The world doesn’t ordinarily revolve around tariffs, but so much has happened to make tariffs into an economic and political linchpin of the moment. Donald Trump put them in the spotlight, of course, and while he’s still seeing roses, things won’t turn out entirely the way he hopes. At the tariff levels he’s instituted, this shouldn’t be too surprising.

While tariff revenue is helping to shave the federal budget deficit, the tax falls largely on the backs of American consumers and businesses with all the attending distortions that entails. Sadly, the extra revenue also seems to have offered a handy excuse to put spending cuts on the back burner. Tariffs and tariff uncertainty have businesses attempting to compromise between reduced margins and price hikes. Thinning margins due to tariffs have played a role in the weak employment numbers we’ve seen over the past few months. And tariffs, at least until now, have quite rightly reinforced the Federal Reserve’s cautious stance toward easing policy. However, the weak labor market has likely convinced the Fed to cut its short-term interest rate target, despite inflation stubbornly remaining well above the Fed’s 2% objective. That upward price pressure will remain.

Now, the legal battle over Trump’s tariff authority is about to reach a climax. That’s what I’ll focus on here. The Supreme Court has agreed to fast track the challenge to the President’s discretion to impose retaliatory tariffs unilaterally. There are two cases at hand: V.O.S. Selections, Inc. v. Trump, and Learning Resources, Inc., et al. v. Donald Trump et al. In both cases, small business plaintiffs contend that Trump’s invocation of the International Emergency Economic Powers Act (IEEPA) is unwarranted, and that “most” of the tariff actions taken by Trump have usurped Congress’ power of the purse under Article I of the Constitution. Here’s Ilya Somin, who is a Volokh Conspiracy regular and one of the attorneys representing the plaintiffs:

“… IEEPA doesn’t even mention tariffs and has never previously been used to impose them, that there is no ‘unusual and extraordinary threat’ of the kind required to invoke IEEPA, the major questions doctrine, the constitutional nondelegation doctrine, and more.“

This isn’t the first time a U.S. president has imposed tariffs unilaterally, but it is easily the most drastic such action. Historically, nearly all tariffs were levied by acts of Congress. Prior to Trump II, perhaps the broadest tariff imposed by a President was Richard Nixon’s brief 10% surcharge on all imports, but that was lifted quickly. Presidents Johnson and Obama imposed some selective tariffs. All of these episodes seem piddling compared to Trump’s tariffs, which are both sweeping and in many cases painfully selective.

Eric Boehm notes that when it comes to major constitutional questions, the Court has taken the position that

“… executive power should be construed narrowly, not broadly …. Rather than tying itself into knots to affirm nearly unlimited executive powers over commerce, the Supreme Court should tell the Trump administration to get permission from Congress before imposing new tariffs.“

I believe that will be the general shape of the outcome here. Maybe there’s a way for the Court to allow the tariffs to stand until Congress decides to “man up”, acting one way or the other. SCOTUS would probably like to do just that! Or maybe the Court could stay the lower court’s injunction until the case is heard by the Court in full on the regular docket, or until Congress acts.

There’s a decent chance, however, that Trump’s tariffs will be struck down, leaving it up to tariff supporters in Congress to lay down statutory rules rather than put up with the impulsive craziness we’ve witnessed thus far. If the Court lets the tariffs stand, it leaves the door open for new tests on the limits of executive discretion. Here is Greg Ip at the link:

“There would also be no end to uncertainty. ‘Unlike most other tariff authorities, these tariffs are not enshrined in statute, there’s no process to change them, and they can change very rapidly, in a day, without much notice, as we’ve seen,’ said Greta Peisch, a trade attorney at Wiley Rein and former general counsel for the U.S. trade representative.“

We’ve already seen strong hints that the Administration would like to force businesses to eat the cost of the tariffs rather than pass them along to consumers in higher prices. There hasn’t been any formal action of this kind by the Administration, at least not yet. Still, one can hardly blame businesses who might perceive an implicit threat if they fail to comply. That kind of bullying represents an a massive abuse of power. The Court could do everyone a big favor by clarifying that the authority to impose tariffs rests with Congress.

Since his inauguration, Donald Trump has been busy finding ways for the government to extort payments and ownership shares from private companies. This has taken a variety of forms. Tad DeHaven summarizes the major pieces of booty extracted thus far in the following bullet points (skipping the quote marks here):

June 13: Trump issues an executive order allowing the Nippon Steel-US Steel deal contingent on giving the government a “golden share” that enables the president to exert extensive control over US Steel’s operations.

July 10: The Department of Defense (DoD) unveils a multi-part package with convertible preferred stock, warrants, and loan guarantees, making it the top shareholder of rare earth metals producer MP Materials.

July 23: The White House claims an agreement with Japan to reduce the president’s so-called reciprocal tariff rate on Japanese imports comes with a $550 billion Japanese “investment fund” that Trump will control.

July 31: Trump claims an agreement with South Korea to reduce the so-called reciprocal tariff on South Korean imports comes with a $350 billion South Korean-financed investment in projects “owned and controlled by the United States” that he will select.

August 12: In a Fox Business interview, Bessent points to the alleged investments from Japan, South Korea, and the EU “to some extent” and says, “Other countries, in essence, are providing us with a sovereign wealth fund.”

August 22: Fifteen days after calling for Intel CEO Lip-Bu Tan to resign, Trump announces that the US will take a 10 percent equity stake in Intel using the CHIPS Act and DoD funds, becoming Intel’s largest single shareholder.

Each of these “deals” has a slightly different back story, but national security is a common theme. And Trump says they’ll all make America great again. They are touted as a way for American taxpayers to benefit from the investment he claims his policies are attracting to the U.S. However, all of these are ill-advised for several reasons, some of which are common to all. That includes the extortionary nature of each and every one of them.

Short Background On “Deals”

The June 13 deal (Nippon/US Steel), the July 10 deal (MP Materials), and the August 22 deal (Intel) all involve U.S. government equity stakes in private companies. The August 11 deal (NVIDIA/AMD) diverts a stream of private revenue to the government. The July 23 and July 31 deals (Japan and South Korea) both involve “investment funds” that Trump will control to one extent or another.

The August 12 entry adds “expected” EU investments with some qualification, but that bullet quotes Treasury Secretary Bessent referring to these investments as part of a sovereign wealth fund (SWF). Secretary of Commerce Lutnick now denies that an SWF will exist. My objections might be tempered slightly (but only slightly) by an SWF because it would probably need to place constraints on an Administation’s control. That might give you a hint as to why Lutnick is now downplaying the creation of an SWF.

I object to the Nippon/US Steel “deal” in part (and only in part) because it was extortion on its face. There is no valid anti-trust argument against the deal (US Steel is the nation’s third largest steelmaker and is broke), and the national security concerns that were voiced (Japan! for one thing) were completely bogus. Even worse, the “Golden Share” would give the federal government authority, if it chose to exercise it, over a variety of the company’s decisions.

The Intel “deal” is another highly questionable transaction. Intel was to receive $11 billion under the CHIPS Act, a fine example of corporate welfare, as Veronique de Rugy once described the law. However, Intel was to receive its grants only if it stood up four fabrication facilities. But it did not. Now, instead of demanding reimbursement of amounts already paid, the government offered to pay the remainder in exchange for a 9.9% stake in the company. And there is no apparent requirement that Intel meet the original committment! This could turn out a bust!

The MP Materials transaction with the Department of Defense has also been rationalized on national security grounds. This excuse comes a little closer to passing the smell test, but the equity stake is objectionable for other reasons (to follow).

The Nvidia/AMD deal has been justified as compensation for allowing the companies to sell chips to China, which is competing with the U.S. to lead the world in AI development. This is another form of selective treatment, here applied to an export license. The chips in question do not have the same advanced specifications as those sold by the companies in the U.S., but let’s not let that get in the way of a revenue opportunity.

While nothing about TikTok appears on the list above, I fear that a resolution of its operational status in the U.S. presents another opportunity for extortion by the Trump Administration. I’m sure there will be many other cases.

Root Cause: Protectionism

The so-called investment funds described in the timeline above are nearly all the result of trade terms negotiated by a dominant and belligerent trading partner: the U.S. My objections to tariffs are one thing, but here we are extorting investment pledges for reductions in the taxes we’ll impose on our own citizens! Additionally, the belief that these investments will somehow prevent a general withdrawal of foreign investment in the U.S. is misguided. In fact, a smaller trade deficit dictates less foreign investment. The difference here is that the government will wrest ownership control over a greater share of less foreign investment.

