No sooner had I posted this piece on the bond market’s bemused reaction to DOGE’s cost-cutting potential than Treasury rates began to drop sharply. The 10-year Treasury note fell by about 30 basis points over the course of a week. It’s stabilized and up a little since then, but that drop had little to do with DOGE and everything to do with uncertainty about Trumpian policies and signs of a flagging economy.

Despite those probable causes, the excitement of falling rates prompted the author of this article to dive headlong into fantasy: “Interest Rates Are Falling Thanks to Cuts in Government Spending”. I hope he’s right that real cuts in government spending will be forthcoming, but that’s highly speculative at this point.

In fact, markets are grappling with massive uncertainties at the moment. Under these circumstances, a preference for safety among investors means a flight to low-risk assets like treasuries, forcing their prices up and yields down.

Tariff threats against long-time allies and adversaries alike are a huge source of uncertainty for markets, especially given Trump’s unpredictable thrusts and parries. The burden of U.S. tariffs falls largely on American buyers and tariffs are of limited revenue potential. They have already prompted announcements of retaliation, so the possibility of a trade war is real, which would create a major disruption in economic activity. This portent comes atop growing signs that a slowdown is already underway in the U.S. economy. As Eric Boehm notes, tariffs are all costs and no benefits, and their mere prospect adds significant risk to the economic and political outlook.

Budgetary developments have also been unsettling to markets. Despite promises of reduced federal spending, signs point to even larger deficits. The budget resolution passed by the House of Representatives in late February calls for various spending reductions, but it would extend the Trump tax cuts and increase defense and border control spending. On balance, deficits under the bill would be higher by $4 trillion over 10 years. That is not reassuring, and Trump still wants to eliminate taxes on tips, overtime, and Social Security benefits, which would require separate legislation. State and local tax deductions are also a hot topic. All this obviously undermines the notion that investors should take a rosy view of the outlook for reduced Treasury borrowing under Trump. Of course, higher deficits would be expected to push Treasury rates upward, but the point here is that on balance, DOGE and the Trump Administration have yet to provide a convincing case that rates should decline.

Every week the administration finds a way to demonstrate its lack of seriousness with respect to paying off the public debt. First we had the $5,000 “DOGE dividend” to all Americans. And last week a Strategic Bitcoin Reserve was authorized by Executive Order, to be funded by crypto asset forfeitures and civil penalties. While this type of funding technically qualifies as “budget neutral”, the better alternative would be to put those funds toward paying off debt. In any case, the whole idea makes about as much sense as a Hawk Tuah coin reserve.

The desire for safe assets is perhaps made more urgent by the bellicosity of Trump’s foreign policy initiatives. His multiple mentions of World War III simply can’t go over well with risk-averse investors. Rightly or wrongly, he’s thrown down the gauntlet with both Iran and Hamas, and he’s taken a fairly confrontational line with Greenland, Panama, Canada, Mexico, Venezuela, China, Russia, and especially (and unfairly) Ukraine. Ah, yes, all in the spirit of negotiating deals. We shall see.

As for DOGE, I’m a big fan of its mission to reduce waste and fraud in government, though its reporting of specific accomplishments thus far has been shrouded by inconsistencies and confusion.DOGE claims to have secured $105 billion in savings in the first six weeks of the Trump presidency, but that figure includes asset sales, which can pay down debt but aren’t deficit reduction. It’s also not clear how adverse court orders are reflected in the figure. For that matter, the reported savings are not given with any time dimension. The real savings thus far certainly don’t add up to $105 billion per year. And even at face value, those savings won’t get DOGE to its goal of $2 trillion in deficit reduction by July 2026 without some spectacular wins along the way. Medicaid fraud might be a big one, but that remains to be seen. This report on DEI initiatives by agency also offers some promising targets. (But now, apparently DOGE’s goal has been scaled back to $1 trillion in savings).

And there is one other hurdle: even after DOGE and the Administration identify and impound amounts already authorized, the savings will not be permanent without congressional action on budgetary recissions. That could be tough.

So the bond market is rightly skeptical of whether DOGE and the Administration can achieve major and permanent reductions in federal deficits. The recent drop in rates has much more to do with the economy and an array of uncertainties surrounding the values of risk assets.

I want a federal government with a less pervasive presence in the private sphere. That’s why I oppose a U.S. sovereign wealth fund (SWF), but President Trump issued an executive order (EO) on February 3 setting in motion the creation of an SWF. It would hold various assets with the ostensible intent to earn a return benefiting American taxpayers.

Here are a few comments on the form an SWF might take:

1) How would the SWF be funded?

—Sales of federal assets like federal land, buildings, and the sale of extraction rights? These are probably the least offensive possibilities for funding an SWF, but the proceeds, if and when they materialize, should be used to pay off our massive federal debt, not to fund a governmental piggy bank.

—Taxes/Tariffs? Funding an SWF via taxes or tariffs would be contrary to the EO’s stated objective to “lessen the burden of taxes on American families and small businesses”. Moreover, it would be contrary to a pro-growth agenda, undermining any gains an SWF might produce.

—Borrowing? Another contradiction of a basic rationale for the SWF, which is “to promote fiscal sustainability”. It would mean more debt on top of a mountain of debt that is already growing at an unsustainable rate.

—“Deals” that might place assets under government ownership? Already, potential buyers of TikTok are singing the praises of a partnership with the SWF. Trump seems to think the government can acquire interests in certain enterprises in exchange for allowing them to operate in the U.S. He also believes that federal dollars can be used for development in order to acquire ownership capital. The federal government should not engage in the development of private resources. Business enterprises should remain private or be privatized, to the extent that their ownership has nothing to do with the provision of public goods.

2) What kinds of investments would be held in the SWF? Stocks and bonds? TikTok shares? Private equity? Crypto? The Gaza Riviera REIT?

These are all terrible ideas. Government ownership of the means of production, or socialism, virtually guarantees underperformance and subservience to political objectives. Federal acquisition of private businesses is not a legitimate function of the state.

There is no point in having the government hold a Bitcoin or crypto reserve. First, giving the U.S. government an interest in the private blockchain undermines the very purpose that most users feel gives the blockchain value. Second, the return on crypto depends only on price changes, and most forms of crypto are volatile. It is a stretch to believe that crypto assets have value in promoting “fiscal sustainability” or national security.

3) How would the SWF’s assets and earnings ultimately be used?

The EO plainly states that earnings in the SWF are to be used to promote fiscal sustainability and benefit taxpayers. In the presence of a large and growing national debt, the best path toward those objectives would be to use any and all spare funds to pay off debt and limit the explosive interest burden it imposes. This puts the funds back into hands of private investors, who will respond to market incentives by deploying the capital as they see fit. Does anyone truly think government planners know better how to put those funds to use?

SWF and Future Debt Service

Just to clarify matters, let’s quantify two alternatives: 1) pay off debt immediately; 2) create an SWF to invest funds and pay off debt later. Suppose the government stumbles upon a spare $100. It can immediately pay off $100 of debt and avoid a certain $3.50 in interest expense in year one. If instead an SWF invests the funds at an expected (but uncertain) return of 7%, then perhaps a greater reduction in the debt can be made a year later. How much? Not $107, but only $103.50 (assuming the 7% return is realized) because the $3.50 interest expense on the debt was not avoided in year one. The SWF must earn twice the interest cost on debt to break even on the proposition. That might be possible for an average return over many years, but the returns will vary and the government is likely to botch the job in any case.

An Itch For Intervention

The SWF is subject to dangers inherent in many government activities. One is that the funds held in reserve might be used as a tool of market intervention and/or political mischief, much as Joe Biden attempted to tamp down oil prices by releasing millions of barrels from the Strategic Petroleum Reserve. An administration having available a large pool of financial assets might be tempted to use it to intervene in various markets to manipulate asset prices. And even if you happen to like the interventions of one administration, you might hate the interventions of another.

