Note: I’m moving for the first time in many years. We have a lot to do quickly because we’ll close on our new home in early September. It’s in a place with palm trees, but no basements! The clean-up and winnowing of our accumulated papers, possessions, and … junk — not to mention attending to all the details of the move — is taking up all of my time. Anyway, I started the post below a week ago and had to put it aside. Not sure how frequently I’ll be posting till we’re fully settled in the fall, but we’ll see how it goes.

____________________________________________

The inflation news was great last week, with both the Consumer Price Index (CPI) and the Producer Price Index (PPI) reported below expectations. Month-over-month, the increase in the overall CPI was just 0.2%. Year-over-year, CPI inflation was 3%, down from 9% a year ago. Of course, contrary to Joe Biden’s ridiculous claims, this inflation news came despite, and not because of, the pernicious effects of “Bidenomics”. But that aside, just like that, we heard proclamations that the Federal Reserve had finally succeeded in bringing real short-term interest rates into positive territory. Finally, some said, Fed policy had moved into more restrictive territory. But in fact, real rates moved above zero months ago.

The popular rate narrative is based on the fact that the effective Fed Funds rate is now 5.08% while “headline” CPI inflation fell to 2.97%. That would give us a real Fed Funds rate of 3.11%… if that sort of calculation made sense. Here’s an appropriate reaction from Kevin Erdman:

“The short term rate minus trailing 12 month inflation is not a thing. It’s an irrelevant number. Nothing about June 2022 inflation has anything to do with the real fed funds rate in July 2023.”

His statement generalizes to interest rates at any maturity less a corresponding measure of trailing inflation. They are all irrelevant. A proper real rate of interest must incorporate a measure of inflation expectations. Survey data is often used for this purpose, but a better measure can be taken from market expectations by comparing a nominal Treasury rate with a rate on an inflation-indexed Treasury (TIPS) of the same maturity. This is a fairly convenient approach.

Below, we can see that the real one-year Treasury rate has been positive since last November.

And here is the real one-month Treasury rate:

Again, these charts suggest that real short-term rates have been positive much longer than some believe. Whether that represents a “restrictive policy stance” by the Federal Reserve is another matter. We know the Fed has tightened policy, but that began after the notably loose policy conducted throughout the pandemic. Have we truly crossed the threshold into “tightness”?

Here’s the effective (nominal) federal funds rate over the past year.

This rate is under fairly direct control by the Fed, and it is the primary focus of most Fed watchers. It’s an overnight lending rate on loans of reserves between banks, so to adjust it precisely for expected inflation requires an annualized, overnight inflation rate. That’s pretty tricky!

Finding a published measure of expected inflation over durations of less than a year forward is difficult. One can derive one or use a longer-term rate of expected inflation as a proxy, with the proviso that near-term expectations might be more extreme than the proxy, especially if inflation is expected to change from its current pace. Here are one-year inflation expectations over the past year from a Cleveland Fed model that utilizes TIPS returns and other data.

So inflation expectations have declined substantially. If we compare them with short-term interest rates or the effective fed funds rate over the past year, it’s likely the real fed funds rate climbed above zero before the end of the first quarter of 2023. It might even have exceeded the so called “neutral” real Fed funds rate (R*), which was estimated by the Fed to be 1.14% in the first quarter of 2023. A real Fed funds rate above that level would have been deemed restrictive in the first quarter.

My own view is that changes in the Fed funds rate are not at the heart of the transmission mechanism from monetary policy to the real economy. The monetary aggregates are more reliable guides. The broad money stock M2 has been edging lower for well over a year now. That certainly qualifies as a restrictive move, but there is still a lot of excess liquidity out there, left over from the pandemic deluge engineered by the Fed.

The good reports last week might not mark the end of the inflation problem. There are still price pressures fromboth the demand and supply-sides. Furthermore, to put things in context, the month-to-month increases in May and June of last year were large, which helped to hold down the 12-month increases this May and June. But the CPI was flat during the second half of last year. That means month-to-month inflation over the next six months may well translate into an escalation of year-over-year inflation. That might or might not be turn out to be meaningful, but it would provide a pretext for additional Fed tightening.

The main point of this post is that real interest rates cannot be calculated on the basis of reported inflation over prior months. Doing so at this juncture understates the degree of monetary tightening in terms of short-term rates. Real interest rates can only be determined by nominal rates relative to expectations of future inflation. This gives a more accurate picture of actual credit market conditions and the Fed’s rate policy stance.

The inflation news was good last week, with both the consumer and producer price indices (CPI and PPI) for May coming in below expectations. The increase in the core CPI, which excludes food and energy prices, was the same as in April. Asthis series of tweets attempts to demonstrate, teasing out potential distortions from the shelter component of the CPI shows a fairly broad softening. That might be heartening to the Federal Reserve, though at 4.0%, the increase in the CPI from a year ago remains too high, as does the core rate at 5.3%. Later in the month we’ll see how much the Fed’s preferred inflation gauge, the PCE deflator, exceeds the 2% target.

Inflation has certainly tapered since last June, when the CPI had its largest monthly increase of this cycle. After that, the index leveled off to a plateau lasting through December. But the big run-up in the CPI a year ago had the effect of depressing the year-over-year increase just reported, and it will tend to depress next month’s inflation report as well. After this June’s CPI (to be reported in July), the flat base from a year earlier might have a tendency to produce rising year-over-year inflation numbers over the rest of this year. Also, the composition of inflation has shifted away from goods prices and into services, where markets aren’t as interest-rate sensitive. Therefore, the price pressure in services might have more persistence.

So it’s way too early to say that the Fed has successfully brought inflation under control, and they know it. But last week, for the first time in 10 meetings, the Fed’s chief policy-making arm (the Federal Open Market Committee, or FOMC) did not increase its target for the federal funds rate, leaving it at 5% for now. This “pause” in the Fed’s rate hikes might have more to do with internal politics than anything else, as new Vice Chairman Philip Jefferson spoke publicly about the “pause” several days before the meeting. That statement might not have been welcome to other members of the FOMC. Nevertheless, at least the pause buys some time for the “long and variable lags” of earlier monetary tightening to play out.

There are strong indications that the FOMC expects additional rate hikes to be necessary in order to squeeze inflation down to the 2% target. The “median member” of the Committee expects the target FF rate to increase by an additional 50 basis points by the end of 2023. At a minimum, it seems they felt compelled to signal that later rate hikes might be necessary after having their hand forced by Jefferson. That “expectation” might have been part of a “political bargain” struck at the meeting.

In addition, the Fed’s stated intent is to continue drawing down its massive securities portfolio, an act otherwise known as “quantitative tightening” (QT). That process was effectively interrupted by lending to banks in the wake of this spring’s bank failures. And now, a danger cited by some analysts is that a wave of Treasury borrowing following the increase in the debt ceiling, along with QT, could at some point lead to a shortage of bank reserves. That could force the Fed to “pause” QT, essentially allowing more of the new Treasury debt to be monetized. This isn’t an imminent concern, but perhaps next year it could present a test of the Fed’s inflation-fighting resolve.

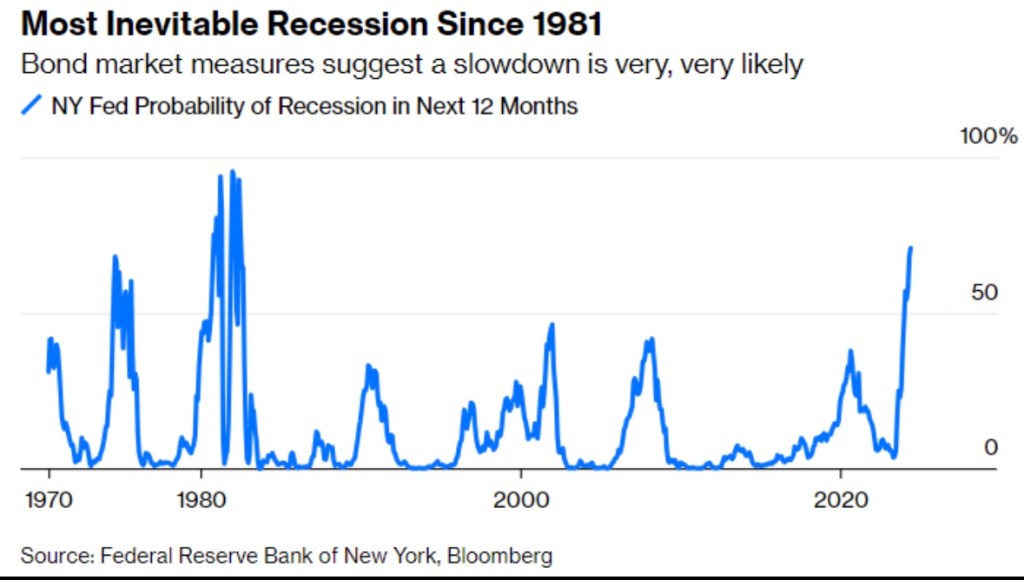

It’s certainly too early to declare that the Fed has engineered a “soft landing”, avoiding recession while successfully reigning-in inflation. The still-inverted yield curve is the classic signal that credit markets “expect” a recession. Here is the New York Federal Reserve Bank’s recession probability indicator, which is at its highest level in over 40 years:

There are other signs of weakness: the index of leading economic indicators has moved down for the last 13 months, real retail sales are down from 13 months ago, and real average weekly earnings have been trending down since January, 2021. A real threat is the weakness in commercial real estate, which could renew pressure on regional banks. Credit is increasingly tight, and that is bound to take a toll on the real economy before long.

The labor market presents its own set of puzzles. The ratio of job vacancies to job seekers has declined, but it is still rather high. Multiple job holders have increased, which might be a sign of stress. Some have speculated that employers are “hoarding” labor, hedging against the advent of an ultimate rebound in the economy, when finding new workers might be a challenge.

Despite some high-profile layoffs in tech and financial services, job gains have held up well thus far. Of course, the labor market typically lags turns in the real economy. We’ve seen declining labor productivity, consistent with changes in real earnings. This is probably a sign that while job growth remains strong, we are witnessing a shift in the composition of jobs from highly-skilled and highly-paid workers to lower-paid workers.

A further qualification is that many of the most highly-qualified job applicants are already employed, and are not part of the pool of idle workers. It’s also true that jobless claims, while not at alarming levels, have been trending higher.

It’s important to remember that the Fed’s policy stance over the past year is intended to reduce liquidity and ultimately excess demand for goods and services. In typical boom-and-bust fashion, the tightening was a reversal from the easy-money policy pursued by the Fed from 2020 – early 2022, even in the face of rising inflation. The money supply has been declining for just over a year now, but the declines have been far short of the massive expansion that took place during the pandemic. There is still quite a lot of liquidity in the system.

That liquidity helps explain the stock market’s recovery in the face of ongoing doubts about the economy. While the market is still well short of the highs reached in early 2022, recent gains have been impressive.

Some would argue that the forward view driving stock prices reflects an expectation of a mild recession and an inevitable rebound in the economy, no doubt accompanied by eventual cuts in the Fed’s interest rate target. But even stipulating that’s the case, the timing of a stock rally on those terms seems a little premature. Or maybe not! It wouldn’t be the first time incoming data revealed a recession had been underway that no one knew was happening in real time. Are we actually coming out of shallow woods?

To summarize, inflation is down but not out. The Fed might continue its pause on rate hikes through one more meeting in late July, but there will be additional rate increases if inflation remains persistent or edges up from present levels, or if the economy shows unexpected signs of strength. I’d like to be wrong about the prospects of a recession, but a downturn is likely over the next 12 months. I’ve been saying that a recession is ahead for the past eight months or so, which reminds me that even a broken clock is right twice a day. In any case, the stock market seems to expect something mild. However misplaced, hopes for a soft landing seem very much alive.

Policy activists have long maintained that manipulating government policy can stabilize the economy. In other words, big spending initiatives, tax cuts, and money growth can lift the economy out of recessions, or budget cuts and monetary contraction can prevent overheating and inflation. However, this activist mirage burned away under the light of experience. It’s not that fiscal and monetary policy are powerless. It’s a matter of practical limitations that often cause these tools to be either impotent or destabilizing to the economy, rather than smoothing fluctuations in the business cycle.

The macroeconomics classes seem like yesterday: Keynesian professors lauded the promise of wise government stabilization efforts: policymakers could, at least in principle, counter economic shocks, particularly on the demand side. That optimistic narrative didn’t end after my grad school days. I endured many client meetings sponsored by macro forecasters touting the fine-tuning of fiscal and monetary policy actions. Some of those economists were working with (and collecting revenue from) government policymakers, who are always eager to validate their pretensions as planners (and saviors). However, seldom if ever do forecasters conduct ex post reviews of their model-spun policy scenarios. In fairness, that might be hard to do because all sorts of things change from initial conditions, but it definitely would not be in their interests to emphasize the record.

In this post I attempt to explain why you should be skeptical of government stabilization efforts. It’s sort of a lengthy post, so I’ve listed section headings below in case readers wish to scroll to points of most interest. Pick and choose, if necessary, though some context might get lost in the process.

Expectations Change the World

Fiscal Extravagance

Multipliers In the Real World

Delays

Crowding Out

Other Peoples’ Money

Tax Policy

Monetary Policy

Boom and Bust

Inflation Targeting

Via Rate Targeting

Policy Coordination

Who Calls the Tune?

