I’ll try to keep this one short. I was starting a post on another topic when Donald Trump distracted me… again. This time it was the $2,000 per person “tariff dividend” he’s proposed. This would be paid to all low- and middle-income Americans starting in mid-2026. As if the federal government was a profitable enterprise. Obviously that’s the wrong model! This is either sheer stupidity or willful government failure. Sure, the Fed can just print money, so why not? Who knew Trump was a closet modern monetary theorist?

It’s such a bad idea…. Tariffs themselves are bad enough. They are taxes, of course, a truth about which Trump and his central trade planners have denied since the beginning of the escapade. Tariffs hurt consumers and businesses who import inputs. Tariffs retard growth by increasing input costs, disrupting supply chains, and raising the prices of not only imports, but also domestically-produced goods that compete with imports. Surely Trump knows all this and the implications for his political capital: he’s already backtracking on tariffs for certain food items.

The tariff dividend is a transparent attempt to compensate consumers for the harms of taxation. It’s also a transparent attempt to buy or keep votes, much as he’s already sought to buy-off farmers harmed by tariffs. The income limit for the dividend hasn’t been announced, but make no mistake: this represents another form of redistribution.

It’s also striking that the tariffs won’t generate nearly as much revenue as will be required to begin paying the dividend by mid-2026. In fact, it could be short by as much as $300 million! Will the Treasury borrow the rest? More pressure on the bond market and interest rates.

Furthermore, the so-called dividend would be inflationary if the Federal Reserve fails to neutralize it. It would amount to another “helicopter drop” of cash, similar to the cash dump from Covid relief payments: money printing under the guise of fiscal policy.

To the extent that tariff revenue flows, it should be used to reduce the federal deficit or to pay down the gigantic government debt already outstanding ($38 trillion today not including the impending cost of funding entitlement programs). Instead, Trump is proudly following in the footsteps of generations of spendthrift politicians.

Keep in mind that the dividend is a promise Trump might not be able to keep. The Supreme Court will soon announce its decision on presidential power to impose tariffs. This decision will bear on the president’s authority under the International Emergency Economic Powers Act (IEEPA) — if and when an actual emergency is at hand, which it clearly is not. More broadly, the decision hinges on whether a “foreign facing” tax falls within the president’s Article II powers under the Constitution.

The proposed tariff dividend undermines the Administration’s argument before the Court that tariffs are primarily regulatory tools, and that any revenue from tariffs is merely incidental. Thank God the dividend would have to be authorized by Congress! I truly hope there are enough sensible legislators on the Hill to beat back this idiocy.

The Juneteenth holiday (June 19th) marks the anniversary of the abolition of slavery in the U.S. It should be viewed as a celebration of basic human rights. However, in purely economic terms, slavery was (and still is in many parts of the world) a complete revocation of property rights (self-ownership). But not only was slave-holding the worst sort of theft, it represented a total suspension of the labor market mechanism and had dire consequences for long-term economic development, especially in the south.

Government sanction of slaveholding in the southern U.S. and an extremely low effective wage for slaves promoted an excessive and inefficient dependence on, and utilization of, the low-cost input: slave labor. As a result, slavery created an obstacle to economic development, innovation, and capital deepening. The overall impact on the U.S. was to reduce economic welfare and development, and the dysfunction was obviously concentrated in the south.

That hasn’t stopped some activists from making the claim that slavery enabled the success of American capitalism. For example, this book contends that:

“… the expansion of slavery in the first eight decades after American independence drove the evolution and modernization of the United States.“

The so-called 1619 Project has promoted this narrative as well. Interestingly, this is similar to claims made prior to emancipation by defenders of slavery.

Of course, one can’t overemphasize the injustices suffered by American slaves, like those of other enslaved peoples throughout history. But it is foolhardy to attribute the long-term economic success of the American economy to slavery. Even today, 160 years after emancipation, it’s a safe bet that most Americans would be better off without its legacy.

To be clear I’ll outline several assertions I’m making here. First, if slaves had been free workers, they would have enjoyed freedoms and captured the value of their labors from the start. (Though it is not clear how many Africans would have come to America voluntarily as free workers, had they been given the opportunity. Some, however, were already enslaved.)

Under this counterfactual, more efficient pricing of labor would have led to deeper capital. At the same time, while many black non-slaves would still have worked in agriculture, blacks would have been more dispersed occupationally, working at tasks that best suited individual skills. The resulting efficiency gains would have been magnified by virtue of working in combination with more capital assets, enhancing productivity. And these workers would have been free to build their own human capital through education and work experience. Meanwhile, government would not have wasted resources enforcing slave ownership, and plantation owners (and other slave holders) would have made more rational resource allocation decisions. All these factors would have produced a net gain in welfare and improved economic development from at least the time of the nation’s founding.

There is no question that enslavement and the welfare losses suffered by slaves (and many of their descendants) far outweighed the gains captured by those who employed slave labor, as well as those who consumed or otherwise made use of the product of slave labor. A proper economic accounting of these losses acknowledges that slaves were denied their worker surplus and their ability to earn an opportunity cost, and they were often punished or tortured as a means of coercing greater effort. This serves to emphasize the implausibility of the argument that the America reaped net economic benefits from slavery.

Slavery was so powerful an institution that it permeated southern culture and perceptions of status. Wealth was tied-up in slave-chattel, and the free labor made for a handsome return on investment. Thus, both economic and cultural factors acted to lock producers into an unending series of short-run input decisions.

Furthermore, as Phil Magness explains in a letter to the Editor in the Wall Street Journal:

“… slavery’s economics … largely depended on government support. Fugitive slave patrols, military expenditures to fend off the threat of slave revolts and censorship of abolitionist materials by the post office were necessary to secure the institution’s economic position. These policies transferred the burden of enforcing the slave system from the plantation masters on to the taxpaying public.“

Meanwhile, the distortions to the cost of labor slowed the adoption of a variety of production techniques, including horse-drawn cultivators and harrows, steel plows, and steam-powered machinery. In other words, planters had little incentive to modernize production. Other technologies commonly used in the north during that era could have been applied in the south, but only to its much smaller share of acreage dedicated to grain crops.

Southern agricultural practices were “frozen in place”, as Rod D. Martin puts it. Ultimately, had southern planters adopted labor-saving technologies, and had southern governments shifted resources away from protecting slavery as an institution toward more diversified economic development, the antebellum economy would have experienced more rapid growth.

Growth in demand for cotton exports was certainly a boon to the south during the years preceding the Civil War, but the reliance on cotton was such that the southern economy was heavily exposed to risks of draught and other shocks. Furthermore, the lack of industrialization meant that southern states captured little of the final value of the textiles produced with cotton. The inadequacy of transportation infrastructure in the south was another serious detriment to long-term growth.

The work of Nathan Nunn, which is cited by Martin, generally supports the hypothesis that slavery retards economic growth. Nunn found a strong negative correlation between slave use and later economic development across different “New World” economies, as well as U.S. states and counties.

Martin goes so far as to say that the Union’s victory over the Confederacy was due in large part to economic under-development attributable to slavery in the south. That narrative has been challenged by a few scholars who claimed that the south was actually wealthier than the north. The owners of large southern plantations were quite well off, of course, but estimates of their wealth are unreliable, and in any case slaves themselves were highly illiquid “assets”. That meant planters would have been hard pressed to raise the capital needed for investment in labor-saving technologies, even if they’d had proper incentives to do so.

On the whole, there is no question the north was far more industrialized, diversified, and prosperous than the south. It was also much larger in terms of population and total output. Thus, Martin’s assertion that slavery explains why the south lost the Civil War is probably a bit too sweeping.

Nevertheless, the slavery “ecosystem” helps explain the south’s historic under-development. It was characterized by artificially cheap labor, illiquidity, a lack of diversification, a rigid social hierarchy based on the aberrant ownership of human chattel, and state subsidization of slave owners. These conditions restricted the supply of investment capital in the south. This was a drag on economic development before the Civil War. Those characteristics, along with the direct costs of the war itself, go a long way toward explaining the south’s lengthy period of depressed conditions after the Civil War as well.

