Social Security wasn’t designed as a true saving vehicle for workers. Instead, SS has always been a pay-as-you-go system under which current benefits are funded by the payroll taxes levied on the current employed population. In fact, many Americans earn lousy effective returns on their tax “contributions” (also see here), though low-income individuals do much better than those near or above the median income. Worst of all, under pay-as-you-go, the system can collapse like a Ponzi scheme when the number of workers shrinks drastically relative to the retired population, leading to the kind of situation we face today.

Unfunded Obligations

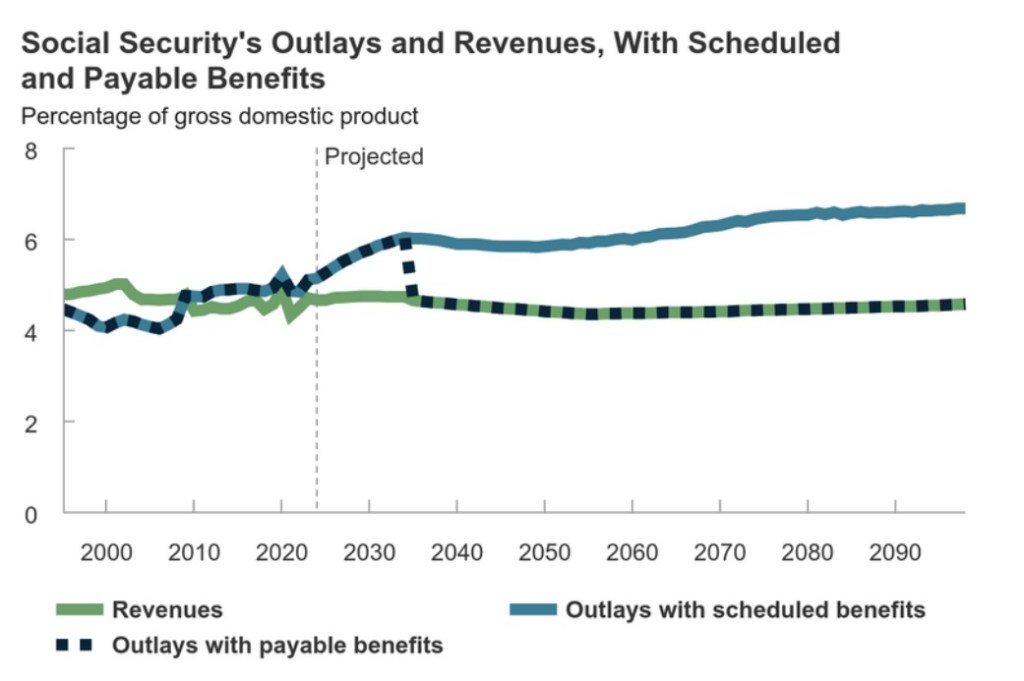

Payroll tax revenue is no longer adequate to pay for current Social Security and Medicare benefits, and the problem is huge: according to the Penn-Wharton Budget Model, the unfunded obligations of Social Security (including old age, survivorship and disability) through 2095 have a present value of $18.1 trillion in constant 2024 dollars (using a discount rate of 4.4%). The comparable figure for Medicare Part A is $18.6 trillion. Together these amount to more than the current national debt.

Barring earlier reform, the Social Security Trust Fund is expected to be exhausted in 2033 (excluding the disability fund). At that point, a 20% reduction in benefits will be required by law. (More on the trust fund below.)

What To Do?

The most prominent reform proposals involve reduced benefits for wealthy beneficiaries, increased payroll taxes on high earners, and an increase in the retirement age. However, President-Elect Donald Trump shows no inclination to make any changes on his watch. This is unfortunate because the sooner the system’s insolvency is addressed, the less draconian the necessary reforms will be.

A neglected reform idea is for SS to be privatized. Many observers agree in principle that current workers could earn better returns over the long-term by investing funds in a conservative mix of equities and bonds. The transition to private accounts could be made voluntary, so that no one is forced to give up the benefits to which they’re “entitled”.

Takers would receive an initial deposit from the government in a tax-deferred account. For participating pre-retirees, ongoing FICA contributions (in whole or in part) would be deposited into their private accounts. They could purchase a private annuity with the balance at retirement if they choose. The income tax treatment of annuity payments or distributions could mimic the current tax treatment of SS benefits.

Given that the balance remaining at death would be heritable, some individuals might be willing to accept an initial deposit less than the actuarial PV of the future SS benefits they’ve accumulated to-date (discounted at an internal rate of return equating future benefits “earned” to-date and contributions to-date). I also believe many individuals would willingly accept a lower initial deposit because they would gain some control over investment direction. Such voluntarily-accepted reductions in initial deposits to personal accounts would mean the government’s issue of new debt would be smaller than the decrease in future benefit obligations.

Nevertheless, funding the accounts at the time of transition would necessitate a huge and immediate increase in federal debt. Market participants and political interests are likely to fear an impossible strain on the credit market. Perhaps the transition could be staged over time to make it less “shocking”, but that would complicate matters. In any case, heavy debt issuance is the rub that dissuades most observers from supporting privatization.

Fiscal Theory of Price Level

The fiscal theory of the price level (FTPL) implies that such a privatization might not be an insurmountable challenge after all, at least in terms of comparative dynamics. Much background on FTPL can be found at John Cochrane’s Grumpy Economist Substack.

FTPL asserts that fiscal policy can influence the price level due to a constraint on the market value of government debt. This market value must be in balance with the expected stream of future government primary surpluses. This is known as the government budget constraint.

The primary surplus excludes the government’s interest expense, a budget component that must be paid out of the primary surplus or else borrowed. Of course, the market value of government debt incorporates the discounted value of future interest payments.

This budget constraint must be true in an expectational sense. That is, the market must be convinced that future surpluses will be adequate to pay all future obligations associated with the debt. Otherwise, the value of the debt must change.

Should a spending initiative require the government to issue new debt with no credible offset in terms of future surpluses, the market value of the debt must decline. That means interest rates and/or the price level must rise. If interest rates are fixed by the monetary authority (the Fed) then only prices will rise.

A SS Private Option Under FTPL

But what about FTPL in the context of entitlement reform, specifically a privatization of Social Security? Suppose the government issues debt and then deposits the proceeds into personal accounts to fund future benefits. Future government surpluses (deficits) would increase (decrease) by the reduction in future SS benefit payments.

This improved budgetary position should be highly credible to financial markets, despite the fact that benefits are not and never have been guaranteed. If it is credible to markets, the new debt would not raise prices, nor would it be valued differently than existing debt. There need not be any change in interest rates.

But Thin Ice

There are risks, of course. It might be too much to hope that other federal spending can be restrained. That kind of failure would subvert the rationale for any budgetary reform. A variety of other crises and economic shocks are also possible. Those could disrupt markets and jeopardize budget discipline as well. Given a severe shock, interest expense could more readily explode given the massive debt issuance required by the reform discussed here. So there are big risks, but one might ask whether they could turn out to be more disastrous in the absence of reform.

Other Details

The private account “offers” extended to workers or beneficiaries relative to the actuarial PVs of their future benefits would be controversial. Different offer percentages (discounts) could be tested to guage uptake.

Another issue: provisions would have to be made for individuals in “unbanked” households, estimated by the FDIC to be about 4.2% of all U.S. households in 2023. Voluntary uptake of the “offer” is likely to be lower among the unbanked and among those having less confidence in their ability to make financial decisions. However, even a simplified set of choices might be superior to the returns under today’s SS, even for low-income workers, not to mention the very real threat of future reductions in benefits. Furthermore, financial institutions might compete for new accounts in part by offering some level of financial education for new clients.