Trump the Socialist?

Needless to say, I don’t favor government ownership of the means of production. That’s socialism, but do matters of national security offer a rationale for public ownership? For example, rare earth minerals are important to national defense. Therefore, it’s said that we must ensure a domestic supply of those minerals. I’m not convinced that’s true, but in any case, fat defense contracts should create fat profit opportunities in mining rare earths (enter MP Materials). None of that means public ownership is necessary or a good idea.

All of these federal investments are construed, to one extent or another, as matters of national security, but that argument for market intervention is much too malleable. Must we ensure a domestic supply of semiconductors for national security reasons? And public ownership? Is the same true of steel? Is the same true of our “manufacturing security”? It can go on and on. The next thing you know, someone will argue that grocery stores should be owned by the government in the name of “food security”! Oh, wait…

Trump the Central Planner

Government ownership takes the notion of industrial planning a huge step beyond the usual conception of that term. Ordinarily, when government takes the role of encouraging or discouraging activity in particular industries or technologies, it attempts to select winners and losers. The very idea presumes that the market is not allocating resources in an optimal way, as if the government is in any position to gainsay the decisions of private market participants who have skin in the game. This is a foolhardy position with predictably negative consequences. (For some examples, see the first, second, and fourth articles linked here by Don Boudreaux.) The fundamental flaw in central planning always comes down to the inability of planners to collect, process, and act on the information that the market handles with marvelous efficiency.

When government invests taxpayer funds in exchange for ownership positions in private concerns, the potential levers of control are multiplied. One danger is that political guidance will replace normal market incentives. And as de Rugy points out, the government’s potential role as a regulator creates a clear conflict of interest. In a strong sense, a government ownership stake is worse for private owners than a mere dilution of their interests. It looms as a possible taking, as private owners and managers surrender to creeping government extortion.

Financial Malfeasance

In addition to the objections above, I maintain that these investments represent poor stewardship of public funds. The U.S. public debt currently stands at $37 trillion with an entitlement disaster still to come. In fact, according to one estimate, the federal government’s total unfunded obligations amount to additional $121 trillion! Putting aside the extortion we’re witnessing, any spare dollar should be put toward retiring debt, rather than allowing its upward progression.

As I’ve noted before, paying off a dollar of debt entails a risk-free “return” in the form of interest cost avoidance, let’s say 3.5% for the sake of argument. If instead the dollar is “invested” in risk assets by the government, the interest cost is still incurred. To earn a net return as high as the that foregone from interest avoidance, the government must consistently earn at least 7% on its invested dollar. But of course that return is not risk-free!

A continuing failure to pay down the public debt will ultimately poison the debt market’s assessment of the government’s will to stay within its long-run budget constraint. That would ultimately manifest in an inflation, shrinking the real value of the public debt even as it undermines the living standards of many Americans.

One final thought: Though few MAGA enthusiasts would admit it even if they understood, we’re witnessing a bridging of two ends of the idealogical “horseshoe”. Right-wing populism and protectionism meet the left-wing ideal of central planning and public ownership. There is a name for this particular form of corporatist state, and it is fascism.

The federal government ran a budget surplus of $27 billion in June, much to the surprise of nearly everyone. The Trump Administration and MAGA-friendly media were eager to credit a big revenue boost from higher tariffs, which… ahem … they have assured us are notreally taxes. In any case, to attribute the June surplus to tariffs is flatly ridiculous. The truth is these “non-tax” magic revenue generators made a relatively small contribution to the apparent shift in the government’s fiscal position in June. And I say “apparent” because the surplus itself was something of a mirage.

Yes, tariffs brought in a total of almost $27B during June, which is about the same as the surplus recorded, but that was purely coincidental. It does not imply that tariffs “created” a surplus. Nor does it suggest that tariffs might just be able to balance the federal budget. Not a chance!

Here is one of two other sides of the story: the Treasury reported that the budget balance this June improved from a year ago by a total of $89 billion, from a deficit of $72B in June of 2024 to the aforementioned surplus of $27B in June 2025. Outlays were lower by about $38B this June, accounting for almost 43% of the improvement. Receipts were about $59B higher, with tariffs increasing by $20B relative to June 2024. So tariffs contributed just over a third of the boost in receipts. Altogether then, tariffs accounted for 22.5% of the improvement in the June budget balance between 2024 and 2025. That version of the story, as far as it goes, does not support the contention that tariffs “caused” the budget surplus in June, only that tariff revenue was a contributing factor.

Let’s dig a little deeper, however. Were it not for so-called “calendar adjustments” made by the Treasury, it would have reported a deficit of $70B in June. The reason? The first day of June fell on a Sunday this year, socertain payments were shifted to the last prior business day: Friday, May 30. That reduced June outlays substantially. Moreover, an extra business day in June 2025 added revenue. So the surplus in June was, in essence, an artifact of the calendar and had little to do with tariff revenue.

Incidentally, no one should be surprised by the growth of tariff revenue collected in June. When a tax rate more than triples (from a pre-Trump average of about 3% to 10% plus in June — net of tariff exclusions), one should expect revenue from that tax to increase substantially (and it was probably exaggerated by the extra business day).

Oh wait! Did I say tax?

With time, buyers will adjust and scale back their import purchases, reducing the revenue impact of the tariff hikes. However, we still don’t know how high tariffs will go. That means we could see substantially higher tariff revenue, though the demand response and a likely negative impact on incomes will cut into those gains. Either way, the revenue potential of tariffs is limited. Some estimates put the revenue impact of Trump’s tariffs at less than $250B annually. That seems conservative, but it’s significant revenue if it holds up. Still, it won’t come close to balancing a federal budget that’s almost $2 trillion in the hole. It certainly doesn’t justify a headlong dive into protectionism, which amounts to taking a crap on the economic freedom and prosperity of the American public.

Supporters of President Trump’s hard line on trade make so many false assertions that it’s hard to keep up. I’ve addressed several of these in earlier posts and I’ll address two more fallacies here: 1) that the U.S. manufacturing sector is in a state of crisis; and 2) that tariffs played a key role in promoting economic growth in the U.S. during the so-called gilded age of the late 19th and early 20th centuries.

Security

First, let’s revisit one tenet of protectionism: national security demands self-sufficiency. This undergirds the story that we must produce physical “things”, in addition to often higher-valued services, to be a great nation, or even to survive!

Of course, protecting industries critical to national security might seems like a natural concession to make, even for those supportive of liberalized trade. Ross Douthat says this:

“I think trying to reshore some manufacturing and decouple more from China makes sense from a national security standpoint, even if it costs something to G.D.P. and the stock market.“

Unfortunately, this kind of rationale is far too malleable. There is never a clearly defined limiting principle. Someone decides which goods are “critical” to national security, and this deliberation becomes the subject of much political jockeying and favor-seeking. But wait! Economic security is also cited as an adequate excuse for trade protections! And how about data security? Health security? Job security? Always there is insistence that “security” of one sort or another demands that we provide for our own needs. For definitive proof, take a look at this nonsense! Give them an inch and they’ll take a mile.

Pretty soon you “protect” such a wide swath of industries in a quest for self-sufficiency that the entire economy is unmoored from opportunity costs, comparative advantages, and the information about scarcities provided by market prices. Absolute “security” comes at the cost of transforming the economy’s productive machinery into a complacent hulk rivaling the inefficiency of Soviet industrial planning. Competition is the solution, but not limited to firms under the same set of protective trade barriers.