The Scratch That Corrupts

In testament to the inefficacy and corruption inherent in government intervention in private markets, Peter Earle offers a number of examples of government planning gone awry. It’s not difficult to understand the dysfunction:

“A sovereign wealth fund would not, whatever the intentions of its government administrators, be guided purely by market signals but rather by political interests. That virtually ensures poor investment choices, investments in politically favored industries, and/or wasteful subsidies tending to yield subpar returns.

“Government officials will not have the same rigorous concern for opportunity costs that drives private investors and for-profit managers, as bureaucratic decision-making is often guided by political priorities and budget cycles rather than the disciplined allocation of capital to its most productive use. The Knowledge Problem is real — and ignoring it is expensive.“

“…there are systemic governance issues and regulatory gaps that can enable SWFs to act as conduits of corruption, money laundering, and other illicit activities.“

Therefore, the management and operations of an SWF require great transparency as well as strong governance and oversight. This obviously adds a layer of cost as well.

Sound Planning

There is an economic rationale for holding funds in reserve for certain, earmarked purposes. For example, private businesses usually maintain reserves for the upkeep or replacement of physical capital. Shouldn’t the government do the same for public infrastructure such as highways or harbors? Public investments in physical capital should be planned such that the flow of tax revenue is adequate to replenish infrastructure from wear and tear. To the extent that the necessary expenditures are “lumpy”, however, a maintenance reserve fund is sound practice, as long as its management is transparent and accountable, and its holdings represent prudent risks.

Another example is the maintenance of a reserve fund for pension payments. This is a reasonable and even necessary practice under traditional defined benefit plans, but those plans have often fallen short of their obligations in practice. The private sector stayed ahead of this risk by shifting overwhelmingly to defined contribution plans. As part of this shift, the existing pension obligations of many private entities were converted to vested “cash value” balances. The public sector should do the same, putting employees in charge of their own retirement savings.

Countries with SWFs tend to be small and also tend to run budget surpluses. Very often, they are funded with revenue earned from abundant natural resources. But even those governments short-change their citizens by failing to reduce tax rates, which would promote growth.

Nonsensical Appeal to Nationalism

Why does the creation of an SWF sound so good to people who should know better? I think it has something to do with the nationalist urge to embrace symbols of patriotic strength. An SWF might evoke the emotive impact of phrases like “sound money” or “a strong dollar”. But in the presence of a large public debt and large, continuing budget deficits, the kind of SWF envisioned by Trump would be counterproductive. Future obligations to pay down the public debt are better addressed in the present, to the extent possible. The government has no business hoarding private financial assets as a means of outrunning debt. Sure, the return on equity usually exceeds the interest rate on public debt, but private investors are better at allocating capital than government, so government should not attempt to take on that role.

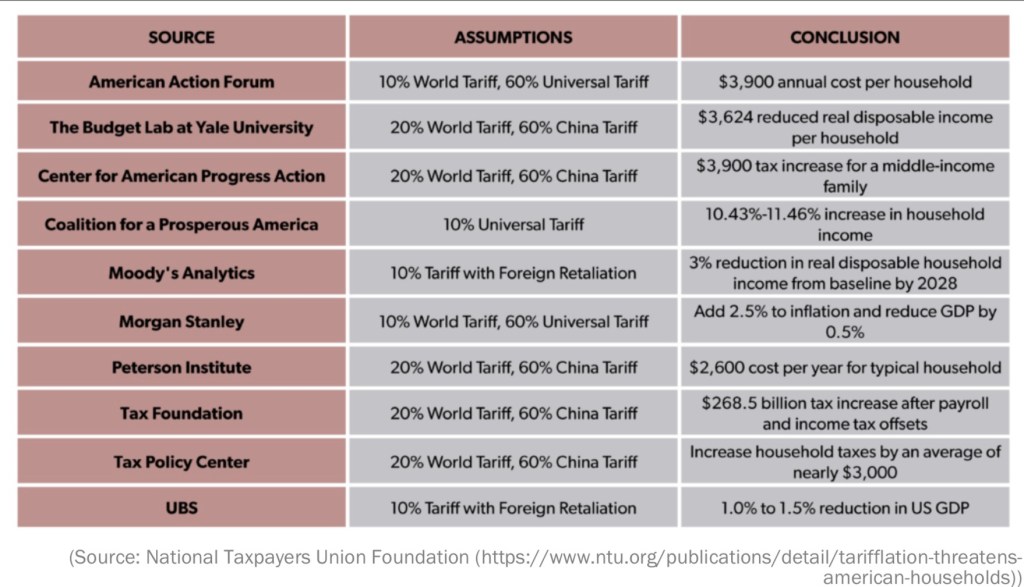

The table above is from Eric Boehm at Reason.com. It shows a variety of negative economic projections based on the likely imposition of tariffs by the incoming Trump Administration. Donald Trump’s protectionist agenda is motivated in large part by the notion that imports of foreign goods and services harm the U.S. economy. This misapprehension is common on both the populist left and the nationalist right, but it is also fueled by special interests averse to competition. Especially puzzling are those who extol the virtues of capitalism and free markets while claiming that free markets across borders are inimical to our nation’s economic interests.

Imports and Domestic Spending

Many assume that imports directly reduce GDP. In fact, on this point, some might be led astray by a superficial exposure to macroeconomics. As Noah Smith has noted, they might think back to the simple spending definition of GDP they learned as college freshmen:

GDP = C + I + G + (X – M),

where C is consumer spending on final goods and services, I is investment spending, G is government spending, X is foreign spending on U.S. exports, and M is U.S. spending on imports from abroad. So imports are subtracted! Doesn’t that mean imports directly reduce GDP?

The key here is to recognize that C, I, and G already include spending on imported goods. Therefore, imports must be subtracted from the spending totals to find the value spent on domestically-produced final goods and services. No, imports are not a direct, net subtraction from GDP.

Your Loathsome Foreign Car

Of course the domestic impact of imports goes deeper than this simple accounting framework. If someone decides to purchase an imported good instead of a close substitute produced domestically, what happens to GDP? If the decision has an immediate impact on production, then U.S. GDP declines. Otherwise, the domestic good is new inventory investment (part of I above), and there is no change. But if the import decision is repeated, the result is permanently lower U.S. GDP relative to the alternative, as producers won’t want to add to inventories indefinitely. The same is true if a domestic producer decides to purchase a component or raw material produced overseas rather than one produced at home.

The import decision causes a domestic producer to lose a sale along with the profit that sale would have earned. That puts pressure on the firm’s workers and wages as well. The firm still has the value of the unit in inventory, but if the import decision is repeated there will be more substantial follow-on effects on production, employment, spending, and saving.

Not So Fast

There is still more to the story, of course. By purchasing the foreign good,,which in the buyer’s estimation delivers greater value at that point in time, there is a gain in consumer surplus that is very real. To the buyer, that gain is perhaps equivalent to dollars in the bank. Their real wealth has increased relative to the surplus value of the foregone domestic purchase. This, too, will likely have follow-on effects in terms of spending and saving, but positive effects.

Therefore, to a first approximation, the immediate effects of an import purchase on total domestic welfare are ambiguous. Consumers of imports gain value; producers of import-competing goods lose value.

As to the loss of the domestic sale, competition is tough, but it greatly contributes to the efficiency of the free market system and to the well being of consumers. Let’s face it: ultimately, the whole point of economic activity is to enable consumption. Production has no other purpose. So producers must react to competition and strive to improve value for buyers along any margins they can. That, in turn, is unequivocally positive for potential buyers both here and abroad.

It’s also true that the purchase of foreign goods means that dollars must be sold in exchange for foreign currency. That weakens the dollar, but those “excess dollars” are generally used to purchase U.S. assets, including physical capital. That direct investment promotes economic growth.

Open Economy, Open Mind

No matter what you believe about the net benefits or costs of a single import transaction like the one described above, it is misleading to draw conclusions about the benefits of foreign trade based on a single transaction, or even a series of repeated transactions.