A similar reform could be applied to Medicare, which like SS is also technically insolvent. Participating beneficiaries could receive some proportion of expected future benefits in a private account, which they could use to pay for private or public health insurance coverage or medical expenses. From a budget perspective, the increase in federal debt would be balanced against the reduction in future Medicare benefits, which would constitute a credible increase (decrease) in future surpluses (deficits).

Credibility

But again, how credible would markets find the decrease in benefit obligations? Direct reductions in future entitlements should be convincing, though politicians are likely to find plenty of other ways to use the savings.

On the other hand, markets already give some weight to the possibility of future benefit cuts (or other policies that would reduce SS shortfalls). So it’s likely that markets will give the reform’s favorable budget implications significant but only “incremental credit”.

Another possible complication is that the market, prior to execution of the reform, might discount the uptake by workers and current retirees. This would necessitate better offers to improve uptake and more debt issuance for a given reduction in future obligations. Skepticism along these lines might worsen implications for the price level and interest rates.

The Trust Fund

Finally, what about the SS Trust Fund? Can it play in role in the reform discussed above? The answer depends on how the trust fund fits into the federal government’s budgetary position.

The trust fund holds as assets only non-marketable Treasury securities acquired in the past when SS contributions exceeded benefit payments. The excess payroll tax revenue was placed in the trust fund, which in turn lent the funds to the federal government to help meet other budgetary needs. Hence the bond holdings.

In terms of the government’s fiscal position, the money has already been pissed away, as it were. The bonds in the trust fund do not represent a pot of money. As noted above, with our age demographics now reversed, payroll taxes no longer meet benefits. Thus, bonds in the trust fund must be redeemed to pay all SS obligations. The Treasury must pay off the bonds via general revenue or by borrowing additional amounts from the public.

Post-reform, if continuing deficits are the order of the day, redeeming bonds in the trust fund would do nothing to improve the government’s fiscal position. If the trust fund “cashes them in” to help meet benefit payments, the federal government must borrow to raise that cash. In other words, the bonds in the trust fund would be more or less superfluous.

But what if the federal budget swings into a surplus position post-reform? In that case, federal tax revenue would cover the redemption of at least some of the bonds held by the trust fund. SS beneficiaries would then have a meaningful claim on federal taxpayers through the trust fund and the government’s surplus position, which would reduce the new federal debt required by the reform.

Conclusion

The Social Security and Medicare systems are in desperate need reform, but there is little momentum for any such undertaking. Meanwhile, exhaustion of the SS and Medicare trust funds creeps ever closer, along with required benefit cuts. All of the reform options would be painful in one way or another. A voluntary privatization would require a huge makeover, but it might be the least painful option of all. Current workers and beneficiaries would not be compelled to make choices they found inferior. Moreover, the new debt necessary to pay for the reforms would be matched by a reduction in future government obligations. The fiscal theory of the price level implies that the reform would not be inflationary and need not depress the value of Treasury bonds, provided the reform is accompanied by long-term budget discipline.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Note: the chart at the top of this post was produced by the Congressional Budget Office and appears in this publication.

Government budget negotiations never fail to frustrate anyone of a small-government persuasion. We have a huge, ongoing federal budget deficit. Spending’s gone bat-shit out of control over the past several years and too few in Congress are willing to do anything about it. Democrats would rather see politically-targeted tax increases. While some Republicans advocate spending cuts, the focus is almost entirely on discretionary spending. Meanwhile, the entitlement state is off the table, including Social Security reform.

Fiscal Indiscretion

Sadly, non-discretionary outlays (entitlements) today make a much larger contribution to the deficit than discretionary spending. That includes the programs like Social Security (SS) and Medicare, in which spending levels are programmatic and not subject to annual appropriations by Congress. When these programs were instituted there were a large number of workers relative to retirees, so tax contributions exceeded benefit levels for many decades. The revenue excesses were placed into “trust funds” and invested in Treasury debt. In other words, surpluses under non-discretionary SS and Medicare programs were used to finance discretionary spending!

The aging of Baby Boomers ultimately led to a reversal in the condition of the trust funds. Fewer workers relative to retirees meant that annual payroll tax collections were not adequate to cover annual benefits, and that meant drawing down the trust funds. Current projections by the system trustees call for the SS Trust Fund to be exhausted by 2035. Once that occurs, benefits will automatically be reduced by roughly 20% unless Congress acts to shore up the system before then.

A Few Proposals

I’ve written about the need for SS reform on several occasions (though the first article at that link is not germane here). It seems imperative for Congress and the President to address these shortfalls. By all appearances, however, many Republicans have put the issue aside. For his part, Joe Biden has apparently accepted the prospect of an automatic reduction in benefits in 2035, or at least he’s willing to kick that can down the road. He has, however, endorsed taxes on high earners to fund Medicare. Senator John Kennedy (R-LA) suggests raising the retirement age, or at least raise the minimum age at which one may claim benefits (now 62). Senators Bill Cassidy (R-La.) and Angus King (I-Maine) were working on a compromise that would create an investment fund to fortify the system, but the specifics are unclear, as well as how much that would accomplish.

Meanwhile, Senator Bernie Sanders (S-VT) proposes to expand SS benefits by $2,400 a year and add funding by extending payroll taxes to earners above the current limit of $160,000. Senator Joe Manchin (D-WV) has endorsed the latter as a “quick fix”.

There is also at least oneproposal in Congress to end the practice of taxing a portion of SS benefits as income. I have trouble believing it will gain wide support, despite the clear double-taxation involved.

Then there are always discussions of reducing benefits at higher income levels or even means-testing benefits. In fact, it would be interesting to know what proportion of current benefits actually function as social insurance, as opposed to a universal entitlement. The answer, at least, could serve as a baseline for more fundamental reforms, including changes in the structure of payroll taxes, voluntary lump-sum payouts, and private accounts.

More Radical Views

There are a few prominent voices who claim that SS is sustainable in its current form, but perhaps with a few “no big deal” tax increases. Oh, that’s only about a $1 trillion “deal”, at least for both Medicare and SS. More offensive still are the scare tactics used by opponents of SS reform any time the subject comes up. I’m not aware of any serious reform proposal made over the past two decades that would have affected the benefits of anyone over the age of 55, and certainly no one then-eligible for benefits. Yet that charge is always made: they want to cut your SS benefits! The Democrats made that claim against George W. Bush, torpedoing what might have been a great accomplishment for all. And now, apparently Donald Trump is willing to use such accusations to damage any rival who has ever mentioned reform, including Mike Pence. Will you please cut the crap?

The System

The thing to remember about SS is that it is currently structured as a pay-as-you-go (PAYGO) system, despite the fact that benefits are defined like many creaky private pensions of old. SS benefits in each period are paid out of current “contributions” (i.e., FICO payroll taxes) plus redemptions of government bonds held in the Trust Fund. Contributions today are not “invested” anywhere because they are not enough to pay for current benefits under PAYGO.

The Trust Fund was accumulated during the years when favorable demographics led to greater FICO contributions than benefit payouts. The excess revenue was “invested” in Treasury bonds, which meant it was used to fund deficits in the general budget. It’s been about 15 years since the Trust Fund entered a “draw-down” status, and again, it will be exhausted by 2035.

SSA Says It’s a Good Deal

A participant’s expected “rate of return” on lifetime payroll tax payments depends on several things: lifetime earnings, age at which benefits are first claimed, life expectancy at that time, marital status, relative earning levels within two-earner couples, and the “full retirement age” for the individual’s birth year. Payroll tax payments, by the way, include the employer’s share because that is one of the terms of a hire. A high rate of return is not the same as a high level of benefits, however. In fact, relative to career income, SS has a great deal of progressivity in terms of rates of return, but not much in terms of benefit levels.

