There is no better example of environmental degradation and waste than the spread of solar farms around the world, spurred on by short-sighted public policy and abetted by a subsidy-hungry investors. As a resource drain, wind farms are right up there, but I’ll focus here on the waste and sheer ugliness of solar farms, inspired by a fine article on their inefficiency by Matt Ridley.

What An Eyesore!

On a drive through the countryside you’ll see once bucolic fields now blanketed with dark solar panels. Hulking windmills are bad enough, but the panels can obliterate an entire landscape. If this objection strikes you as superficial, then your sensibilities run strangely counter to those of traditional environmentalists. It would be a bit less aesthetically offensive if solar farms actually solved a problem, but they don’t, and they impose other costs to boot.

Paltry Power

In terms of power generation, solar collection panels represent an inefficient use of land and other resources. Solar power has very low energy density relative to other sources. As Ridley says:

“Solar power needs around 200 times as much land as gas per unit of energy and 500 times as much as nuclear. Reducing the land we need for human civilisation is surely a vital ecological imperative. The more concentrated the production, the more land you spare for nature.“

The intermittency of solar power means that its utilization or capacity factor is far less than nameplate capacity, yet the latter is usually quoted by promoters and investors. The mismatch in timing between power demand and power generated by solar will not be overcome by battery technology any time soon.

And yet governments coerce taxpayers in order to create artificially high returns on the construction and operation of solar farms, a backward intervention that puts more efficient sources of power at a disadvantage.

Seduction On the Farm

Solar farms installed on erstwhile cropland reflect confused public priorities. Land that is well-suited to growing crops or grazing livestock is probably better left available for those purposes. Granted, rural landowners who add solar panels probably limit installations to their least productive crop- or rangeland, but not always. Private incentives are distorted by the firehose of subsidies available for solar installations. Regardless, lands left fallow, dormant or forested still put the sun’s energy to good ecological use.

Capital invested in solar power entails unutilized capacity at night and under-utilized capacity over much of the day. Peaks in solar collection generally occur when power demand is low during daylight hours, but it is unavailable when power demand is high in the evening. Battery technology remains woefully inadequate for effective storage, necessitating a steep ramp in back-up power sources at night. And those back-up sources are, in turn, underutilized during daylight hours. The over-investment made necessary by renewables is staggering.

Landowners can try to grow certain crops underneath or between panels, or grass and weeds for grazing livestock, on what sunlight reaches ground level. This is known as Agrivoltaics. It comes with extra costs, however, and it is a bit of a dive for crumbs. Ridley says agrivoltaics is a zero-sum game, but the federal government offers subsidized funding for “experiments” of this nature. Absent subsidies, agrivoltaics might well be negative-sum in an economic sense.

Environmental Hazards

Ridley discusses the severe environmental costs and add-on risks of solar farming to local environments. Fabrication of the panels themselves requires intensive mining, processing and energy consumption. In the field, the underlying structural requirements are massive. The panels raise air temperatures within their vicinity and present a hazard to waterfowl. Panels damaged by storms, birds, or deterioration due to age are pollution hazards. Furthermore, panels have heavy disposal costs at the end of their useful lives. and old panels are often toxic. Adding today’s inefficient battery technology to solar installations only compounds these environmental risks.

Better Alternatives

Solar and renewable energy advocates seem to have little interest in the efficiency advantages of dispatchable, zero-carbon nuclear power. Nor will they wait for prospective space-based solar collection. Instead, they continue to push terrestrial solar and the idle capital it entails.

It’s worth asking why advocates of energy planning tolerate the obvious ugliness and inefficiencies of solar farming. Of course, they are preoccupied with climate risk, or at least they’d like for you to be so preoccupied. They prescribe measures against climate risk that seem to offer immediacy, but these measures are ineffectual at best and damaging in other ways. There are better technologies for producing zero-carbon energy, and it looks as if the power demands of the AI revolution might finally provide the impetus for a renaissance in nuclear power investment.

As of February 2026, I’m adding this short preamble to a few older posts on the subject of AI and future prospects for human labor. In the original post below (and a few others), I overstated the case that the law of comparative advantage would assure a continued role for humans in production. I still think the case is strong, mind you, but now I’m convinced that the outcome depends on elasticities of input substitution and how those elasticities might shift given the advent of AI-augmented capital. You can read my most recent thoughts on the matter here.

____________________________________________

In this case, the “A” stands for Altman. Now Sam Altman is no slouch, but he’s taken a few ill-considered positions on public policy. Altman, the CEO of Open AI, wrote a blog post back in 2021 entitled “Moore’s Law For Everything” in which he predicted that AI will feed an explosion of economic growth. He also said AI will put a great many people out of work and drive down the price of certain kinds of labor. Furthermore, he fears that the accessibility of AI will be heavily skewed against the lowest socioeconomic classes. In later interviews (see here and here), Altman is somewhat demure about those predictions, but the general outline is the same: despite exceptional growth of GDP and wealth, he envisions job losses, an underclass of AI-illiterates, and a greater degree of income and wealth inequality.

Not Quite Like That

We’ve yet to see an explosion of growth, but it’s still very early in the AI revolution. The next several years will be telling. AI holds the potential to vastly increase our production possibilities over the course of the next few decades. For that and other reasons, I don’t buy the more dismal aspects of Altman’s scenario, as my last two posts make clear (here and here).

There will be plenty of jobs for people because humans will have comparative advantages in various areas of production. AI agents might have absolute advantages across most or even all jobs, but a rational deployment would have AI agents specialize only where they have a comparative advantage.

Scarcity will not be the sort of anachronism envisioned by some AI futurists, Altman included, and scarcity of AI agents (and their inputs) will necessitate their specialization in certain tasks. The demand for AI agents will be quite high, and their energy and “compute” requirements will be massive. AI agents will face extremely high opportunity costs in other tasks, leaving many occupations open for human labor, to say nothing of abundant opportunities for human-AI collaboration.

However, I don’t dismiss the likelihood of disruptions in markets for certain kinds of labor if the AI revolution proceeds as rapidly as Altman thinks it will. Many workers would be displaced, and it would take time, training, and a willingness to adapt for them to find new opportunities. But new kinds of jobs for people will emerge with time as AI is embedded throughout the economy.

Altman’s Rx

Altman’s somewhat pessimistic outlook for human employment and inequality leads him to make a couple of recommendations:

1) Ownership of capital must be more broadly distributed.

2) Capital and land must be taxed, potentially replacing income taxes, but primarily to fund equity investments for all Americans.