First, consumer sovereignty is based on freedom of choice, including the freedom to purchase from any seller, domestic or foreign. Consumers greatly benefit from that broad freedom. Add to that the benefit of producers who are free to purchase inputs from any source they believe to offer the greatest value (a benefit that ultimately flows through to consumers). These freedoms ultimately enhance productivity and well being.

Trade across borders leverages the same economic advantages as trade within borders. People tend to accept the latter as truth without giving it a thought, yet the former is often rejected reflexively. The question is inappropriately bound up in issues like patriotism and, over time, an excessive focus on high-visibility job losses in traditional industries.

Trade allows people and their countries to specialize in producing things at which they are comparatively efficient, i.e., in which they are lower-cost producers. This is at the very heart of mutually beneficial exchange: no party to a voluntary transaction expects to suffer a loss. And in trade, when an external, domestic party sustains a lost sale, for example, they have the opportunity to improve or reallocate their resources to endeavors to which they are better suited. So there are direct gains from trade and there are indirect gains via the discipline of competition, including the benefits of reallocating scarce resources from inefficient to efficient uses.

Tariff Gains

Now we shift gears to tariffs: interventions having benefits that are more concentrated than costs, and which tend to be more ephemeral:

— Domestic producers who compete with imports gain through the grant of additional market power, given the tax on foreign goods and services. These producers now have more pricing flexibility, and what is often more pertinent, survivability.

— Workers at domestic firms will benefit to the extent that their employers face reduced foreign competition. Some combination of employment, hours, and wages may rise.

— Some firms have mixed gains and losses, with more pricing power over final product but elevated costs due to the use of taxed foreign components.

Tariff Losses

Who pays when government succumbs to irrational protectionist pressure and attempts to restrict imports via tariffs?

— Domestic consumers suffer a loss of freedom and bear a large part of the burden of the tariff tax.

— Higher prices for imports lead to higher prices for competing domestic goods, causing consumers to experience a loss of purchasing power.

— Domestic businesses suffer a loss of control over input decisions. Those already utilizing foreign inputs (and their buyers downstream) bear some of the burden of the tariff tax. For example, tariffs could be quite damaging to the U.S. AI industry, a result that would run strongly contrary to Trump’s promise to promote American AI.

— The U.S. suffers a loss of foreign investment, which could engender higher interest rates, lower productivity growth, and lower real wages.

— As Tyler Cowen puts it in a review of this paper, “… lobbying, logrolling and political horse-trading were essential features of the shift toward higher US tariffs. A lot of the tariffs of the time [1870 -1909] depended on which party controlled Congress, rather than economic rationality.“

— Tariffs tend to reduce economic growth due to diminished productivity in tariff-protected industries, which also erodes real wages. Less productive firms capture a significant share of the benefits of tariffs, so that economic growth falls due to a compositional effect. Higher prices for imports and import-competing goods undermine the real gains of import-protected workers.

— Finally, tariffs invariably beget retaliatory tariffs by erstwhile friendly trading partners. Export industries and their employees take a direct hit. This retaliation damages the prospects of the most productive exporters, while weaker exporting firms might be forced to close shop unnecessarily.

One other note: the discussion of gains and losses above is essentially the same for policies that reward the use of American labor via tax breaks. This not only penalizes imports of final and intermediate foreign goods, it subsidizes high-cost domestic labor. Obviously, the upshot is a less competitive U.S. economy.

Tariff-Threat Policy

To be fair, Donald Trump has said he’d use the threat of tariffs strategically to achieve a variety of objectives, not all of which are directly related to trade. We can hope that many of those threats won’t be acted upon. On one hand, that’s more appealing than general tariffs, with potential foreign policy gains and less in the way of general damage to the economy. On the other hand, the discretionary application of tariffs could invite political favoritism and foster a corrupt rent-seeking environment.

Conclusion

Trade protectionism protects weak and strong producers alike. The weak should not be given artificial incentives to produce goods inefficiently. That’s simply a waste of resources. Protecting the strong is unnecessary and discourages the drive for efficiency as well as real value creation. It lends market power to already powerful firms, leading to higher prices and penalizing domestic consumers.

One last aside: tariffs cannot raise anywhere close to the revenue necessary to replace the income tax, an absurd claim made by Trump on the campaign trail.

Only free trade is consistent with the values of a free society. It enhances choice, makes markets more competitive, creates incentives for efficiency, and cultivates opportunities for economic growth, That would serve Trump and the nation much better than the fixation on tariffs.

Wow! We’re less than a week from Election Day! I’d hoped to write a few more detailed posts about the platforms and policies of Kamala Harris and Donald Trump, but I was waylaid by Hurricane Milton. It sent us scrambling into prep mode, then we evacuated to the Florida Panhandle. The drive there and back took much longer than expected due to the mass exodus. On our return we found the house was fine, but there was significant damage to an exterior structure and a mess in the yard. We also had to “de-prep” the house, and we’ve been dealing with contractors ever since. It was an exhausting episode, but we feel like we were very lucky.

Now, with less than a week left till the election, I’ll limit myself to a summary of the positions of the candidates in a number of areas, mostly but not all directly related to policy. I assign “grades” in each area and calculate an equally-weighted “GPA” for each candidate. My summaries (and “grades”) are pretty off-the-cuff and not adequate treatments on their own. Some of these areas are more general than others, and I readily admit that a GPA taken from my grade assignments is subject to a bit of double counting. Oh well!

Role of Government: Kamala Harris is a statist through and through. No mystery there. Trump is more selective in his statist tendencies. He’ll often favor government action if it’s politically advantageous. However, in general I think he is amenable to a smaller role for the public than the private sector. Harris: F; Trump: C

Regulation: There is no question that Trump stands for badly needed federal regulatory reform. This spans a wide range of areas, and it extends to a light approach to crypto and AI regulation. Trump plans to appoint Elon Musk as his “Secretary of Cost Cutting”. Harris, on the other hand, seems to favor a continuation of the Biden Administration’s heavy regulatory oversight. This encourages a bloated federal bureaucracy, inflicts high compliance costs on the private sector, stifles innovation, and tends to concentrate industrial power. Harris: F; Trump: A

Border Policy: Trump wants to close the borders (complete the wall) and deport illegal immigrants. Both are easier said than done. Except for criminal elements, the latter will be especially controversial. I’d feel better about Trump’s position if it were accompanied by a commitment to expanded legal immigration. We need more legal immigrants, especially the highly skilled. For her part, Harris would offer mass amnesty to illegals. She’d continue an open border policy, though she claims to want certain limits on illegal border crossings going forward. She also claims to favor more funds for border control. However, it is not clear how well this would translate into thorough vetting of illegal entrants, drug interdiction at the border, or sex trafficking. Harris: D; Trump: B-

Antitrust: Accusations of price gouging by American businesses? Harris! Forty three corporations in the S&P 500 under investigation by the DOJ? The Biden-Harris Administration. This reflects an aggressively hostile and manipulative attitude toward the business community. Trump, meanwhile, might wheedle corporations to act on behalf of certain of his agendas, but he is unlikely to take such a broadly punitive approach. Harris: F; Trump: B-

Foreign Policy: Harris is likely to continue the Biden Administration’s conciliatory approach to dealing with America’s adversaries. The other side of that coin is an often tepid commitment to longtime allies like Israel. Trump believes that dealing from a position of strength is imperative, and he’s willing to challenge enemies with an array of economic and political sticks and carrots. He had success during his first term in office promoting peace in the Middle East. A renewed version of the Abraham Accords that strengthened economic ties across the region would do just that. Ideally, he would like to restore the strength of America’s military, about which Harris has less interest. Trump has also shown a willingness to challenge our NATO partners in order to get them to “pay their fair share” toward the alliance’s shared defense. My major qualification here has to do with the candidates’ positions with respect to supporting Ukraine in its war against Putin’s mad aggression. Harris seems more likely than Trump to continue America’s support for Ukraine. Harris: D+; Trump: B-

Trade: Nations who trade with one another tend to be more prosperous and at peace. Unfortunately, neither candidate has much recognition of these facts. Harris is willing to extend the tariffs enforced during the Biden Administration. Trump, however, is under the delusion that tariffs can solve almost anything that ails the country. Of course, tariffs are a destructive tax on American consumers and businesses. Part of this owes to the direct effects of the tax. Part owes to the pricing power tariffs grant to domestic producers. Tariffs harm incentives for efficiency and the competitiveness of American industry. Retaliatory action by foreign governments is a likely response, which magnifies the harm.