It’s certainly not a knock on the slave population prior to emancipation to say that they were not responsible for the success of American capitalism. It’s a knock on the institution of slavery itself. Our wealth and the bounties produced by today’s economy are not supercharged by the efforts of slave labor in the distant past. If anything, our prosperity would be far greater had slavery never been practiced on U.S. soil.

I oppose reparations as a form of redistribution partly because most prospective payers today have absolutely no connection to slave-holding in antebellum America. It’s ironic that certain activists now argue for reparations based on imagined economic benefits once used to defend slavery itself.

First, a preliminary issue: many resources qualify as commons in the very broadest sense, yet free societies have learned over time that many resources are used much more productively when property rights are assigned to individuals. For example, modern agriculture owes much to defining exclusive property rights to land so that conflicting interests don’t have to compete (e.g,, the farmer and the cowman). Federal land is treated as a commons, however. There is a rich history on the establishment of property rights, but within limits, the legal framework in place can define whether a resource is treated as a commons, a club good, or private property. The point here is that there are substantial economic advantages to preserving strong property rights, rather than treating all resources as communal.

The authors of the planetary commons (PC) paper present a rough sketch for governance over use of the planet’s resources, given their belief that a planetary crisis is unfolding before our eyes. The paper has two main thrusts as I see it. One is to broadly redefine virtually all physical resources as common pool interests because their use, in the authors’ view, may entail some degree of external cost involving degradation of the biosphere. The second is to propose centralized, “planetary” rule-making over the amounts and ways in which those resources are used.

It’s an Opinion Piece

The PC paper is billed as the work product of a “collaborative team of 22 leading international researchers”. This group includes four attorneys (one of whom was a lead author) and one philosopher. Climate impact researchers are represented, who undoubtedly helped shape assumptions about climate change and its causes that drive the PC’s theses. (More on those assumptions in a section below.) There are a few social scientists of various stripes among the credited authors, one meteorologist, and a few “sustainability”, “resilience”, and health researchers. It’s quite a collection of signees, er… “research collaborators”.

Grabby Interventionists

The reasoning underlying a “planetary commons” (PC) is that the planet’s biosphere qualifies as a commons. The biosphere must include virtually any public good like air and sunshine, any common good like waterways, or any private good or club good. After all, any object can play host to tiny microbes regardless of ownership status. So the PC authors characterization of the planet’s biosphere as a commons is quite broad in terms of conventional notions of resource attributes.

We usually think of spillover or external costs as arising from some use of a private resource that imposes costs on others, such as air or water pollution. However, mere survival requires that mankind exploit both public and non-public resources, acts that can always be said to impact the biosphere in some way. Efforts to secure shelter, food, and water all impinge on the earth’s resources. To some extent, mankind must use and shape the biosphere to succeed, and it’s our natural prerogative to do so, just like any other creature in the food chain.

Even if we are to accept the PC paper’s premise that the entire biosphere should be treated is a commons, most spillovers are de minimus. From a public policy perspective, it makes little sense to attempt to govern over such minor externalities. Monitoring behavior would be costly, if not impossible, at such an atomistic level. Instead, free and civil societies rely on a high degree of self-governance and informal enforcement of ethical standards to keep small harms to a minimum.

Unfortunately, the identification and quantification of meaningful spillover costs is not always clear-cut. This has led to an increasingly complex regulatory environment, an increasingly litigious business environment, and efforts by policymakers to manage the detailed inputs and outputs of the industrial economy.

All of that is costly in its own right, especially because the activities giving rise to those spillovers often enable large welfare enhancements. Regulators and planners face great difficulties in estimating the costs and benefits of various “correctives”. The very undertaking creates risk that often exceeds the cost of the original spillover. Nevertheless, the PC paper expands on the murkiest aspects of spillover governance by including “… all critical biophysical Earth-regulating systems and their functions, irrespective of where they are located…” as part of a commons requiring “… additional governance arrangements….”

Adoption of the PC framework would authorize global interventions (and ultimately local interventions, including surveillance) on a massive scale based on guesswork by bureaucrats regarding the evolution of the biosphere.

Ostrom Upside Down

Not only would the PC framework represent an expansion of the grounds for intervention by public authorities, it seeks to establish international authority for intervention into public and private affairs within sovereign states. The authors attempt to rationalize such far-reaching intrusions in a rather curious way:

“Drawing on the legacy of Elinor Ostrom’s foundational research, which validated the need for and effectiveness of polycentric approaches to commons governance (e.g., ref. 35, p. 528, ref. 36, p. 1910), we propose that a nested Earth system governance approach be followed, which will entail the creation of additional governance arrangements for those planetary commons that are not yet adequately governed.”

Anyone having a passing familiarity with Elinor Ostrom’s work knows that she focused on the identification of collaborative solutions to common goods problems. She studied voluntary and often strictly private efforts among groups or communities to conserve common pool resources, as opposed to state-imposed solutions. Ostrom accepted assigned rights and pricing solutions to managing common resources, but she counseled against sole reliance on market-based tools.

Surely the PC authors know they aren’t exactly channeling Ostrom:

“An earth system governance approach will require an overarching global institution that is responsible for the entire Earth system, built around high-level principles and broad oversight and reporting provisions. This institution would serve as a universal point of aggregation for the governance of individual planetary commons, where oversight and monitoring of all commons come together, including annual reporting on the state of the planetary commons.”

Polycentricity was used by Ostrom to describe the involvement of different, overlapping “centers of authority”, such as individual consumers and producers, cooperatives formed among consumers and producers, other community organizations, local jurisdictions, and even state or federal regulators. Some of these centers of authority supersede others in various ways. For example, solutions developed by cooperatives or lower centers of authority must align with the legal framework within various government jurisdictions. However, as David Henderson has noted, Ostrom observed that management of pooled resources at lower levels of authority was generally superior to centralized control. Henderson quotes Ostrom and a co-author on this point:

“When users are genuinely engaged in decisions regarding rules affecting their use, the likelihood of them following the rules and monitoring others is much greater than when an authority simply imposes rules.”

The authors of the PC have something else in mind, and they bastardize the spirit of Ostrom’s legacy in the process. For example, the next sentence is critical for understanding the authors’ intent:

“If excessive emissions and harmful activities in some countries affect planetary commons in other areas—for example, the melting of polar ice—strong political and legal restrictions for such localized activities would be needed.”

Of course, there are obvious difficulties in measuring impacts of various actions on polar ice, assigning responsibility, and determining the appropriate “restrictions”. But in essence, the PC paper advocates for a top-down model of governance. Polycentrism is thus reduced to “you do as we say”, which is not in the spirit of Ostrom’s research.

Planetary Governance

Transcending national sovereignty on questions of the biosphere is key to the authors’ ambitions. At a bare minimum, the authors desire legally-binding commitments to international agreements on environmental governance, unlike the unenforceable promises made for the Paris Climate Accords:

“At present, the United Nations General Assembly, or a more specialized body mandated by the Assembly, could be the starting point for such an overarching body, even though the General Assembly, with its state-based approach that grants equal voting rights to both large countries and micronations, represents outdated traditions of an old European political order.”

But the votes of various “micronations” count for zilch when it comes to real “claims” on the resources of other sovereign nations! Otherwise, there is nothing “voluntary” about the regime proposed in the PC paper.

“A challenge for such regimes is to duly adapt and adjust notions of state sovereignty and self-determination, and to define obligations and reciprocal support and compensation schemes to ensure protection of the Earth system, while including comprehensive stewardship obligations and mandates aimed at protecting Earth-regulating systems in a just and inclusive way.”

So there! The way forward is to adopt the broadest possible definition of market failure and global regulation of any and all private activity touching on nature in any way. And note here a similarity to the Paris Accords: achieving commitments would fall to national governments whose elites often demonstrate a preference for top-down solutions.

Ah Yes, Redistribution

It should be apparent by now that the PC paper follows a now well-established tradition in multi-national climate “negotiations” to serve as subterfuge for redistribution (which, incidentally, includes the achievement of interspecies justice):

“For instance, a more equal sharing of the burdens of climate stabilization would require significant multilateral financial and technology transfers in order not to harm the poorest globally (116).”