Stable Policy, Stable Economy

Expectations Change the World

There were always some realists in the economics community. In May we saw the passing of one such individual: Robert Lucas was a giant intellect within the economics community, and one from whom I had the pleasure of taking a class as a graduate student. He was awarded the Nobel Prize in Economic Science in 1995 for his applications of rational expectations theory and completely transforming macro research. As Tyler Cowen notes, Keynesians were often hostile to Lucas’ ideas. I remember a smug classmate, in class, telling the esteemed Lucas that an important assumption was “fatuous”. Lucas fired back, “You bastard!”, but proceeded to explain the underlying logic. Cowen uses the word “charming” to describe the way Lucas disarmed his critics, but he could react strongly to rude ignorance.

Lucas gained professional fame in the 1970s for identifying a significant vulnerability of activist macro policy. David Henderson explains the famous “Lucas Critique” in the Wall Street Journal:

“… because these models were from periods when people had one set of expectations, the models would be useless for later periods when expectations had changed. While this might sound disheartening for policy makers, there was a silver lining. It meant, as Lucas’s colleague Thomas Sargent pointed out, that if a government could credibly commit to cutting inflation, it could do so without a large increase in unemployment. Why? Because people would quickly adjust their expectations to match the promised lower inflation rate. To be sure, the key is government credibility, often in short supply.”

Non-credibility is a major pitfall of activist macro stabilization policies that renders them unreliable and frequently counterproductive. And there are a number of elements that go toward establishing non-credibility. We’ll distinguish here between fiscal and monetary policy, focusing on the fiscal side in the next several sections.

Fiscal Extravagance

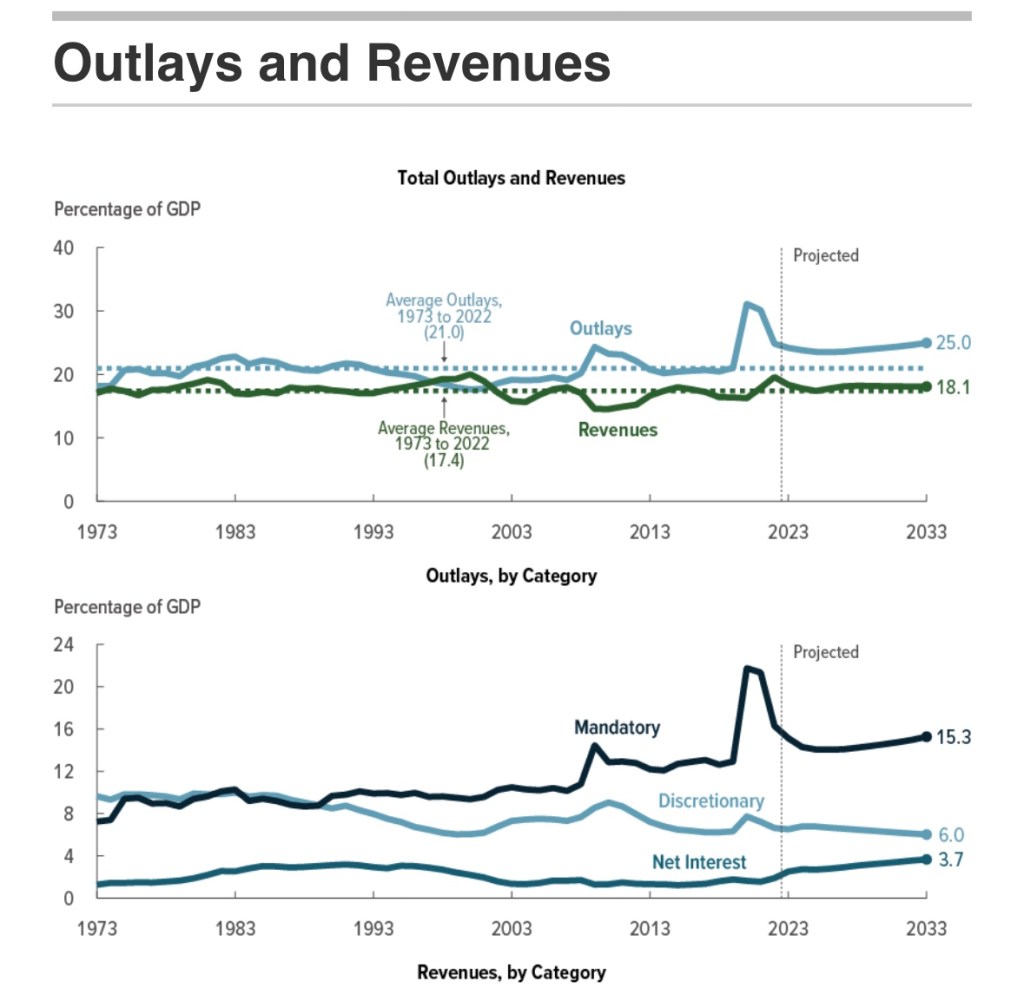

We’ve seen federal spending and budget deficits balloon in recent years. Chronic and growing budget deficits make it difficult to deliver meaningful stimulus, both practically and politically.

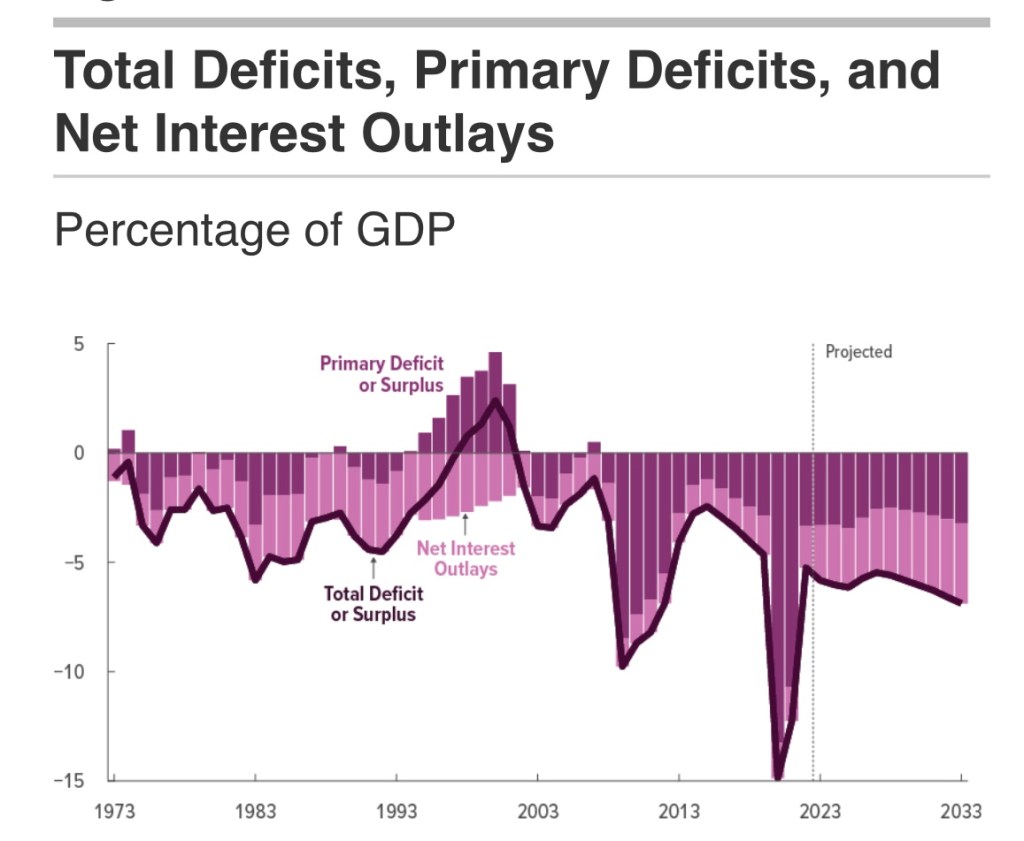

The next chart is from the most recent Congressional Budget Office (CBO) report. It shows the growing contribution of interest payments to deficit spending. Ever-larger deficits mean ever-larger amounts of debt on which interest is owed, putting an ever-greater squeeze on government finances going forward. This is particularly onerous when interest rates rise, as they have over the past few years. Both new debt is issued and existing debt is rolled over at higher cost.

Relief payments made a large contribution to the deficits during the pandemic, but more recent legislation (like the deceitfully-named Inflation Reduction Act) piled-on billions of new subsidies for private investments of questionable value, not to mention outright handouts. These expenditures had nothing to do with economic stabilization and no prayer of reducing inflation. Pissing away money and resources only hastens the debt and interest-cost squeeze that is ultimately unsustainable without massive inflation.

Hardly anyone with future political ambitions wants to address the growing entitlements deficit … but it will catch up with them. Social Security and Medicare are projected to exhaust their respective trust funds in the early- to mid-2030s, which will lead to mandatory benefit cuts in the absence of reform.

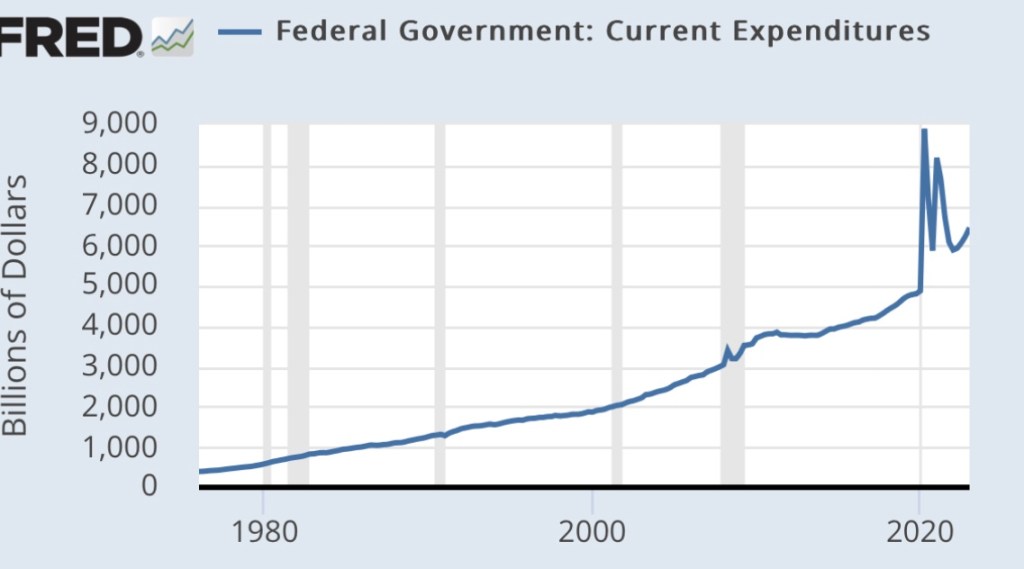

If it still isn’t obvious, the real problem driving the budget imbalance is spending, not revenue, as the next CBO chart demonstrates. The “emergency” pandemic measures helped precipitate our current stabilization dilemma. David Beckworth tweets that the relief measures “spurred a rapid recovery”, though I’d hasten to add that a wave of private and public rejection of extreme precautions in some regions helped as well. And after all, the pandemic downturn was exaggerated by misdirected policies including closures and lockdowns that constrained both the demand and supply sides. Beckworth acknowledges the relief measures “propelled inflation”, but the pandemic also seemed to leave us on a permanently higher spending path. Again, see the first chart below.

The second chart below shows that non-discretionary spending (largely entitlements) and interest outlays are how we got on that path. The only avenue for countercyclical spending is discretionary expenditures, which constitute an ever-smaller share of the overall budget.

We’ve had chronic deficits for years, but we’ve shifted to a much larger and continuing imbalance. With more deficits come higher interest costs, especially when interest rates follow a typical upward cyclical pattern. This creates a potentially explosive situation that is best avoided via fiscal restraint.

Putting other doubts about fiscal efficacy aside, it’s all but impossible to stimulate real economic activity when you’ve already tapped yourself out and overshot in the midst of a post-pandemic economic expansion.

Multipliers In the Real World

So-called spending multipliers are deeply beloved by Keynesians and pork-barrel spenders. These multipliers tell us that every dollar of extra spending ultimately raises income by some multiple of that dollar. This assumes that a portion of every dollar spent by government is re-spent by the recipient, and a portion of that is re-spent again by another recipient. But spending multipliers are never what they’re cracked up to be for a variety of reasons. (I covered these in“Multipliers Are For Politicians”, and also see this post.) There are leakages out of the re-spending process (income taxes, saving, imports), which trim the ultimate impact of new spending on income. When supply constraints bind on economic activity, fiscal stimulus will be of limited power in real terms.

If stimulus is truly expected to be counter-cyclical and transitory, as is generally claimed, then much of each dollar of extra government spending will be saved rather than spent. This is the lesson of the permanent income hypothesis. It means greater leakages from the re-spending stream and a lower multiplier. We saw this with the bulge in personal savings in the aftermath of pandemic relief payments.

Another side of this coin, however, is that cutting checks might be the government’s single-most efficient activity in execution, but it can create massive incentive problems. Some recipients are happy to forego labor market participation as long as the government keeps sending them checks, but at least they spend some of the income.