The Social Security Administration (SSA) has calculated illustrative real internal rates of return (IRR) for many categories of earners given certain assumptions. (An IRR is a discount rate that equalizes the present value (PV) of a stream of payments and the PV of a stream of payoffs.) The SSA’s most recent update of this exercise was in April 2022. The report references Old Age, Survivors, and Disability Insurance (OASDI), but the focus is exclusively on seniors.

Three basic scenarios were considered: 1) current law, as scheduled, despite its unsustainability; 2) a payroll tax increase from 12.4% (not including the Medicare tax) to 15.96% starting in 2035, when the Trust Fund is exhausted; and 3) a reduction in benefits of 22% starting in 2035.

The authors of the report concludethat “… the real value of OASDI benefits is extraordinarily high.” This theme has been echoed by several other writers, such as here and here. This conclusion is based on a comparison to returns earned by investments that SSA judges to have comparably low risk.

I note here that I’ve made assertions in the past about relative SS returns based on nominal benefits, rather than inflation-adjusted values. Those comparisons to private returns might have seemed drastic because they were expressed in terms of hypothetical future nominal values at the point of retirement. The gaps are not as large in real terms or if we consider SS returns broadly to include those accruing to low career earners. Medium and high earners tend to earn lower hypothetical returns from SS.

A Mixed Bag

SSA’s calculated IRRs are highest for one-earner couples followed by two-earner couples. Single males do relatively poorly due to their higher mortality rates. Low earners do very well relative to higher earners. Earlier birth years are associated with higher IRRs, but these are not as impressive for cohorts who have not yet claimed benefits. The ranges of birth years provided in the report make this a little imprecise, but I’ll focus on those born in 1955 and later.

Of course the returns are highest under the current law hypothetical than for the scenarios involving a benefit reduction or a payroll tax hike. The current law IRRs can be viewed as baselines for other calculations, but otherwise they are irrelevant. The system is technically insolvent and the scheduled benefits under current law can’t be maintained beyond 2034 without steps to generate more revenue or cut benefits. Those steps will reduce IRRs earned by hypothetical SS “assets” whether they take the form of higher payroll taxes, lower benefits, a greater full retirement age, or other measures.

The tax hike doesn’t have much impact on the IRRs of near-term retirees. It falls instead on younger cohorts with some years of employment (and payroll tax payments) remaining. The effect of a cut in benefits is spread more evenly across age cohorts and the reductions in IRRs is somewhat larger.

With higher payroll taxes after 2034, the average IRRs for birth years of 1955+ range from about 0.5% up to about 6.25%. The returns for single females and two-earner couples are roughly similar and fall between those for single males on the low end and one-earner couples on the high end. In all cases, low earners have much higher IRRs than others.

The reduction in benefits produces returns for the 1955+ age cohorts averaging small, negative values for high-earning single men up to 5.5% to 6% for low-earning, one-earner couples.

But On the Whole…

The IRR values reported by SSA are quite variable across cohorts. Individuals or couples with low earnings can usually expect to “earn” real IRRs on their contributions of better than 3% (and above 5% in a few cases). Medium earners can expect real returns from 1% to 3% (and in some cases above 4%). Many of the returns are quite good for a safe “asset”, but not for high earners.

Again, SSA states that these are real returns, though they provide no detail on the ways in which they adjust the components used in their IRR formula to arrive at real returns. Granting the benefit of the doubt, we saw persistently negative real returns on a range of safe assets in the not-very-distant past, so the IRRs are respectable by comparison.

Qualifications

There are many assumptions in the SSA’s analysis that might be construed as drastic simplifications, such as no divorce and remarriage, uniform career duration, and no relationship between earnings and mortality. But it’s easy to be picky. Many of the assumptions discernible from the report seem to be reasonable simplifications in what could otherwise be an unruly analysis. Nonetheless, there are a few assumptions that I believe bias the IRRs upward (and perhaps a few in the other direction).

In fact, SSA is remarkably non-transparent in their explanation of the details. Repeated checking of SSA’s document for clear answers is mostly futile. Be that as it may, I’m forced to give SSA the benefit of the doubt in several respects. One is the reinvestment of cumulative remaining contributions at the IRR throughout the earning career and retirement. A detailed formula with all components and time subscripts would have been nice.

… And Major Doubts

As to my misgivings, first, the IRRs reported by SSA are based on earners who all reach the age of 65. However, roughly 14% – 15% of individuals who live to be of working age die before they reach the age of 65. Most of those deaths occur in the latter part of that range, after many years of contributions and hypothetical compounding. That means the dollar impact of contributions forfeited at death before age 65 is probably larger than the unweighted share of individuals. These individuals pay-in but receive no retirement benefit in SSA’s IRR framework, although some receive disability benefits for a period of time prior to death. It wouldn’t bother my conscience to knock off at least a tenth of the quoted returns for this consideration alone.

A second major concern surrounds the method of calculating benefits and discounted benefits. SSA assumes that benefits continue for the expected life of the claimant as of age 65. If life expectancy is 19 years at age 65, then “expected” benefits are a flat stream of benefit payments for 19 years. Discounting each payment back to age 65 at the IRR yields one side of the present value equality. This constant cash flow (CCF) treatment is likely to overstate the present value of benefits. Instead of CCFs, each payment should be weighted by the probability that the claimant will be alive to receive it with a limit at some advanced age like 100. CCF overcounts present values up to the expected life, but it undercounts present values beyond the expected life because the assumed CCF benefits then are zero!! Weighting benefit payments by the probability of survival to each age produces continuing additions to the PV, but increasing mortality and decaying discount factors become quite substantial beyond expected life, leading to relatively minor additions to PV over that range. The upshot is that the CCFs employed by SSA overstate PVs by front-loading all benefits earlier in retirement. For a given PV of contributions, an overstated PV of benefits requires a higher (and overstated) IRR to restore the PV equality, and this might be a substantial source of upward bias in SSA’s calculations.

Third, when comparing an SS “asset” to private returns, a big difference is that private balances remaining at death become assets of the earner’s estate. Meanwhile, a single beneficiary forfeits their SS benefits at death (except for a small death benefit), while a surviving spouse having lower benefits receives ongoing payments of the decedent’s benefits for life. This consideration, however, in and of itself, means that private plans have a substantial advantage: the “expected” residual at death can be “optimized” at zero or some higher balance, depending on the strength of the earner’s bequest motive.

Finally, in a footnote, the SSA report notes that their treatment of income taxes on Social Security benefits for claimants with higher incomes might bias some of the IRRs upward. That seems quite likely.

It would be difficult to recast SSA’s report based on adjustments for all of these qualifications. However, it’s likely that the IRRs in the SSA report are sharply overstated. That means many more beneficiaries with medium and higher earnings records would have returns in the 0% to 2% range, with more IRRs in the negative range for singles. Low earners, however, might still get returns in a range of 3% to 5%.

The SSA analysis attempts to demonstrate some limits to the risks faced by participants, given the scenarios involving a payroll tax increase or a benefits reduction in 2035. Nevertheless, there are additional political risks to the returns of certain classes of current and future retirees. For example, payroll taxes could be made much more progressive, benefits could be made subject to means testing, or indexing of benefits could be reduced. In fact, there are additional demographic risks that might confront retirees several decades ahead. Continued declines in fertility could further undermine the system’s solvency, requiring more drastic steps to shore up the system. As a hypothetical asset, by no means is SS “risk-free”.