The authors insist that participation in this governance would be “voluntary”, but the following sentence seems inconsistent with that assurance:

“… considering that any move to strengthen planetary commons governance would likely be voluntarily entered into, the burdens of conservation must be shared fairly (115).”

Wait, what? “Voluntary” at what level? Who defines “fairness”? The authors approvingly offer this paraphrase of the words of Brazilian President Lula da Silva,

“… who affirmed the Amazon rainforest as a collective responsibility which Brazil is committed to protect on behalf of all citizens around the world, and that deserves and justifies compensation from other nations (117).”

Let Them Eat Cake

Furthermore, PC would require de-growth and so-called “sufficiency” for thee (i.e., be happy with less), if not for those who’ll design and administer the regime.

“… new principles that align with novel Anthropocene dynamics and that could reverse the path-dependent course of current governance. These new principles are captured under a new legal paradigm designed for the Anthropocene called earth system law and include, among others, the principles of differentiated degrowth and sufficiency, the principle of interconnectivity, and a new planetary ethic (e.g., principle of ecological sustainability) (134).”

If we’re to take the PC super-regulators at their word, the regulatory regime wouldimpinge on fertility decisions as well. Just who might we trust to govern humanity thusly? If we’re wise enough to applythe Munger Test, we wouldn’t grant that kind of power to our worst enemy!

Global Warmism

The underlying premise of the PC proposal is that a global crisis is now unfolding before our eyes: anthropomorphic global warming (AGW). The authors maintain that emissions of carbon dioxide are the cause of rising temperatures, rapidly rising sea levels, more violent weather, and other imminent disasters.

“It is now well established that human actions have pushed the Earth outside of the window of favorable environmental conditions experienced during the Holocene…”

“Earth system science now shows that there are biophysical limits to what existing organized human political, economic, and other social systems can appropriate from the planet.”

For a variety of reasons, both of these claims are more dubious than one might suppose based on popular narratives. As for the second of these, mankind’s limitless capacity for innovation is a more powerful force for sustainability than the authors would seem to allow. On the first claim, it’s important to note that the PC paper’s forebodings are primarily based on modeled, prospective outcomes, not historical data. The models are drastically oversimplified representations of the earth’s climate dynamics driven by exogenous carbon forcing assumptions. Their outputs have proven to be highly unreliable, overestimating warming trends almost without exception. These models exaggerate climate sensitivity to carbon forcings, and they largely ignore powerful natural forcings such as variations in solar irradiance, geological heating, and even geological carbon forcings. The models are also notorious for their inadequate treatment of feedback effects from cloud cover. Their predictions of key variables like water vapor are wildly in error.

The measurement of the so-called “global temperature” is itself subject to tremendous uncertainty. Weather stations come and go. They are distributed very unevenly across land masses, and measurement at sea is even sketchier. Averaging all these temperatures would be problematic even if there were no other issues… but there are. Individual stations are often sited poorly, including distortions from heat island effects. Aging of equipment creates a systematic upward bias, but correcting for that bias (via so-called homogenization) causes a “cooling the past” bias. It’s also instructive to note that the increase in global temperature from pre-industrial times actually began about 80 years prior to the onset of more intense carbon emissions in the 20th century.

Climate alarmists often speak in terms of temperature anomalies, rather than temperature levels. In other words, to what extent do temperatures differ from long-term averages? The magnitude of these anomalies, using the past several decades as a base, tend to be anywhere from zero degrees to well above one degree Celsius, depending on the year. Relative to temperature levels, the anomalies are a small fraction. Given the uncertainty in temperature levels, the anomalies themselves are dwarfed by the noise in the original series!

Pick Your Own Tipping Point

It seems that“tipping point” scares are heavily in vogue at the moment, and the PC proposal asks us to quaff deeply of these narratives. Everything is said to be at a tipping point into irrecoverable disaster that can be forestalled only by reforms to mankind’s unsustainable ways. To speak of the possibility of other causal forces would be a sacrilege. There are supposed tipping points for the global climate itself as well as tipping points for the polar ice sheets, the world’s forests, sea levels and coastal environments, severe weather, and wildlife populations. But none of this is based on objective science.

For example, the 1.5 degree limit on global warming is a wholly arbitrary figure invented by the IPCC for the Paris Climate Accords, yet the authors of the PC proposal would have us believe that it was some sort of scientific determination. And it does not represent a tipping point. Cliff Mass explains that climate models do not behave as if irreversible tipping points exist.

Likewise, the rise of sea levels has not accelerated from prior trends, so it has nothing to do with carbon forcing.

One thing carbon forcings have accomplished is a significant greening of the planet, which if anything bodes well for the biosphere

What about the disappearance of the polar ice sheets? On this point, Cliff Mass quotes Chapter 3 of the IPCC’s Special Report on the implications of 1.5C or more warming:

“there is little evidence for a tipping point in the transition from perennial to seasonal ice cover. No evidence has been found for irreversibility or tipping points, suggesting that year-round sea ice will return given a suitable climate.”

The PC paper also attempts to connect global warming to increases in forest fires, but that’s incorrect: there has been no increasing trend in forest fires or annual burned acreage. If anything, trends in measures of forest fire activity have been negative over the past 80 years.

Concluding Thoughts

The alarmist propaganda contained in the PC proposal is intended to convince opinion leaders and the public that they’d better get on board with draconian and coercive steps to curtail economic activity. They appeal to the sense of virtue that must always accompany consent to authoritarian action, and that means vouching for sacrifice in the interests of environmental and climate equity. All the while, the authors hide behind a misleading version of Elinor Ostrom’s insights into the voluntary and cooperative husbandry of common pool resources.

One day we’ll be able to produce enough carbon-free energy to accommodate high standards of living worldwide and growth beyond that point. In fact, we already possess the technological know-how to substantially reduce our reliance on fossil fuels, but we lack the political will to avail ourselves of nuclear energy. With any luck, that will soften with installations of modular nuclear units.

Ultimately, we’ll see advances in fusion technology, beamed non-intermittent solar power from orbital collection platforms, advances in geothermal power, and effective carbon capture. Developing these technologies and implementing them at global scales will require massive investments that can be made possible only through economic growth, even if that means additional carbon emissions in the interim. We must unleash the private sector to conduct research and development without the meddling and clumsy efforts at top-down planning that typify governmental efforts (including an end to mandates, subsidies, and taxes). We must also reject ill-advised attempts at geoengineered cooling that are seemingly flying under the regulatory radar. Meanwhile, let’s save ourselves a lot of trouble by dismissing the interventionists in the planetary commons crowd.

We’re told again and again that government must take action to correct “market failures”. Economists are largely responsible for this widespread view. Our standard textbook treatments of external costs and benefits are constructed to demonstrate departures from the ideal of perfectly competitive market equilibria. This posits an absurdly unrealistic standard and diminishes the power and dramatic success of real-world markets in processing highly dispersed information, allocating resources based on voluntary behavior, and raising human living standards. It also takes for granted the underlying institutional foundations that lead to well-functioning markets and presumes that government possesses the knowledge and ability to rectify various departures from an ideal. Finally, “corrective” interventions are usually exposited in economics classes as if they are costless!

Failed Disgnoses

This brings into focus the worst presumption of all: that government solutions to social and economic problems never fail to achieve their intended aims. Of course that’s nonsense. If defined on an equivalent basis, government failure is vastly more endemic and destructive than market failure.

“According to ancient legend, a Roman emperor was asked to judge a singing contest between two participants. After hearing the first contestant, the emperor gave the prize to the second on the assumption that the second could be no worse than the first. Of course, this assumption could have been wrong; the second singer might have been worse. The theory of market failure committed the same mistake as the emperor. Demonstrating that the market economy failed to live up to the ideals of general competitive equilibrium was one thing, but to gleefully assert that public action could costlessly correct the failure was quite another matter. Unfortunately, much analytical work proceeded in such a manner. Many scholars burst the bubble of this romantic vision of the political sector during the 1960s. But it was [James] Buchanan and Gordon Tullock who deserve the credit for shifting scholarly focus.”