Delays

Another unappreciated and destabilizing downside of fiscal stimulus is that it often comes too late, just when the economy doesn’t need stimulus. That’s because a variety of delays are inherent in many spending initiatives: legislative, regulatory, legal challenges, planning and design, distribution to various spending authorities, and final disbursement. As I noted here:

“Even government infrastructure projects, heralded as great enhancers of American productivity, are often subject to lengthy delays and cost overruns due to regulatory and environmental rules. Is there any such thing as a federal ‘shovel-ready’ infrastructure project?”

Crowding Out

The supply of savings is limited, but when government borrows to fund deficits, it directly competes with private industry for those savings. Thus, funds that might otherwise pay for new plant, equipment, and even R&D are diverted to uses that should qualify as government consumption rather than long-term investment. Government competition for funds “crowds-out” private activity and impedes growth in the economy’s productive capacity. Thus, the effort to stimulate economic activity is self-defeating in some respects.

Other Peoples’ Money

Government doesn’t respond to price signals the way self-interested private actors do. This indifference leads to mis-allocated resources and waste. It extends to the creation of opportunities for graft and corruption, typically involving diversion of resources into uses that are of questionable productivity (corn ethanol, solar and wind subsidies).

Consider one other type of policy action perceived as counter-cyclical: federal bailouts of failing financial institutions or other troubled businesses. These rescues prop up unproductive enterprises rather than allowing waste to be flushed from the system, which should be viewed as a beneficial aspect of recession. The upshot is that too many efforts at economic stabilization are misdirected, wasteful, ill-timed, and pro-cyclical in impact.

Tax Policy

Like stabilization efforts on the spending side, tax changes may be badly timed. Tax legislation is often complex and can take time for consumers and businesses to adjust. In terms of traditional multiplier analysis, the initial impact of a tax change on spending is smaller than for expenditures, so tax multipliers are smaller. And to the extent that a tax change is perceived as temporary, it is made less effective. Thus, while changes in tax policy can have powerful real effects, they suffer from some of the same practical shortcomings for stabilization as changes in spending.

However, stimulative tax cuts, if well crafted, can boost disposable incomes and improve investment and work incentives. As temporary measures, that might mean an acceleration of certain kinds of activity. Tax increases reduce disposable incomes and may blunt incentives, or prompt delays in planned activities. Thus, tax policy may bear on the demand side as well as the timing of shifts in the economy’s productive potential or supply side.

Monetary Policy

Monetary policy is subject to problems of its own. Again, I refer to practical issues that are seemingly impossible for policy activists to overcome. Monetary policy is conducted by the nation’s central bank, the Federal Reserve (aka, the Fed). It is theoretically independent of the federal government, but the Fed operates under a dual mandate established by Congress to maintain price stability and full employment. Therein lies a basic problem: trying to achieve two goals that are often in conflict with a single policy tool.

Make no mistake: variations in money supply growth can have powerful effects. Nevertheless, they are difficult to calibrate due to “long and variable lags” as well as changes in money “velocity” (or turnover) often prompted by interest rate movements. Excessively loose money can lead to economic excesses and an overshooting of capacity constraints, malinvestment, and inflation. Swinging to a tight policy stance in order to correct excesses often leads to “hard landings”, or recession.

Boom and Bust

The Fed fumbled its way into engineering the Great Depression via excessively tight monetary policy. “Stop and go” policies in the 1970s led to recurring economic instability. Loose policy contributed to the housing bubble in the 2000s, and subsequent maladjustments led to a mortgage crisis (also see here). Don’t look now, but the inflationary consequences of the Fed’s profligacy during the pandemic prompted it to raise short-term interest rates in the spring of 2022. It then acted with unprecedented speed in raising rates over the past year. While raising rates is not always synonymous with tightening monetary conditions, money growth has slowed sharply. These changes might well lead to recession. Thus, the Fed seems given to a pathology of policy shifts that lead to unintentional booms and busts.

Inflation Targeting

The Fed claims to follow a so-called flexible inflation targeting policy. In reality, it has reacted asymmetrically to departures from its inflation targets. It took way too long for the Fed to react to the post-pandemic surge in inflation, dithering for months over whether the surge was “transitory”. It wasn’t, but the Fed was reluctant to raise its target rates in response to supply disruptions. At the same time, the Fed’s own policy actions contributed massively to demand-side price pressures. Also neglected is the reality that higher inflation expectations propel inflation on the demand side, even when it originates on the supply side.

Via Rate Targeting

At a more nuts and bolts level, today the Fed’s operating approach is to control money growth by setting target levels for several key short-term interest rates (eschewing a more direct approach to the problem). This relies on price controls (short-term interest rates being the price of liquidity) rather than allowing market participants to determine the rates at which available liquidity is allocated. Thus, in the short run, the Fed puts itself into the position of supplying whatever liquidity is demanded at the rates it targets. The Fed makes periodic adjustments to these rate targets in an effort to loosen or tighten money, but it can be misdirected in a world of high debt ratios in which rates themselves drive the growth of government borrowing. For example, if higher rates are intended to reduce money growth and inflation, but also force greater debt issuance by the Treasury, the approach might backfire.

Policy Coordination

While nominally independent, the Fed knows that a particular monetary policy stance is more likely to achieve its objectives if fiscal policy is not working at cross purposes. For example, tight monetary policy is more likely to succeed in slowing inflation if the federal government avoids adding to budget deficits. Bond investors know that explosive increases in federal debt are unlikely to be repaid out of future surpluses, so some other mechanism must come into play to achieve real long-term balance in the valuation of debt with debt payments. Only inflation can bring the real value of outstanding Treasury debt into line. Continuing to pile on new debt simply makes the Fed’s mandate for price stability harder to achieve.

Who Calls the Tune?

The Fed has often succumbed to pressure to monetize federal deficits in order to keep interest rates from rising. This obviously undermines perceptions of Fed independence. A willingness to purchase large amounts of Treasury bills and bonds from the public while fiscal deficits run rampant gives every appearance that the Fed simply serves as the Treasury’s printing press, monetizing government deficits. A central bank that is a slave to the spending proclivities of politicians cannot make credible inflation commitments, and cannot effectively conduct counter-cyclical policy.

Stable Policy, Stable Economy

Activist policies for economic stabilization are often perversely destabilizing for a variety of reasons. Good timing requires good forecasts, but economic forecasting is notoriously difficult. The magnitude and timing of fiscal initiatives are usually wrong, and this is compounded by wasteful planning, allocative dysfunction, and a general absence of restraint among political leaders as well as the federal bureaucracy..

Predicting the effects of monetary policy is equally difficult and, more often than not, leads to episodes of over- and under-adjustment. In addition, the wrong targets, the wrong operating approach, and occasional displays of subservience to fiscal pressure undermine successful stabilization. All of these issues lead to doubts about the credibility of policy commitments. Stated intentions are looked upon with doubt, increasing uncertainty and setting in motion behaviors that lead to undesirable economic consequences.

The best policies are those that can be relied upon by private actors, both as a matter of fulfilling expectations and avoiding destabilization. Federal budget policy should promote stability, but that’s not achievable institutions unable to constrain growth in spending and deficits. Budget balance would promote stability and should be the norm over business cycles, or perhaps over periods as long as typical 10-year budget horizons. Stimulus and restraint on the fiscal side should be limited to the effects of so-called automatic stabilizers, such as tax rates and unemployment compensation. On the monetary side, the Fed would do more to stabilize the economy by adopting formal rules, whether a constant rate of money growth or symmetric targeting of nominal GDP.

To the great chagrin of some market watchers, the Federal Reserve Open Market Committee (FOMC) increased its target for the federal funds rate in March by 0.25 points, to range of 4.75 – 5%. This was pretty much in line with plans the FOMC made plain in the fall. The “surprise” was that this increase took place against a backdrop of liquidity shortfalls in the banking system, which also had taken many by surprise. Perhaps a further surprise was that after a few days of reflection, the market didn’t seem to mind the rate hike all that much.

Switchman Sleeping

There’s plenty of blame to go around for bank liquidity problems. Certain banks and their regulators (including the Fed) somehow failed to anticipate that carrying large, unhedged positions in low-rate, long-term bonds might at some point alarm large depositors as interest rates rose. Those banks found themselves way short of funds needed to satisfy justifiably skittish account holders. A couple of banks were closed, but the FDIC agreed to insure all of their depositors. As the lender of last resort, the Fed provided banks with “credit facilities” to ease the liquidity crunch. In a matter of days, the fresh credit expanded the Fed’s balance sheet, offsetting months of “quantitative tightening” that had taken place since last June.

Of course, the Fed is no stranger to dozing at the switch. Historically, the central bank has failed to anticipate changes wrought by its own policy actions. Today’s inflation is a prime example. That kind of difficulty is to be expected given the “long and variable lags” in the effects of monetary policy on the economy. It makes activist policy all the more hazardous, leading to the kinds of “boom and bust” cycles described in Austrian business cycle theory.

Persistent Inflation

When the Fed went forward with the 25 basis point hike in the funds rate target in March, it was greeted with dismay by those still hopeful for a “soft landing”. In the Fed’s defense, one could say the continued effort to tighten policy is an attempt to make up for past sins, namely the Fed’s monetary profligacy during the pandemic.