Here I agree with the spirit of #1. Broad ownership of capital is desirable. It allows greater participation in the capitalist system, which fosters political and economic stability. And wider access to capital, whether owned or not, allows a greater release of entrepreneurial energy. It also diversifies incomes and reduces economic dependency.

Altman proposes the creation of an American Equity Fund (AEF) to hold the proceeds of taxes on land and corporate assets for the benefit of all Americans. I’ll get to the taxes in a moment, but in discussing the importance of educating the public on the benefits of compounding, Altman seems to imply that assets in AEF would be held in individual accounts, as opposed to a single “public” account controlled by the federal government. Individual accounts would be far preferable, but it’s not clear how much control Altman would grant individuals in managing their accounts.

To Kill a Golden Goose

Taxes on capital are problematic. Capital can only be accumulated over time by saving out of income. Thus, as Michael Munger points out, as a general proposition under an income tax, all capital has already been taxed once. And we tax the income from capital at both the corporate and individual level. So corporate income is already double taxed: corporate profits are taxed along with dividend payments to shareholders.

Altman proposed in his 2021 blog post to levy a tax of 2.5% on the market value of publicly-traded corporations each year. The tax would be payable in cash or in corporate shares to be placed into the AEF. The latter would establish a kind of UnLiquidated Tax Reserve Accounts (ULTRA), which Munger discusses in the article linked above (my bracketed x% in the quote here):

“Instead of taking [x%] of the liquidated value of the wealth, the state would simply take ownership of the wealth, in place. An ULTRA is a ‘notional equity interest.’ The government literally takes a portion of the value of the asset; that value will be paid to the state when the asset is sold. Now, it is only a ‘notional’ stake, in the sense that no shared right of control or voting rights exists. But for those who advocate for ULTRAs, in any situation where tax agencies are authorized to tax an asset today, but cannot because there is no evaluation event, the taxpayer could be made to pay with an ULTRA rather than with cash.”

This solves all sorts of administrative problems associated with wealth taxes, but it is draconian nevertheless. Munger quotes an example of a successful, privately-held business subject to a 2% wealth tax every year in the form of an ULTRA. After 20 years, the government owns more than a third of the company’s value. That represents a substantial penalty for success! However, the incidence of such a tax might fall more on workers and customers and less on business owners. And Altman would tax corporations more heavily than in Munger’s example.

A tax on wealth essentially penalizes thrift, reduces capital accumulation, and diminishes productivity and real wages. But another fundamental reason that taxes on capital should be low is that the supply of capital is elastic. A tax on capital discourages saving and encourages capital flight. The use of avoidance schemes will proliferate, and there will be intense pressure to carve out special exemptions.

A Regressive Dimension

Another drawback of a wealth tax is its regressivity with respect to returns on capital. To see this, we can convert a tax on wealth to an equivalent income tax on returns. Here is Chris Edwardson that point:

“Suppose a person received a pretax return of 6 percent on corporate equities. An annual wealth tax of 2 percent would effectively reduce that return to 4 percent, which would be like a 33 percent income tax—and that would be on top of the current federal individual income tax, which has a top rate of 37 percent.”

… The effect is to impose lower effective tax rates on higher‐yielding assets, and vice versa. If equities produced returns of 8 percent, a 2 percent wealth tax would be like a 25 percent income tax. But if equities produced returns of 4 percent, the wealth tax would be like a 50 percent income tax. People with the lowest returns would get hit with the highest tax rates, and even people losing money would have to pay the wealth tax.“

Edwards notes the extreme inefficiency of wealth taxes demonstrated by the experience of a number of OECD countries. There are better ways to increase revenue and the progressivity of taxes. The best alternative is a tax on consumption, which rewards saving and capital accumulation, promoting higher wages and economic growth. Edwards dedicates a lengthy section of his paper to the superiority of a consumption tax.

Is a Wealth Tax Constitutional?

The constitutionality of a wealth tax is questionable as well. Steven Calabresi and David Schizer (C&S)contend that a federal wealth tax would qualify as a direct tax subject to the rule of apportionment, which would also apply to a federal tax on land. That is, under the U.S. Constitution, these kinds of taxes would have to be the same amount per capita in every state. Thus, higher tax rates would be necessary in less wealthy states.

C&S also note a major distinction between taxes on the value of wealth relative to income, excise, import, and consumption taxes. The latter are all triggered by transactions entered into voluntarily. They are avoidable in that sense, but not wealth taxes. Moreover, C&S believe the founders’ intent was to rely on direct taxes only as a backstop during wartime.

The recent Supreme Court decision in Moore v. United States created doubt as to whether the Court had set a precedent in favor of a potential wealth tax. According to earlier precedent, the Constitution forbade the “laying of taxes” on “unrealized” income or changes in wealth. However, in Moore, the Court ruled that undistributed profits from an ownership interest in a foreign business are taxable under the mandatory repatriation tax, signed into law by President Trump in 2017 as part of his tax overhaul package. But Justice Kavanaugh, who wrote the majority opinion, stated that the ruling was based on the foreign company’s status as a pass-through entity. The Wall Street Journalsays of the decision:

“Five Justices open the door to taxing unrealized gains in assets. Democrats will walk through it.”

In a brief post, Calabrisi laments Justice Ketanji Brown Jackson’s expansive view of the federal government’s taxing authority under the Sixteenth Amendment, which might well be shared by the Biden Administration. But the Wall Street Journal piece also describes Kavanaugh’s admonition regarding any expectation of a broader application of the Moore opinion:

“Justice Kavanaugh does issue a warning that ‘the Due Process Clause proscribes arbitrary attribution’ of undistributed income to shareholders. And he writes that his opinion should not ‘be read to authorize any hypothetical congressional effort to tax both an entity and its shareholders or partners on the same undistributed income realized by the entity.’”

Growth Is the Way, Not Taxes

AI growth will lead to rapid improvements in labor productivity and real wages in many occupations, despite a painful transition for some workers requiring occupational realignment and periods of unemployment and training. However, people will retain comparative advantages over AI agents in a number of existing occupations. Other workers will find that AI allows them to shift their efforts toward higher-value or even new aspects of their jobs. Along the same lines, there will be a huge variety of new occupations made possible by AI of which we’re only now catching the slightest glimpse. Michael Strain has emphasized this aspect of technological diffusion, noting that 60% of the jobs performed in 2018 did not exist in 1940. In fact, few of those “new” jobs could have been imagined in 1940.