To be fair, Trump believes he can use tariffs as a negotiating tool in nearly all international matters, whether economic, political, or military. This might work to achieve some objectives, but at the cost of damaging relations more broadly and undermining the U.S. economy. Trump is an advocate for not just selective, punitive tariffs, but for broad application of tariffs. Someone needs to disabuse him of the notion that tariffs have great revenue-raising potential. They don’t. And Trump is seemingly unaware of another basic fact: the trade deficit is mirrored by foreign investment in the U.S. economy, which spurs domestic economic growth. Quashing imports via tariffs will also quash that source of growth. I’ll add one other qualification below in the section on taxes, but I’m not sure it has a meaningful chance.

Harris: C-; Trump: F

Inflation: This is a tough one to grade. The President has no direct control over inflation. Harris wants to challenge “price gougers”, which has little to do with actual inflation. I expect both candidates to tolerate large deficits in order to fulfill campaign promises and other objectives. That will put pressure on credit markets and is likely to be inflationary if bond investors are surprised by the higher trajectory of permanent government indebtedness, or if the Federal Reserve monetizes increasing amounts of federal debt. Deficits are likely to be larger under Trump than Harris due in large part to differences in their tax plans, but I’m skeptical that Harris will hold spending in check. Trump’s policies are more growth oriented, and these along with his energy policies and deregulatory actions could limit the inflationary consequences of his spending and tax policies. Higher tariffs will not be of much help in funding larger deficits, and in fact they will be inflationary. Harris: C; Trump: C

Federal Reserve Independence: Harris would undoubtedly like to have the Fed partner closely with the Treasury in funding federal spending. Her appointments to the Board would almost certainly lead to a more activist Fed with a willingness to tolerate rapid monetary expansion and inflation. Trump might be even worse. He has signaled disdain for the Fed’s independence, and he would be happy to lean on the Fed to ease his efforts to fulfill promises to special interests. Harris: D; Trump: F

Entitlement Reform: Social Security and Medicare are both insolvent and benefits will be cut in 2035 without reforms. Harris would certainly be willing to tax the benefits of higher-income retirees more heavily, and she would likely be willing to impose FICA and Medicare taxes on incomes above current earning limits. These are not my favorite reform proposals. Trump has been silent on the issue except to promise no cuts in benefits. Harris: C-; Trump: F

Health Care: Harris is an Obamacare supporter and an advocate of expanded Medicaid. She favors policies that would short-circuit consumer discipline for health care spending and hasten the depletion of the already insolvent Medicare and Medicaid trust funds. These include a $2,000 cap on health care spending for Americans on Medicare, having Medicare cover in-home care, and extending tax credits for health insurance premia. She supports funding to address presumed health care disparities faced by black men. She also promises efforts to discipline or supplant pharmacy benefit managers. Trump, for his part, has said little about his plans for health care policy. He is not a fan of Obamacare and he has promised to take on Big Pharma, whatever that might mean. I fear that both candidates would happily place additional controls of the pricing of pharmaceuticals, a sure prescription for curtailed research and development and higher mortality. Harris: F; Trump: D+

Abortion: The Supreme Court’s 2022 decision in Dobbs v. Jackson essentially relegated abortion law to individual states. That’s consistent with federalist principles, leaving the controversial balancing of abortion vs. the unborn child’s rights up to state voters. Geographic differences of opinion on this question are dramatic, and Dobbs respects those differences. Trump is content with it. Meanwhile, Harris advocates for the establishment of expanded abortion rights at the federal level, including authorization of third trimester abortions by “care providers”. And Harris does not believe there should be religious exemptions for providers who do not wish to offer abortion services. No doubt she also approves of federally funded abortions. Harris: F; Trump: A

Housing: The nation faces an acute housing shortage owing to excessive regulation that limits construction of new or revitalized housing. These excessive rules are primarily imposed at the state and local level. While the federal government has little direct control over many of these decisions, it has abetted this regulatory onslaught in a variety of ways, especially in the environmental arena. Harris is offering stimulus to the demand side through a $25,000 housing tax credit for first-time home buyers. This will succeed in raising the cost of housing. She has also called for heavier subsidies for developers of low-income housing. If past is prologue, this might do more to line the pockets of developers than add meaningfully to the stock of affordable housing. Harris also favors rent controls, a sure prescription for deterioration in the housing stock, and she would prohibit software allowing landlords to determine competitive neighborhood rents. Trump has called for deregulation generally and would not favor rent controls. Harris: F; Trump B

Taxes: Harris has broached several wildly destructive tax proposals. Perhaps the worst of these is to tax unrealized capital gains, and while she promises it would apply only to extremely wealthy taxpayers, it would constitute a wealth tax. Once that line is crossed, the threat of widening the base becomes a very slippery slope. It would also be a strong detriment to domestic capital investment and economic growth. Harris would increase the top marginal personal tax rate and the corporate tax rate, which would discourage investment and undermine real wage growth. She’d also increase estate tax rates. As discussed above, she unwisely calls for a $25,000 tax credit for first-time homebuyers. She also wants to expand the child care tax credit to $6,000 for families with newborns. A proposed $50,000 small business tax credit would allow the federal government to subsidize and encourage risky entrepreneurial activity at taxpayers’ expense. I’m all for small business, but this style of industrial planning is bonkers. She would sunset the Trump (TCJA) tax cuts in 2026.

Finally, Harris has mimicked Trump in calling for no taxes on tips. Treating certain forms of income more favorably than others is a recipe for distortions in economic activity. Employers of tip-earning workers will find ways to shift employees’ income to tips that are mandatory for patrons. It will also skew labor supply decisions toward occupations that would otherwise have less economic value. But Trump managed to find an idea so politically seductive that Harris couldn’t resist.

Trump’s tax plans are a mixed bag of good and bad ideas. They include extending his earlier tax cuts (TCJA) and restoring the SALT deduction. The latter is an alluring campaign tidbit for voters in high-tax states. He would reduce the corporate tax rate, which I strongly favor. Corporate income is double-taxed, which is a detriment to growth as well as a weight on real wages. He would eliminate taxes on overtime income, another example of favoring a particular form of income over others. Wage earners would gain at the expense of salaried employees, so one could expect a transition in the form employees are paid over time. Otherwise, the classification of hours as “overtime” would have to be standardized. One could expect existing employees to work longer hours, but at the expense of new jobs. Finally, Trump says Social Security benefits should not be taxed, another kind of special treatment by form of income. This might encourage early retirement and become an additional drain on the Social Security Trust Fund.

The higher tariffs promised by Trump would collect some revenue. I’d be more supportive of this plank if the tariffs were part of a larger transition from income taxes to consumption taxes. However, Trump would still like to see large differentials between tariffs and taxes imposed on the consumption of domestically-produced goods and services.