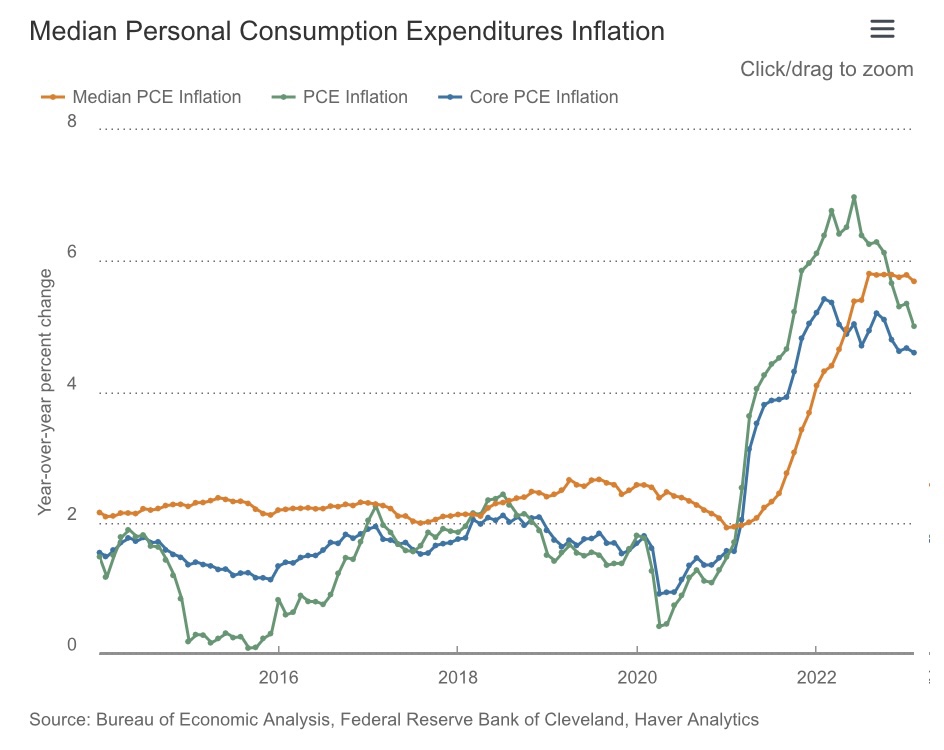

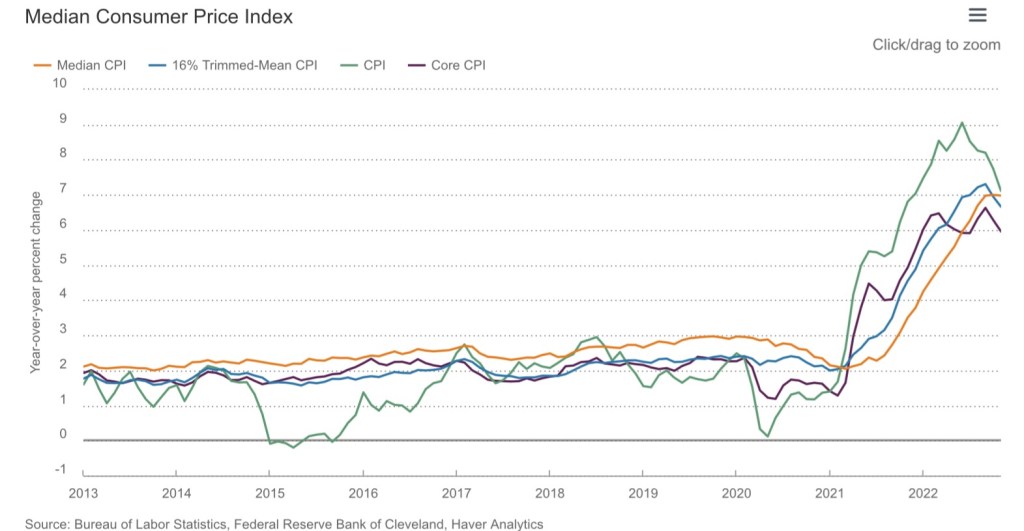

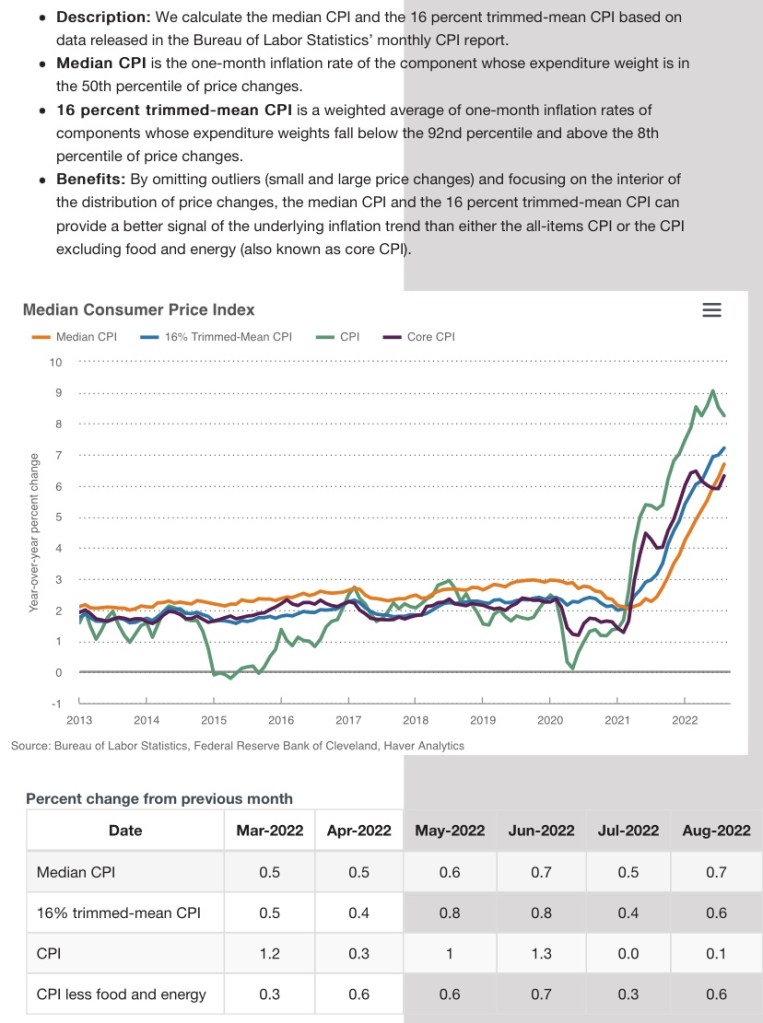

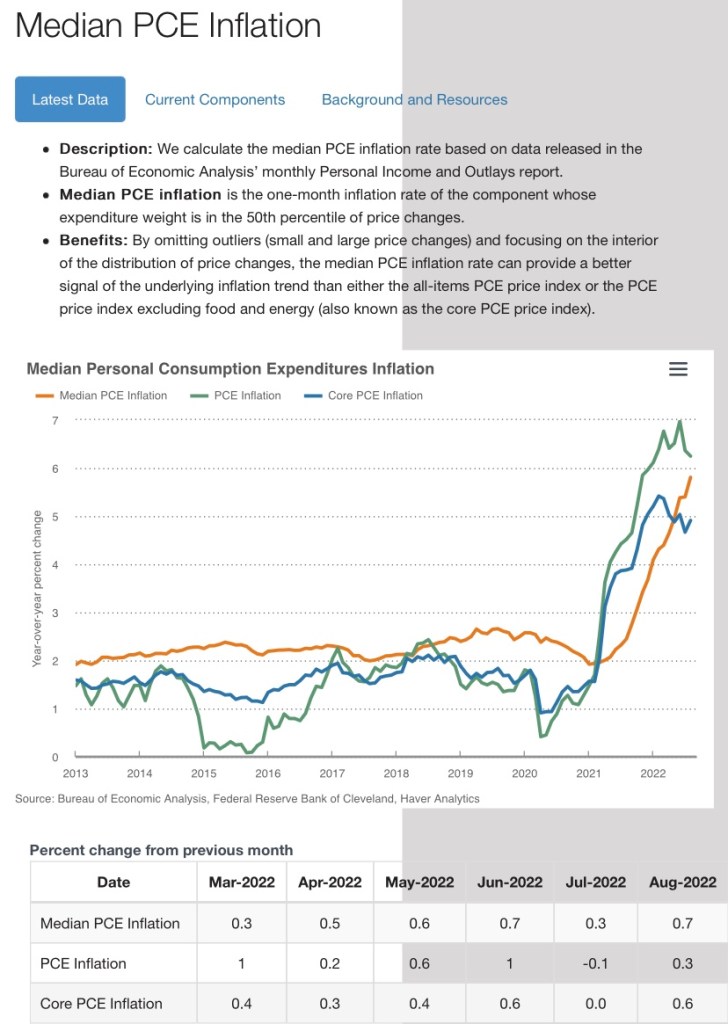

The Fed’s rationale for this latest rate hike was that inflation remains persistent. Here are four CPI measures from the Cleveland Fed, which show some recent tapering of price pressures. Perhaps “flattening” would be a better description, at least for the median CPI:

Those are 12-month changes, and just in case you’ve heard that month-to-month changes have tapered more sharply, that really wasn’t the case in January and February:

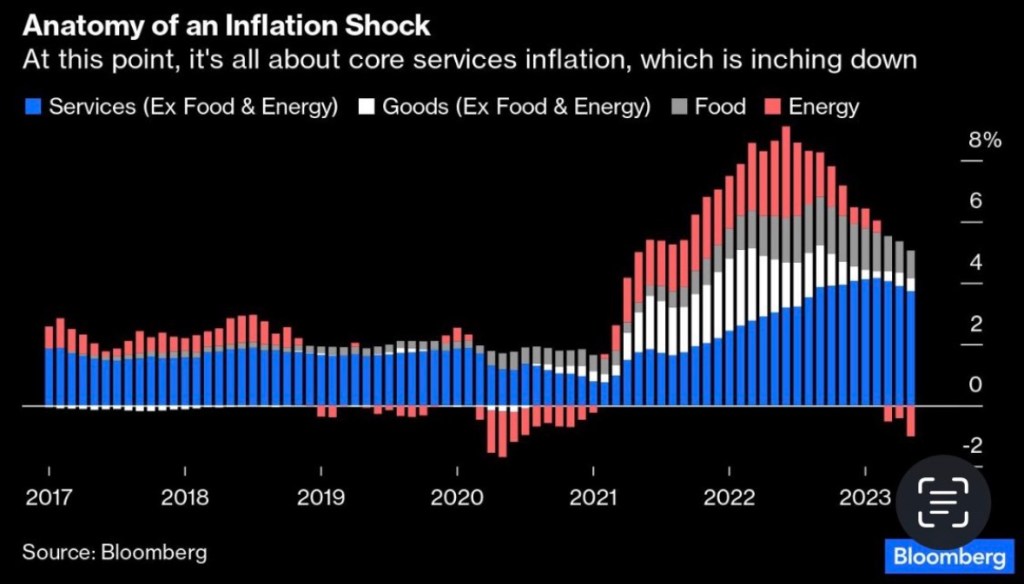

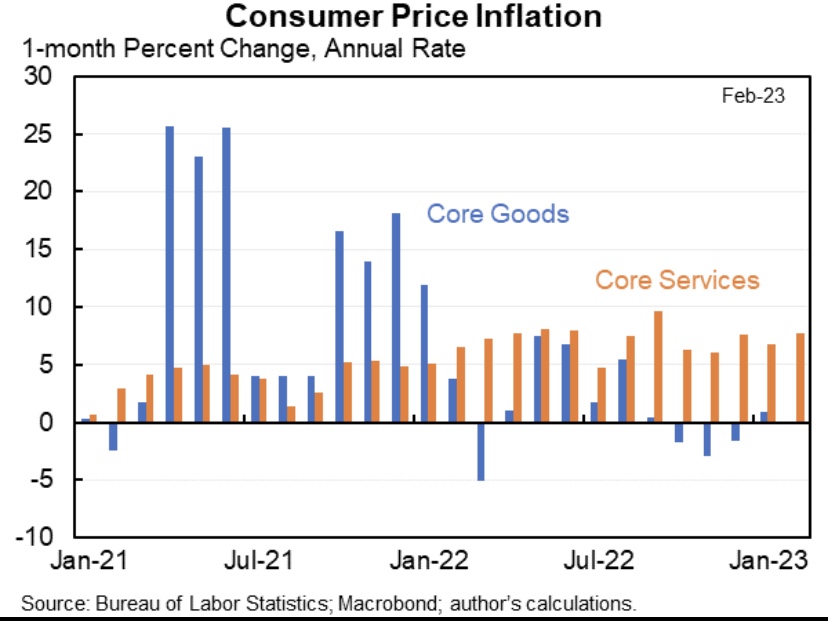

Jason Furman notedin a series of tweets that the prices of services are driving recent inflation, while goods prices have been flat:

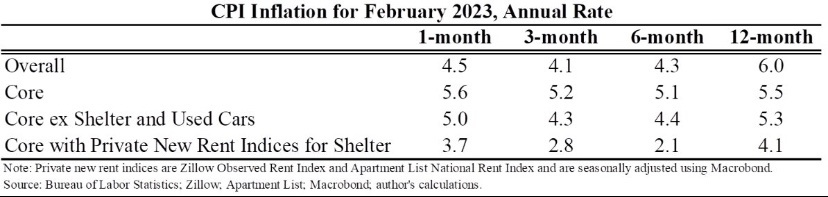

A compelling argument is that the shelter component of the CPI is overstating services inflation, and it’s weighted at more than one-third of the overall index. CPI shelter costs are known as “owner’s equivalent rent” (OER), which is based on a survey question of homeowners as to the rents they think they could command, and it is subject to a fairly long lag. Actual rent inflation has slowed sharply since last summer, so the shelter component is likely to relieve pressure on CPI inflation (and the Fed) in coming months. Nevertheless, Furman points out that CPI inflation over the past 3 -4 months was up even when housing is excluded. Substituting a private “new rent” measure of housing costs for OER would bring measured inflation in services closer the Fed’s comfort zone, however.

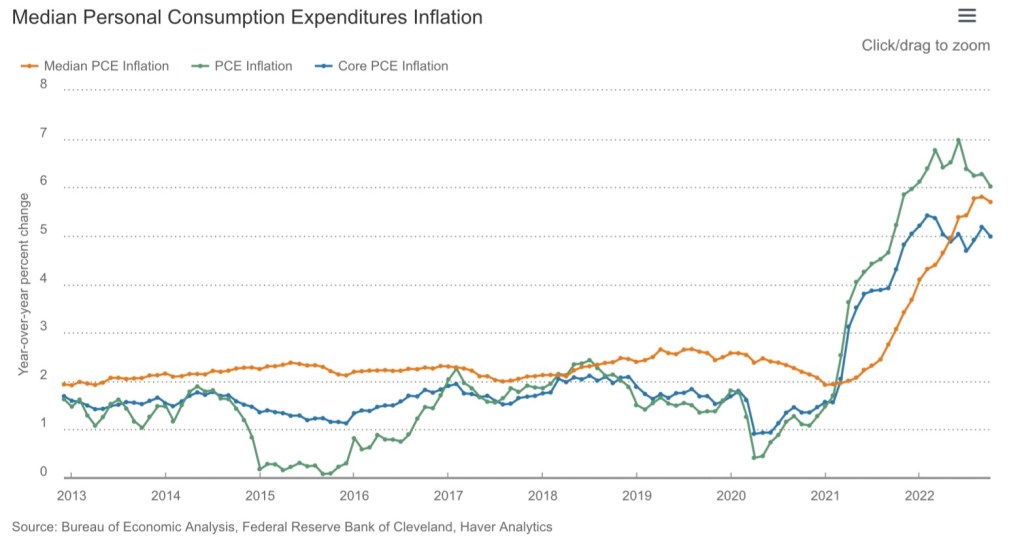

The Fed’s preferred measure of inflation, the deflator for personal consumption expenditures (PCE), uses a much lower weight on housing costs, though it might also overstate inflation within that component. Here’s another chart from the Cleveland Fed:

Inflation in the Core PCE deflator, which excludes food and energy prices, looks as if it’s “flattened” as well. This persistence is worrisome because inflation is difficult to stop once it becomes embedded in expectations. That’s exactly what the Fed says it’s trying to prevent.

Rate Targets and Money Growth

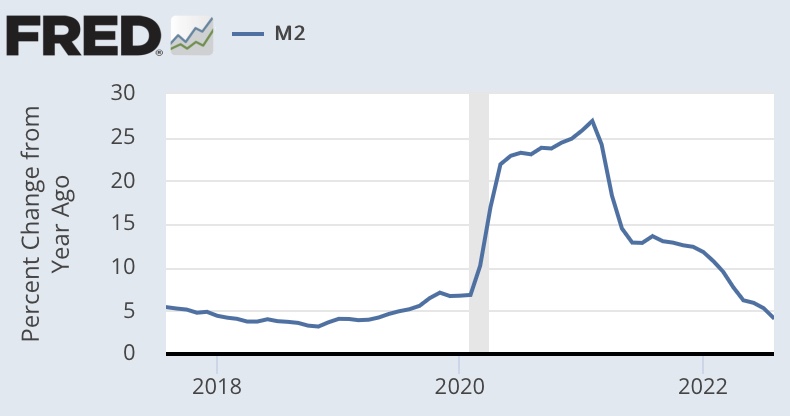

Targeting the federal funds rate (FFR) is the Fed’s primary operational method of conducting monetary policy. The FFR is the rate at which banks borrow from one another overnight to meet short-term needs for reserves. In order to achieve price stability, the Fed would do better to focus directly on controlling the money supply. Nevertheless, it has successfully engineered a decline in the money supply beginning last April, and recently the money supply posted year-over-year negative growth.