John Cochrane sums up the whole case succinctly in the “punchline” of a recent post:

“The case for free markets never was their perfection. The case for free markets always was centuries of experience with the failures of the only alternative, state control. Free markets are, as the saying goes, the worst system; except for all the others.”

Tracing Failures

We can view the relation between market failure and government failure in two ways. First, we can try to identify market failures and root causes. For example, external costs like pollution cause harm to innocent third parties. This failure might be solely attributable to transactions between private parties, but there are cases in which government engages as one of those parties, such as defense contracting. In other cases government effectively subsidizes toxic waste, like the eventual disposal of solar panels. Another kind of market failure occurs when firms wield monopoly power, but that is often abetted by costly regulations that deliver fatal blows to small competitors.

The second way to analyze the nexus between government and market failures is to first examine the taxonomy of government failure and identify the various damages inflicted upon the operation of private markets. That’s the course I’ll follow below, though by no means is the discussion here exhaustive.

Failures In and Out of Scope

An extensive treatment of government failure was offered eight years ago by William R. Keech and Michael Munger. To start, they point out what everyone knows: governments occasionally perpetrate monstrous acts like genocide and the instigation of war. That helps illustrate a basic dichotomy in government failures:

“… government may fail to do things it should do, or government may do things it should not do.’

Both parts of that statement have numerous dimensions. Failures at what government should do run the gamut from poor service at the DMV, to failure to enforce rights, to corrupt bureaucrats and politicians skimming off the public purse in the execution of their duties. These failures of government are all too common.

What government should and should not do, however, is usually a matter of political opinion. Thomas Jefferson’s axioms appear in a single sentence at the beginning of the Declaration of Independence; they are a tremendous guide to the first principles of a benevolent state. However, those axioms don’t go far in determining the range of specific legal protections and services that should and shouldn’t be provided by government.

Pareto Superiority

Keech and Munger engage in an analytical exercise in which the “should and shouldn’t” question is determined under the standard of Pareto superiority. A state of the world is Pareto superior if at least one person prefers it to the current state (and no one else is averse to it). Coincidentally, voluntary trades in private markets always exploit Pareto superior opportunities, absent legitimate external costs and benefits.

The set of Pareto superior states available to government can be expanded by allowing for side payments or compensation to those who would have preferred the current state. Still, those side payments are limited by the magnitude of the gains flowing to those who prefer the alternative (and if those gains can be redistributed monetarily).

Keech and Munger define government failure as the unexploited existence of Pareto superior states. Of course, by this definition, only a benevolent, omniscient, and omnipotent dictator could hope to avoid government failure. But this is no more unrealistic than the assumptions underlying perfectly competitive market equilibrium from which departure are deemed “market failures” that government should correct. Thus, Keech and Munger say:

“The concept of government failure has been trapped in the cocoon of the theory of perfect markets. … Government failure in the contemporary context means failing to resolve a classic market failure.”

But markets must operate within a setting defined by culture and institutions. The establishment of a social order under which individuals have enforceable rights must come prior to well-functioning markets, and that requires a certain level of state capacity. Keech and Munger are correct that market failure is often a manifestation of government failure in setting and/or enforcing these “rules of the game”.

“The real question is … how the rules of the game should be structured in terms of incentives, property rights, and constraints.”

The Regulatory State and Market Failures

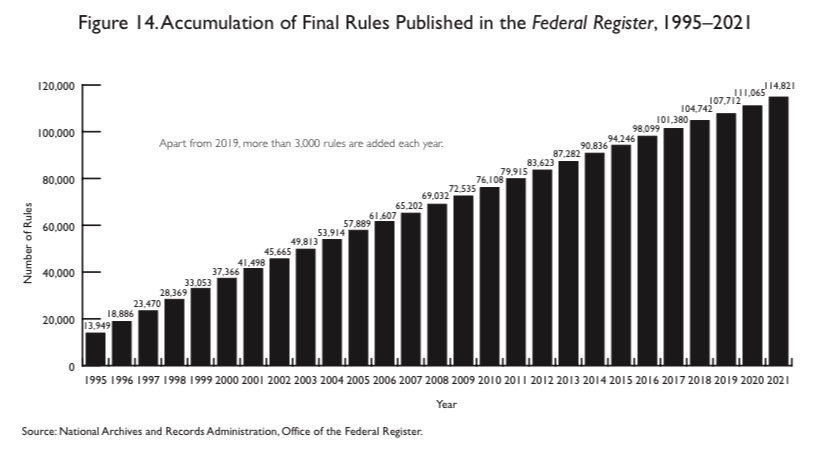

Government can do too little in defining and enforcing rights, and that’s undoubtedly a cause of failure in markets in even the most advanced economies. At the same time there is an undeniable tendency for mission creep: governments often try to do too much. Overregulation in the U.S. and other developed nations creates a variety of market failures. This includes the waste inherent in compliance costs that far exceed benefits; welfare losses from price controls, licensing, and quotas; diversion of otherwise productive resources into rent seeking activity, anti-competitive effects from “regulatory capture”; Chevron-like distortions endemic to the administrative judicial process; unnecessary interference in almost any aspect of private business; and outright corruption and bribe-taking.

Central Planning and Market Failures

Another category of government attempting to “do too much” is the misallocation of resources that inevitably accompanies efforts to pick “winners and losers”. The massive subsidies flowing to investors in various technologies are often misdirected. Many of these expenditures end up as losses for taxpayers, and this is not the only form in which failed industrial planning takes place. A related evil occurs when steps are taken to penalize and destroy industries in political disfavor with thin economic justification.

Other clear examples of government “planning” failure are protectionist laws. These are a net drain on our wealth as a society, denying consumers of free choice and saddling the country with the necessity to produce restricted products at high cost relative to erstwhile trading partners.

There are, of course, failures lurking within many other large government spending programs in areas such as national defense, transportation, education, and agriculture. Many of these programs can be characterized as centrally planning. Not only are some of these expenditures ineffectual, but massive procurement spending seems to invite waste and graft. After all, it’s somebody else’s money.

Redistribution and Market Failures

One might regard redistribution programs as vehicles for the kinds of side payments described by Keech and Munger. Some might even say these are the side payments necessary to overcome resistance from those unable to thrive in a market economy. That reverses the historical sequence of events, however, since the dominant economic role of markets preceded the advent of massive redistribution schemes. Unfortunately, redistribution programs have been plagued by poor design, such as the actuarial nightmare inherent in Social Security and the destructive work incentives embedded in other parts of the social safety net. These are rightly viewed as government failures, and their distortionary effects spill variously into capital markets, labor markets and ultimately product markets.

Taxation and Market Failures

All these public initiatives under which government failures precipitate assorted market failures must be paid for by taxpayers. Therefore, we must also consider the additional effects of taxation on markets and market failures. The income tax system is rife with economic distortions. Not only does it inflict huge compliance costs, but it alters incentives in ways that inhibit capital formation and labor supply. That hampers the ability of input markets to efficiently meet the needs of producers, inhibiting the economy’s productive capacity. In turn, these effects spill into output market failures, with consequent losses in .social welfare. Distortionary taxes are a form of government failure that leads to broad market failures.

Deficits and Market Failure

More often than not, of course, tax revenue is inadequate to fund the entire government budget. Deficit spending and borrowing can make sense when public outlays truly produce long-term benefits. In fact, the mere existence of “risk-free” assets (Treasury debt) across the maturity spectrum might enhance social welfare if it enables improvements in portfolio diversification that outweigh the cost of the government’s interest obligations. (Treasury securities do bear interest-rate risk and, if unindexed, they bear inflation risk.)

Nevertheless, borrowing can reflect and magnify deleterious government efforts to “do too much”, ultimately leading to market failures. Government borrowing may “crowd out” private capital formation, harming economy-wide productivity. It might also inhibit the ability of households to borrow at affordable rates. Interest costs of the public debt may become explosive as they rise relative to GDP, limiting the ability of the public sector to perform tasks that it should *actually* do, with negative implications for market performance.

Inflation and Market Failure

Deficit spending promotes inflation as well. This is more readily enabled when government debt is monetized, but absent fiscal discipline, the escalation of goods prices is the only remaining force capable of controlling the real value of the debt. This is essentially the inflation tax.

