. The variety of distortions created when government fails at what it should do, or does what it shouldn’t do, is truly daunting. Yet it’s difficult to find leaders willing to face up to all this. Statism has a powerful allure, and too many elites are in thrall to the technocratic scientism of government solutions to social problems and central planning in the allocation of resources.

The inflation news was good last week, with both the consumer and producer price indices (CPI and PPI) for May coming in below expectations. The increase in the core CPI, which excludes food and energy prices, was the same as in April. Asthis series of tweets attempts to demonstrate, teasing out potential distortions from the shelter component of the CPI shows a fairly broad softening. That might be heartening to the Federal Reserve, though at 4.0%, the increase in the CPI from a year ago remains too high, as does the core rate at 5.3%. Later in the month we’ll see how much the Fed’s preferred inflation gauge, the PCE deflator, exceeds the 2% target.

Inflation has certainly tapered since last June, when the CPI had its largest monthly increase of this cycle. After that, the index leveled off to a plateau lasting through December. But the big run-up in the CPI a year ago had the effect of depressing the year-over-year increase just reported, and it will tend to depress next month’s inflation report as well. After this June’s CPI (to be reported in July), the flat base from a year earlier might have a tendency to produce rising year-over-year inflation numbers over the rest of this year. Also, the composition of inflation has shifted away from goods prices and into services, where markets aren’t as interest-rate sensitive. Therefore, the price pressure in services might have more persistence.

So it’s way too early to say that the Fed has successfully brought inflation under control, and they know it. But last week, for the first time in 10 meetings, the Fed’s chief policy-making arm (the Federal Open Market Committee, or FOMC) did not increase its target for the federal funds rate, leaving it at 5% for now. This “pause” in the Fed’s rate hikes might have more to do with internal politics than anything else, as new Vice Chairman Philip Jefferson spoke publicly about the “pause” several days before the meeting. That statement might not have been welcome to other members of the FOMC. Nevertheless, at least the pause buys some time for the “long and variable lags” of earlier monetary tightening to play out.

There are strong indications that the FOMC expects additional rate hikes to be necessary in order to squeeze inflation down to the 2% target. The “median member” of the Committee expects the target FF rate to increase by an additional 50 basis points by the end of 2023. At a minimum, it seems they felt compelled to signal that later rate hikes might be necessary after having their hand forced by Jefferson. That “expectation” might have been part of a “political bargain” struck at the meeting.

In addition, the Fed’s stated intent is to continue drawing down its massive securities portfolio, an act otherwise known as “quantitative tightening” (QT). That process was effectively interrupted by lending to banks in the wake of this spring’s bank failures. And now, a danger cited by some analysts is that a wave of Treasury borrowing following the increase in the debt ceiling, along with QT, could at some point lead to a shortage of bank reserves. That could force the Fed to “pause” QT, essentially allowing more of the new Treasury debt to be monetized. This isn’t an imminent concern, but perhaps next year it could present a test of the Fed’s inflation-fighting resolve.

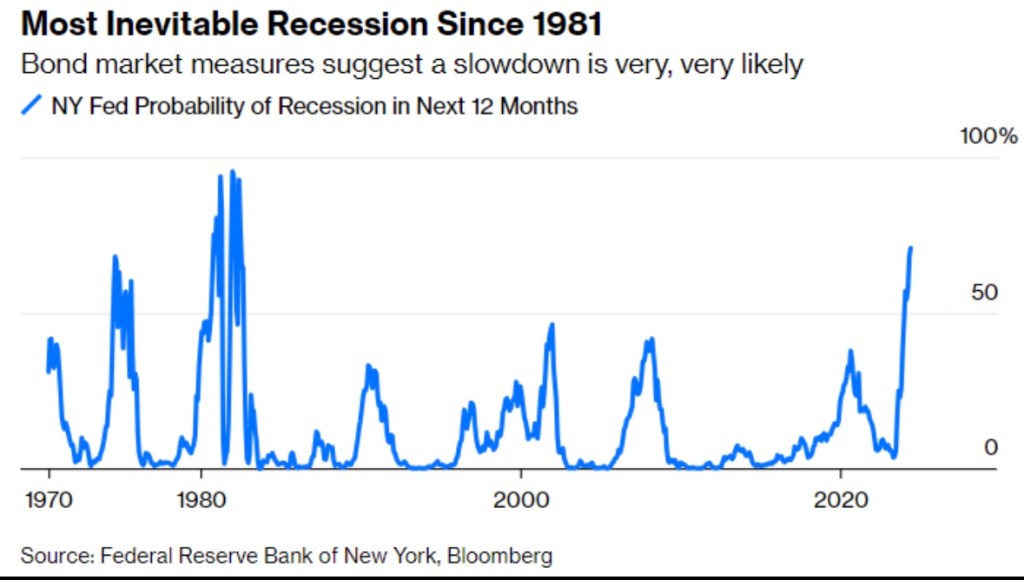

It’s certainly too early to declare that the Fed has engineered a “soft landing”, avoiding recession while successfully reigning-in inflation. The still-inverted yield curve is the classic signal that credit markets “expect” a recession. Here is the New York Federal Reserve Bank’s recession probability indicator, which is at its highest level in over 40 years:

There are other signs of weakness: the index of leading economic indicators has moved down for the last 13 months, real retail sales are down from 13 months ago, and real average weekly earnings have been trending down since January, 2021. A real threat is the weakness in commercial real estate, which could renew pressure on regional banks. Credit is increasingly tight, and that is bound to take a toll on the real economy before long.

The labor market presents its own set of puzzles. The ratio of job vacancies to job seekers has declined, but it is still rather high. Multiple job holders have increased, which might be a sign of stress. Some have speculated that employers are “hoarding” labor, hedging against the advent of an ultimate rebound in the economy, when finding new workers might be a challenge.

Despite some high-profile layoffs in tech and financial services, job gains have held up well thus far. Of course, the labor market typically lags turns in the real economy. We’ve seen declining labor productivity, consistent with changes in real earnings. This is probably a sign that while job growth remains strong, we are witnessing a shift in the composition of jobs from highly-skilled and highly-paid workers to lower-paid workers.

A further qualification is that many of the most highly-qualified job applicants are already employed, and are not part of the pool of idle workers. It’s also true that jobless claims, while not at alarming levels, have been trending higher.

It’s important to remember that the Fed’s policy stance over the past year is intended to reduce liquidity and ultimately excess demand for goods and services. In typical boom-and-bust fashion, the tightening was a reversal from the easy-money policy pursued by the Fed from 2020 – early 2022, even in the face of rising inflation. The money supply has been declining for just over a year now, but the declines have been far short of the massive expansion that took place during the pandemic. There is still quite a lot of liquidity in the system.

That liquidity helps explain the stock market’s recovery in the face of ongoing doubts about the economy. While the market is still well short of the highs reached in early 2022, recent gains have been impressive.