That doesn’t mean money growth has been “optimized” in any sense, but a slowdown in money growth was way overdue after the pandemic money creation binge. You might not like the way the Fed executed the reversal or its operating policy in general, and neither do I, but it did restrain money growth. In that sense, I applaud the Fed for exercising its independence, standing up to the Treasury rather than continuing to monetize yawning federal deficits. That’s encouraging, but at some point the Fed will reverse course and ease policy. We’ll probably hope in vain that the Fed can avoid sending us once again along the path of boom and bust cycles.

In effect, the FFR target is a price control with a dynamic element: the master fiddles with the target whenever economic conditions are deemed to suggest a change. This “controlled” rate has a strong influence on other short-term interest rates. The farther out one goes on the maturity spectrum, however, the weaker is the association between changes in the funds rate and other interest rates. The Fed doesn’t truly “control” those rates of most importance to consumers, corporate borrowers, government borrowers, and investors. It definitely influences those rates, but credit risk, business opportunities, and long-term expectations are often dominant.

The FOMC’s latest rate increase suggests its members don’t expect an immediate downturn in economic activity or a definitive near-term drop in inflation. The Committee may, however, be willing to pause for a period of several meeting cycles (every six weeks) to see whether the “long and variable lags” in the transmission of tighter monetary policy might begin to kick-in. As always, the FOMC’s next step will be “data dependent”, as Chairman Powell likes to say. In the meantime, the economic response to earlier tightening moves is likely to strengthen. Lenders are responding to the earlier rate hikes and reduced lending margins by curtailing credit and attempting to rebuild their own liquidity.

Is It Supply Or Demand?

There’s an ongoing debate about whether monetary policy is appropriate for fighting this episode of inflation. It’s true that monetary policy is ill-suited to addressing supply disruptions, though it can help to stem expectations that might cause supply-side price pressures to feed upon themselves (and prevent them from becoming demand-side pressures). However, profligate fiscal and monetary policy did much to create the current inflation, which is pressure on the demand-side. On that point, David Beckworth leaves little doubt as to where he stands:

“The real world is nominal. And nominal PCE was about $1.6 trillion above trend thru February. Unless one believes in immaculate above-trend spending, this huge surge could 𝙣𝙤𝙩 have happened without support from fiscal and monetary policy.”

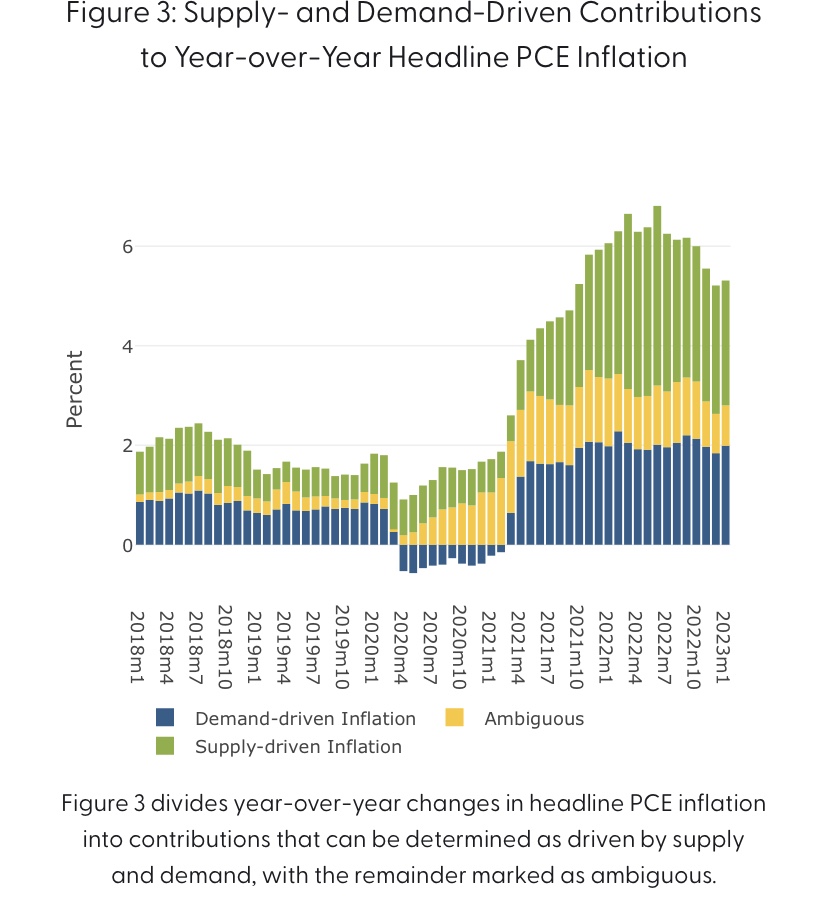

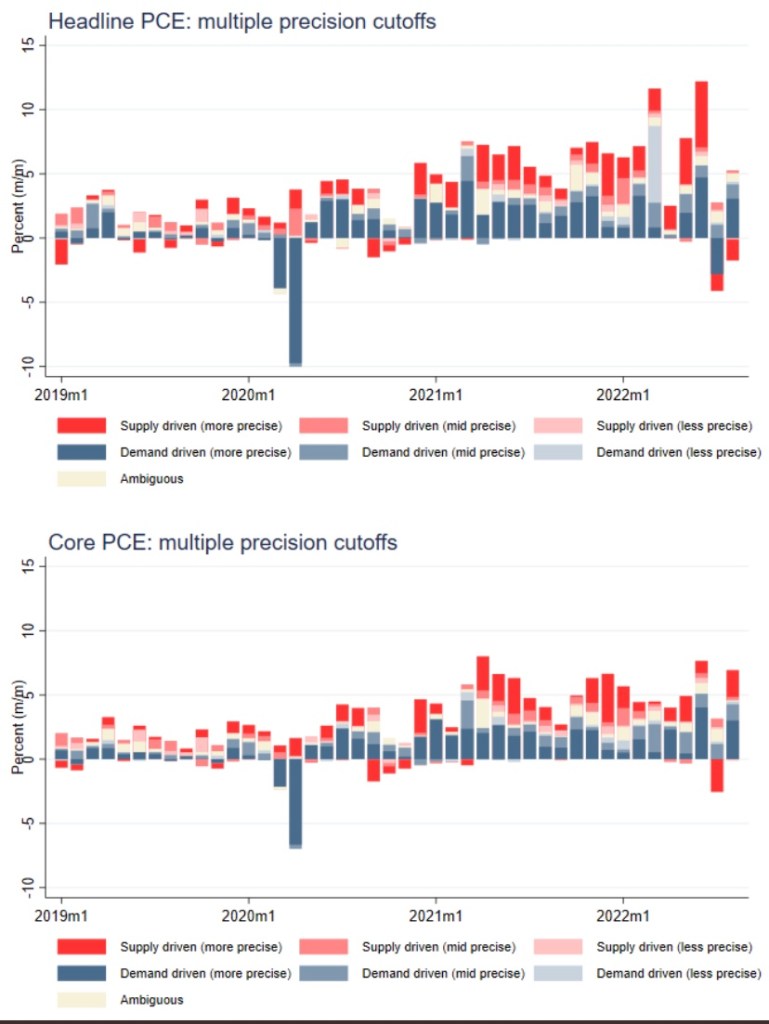

In reality, this inflationary episode was borne of a mix of demand and supply-side pressures, and policy either caused or accommodated all of it. Nevertheless, it’s interesting to consider efforts to decompose these forces. This NBER paper attributed about 2/3 of inflation from December 2019 – June 2022 to the demand-side. Given the ongoing tenor of fiscal policy and the typical policy lags, it’s likely that the effects of fiscal and monetary stimulus have persisted well beyond that point. Here is a page from the San Francisco Fed’s site that gives an edge to supply-side factors, as reflected in this breakdown of the Fed’s favorite inflation gauge:

Of course, all of these decompositions are based on assumptions and are, at best, model-based. Nevertheless, to the extent that we still face supply constraints, they would impose limits to the Fed’s ability to manage inflation downward without a “hard landing”.

There’s also no doubt that supply side policies would reduce the kinds of price pressures we’re now experiencing. Regulation and restrictive energy policies under the Biden Administration have eroded productive capacity. These policies could be reversed if political leaders were serious about improving the nation’s economic health.

The Dark Runway Ahead

Will we have a recession? And when? There are no definite signs of an approaching downturn in the real economy just yet. Inventories of goods did account for more than half of the fourth quarter gain in GDP, which may now be discouraging production. There are layoffs in some critical industries such as tech, but we’ll have to see whether there is new evidence of overall weakness in next Friday’s employment report. Real wages have been a little down to flat over the past year, while consumer debt is climbing and real retail sales have trended slightly downward since last spring. Many firms will experience higher debt servicing costs going forward. So it’s not clear that the onset of recession is close at hand, but the odds are good that we’ll see a downturn as the year wears on, especially with credit increasingly scarce in the wake of the liquidity pinch at banks. But no one knows for sure, including the Fed.

It’s as if people view the debt limit controversy as a political nuisance rather than the stopgap enforcement mechanism for fiscal sanity that it’s intended to be. That’s a lesson in how far we’ve gone toward an unhealthy acceptance of permanent federal deficits. Oh, most people seem to realize the the government’s spending is prodigious and beyond our capacity to collect taxes, but many don’t grasp the recklessness of the ongoing blowout. Federal deficits are expected to average $1.6 trillion per year over the next decade, versus less than $0.9 trillion and $1.25 trillion over the two previous decades, respectively. That $1.25 trillion includes the massive (and excessive) transfers that took place during the pandemic, which is why we’ve bumped up against the debt limit earlier than had been expected. The trend isn’t abating, despite the fact that the pandemic is behind us. And keep in mind that the Congressional Budget Office has been too optimistic for the past 20 years or so. Take a look at federal debt relative to GDP:

Unpleasant Arithmetic

With federal debt growing faster than GDP, the burden of servicing the debt mounts. This creates a strain in the coordination of fiscal and monetary policy, as described by David Andolfatto, who last year reviewed the implications of “Some Unpleasant Monetarist Arithmetic” for current policy. His title was taken from a seminal paper written by Thomas Sargent and Neil Wallace in 1981. Andolfatto says that:

“… attempting to monetize a smaller fraction of outstanding Treasury securities has the effect of increasing the rate of inflation. A tighter monetary policy ends up increasing the interest expense of debt issuance. And if the fiscal authority is unwilling to curtail the rate of debt issuance, the added interest expense must be monetized—at least if outright default is to be avoided.

Andolfatto wrote that last spring, before the Federal Reserve began its ongoing campaign to tighten monetary policy by raising short-term interest rates. But he went on to say:

“Deficit and debt levels are elevated relative to their historical norms, and the current administration seems poised to embark on an ambitious public spending program. … In the event that inflation rises and then remains intolerably above target, the Federal Reserve is expected to raise its policy rate. … if the fiscal authority is determined to pursue its deficit policy into the indefinite future, raising the policy rate may only keep a lid on inflation temporarily and possibly only at the expense of a recession. In the longer run, an aggressive interest rate policy may contribute to inflationary pressure—at least until the fiscal regime changes.”

So it is with a spendthrift government: escalating debt and interest expense must ultimately be dealt with via higher taxes or inflation, despite the best intentions of a monetary authority.

Fiscal Wrasslin’

Some people think the debt limit debate is all a big fake. Maybe … there are spendthrifts on both sides of the aisle. Still, the current debt limit impasse could serve a useful purpose if fiscal conservatives succeed in efforts to restrain spending. There is, however, an exaggerated uproar over the possibility of default, meaning a failure to make scheduled payments on Treasury securities. The capital markets aren’t especially worried because an outright default is very unlikely. Establishment Republicans may well resort to their usual cowardice and accept compromise without holding out for better controls on spending. Already, in a politically defensive gesture, House Speaker Kevin McCarthy has said the GOP wishes to strengthen certain entitlement programs. Let’s hope he really means restoring solvency to the Social Security and Medicare Trust Funds via fundamental reforms. And if the GOP rules out cuts to any program, let’s hope they don’t rule out cuts in the growth of these programs, or privatization. For their part, of course, Democrats would like to eliminate the debt ceiling entirely.

One of the demands made by Republicans is a transformation of the federal tax system. They would like to eliminate the income tax and substitute a tax on consumption. Economists have long favored the latter because it would eliminate incentives that penalize saving, which undermine economic growth. Unfortunately, this is almost dead in the water as a political matter, but the GOP further sabotaged their own proposal in their zeal to abolish the IRS. Their consumption tax would be implemented as a national sales tax applied at the point of sale, complete with a new Treasury agency to administer the tax. They’d have done better to propose a value added tax (VAT) or a tax on a simple base of income less saving (and other allowances).