Better Returns

Now let’s consider returns earned by private assets, which represent investments in productive capital. For stocks, these include the sum of all dividends and capital gains (growth in value). For compounding purposes, we assume that all returns are reinvested until retirement. Remember that private returns are much less variable over spans of decades than over durations of a few years. Over the course of 40 year spans (SSA’s career assumption), private returns have been fairly stable historically, and have been high enough to cushion investors from setbacks. Here is Seeking Alpha on annualized returns on the basket of stocks in the S&P 500:

“… the return on the S&P 500 since the beginning of valuation in 1928, is 10.22%, whereas the inflation-adjusted return on the market since that time is 7.01%…”

That real return would generate benefits far in excess of SS for most participants, but it’s not an adequate historical perspective on market performance. A more complete picture of real returns on the S&P, though one that is still potentially flawed, emerges from this calculator, which relies on data from Robert Shiller. The returns extend back to 1871, but the index as we know it today has existed only since 1957. The earlier returns tend to be lower, so these values may be biased:

Real stock market returns over rolling 40-year time spans varied considerably over this longer period. Still, those kind of stock returns would be superior to the IRRs in the SSA report going forward in all but a few cases (and then only for low and very low earners).

Most workers facing a choice between investing at these rates for 40 years, with market risk, and accepting standard SS benefits, uncertain as they are, couldn’t be blamed for choosing stocks. In fact, if we think of contributions to either type of plan as compounding to a hypothetical sum at retirement, the stock investments would produce a “pot of gold” several times greater in magnitude than SS.

However, we still don’t have a fair comparison because workers choosing a stock plan would essentially engage in a kind of dollar-cost averaging over 40 years, meaning that investments would be made in relatively small amounts over time, rather than investing a lump-sum at the beginning. This helps to smooth returns because purchases are made throughout the range of market prices over time, but it also means that returns tend to be lower than the 40-year rolling returns shown above. That’s because the average contribution is invested for only half the time.

To be very conservative, if we assume that real stock returns average between 5% and 6% annually, $1 invested every year would grow to between $131 – $155 after 40 years in constant dollars. At returns of 1% to 2% from SS, which I believe are typical of the IRRs for many medium earners, the cumulative “pot” would grow to $49 – $60. Assuming that the tax treatment of the stock plan was the same as contributions and benefits under SS, the stock plan almost triples your money.

Dealing With the Transition

Privatization covers a range of possible alternatives, all of which would require federal borrowing to pay transition costs. Unfortunately, the Achilles heel in all this is that now is a bad time to propose more federal borrowing, even if it has clear long-term benefits to future retirees.

Todd Henderson in the Wall Street Journal suggests a seeding of capital provided by government at birth along with an insurance program to smooth returns. Another idea is to offer an inducement to delay retirement claims by allowing at least a portion of future benefits to be taken as a lump sum. If retirees can privately invest at a more advantageous return, they might be willing to accept a substantial discount on the actuarial value of their benefits.

In fact, there is evidence that a majority of participants seem to prefer distributions of lump sums because they don’t value their future benefits at anything like that suggested by the SSA analysis. In fact, many participants would defer retirement by 1 – 2 years given a lump sum payment. Discounts and/or delayed claims would reduce the ultimate funding shortfall, but it would require substantial federal borrowing up front.

Additional federal borrowing would also be required under a private option for investing one’s own contributions for future dispersal. The impact of this change on the system’s long-term imbalances would depend on the share of earners willing to opt-out of the traditional SS program in whole or in part. More opt-outs would mean a smaller long-term obligations for the traditional system, but it would be hampered by a costly transition over a number of years. Starting from today’s PAYGO system, someone still has to pay the benefits of current retirees. This would almost certainly mean federal borrowing. Spreading the transition over a lengthy period of time would reduce the impact on credit markets, but the borrowing would still be substantial.

For example, perhaps earners under 35 years of age could begin opting out of a portion or all of the traditional program at their discretion, investing contributions for their own future use. Thus, only a small portion of contributions would be diverted in the beginning, and amounts diverted would contribute to the nation’s available pool of saving, helping to keep borrowing costs in check. By the time these younger earners reach retirement age, nearly all of today’s retirees will have passed on. Ultimately, the average retiree will benefit from higher returns than under the traditional program, but since they won’t be (fully) paying the benefits of current or near-term retirees, the public must come to grips with the bad promises of the past and fund those obligations in some other way: reduced benefits, taxes, or borrowing.

Another objection to privatization is financial risk, particularly for lower-income beneficiaries. Limiting opt-outs to younger earners with adequate time for growth would mitigate this risk, along with a reversion to the traditional program after age 45, for example. Some have proposed limiting opt-outs to higher earners. Bear in mind, however, that the financial risk of private accounts should be weighed against the political and demographic risk already inherent in the existing system.

One more possibility for bridging the transition to private, individually-controlled accounts is to sell federal assets. I have discussed this before in the context of funding a universal basic income (which I oppose). The proceeds of such sales could be used to pay the benefits of current and near-term retirees so as to allow the opt-out for younger workers. Or it could be used to pay off federal debt accumulated in the process. The asset sales would have to proceed at a careful and deliberate pace, perhaps stretching over several decades, but those sales could include everything from the huge number of unoccupied federal buildings to vast tracts of public lands in the west, student loans, oil and gas reserves, and airports and infrastructure such as interstate highways and bridges. Of course, these assets would be more productive in private hands anyway.

The Likely Outcome

Will any such privatization plan ever see the light of day? Probably not, and it’s hard to guess when anything will be done in Washington to address the insolvency we already face. Instead, we’ll see some combination of higher payroll taxes, higher payroll taxes on high earners through graduated payroll tax rates or by lifting the earnings cap, reduced benefits on further retirees, limits on COLAs to low career earners, and means-tested benefits. Some have mentioned funding Social Security shortfalls with income taxes. All of these proposals, with the exception of automatic benefit cuts in 2035, would require acts of Congress.

It’s as if people view the debt limit controversy as a political nuisance rather than the stopgap enforcement mechanism for fiscal sanity that it’s intended to be. That’s a lesson in how far we’ve gone toward an unhealthy acceptance of permanent federal deficits. Oh, most people seem to realize the the government’s spending is prodigious and beyond our capacity to collect taxes, but many don’t grasp the recklessness of the ongoing blowout. Federal deficits are expected to average $1.6 trillion per year over the next decade, versus less than $0.9 trillion and $1.25 trillion over the two previous decades, respectively. That $1.25 trillion includes the massive (and excessive) transfers that took place during the pandemic, which is why we’ve bumped up against the debt limit earlier than had been expected. The trend isn’t abating, despite the fact that the pandemic is behind us. And keep in mind that the Congressional Budget Office has been too optimistic for the past 20 years or so. Take a look at federal debt relative to GDP:

Unpleasant Arithmetic

With federal debt growing faster than GDP, the burden of servicing the debt mounts. This creates a strain in the coordination of fiscal and monetary policy, as described by David Andolfatto, who last year reviewed the implications of “Some Unpleasant Monetarist Arithmetic” for current policy. His title was taken from a seminal paper written by Thomas Sargent and Neil Wallace in 1981. Andolfatto says that:

“… attempting to monetize a smaller fraction of outstanding Treasury securities has the effect of increasing the rate of inflation. A tighter monetary policy ends up increasing the interest expense of debt issuance. And if the fiscal authority is unwilling to curtail the rate of debt issuance, the added interest expense must be monetized—at least if outright default is to be avoided.

Andolfatto wrote that last spring, before the Federal Reserve began its ongoing campaign to tighten monetary policy by raising short-term interest rates. But he went on to say:

“Deficit and debt levels are elevated relative to their historical norms, and the current administration seems poised to embark on an ambitious public spending program. … In the event that inflation rises and then remains intolerably above target, the Federal Reserve is expected to raise its policy rate. … if the fiscal authority is determined to pursue its deficit policy into the indefinite future, raising the policy rate may only keep a lid on inflation temporarily and possibly only at the expense of a recession. In the longer run, an aggressive interest rate policy may contribute to inflationary pressure—at least until the fiscal regime changes.”

So it is with a spendthrift government: escalating debt and interest expense must ultimately be dealt with via higher taxes or inflation, despite the best intentions of a monetary authority.