Harris: F; Trump C+

Climate Policy: This topic has undergone a steep decline in relative importance to voters. Harris favors more drastic climate interventions than Trump, including steep renewable subsidies, EV mandates, and a panoply of other initiatives, many of which would carry over from the Biden Administration. Harris: F; Trump: B

Energy: Low-cost energy encourages economic growth. Just ask the Germans! Consistent with the climate change narrative, Harris wishes to discourage the use of fossil fuels, their domestic production, and even their export. She has been very dodgy with respect to restrictions on fracking. Her apparent stance on energy policy would be an obvious detriment to growth and price stability (or I should say a continuing detriment). Trump wishes to encourage fossil fuel production. Harris: F; Trump: A

Constitutional Integrity: Harris has supported the idea of packing the Supreme Court, which would lead to an escalating competition to appoint more and more justices with every shift in political power. She’s also disparaged the Electoral College, without which many states would never have agreed to join the Union. Under the questionable pretense of “protecting voting rights”, she has opposed steps to improve election integrity, such voter ID laws. And operatives within her party have done everything possible to register non-citizens as voters. Harris: F; Trump: A

First Amendment Rights: Harris has called for regulation and oversight of social media content and moderation. A more descriptive word for this is censorship. Trump is generally a free speech advocate. Harris: F; Trump A-

Second Amendment Rights: Harris would like to ban so-called “assault weapons” and high-capacity magazines, and she backs universal background checks for gun purchases. Trump has not called for any new restrictions on gun rights. Harris: F; Trump: A

DEI: Harris is strongly supportive of diversity and equity initiatives, which have undermined social cohesion and the economy. That necessarily makes her an enemy of merit-based rewards. Trump has no such confusion. Harris: F; Trump: A

Hysteria: The Harris campaign has embraced a strategy of demonizing Donald Trump. Of course, that’s not a new approach among Democrats, who have fabricated bizarre stories about Trump escapades in Russia, Trump as a pawn of Vladimir Putin, and Russian manipulation of the 2016 Trump campaign. Congressional democrats spent nearly all of Trump’s first term in office trying to find grounds for impeachment. Concurrently, there were a number of other crazy and false stories about Trump. The current variation on “Orange Man Bad” is that Trump is a fascist and a Nazi, and that all of his supporters are Nazis. And that Trump will use the military against his domestic political opponents, the so-called “enemy within”. And that Trump will send half the country’s populace to labor camps. The nonsense never ends, but could anything more powerfully ignite the passions of violent extremists than this sort of hateful rhetoric? Would it not be surprising if at least a few leftists weren’t interested in assassinating “Hitler” himself. This is hysteria, and one has to wonder if that is not, in fact, the intent.

Can any of these people actually define the term fascist? Most fundamentally, a fascist desires the use of government coercion for private gain (of wealth or power) for oneself and/or one’s circle of allies. By that definition, we could probably categorize a great many American politicians as fascists, including Barack Obama, Joe Biden, Donald Trump, and a majority of both houses of Congress. That only demonstrates that corporatism is fundamental to fascist politics. Less-informed definitions of fascism conflate it with everything from racism (certainly can play a part) and homophobia (certainly can play a part) to mere capitalism. But take a look at the demographics of Trump’s supporters and you can see that most of these definitions are inapt.

Is the Trump campaign suffering from any form of hysteria? It’s shown great talent at poking fun at the left. Of course, Trump’s reactions to illegal immigration, crime, and third-trimester abortions are construed by leftists to be hysterical. I mean, why would anyone get upset about those kinds of things?

Harris: F; Trump: A

“Grade Point Average”

I’m sure I forgot an area or two I should have covered. Anyway, the following are four-point “GPAs” calculated over 20 categories. I’m deducting a quarter point for a “minus” grade and adding a quarter point for a “plus” grade. Here’s what I get:

If there’s one simple lesson in economics that’s hard to get across it’s the destructive nature of protectionism. The economics aren’t hard to explain, but for many, the lessons of protectionist failure just don’t want to sink in. Putting aside matters of national security, the harms of protectionism to the domestic economy are greater than any gains that might inure to protected firms and workers. Shielding home industries and workers from foreign competition is generally not smart nor an act of patriotism, but that sentiment seems fairly common nonetheless.

The Pathology of Protectionism

Jingoistic slogans like “Buy American” are a pitch for voluntary loyalty to American brands. I’m all for voluntary action. Still, that propaganda relies on shaming those who find certain foreign products to have superior attributes or to be more economical. This feeds a psychology of economic insularity and encourages those who favors trade barriers, which is one of the earliest species of failed central planning.

The cognitive resistance to a liberal trade regime might have to do with the concentrated benefits of protectionist measures relative to the more diffuse (but high) costs it imposes on society. Some of the costs of protectionism manifest only with time, which makes the connection to policy less obvious to observers. Or again, obstructing trade and taxing “others” in the hope of helping ourselves may simply inflame nationalist passions.

Both Democrats and Republicans rally around policy measures that tilt the playing field in favor of domestic producers, often severely. And again, this near unanimity exists despite innumerable bouts with the laws of economics. I mean, how many times do you have to be beaten over the head to realize that this is a mistake? Unfortunately, politicians just don’t live in the long-term, they leap to defend powerful interests, and they seldom pay the long-term consequences of their mistakes.

Joe Biden’s “Buy American”

The Biden Administration has pushed a “Made In America” agenda since the President took office, It’s partly a sop to unions for their election support. Much of it had to do with tightening waivers granted under made-in-America laws (dating back to 1933) governing foreign content in goods procured by the federal government. The most recent change by Biden is an increase in the requirement for domestic content to 60% immediately and gradually to 75% from there. Also, “price preferences” will be granted to domestic producers of goods to strengthen supply chains identified as “critical”, including active pharmaceutical ingredients, certain minerals including rare earths and carbon fibers, semiconductors and their advanced packaging, and large capacity batteries such as those used in EVs.

There’s a strong case to be made for developing domestic supplies of certain goods based on national security considerations. That can play a legitimate role where defense goods or even some kinds of civilian infrastructure are involved, but Biden’s order applies much more broadly, including protections for industries that are already heavily subsidized by taxpayers. For example, the CHIPS Act of 2022 included $76 billion of subsidies and tax credits to the semiconductor industry.

“‘Buy American,’ like protectionism generally, can protect some blue-collar jobs — but at a steep price: A Peterson Institute for International Economics study concludes that it costs taxpayers $250,000 annually for each job saved in a protected industry. And lots of white-collar jobs are created for lawyers seeking waivers from the rules. And for accountants tabulating U.S. content in this and that, when, say, an auto component might cross international borders (U.S., Canadian, Mexican) five times before it is ready for installation in a vehicle.”

Biden’s new rules will increase the cost of federal procurement. They will squeeze out contracts with foreign suppliers whose wares are sometimes the most price-competitive or best-suited to a project. This is not a prescription for spending restraint, and it comes at a time when the federal budget is under severe strain. Here’s George Will again:

“This will mean more borrowing, not fewer projects. Federal spending is not constrained by a mere shortage of revenue. So, Biden was promising to increase the deficit. And this policy, which elicited red-and-blue bonhomie in the State of the Union audience, also will give other nations an excuse to retaliate (often doing what they want to do anyway) by penalizing U.S. exporters of manufactured goods. ….. Washington lobbyists for both will prosper.”

Domestic manufacturers who find their contracting status “protected” from foreign competition will face less incentive to perform efficiently. They can relax, rather than improve or even maintain productivity levels, and they’ll feel less pressure to price competitively. Those domestic firms providing goods designated by the government as “critical” will be advantaged by the “price preferences” granted in the rules, leading to a less competitive landscape and higher prices. Thus, Biden’s “Buy American” order is likely to mean higher prices and more federal spending. This is destructive and counter to our national interests.

Donald Trump’s Tariffs

In a recent set of proposals trialed for his presidential election campaign, Donald Trump called for “Universal Baseline Tariffs” on imported goods. In a testament to how far Trump has stumbled down the path of economic ignorance, his campaign mentions “patriotic protectionism” and “mercantilism for the 21st century”. Good God! Trump might be worse than Biden!

This isn’t just about China, though there are some specific sanctions against China in the proposal. After all, these new tariffs would be “universal”. Nevertheless, the Trump campaign took great pains to cloak the tariffs in anti-China rhetoric. Now, I’m very unfavorably disposed to the CCP and to businesses who serve or rely on China and (by implication) the CCP. Certainly, in the case of China, national security may dictate the imposition of certain forms of protectionism, slippery slope though it might be. Nevertheless, that is not what universal tariffs are about.