Manufacturing Is Mostly Fine

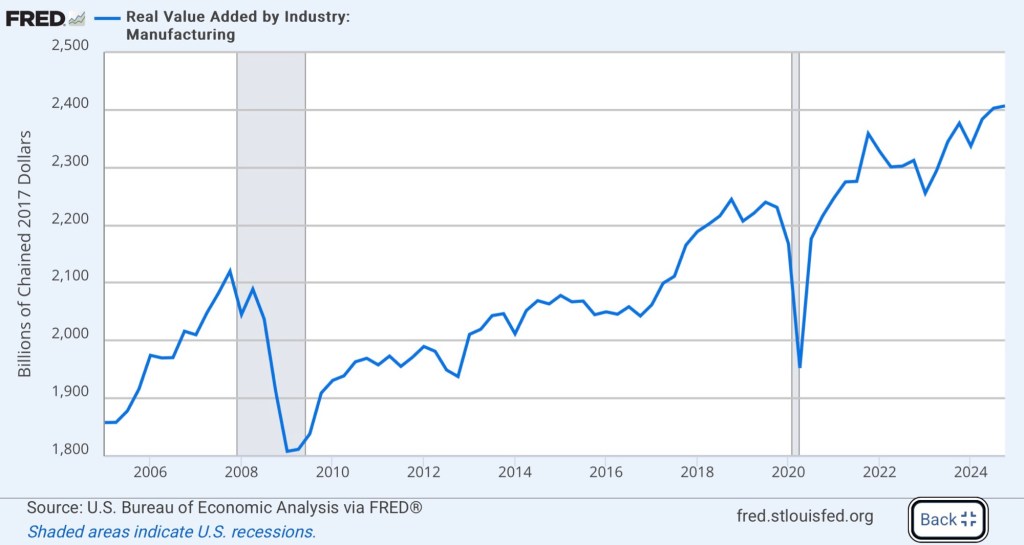

Trade warriors, including members of Trump’s team, insist that our decline as a nation is being hastened by a crisis in manufacturing. However, value added in U.S. manufacturing is at an all-time high.

There has been a long-term decline in manufacturing employment, but not manufacturing output. In fact, manufacturing output has doubled since 1980. As Jeff Jacoby notes, “the purpose of manufacturing is to make things, not jobs.” If our overarching social goal was job security, we’d have revolted long ago against the tremendous reduction in agricultural employment experienced over the past century. We’d rely on switchboard operators to load web pages, and we’d dig trenches and tunnels with spoons (to paraphrase Milton Friedman).

The secular decline in manufacturing employment is a consequence of growth in manufacturing productivity. Economy-wide, this phenomenon allows real income and our standard of living to grow.

Take That Job and …

It’s also significant that few Americans have much interest in factory work. It’s typically less dangerous than in times past, but many of today’s factory jobs are still physically challenging and relatively risky. Perhaps that helps explain why nearly half-a-million jobs in manufacturing are unfilled.

Jacoby describes the transition that has changed the face of American manufacturing:

“… US plants have largely turned away from making many of the low-tech, labor-intensive consumer items they once specialized in — sneakers, T-shirts, small appliances, toys. Those jobs have mostly gone overseas, and trying to bring them back by means of a trade war would be ruinous. Yet America remains a global manufacturing powerhouse — highly skilled, highly innovative, and highly efficient.“

And yet, even as wages in manufacturing have grown, many factory jobs do not pay as well as positions requiring far less strenuous toil in the services sector. It’s also true that the best manufacturing jobs in the U.S. today require high-level skills, which are in short supply. These factors help explain why manufacturers believe finding qualified workers is one of their biggest challenges.

Isolating Weak Sectors

There are specific sectors within manufacturing that have fared poorly, including textiles, furniture, metals, and low-end electronics. The loss of competitiveness that drove those sectoral declines is not a new development. It has, however, devastated communities in the U.S. that were heavily dependent on these industries. These misfortunes are regrettable, but trade barriers are not an effective prescription for revitalizing depressed areas.

Meanwhile, other manufacturing sectors have enjoyed growth, such as computers, aerospace, and EVs. While we’ve seen a decline in the number of manufacturing firms, theperformance of U.S. manufacturing in the 21st century can be described as mixed at the very worst.

The author of this piece seems to accept the false notion that U.S. manufacturing is moribund, but he knows tariffs aren’t an effective way to strengthen domestic goods production. He has a number of better suggestions, including a commitment to infrastructure investment, reforms to education and health, and reconfiguring certain corporate income tax policies. Unfortunately, his ideas on tariffs are sometimes as mistaken as Trump’s,

The Gilded Age

Finally, the other false assertion noted in the opening paragraph is that tariffs somehow spurred economic growth in the late 19th and early 20th centuries. Brian Albrecht corrects this protectionist fallacy, which lies at the root of many defenses of Trump’s tariffs. Albrecht cites favorable conditions for growth that were sufficient to overwhelm the negative effects of tariffs, including:

“… explosive population growth, mass European immigration, rapid technological innovation, westward expansion, abundant natural resources, high literacy rates, and stable property rights.”

While cross-country comparisons indicate a positive correlation between tariffs and growth during the 1870 – 1920 period, those differences were caused by other forces that dominated tariffs. Cross-industry research discussed by Albrecht indicates that tariffs on manufactured goods during the gilded era reduced labor productivity and stimulated the entry of smaller, less productive firms. Likewise, natural experiments find that tariffs allowed inefficient firms to survive and discouraged innovation.

Conclusion

The U.S. manufacturing sector is not in any sort of crisis, and its future growth won’t be powered by attempts to restore the sort of low-value production offshored over the past several decades. What protectionists interpret as failure is the natural progression of a technically advanced market-based civilization, where high-value services account for greater shares of growing total output. Of course, low-value production is sometimes “crowded out” in this process, depending on its trade-ability and comparative advantages. The logic of the process is encapsulated by Veronique de Rugy’s recent discussion of iPhone production (HT: Don Boudreaux):

“Then there’s [Commerce Secretary Howard] Lutnick, pining for a world where Americans flood back into massive factories to assemble iPhones. This is nostalgic industrial cosplay masquerading as economic strategy. Yes, iPhones aren’t assembled by Americans. But this isn’t a failure; it’s a feature of smart economic specialization. We design the iPhone here. That’s the high-value, high-margin part. The sophisticated chips, software, architecture, and intellectual property are all created in the U.S. The marketing is done here, too. That’s most of the value of the iPhone. The lower-value labor-intensive assembly work is done abroad because those tasks are more efficiently performed abroad.“

There is certainly no crisis in U.S. manufacturing. That narrative is driven by a combination of politics, rent seeking, and misplaced nostalgia.

First, a few more comments re: my speculative musings that Donald Trump’s tariff rampage could ultimately result in a regime with lower trade barriers, at least with a subset of trading partners. Arthur Laffer and Stephen Moore suggested last week that the White House should propose reciprocal free trade with zero barriers and zero subsidies for exports to any country that wishes to negotiate. A more cynical Ben Zycher scoffed at the very possibility, noting that Trump and his lieutenants view any trade deficit as evidence of cheating in one form or another. Zycher is convinced that Trump lacks a basic understanding of the (mostly) benign forces that drive trade imbalances.

I’ve said much the same. Trump’s crazy notions about trade could scuttle negotiations, or he might later accuse a trading partner of cheating on the pretext of a bilateral trade deficit (he’s done so already). And all this is to say nothing of the serious constitutional questions surrounding Trump’s tariff actions.

The mistaken focus on bilateral trade deficits also manifests in certain proposals made during trade negotiations: “Okay, but you’re gonna have to purchase vast quantities of our soybeans every year.” This sort of export promotion is a further drift into industrial planning, and it’s just too much for Trump’s trade negotiators to resist.

This might well turn out as an exercise in self-harm for Trump. However, I’ve also wondered whether his trade hokum is pure posturing, especially because he expressed support for a free trade regime in 2018. Let’s hope he meant it and that he’ll pursue that objective in trade talks. Please, just negotiate lower trade barriers on both sides without the mercantilist baggage.

Which brings me to the theme of this post: it would probably be simpler and more effective for the U.S. to simply drop all of its trade barriers unilaterally. There should be limited exceptions related to national security, but in general we should “turn the other cheek” and let recalcitrant trade partners engage in economic self-harm, if they must.

Okay, Wise Guy, What’s Your Plan?

I have a few friends who bemoan the lack of “fair play” against the U.S. in foreign trade. They have a point, but they also hold an unshakable belief that the U.S. can be just as efficient at producing anything as any other country. They are pretty much in denial that comparative advantages exist in the real world. They are seemingly oblivious to the critical role of specialization in unlocking gains from trade and lifting much of the world’s population out of penury over the past few centuries.

Furthermore, these friends believe that Trump is justified in “retaliating” against countries with whom the U.S. runs trade deficits. If tariffs are so bad, they ask, what would I do instead? Again, here’s my answer:

Eliminate (almost) all barriers to trade imposed by the U.S. Let protectionist nations choke themselves with tariffs/trade barriers.

Before getting into that, I’ll address one fact that is often denied by protectionists.

Yes, a Tariff Is a Tax!