Inflation is a destructive force. It distorts the meaning of prices, causes the market to misallocate resources due to uncertainty, and inflicts costs on those with fixed incomes or whose incomes cannot keep up with inflation. Sadly, the latter are usually in lower socioeconomic strata. These are symptoms of market failure prompted by government failure to control spending and maintain a stable medium of exchange.

Conclusion

Markets may fail, but when they do it’s very often rooted in one form of government failure or another. Sometimes it’s an inadequacy in the establishment or enforcement of property rights. It could be a case of overzealous regulation. Or government may encroach on, impede, or distort decisions regarding the provision of goods or services best left to the market. More broadly, redistribution and taxation, including the inflation tax, distort labor and capital markets. The variety of distortions created when government fails at what it should do, or does what it shouldn’t do, is truly daunting. Yet it’s difficult to find leaders willing to face up to all this. Statism has a powerful allure, and too many elites are in thrall to the technocratic scientism of government solutions to social problems and central planning in the allocation of resources.

Government budget negotiations never fail to frustrate anyone of a small-government persuasion. We have a huge, ongoing federal budget deficit. Spending’s gone bat-shit out of control over the past several years and too few in Congress are willing to do anything about it. Democrats would rather see politically-targeted tax increases. While some Republicans advocate spending cuts, the focus is almost entirely on discretionary spending. Meanwhile, the entitlement state is off the table, including Social Security reform.

Fiscal Indiscretion

Sadly, non-discretionary outlays (entitlements) today make a much larger contribution to the deficit than discretionary spending. That includes the programs like Social Security (SS) and Medicare, in which spending levels are programmatic and not subject to annual appropriations by Congress. When these programs were instituted there were a large number of workers relative to retirees, so tax contributions exceeded benefit levels for many decades. The revenue excesses were placed into “trust funds” and invested in Treasury debt. In other words, surpluses under non-discretionary SS and Medicare programs were used to finance discretionary spending!

The aging of Baby Boomers ultimately led to a reversal in the condition of the trust funds. Fewer workers relative to retirees meant that annual payroll tax collections were not adequate to cover annual benefits, and that meant drawing down the trust funds. Current projections by the system trustees call for the SS Trust Fund to be exhausted by 2035. Once that occurs, benefits will automatically be reduced by roughly 20% unless Congress acts to shore up the system before then.

A Few Proposals

I’ve written about the need for SS reform on several occasions (though the first article at that link is not germane here). It seems imperative for Congress and the President to address these shortfalls. By all appearances, however, many Republicans have put the issue aside. For his part, Joe Biden has apparently accepted the prospect of an automatic reduction in benefits in 2035, or at least he’s willing to kick that can down the road. He has, however, endorsed taxes on high earners to fund Medicare. Senator John Kennedy (R-LA) suggests raising the retirement age, or at least raise the minimum age at which one may claim benefits (now 62). Senators Bill Cassidy (R-La.) and Angus King (I-Maine) were working on a compromise that would create an investment fund to fortify the system, but the specifics are unclear, as well as how much that would accomplish.

Meanwhile, Senator Bernie Sanders (S-VT) proposes to expand SS benefits by $2,400 a year and add funding by extending payroll taxes to earners above the current limit of $160,000. Senator Joe Manchin (D-WV) has endorsed the latter as a “quick fix”.

There is also at least oneproposal in Congress to end the practice of taxing a portion of SS benefits as income. I have trouble believing it will gain wide support, despite the clear double-taxation involved.

Then there are always discussions of reducing benefits at higher income levels or even means-testing benefits. In fact, it would be interesting to know what proportion of current benefits actually function as social insurance, as opposed to a universal entitlement. The answer, at least, could serve as a baseline for more fundamental reforms, including changes in the structure of payroll taxes, voluntary lump-sum payouts, and private accounts.

More Radical Views

There are a few prominent voices who claim that SS is sustainable in its current form, but perhaps with a few “no big deal” tax increases. Oh, that’s only about a $1 trillion “deal”, at least for both Medicare and SS. More offensive still are the scare tactics used by opponents of SS reform any time the subject comes up. I’m not aware of any serious reform proposal made over the past two decades that would have affected the benefits of anyone over the age of 55, and certainly no one then-eligible for benefits. Yet that charge is always made: they want to cut your SS benefits! The Democrats made that claim against George W. Bush, torpedoing what might have been a great accomplishment for all. And now, apparently Donald Trump is willing to use such accusations to damage any rival who has ever mentioned reform, including Mike Pence. Will you please cut the crap?

The System

The thing to remember about SS is that it is currently structured as a pay-as-you-go (PAYGO) system, despite the fact that benefits are defined like many creaky private pensions of old. SS benefits in each period are paid out of current “contributions” (i.e., FICO payroll taxes) plus redemptions of government bonds held in the Trust Fund. Contributions today are not “invested” anywhere because they are not enough to pay for current benefits under PAYGO.

The Trust Fund was accumulated during the years when favorable demographics led to greater FICO contributions than benefit payouts. The excess revenue was “invested” in Treasury bonds, which meant it was used to fund deficits in the general budget. It’s been about 15 years since the Trust Fund entered a “draw-down” status, and again, it will be exhausted by 2035.

SSA Says It’s a Good Deal

A participant’s expected “rate of return” on lifetime payroll tax payments depends on several things: lifetime earnings, age at which benefits are first claimed, life expectancy at that time, marital status, relative earning levels within two-earner couples, and the “full retirement age” for the individual’s birth year. Payroll tax payments, by the way, include the employer’s share because that is one of the terms of a hire. A high rate of return is not the same as a high level of benefits, however. In fact, relative to career income, SS has a great deal of progressivity in terms of rates of return, but not much in terms of benefit levels.

The Social Security Administration (SSA) has calculated illustrative real internal rates of return (IRR) for many categories of earners given certain assumptions. (An IRR is a discount rate that equalizes the present value (PV) of a stream of payments and the PV of a stream of payoffs.) The SSA’s most recent update of this exercise was in April 2022. The report references Old Age, Survivors, and Disability Insurance (OASDI), but the focus is exclusively on seniors.

Three basic scenarios were considered: 1) current law, as scheduled, despite its unsustainability; 2) a payroll tax increase from 12.4% (not including the Medicare tax) to 15.96% starting in 2035, when the Trust Fund is exhausted; and 3) a reduction in benefits of 22% starting in 2035.

The authors of the report concludethat “… the real value of OASDI benefits is extraordinarily high.” This theme has been echoed by several other writers, such as here and here. This conclusion is based on a comparison to returns earned by investments that SSA judges to have comparably low risk.

I note here that I’ve made assertions in the past about relative SS returns based on nominal benefits, rather than inflation-adjusted values. Those comparisons to private returns might have seemed drastic because they were expressed in terms of hypothetical future nominal values at the point of retirement. The gaps are not as large in real terms or if we consider SS returns broadly to include those accruing to low career earners. Medium and high earners tend to earn lower hypothetical returns from SS.

A Mixed Bag

SSA’s calculated IRRs are highest for one-earner couples followed by two-earner couples. Single males do relatively poorly due to their higher mortality rates. Low earners do very well relative to higher earners. Earlier birth years are associated with higher IRRs, but these are not as impressive for cohorts who have not yet claimed benefits. The ranges of birth years provided in the report make this a little imprecise, but I’ll focus on those born in 1955 and later.

Of course the returns are highest under the current law hypothetical than for the scenarios involving a benefit reduction or a payroll tax hike. The current law IRRs can be viewed as baselines for other calculations, but otherwise they are irrelevant. The system is technically insolvent and the scheduled benefits under current law can’t be maintained beyond 2034 without steps to generate more revenue or cut benefits. Those steps will reduce IRRs earned by hypothetical SS “assets” whether they take the form of higher payroll taxes, lower benefits, a greater full retirement age, or other measures.

The tax hike doesn’t have much impact on the IRRs of near-term retirees. It falls instead on younger cohorts with some years of employment (and payroll tax payments) remaining. The effect of a cut in benefits is spread more evenly across age cohorts and the reductions in IRRs is somewhat larger.