One destructive consequence of imposing tariffs or import quotas is that foreign governments are usually quick to retaliate with tariffs and quotas of their own. Thus, export markets are shut off to American producers in an escalating trade conflict. That creates serious recession risks or might reinforce other recessionary forces. Lost production for foreign markets and job losses in the affected export industries are the most obvious examples of protectionist harm.

Then consider what happens in protected industries in the U.S. and the negative repercussions in other sectors. The prices charged for protected goods by domestic producers rise for two reasons: more output is demanded of them, and protected firms have less incentive to restrain pricing. Just what the protectionists wanted! In turn, with their new-found, government-granted market power, protected firms will compete more aggressively for workers and other inputs. That puts non-protected firms in a bind, as they’ll be forced to pay higher wages to compete with protected firms for labor. Other inputs may be more costly as well, particularly if they are imported. These distortions lead to reduced output and jobs in non-protected industries. It also means American consumers pay higher prices for both protected and unprotected goods.

Consumers not only lose on price. They also suffer a loss of consumer sovereignty to a government wishing to manipulate their choices. When choices are curtailed, consumers typically lose on other product attributes they value. It also curtails capital inflows to the U.S. from abroad, which can have further negative repercussions for U.S. productivity growth.

When imports constitute a large share of a particular market, it implies that foreign nations have a comparative advantage in producing the good in question. In other words, they sacrifice less to produce the good than we would sacrifice to produce it in the U.S. But if country X has a comparative advantage in producing good X, it means it must have a comparative disadvantage in producing certain other goods, let’s say good Y. (That is, positive tradeoffs in one direction necessarily imply negative tradeoffs in the other.) It makes more economic sense for other countries (country Y, or perhaps the U.S.) to produce good Y, rather than country X, since country Y sacrifices less to do so. And that is why countries engage in trade with each other, or allow their free citizens to do so. It is mutually beneficial. It makes economic sense!

To outlaw or penalize opportunities for mutually beneficial trade will only bring harm to both erstwhile trading partners, though it might well benefit specific interests, including some third parties. Those third parties include opportunistic politicians wishing to leverage nationalist sentiments, their cronies in protected industries, and the bureaucrats, attorneys, and bean counters who manage compliance.

When Is Trade Problematic?

Protectionists often accuse other nations of subsidizing their export industries, giving them unfair advantages or dumping their exports below cost on the U.S. market. There are cases in which this happens, but all such self-interested claims should be approached with a degree of skepticism. There are established channels for filing complaints (and see here) with government agencies and trade organizations, and specific instances often prompt penalties or formal retaliatory actions.

There are frequently claims that foreign producers and even prominent American businesses are beneficiaries of foreign slave labor. A prominent example is the enslavement of Uyghur Muslims in China, who reportedly have been used in the manufacture of goods sold by a number of big-name American companies. This should not be tolerated by these American firms, their customers, or by the U.S. government. Unfortunately, there is a notable lack of responsiveness among many of these parties.

Much less compelling are assertions of slave labor based on low foreign wage rates without actual evidence of compulsion. This is a case of severely misplaced righteousness. Foreign wage rates may be very low by American standards, but they typically provide for a standard of living in the workers’ home country that is better than average. There is no sin in providing jobs to foreign workers at a local wage premium or even a discount, depending on the job. In fact, a foreign wage that is low relative to American wages is often the basis for their comparative advantage in producing certain goods. Under these innocent circumstances, there is no rational argument for producing those goods at much higher cost in the U.S.

Very troublesome are the national security risks that are sometimes attendant to foreign trade. When dealing with a clear adversary nation, there is no easy “free trade” answer. It is not always clear or agreed, however, when international relations have become truly adversarial, and whether trade can be usefully leveraged in diplomacy.

Conclusion

As I noted earlier, protectionism has appeal from a nationalist perspective, but it is seldom a legitimate form of patriotism. It’s not patriotic to limit the choices and sovereignty of the individual, nor to favor certain firms or workers by shielding them from competition while penalizing firms requiring inputs from abroad. We want our domestic industries to be healthy and competitive. Shielding them from competition is the wrong approach.

So much of the “problem” we have with trade is the infatuation with goals tied to jobs and production. Those things are good, but protectionists focus primarily on first-order effects without considering the damaging second-order consequences. And of course, jobs and production are not the ultimate goals of economic activity. In the end, we engage in economic activity in order to consume. We are a rich nation, and we can afford to consume what we like from abroad. It satisfies wants, it brings market discipline, and it leads to foreign investment in the American economy.

Biden and Trump share the misplaced objectives of mercantilism. They are both salesmen in the end, though with strikingly different personas. Salesmen want to sell, and I’m almost tempted to say that their compulsion causes them see trade as a one-way street. Biden is selling his newest “Buy American” rules not only as patriotic, but as a national security imperative. The former is false and the latter is largely false. In fact, obstructions to trade make us weaker. They will also contribute to our fiscal imbalances, and that contributes to monetary and price instability.

Like “Buy American”, Trump’s tariffs are misguided. Apparently, Trump and other protectionists wish to tax the purchases of foreign goods by American consumers and businesses. In fact, they fail to recognize tariffs as the taxes on Americans that they are! And tariffs represent a pointed invitation to foreign trading partners to impose tariffs of their own on American goods. You really can’t maximize anything by foreclosing opportunities for gain, but that’s what protectionism does. It’s astonishing that such a distorted perspective sells so well.

Much of what is labeled market failure is a consequence of government failure, or rather, failure caused by misguided public intervention, not just in individual markets but in the economy more generally. Misguided efforts to correct perceived excesses in pricing are often the problem, but there are myriad cases of regulatory overreach, ham-handed application of taxes and subsidies for various enterprises, and widespread cronyism. But it is often convenient for politicians to appear as if they are doing something, which makes activism and active blame of private enterprise a tempting path. The Biden Administration’s energy crisis offers a case in point. First, a digression on the efficiency of free markets. Skip the next two sections to get straight to Biden’s mess.

Behold the Bounty

I always spent part of the first class session teaching Principles of Economics on some incredible things that happen each and every day. Most college freshmen seem to take them for granted: the endless variety of goods that arrive on shelves each day; the ongoing flow of services, many appearing like magic at the flick of a switch; the high degree of coincidence between specific wants and all these fresh supplies; the variety and flow of raw materials and skills that are brought to bear; the fantastic array of sophisticated equipment deployed to assist in these efforts; and the massive social coordination necessary to accomplish all this. How does it all happen? Who collects all the information on what is wanted, and by whom? On the feasibility of actually producing and distributing various things? What miracle computer processes the vast set of information guiding these decisions and actions? Does some superior intelligence within an agency plan all this stuff?

The answer is simple. The seemingly infinite set of knowledge is marshaled, and all these tasks are performed, by the greatest institution of social cooperation to ever emerge: decentralized, free markets! Buying decisions are guided by individual needs and wants. Production and selling decisions are guided by resource availability and technology. And all sides react to evolving prices. Preferences, resources, and technology are in a constant state of flux, but prices react, signaling producers and consumers to make individual adjustments that correct larger imbalances. It is tempting to describe the process as the evolving solution to a gigantic set of dynamic equations.

The Impossible Conceit

No human planner or government agency is capable of solving this problem as seamlessly and efficiently as markets, nor can they hope to achieve the surplus welfare that redound to buyers and sellers in markets. Central planners or intervening authorities cannot possess the knowledge and coordinating power of the market mechanism. That doesn’t mean markets are “perfect”, of course. Things like external costs and benefits, dominant sellers, and asymmetric information can cause market outcomes to deviate from the competitive “ideal”. Inequities can arise from some of these imperfections as well.