AI entrepreneurs and AI investors will certainly capture a disproportionate share of gains from an AI revolution. Of course, they’ll have created a disproportionate share of that wealth. It might well skew the distribution of wealth in their favor, but that does not reflect negatively on the market process driving the outcome, especially because it will also give rise to widespread gains in living standards.

Altman goes wrong in proposing tax-funded redistribution of equity shares. Those taxes would slow AI development and deployment, reduce economic growth, and produce fewer new opportunities for workers. The surest way to effect a broader distribution of equity capital, and of equity in AI assets, is to encourage innovation, economic growth, and saving. Taxing capital more heavily is a very bad way to do that, whether from heavier taxes on income from capital, new taxes on unrealized gains, or (worst of all) from taxes on the value of capital, including ULTRA taxes.

Altman is right, however, to bemoan the narrow ownership of capital. As I mentioned above, he’s also on-target in saying that most people do not fully appreciate the benefits of thrift and the miracle of compounding. That represents both a failure of education and our calamitously high rate of time preference as a society. Perhaps the former can be fixed! However, thrift is a decision best left in private hands, especially to the extent that AI stimulates rapid income growth.

Killer Regulation

Altman also supports AI regulation, and I’ll cut him some slack by noting that his motives might not be of the usual rent-seeking variety. Maybe. Anyway, he’ll get some form of his wish, as legislators are scrambling to draft a “roadmap” for regulating AI. Some are calling for billions of federal outlays to “support” AI development, with a likely and ill-advised effort to “direct” that development as well. That is hardly necessary given the level of private investment AI is already attracting. Other “roadmap” proposals call for export controls on AI and protections for the film and recording industries.

These proposals are fueled by fears about AI, which run the gamut from widespread unemployment to existential risks to humanity. Considerable attention has been devoted to the alignment of AI agents with human interests and well being, but this has emerged largely within the AI development community itself. There are many alignment optimists, however, and still others who decry any race between tech giants to bring superhuman generative AI to market.

The Biden Administration stepped in last fall with an executive order on AI under emergency powers established by the Defense Production Act. The order ranges more broadly than national defense might necessitate, and it could have damaging consequences. Much of the order is redundant with respect to practices already followed by AI developers. It requires federal oversight over all so-called “foundation models” (e.g., ChatGPT), including safety tests and other “critical information”. These requirements are to be followed by the establishment of additional federal safety standards. This will almost certainly hamstring investment and development of AI, especially by smaller competitors.

Patrick Hedger discusses the destructive consequences of attempts to level the competitive AI playing field via regulation and antitrust actions. Traditionally, regulation tends to entrench large players who can best afford heavy compliance costs and influence regulatory decisions. Antitrust actions also impose huge costs on firms and can result in diminished value for investors in AI start-ups that might otherwise thrive as takeover targets.

Conclusion

Sam Altman’s vision of funding a redistribution of equity capital via taxes on wealth suffers from serious flaws. For one thing, it seems to view AI as a sort of exogenous boon to productivity, wholly independent of investment incentives. Taxing capital would inhibit investment in new capital (and in AI), diminish growth, and thwart the very goal of broad ownership Altman wishes to promote. Any effort to tax capital at a global level (which Altman supports) is probably doomed to failure, and that’s a good thing. The burden of taxes on capital at the corporate level would largely be shifted to workers and consumers, pushing real wages down and prices up relative to market outcomes.

Low taxes on income and especially on capital, together with light regulation, promote saving, capital investment, economic growth, higher real wages, and lower prices. For AI, like all capital investment, public policy should focus on encouraging “aligned” development and deployment of AI assets. A consumption tax would be far more efficient than wealth or capital taxes in that respect, and more effective in generating revenue. Policies that promote growth are the best prescription for broadening the distribution of capital ownership.

As of February 2026, I’m adding this short preamble to a few older posts on the subject of AI and future prospects for human labor. In the original post below (and a few others), I overstated the case that the law of comparative advantage would assure a continued role for humans in production. I still think the case is strong, mind you, but now I’m convinced that the outcome depends on elasticities of input substitution and how those elasticities might shift given the advent of AI-augmented capital. You can read my most recent thoughts on the matter here.

____________________________________________

I was happy to see Noah Smith’s recent post on the graces of comparative advantage and the way it should mediate the long-run impact of AI on job prospects for humans. However, I’m embarrassed to have missed his post when it was published in March (and I also missed a New York Timespiece about Smith’s position).

I said much the same thing as Smith in my post two weeks ago about the persistence of a human comparative advantage, but I wondered why the argument hadn’t been made prominently by economists.I discussed it myself about seven years ago. But alas, I didn’t see Smith’s post until last week!

I highly recommend it, though I quibble on one or two issues. Primarily, I think Smith qualifies his position based on a faulty historical comparison. Later, he doubles back to offer a kind of guarantee after all. Relatedly, I think Smith mischaracterizes the impact of energy costs on comparative advantages, and more generally the impact of the resources necessary to support a human population.

We Specialize Because…

Smith encapsulates the underlying phenomenon that will provide jobs for humans in a world of high automation and generative AI: “… everyone — every single person, every single AI, everyone — always has a comparative advantage at something!” He tells technologists “… it’s very possible that regular humans will have plentiful, high-paying jobs in the age of AI dominance — often doing much the same kind of work that they’re doing right now …”

… often, but probably transformed in fundamental ways by AI, and also doing many other new kinds of work that can’t be foreseen at present. Tyler Cowen believes themost important macro effects of AI will be from “new” outputs, not improvements in existing outputs. That emphasis doesn’t necessarily conflict with Smith’s narrative, but again, Smith thinks people will do many of the same jobs as today in a world with advanced AI.

Smith’s Non-Guarantee

Smith hedges, however, in a section of his post entitled “‘Possible’ doesn’t mean guaranteed”. This despite his later assertion that superabundance would not eliminate jobs for humans. That might seem like a separate issue, but it’s strongly intertwined with the declining AI cost argument at the basis of his hedge. More on that below.

On his reluctance to “guarantee” that humans will have jobs in an AI world, Smith links to a 2013 Tyler Cowen post on“Why the theory of comparative advantage is overrated”. For example, Cowen says, why do we ever observe long-term unemployment if comparative advantage rules the day? Of course there are many reasons why we observe departures from the predicted results of comparative advantage. Incentives are often manipulated by governments and people differ drastically in their capacities and motivation.