Fiscal Wrasslin’

Some people think the debt limit debate is all a big fake. Maybe … there are spendthrifts on both sides of the aisle. Still, the current debt limit impasse could serve a useful purpose if fiscal conservatives succeed in efforts to restrain spending. There is, however, an exaggerated uproar over the possibility of default, meaning a failure to make scheduled payments on Treasury securities. The capital markets aren’t especially worried because an outright default is very unlikely. Establishment Republicans may well resort to their usual cowardice and accept compromise without holding out for better controls on spending. Already, in a politically defensive gesture, House Speaker Kevin McCarthy has said the GOP wishes to strengthen certain entitlement programs. Let’s hope he really means restoring solvency to the Social Security and Medicare Trust Funds via fundamental reforms. And if the GOP rules out cuts to any program, let’s hope they don’t rule out cuts in the growth of these programs, or privatization. For their part, of course, Democrats would like to eliminate the debt ceiling entirely.

One of the demands made by Republicans is a transformation of the federal tax system. They would like to eliminate the income tax and substitute a tax on consumption. Economists have long favored the latter because it would eliminate incentives that penalize saving, which undermine economic growth. Unfortunately, this is almost dead in the water as a political matter, but the GOP further sabotaged their own proposal in their zeal to abolish the IRS. Their consumption tax would be implemented as a national sales tax applied at the point of sale, complete with a new Treasury agency to administer the tax. They’d have done better to propose a value added tax (VAT) or a tax on a simple base of income less saving (and other allowances).

Gimmicks and Measures

We’ve seen proposals for various accounting tricks to allow the government to avoid a technical default and buy time for an agreement to be reached on the debt limit. Treasury Secretary Janet Yellen already has implemented “extraordinary measures” to stay under the debt limit until June, she estimates. The Treasury is drawing down cash, skipping additional investments in government retirement accounts (which can be made up later without any postponement of benefits), plus a few other creative accounting maneuvers.

Payment prioritization, whereby the Treasury makes payments on debt and critical programs such as Social Security and Medicare, but defers a variety of other payments, has also been considered. Those deferrals could include amounts owed to contractors or even government salaries. However, a deferral of payments owed to anyone represents a de facto default. Thus, payment prioritization is not a popular idea, but if push comes to shove, it might be viewed as the lesser of two evils. Missing payments on government bonds could precipitate a financial crisis, but no one believes it will come to that.

Two other ideas for avoiding a breach of the debt ceiling are rather audacious. One involves raising new cash via the sale of premium bonds by the Treasury, as described here by Josh Barro (and here by Matt Levine). The other idea is to mint a large denomination ($1 trillion) platinum, “commemorative” coin, which the Treasury would deposit at the Federal Reserve, enabling it to conduct business as usual until the debt limit impasse is resolved. I’ll briefly describe each of these ideas in more detail below.

Premium Bonds

Premium bonds would offer a solution to the debt limit controversy because the debt ceiling is defined in terms of the par value of Treasury debt outstanding, as opposed to the amount actually raised from selling bonds at auction. For example, a note that promises to pay $100 in one year has a par value of $100. If it also promises to pay $100 in interest, it will sell at a steep premium. Thus, the Treasury collects, say, $185 at auction, and it could use the proceeds to pay off $100 of maturing debt and fund $85 of federal spending. That would almost certainly require a “market test” by the Treasury on a limited scale, and the very idea might reveal any distaste the market might have for obviating the debt limit in this fashion. But distaste is probably too mild a word.

An extreme example of this idea is for the Treasury to sell perpetuities, which have a zero par value but pay interest forever, or at least until redeemed beyond some minimum (but lengthy) term. John Cochrane has made this suggestion, though mainly just “for fun”. The British government sold perpetuities called consols for many years. Such bonds would completely circumvent the debt limit, at least without legislation to redefine the limit, which really is long overdue.

The $1 Trillion Coin

Minting a trillion dollar coin is another thing entirely. Barro has a separate discussion of this option, as does Cochrane. The idea was originally proposed and rejected during an earlier debt-limit controversy in 2011. Keep in mind, in what follows, that the Fed does not follow Generally Accepted Accounting Principles (GAAP).

Skeptics might be tempted to conclude that the “coin trick” is a ploy to engineer a huge increase the money supply to fund government expansion, but that’s not really the gist of this proposal. Instead, the Treasury would deposit the coin in its account at the Fed. The Fed would hold the coin and give the Treasury access to a like amount of cash. To raise that cash, the Fed would sell to the public $1 trillion out of its massive holdings of government securities. The Treasury would use that cash to meet its obligations without exceeding the debt ceiling. As Barro says, the Fed would essentially substitute sales of government bonds from its portfolio for bonds the Treasury is prohibited from selling under the debt limit. The effect on the supply of money is basically zero, and it is non-inflationary unless the approach has an unsettling impact on markets and inflation expectations (which of course is a distinct possibility).

When the debt ceiling is finally increased by Congress, the process is reversed. The Treasury can borrow again and redeem its coin from the Fed for $1 trillion, then “melt it down”, as Barro says. The Fed would repurchase from the public the government securities it had sold, adding them back to its portfolio (if that is consistent with its objectives at that time). Everything is a wash with respect to the “coin trick”, as long as the Treasury ultimately gets a higher debt limit.

Lust For the Coin

In fairness to skeptics, it’s easy to understand why the “coin trick” described above might be confused with another coin minting idea that arose from the collectivist vanguard during the pandemic. Representative Rashida Tlaib (D-MI) proposed minting coins to fund monthly relief payments of $1,000 – $2,000 for every American via electronic benefit cards. She was assisted in crafting this proposal by Rohan Grey, a prominent advocate of Modern Monetary Theory (MMT), the misguided idea that government can simply print money to pay for the resources it demands without inflationary consequences.

Tlaib’s plan would have required the Federal Reserve to accept the minted coins as deposits into the Treasury’s checking account. But then, rather than neutralizing the impact on the money supply by selling government bonds, the coin itself would be treated as base money. Cash balances would simply be made available in the Treasury’s checking account with the Fed. That’s money printing, pure and simple, but it’s not at all the mechanism under discussion with respect to short-term circumvention of the debt limit.

Fed Independence

The “coin trick” as a debt limit work-around is probably an impossibility, as Barro and others point out. First, the Fed would have to accept the coin as a deposit, and it is under no legal obligation to do so. Second, it obligates the Fed to closely coordinate monetary policy with the Treasury, effectively undermining its independence and its ability to pursue its legal mandates of high employment and low inflation. Depending on how badly markets react, it might even present the Fed with conflicting objectives.

Believe me, you might not like the Fed, but we certainly don’t want a Fed that is subservient to the Treasury… maintaining financial and economic stability in the presence of an irresponsible fiscal authority is bad enough without seating that authority at the table. As Barro says of the “coin trick”:

“These actions would politicize the Fed and undermine its independence. In order to stabilize expectations about inflation, the Fed would have to communicate very clearly about its intentions to coordinate its fiscal actions with Treasury — that is, it would have to tell the world that it’s going to act as Treasury’s surrogate in selling bonds when Treasury can’t. …

These actions would interfere with the Fed’s normal monetary operations. … the Fed is currently already reducing its holdings of bonds as part of its strategy to fight inflation. If economic conditions change (fairly likely, in the event of a near-default situation) that might change the Fed’s desired balance sheet strategy.”

On With The Show

Discussions about the debt limit continue between the White House and both parties in Congress. Kevin McCarthy met with President Biden today (2/1), but apparently nothing significant came it. Fiscal conservatives wonder whether McCarthy and other members of the GOP lack seriousness when it comes to fiscal restraint. But spending growth must slow to achieve deficit reduction, non-inflationary growth, and financial stability.

Meanwhile, even conservative media pundits seem to focus only on the negative politics of deficit reduction, ceding the advantage to Democrats and other fiscal expansionists. For those pundits, the economic reality pales in significance. That is a mistake. Market participants are increasingly skeptical that the federal government will ever pay down its debts out of future surpluses. This will undermine the real value of government debt, other nominal assets, incomes and buying power. That’s the inflation tax in action.