What can be much worse is the damage to market performance caused by government policy. Usually the intent is to “correct” imperfections, and the rationale might be defensible. The knowledge to do it very well is often lacking, however. Taxes, subsidies, regulations, tariffs, quotas, capital controls, and manipulation of interest rates (and monetary and credit aggregates) are very general categories of distortion caused by the public sector. Then there is competition for resources via government procurement, which is frequently graft-ridden or price-insensitive.

Many public interventions create advantages for large sellers, leading to greater market concentration. This might best serve the private political power of the wealthy or might convey advantages to investments that happen to be in vogue among the political class. These are the true roots of fascism, which leverages coercive state power for the benefit of private interests.

Energy Vampires

Now we have the curious case of the Biden Administration and it’s purposeful disruption of energy markets in an effort to incentivize a hurried transition from fossil fuels to renewable energy. As I described in a recent post on stagflation,

“… Biden took several steps to hamstring the domestic fossil fuel industry at a time when the economy was still recovering from the pandemic. This included revoking permits for the Keystone pipeline, a ban on drilling on federal lands and federally-controlled waters in the Gulf, shutting down production on some private lands on the pretext of enforcing the Endangered Species Act, and capping methane emissions by oil and gas producers. And all that was apparently just a start.

As Mark Theisen notes, when you promise to destroy a particular industry, as Joe Biden has, by taxing and regulating it to death, who wants to invest in or even maintain production facilities? Some leftists with apparent influence on the administration are threatening penalties against the industry up to and including prosecution for ‘crimes against humanity’!”

In addition to killing Keystone, there remains a strong possibility that Biden will shut down the Line 5 pipeline in Michigan, and there are other pipelines currently under federal review. Biden’s EPA also conducted a purge of science advisors considered “too friendly” to oil and gas industry. This was intertwined with a “review” of new methane rules, which harm smaller, independent oil and gas drillers disproportionately.

Joe Biden’s “Build Back Better” (BBB) legislation, as clumsy in policy as it is in name, introduces a number of “Green New Deal” provisions that would further disadvantage the production and use of fossil fuels. Hart Energy provides descriptions of various tax changes that appeared in the Treasury’s so-called “Greenbook”, a collection of revenue proposals, many of which appear in the BBB legislation that recently passed in the House. These include rollbacks of various deductions for drilling costs, depletion allowances, and recovery rules, as well as hikes in certain excise taxes as well as taxes on foreign oil income. And all this while granting generous subsidies to intermittent and otherwise uneconomic technologies that happen to be in political favor. This is a fine payoff for cronies having invested significantly in these rent seeking opportunities. While the bill still faces an uphill fight in the Senate, apparently Biden has executive orders, held in abeyance, that would inflict more pain on consumers and producers of fossil fuels.

Biden’s energy policies are obviously intended to reduce supplies of oil, gas, and other fossil fuels. Prices have responded, as Green notes:

“Gas is up an average of 57% this year, with corresponding increases of 44% for diesel and a whopping 60% for fuel oil.”

The upward price pressure is not limited to petroleum: electricity rates are jumping as well. Consumers and shippers have noticed. In fact, while Biden crows about wanting “the rich” to pay for BBB, his energy policies are steeply regressive in their impact, as energy absorbs a much larger share of budgets among the poor than the rich. This is politically suicidal, but Biden’s advisors have chosen a most cynical tact as the reality has dawned on them.

Abusive Victim Blaming

Who to blame? After the predictable results of cramping domestic production and attacking fossil fuel producers, the Biden team naturally blames them for rising prices! “Price gouging” is a charge made by political opportunists and those who lack an understanding of how markets allocate scarce resources. More severe scarcity means that prices must rise to ration available quantities and to incentivize those capable of bringing forth additional product under difficult circumstances. That is how a market is supposed to function, and it mitigates scarcity!

But here comes the mendacious and Bumbling Buster Biden. He wants antitrust authorities at the FTC to investigate oil pricing. Again from Stephen Green:

There’s nothing quite like a threat to market participants to prevent the price mechanism from performing its proper social function. But a failure to price rationally is a prescription for more severe shortages.

Biden has also ordered the Strategic Petroleum Reserve (SPR) to release 50 million barrels of oil, a move that replaces a total of 2.75 days of monthly consumption in the U.S. The SPR is supposed to be drawn upon only in the case of emergencies like natural disasters, so this draw-down is as irresponsible as it is impotent. In fact, OPEC is prepared to offset the SPR release with a production cut. Biden has resorted to begging OPEC to increase production, which is pathetic because the U.S. was a net exporter of oil not long ago … until Biden took charge.

Conclusion

Properly stated, the challenge mounted against markets as an institution is not that they fall short of “perfection”. It is that some other system would lead to superior results in terms of efficiency and/or equity. Central planning, including the kind exercised by the Biden Administration in it’s hurried and foolish effort to tear down and remake the energy economy, is not even a serious candidate on either count.

Granted, there is a long history of subsidies to the oil and gas sector. I cannot defend those, but the development of the technology (even fracking) largely preceded the fruits of the industry’s rent seeking. At this point, green fuels receive far more subsidies (despite some claims to the contrary). Furthermore, the primacy of fossil fuels was not achieved by tearing down competing technologies and infrastructure. In contrast, the current round of central planning requires destruction of entire sectors of the economy that could otherwise produce efficiently for the foreseeable future, if left unmolested.

The Biden Administration has adopted the radical green agenda. Their playbook calls for a severe tilting of price incentives in favor uneconomic, renewable energy sources, despite the economy’s heretofore sensible reliance on plentiful fossil fuels. It’s no surprise that Biden’s policy is unpopular across the economic spectrum. His natural inclination is to blame a competitive industry victimized by his policy. It’s a futile attempt to avoid accountability, as if he thinks doubling down on the fascism will help convince the electorate that oil and gas producers dreamt up this new, nefarious strategy of overcharging customers. People aren’t that dumb, but it’s typical for the elitist Left presume otherwise.

As if you needed more evidence that governments are incompetent, look no further than trade policy: public officials the world over are almost universally ignorant regarding the effects of international trade and trade imbalances. In this sense, the Trump Administration’s new tariffs on imported steel and aluminum are in keeping with the long history of public sector foibles on trade. This phenomenon stems from an unhealthy and obsessive focus on the well-being of producers without regard to the implications of policy for consumers. Warren Meyer of Coyote Blog offers an evaluation of Chinese trade policy, which he mischievously (I believe) claims was written by a Chinese blogger on a “sister blog” called “Panda Blog“. Despite Meyer’s playfulness, the post is instructive:

“Our Chinese government continues to pursue a policy of export promotion, patting itself on the back for its trade surplus in manufactured goods with the United States. The Chinese government does so through a number of avenues, … each and every one of these government interventions subsidizes US citizens and consumers at the expense of Chinese citizens and consumers. A low yuan makes Chinese products cheap for Americans but makes imports relatively dear for Chinese. So-called ‘dumping’ represents an even clearer direct subsidy of American consumers over their Chinese counterparts. And limiting foreign exchange re-investments to low-yield government bonds has acted as a direct subsidy of American taxpayers and the American government, saddling China with extraordinarily low yields on our nearly $1 trillion in foreign exchange. Every single step China takes to promote exports is in effect a subsidy of American consumers by Chinese citizens.“

The very idea of a trade deficit is often used to intimate a threat to a nation’s economic health. Conversely, a trade surplus is used to suggest that a nation is achieving great economic success. Both contentions are nonsense. Here is more from “Panda Blog“:

“We at Panda Blog believe it is insane for our Chinese government to continue to chase the chimera of ever-growing foreign exchange and trade surpluses. These achieved nothing lasting for Japan and they will achieve nothing for China. In fact, the only thing that amazes us more than China’s subsidize-Americans strategy is that the Americans seem to complain about it so much. They complain about their trade deficits, which are nothing more than a reflection of their incredible wealth. … They complain about China buying their government bonds, which does nothing more than reduce the costs of their Congress’s insane deficit spending. They even complain about dumping, which is nothing more than a direct subsidy by China of lower prices for American consumers.