Gimmicks and Measures

We’ve seen proposals for various accounting tricks to allow the government to avoid a technical default and buy time for an agreement to be reached on the debt limit. Treasury Secretary Janet Yellen already has implemented “extraordinary measures” to stay under the debt limit until June, she estimates. The Treasury is drawing down cash, skipping additional investments in government retirement accounts (which can be made up later without any postponement of benefits), plus a few other creative accounting maneuvers.

Payment prioritization, whereby the Treasury makes payments on debt and critical programs such as Social Security and Medicare, but defers a variety of other payments, has also been considered. Those deferrals could include amounts owed to contractors or even government salaries. However, a deferral of payments owed to anyone represents a de facto default. Thus, payment prioritization is not a popular idea, but if push comes to shove, it might be viewed as the lesser of two evils. Missing payments on government bonds could precipitate a financial crisis, but no one believes it will come to that.

Two other ideas for avoiding a breach of the debt ceiling are rather audacious. One involves raising new cash via the sale of premium bonds by the Treasury, as described here by Josh Barro (and here by Matt Levine). The other idea is to mint a large denomination ($1 trillion) platinum, “commemorative” coin, which the Treasury would deposit at the Federal Reserve, enabling it to conduct business as usual until the debt limit impasse is resolved. I’ll briefly describe each of these ideas in more detail below.

Premium Bonds

Premium bonds would offer a solution to the debt limit controversy because the debt ceiling is defined in terms of the par value of Treasury debt outstanding, as opposed to the amount actually raised from selling bonds at auction. For example, a note that promises to pay $100 in one year has a par value of $100. If it also promises to pay $100 in interest, it will sell at a steep premium. Thus, the Treasury collects, say, $185 at auction, and it could use the proceeds to pay off $100 of maturing debt and fund $85 of federal spending. That would almost certainly require a “market test” by the Treasury on a limited scale, and the very idea might reveal any distaste the market might have for obviating the debt limit in this fashion. But distaste is probably too mild a word.

An extreme example of this idea is for the Treasury to sell perpetuities, which have a zero par value but pay interest forever, or at least until redeemed beyond some minimum (but lengthy) term. John Cochrane has made this suggestion, though mainly just “for fun”. The British government sold perpetuities called consols for many years. Such bonds would completely circumvent the debt limit, at least without legislation to redefine the limit, which really is long overdue.

The $1 Trillion Coin

Minting a trillion dollar coin is another thing entirely. Barro has a separate discussion of this option, as does Cochrane. The idea was originally proposed and rejected during an earlier debt-limit controversy in 2011. Keep in mind, in what follows, that the Fed does not follow Generally Accepted Accounting Principles (GAAP).

Skeptics might be tempted to conclude that the “coin trick” is a ploy to engineer a huge increase the money supply to fund government expansion, but that’s not really the gist of this proposal. Instead, the Treasury would deposit the coin in its account at the Fed. The Fed would hold the coin and give the Treasury access to a like amount of cash. To raise that cash, the Fed would sell to the public $1 trillion out of its massive holdings of government securities. The Treasury would use that cash to meet its obligations without exceeding the debt ceiling. As Barro says, the Fed would essentially substitute sales of government bonds from its portfolio for bonds the Treasury is prohibited from selling under the debt limit. The effect on the supply of money is basically zero, and it is non-inflationary unless the approach has an unsettling impact on markets and inflation expectations (which of course is a distinct possibility).

When the debt ceiling is finally increased by Congress, the process is reversed. The Treasury can borrow again and redeem its coin from the Fed for $1 trillion, then “melt it down”, as Barro says. The Fed would repurchase from the public the government securities it had sold, adding them back to its portfolio (if that is consistent with its objectives at that time). Everything is a wash with respect to the “coin trick”, as long as the Treasury ultimately gets a higher debt limit.

Lust For the Coin

In fairness to skeptics, it’s easy to understand why the “coin trick” described above might be confused with another coin minting idea that arose from the collectivist vanguard during the pandemic. Representative Rashida Tlaib (D-MI) proposed minting coins to fund monthly relief payments of $1,000 – $2,000 for every American via electronic benefit cards. She was assisted in crafting this proposal by Rohan Grey, a prominent advocate of Modern Monetary Theory (MMT), the misguided idea that government can simply print money to pay for the resources it demands without inflationary consequences.

Tlaib’s plan would have required the Federal Reserve to accept the minted coins as deposits into the Treasury’s checking account. But then, rather than neutralizing the impact on the money supply by selling government bonds, the coin itself would be treated as base money. Cash balances would simply be made available in the Treasury’s checking account with the Fed. That’s money printing, pure and simple, but it’s not at all the mechanism under discussion with respect to short-term circumvention of the debt limit.

Fed Independence

The “coin trick” as a debt limit work-around is probably an impossibility, as Barro and others point out. First, the Fed would have to accept the coin as a deposit, and it is under no legal obligation to do so. Second, it obligates the Fed to closely coordinate monetary policy with the Treasury, effectively undermining its independence and its ability to pursue its legal mandates of high employment and low inflation. Depending on how badly markets react, it might even present the Fed with conflicting objectives.

Believe me, you might not like the Fed, but we certainly don’t want a Fed that is subservient to the Treasury… maintaining financial and economic stability in the presence of an irresponsible fiscal authority is bad enough without seating that authority at the table. As Barro says of the “coin trick”:

“These actions would politicize the Fed and undermine its independence. In order to stabilize expectations about inflation, the Fed would have to communicate very clearly about its intentions to coordinate its fiscal actions with Treasury — that is, it would have to tell the world that it’s going to act as Treasury’s surrogate in selling bonds when Treasury can’t. …

These actions would interfere with the Fed’s normal monetary operations. … the Fed is currently already reducing its holdings of bonds as part of its strategy to fight inflation. If economic conditions change (fairly likely, in the event of a near-default situation) that might change the Fed’s desired balance sheet strategy.”

On With The Show

Discussions about the debt limit continue between the White House and both parties in Congress. Kevin McCarthy met with President Biden today (2/1), but apparently nothing significant came it. Fiscal conservatives wonder whether McCarthy and other members of the GOP lack seriousness when it comes to fiscal restraint. But spending growth must slow to achieve deficit reduction, non-inflationary growth, and financial stability.

Meanwhile, even conservative media pundits seem to focus only on the negative politics of deficit reduction, ceding the advantage to Democrats and other fiscal expansionists. For those pundits, the economic reality pales in significance. That is a mistake. Market participants are increasingly skeptical that the federal government will ever pay down its debts out of future surpluses. This will undermine the real value of government debt, other nominal assets, incomes and buying power. That’s the inflation tax in action.

Unbridled growth of the government’s claims on resources at the expense of the private sector destroys the economy’s productive potential, to say nothing of growth. The same goes for government’s insatiable urge to regulate private activities and to direct patterns of private resource use. Unfortunately, so many policy areas are in need of reform that imposition of top-down controls on spending seems attractive as a stopgap. Concessions on the debt limit should only be granted in exchange for meaningful change: limits on spending growth, regulatory reforms, and tax simplification (perhaps replacing the income tax with a consumption tax) should all be priorities.

In the meantime, let’s avoid trillion dollar coins. As a debt limit work-around, premium bonds are more practical without requiring any compromise to the Fed’s independence. Other accounting gimmicks will be used to avoid missing payments, of course, but the fact that premium bonds and platinum coins are under discussion highlights the need to redefine the debt limit. When the eventual time of default draws near, fiscal conservatives must be prepared to stand up to their opponents’ convenient accusations of “brinksmanship”. The allegation is insincere and merely a cover for government expansionism.

The answer to that question, kids, is a resounding no! The Federal Reserve created far too much liquidity during and after the pandemic and waited too long to reverse that policy. That’s a common view among the “monetarazzi”, but far too many analysts, in the next breath, assert that the Fed is going too far in tightening policy. Sorry, but you can’t have it both ways! Thus far, the reductions we’ve seen in the monetary aggregates (M1, M2, M3) represent barely a trickle out of the ocean of liquidity released during the previous two years. The recent slight moderation in the rate of inflation is unlikely to gain momentum without persistence by the Fed.

This Could Be Easier

I humbly concede, however, that a different approach by the Fed might have been less disruptive. A better alternative would have involved more aggressive reductions in the gigantic portfolio of securities it acquired via “quantitative easing” (QE) during the pandemic while avoiding direct intervention to raise short-term interest rates. In fact, allowing interest rates to be determined by the market, rather than via central bank intervention, is more sensible in terms of pricing debt of any duration. It also suggests a more direct and sensible approach to managing the growth of the money supply. Of course, had the Fed unwound QE more aggressively, short-term rates would surely have risen anyway, but to levels appropriate to rationing liquidity more efficiently. Furthermore, those rates could have served as a useful indicator of the market’s ability to digest a particular volume of sales from the Fed’s portfolio.

Getting Tight

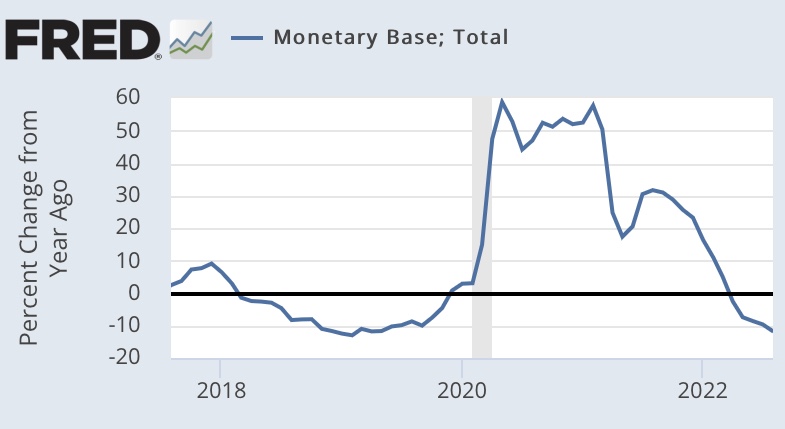

The chart below shows the level of the monetary base (bank reserves plus currency) over the past five years from the Trading Economics site. The monetary base is the narrow monetary aggregate supporting growth of the money stock and is under fairly direct control of the Fed.

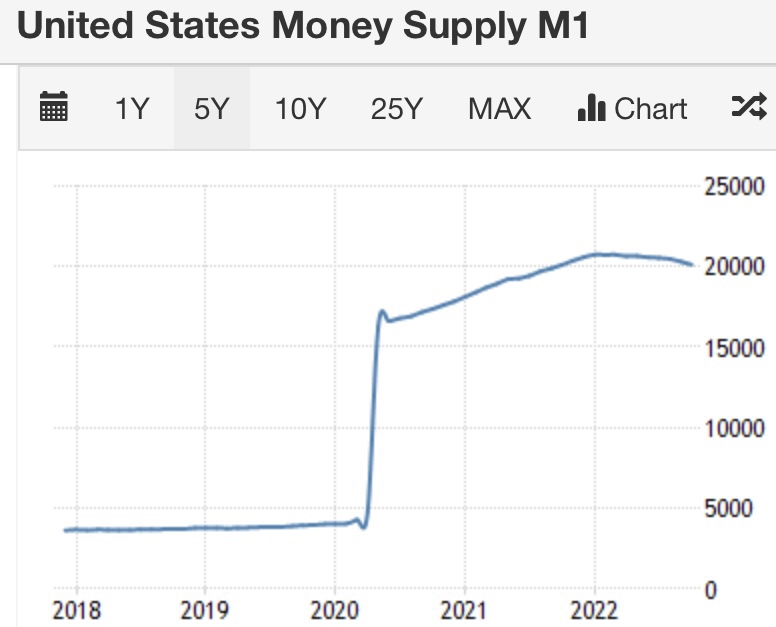

The base has declined substantially during 2022 largely as a consequence of the Fed’s restrictive policies. However, it has retraced only about a third of the massive expansion engineered by the Fed over the two prior years. Here is the corresponding plot of the M1 money stock (currency plus checking deposits):

So the reductions in the base have yet to translate into much of a reduction in the money stock, though growth in all of the aggregates has certainly declined. No one thinks this will be a walk in the park. Withdrawing liquid capital from markets accustomed to swilling in excesses will have consequences, particularly for investors who’ve grown undisciplined in their approach to evaluating prospective assets. Investors and society at large inevitably pay the price for the malinvestment encouraged by unbridled money growth (not to mention misdirected industrial policies … that’s a different can of worms).

But the squeamish resist! I got a kick out of this tweet by Noah Smith in which he pokes fun at those who insist that the surge in inflation was a mere transitory phenomenon:

“Team Transitory: OMG inflation is just going to go away, you don’t need to raise interest rates.

Fed: *raises interest rates*

Inflation: *goes down a bit*

Team Transitory: SEE, I told you inflation was going away and that you didn’t need to raise interest rates!!”

Well, in fairness, “Team Transitory” has been fixated on supply disruptions that very well should resolve with private efforts over time. Some have resolved already. And again, we’ve yet to feel much impact from the Fed’s tighter policy, but I’m amused by the tweet nevertheless.

In fact, the surge in inflation has been driven by both supply and demand factors, and it’s true the Fed can do very little about the former. But stalling the effort to purge excess liquidity and demand-side inflation risks allowing expectations of inflation to edge higher, creating an environment in which price pressures are more resistant to policy actions.