Unbridled growth of the government’s claims on resources at the expense of the private sector destroys the economy’s productive potential, to say nothing of growth. The same goes for government’s insatiable urge to regulate private activities and to direct patterns of private resource use. Unfortunately, so many policy areas are in need of reform that imposition of top-down controls on spending seems attractive as a stopgap. Concessions on the debt limit should only be granted in exchange for meaningful change: limits on spending growth, regulatory reforms, and tax simplification (perhaps replacing the income tax with a consumption tax) should all be priorities.

In the meantime, let’s avoid trillion dollar coins. As a debt limit work-around, premium bonds are more practical without requiring any compromise to the Fed’s independence. Other accounting gimmicks will be used to avoid missing payments, of course, but the fact that premium bonds and platinum coins are under discussion highlights the need to redefine the debt limit. When the eventual time of default draws near, fiscal conservatives must be prepared to stand up to their opponents’ convenient accusations of “brinksmanship”. The allegation is insincere and merely a cover for government expansionism.

Here’s a bit of zero-sum ignorance: private profits are robbed from consumers; only non-profits or government can deliver full value, or so this logic goes. Those who subscribe to this notion dismiss the function of private incentives in creating value, yet those incentives are responsible for nearly all of the material blessings of modern life. What the government seems to do best, on the other hand, is writing checks. It’s not really clear it does that very well, of course, but it does have the coercive power of taxation required to do so. Capital employed by government is not a “free” input. It bears opportunity costs and incentive costs that are seldom considered by critics of the private sector.

The role of private profit and the zero-sum fallacy come up in the context of proposals to privatize government services. In what follows, I discuss a case in point: privatization of Medicare. Rep. Tom Price, the Chairman of the House Budget Committee, is Donald Trump’s nominee to head HHS. In November, Price said Congress would attempt to pass legislation overhauling Medicare in the first year of the Trump Administration. James Capretta of the American Enterprise Institute (AEI) explains some of the features of the possible reforms. Price has supported the concept of a premium support plan whereby seniors would purchase their own coverage from private insurers, paid at least in part by the government (also see here).

Medicare and Its Ills

The Medicare program is beset with problems: it has huge unfunded liabilities; it’s cash flows are being undermined by demographic trends; fraud and bureaucratic waste run rampant; it’s unpopular with doctors; and the regulations imposed on healthcare providers are often misguided.

Writing checks to health care providers is really the primary “good” created by the federal government in the administration of Medicare. The Centers for Medicare & Medicaid Services (CMS), a branch of the Department of Health and Human Services (HHS), also performs regulatory functions mandated by legislation, such as the Affordable Care Act (ACA).

More recently, CMS has been implementing the Medicare Access and Chip Reauthorization Act of 2015 (MACRA), which will introduce changes to the payment formulas for physician compensation under the plan. Economist John C. Goodman offers a cogent explanation of the ill-conceived economic planning at the heart of Medicare regulation and its implementation of MACRA in particular:

“…the government’s current payment formulas create perverse economic incentives — to maximize income against the formulas instead of putting patient welfare first. The goal is to change those incentives, so that providers will get paid more if they lower costs and raise quality.

But after the new formulas replace the old ones, provider incentives in a very real sense will be unchanged. They will still have an economic incentive to maximize income by exploiting the formulas, even if that is at the expense of their patients.“

After describing several ways in which Medicare regulation, now and prospectively, leads to perverse results, Goodman advances the powerful argument that the market can regulate health care delivery to seniors more effectively than CMS.

“If the government’s metrics are sound, why not allow health plans to advertise their metrics to potential enrollees and compete on these quality measures. Right now, they cannot. Every communication from health plans to Medicare enrollees must be approved by CMS. … Under MACRA, health plans profit by satisfying the government, not their customers. … Better yet, why not let the market (rather than government) decide on the quality metrics?“

Private Medicare Exists

Wait a minute: profit? But isn’t Medicare a government program, free from the presumed evils of profit-seekers? Well, here’s the thing: almost all of the tasks of managing the provision of Medicare coverage are handled by the private sector under contract with CMS, subject to CMS regulation, of course. That is true even for Part A and Part B benefits, or “original Medicare”, as it’s sometimes called.

Under “original” Medicare, private insurers process “fee-for-service” claims and payments, provide call center services, manage clinician enrollment, and perform fraud investigations. Yes, these companies can earn a profit on these services. Unfortunately, CMS regulation probably serves to insulate them from real competition, subverting efficiency goals. Goodman’s suggestion would refocus incentives on providing value to the consumers these insurers must ultimately serve.

Then there are “Medigap” or Medicare Supplement policies that cover out-of-pocket costs not covered under Parts A and B. These policies are designed by CMS, but they are sold and managed by private insurers.

And I haven’t even mentioned Medicare Parts C and D, which are much more significantly privatized than original Medicare or Medigap. The Part C program, also known as Medicare Advantage, allows retirees to choose from a variety of privately-offered plans as an alternative to traditional Medicare. At a minimum, these plans must cover benefits that are the equivalent to Parts A and B, as judged by CMS, though apparently “equivalency” still allows some of those benefits to be declined in exchange for a rebate on the premium. More optional benefits are available for an additional premium under these plans, including a reduced out-of-pocket maximum, a lower deductible, and reduced copays. Part C has grown dramatically since its introduction in 1996 and now covers 32% of Medicare enrollees. Apparently these choices are quite popular with seniors. So why, then, is privatization such a bogeyman with the left, and with seniors who are cowed by the anti-choice narrative?

What’s To Privatize?

Not privatized are the following Medicare functions: the collection of payroll-tax contributions of current workers; accounting and reporting functions pertaining to the Trust Fund; decisions surrounding eligibility criteria; the benefit designs and pricing of Part A (hospitalization) and Part B (optional out-patient medical coverage, including drugs administered by a physician); approval of provider plan designs and pricing under Parts C; regulation and oversight of all other aspects of Medicare, including processes managed by private administrative contractors and providers of optional coverage; and regulation of health care providers.

The Independent Payment Advisory Board (IPAB) was created under the Affordable Care Act (ACA), aka Obamacare, to achieve Medicare costs savings under certain conditions, beginning in 2015. Its mandate is rather confusing, however, as IPAB is ostensibly restricted by the ACA from meddling with health care coverage and quality. Proposals from IPAB are expected to cover such areas as government negotiation of drug prices under Part D, a Part B formulary, restrictions on the “protected status” of certain drugs, and increasing incentives for diagnostic coding for Part C plans. Note that these steps are confined to optional or already-private parts of Medicare. They are extensions of the administrative and regulatory functions described above. Despite the restrictions on IPAB’s activities under the ACA, these steps would have an impact on coverage and quality, and they mostly involve functions for which market solutions are better-suited than one-size-fits-all regulatory actions.

The opportunities for privatization are in 1) creating more choice and flexibility in Parts A and B, or simply migrating them to Parts C and D, along with premium support; 2) eliminating regulatory burdens, including the elimination of IPAB.

Impacts On Seniors Now and Later

Privatization is unlikely to have any mandatory impact on current or near-future Medicare beneficiaries. That it might is a scare story circulating on social media (i.e., fake news), but I’m not aware of any privatization proposal that would make mandatory changes affecting anyone older than their mid-50s. Voluntary benefit choices, such as Part C and D plans, would be given more emphasis.

There should be an intensive review of the regulatory costs imposed on providers and, in turn, patients. Many providers simply refuse to accept patients with Medicare coverage, and regulation encourages health care delivery to become increasingly concentrated into large organizations, reducing choices and often increasing costs. Lightening the regulatory burden is likely to bring immediate benefits to seniors by improving access to care and allowing providers to be more patient-focused, rather than compliance-focused.