And, incredibly, the Americans complain that it is they that run a security risk with their current trade deficit with China! This claim is so crazy, we at Panda Blog have come to the conclusion that it must be the result of a misdirection campaign by CIA-controlled American media. After all, the fact that China exports more to the US than the US does to China means that by definition, more of China’s economic production is dependent on the well-being of the American economy than vice-versa.“

By the way, those “quotes” from “Panda Blog” appeared on Coyote Blog 12 years ago!

All nations tend to play these trade games to one extent or another. But protectionist actions always harm a nation’s consumers more than they help producers, a proposition that is easy to demonstrate using a simple supply and demand diagram. While the class of consumers is broader than the class of producers, ultimately “producer” and “consumer” are different roles played by the same individuals. So protectionism is always harmful to a nation, on balance. Furthermore, retaliation against another nation for its dim-witted trade barriers also harms the retaliating nation’s consumers more than it helps its producers, and that’s true regardless of whether retaliation begets reciprocal actions.

Of course, producers are generally in a better position than consumers to grease the political skids in their favor. In a separate post, Meyer notes that protectionist trade policies are rooted in cronyism. The costs to society are very real, but they tend to be diffuse and therefore less obvious to most consumers.

“A lot of the media seems to believe the biggest reason they are bad is that they will incite retaliatory tariffs from other countries, which they almost certainly will. But even if no one retaliated, even if the tariffs were purely unilateral, they would still be bad. In case after case, they are justified as increasing the welfare of a certain number of workers in targeted industries, but they hurt the welfare of perhaps 100x more people who consume or work for companies that consume the targeted products. Prices will rise for everyone and choices will be narrowed.“

A couple of points deserve emphasis in relation to my last post on Trump’s tariff action:

In terms of jobs, the tariffs announced by President Trump present a very poor risk-reward tradeoff (WSJ article is gated):

“The policy point is that Mr. Trump’s tariffs are trying to revive a world of steel production that no longer exists. He is taxing steel-consuming industries that employ 6.5 million and have the potential to grow more jobs to help a declining industry that employs only 140,000.“

Stephen Mihm discusses ways in which the U.S. steel industry squandered its superiority in the post-World War II era. Much of Mihm’s article is devoted to the industry’s failure to upgrade to new production technologies. Interestingly, however, it fails to mention the damaging role played by unions in the process. “Dumping” had very little to do with it.

Finally, Pierre Lemieux takes a closer look at the national security argument for trade barriers. He concludes that it is fallacious. Of course, it is an excuse for cronyism. Protectionism harms the competitiveness of the protected industries, which actually undermines national security. And protectionism is usually unnecessary on close examination. In the case of steel, for example, national defense and homeland security use only about 3% of American steel production. Beyond that simple fact, the argument is dangerously open-ended. Almost anything can be represented as critical to national security: steel, food, clothing, and many other categories. Even human resources.

Today, Trump announced that Canada and Mexico will be exempt from the new tariffs while a renegotiation of the North American Free Trade Agreement (NAFTA) is underway. That’s better, but this carve-out exempts only 25% of U.S. steel imports. Perhaps Australia will be granted an exemption as well, but additional carve-outs will prompt further increases in tariffs on non-exempt imports. Trump also said that U.S. flexibility in applying the new tariffs to allies will depend on their commitments for military spending!

Thus, rather than maintaining the pretense that trade relationships are about economics, the administration has conceded that the tariffs and the exemption process will be transparently political, never a prescription for efficient resource allocation. Moreover, U.S. trading partners are likely to be reluctant to test the politics of modifying their own trade manipulations at home. Indeed, the politics may dictate retaliation, rather than concessions. In any case, the governments of our trading partners are as clueless on trade as Trump, his Commerce Secretary Wilbur Ross, and his economic advisor Peter Navarro, or they would never intervene in private trade decisions to begin with.

You can get away with lousy policy by calling it a “negotiating tactic” for only so long. But that dubious ploy is one of the rationales offered last week by the Trump Administration for imposing a 25% tariff on imported steel and a 10% tariff on imported aluminum. Sure, the tariffs are like gifts rendered onto American steel and aluminum producers, their shareholders, and their unionized workers. The tariffs allow them to compete more effectively, without any effort, with foreign steel and aluminum in the domestic market, and the tariffs may also give them leeway to raise prices. The tariffs are also forgiving of degraded performance by domestic producers, since reduced competition relieves pressure for efficiency, a primary social cost of monopoly power.

So who pays for these gifts to the domestic steel and aluminum industries? A tariff, of course, is a tax, and a significant portion of it will be passed along into higher prices of both imported and domestically-produced steel and aluminum. Therefore, the burden of that tax will be borne to a large extent by domestics users, including every domestic industry that uses steel or aluminum as an input, and by consumers who purchase those products. That erodes the job security of many domestic workers outside of the steel and aluminum industries. In fact, the tariffs are unlikely to create more jobs even in the steel and aluminum industries given the negative impact of higher prices on the quantities of those metals demanded.

The desperate story line in support of tariffs also includes the assertion that the U.S. steel and aluminum industries are in such dire straits that they are in danger of vanishing. Statistics on U.S. production hardly suggest that is the case, however. Steel output in the U.S. has been reasonably steady since recovering from the last recession, though it has not achieved its pre-recession level. While aluminum output has been declining, it is hardly in a free fall. The stock prices of major steel and aluminum producers, which are forward-looking, have not demonstrated a particular need for government aid (as if that could ever justify a too-big or too-important-to-fail mentality).

Defenders of the tariffs claim that one effect will include additional direct investment in the U.S. by foreign producers of steel and aluminum, because they can avoid the tariffs by setting up production within our borders. Perhaps a few will, but capital is mobile in other sectors as well. Producers in other industries requiring intensive use of steel or aluminum inputs will now have an incentive to shift production overseas, where the tariffs won’t apply. Attempting to prevent such shifts via import tariffs on final products would quickly become a nightmare of central planning.

Apologists for the tariffs go even further, noting that our new regulatory and tax environment will bring foreign producers to the U.S., essentially making the tariffs irrelevant. If that’s the case, why bother imposing the tariffs at all? And why penalize consumers and industries requiring intensive use of steel or aluminum?

The argument that tariffs provide a stronger position from which to negotiate with foreign “trading partners” (or rather, their governments) is tenuous at best. More likely, the tariffs will prompt retaliation by foreign governments against a range of American products. The very notion that “trade wars are good”, tweeted by President Trump on Friday morning, is as nonsensical as a suggestion that voluntary exchange is destructive. Already, the EU has announced plans to retaliate by imposing tariffs on bourbon and motorcycles produced in the U.S.

Negotiations are unlikely to be successful. Perhaps some foreign governments who subsidize their steel and aluminum producers could be persuaded to enter talks. Our own domestic producers are penalized by various tariffs and quotas in place abroad, and those might be used by foreign interests as a lever in negotiations. However, the most fundamental foreign trade advantages, when they exist, have to do with low wages, less regulation, more efficient production facilities, and sometimes a more favorable tax environment. Wage levels reflect labor productivity, but those wage levels are valued more highly in their home countries than in the U.S, and penalizing these countries with trade sanctions merely penalizes their workers. Not all dimensions of a cost advantage can be negotiated, and in any case, healthy competition in any industry is always in the interests of a nation’s consumers.

National security is another standard argument in favor of protectionist measures. We’re told, for example, that we cannot allow China to produce all of the steel, but China provides only a small fraction of U.S. steel imports. Canada, Brazil and Mexico provide far more. In fact, China was in 11th place on that list in 2017. So our sources of steel are fairly well diversified. A domestic shortage of steel or aluminum caused by a breakdown in relations with one or more steel-exporting countries would lead to higher prices, but it would bring forth greater supplies from other countries and even from high-cost domestic sources. That is not a national emergency.