Protectionists often claim that tariffs are not really taxes on U.S. buyers. However, tariffs are charged to buyers of imported goods (often businesses who sell imported goods to consumers or other businesses). In principle, tariffs operate just like a sales tax charged to retail buyers. Both raise government revenue, and they are both excise taxes.

In both cases, the buyer pays but generally bears less than the full burden of the tax. That’s because demand curves slope downward, so sellers (foreign exporters) try to avoid losing sales by moderating their prices in response to the tariff. In both cases, sellers end up shouldering part of the tax burden. How much depends on how buyers react to price: a steep (inelastic) demand curve implies that buyers bear the greater part of the burden of a tariff or sales tax.

People sometimes buy imports due to a lack of substitutes, which implies a steep demand curve. Consumer imports are often luxury items, and well-heeled buyers may be somewhat insensitive to price. Most imports, however, are inputs purchased by businesses, either capital goods or intermediate goods. In the face of higher tariffs, those businesses find it difficult and costly to arrange new suppliers, let alone domestic suppliers, who can deliver quickly and meet their specifications.

These considerations imply that the demand for imports is fairly inelastic (steeper), especially in the short run (when alternatives can’t easily be arranged). Thus, import buyers bear a large portion of the burden in the immediate aftermath of an increased tariff. By imposing tariffs we tax our own citizens and businesses, forcing them to incur higher costs. Correspondingly, if demand is inelastic, an importing country tends to gain more than its trading partners by unilaterally eliminating its own tariffs.

Tariffs on imports also trigger price hikes by import-competing producers. Sometimes this is opportunistic, but even these producers incur higher costs in attempting to meet new demand from buyers who formerly purchased imports. (See this post for an explanation of the costly transition, including a nice exposition of the waste of resources it entails.)

Other Forms of Blood Letting

Beyond tariffs, certain barriers to trade make it more difficult or impossible to purchase goods produced abroad. This includes import quotas and domestic content restrictions. These barriers are often as bad or worse than tariffs because they increase costs and encumber freedom of choice and consumer sovereignty.

Another kind of trade intervention, export subsidies, must be funded by taxpayers. Subsidies are too easily used to protect special interests who otherwise can’t compete. Currency manipulation can both subsidize exports and discourage imports, but it is often unsustainable. The common theme of these interventions is to undermine economic efficiency by shielding the domestic economy from real price signals.

Let Them Tax Themselves

Suppose the U.S. simply turns the other cheek, eliminating all of our own trade interventions with respect to country X despite X’s tariffs and other interventions.

To start with, the existence of barriers means that both countries are unable to exploit all of the benefits of specialization and mutually beneficial trade. Both countries must produce an excess of goods in which they lack a comparative advantage, and both countries produce too few goods in which they have a comparative advantage. Both incur extra costs and produce less output than they could in the absence of trade barriers.

Unilateral elimination of U.S. tariffs and other barriers would reduce high-cost domestic production of certain goods in favor of better substitutes from country X. But Country X gains as well, because it is now able to produce more goods and services for export in which it possesses a comparative advantage. Therefore, the unilateral move by the U.S. is beneficial to both countries.

On the other hand, U.S. export industries are still constrained by country X’s import tax or other restraints. These would-be exporters are no worse off than before, but they are worse off relative to a state in which buyers in country X could freely express their preferences in the marketplace.

What exactly does country X gain from tariffs and other trade burdens on its citizens? It denies them full access to what they deem to be superior goods and services at an acceptable price. It means that resources are misallocated, forcing abstention or the use of inferior or costlier domestic alternatives. Resources must be diverted to relatively inefficient firms. In short, the tariff makes country X less prosperous.

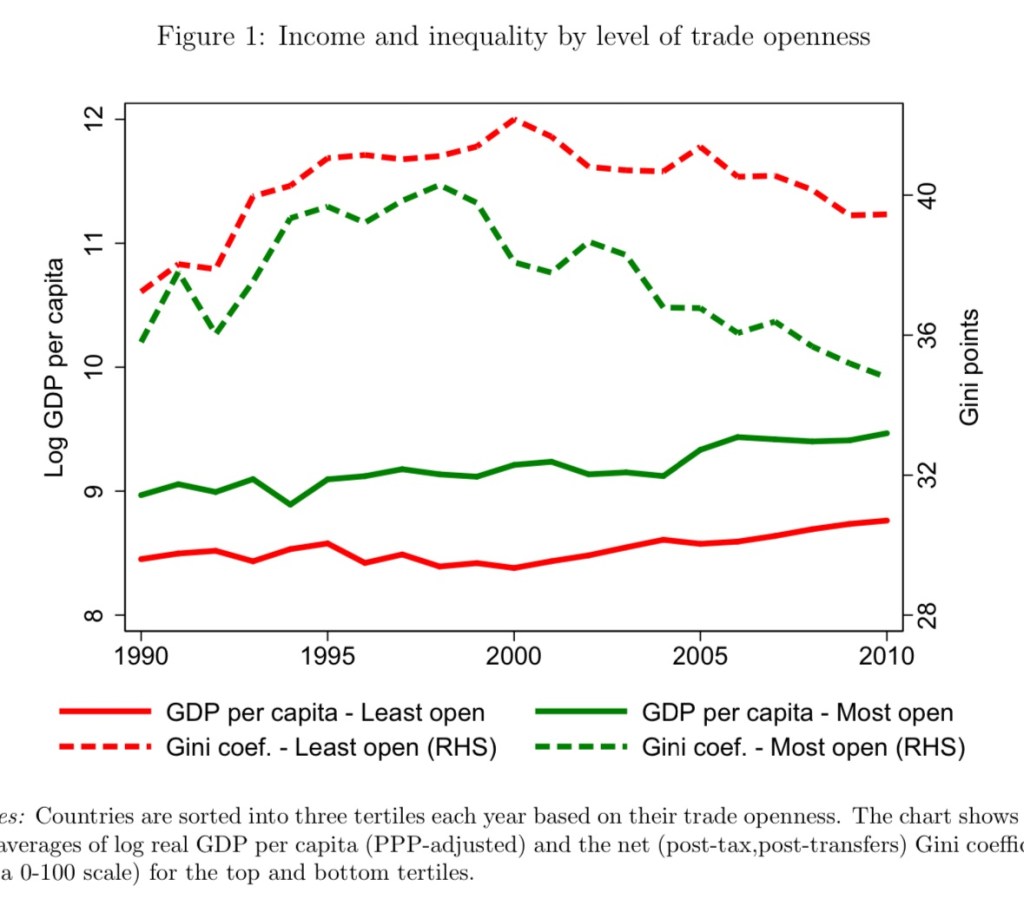

Empirical evidence shows that more open economies (with fewer trade barriers) enjoy greater income and productivity growth. This study found that “trade’s impact on real income [is] consistently positive and significant over time.”See this paper as well. Trade barriers tend to increase the income gap between rich and poor countries. The chart below (from this link) compares real GDP per capita from the top third and bottom third of the distribution of countries on a measure of trade “openness”. Converting logs to levels, the top third has more than twice the average real GDP per capita of the bottom third. And of course, the averaging process mutes differences between very open and very closed trade policies.

The chart also shows that countries more “open” to trade have more equal distributions of income, as measured by their Gini coefficients.

An important qualification is that domestic production of certain goods and services might be critical to national security. We must be willing to tolerate some inefficiencies in that case. It would be foolish to depend on a hostile nation for those supplies, despite any comparative advantage they might possess. It’s reasonable to expect such a list of critical goods and services to evolve with technological developments and changing security threats. However, merely acknowledging this justification leaves the door open for excessively broad interpretations of “critical goods”, especially in times of crisis.

Setting a Good Policy and Example

Here’s an attempt to summarize:

Tariffs are taxes, and non-tariff barriers inflict costs by distorting prices or diminishing choice

Trade barriers reduce economic efficiency and produce welfare losses

Trade barriers deny the citizens of a country the benefits of specialization

Both countries gain when one trading partner eliminates tariffs on imports from the other

The demand for imports is fairly inelastic, at least in the short run. Thus, the gain from eliminating a tariff will be skewed toward the domestic importers

Both countries gain when they agree to eliminate any and all trade barriers

Across countries, trade barriers are associated with lower incomes, lower income growth, and more unequal distributions of income

The U.S. has a large number of trading partners. Every liberalization we initiate means a welfare gain for us and one trading partner, who would do well to follow our example and reciprocate in full. Not doing so foregoes welfare gains and leads to incremental losses in income relative to more trade-friendly nations. Across all of our trading relationships, a unilateral end to U.S. trade barriers would almost certainly convince some countries to reciprocate. Those that refuse would suffer. Let them self-flagulate. Let them tax themselves.