But Cowen cites a theoretical weakness of comparative advantage: that inputs are substitutable (or complementary) by degrees, and the degree might change under different market conditions. An implication is that “comparative advantages are endogenous to trade”, specialization, and prices. Fair enough, but one could say the same thing about any supply curve. And if equilibria exist in input markets it means these endogenous forces tend toward comparative advantages and specializations balancing the costs and benefits of production and trade. These processes might be constrained by various frictions and interventions, and their dynamics might be complex and lengthy, but that doesn’t invalidate their role in establishing specializations and trade.

The Glue Factory

Smith concerns himself mainly with another one of Cowen’s “failings of comparative advantage”: “They do indeed send horses to the glue factory, so to speak.” The gist here is that when a new technology, motorized transportation, displaced draft horses, there was no “wage” low enough to save the jobs performed by horses. Smith says horses were too costly to support (feed, stables, etc…), so their comparative advantage at “pulling things” was essentially worthless.

True, but comparing outmoded draft horses to humans in a world of AI is not quite appropriate. First, feedstock to a “glue factory” better not be an alternative use for humans whose comparative advantages become worthless. We’ll have to leave that question as an imperative for the alignment community.

Second, horses do not have versatile skill sets, so the comparison here is inapt due to their lack of alternative uses as capital assets. Yes, horses can offer other services (racing, riding, nostalgic carriage rides), but sadly, the vast bulk of work horses were “one-trick ponies”. Most draft horses probably had an opportunity cost of less than zero, given the aforementioned costs of supporting them. And it should be obvious that a single-use input has a comparative advantage only in its single use, and only when that use happens to be the state-of-the-art, or at least opportunity-cost competitive.

The drivers, on the other hand, had alternatives, and saw their comparative advantage in horse-driving occupations plunge with the advent of motorized transport. With time it’s certain many of them found new jobs, perhaps some went on to drive motorized vehicles. The point is that humans have alternatives, the number depending only on their ability to learn a crafts and perhaps move to a new location. Thus, as Smith says, “… everyone — every single person, every single AI, everyone — always has a comparative advantage at something!” But not draft horses in a motorized world, and not square pegs in a world of round holes.

AI Producer Constraints

That brings us to the topic of what Smith calls producer-specific constraints, which place limits on the amount and scope of an input’s productivity. For example, in my last post, there was only one super-talented Harvey Specter, so he’s unlikely to replace you and keep doing his own job. Thus, time is a major constraint. For Harvey or anyone else, the time constraint affects the slope of the tradeoff (and opportunity costs) between one type of specialization versus another.

Draft horses operated under the constraints of land, stable, and feed requirements, which can all be viewed as long-run variable costs. The alternative use for horses at the glue factory did not have those costs.

Humans reliant on wages must feed and house themselves, so those costs also represent constraints, but they probably don’t change the shape of the tradeoff between one occupation and another. That is, they probably do not alter human comparative advantages. Granted, some occupations come with strong expectations among associates or clients regarding an individual’s lifestyle, but this usually represents much more than basic life support. In the other end of the spectrum, displaced workers will take actions along various margins: minimize living costs; rely on savings; avail themselves of charity or any social safety net as might exist; and ultimately they must find new positions at which they maintain comparative advantages.

The Compute Constraint

In the case of AI agents, the key constraint cited by Smith is “compute”, or computer resources like CPUs or GPUs. Advancements in compute have driven the AI revolution, allowing AI models to train on increasingly large data sets and levels of compute. In fact, by one measure of compute, floating point operations per second (FLOPs), compute has become drastically cheaper, with FLOPs per dollar almost doubling every two years. Perhaps I misunderstand him, but Smith seems to assert the opposite: that compute costs are increasing. Regardless, compute is scarce, and will always be scarce because advancements in AI will require vast increases in training. This author explains that while lower compute costs will be more than offset by exponential increases in training requirements, there nevertheless will be an increasing trend in capabilities per compute.

Every AI agent will require compute, and while advancements are enabling explosive growth in AI capabilities, scarce compute places constraints on the kinds of AI development and deployment that some see as a threat to human jobs. In other words, compute scarcity can change the shape of the tradeoffs between various AI applications and thus, comparative advantages.

The Energy Constraint

Another producer constraint on AI is energy. Certainly highly complex applications, perhaps requiring greater training, physical dexterity, manipulation of materials, and judgement, will require a greater compute and energy tradeoff against simpler applications. Smith, however, at one point dismisses energy as a differential producer constraint because “… humans also take energy to run.” That is a reference to absolute energy requirements across inputs (AI vs. human), not differential requirements for an input across different outputs. Only the latter impinge on tradeoffs or opportunity costs facing an inputs. Then, the input having the lowest opportunity cost for a particular output has a comparative advantage for that output. However, it’s not always clear whether an energy tradeoff across outputs for humans will be more or less skewed than for AI, so this might or might not influence a human comparative advantage.

Later, however, Smith speculates that AI might bid up the cost of energy so high that “humans would indeed be immiserated en masse.” That position seems inconsistent. In fact, if AI energy demands are so intensive, it’s more likely to dampen the growth in demand for AI agents as well as increase the human comparative advantage because the most energy-intensive AI applications will be disadvantaged.

And again, there is Smith’s caution regarding the energy required for human life support. Is that a valid long-run variable cost associated with comparative advantages possessed by humans? It’s not wrong to include fertility decisions in the long-run aggregate human labor supply function in some fashion, but it doesn’t imply that energy requirements will eliminate comparative advantages. Those will still exist.

Hype, Or Hyper-Growth?

AI has come a long way over the past two years, and while its prospective impact strikes some as hyped thus far, it has the potential to bring vast gains across a number of fields within just a few years. According to this study, explosive economic growth on the order of 30% annually is a real possibility within decades, as generative AI is embedded throughout the economy. “Unprecedented” is an understatement for that kind of expansive growth. Dylan Matthews in Vox surveys the arguments as to how AI will lead to super-exponential economic growth. This is the kind of scenario that would give rise to superabundance.

I noted above that Smith, despite his unwillingness to guarantee that human jobs will exist in a world of generative AI, asserts (in an update) at the bottom of his post that a superabundance of AI (and abundance generally) would not threaten human comparative advantages. This superabundance is a case of decreasing costs of compute and AI deployment. Here Smith says:

“The reason is that the more abundant AI gets, the more value society produces. The more value society produces, the more demand for AI goes up. The more demand goes up, the greater the opportunity cost of using AI for anything other than its most productive use.