Again, the most heavily privatized parts of Medicare are obviously quite popular with seniors. The benefits are also provided at lower cost, although the government pays the providers of those plans extra subsidies, which may increase their cost to taxpayers. Enrollees should be granted more flexibility through the private market, including choices to limit coverage, even down to catastrophic health events. Consumers should be given at least limited control over the funds used to pay their premia. That would include choice over whether to choose lower premia and put the excess premium support into consumer-controlled Health Saving Account (HSA) contributions.

Other Reforms

Pricing is a controversial area, but that’s where the terms of mutually beneficial trades are made, and it’s what markets do best. Pricing flexibility for private plans would be beneficial from the standpoint of matching consumer needs with the appropriate level of coverage, especially with fewer regulatory restrictions. Such flexibility need not address risk rating in order to have beneficial effects.

Regulations imposed on physicians and other providers should be limited to those demanded by private plans and the networks to which they belong, as well as clear-cut legislative rules and standards of practice imposed by professional licensing boards. The better part of future contributions to the Trust Fund by younger workers (i.e., those not grandfathered into the existing program) should be redirected toward the purchase today of future benefits in retirement, based on actuarial principles.

Perhaps the best cost-control reform would be repeal of the tax deductibility of insurance premia on employer-paid insurance plans. This provision of the tax code has already inflated health care costs for all consumers, including seniors, via demand-side pressure, and it has inflated their insurance premia as well. If extended to all consumers, tax deductibility would be less discriminatory toward consumers in the individual market and most seniors, but it would inflate costs all the more, with unevenly distributed effects. Unfortunately, rather than eliminating it entirely, qualification for the tax deduction is very likely to be broadened.

Conclusions

The Medicare program is truly in need of an overhaul, but reform proposals, and especially proposals that would put decision-making power into the hands of consumers, are always greeted with reflexive shrieks from sanctimonious worshippers of the state. The most prominent reform under consideration now would offer more of what’s working best in the Medicare program: private choices in coverage and costs. Solving the long-term funding issues will be much easier without a centralized regime that encourages escalating costs.

Earning a profit is usually the mark of a job well done. It is compensation for the use of capital and the assumption of risk (i.e., no bailouts). Physicians, nurses, chiropractors, insurance agents and customer service reps all earn compensation for their contributions. Providers of capital should too, including the owners of health insurance companies who do well by their customers. And if you think the absence of profit in the public sector creates value, remember the damage inflicted by taxes. Capital isn’t “free” to society just because it can be confiscated by the government.

The Western U.S. is dealing with its water crisis in a variety of ways, but the most promising solutions, and the least draconian, involve the creation of water ownership rights and markets in which they can be traded. This recent Vox interview with John Fleck, author of “Water Is for Fighting Over“, emphasizes the dramatic reductions in usage that have taken place over the past few decades. Unmentioned, however, is that without correct price incentives, much of this adaptation involves unnecessary costs. Many users are forced to restrict water use via coercive rules. Even when conservation entails the installation of relatively simple technologies like low-flow toilets and less water-intensive landscaping, mandates do not encourage water to flow to its highest-valued uses. Mandates force conservation on all uses regardless of the efficiency with which it can be accomplished, leading to higher costs. Of course, droughts induce changes in agricultural usage as well (and reduce yields), but those changes are always suboptimal to the extent that real price incentives for a crucial input are absent.

Fleck is highly supportive of a few cases of water trading within and between certain irrigation districts. Despite these cases, however, water is priced too low in most jurisdictions to reflect its actual scarcity, and the adjustments that do occur are generally indiscriminate in terms of economic efficiency.

The only way to bring rationality to water use is for all parties to have an interest in its long-term sustainability. Markets can do that much better than collective action or forms of regulation instigated by the state. But for markets to work, traders must have a secure right in the thing being traded. Water rights are controversial, to say the least. Some basics of water rights are discussed briefly in this review of a book called “Water Capitalism: The Case for Privatizing Oceans, Rivers, Lakes, and Aquifers“, by Walter Block and Peter Nelson.

First, the riparian system, which works only when water is plentiful:

“‘The concept is that ownership of the adjacent land includes the riparian zone [the water frontage zone, i.e. shore] … typically to the centerline (unless he has holdings on both sides …) as well as the water [itself]. Pure riparian ownership gives the proprietor the privilege of drawing water … as long as there is any [to draw]’“

The in-toto system requires that any body of water, or any independent source of water, be owned by one entity, whether that is an individual, a cooperative, or a corporation. In such a world, owners of water assets would have an economic interest in good stewardship, and would charge rates that would effectively limit drawdowns to a sustainable flow. That is the only way to preserve the long-term value of their asset. However, the idea of an “independent” source of water is often problematic or even superfluous, as many or even most sources of water are dependent on others to one degree or another.

The prior appropriation system of water rights is described by Peter Nelson in this quote:

“‘This type of ownership both involves the water and measures it. The first user constructed the device(s) necessary to utilize and/or divert what he needed. In so doing, he mixed his labor with a natural resource. But what exactly does he own? It is not geometric in nature. The flow of water is what he possesses.’“

In some respects, prior appropriation is similar to the concept of squatter’s rights. However, the author of the book review linked above, Ryan Griggs, claims that ownership in a rate of flow, a usage right, is fundamentally different than a property right. I disagree. There are other forms of property that constitute claims to future flows of income, such as shares of stock or bonds held in perpetuity, and those flows are valued and traded as property. In any case, I’m not sure why ownership in a rate of usage is problematic from the perspective of the resource allocation problem at hand.

Prior appropriation is a convenient way of addressing the problem of vesting users with rights. Those rights would necessarily be attached to the land or area on which usage occurs, rather than portable for users, but I will continue to refer to “users” in what follows, rather than “places”. To simplify, suppose that each user owns an annual allotment of water as a percentage of total availability. If total availability fluctuates, some users will find it easier than others to adjust their usage. Individual users would receive their allotments based on prior use. They would pay a fee for the infrastructure and technology needed to extract and distribute water to them, and they would pay an additional rate per unit for water used above their allotment. If they use less than their allotment, they receive a rebate at the same rate per unit (or a “feebate“, a term sometimes used in conservation circles). Thus, users are given a conservation incentive.

In a low-water year when total availability is down, the price of usage will rise as users requiring more water than allotted bid on the available supplies. Those able to adjust their usage downward might find it profitable take “feebates”, in effect selling part of their allotment to other users. In this sense, water will flow to those uses in which its value is highest. The price of these trades will reflect the actual scarcity of the resource, and the higher price leads to more intensive conservation efforts. In fact, depending on the going rate, it’s possible for a user to become a net water seller, in term of monetary value, in a given period. It is also possible to arrange trades of longer-term water transfers, future water transfers, and even contingent water transfers.

The initial allotments are relatively easy to measure, though the details surrounding the measurement of historical usage must be agreed upon. However, future adjustments must be based on changes in total availability. How is that measured? A first step is to determine the extent to which total water supply is above or below a range deemed acceptable from a natural perspective. This, in turn, depends upon the annual rate at which the stock is recharged or replenished from natural sources. These data allow the calculation of a flow of usage each year that is consistent with moving toward the acceptable range for the water level. Depending on initial conditions, the allotments might require adjustments in usage in subsequent years, but that depends on the type of water source and the response of usage to the new conservation incentive. The path to “sustainable” allocations might have to be gradual, requiring several years. This might also require water authorities to purchase flows from other basins to bridge the gap, with the cost passed on to users in the marginal water rate (and reflected in feebates to the suppliers).