With higher payroll taxes after 2034, the average IRRs for birth years of 1955+ range from about 0.5% up to about 6.25%. The returns for single females and two-earner couples are roughly similar and fall between those for single males on the low end and one-earner couples on the high end. In all cases, low earners have much higher IRRs than others.

The reduction in benefits produces returns for the 1955+ age cohorts averaging small, negative values for high-earning single men up to 5.5% to 6% for low-earning, one-earner couples.

But On the Whole…

The IRR values reported by SSA are quite variable across cohorts. Individuals or couples with low earnings can usually expect to “earn” real IRRs on their contributions of better than 3% (and above 5% in a few cases). Medium earners can expect real returns from 1% to 3% (and in some cases above 4%). Many of the returns are quite good for a safe “asset”, but not for high earners.

Again, SSA states that these are real returns, though they provide no detail on the ways in which they adjust the components used in their IRR formula to arrive at real returns. Granting the benefit of the doubt, we saw persistently negative real returns on a range of safe assets in the not-very-distant past, so the IRRs are respectable by comparison.

Qualifications

There are many assumptions in the SSA’s analysis that might be construed as drastic simplifications, such as no divorce and remarriage, uniform career duration, and no relationship between earnings and mortality. But it’s easy to be picky. Many of the assumptions discernible from the report seem to be reasonable simplifications in what could otherwise be an unruly analysis. Nonetheless, there are a few assumptions that I believe bias the IRRs upward (and perhaps a few in the other direction).

In fact, SSA is remarkably non-transparent in their explanation of the details. Repeated checking of SSA’s document for clear answers is mostly futile. Be that as it may, I’m forced to give SSA the benefit of the doubt in several respects. One is the reinvestment of cumulative remaining contributions at the IRR throughout the earning career and retirement. A detailed formula with all components and time subscripts would have been nice.

… And Major Doubts

As to my misgivings, first, the IRRs reported by SSA are based on earners who all reach the age of 65. However, roughly 14% – 15% of individuals who live to be of working age die before they reach the age of 65. Most of those deaths occur in the latter part of that range, after many years of contributions and hypothetical compounding. That means the dollar impact of contributions forfeited at death before age 65 is probably larger than the unweighted share of individuals. These individuals pay-in but receive no retirement benefit in SSA’s IRR framework, although some receive disability benefits for a period of time prior to death. It wouldn’t bother my conscience to knock off at least a tenth of the quoted returns for this consideration alone.

A second major concern surrounds the method of calculating benefits and discounted benefits. SSA assumes that benefits continue for the expected life of the claimant as of age 65. If life expectancy is 19 years at age 65, then “expected” benefits are a flat stream of benefit payments for 19 years. Discounting each payment back to age 65 at the IRR yields one side of the present value equality. This constant cash flow (CCF) treatment is likely to overstate the present value of benefits. Instead of CCFs, each payment should be weighted by the probability that the claimant will be alive to receive it with a limit at some advanced age like 100. CCF overcounts present values up to the expected life, but it undercounts present values beyond the expected life because the assumed CCF benefits then are zero!! Weighting benefit payments by the probability of survival to each age produces continuing additions to the PV, but increasing mortality and decaying discount factors become quite substantial beyond expected life, leading to relatively minor additions to PV over that range. The upshot is that the CCFs employed by SSA overstate PVs by front-loading all benefits earlier in retirement. For a given PV of contributions, an overstated PV of benefits requires a higher (and overstated) IRR to restore the PV equality, and this might be a substantial source of upward bias in SSA’s calculations.

Third, when comparing an SS “asset” to private returns, a big difference is that private balances remaining at death become assets of the earner’s estate. Meanwhile, a single beneficiary forfeits their SS benefits at death (except for a small death benefit), while a surviving spouse having lower benefits receives ongoing payments of the decedent’s benefits for life. This consideration, however, in and of itself, means that private plans have a substantial advantage: the “expected” residual at death can be “optimized” at zero or some higher balance, depending on the strength of the earner’s bequest motive.

Finally, in a footnote, the SSA report notes that their treatment of income taxes on Social Security benefits for claimants with higher incomes might bias some of the IRRs upward. That seems quite likely.

It would be difficult to recast SSA’s report based on adjustments for all of these qualifications. However, it’s likely that the IRRs in the SSA report are sharply overstated. That means many more beneficiaries with medium and higher earnings records would have returns in the 0% to 2% range, with more IRRs in the negative range for singles. Low earners, however, might still get returns in a range of 3% to 5%.

The SSA analysis attempts to demonstrate some limits to the risks faced by participants, given the scenarios involving a payroll tax increase or a benefits reduction in 2035. Nevertheless, there are additional political risks to the returns of certain classes of current and future retirees. For example, payroll taxes could be made much more progressive, benefits could be made subject to means testing, or indexing of benefits could be reduced. In fact, there are additional demographic risks that might confront retirees several decades ahead. Continued declines in fertility could further undermine the system’s solvency, requiring more drastic steps to shore up the system. As a hypothetical asset, by no means is SS “risk-free”.

Better Returns

Now let’s consider returns earned by private assets, which represent investments in productive capital. For stocks, these include the sum of all dividends and capital gains (growth in value). For compounding purposes, we assume that all returns are reinvested until retirement. Remember that private returns are much less variable over spans of decades than over durations of a few years. Over the course of 40 year spans (SSA’s career assumption), private returns have been fairly stable historically, and have been high enough to cushion investors from setbacks. Here is Seeking Alpha on annualized returns on the basket of stocks in the S&P 500:

“… the return on the S&P 500 since the beginning of valuation in 1928, is 10.22%, whereas the inflation-adjusted return on the market since that time is 7.01%…”

That real return would generate benefits far in excess of SS for most participants, but it’s not an adequate historical perspective on market performance. A more complete picture of real returns on the S&P, though one that is still potentially flawed, emerges from this calculator, which relies on data from Robert Shiller. The returns extend back to 1871, but the index as we know it today has existed only since 1957. The earlier returns tend to be lower, so these values may be biased:

Real stock market returns over rolling 40-year time spans varied considerably over this longer period. Still, those kind of stock returns would be superior to the IRRs in the SSA report going forward in all but a few cases (and then only for low and very low earners).

Most workers facing a choice between investing at these rates for 40 years, with market risk, and accepting standard SS benefits, uncertain as they are, couldn’t be blamed for choosing stocks. In fact, if we think of contributions to either type of plan as compounding to a hypothetical sum at retirement, the stock investments would produce a “pot of gold” several times greater in magnitude than SS.

However, we still don’t have a fair comparison because workers choosing a stock plan would essentially engage in a kind of dollar-cost averaging over 40 years, meaning that investments would be made in relatively small amounts over time, rather than investing a lump-sum at the beginning. This helps to smooth returns because purchases are made throughout the range of market prices over time, but it also means that returns tend to be lower than the 40-year rolling returns shown above. That’s because the average contribution is invested for only half the time.

To be very conservative, if we assume that real stock returns average between 5% and 6% annually, $1 invested every year would grow to between $131 – $155 after 40 years in constant dollars. At returns of 1% to 2% from SS, which I believe are typical of the IRRs for many medium earners, the cumulative “pot” would grow to $49 – $60. Assuming that the tax treatment of the stock plan was the same as contributions and benefits under SS, the stock plan almost triples your money.

Dealing With the Transition

Privatization covers a range of possible alternatives, all of which would require federal borrowing to pay transition costs. Unfortunately, the Achilles heel in all this is that now is a bad time to propose more federal borrowing, even if it has clear long-term benefits to future retirees.

Todd Henderson in the Wall Street Journal suggests a seeding of capital provided by government at birth along with an insurance program to smooth returns. Another idea is to offer an inducement to delay retirement claims by allowing at least a portion of future benefits to be taken as a lump sum. If retirees can privately invest at a more advantageous return, they might be willing to accept a substantial discount on the actuarial value of their benefits.

In fact, there is evidence that a majority of participants seem to prefer distributions of lump sums because they don’t value their future benefits at anything like that suggested by the SSA analysis. In fact, many participants would defer retirement by 1 – 2 years given a lump sum payment. Discounts and/or delayed claims would reduce the ultimate funding shortfall, but it would require substantial federal borrowing up front.