Inflation And Its Proximate Sources

It is indeed good news that inflation has tapered slightly over the past few months, or at least the “headline” inflation numbers have tapered. Weaker energy prices helped a great deal, though releases from the Strategic Petroleum Reserve aren’t sustainable. Measures of “core” inflation that exclude food and energy prices, and more central measures of inflation within the spectrum of goods and services, have moved sideways or perhaps shown signs of a slight moderation.

Here’s a plot of several measures of CPI inflation taken from the Cleveland Fed’s web site. Note that the median component of the CPI has finally hit a plateau, and a “trimmed” measure that excludes CPI components with extreme changes has dipped slightly. The Core CPI has fluctuated in a range just above 6% for most of the year.

The deflator for personal consumption expenditures (PCE) gets more emphasis from the Fed in its policy deliberations. The latest release at the start of December showed patterns similar to the CPI:

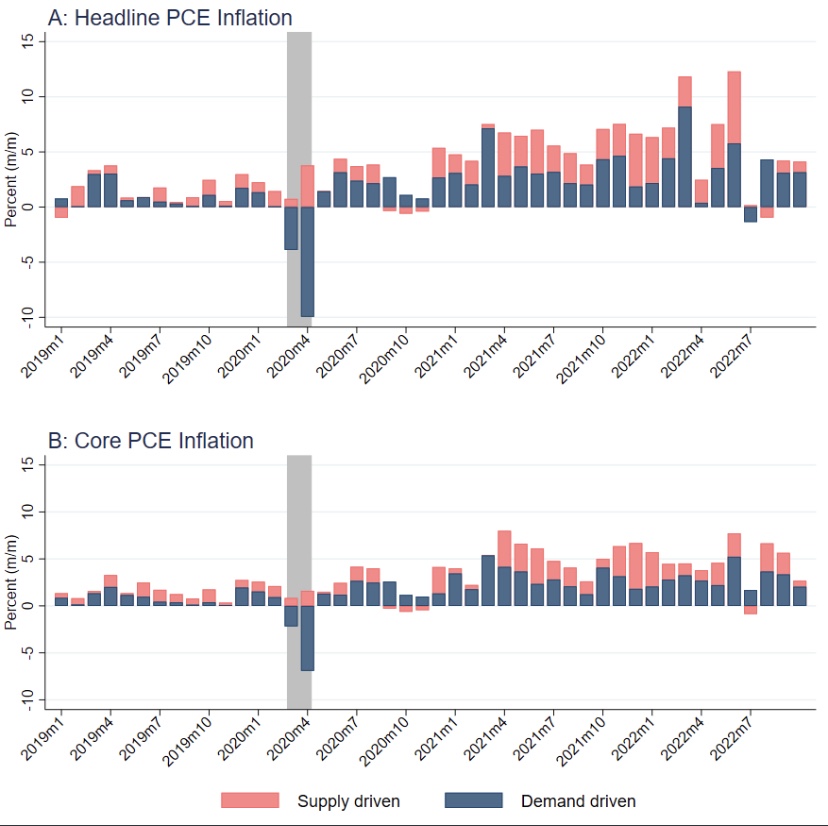

With respect to the PCE deflator, the slight dampening of price pressure we’ve seen recently came primarily from the supply side, with some progress on the demand side as well. Energy was one factor on the supply side, but even the core PCE deflator shows less supply pressure. Adam Shapiro has a decomposition of the PCE deflator into supply-driven and demand-driven components (but the chart only goes through October):

First, without endorsing Shapiro’s construction of this dichotomy, I note that the impact of monetary policy is primarily through the demand side of the economy. Of course, monetary instability isn’t good for producers, and excessive money growth and inflation create uncertainty that inhibits supply. But what we’ve seen recently has more to do with the curing of supply chain bottlenecks that cropped up during the pandemic (or in its wake), and Shapiro attempts to capture that kind of phenomenon here.

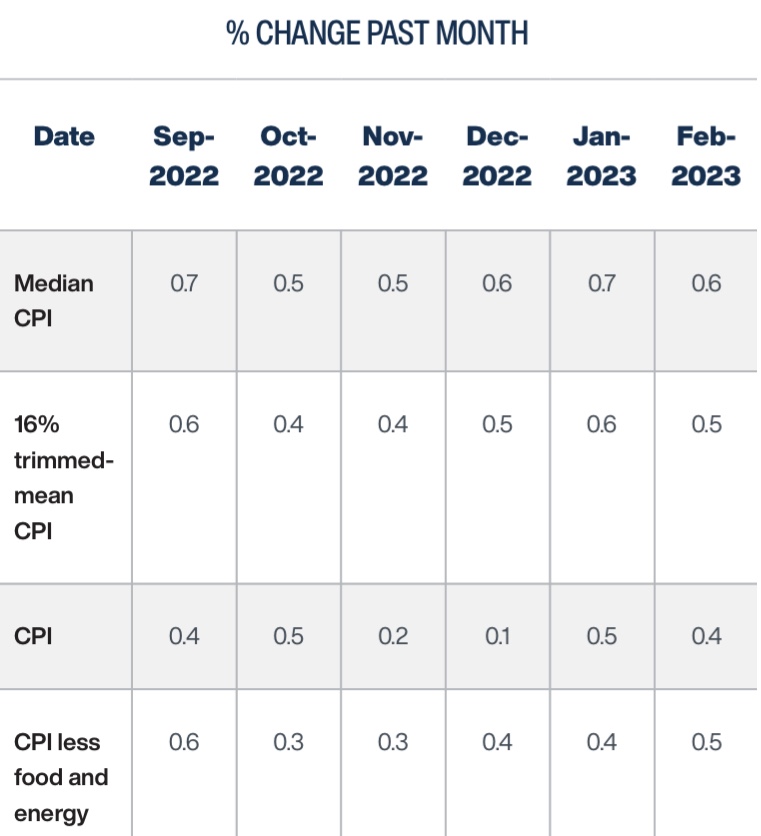

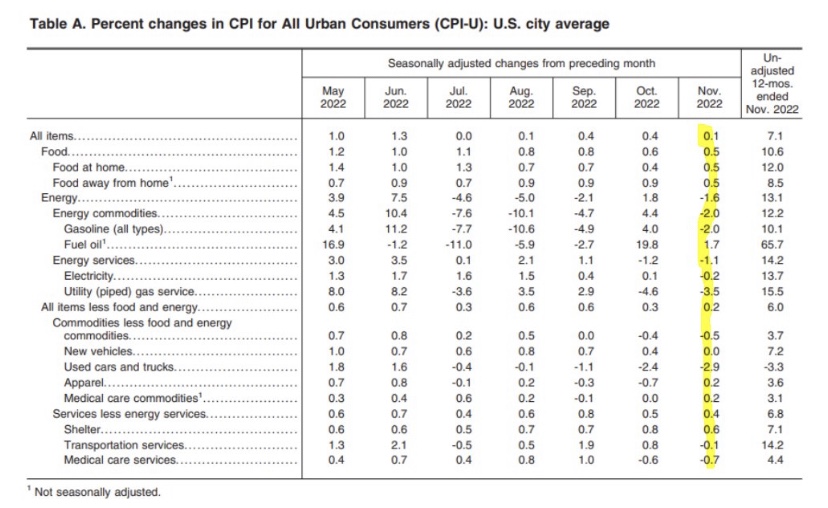

Still, many would argue that the November CPI showed sufficient progress for the Fed to pause its tightening campaign. The reductions in the monthly price increases were fairly widespread, as shown by this table from the CPI report:

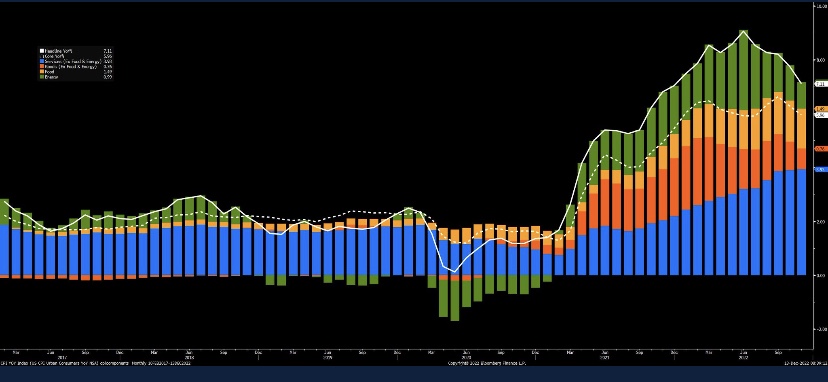

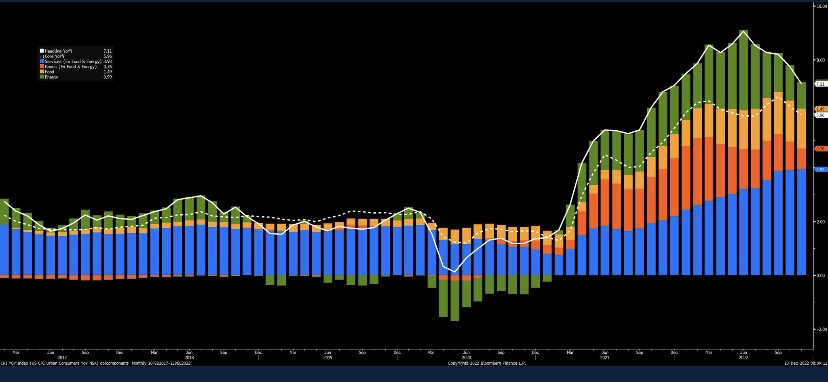

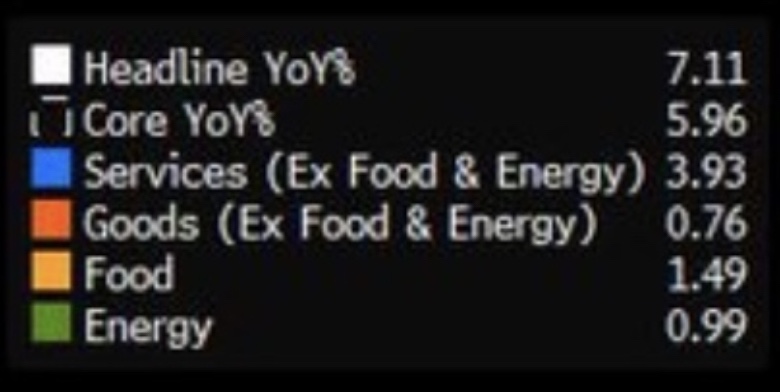

The next chart from Joe Wiesenthal (via Bloomberg) displays trends in broad CPI categories, but it shows vividly that the reductions were concentrated in energy components and goods prices, while services and food inflation did not really abate. (The legend is so hard to read that I took the liberty of blowing it up a bit below the chart itself):

Playing Catch-Up

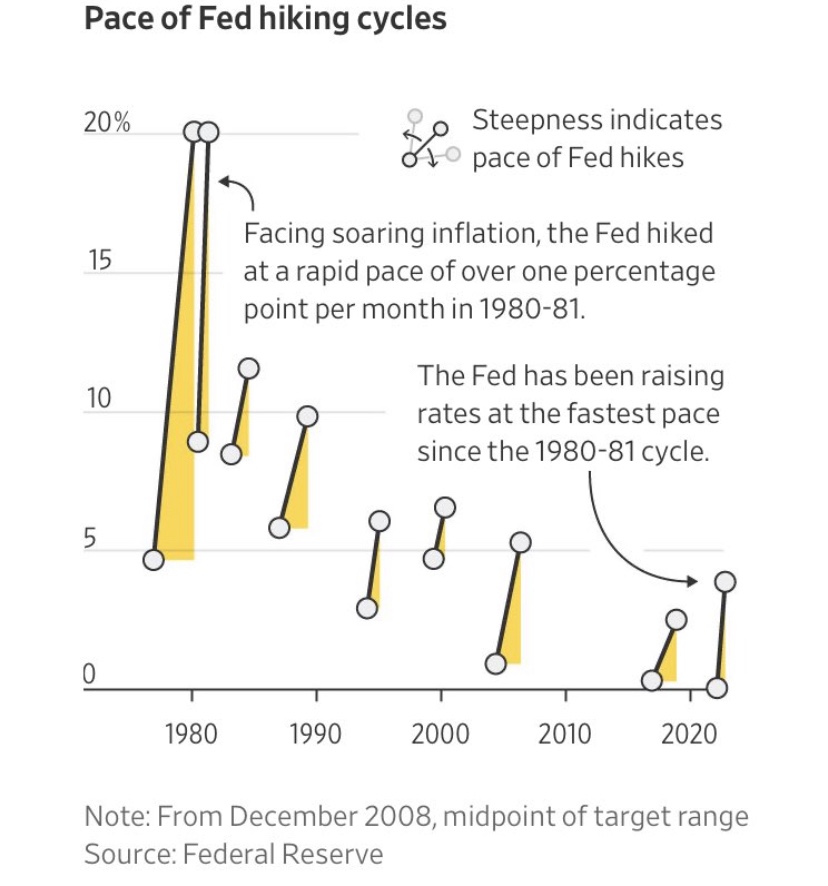

While the Fed’s effort to restrain inflation began in earnest in the spring of this year, it lifted the federal funds rate target rapidly. Here’s another chart from Adam Shapiro, via the Wall Street Journal: the Fed’s current tightening cycle is the fastest in 40 years in terms of those rate hikes:

Fast, yes, but they got a late start in the face of a rapid acceleration of inflation, and for what it’s worth, the Fed’s rate target remains below the rate of inflation. Yes, I’m forced to acknowledge here that the Fed’s preference for rate intervention and targeting is just what they do, for now. In any case, top-line inflation and strictly demand-side inflation are still above the Fed’s 2% target.