This might sound suspiciously like a “cap and trade” system because that’s exactly what it is. The determination of the initial allotments is a relatively benign exercise. The process for determining later adjustments is described above as a strictly technological problem, but in truth, it would be fraught with controversy, requiring a series of of political compromises. Battles over changes to allotments are likely to recur during periods of severe drought. This has been the case in Australia, for example, where the development of water markets is at a fairly advanced stage.

Australia succeeded in developing extensive water markets in response to the severe scarcity faced by farmers and other users in certain water basins. The National Water Commission published this report on water markets in 2011, which provides something of a blueprint for their system. These markets are primarily for water used in irrigation. The details of allotments in Australia are discussed in the report. No feebate system as described above is mentioned. Their water markets are now overseen by the Department of Agriculture and Water Resources. There are water brokers and exchanges to facilitate trading. WaterExhange and Waterfind provide on-line platforms for water trades. This Reuters article from September 2015 is of interest for its description of how water markets can become highly politicized under certain circumstances. This recent Bloomberg piece makes essentially the same point.

Regardless of the political complexities, the growing scarcity of water in the American West demands innovative new approaches to conservation. Creating secure rights in water flows and allowing users to engage in mutually beneficial trades of water gives them the right incentives for rational water management. Traditional approaches such as usage restrictions, mandates, and large water storage infrastructure projects are all costly and do not promote the efficiencies that come naturally by way of market solutions.

In general parlance, an entitlement is a thing to which one is entitled. If you have paid into Social Security (FICA payroll “contributions”), you should feel entitled to receive benefits one day. Why do I so often hear indignant complaints about the use of the term “entitlement” when applied to Social Security and Medicare? I’ve heard it from both ends of the political spectrum, but more often from the Left. It is usually accompanied by a statement about having “paid for those benefits!”. Exactly, you should feel entitled to them. You are not asking society to pay you alms!

Yet there seems to be resentment of an imagined implication that such “entitlements” are equivalent to “welfare” of some kind. That might be because the definition of an entitlement is somewhat different in the federal budget: it is a payment or benefit for which Congress sets eligibility rules with mandatory funding, as contrasted with discretionary budget items with explicit approval of funding. Because payments are based solely on eligibility, Social Security, Medicare and many forms of welfare benefits are all classified as entitlements in the federal budget. Obviously, those complaining about the use of the term in connection with Social Security believe there is a difference between their entitlement and welfare. But as long as they are willing to leave their “contributions” and future eligibility in the hands of politicians, their claim on future benefits is tenuous. Yes, you will pay FICA TAXES, and then you might be paid benefits (alms?) if you are eligible at that time. Certainly, the government has behaved as if the funds are fair game for use in the general budget.

Having made that minor rant, I can get to another point of this post: the Social Security retirement system offers terrible returns for its “beneficiaries”. Furthermore, it is insolvent, meaning that its long-term promises are, and will remain, unfunded under the current program design. However, there is a fairly easy fix for both problems from an economic perspective, if not from a political perspective.

The chart at the top of this post shows that Social Security benefits paid to eligible retirees are less than the payroll taxes those same individuals paid into the system. The chart is a couple of years old, but the facts haven’t changed. It’s boggling to realize that you’ll receive a negative return on the funds after a lifetime of “contributions”. That kind of investment performance should be condemned as unacceptable. However, you should know that the program is not “invested” in your retirement at all! Social Security’s so-called “trust fund” is almost a complete fiction. Most FICA tax revenue is not held “in trust”. Instead, it is paid out as an intergenerational transfer to current retirees. In the past, any surplus FICA tax revenue was invested in U.S. Treasury special purpose bonds, which funded part of the federal deficit. Here is a fairly good description of the process. The article quotes the Clinton Office of Management and Budget in the year 2000:

“These balances are available to finance future benefit payments … only in a bookkeeping sense. They do not consist of real economic assets that can be drawn down in the future to fund benefits. Instead, they are claims on the Treasury that, when redeemed, will have to be financed by raising taxes, borrowing from the public, or reducing benefits, or other expenditures.“

Unfortunately, for the past few years, instead of annual surpluses for the trust fund, deficits have been the rule and they are growing. Retiring baby boomers, longer life expectancies, slow income growth and declining labor force participation are taking a toll and will continue to do so. Something will have to change, but reform of any kind has been elusive. An important qualification is that almost any reform would have to be phased in as a matter of political necessity and fairness to current retirees. Unfortunately, just about every reform proposal I’ve heard has been greeted by distorted claims that it would harm either current retirees or those nearing retirement. In fact, leaving the program unaltered is likely to be a greater threat to everyone down the road.

There are three general categories of reform: higher payroll taxes, lower benefits, and at least partial privatization. Tax increases have obvious economic drawbacks, while straight benefit reductions would be harmful to future recipients even if that entailed means testing: the return on contributions is already negative, especially at the upper end of the income spectrum. Michael Tanner discusses specific options within each of these categories, including raising the normal and early retirement ages. None of the options close the funding gap, but at least higher retirement ages reflect the reality of longer life expectancies.

Early in his presidency, the George W. Bush administration offered a reform plan involving no tax increases or benefit cuts. Instead, the plan would have offered voluntary personal accounts for younger individuals. Needless to say, it was not adopted, but it would have kept the system in better shape than it is today. The key to success of any privatization is that unlike the Social Security Trust Fund, workers with private accounts can earn market returns on their contributions, which are in turn reinvested, allowing the accounts to grow faster over time. Tanner notes that 20 other countries have moved to private accounts including Chile, Australia, Mexico, Sweden, Poland, Latvia, Peru, and Uruguay. This sort of change does not preclude a separate social safety net for those who have been unable to accumulate a minimum threshold of assets, as Chile has done. Tanner’s article lays out details of a tiered plan that would allow participants a wider range of investments as their accumulated assets grow.

Economic research suggests that participants do not place a high value on their future benefits. From a 2007 National Bureau of Economic Research (NBER) paper by John Geanakoplos and Stephen Zeldes entitled “The Market Value of Social Security“:

“We find that the difference between market valuation and ‘actuarial’ valuation is large, especially when valuing the benefits of younger cohorts. … The market value of accrued benefits is only 2/3 of that implied by the actuarial approach.“

An implication is that younger workers who have already made contributions could be offered the choice of a future lump sum that is less than the actuarial present value of their benefits when they become eligible. Such a program could cut the long-term funding gap significantly, if the results found by Geanakoplos and Zeldes can be taken at face value, though it could create additional short-term funding pressure at the time of payment.

“Our first finding is that nearly three out of five respondents favor the lump-sum payment if it were approximately actuarially fair, a finding that casts doubt on several leading explanations for why more people do not annuitize. Second, there is some modest price sensitivity and evidence consistent with adverse selection; in particular, people in better health and having more optimistic longevity expectations are more likely to choose the annuity. Third, after controlling on education, more financially literate individuals prefer the annuity. Fourth, people anticipating future Social Security benefit reductions are more likely to choose the lump-sum, suggesting that political risk matters.“

Moreover, lump sums may offer an additional advantage from a funding perspective: a 2012 paper from the Michigan Retirement Research Center at the University of Michigan by Jingjing Chai, Raimond Maurer, Olivia S. Mitchell and Ralph Rogalla called “Exchanging Delayed Social Security Benefits for Lump Sums: Could This Incentivize Longer Work Careers?” found that “... workers given the chance to receive their delayed retirement credit as a lump sum payment would boost their average retirement age by l.5-2 years.”

Certainly, it would be difficult for private accounts to fare as badly in terms of returns on contributions than the system has managed to date. The future appears even less promising without reform. There are several advantages to privatization of Social Security accounts beyond the likelihood of higher returns mentioned above: it would avoid some of the labor market distortions that payroll taxes entail, and it would increase the pool of national savings. Perhaps most importantly, over time, it would release the assets (and future benefits) accumulated by workers from the clutches of the state and self-interested politicians. They are not entitled to pursue their political ends with those assets; they are yours!