“As long as you have to make a choice of where to allocate the AI, it doesn’t matter how much AI there is. A world where AI can do anything, and where there’s massively huge amounts of AI in the world, is a world that’s rich and prosperous to a degree that we can barely imagine. And all that fabulous prosperity has to get spent on something. That spending will drive up the price of AI’s most productive uses. That increased price, in turn, makes it uneconomical to use AI for its least productive uses, even if it’s far better than humans at its least productive uses.

“Simply put, AI’s opportunity cost does not go to zero when AI’s resource costs get astronomically cheap. AI’s opportunity cost continues to scale up and up and up, without limit, as AI produces more and more value.”

This seems as if Smith is backing off his earlier hedge. Some of that spending will be in the form of fabulous investment projects of the kinds I mentioned in my post, and smaller ones as well, all enabled by AI. But the key point is that comparative advantages will not go away, and that means human inputs will continue to be economically useful.

I referenced Andrew Mayne in my last post. He contends that the income growth made possible by AI will ensure that plenty of jobs are available for humans. He mentions comparative advantage in passing, but he centers his argument around applications in which human workers and AI will be strong complements in production, as will sometimes be the case.

A New Age of Worry

The economic success of AI is subject to a number of contingencies. Most important is that AI alignment issues are adequately addressed. That is, the “self-interest” of any agentic AI must align with the interests of human welfare. Do no harm!

The difficulty of universal alignment is illustrated by the inevitability of competition among national governments for AI supremacy, especially in the area of AI-enabled weaponry and espionage. The national security implications are staggering.

A couple of Smith‘s biggest concerns are the social costs of adjusting to the economic disruptions AI is sure to bring, as well as its implications for inequality. Humans will still have comparative advantages, but there will be massive changes in the labor market and transitions that are likely to involve spells of unemployment and interruptions to incomes for some. The speed and strength of the AI revolution may well create social upheaval. That will create incentives for politicians to restrain the development and adoption of AI, and indeed, we already see the stirrings of that today.

Finally, Smith worries that the transition to AI will bring massive gains in wealth to the owners of AI assets, while workers with few skills are likely to languish. I’m not sure that’s consistent with his optimism regarding income growth under AI, and inequality matters much less when incomes are rising generally. Still, the concern is worthy of a more detailed discussion, which I’ll defer to a later post.

As of February 2026, I’m adding this short preamble to a few older posts on the subject of AI and future prospects for human labor. In the original post below (and a few others), I overstated the case that the law of comparative advantage would assure a continued role for humans in production. I still think the case is strong, mind you, but now I’m convinced that the outcome depends on elasticities of input substitution and how those elasticities might shift given the advent of AI-augmented capital. You can read my most recent thoughts on the matter here.

___________________________________________

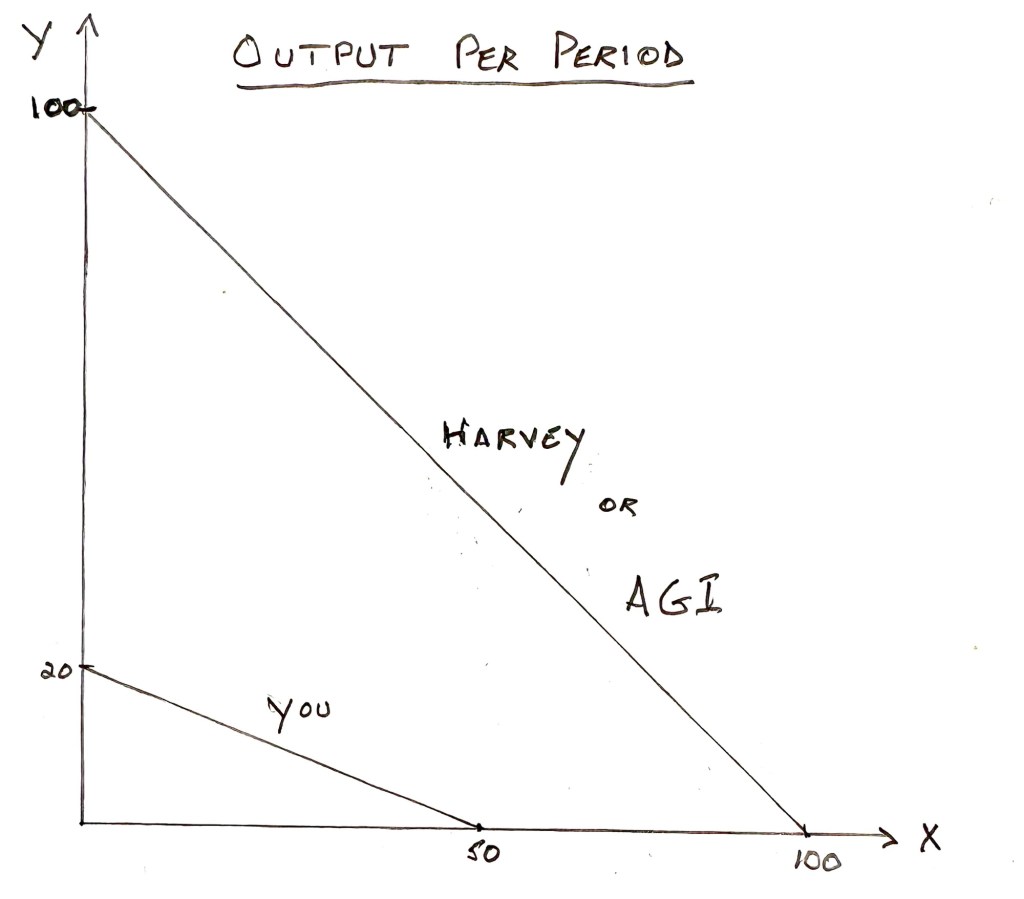

You might know someone so smart and multi-talented that they are objectively better at everything than you. Let’s call him Harvey Specter. Harvey’s prospects on the labor market are very good. Economists would say he has an absolute advantage over you in every single pursuit! What a bummer! But obviously that doesn’t mean Harvey can or should do everything, while you do nothing.

Fears of Human Obsolescence

That’s the very situation many think awaits workers with the advent of artificial general intelligence (AGI), and especially with the marriage of AGI and advanced robotics (also see here). Any job a human can do, AGI or AGI robots of various kinds will be able to do better, faster, and in far greater quantity. The humanoid AGI robots will be like your talented acquaintance Harvey, but exponentiated. They won’t need much “sleep” or downtime, and treating wear and tear on their “health” will be a simple matter of replacing components. AGI and its robotic manifestations will have an absolute advantage in every possible endeavor.