Additional federal borrowing would also be required under a private option for investing one’s own contributions for future dispersal. The impact of this change on the system’s long-term imbalances would depend on the share of earners willing to opt-out of the traditional SS program in whole or in part. More opt-outs would mean a smaller long-term obligations for the traditional system, but it would be hampered by a costly transition over a number of years. Starting from today’s PAYGO system, someone still has to pay the benefits of current retirees. This would almost certainly mean federal borrowing. Spreading the transition over a lengthy period of time would reduce the impact on credit markets, but the borrowing would still be substantial.

For example, perhaps earners under 35 years of age could begin opting out of a portion or all of the traditional program at their discretion, investing contributions for their own future use. Thus, only a small portion of contributions would be diverted in the beginning, and amounts diverted would contribute to the nation’s available pool of saving, helping to keep borrowing costs in check. By the time these younger earners reach retirement age, nearly all of today’s retirees will have passed on. Ultimately, the average retiree will benefit from higher returns than under the traditional program, but since they won’t be (fully) paying the benefits of current or near-term retirees, the public must come to grips with the bad promises of the past and fund those obligations in some other way: reduced benefits, taxes, or borrowing.

Another objection to privatization is financial risk, particularly for lower-income beneficiaries. Limiting opt-outs to younger earners with adequate time for growth would mitigate this risk, along with a reversion to the traditional program after age 45, for example. Some have proposed limiting opt-outs to higher earners. Bear in mind, however, that the financial risk of private accounts should be weighed against the political and demographic risk already inherent in the existing system.

One more possibility for bridging the transition to private, individually-controlled accounts is to sell federal assets. I have discussed this before in the context of funding a universal basic income (which I oppose). The proceeds of such sales could be used to pay the benefits of current and near-term retirees so as to allow the opt-out for younger workers. Or it could be used to pay off federal debt accumulated in the process. The asset sales would have to proceed at a careful and deliberate pace, perhaps stretching over several decades, but those sales could include everything from the huge number of unoccupied federal buildings to vast tracts of public lands in the west, student loans, oil and gas reserves, and airports and infrastructure such as interstate highways and bridges. Of course, these assets would be more productive in private hands anyway.

The Likely Outcome

Will any such privatization plan ever see the light of day? Probably not, and it’s hard to guess when anything will be done in Washington to address the insolvency we already face. Instead, we’ll see some combination of higher payroll taxes, higher payroll taxes on high earners through graduated payroll tax rates or by lifting the earnings cap, reduced benefits on further retirees, limits on COLAs to low career earners, and means-tested benefits. Some have mentioned funding Social Security shortfalls with income taxes. All of these proposals, with the exception of automatic benefit cuts in 2035, would require acts of Congress.

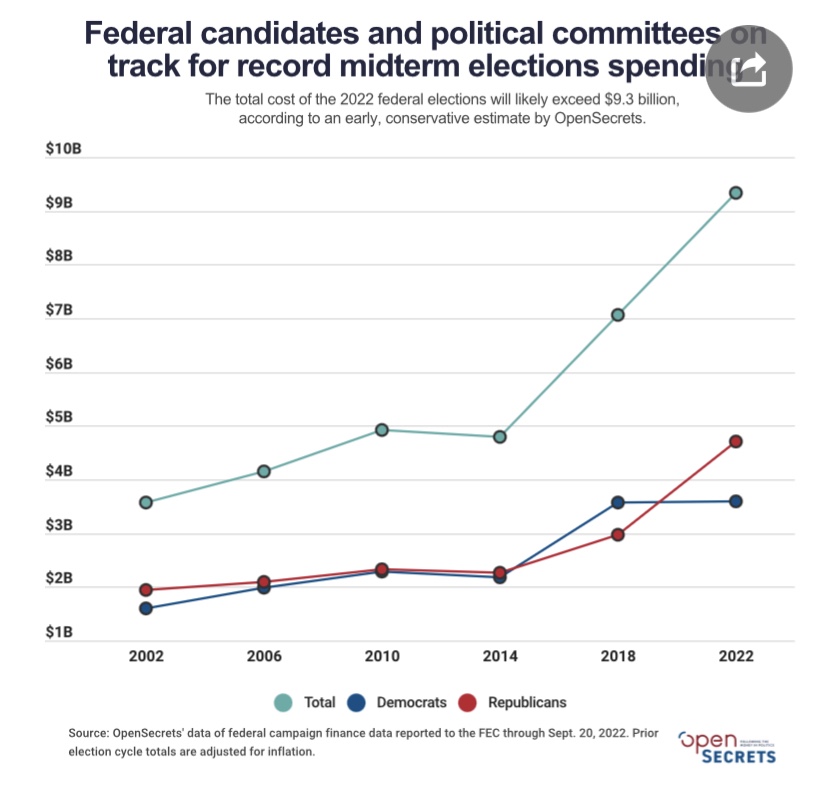

I’m really grateful to have the midterm elections behind us. Well, except for the runoff Senate race in Georgia, the cockeyed ranked-choice Senate race in Alaska, and a few stray House races that remain unsettled after almost two weeks. I’m tired of campaign ads, including the junk mail and pestering “unknown” callers — undoubtedly campaign reps or polling organizations.

It’s astonishing how much money is donated and spent by political campaigns. This year’s elections saw total campaign spending (all levels) hit $16.7 billion, a record for a mid-term. The recent growth in campaign spending for federal offices has been dramatic, as the chart below shows:

Do you think spending of a few hundred million dollars on a Senate campaign is crazy? Me too, though I don’t advocate for legal limits on campaign spending because, for better or worse, that issue is entangled with free speech rights. Campaigns are zero-sum events, but presumably a big donor thinks a success carries some asymmetric reward…. A success rate of better than 50% across several campaigns probably buys much more…. And donors can throw money at sure political bets that are probably worth a great deal…. Many donors spread their largess across both parties, perhaps as a form of “protection”. But it all seems so distasteful, and it’s surely a source of waste in the aggregate.

My reservations about profligate campaign spending include the fact that it is a symptom of big government. Donors obviously believe they are buying something that government, in one way or another, makes possible for them. The greater the scope of government activity, the more numerous are opportunities for rent seeking — private gains through manipulation of public actors. This is the playground of fascists!

There are people who believe that placing things in the hands of government is an obvious solution to the excesses of “greed”. However, politicians and government employees are every bit as self-interested and “greedy” as actors in the private sector. And they can do much more damage: government actors legally exercise coercive power, they are not subject in any way to external market discipline, and they often lack any form of accountability. They are not compelled to respect consumer sovereignty, and they make correspondingly little contribution to the nation’s productivity and welfare.

Actors in the private sector, on the other hand, face strong incentives to engage in optimizing behavior: they must please customers and strive to improve performance to stay ahead of their competition. That is, unless they are seduced by what power they might have to seek rents through public sector activism.

A people who grant a wide scope of government will always suffer consequences they should expect, but they often proceed in abject ignorance. So here is my rant, a brief rundown on some of the things naive statists should expect to get for their votes. Of course, this is a short list — it could be much longer:

Opportunities for graft as bureaucrats administer the spending of others’ money and manipulate economic activity via central planning.

A ballooning and increasingly complex tax code seemingly designed to benefit attorneys, the accounting profession, and certainly some taxpayers, but at the expense of most taxpayers.

Subsidies granted to producers and technologies that are often either unnecessary or uneconomic (and see here), leading to malinvestment of capital. This is often a consequence of the rent seeking and cronyism that goes hand-in-hand with government dominance and ham-handed central planning.

Redistribution of existing wealth, a zero- or even negative-sum activity from an economic perspective, is prioritized over growth.

Redistribution beyond a reasonable safety net for those unable to work and without resources is a prescription for unnecessary dependency, and it very often constitutes a surreptitious political buy-off.

Budgetary language under which “budget cuts” mean reductions in the growth of spending.

Large categories of spending, known in the U.S. as non-discretionary entitlements, that are essentially off limits to lawmakers within the normal budget appropriations process.

“Fiscal illusion” is exploited by politicians and statists to hide the cost of government expansion.