Creative destruction takes place when inefficient producers are outcompeted by other firms, especially those brandishing new technologies. The concept, originally developed by Joseph Schumpeter in the 1940s, came to be accepted as a hallmark of market dynamics and capitalism. Successful market entrants rise to compete and eventually cripple incumbent producers who’ve grown stale in their offerings, inputs, or methods.

Creative destruction encourages long-term economic growth in several ways. First, it allows unproductive firms to fail, freeing resources to be absorbed by firms having solid growth opportunities. Second, creative destruction enables the diffusion of new technologies. Third, it motivates incumbents to improve their game, adapting to new realities in the marketplace. This is a continuous process. There are always firms that fail to keep pace with their competitors, whether old-line producers or failing risk-takers, but this is especially the case during periods of economic weakness.

Harmful Policy Menu

Attempting to prevent creative destruction via public policy is counter-productive, anti-competitive, and it impedes economic growth. Yet we constantly expend well-meaning energies to short circuit the process by attempting to promote uneconomic technologies, shield established firms from competition, and resuscitate dying firms. These efforts include industrial policies, barriers to foreign trade, excessive regulation of new technologies, selective taxation, certain bankruptcy reorganizations, and outright bailouts.

Creative destruction is a sign of flourishing competition, but it is subverted by industrial policies that subsidize politically-favored firms that otherwise would be uncompetitive. These policies create artificial advantages that waste public resources on what are often just bad ideas (see here and here).

Likewise, protectionism breeds weakness while shielding domestic producers from competition. And selective taxes, such as those on online sales, create an uneven playing field, blunting competitive forces.

Policies that encourage the survival of “zombie firms” also thwart creative destruction. These are companies with chronic losses that manage to hang on, sometimes for many years, with refinanced debt. Companies and their lenders can expend a great deal of internal effort forestalling bankruptcy. However, it’s not uncommon for zombie firms to languish for years but ultimately fail even after bankruptcy reorganizations, especially when the sole focus is on financial restructuring rather than business operations.

Government sometimes steps in to prolong the survival of struggling firms via subsidies, loan guarantees, and protracted efforts to keep interest rates low. Bailouts of various kinds have become all too common. Bailout activity creates perverse incentives with respect to risk. It also wastes resources by propping up inefficient operators, trapping resources in uses that return less to society than their opportunity costs.

Macro Maleficence

Ben Landau-Taylor makes a provocative but sensible claim in an article entitled “Industrial Greatness Requires Economic Depressions”. It’s about an unfortunate side effect of government policies intended to stabilize the economy: business failures occur with greater frequency during economic contractions, and that’s when policymakers are most apt to render aid via expansionary fiscal and monetary actions. No one likes economic downturns and unemployment, so “stimulative” policy is easy to sell politically, despite its all-too-typical failures in terms of timing and efficacy (see here and here). One intent is to support firms whose travails are revealed by a weak economy, including those relying on obsolete technologies. It might buy them survival time, but on the public dime. Ultimately, by forestalling creative destruction, these policies undermine economic growth.

Landau-Taylor emphasizes that creative destruction is not costless. Business failures and job losses are painful. And creative destruction brought on by dramatic advances can actually cause recessions or even depressions. Is that a rationale for delaying the inevitable failure of weak incumbents and impeding the broad adoption of new technologies? Our long-term well-being might dictate that we allow such transitions to take place by shunting aside interventionist temptations.

As a rationale for intervention, it’s sometimes said that we can’t regain the output lost during contractions. An appropriate riposte is that government efforts to counter recessionary forces are almost always futile. Furthermore, the lost output might be a pittance relative to the growth and permanent gains made possible by allowing creative destruction to run its course, liberating resources for better opportunities and growth.

On this point, Landau-Taylor says:

“If we want our descendants in 2125 to surpass our living standards the way we surpass our ancestors from 1925, then we will have to permit economic transformations at the scale that our ancestors did, including bankruptcies, job losses, and the cascading depressions that result. The individual pain of depressions does not have to be quite so severe as it once was. Because we are richer, we can and do spend vastly more on welfare, but this should be directed at individuals rather than at megacorporations. But there will always be some pain.“

Conclusion

Too often public policy creates obstacles to natural and healthy market processes, including creative destruction. This prevents the economy from reaching its true growth potential. Subsidies, bailouts, protectionism, and arguably macroeconomic stimulus, too often give safe harbor to struggling producers who manage to retain control over resources having more valued uses, including firms relying on obsolete and impractical technologies. Recessions typically expose firms with the weakest market prospects, but countercyclical fiscal and monetary policy may give them cover, forestalling their inevitable decline. Thus, we risk throwing good resources after bad, foregoing opportunities for growth and a more prosperous future.

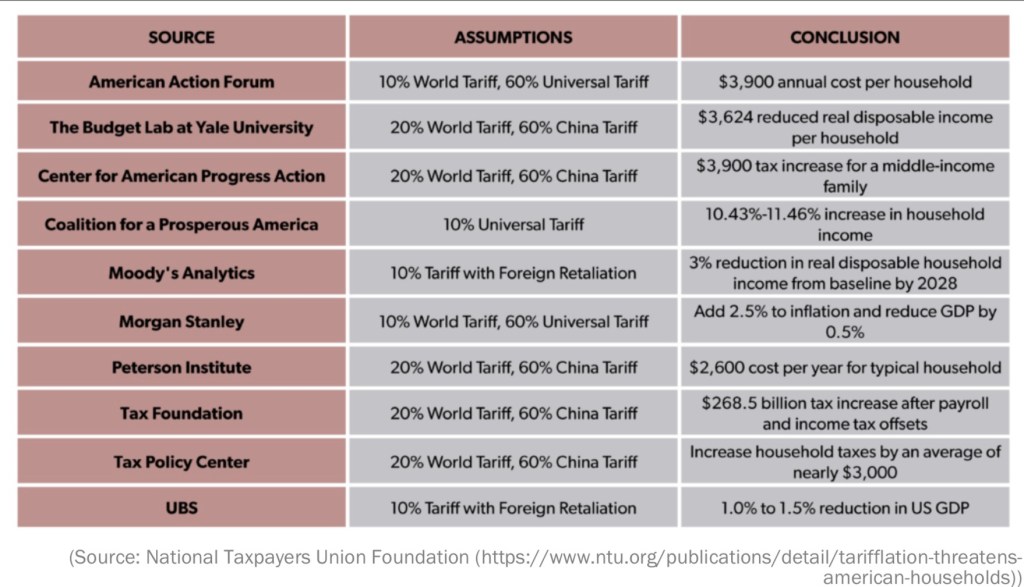

The table above is from Eric Boehm at Reason.com. It shows a variety of negative economic projections based on the likely imposition of tariffs by the incoming Trump Administration. Donald Trump’s protectionist agenda is motivated in large part by the notion that imports of foreign goods and services harm the U.S. economy. This misapprehension is common on both the populist left and the nationalist right, but it is also fueled by special interests averse to competition. Especially puzzling are those who extol the virtues of capitalism and free markets while claiming that free markets across borders are inimical to our nation’s economic interests.

Imports and Domestic Spending

Many assume that imports directly reduce GDP. In fact, on this point, some might be led astray by a superficial exposure to macroeconomics. As Noah Smith has noted, they might think back to the simple spending definition of GDP they learned as college freshmen:

GDP = C + I + G + (X – M),

where C is consumer spending on final goods and services, I is investment spending, G is government spending, X is foreign spending on U.S. exports, and M is U.S. spending on imports from abroad. So imports are subtracted! Doesn’t that mean imports directly reduce GDP?

The key here is to recognize that C, I, and G already include spending on imported goods. Therefore, imports must be subtracted from the spending totals to find the value spent on domestically-produced final goods and services. No, imports are not a direct, net subtraction from GDP.

Your Loathsome Foreign Car

Of course the domestic impact of imports goes deeper than this simple accounting framework. If someone decides to purchase an imported good instead of a close substitute produced domestically, what happens to GDP? If the decision has an immediate impact on production, then U.S. GDP declines. Otherwise, the domestic good is new inventory investment (part of I above), and there is no change. But if the import decision is repeated, the result is permanently lower U.S. GDP relative to the alternative, as producers won’t want to add to inventories indefinitely. The same is true if a domestic producer decides to purchase a component or raw material produced overseas rather than one produced at home.