But even with the existence of super-human AGI robots, I claim that work will be available to you if you want or need it. You won’t face the same set of pre-AGI opportunities, but there will be many opportunities for humans nonetheless. How can that be if AGI robots can do everything better? Won’t they be equipped to meet all of our material needs and wants?

Specter of the Super Productive

Let’s return to the example of you and Harvey, your uber-talented acquaintance. You’ll each have an area of specialization, but on what basis? Harvey has his pick of very lucrative and stimulating opportunities. You, however, are limited to a less dazzling array of prospects. There might be some overlap, and hard work or luck can make up for large differences, but chances are you’ll specialize in something that requires less talent than Harvey. You might wind up in the same profession, but Harvey will be a star.

Where will you end up? The answer is you and Harvey will find your respective areas of specialization based on comparative advantages, not absolute advantages. Relative opportunity cost is the key here, or its inverse: how much do you expect to gain from a certain area of specialization relative to the rewards you must forego.

For example, Harvey doesn’t sacrifice much by shunning less challenging areas of specialization. That is, he faces a low opportunity cost, while his chosen area offers great rewards for his talent.

You, on the other hand, might not have much to gain in Harvey’s line of work, if you can get it. You might be a flop if you do! Realistically, you forego very little if you instead pursue more achievable success in a less daunting area. You’ll be better off choosing an option for which your relative gains are highest, or said differently, where your relative opportunity cost is low.

A Quick Illustration

If you’re unwilling to slog through a simple numerical example, skip this section and the graph below. The graph was produced the old fashioned way: by a human being with a pencil, paper, ruler, and smart phone camera.

Here goes: Harvey can produce up to 100 units of X per period or 100 units of Y, or some linear combination of the two. Harvey’s opportunity costs are constant along this tradeoff between X and Y because it’s a straight line. It costs him one unit of Y output to produce every additional unit of X, and vice versa.

You, on the other hand, cannot produce X or Y as well as Harvey in an absolute sense. At most, you can produce up to 50 units of X per period, 20 units of Y, or some combination of the two along your own constant cost (straight line) tradeoff. You sacrifice 5/2 = 2.5 units of X to produce each unit of Y, so Harvey has the lower opportunity cost and a comparative advantage for Y. But it only costs you 2/5 = 0.4 units of Y to produce each additional unit of X, so you have a comparative advantage over Harvey in X production.

Reciprocal Advantages

In the end, you and Harvey specialize in the respective areas for which each has their lowest relative opportunity cost and a comparative advantage. If he has a comparative advantage in one area of production, and unless your respective tradeoffs have identical slopes (unlikely), the reciprocal nature of opportunity costs dictates that you have a comparative advantage in the other area of production.

Obviously, Harvey’s formidable absolute advantage over you in everything doesn’t impinge on these choices. In the real world, of course, comparative advantages play out across many dimensions of output, but the principle is the same. And once we specialize, we can trade with one another to mutual advantage.

No Such Thing As a Free AGI Robot

That brings us back to AGI and AGI robots. Like Harvey, they might well have an absolute advantage in every area of specialization, or they can learn quickly to achieve such an advantage, but that doesn’t mean they should do everything!

Just as in times preceding earlier technological breakthroughs, we cannot even imagine the types of jobs that will dominate the human and AGI work forces in the future. We already see complementarity between humans and AGI in many applications. AGI makes those workers much more productive, which leads to higher wages.

However, substitution of AGIs for human labor is a dominant theme of the many AGI “harm” narratives. In fact, substitution is already a reality in many occupations, like coding, and substitution is likely to broaden and intensify as the marriage of AGI and robotics gains speed. But that will occur only in industries for which the relative opportunity costs of AGIs, including all of the ancillary resources needed to produce them, are favorable. Among other things, AGI will require a gigantic expansion in energy production and infrastructure, which necessitates a massive exploitation of resources. Relative opportunity costs in the use of these resources will not always favor the dominance of AGIs in production. Like Harvey, AGIs and their ancillary resources cannot do everything because they cannot have comparative advantages without reciprocal comparative disadvantages.

Super-Abundance vs. Scarcity

Some might insist that AGIs will lead to such great prosperity that humans will no longer need to work. All of our material wants will be met in a new age of super-abundance. Despite the foregoing, that might suggest to some that AGIs will do everything! But here I make another claim: our future demands on resources will not be satisfied by whatever abundance AGIs make possible. We will still want to do more, whether we choose to construct fusion reactors, megastructures in space (like Dyson spheres or ring worlds), terraform Mars, undertake interstellar travel, perfect asteroid defense, battle disease, extend longevity, or improve our lives in ways now imagined or unimagined.

As a result, scarcity will remain a major force. To that extent, resources will have competing uses, they will face opportunity costs, and they will have comparative advantages vis a vis alternative uses to which they can be put. Scarcity is a reality that governs opportunity costs, and that means humans will always have roles to play in production.

Concluding Remarks

I wrote about human comparative advantages once before, about seven years ago. I think I was groping along the right path. The only other article I’ve seen to explicitly mention a comparative advantage of human labor vs. AGIs in the correct context is by Andrew Mayne in the most recent issue of Reason Magazine. It’s almost a passing reference, but it deserves more because it is foundational.

Harvey Specter shouldn’t occupy his scarce time performing tasks that compromise his ability to deliver his most rewarding services. Likewise, before long it will become apparent that highly productive AGI assets, and the resources required to build and operate them, should not be tied up in activities that humans can perform at lesser sacrifice. That’s a long way of saying that humans will still have productive roles to play, even when AGI achieves an absolute advantage in everything. Some of the roles played by humans will be complimentary to AGIs in production, but human labor will also be valuable as a substitute for AGI assets in other applications. As long as AGI assets have any comparative advantages, humans will have reciprocal comparative advantages as well.

Housing costs are taking a toll on many Americans. Home prices have risen about 47% cumulatively since 2020, while higher mortgage rates have compounded the difficulties faced by potential homebuyers. Meanwhile, rents are up about 23% over the same period. There just aren’t enough homes available, and the primary cause is an extensive set of regulatory obstacles to increasing the supply of homes.

High housing costs are often blamed on various manifestations of greed. Renters tend to resent their landlords, while those suffering from housing sticker-shock sometimes cast paranoid blame on people with second homes, investor properties, Airbnb rentals, and even residential developers, as if those seeking to build new housing are at the root of the problem.