Fabian Fiscal Expansionists

One “fix” recommended in some circles suggests that the Fed’s inflation target is too low, as if price stability had nothing to do with its mandate! The idea that low-grade inflation is a healthy thing has never been convincingly demonstrated. In fact, the monetary literature leans strongly in the direction of price stability and an optimal rate of inflation of zero! That the Fed should aim for higher inflation seems like a cop-out intended to appease those who still subscribe to the discredited notion that there exists a reliable long-run tradeoff between inflation and unemployment.

In fact, proposals to increase the central bank’s inflation target would enable more deficit spending financed with the “printing press”, which is at the root of the demand-side inflation problem we now face. A major justifications for ballooning levels of federal spending has been so-called Modern Monetary Theory (MMM), which has gained adherents among statists in the years since the Great Recession. MMM holds that “important” initiatives can simply be paid for with new money creation, rather than interest bearing debt, or God forbid, taxes! “Partisan” is probably a better description than “theorist” for any fan of MMM, and they have convinced themselves that money financed deficits are without inflationary consequences. Of course, this represents a complete suspension of the law of resource scarcity, not to mention years of monetary history. Raising the Fed’s inflation target plays well with the same free-lunch advocates who rally behind MMM.

The Fed’s Unfaithful Fiscal Partner

Federal budget control is likely to take another hit this week with passage of the $1.7 omnibus spending bill. It includes spending increases with no immediate offsets as required under the pay-as-you-go budget law. It delays those offsets to 2025 and increases deficits in the interim by hundreds of billions of dollars. It also sets a new, higher baseline for discretionary appropriations in future years. The federal deficit has already risen dramatically compared to a year ago under the fiscal profligacy of Congress and the Administration. Another contributing factor, however, is that the interest cost of servicing the national debt has spiked as interest rates have risen. Needless to say, none this makes the Fed’s job any easier, especially as it seeks to reverse QE.

Say Uncle!?

When will the Fed begin to take its foot off the brake? It “only” raised the Fed funds target by 50 basis points at its meeting last week (after four 75 bps moves in a row. It is expected to raise the target another 50 bps in early February and perhaps another 25 in March. Strong signals of imminent recession would be needed for the Fed to call it off any sooner, and we’re definitely seeing more hints of a weakening economy in the data (and see here, here, here, and here). More definitive declines in inflation would obviously help settle things. Otherwise, the Fed may pause after March in order to gauge progress toward its goal of 2% inflation.

The debate over the Federal Reserve’s policy stance has undergone an interesting but understandable shift, though I disagree with the “new” sentiment. For the better part of this year, the consensus was that the Fed waited too long and was too dovish about tightening monetary policy, and I agree. Inflation ran at rates far in excess of the Fed’s target, but the necessary correction was delayed and weak at the start. This violated the necessary symmetry of a legitimate inflation-targeting regime under which the Fed claims to operate, and it fostered demand-side pressure on prices while risking embedded expectations of higher prices. The Fed was said to be “behind the curve”.

Punch Bowl Resentment

The past few weeks have seen equity markets tank amid rising interest rates and growing fears of recession. This brought forth a chorus of panicked analysts. Bloomberg has a pretty good take on the shift. Hopes from some economists for a “soft landing” notwithstanding, no one should have imagined that tighter monetary policy would be without risk of an economic downturn. At least the Fed has committed to a more aggressive policy with respect to price stability, which is one of its key mandates. To be clear, however, it would be better if we could always avoid “hard landings”, but the best way to do that is to minimize over-stimulation by following stable policy rules.

Price Trends

Some of the new criticism of the Fed’s tightening is related to a perceived change in inflation signals, and there is obvious logic to that point of view. But have prices really peaked or started to reverse? Economist Jeremy Siegel thinks signs point to lower inflation and believes the Fed is being too aggressive. He cites a series of recent inflation indicators that have been lower in the past month. Certainly a number of commodity prices are generally lower than in the spring, but commodity indices remain well above their year-ago levels and there are new worries about the direction of oil prices, given OPEC’s decision this week to cut production.

Central trends in consumer prices show that there is a threat of inflation that may be fairly resistant to economic weakness and Fed actions, as the following chart demonstrates:

Overall CPI growth stopped accelerating after June, and it wasn’t just moderation in oil prices that held it back (and that moderation might soon reverse). Growth of the Core CPI, which excludes food and energy prices, stopped accelerating a bit earlier, but growth in the CPI and the Core CPI are still running above 8% and 6%, respectively. More worrisome is the continued upward trend in more central measures of CPI growth. Growth in the median component of the CPI continues to accelerate, as has the so-called “Trimmed CPI”, which excludes the most extreme sets of high and low growth components. The response of those central measures lagged behind the overall CPI, but it means there is still inflationary momentum in the economy. There is a substantial risk that expectations of a more permanent inflation are becoming embedded in expectations, and therefore in price and wage setting, including long-term contracts.

The Fed pays more attention to a measure of prices called the Personal Consumption Expenditures (PCE) deflator. Unlike the CPI, the PCE deflator accounts for changes in the composition of a typical “basket” of goods and services. In particular, the Fed focuses most closely on the Core PCE deflator, which excludes food and energy prices. Inflation in the PCE deflator is lower than the CPI, in large part because consumers actively substitute away from products with larger price increases. However, the recent story is similar for these two indices:

Both overall PCE inflation and Core PCE inflation stopped accelerating a few months ago, but growth in the median PCE component has continued to increase. This central measure of inflation still has upward momentum. Again, this raises the prospect that inflationary forces remain strong, and that higher and more widespread expected inflation might make the trend more difficult for the Fed to rein in.

That leaves the Fed little choice if it hopes to bring inflation back down to its target level. It’s really a only a choice of whether to do it faster or slower. One big qualification is that the Fed can’t do much about supply shortfalls, which have been a source of price pressure since the start of the rebound from the pandemic. However, demand pressures have been present since the acceleration in price growth began in earnest in early 2021. At this point, it appears that they are driving the larger part of inflation.

The following chart shows share decompositions for growth in both the “headline” PCE deflator and the Core PCE deflator. Actual inflation rates are NOT shown in these charts. Focus only on the bolder colored bars. (The lighter bars represent estimates having less precision.) Red represents “supply-side” factors contributing to changes in the PCE deflator, while blue summarizes “demand-side” factors. This division is based on a number of assumptions (methodological source at the link), but there is no question that demand has contributed strongly to price pressures. At least that gives a sense about how much of the inflation can be addressed by actions the Fed might take.

I mentioned the role of expectations in laying the groundwork for more permanent inflation. Expected inflation not only becomes embedded in pricing decisions: it also leads to accelerated buying. So expectations of inflation become a self-fulfilling prophesy that manifests on both the supply side and the demand-side. Firms are planning to raise prices in 2023 because input prices are expected to continue rising. In terms of the charts above, however, I suspect this phenomenon is likely to appear in the “ambiguous” category, as it’s not clear that the counting method can discern the impacts of expectations.

What’s a Central Bank To Do?

Has the Fed become too hawkish as inflation accelerated this year while proving to be more persistent than expected? One way to look at that question is to ask whether real interest rates are still conducive to excessive rate-sensitive demand. With PCE inflation running at 6 – 7% and Treasury yields below 4%, real returns are still negative. That’s hardly seems like a prescription for taming inflation, or “hawkish”. Rate increases, however, are not the most reliable guide to the tenor of monetary policy. As both John Cochrane and Scott Sumner point out, interest rate increases are NOT always accompanied by slower money growth or slowing inflation!

However, Cochrane has demonstrated elsewhere that it’s possible the Fed was on the right track with its earlier dovish response, and that price pressures might abate without aggressive action. I’m skeptical to say the least, and continuing fiscal profligacy won’t help in that regard.

The Policy Instrument That Matters

Ultimately, the best indicator that policy has tightened is the dramatic slowdown (and declines) in the growth of the monetary aggregates. The three charts below show five years of year-over-year growth in two monetary measures: the monetary base (bank reserves plus currency in circulation), and M2 (checking, saving, money market accounts plus currency).

Growth of these aggregates slowed sharply in 2021 after the Fed’s aggressive moves to ease liquidity during the first year of the pandemic. The monetary base and M2 growth have slowed much more in 2022 as the realization took hold that inflation was not transitory, as had been hoped. Changes in the growth of the money stock takes time to influence economic activity and inflation, but perhaps the effects have already begun, or probably will in earnest during the first half of 2023.

The Protuberant Balance Sheet

Since June, the Fed has also taken steps to reduce the size of its bloated balance sheet. In other words, it is allowing its large holdings of U.S. Treasuries and Agency Mortgage-Backed Securities to shrink. These securities were acquired during rounds of so-called quantitative easing (QE), which were a major contributor to the money growth in 2020 that left us where we are today. The securities holdings were about $8.5 trillion in May and now stand at roughly $8.2 trillion. Allowing the portfolio to run-off reduces bank reserves and liquidity. The process was accelerated in September, but there is increasing tension among analysts that this quantitative tightening will cause disruptions in financial markets and ultimately the real economy, There is no question that reducing the size of the balance sheet is contractionary, but that is another necessary step toward reducing the rate of inflation.

The Federal Spigot

The federal government is not making the Fed’s job any easier. The energy shortages now afflicting markets are largely the fault of misguided federal policy restricting supplies, with an assist from Russian aggression. Importantly, however, heavy borrowing by the U.S. Treasury continues with no end in sight. This puts even more pressure on financial markets, especially when such ongoing profligacy leaves little question that the debt won’t ever be repaid out of future budget surpluses. The only way the government’s long-term budget constraint can be preserved is if the real value of that debt is bid downward. That’s where the so-called inflation tax comes in, and however implicit, it is indeed a tax on the public.

Don’t Dismiss the Real Costs of Inflation

Inflation is a costly process, especially when it erodes real wages. It takes its greatest toll on the poor. It penalizes holders of nominal assets, like cash, savings accounts, and non-indexed debt. It creates a high degree of uncertainty in interpreting price signals, which ordinarily carry information to which resource flows respond. That means it confounds the efficient allocation of resources, costing all of us in our roles as consumers and producers. The longer it continues, the more it erodes our economy’s ability to enhance well being, not to mention the instability it creates in the political environment.

Imminent Recession?

So far there are only limited signs of a recession. Granted, real GDP declined in both the first and second quarters of this year, but many reject that standard as overly broad for calling a recession. Moreover, consumer spending held up fairly well. Employment statistics have remained solid, though we’ll get an update on those this Friday. Nevertheless, payroll gains have held up and the unemployment rate edged up to a still-low 3.7% in August.

Those are backward-looking signs, however. The financial markets have been signaling recession via the inverted yield curve, which is a pretty reliable guide. The weak stock market has taken a bite out of wealth, which is likely to mean weaker demand for goods. In addition to energy-supply shocks, the strong dollar makes many internationally-traded commodities very costly overseas, which places the global economy at risk. Moreover, consumers have run-down their savings to some extent, corporate earnings estimates have been trimmed, and the housing market has weakened considerably with higher mortgage rates. Another recent sign of weakness was a soft report on manufacturing growth in September.

Deliver the Medicine

The Fed must remain on course. At least it has pretensions of regaining credibility for its inflation targeting regime, and ultimately it must act in a symmetric way when inflation overshoots its target, and it has. It’s not clear how far the Fed will have to go to squeeze demand-side inflation down to a modest level. It should also be noted that as long as supply-side pressures remain, it might be impossible for the Fed to engineer a reduction of inflation to as low as its 2% target. Therefore, it must always bear supply factors in mind to avoid over-contraction.

As to raising the short-term interest rates the Fed controls, we can hope we’re well beyond the halfway point. Reductions in the Fed’s balance sheet will continue in an effort to tighten liquidity and to provide more long-term flexibility in conducting operations, and until bank reserves threaten to fall below the Fed’s so-called “ample reserves” criterion, which is intended to give banks the wherewithal to absorb small shocks. Signs that inflationary pressures are abating is a minimum requirement for laying off the brakes. Clear signs of recession would also lead to more gradual moves or possibly a reversal. But again, demand-side inflation is not likely to ease very much without at least a mild recession.

The Federal Reserve just announced tighter monetary policy in an attempt to reduce inflationary pressures. First, it raised its target range for the federal funds rate (on overnight loans between banks) by 0.5%. The new range is 0.75% – 1%. Second, on June 1, the Fed will begin taking steps to reduce the size of its $9 trillion portfolio of securities. These holdings were acquired during periods of so-called quantitative easing (QE) beginning in 2008, including dramatic expansions in 2020-21. A shorthand reference for this portfolio is simply the Fed’s “balance sheet”. It includes government debt the Fed has purchased as well as privately-issued mortgage-backed securities (MBS).

What Is This Balance Sheet You Speak Of?