The import decision causes a domestic producer to lose a sale along with the profit that sale would have earned. That puts pressure on the firm’s workers and wages as well. The firm still has the value of the unit in inventory, but if the import decision is repeated there will be more substantial follow-on effects on production, employment, spending, and saving.

Not So Fast

There is still more to the story, of course. By purchasing the foreign good,,which in the buyer’s estimation delivers greater value at that point in time, there is a gain in consumer surplus that is very real. To the buyer, that gain is perhaps equivalent to dollars in the bank. Their real wealth has increased relative to the surplus value of the foregone domestic purchase. This, too, will likely have follow-on effects in terms of spending and saving, but positive effects.

Therefore, to a first approximation, the immediate effects of an import purchase on total domestic welfare are ambiguous. Consumers of imports gain value; producers of import-competing goods lose value.

As to the loss of the domestic sale, competition is tough, but it greatly contributes to the efficiency of the free market system and to the well being of consumers. Let’s face it: ultimately, the whole point of economic activity is to enable consumption. Production has no other purpose. So producers must react to competition and strive to improve value for buyers along any margins they can. That, in turn, is unequivocally positive for potential buyers both here and abroad.

It’s also true that the purchase of foreign goods means that dollars must be sold in exchange for foreign currency. That weakens the dollar, but those “excess dollars” are generally used to purchase U.S. assets, including physical capital. That direct investment promotes economic growth.

Open Economy, Open Mind

No matter what you believe about the net benefits or costs of a single import transaction like the one described above, it is misleading to draw conclusions about the benefits of foreign trade based on a single transaction, or even a series of repeated transactions.

First, consumer sovereignty is based on freedom of choice, including the freedom to purchase from any seller, domestic or foreign. Consumers greatly benefit from that broad freedom. Add to that the benefit of producers who are free to purchase inputs from any source they believe to offer the greatest value (a benefit that ultimately flows through to consumers). These freedoms ultimately enhance productivity and well being.

Trade across borders leverages the same economic advantages as trade within borders. People tend to accept the latter as truth without giving it a thought, yet the former is often rejected reflexively. The question is inappropriately bound up in issues like patriotism and, over time, an excessive focus on high-visibility job losses in traditional industries.

Trade allows people and their countries to specialize in producing things at which they are comparatively efficient, i.e., in which they are lower-cost producers. This is at the very heart of mutually beneficial exchange: no party to a voluntary transaction expects to suffer a loss. And in trade, when an external, domestic party sustains a lost sale, for example, they have the opportunity to improve or reallocate their resources to endeavors to which they are better suited. So there are direct gains from trade and there are indirect gains via the discipline of competition, including the benefits of reallocating scarce resources from inefficient to efficient uses.

Tariff Gains

Now we shift gears to tariffs: interventions having benefits that are more concentrated than costs, and which tend to be more ephemeral:

— Domestic producers who compete with imports gain through the grant of additional market power, given the tax on foreign goods and services. These producers now have more pricing flexibility, and what is often more pertinent, survivability.

— Workers at domestic firms will benefit to the extent that their employers face reduced foreign competition. Some combination of employment, hours, and wages may rise.

— Some firms have mixed gains and losses, with more pricing power over final product but elevated costs due to the use of taxed foreign components.

Tariff Losses

Who pays when government succumbs to irrational protectionist pressure and attempts to restrict imports via tariffs?

— Domestic consumers suffer a loss of freedom and bear a large part of the burden of the tariff tax.

— Higher prices for imports lead to higher prices for competing domestic goods, causing consumers to experience a loss of purchasing power.

— Domestic businesses suffer a loss of control over input decisions. Those already utilizing foreign inputs (and their buyers downstream) bear some of the burden of the tariff tax. For example, tariffs could be quite damaging to the U.S. AI industry, a result that would run strongly contrary to Trump’s promise to promote American AI.

— The U.S. suffers a loss of foreign investment, which could engender higher interest rates, lower productivity growth, and lower real wages.

— As Tyler Cowen puts it in a review of this paper, “… lobbying, logrolling and political horse-trading were essential features of the shift toward higher US tariffs. A lot of the tariffs of the time [1870 -1909] depended on which party controlled Congress, rather than economic rationality.“

— Tariffs tend to reduce economic growth due to diminished productivity in tariff-protected industries, which also erodes real wages. Less productive firms capture a significant share of the benefits of tariffs, so that economic growth falls due to a compositional effect. Higher prices for imports and import-competing goods undermine the real gains of import-protected workers.

— Finally, tariffs invariably beget retaliatory tariffs by erstwhile friendly trading partners. Export industries and their employees take a direct hit. This retaliation damages the prospects of the most productive exporters, while weaker exporting firms might be forced to close shop unnecessarily.

One other note: the discussion of gains and losses above is essentially the same for policies that reward the use of American labor via tax breaks. This not only penalizes imports of final and intermediate foreign goods, it subsidizes high-cost domestic labor. Obviously, the upshot is a less competitive U.S. economy.

Tariff-Threat Policy

To be fair, Donald Trump has said he’d use the threat of tariffs strategically to achieve a variety of objectives, not all of which are directly related to trade. We can hope that many of those threats won’t be acted upon. On one hand, that’s more appealing than general tariffs, with potential foreign policy gains and less in the way of general damage to the economy. On the other hand, the discretionary application of tariffs could invite political favoritism and foster a corrupt rent-seeking environment.

Conclusion

Trade protectionism protects weak and strong producers alike. The weak should not be given artificial incentives to produce goods inefficiently. That’s simply a waste of resources. Protecting the strong is unnecessary and discourages the drive for efficiency as well as real value creation. It lends market power to already powerful firms, leading to higher prices and penalizing domestic consumers.

One last aside: tariffs cannot raise anywhere close to the revenue necessary to replace the income tax, an absurd claim made by Trump on the campaign trail.

Only free trade is consistent with the values of a free society. It enhances choice, makes markets more competitive, creates incentives for efficiency, and cultivates opportunities for economic growth, That would serve Trump and the nation much better than the fixation on tariffs.

Choosing between the lesser of evils is a bummer, but that’s often the reality for voters. That goes almost without saying… our choices are politicians! I’ll certainly be in that quandary if Donald Trump is the Republican nominee for president in 2024, which looks increasingly likely. I held my nose and voted for him — twice — primarily because the Big Government solutions promoted consistently by Democrats are so awful.

At this point I’m not fully on board with any GOP candidate. That could change, but not yet. Now, if you’re a Trump supporter and you think the rambling opinions below are too critical of your guy, cut me some slack. I’m not a “Never Trumper”. I’m a “Never Statist”. And while I’ve never had much faith that Trump is with me on that count, he will almost surely be the lesser of evils.

The Abused Politician

Trump has been subjected to despicable treatment by political opponents since well before his inauguration in 2016, and his abusers in and out of government never let up. Many of the charges and accusations against him have been pure fiction and at this point represent obvious election interference. So I’m somewhat sympathetic to him despite some of his positions and often disagreeable manner. Still, I credit him for being a fighter, and as an aside, I’ll add that I actually enjoy some of his rants. He has the style of a nasty stand-up comic, which gives me some occasional laughs.

I agree with Trump on certain policy matters. On others, including some fundamental points, I find it hard to trust him as a leader, and I said that long before he was elected in 2016. He claims not to be a politician, but he is a politician through and through. He’s also a populist. And while populism can serve as a valuable check on certain excesses of government, it often cuts the wrong way, favoring what I like to call “do-somethingism”. That usually means public intervention. Populism is a perfectly natural home for a “pick-and-choose” statist like Trump, however. Moreover, I’m not happy that he refused to debate his opponents, and that too was a purely political decision.

Malign Neglect

If you need proof of Trump’s base instincts as a politician, look no further than his refusal to engage on the subject of entitlement reform. It’s no secret that both Social Security (SS) and Medicare are technically insolvent. This is probably the most important fiscal issue the country will face in the foreseeable future.

Without reform, SS benefits will be cut 23% in 2034. That would bring certain outrage among seniors and anyone approaching retirement. Sure, it’s a decade down the road, but addressing it sooner would be far less painful. Does Trump favor a huge cut in benefits? Probably not. Does he think benefits can simply continue without additional funding or reform of some kind? Does he prefer a greater inflation tax, rather than reform? Does he secretly favor “just print the money” like the modern monetary theorists of the Left? There are much better alternatives, but where is his leadership on this issue?