Quite the contrary: we have an acute shortage of housing. The chart below shows how home vacancy rates have fallen to a level that can’t accommodate the normal frictions associated with housing turnover.

Doubts about this shortfall might owe to confusion over the meaning of one statistic: our high current level of housing units per capita. It does not indicate a plentiful stock of housing, as some assume. Alex Tabarrok, in commenting favorably on a lengthier post by Kevin Erdman, offers a simple example demonstrating that units per capita is not a reliable guide to the adequacy of housing supply:

“Suppose we have 100 homes and 100 families, each with 2 parents and 2 kids. Thus, there are 100 homes, 400 people and 0.25 homes per capita. Now the kids grow up, get married, and want homes of their own but they have fewer kids of their own, none for simplicity. Imagine that supply increases substantially, say to 150 homes. The number of homes per capita goes up to 150/400 (.375), an all time high! Supply-side skeptics are right about the numbers, wrong about the meaning. The reality is that the demand for homes has increased to 200 but supply has increased to just 150 leading to soaring prices.”

Fewer kids have led to more homes per capita even as we suffer from a shortage of housing. In the long run, lower fertility might make it easier for housing supply to catch up with demand, but not if government continues to hamstring housing construction. Only new construction can rectify this shortfall.

That’s the message of Bryan Caplan’s “Build Baby, Build!”. Caplan has been a prominent advocate of eliminating obstacles to the construction of new housing. His book is rather unique in its contribution to economic literature because it tells the story of counterproductive housing policy in the form of a “graphic novel”, which is to say an elaborate comic book. Caplan appears in the book as protagonist, teacher and persistent gadfly.

Government obstructs additions to the supply of housing in a variety of ways: rent controls, zoning laws, density restrictions, height limits, environmental rules, and compliance paperwork. And very often these interventions are supported by existing occupants and even owners of existing homes as a matter of NIMBYism. Construction of new homes, the sure answer to the problem of an inadequate supply of housing, is actively resisted. These limitations have widespread implications for the health of the economy.

As Caplan points out, the scarcity and expense of housing limits mobility, so workers are often unable to exploit opportunities that require a move, particularly to areas of rapid growth. This makes it difficult for the labor market to adjust to negative shocks or long-term decline that might displace workers in specific locales. The mobility of resources is key to well-functioning economy, but our policies fail miserably on this count.

Rent control is an insidious policy option usually favored in dense urban areas by current renters as well as politicians seeking a visible and easy “fix” to rising rental rates. The problem is obvious: rent control destroys incentives to improve or even maintain properties. Depending on specific rules, it might even discourage development of new rental units. The result is a slow decay of the existing housing stock.

Zoning laws are an old tool of NIMBYism. The objective is to keep multifamily housing (or certain kinds of commercial development) safely away from single-family neighborhoods, or to prevent developments with relatively small lot sizes. There is also agricultural zoning, which can prevent new development along urban peripheries. It’s not difficult to understand how restrictive zoning causes rents and housing prices to escalate.

Similarly, density limits, height restrictions, burdensome filing requirements, and environmental rules all work to limit the supply of new homes.

As if crushing the supply side wasn’t enough, housing costs will come under pressure from the demand side as the Biden Administration pushes new home buying subsidies. They propose tax credits of $400 a month (at least while mortgage rates remain elevated) and an end to title insurance fees on government-backed mortgages. This would drive prices higher still. The Administration also threatens to prosecute landlords who “collude” in utilizing third-party algorithms for information in establishing rental rates. Finally, Biden proposes to dedicate billions to the construction of affordable housing, but the history of affordable housing initiatives and building subsidies is one of drastically inflated costs. This is unlikely to differ in that regard.

As wrongheaded as it is, the fact that the public is often favorably disposed to so much housing regulation is easy to understand. Rent controls prevent increases in rents to existing tenants, an easily “seen” benefit. The deleterious long-term consequences on the stock of housing are “unseen”, in the language of Frederic Bastiat.

As for zoning, homeowners are resistant to the construction of nearby “low-value” units for a variety of reasons, some aesthetic and some practical, like maintaining home values or preventing excessive traffic. “Keeping the riffraff out” is undoubtedly at play as well.

This resistance extends well beyond the limits of enforcing private property rights. It is pure rent seeking behavior in the public sphere for private benefit. Politicians and government officials tend to view the motives behind zoning as sensible, however, despite the long-term consequences of strict zoning for housing supply. Similarly, environmental restrictions sound well and good, but they too have their “unseen” negative consequences.

Most puzzling is the animus with which so many regard private residential developers, who generally build what people want: low-density suburban enclaves. Developers do it for profit, but this alienates voters who are ignorant of the economic role of profit. As in any other pursuit, profit creates a basic incentive for development activity, and to provide the kinds of homes and neighborhood amenities demanded by consumers, and to do so efficiently.

On the other hand, sprawling development inflicts external costs on incumbent residents due to added congestion, and developers and their home buyers benefit from the provision of roads that are free to users. The solution is to internalize the cost of building roads by pricing their use. Homebuyers would then weigh the value of buying in a particular area against the full marginal cost, including road use, while helping to defray the cost of maintenance and upgrades to roads and other infrastructure.

Our housing policies restrict the actions of landlords, developers, and ultimately consumers of housing. The misallocations of resources occur every time a tenant or homeowner feels they can’t afford to move in response to changing circumstances. Here is Veronique de Rugy, in an article inspired by Ryan Bourne’s “The War on Prices”, on the constraints imposed on individuals by one form of misguided intervention (my bracketed additions):

“Prices and wages [and housing rents] set on market dynamics reflect underlying economic realities and then send out a signal for help. Price [rent] controls only mask these realities, which inevitably worsens the economy’s ability to respond with what ordinary consumers and workers need.“

But our housing problem is not solely caused by interference with the price mechanism. Rather, excessive regulation of rents and a panoply of other details of the legal environment for housing have led to our current shortfall. The lesson is deregulate, and to let developers build (and rehabilitate) the housing that people need.