The strained refrain that too many private activities impose external costs is stretched to the point at which government authorities externalize internalities via coercive taxes, regulation, or legal actions.

Inflation and diminished buying power stoked by monetized deficits, which is a long tradition in financing excessive government.

Malinvestment of private capital created by monetary excess and surplus liquidity.

That malinvestment of private capital creates macroeconomic instability. The poorly deployed capital must be written off and/or reallocated to productive uses at great cost.

Funding for bizarre activities folded into larger budget appropriations, like holograms of dead comedians, hamster fighting experiments, and an IHOP for a DC neighborhood.

A gigantic public sector workforce in whose interest is a large and growing government sector, and who believe that government shutdowns are the end of the world.

Attempts to achieve central control of information available to the public, and the quashing of dissent, even in a world with advanced private information technology. See the story of Hunter Biden’s laptop. This extends to control of scientific narratives to ensure support for certain government programs.

Central funding brings central pursestrings and control. This phenomenon is evident today in local governance, education, and science. This is another way in which big government fosters dependency.

Mission creep as increasing areas of economic activity are redefined as “public” in nature.

Law and tax enforcement, security, and investigative agencies pressed into service to defend established government interests and to compromise opposition.

I’ve barely scratched the surface! Many of the items above occur under big government precisely because various factions of the public demand responses to perceived problems or “injustices”, despite the broader harms interventions may bring. The press is partly responsible for this tendency, being largely ignorant and lacking the patience for private solutions and market processes. And obviously, those kinds of demands are a reason government gets big to begin with. In the past, I’ve referred to these knee-jerk demands as “do somethingism”, and politicians are usually too eager to play along. The squeaky wheel gets the oil.

I mentioned cronyism several times in the list. The very existence of broad public administration and spending invites the clamoring of obsequious cronies. They come forward to offer their services, do large and small “favors”, make policy suggestions, contribute to lawmakers, and to offer handsomely remunerative post-government employment opportunities. Of course, certaIn private parties also recognize the potential opportunities for market dominance when regulators come calling. We have here a perversion of the healthy economic incentives normally faced by private actors, and these are dynamics that gives rise to a fascist state.

It’s true, of course, that there are areas in which government action is justified, if not necessary. These include pure public goods such as national defense, as well as public safety, law enforcement, and a legal system for prosecuting crimes and adjudicating disputes. So a certain level of state capacity is a good thing. Nevertheless, as the list suggests, even these traditional roles for government are ripe for unhealthy mission creep and ultimately abuse by cronies.

The overriding issue motivating my voting patterns is the belief in limited government. Both major political parties in the U.S. violate this criterion, or at least carve out exceptions when it suits them. I usually identify the Democrat Party with statism, and there is no question that democrats rely far too heavily on government solutions and intervention in private markets. The GOP, on the other hand, often fails to recognize the statism inherent in it’s own public boondoggles, cronyism, and legislated morality. In the end, the best guide for voting would be a political candidate’s adherence to the constitutional principles of limited government and individual liberty, and whether they seem to understand those principles. Unfortunately, that is often too difficult to discern.

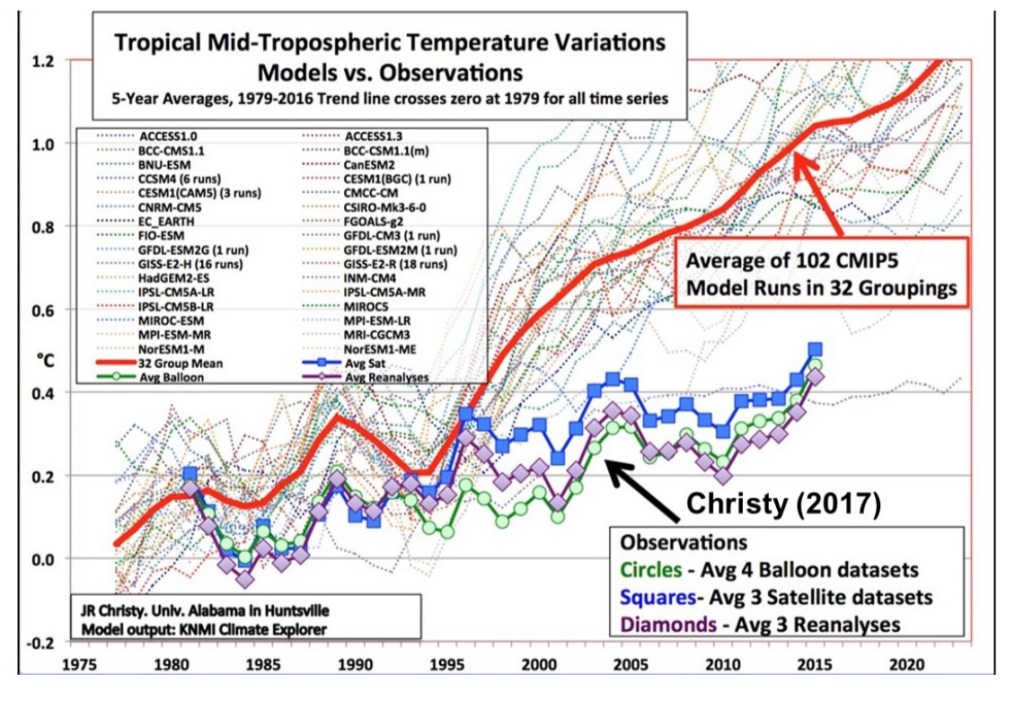

The weak methodology and accuracy of climate models is the subject of an entertaining Norman Rogers post. I want to share just a few passages along with a couple of qualifiers.

Rogers quotes Kevin Trenberth, former Head of Climate Analysis at the National Center for Atmospheric Research, with apparent approval. Oddly, Rogers does not explain that Trenberth is a strong proponent of the carbon-forcing models used by the UN’s Intergovernmental Panel on Climate Change (IPCC). He should have made that clear, but Trenberth actually did say the following:

“‘[None of the] models correspond even remotely to the current observed climate [of the Earth].’“

I’ll explain the context of this comment below, but it constitutes a telling admission of the poor foundations on which climate alarmism rests. The various models used by the IPCCc are all a little different and they are calibrated differently. I’ve noted elsewhere that their projections are consistently biased toward severe over-predictions of temperature trends. Rogers goes on from there:

“The models can’t properly model the Earth’s climate, but we are supposed to believe that, if carbon dioxide has a certain effect on the imaginary Earths of the many models it will have the same effect on the real earth.”

But how on earth can a modeler accept the poor track record of these models? It’s not as if the bias is difficult to detect! On this question, Rogers says:

“The climate models are an exemplary representation of confirmation bias, the psychological tendency to suspend one’s critical facilities in favor of welcoming what one expects or desires. Climate scientists can manipulate numerous adjustable parameters in the models that can be changed to tune a model to give a ‘good’ result.“

And why are calamitous projections desirable from the perspective of climate modelers? Follow the money and the status rewards of reinforcing the groupthink:

“Once money and status started flowing into climate science because of the disaster its denizens were predicting, there was no going back. Imagine that a climate scientist discovers gigantic flaws in the models and the associated science. Do not imagine that his discovery would be treated respectfully and evaluated on its merits. That would open the door to reversing everything that has been so wonderful for climate scientists. Who would continue to throw billions of dollars a year at climate scientists if there were no disasters to be prevented? “

Indeed, it has been a gravy train. Today, it is reinforced by green-preening politicians, the many billions of dollars committed by investors seeking a continuing flow of public subsidies for renewables, tempting opportunities for international redistribution (and graft), and a mainstream media addicted to peddling scare stories. The parties involved all rely on, and profit by, alarmist research findings.

Rogers’ use of the Trenberth quote above might suggest that Trenberth is a critic of the climate models used by the IPCC. However, the statement was in-line with Trenberth’s long-standing insistence that the IPCC models are exclusively for constructing “what-if” scenarios, not actual forecasting. Perhaps his meaning also reflected his admission that climate models are “low resolution” relative to weather forecasting models. Or maybe he was referencing longer-term outcomes that are scenario-dependent. Nevertheless, the quote is revealing to the extent that one would hope these models are well-calibrated to initial conditions. That is seldom the case, however.