His unwillingness to discuss entitlements, and indeed, his denigration of anyone who so much as mentions the need for serious reforms, is a disgrace. He knows the train wreck is coming, but his focus is squarely on short-term politics. Why are so many on the Right willing to fall for this? Maybe they too understand it’s an elephant in the room, but an elephant that must not be named. After all, it’s not as if the Democrats have done a thing to address the issue.

False Fealty to Workers

Trump is a protectionist, given to the mercantilist fallacy that only exports are good and imports are bad. We import heavily because we are a high-income nation. The other side of that coin is that the world craves our assets, including the U.S. dollar (which is in absolutely no danger of losing its dominance as the primary currency of international transactions).

Here’s a little truth from “Trade Flows 101”: U.S. imports of goods and services correspond to purchases of U.S. assets by the rest of the world. In other words, U.S. trade deficits present opportunities for foreign investors to supply us with capital. That helps foster greater U.S. productive capacity, greater worker productivity, and higher wages.

On the other hand, government intervention to discourage imports via quotas or tariffs increases domestic prices and erodes real wages in the U.S. Furthermore, to favor certain industries (exporters) over others (importers) is a grotesque application of corporatist industrial policy. Why does the Right tolerate Trump’s advocacy for this sort of government central planning? Part of the answer is national security, which I accept to a limited extent, but not when “critical industries” are extended favors by government that are redundant to already powerful market forces.

Protectionism owes some of its popularity to the appeal of nationalism, as distinct from patriotism. However, it promotes sclerosis among domestic producers by shielding them from competition, causing direct harm to U.S. consumers. There is nothing patriotic about protectionism.

Real Stuff

A fallacy closely related to protectionism, and one to which Trump subscribes, is that the U.S. must produce more “things” — more commodities and manufactured goods. That’s not the market’s judgement, but one that appeals to the instincts of interventionists. In any case, services are often more highly valued than physical goods. If your comparative advantage is in producing a highly-valued service, don’t beat yourself up over neglecting to produce hard goods at which you’re comparatively lousy. Specialization and trade are under-appreciated as true social and economic miracles.

That said, we certainly have an advantage in the production of fossil fuels and should continue to produce them without interference. I’m with Trump on that. One day, reliable sources of “clean” energy will be economic, but we’re not there yet.

Corporate State

Well before his presidential run, Trump had a history of leveraging government to achieve his private ends. Eminent domain actions were useful to his development projects and expanding his own property rights at the expense of others. Naturally, he claimed his projects were in the public interest. Ah, the mindset of a rent seeker: government exists to actively facilitate the acquisitive interests of private business, or at least the “winners”. That thinking is thoroughly contrary to the libertarian view of the state’s role in establishing a neutral social environment under the rule-of-law.

In other ways, as President, Trump sought to bring major corporations under his political sway. Trump’s protectionist leanings as president were a prime example of corporatism in action.And read this account of a public meeting (and watch it at the link) at which one CEO after another, under Trump’s furrowed gaze, took turns describing something great they were doing for the country and committing to do more. It was one big, weird suck-up session intended to make the puffed-up Trump look like a great leader. As the author at the link says:

“These are corporate executives doing the President’s bidding for fear or favour.”

I supported Trump’s tax cuts, though they were certainly designed to reduce taxes on corporate income. Was this corporatist largess? That might have been part of his motivation. However, as I’ve argued before, corporate income is largely double-taxed. Moreover, shareholders do not bear the full burden of corporate taxes. Workers bear a significant portion of the burden, so Trump’s corporate tax cuts encouraged growth in real wages, whether he understood it or not.

It’s Still So Big

Tax cuts paired with reduced spending would have been a welcome approach. Unfortunately, Trump was a fairly big spender during his term in office, even if you exclude Covid emergency spending. Growth in the government’s dominance over resources did not slow on his watch. Fiscally disciplined he’s not!

It’s true that his administration made efforts to curtail regulation, but in retrospect, those steps at best arrested the growth of regulation, rather than achieving reductions. The hope of seeing any real deconstruction of the administrative state under Trump was fleeting.

Migration

Immigration is a complicated issue when it comes to assessing Trump’s candidacy. I’m strongly in favor of greater legal immigration because it would improve our demographics and labor supply while shrinking our entitlements deficits. Legal migrants are often technically proficient and many come with sponsorships. On the whole, legal migrants tend to be ready and willing to work,

This position is often condemned by Trump’s most ardent cheerleaders, however. I’ve generally supported Trump’s position on illegal immigration as a matter of national security, to eliminate human trafficking, and to reduce burdens on public aid and support systems. Unfortunately, during Trump’s presidency, he did more to reduce legal immigration than illegal immigration. I have no qualms about “the Wall” except for its expense and the likelihood that cheaper and superior technologies could be deployed for border security. Trump might prefer the Wall’s symbolic value.

Rightly or wrongly, Trump’s messaging on immigration strikes many as nativist, providing an easy excuse for the Left to accuse him of racism. That certainly won’t help his election prospects.

Conclusion

Trump will almost surely be the GOP nominee, unless Democrats succeed in putting him behind bars by then. If the choice is Trump vs. almost any Democrat I can imagine, I’ll have to vote for him. For all his faults and wild card qualities, I still consider him a safer alternative than the devils we know on the Left. But I’d feel much better about him if he’d take a responsible position on Social Security and Medicare reform, abandon protectionism except in cases of critical national security needs (and without overkill), commit to spending reductions, and adopt a more productive approach to legal immigration.

We’re told again and again that government must take action to correct “market failures”. Economists are largely responsible for this widespread view. Our standard textbook treatments of external costs and benefits are constructed to demonstrate departures from the ideal of perfectly competitive market equilibria. This posits an absurdly unrealistic standard and diminishes the power and dramatic success of real-world markets in processing highly dispersed information, allocating resources based on voluntary behavior, and raising human living standards. It also takes for granted the underlying institutional foundations that lead to well-functioning markets and presumes that government possesses the knowledge and ability to rectify various departures from an ideal. Finally, “corrective” interventions are usually exposited in economics classes as if they are costless!

Failed Disgnoses

This brings into focus the worst presumption of all: that government solutions to social and economic problems never fail to achieve their intended aims. Of course that’s nonsense. If defined on an equivalent basis, government failure is vastly more endemic and destructive than market failure.

“According to ancient legend, a Roman emperor was asked to judge a singing contest between two participants. After hearing the first contestant, the emperor gave the prize to the second on the assumption that the second could be no worse than the first. Of course, this assumption could have been wrong; the second singer might have been worse. The theory of market failure committed the same mistake as the emperor. Demonstrating that the market economy failed to live up to the ideals of general competitive equilibrium was one thing, but to gleefully assert that public action could costlessly correct the failure was quite another matter. Unfortunately, much analytical work proceeded in such a manner. Many scholars burst the bubble of this romantic vision of the political sector during the 1960s. But it was [James] Buchanan and Gordon Tullock who deserve the credit for shifting scholarly focus.”

John Cochrane sums up the whole case succinctly in the “punchline” of a recent post:

“The case for free markets never was their perfection. The case for free markets always was centuries of experience with the failures of the only alternative, state control. Free markets are, as the saying goes, the worst system; except for all the others.”

Tracing Failures

We can view the relation between market failure and government failure in two ways. First, we can try to identify market failures and root causes. For example, external costs like pollution cause harm to innocent third parties. This failure might be solely attributable to transactions between private parties, but there are cases in which government engages as one of those parties, such as defense contracting. In other cases government effectively subsidizes toxic waste, like the eventual disposal of solar panels. Another kind of market failure occurs when firms wield monopoly power, but that is often abetted by costly regulations that deliver fatal blows to small competitors.

The second way to analyze the nexus between government and market failures is to first examine the taxonomy of government failure and identify the various damages inflicted upon the operation of private markets. That’s the course I’ll follow below, though by no means is the discussion here exhaustive.

Failures In and Out of Scope

An extensive treatment of government failure was offered eight years ago by William R. Keech and Michael Munger. To start, they point out what everyone knows: governments occasionally perpetrate monstrous acts like genocide and the instigation of war. That helps illustrate a basic dichotomy in government failures:

“… government may fail to do things it should do, or government may do things it should not do.’

Both parts of that statement have numerous dimensions. Failures at what government should do run the gamut from poor service at the DMV, to failure to enforce rights, to corrupt bureaucrats and politicians skimming off the public purse in the execution of their duties. These failures of government are all too common.

What government should and should not do, however, is usually a matter of political opinion. Thomas Jefferson’s axioms appear in a single sentence at the beginning of the Declaration of Independence; they are a tremendous guide to the first principles of a benevolent state. However, those axioms don’t go far in determining the range of specific legal protections and services that should and shouldn’t be provided by government.

Pareto Superiority

Keech and Munger engage in an analytical exercise in which the “should and shouldn’t” question is determined under the standard of Pareto superiority. A state of the world is Pareto superior if at least one person prefers it to the current state (and no one else is averse to it). Coincidentally, voluntary trades in private markets always exploit Pareto superior opportunities, absent legitimate external costs and benefits.

The set of Pareto superior states available to government can be expanded by allowing for side payments or compensation to those who would have preferred the current state. Still, those side payments are limited by the magnitude of the gains flowing to those who prefer the alternative (and if those gains can be redistributed monetarily).

Keech and Munger define government failure as the unexploited existence of Pareto superior states. Of course, by this definition, only a benevolent, omniscient, and omnipotent dictator could hope to avoid government failure. But this is no more unrealistic than the assumptions underlying perfectly competitive market equilibrium from which departure are deemed “market failures” that government should correct. Thus, Keech and Munger say:

“The concept of government failure has been trapped in the cocoon of the theory of perfect markets. … Government failure in the contemporary context means failing to resolve a classic market failure.”

But markets must operate within a setting defined by culture and institutions. The establishment of a social order under which individuals have enforceable rights must come prior to well-functioning markets, and that requires a certain level of state capacity. Keech and Munger are correct that market failure is often a manifestation of government failure in setting and/or enforcing these “rules of the game”.

“The real question is … how the rules of the game should be structured in terms of incentives, property rights, and constraints.”

The Regulatory State and Market Failures

Government can do too little in defining and enforcing rights, and that’s undoubtedly a cause of failure in markets in even the most advanced economies. At the same time there is an undeniable tendency for mission creep: governments often try to do too much. Overregulation in the U.S. and other developed nations creates a variety of market failures. This includes the waste inherent in compliance costs that far exceed benefits; welfare losses from price controls, licensing, and quotas; diversion of otherwise productive resources into rent seeking activity, anti-competitive effects from “regulatory capture”; Chevron-like distortions endemic to the administrative judicial process; unnecessary interference in almost any aspect of private business; and outright corruption and bribe-taking.

Central Planning and Market Failures

Another category of government attempting to “do too much” is the misallocation of resources that inevitably accompanies efforts to pick “winners and losers”. The massive subsidies flowing to investors in various technologies are often misdirected. Many of these expenditures end up as losses for taxpayers, and this is not the only form in which failed industrial planning takes place. A related evil occurs when steps are taken to penalize and destroy industries in political disfavor with thin economic justification.

Other clear examples of government “planning” failure are protectionist laws. These are a net drain on our wealth as a society, denying consumers of free choice and saddling the country with the necessity to produce restricted products at high cost relative to erstwhile trading partners.

There are, of course, failures lurking within many other large government spending programs in areas such as national defense, transportation, education, and agriculture. Many of these programs can be characterized as centrally planning. Not only are some of these expenditures ineffectual, but massive procurement spending seems to invite waste and graft. After all, it’s somebody else’s money.

Redistribution and Market Failures

One might regard redistribution programs as vehicles for the kinds of side payments described by Keech and Munger. Some might even say these are the side payments necessary to overcome resistance from those unable to thrive in a market economy. That reverses the historical sequence of events, however, since the dominant economic role of markets preceded the advent of massive redistribution schemes. Unfortunately, redistribution programs have been plagued by poor design, such as the actuarial nightmare inherent in Social Security and the destructive work incentives embedded in other parts of the social safety net. These are rightly viewed as government failures, and their distortionary effects spill variously into capital markets, labor markets and ultimately product markets.

Taxation and Market Failures

All these public initiatives under which government failures precipitate assorted market failures must be paid for by taxpayers. Therefore, we must also consider the additional effects of taxation on markets and market failures. The income tax system is rife with economic distortions. Not only does it inflict huge compliance costs, but it alters incentives in ways that inhibit capital formation and labor supply. That hampers the ability of input markets to efficiently meet the needs of producers, inhibiting the economy’s productive capacity. In turn, these effects spill into output market failures, with consequent losses in .social welfare. Distortionary taxes are a form of government failure that leads to broad market failures.

Deficits and Market Failure

More often than not, of course, tax revenue is inadequate to fund the entire government budget. Deficit spending and borrowing can make sense when public outlays truly produce long-term benefits. In fact, the mere existence of “risk-free” assets (Treasury debt) across the maturity spectrum might enhance social welfare if it enables improvements in portfolio diversification that outweigh the cost of the government’s interest obligations. (Treasury securities do bear interest-rate risk and, if unindexed, they bear inflation risk.)

Nevertheless, borrowing can reflect and magnify deleterious government efforts to “do too much”, ultimately leading to market failures. Government borrowing may “crowd out” private capital formation, harming economy-wide productivity. It might also inhibit the ability of households to borrow at affordable rates. Interest costs of the public debt may become explosive as they rise relative to GDP, limiting the ability of the public sector to perform tasks that it should *actually* do, with negative implications for market performance.

Inflation and Market Failure

Deficit spending promotes inflation as well. This is more readily enabled when government debt is monetized, but absent fiscal discipline, the escalation of goods prices is the only remaining force capable of controlling the real value of the debt. This is essentially the inflation tax.

Inflation is a destructive force. It distorts the meaning of prices, causes the market to misallocate resources due to uncertainty, and inflicts costs on those with fixed incomes or whose incomes cannot keep up with inflation. Sadly, the latter are usually in lower socioeconomic strata. These are symptoms of market failure prompted by government failure to control spending and maintain a stable medium of exchange.

Conclusion

Markets may fail, but when they do it’s very often rooted in one form of government failure or another. Sometimes it’s an inadequacy in the establishment or enforcement of property rights. It could be a case of overzealous regulation. Or government may encroach on, impede, or distort decisions regarding the provision of goods or services best left to the market. More broadly, redistribution and taxation, including the inflation tax, distort labor and capital markets. The variety of distortions created when government fails at what it should do, or does what it shouldn’t do, is truly daunting. Yet it’s difficult to find leaders willing to face up to all this. Statism has a powerful allure, and too many elites are in thrall to the technocratic scientism of government solutions to social problems and central planning in the allocation of resources.

Recent advances in artificial intelligence (AI) are giving hope to advocates of central economic planning. Perhaps, they think, the so-called “knowledge problem” (KP) can be overcome, making society’s reliance on decentralized market forces “unnecessary”. The KP is the barrier faced by planners in collecting and using information to direct resources to their most valued uses. KP is at the heart of the so-called “socialist calculation debate”, but it applies also to the failures of right-wing industrial policies and protectionism.

Apart from raw political motives, run-of-the-mill government incompetence, and poor incentives, the KP is an insurmountable obstacle to successful state planning, as emphasized by Friedrich Hayek and many others. In contrast, market forces are capable of spontaneously harnessing all sources of information on preferences, incentives, resources, as well as existing and emergent technologies in allocating resources efficiently. In addition, the positive sum nature of mutually beneficial exchange makes the market by far the greatest force for voluntary social cooperation known to mankind.

Nevertheless, the hope kindled by AI is that planners would be on an equal footing with markets and allow them to intervene in ways that would be “optimal” for society. This technocratic dream has been astir for years along with advances in computer technology and machine learning. I guess it’s nice that at least a few students of central planning understood the dilemma all along, but as explained below, their hopes for AI are terribly misplaced. AI will never allow planners to allocate resources in ways that exceed or even approximate the efficiency of the market mechanism’s “invisible hand”.

Michael Munger recently described the basic misunderstanding about the information or “data” that markets use to solve the KP. Markets do not rely on a given set of prices, quantities, and production relationships. They do not take any of those as givens with respect to the evolution of transactions, consumption, production, investment, or search activity. Instead, markets generate this data based on unobservable and co-evolving factors such as the shape of preferences across goods, services, and time; perceptions of risk and its cost; the full breadth of technologies; shifting resource availabilities; expectations; locations; perceived transaction costs; and entrepreneurial energy. Most of these factors are “tacit knowledge” that no central database will ever contain.