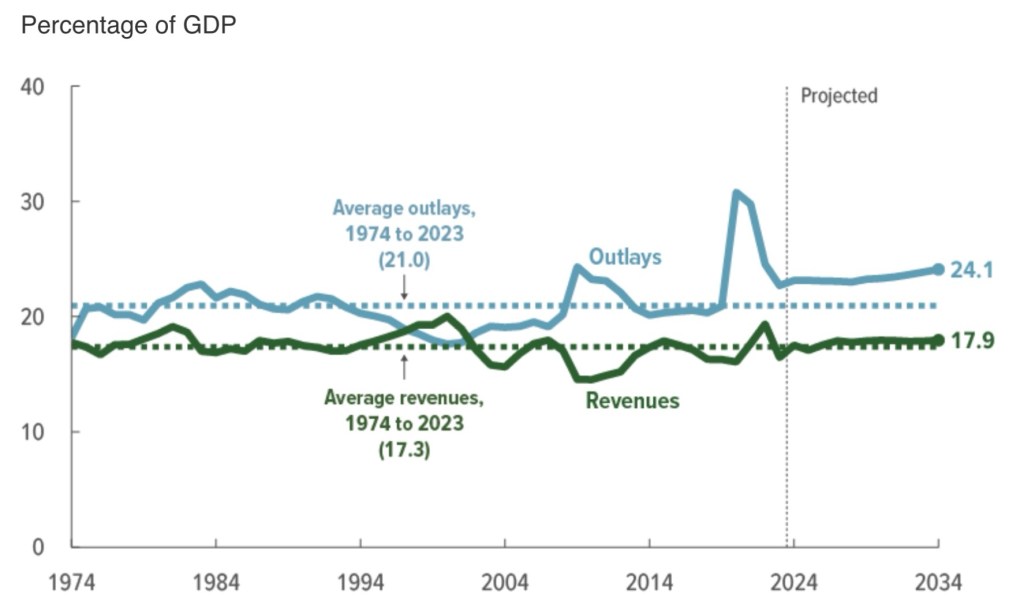

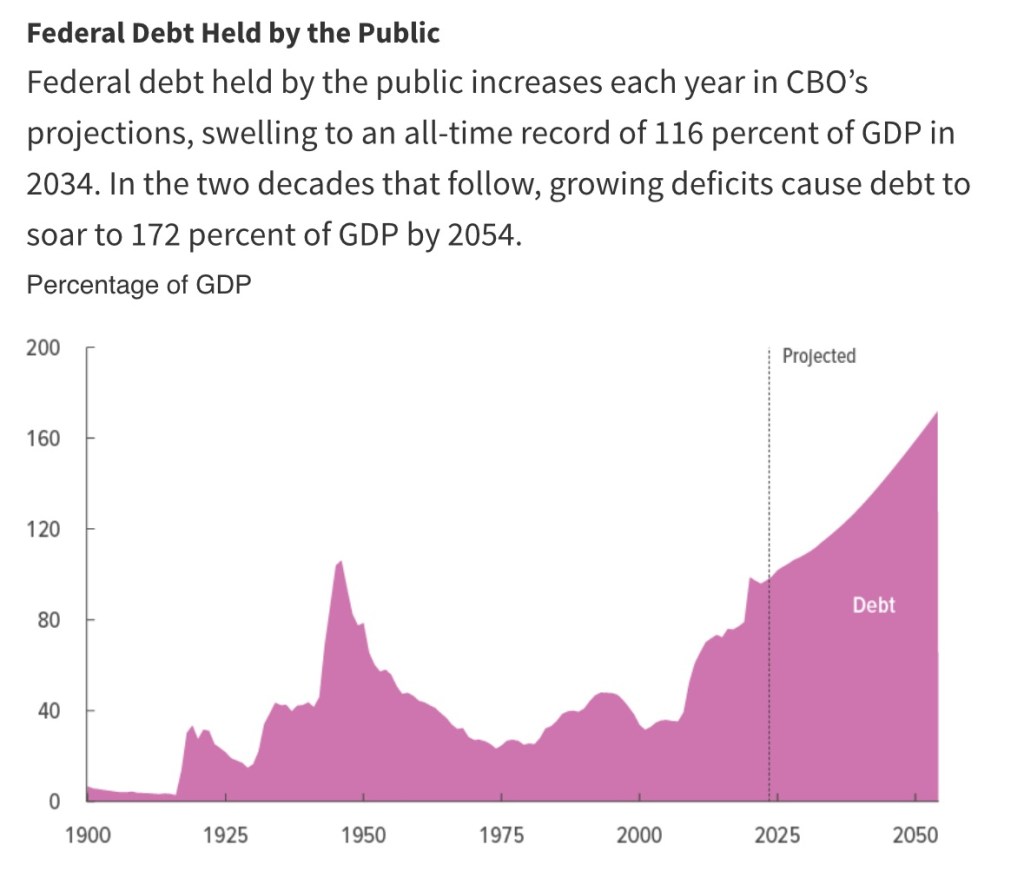

The chart above makes a convincing case that we have a spending problem at the federal level. Really, we’ve had a spending problem for a long time. But at least tax revenue today remains reasonably well-aligned with its 50-year historical average as a share of GDP. Not spending. Even larger deficits opened up during the pandemic and they haven’t returned to pre-pandemic levels.

We’ve seen Joe Biden break spending records. His initiatives, often with questionable merit, have included the $1.8 trillion American Rescue Plan and the nearly $0.8 trillion Infrastructure Investment and Jobs Act, along with several other significant spending initiatives such as the Promise to Address Comprehensive Toxics Act and the subsidy-laden CHIPS Act. Meanwhile, emergency spending has become a regular occurrence on Biden’s watch. More recently, he’s made repeated efforts to forgive massive amounts of student loans despite the Supreme Court’s clear ruling that such gifts are unconstitutional.

Indeed, while Biden keeps pretty busy spinning tales of his days driving an 18-wheeler, cannibals devouring his Uncle Bosie Finnegan, his upbringing in black churches, synagogues, or in the Puerto Rican community, he still finds time to dream up ways for the government to spend money it doesn’t have. Or his kindly puppeteers do.

Biden’s New Budget

Eric Boehm expressed wonderment at Biden’s fiscal 2025 budget not long after its release in March. He was also mystified by the gall it took to produce a “fact sheet” in which the White House congratulated itself on fiscal responsibility. That’s how this Administration characterizes deficits projected at $16 trillion over the next ten years. No joke!

Furthermore, the Administration says the record spending will be “paid for”. Well, yes, with tax increases and lots of borrowing! There are a great many fabulist claims made by the White House about the budget. This link from the Office of Management and Budget includes a handy list of propaganda sheets they’ve managed to produce on the virtues of their proposal.

The Congressional Budget Office (CBO) projects ten-year deficits under current law that are $3 trillion higher than Biden’s proposed budget. That’s the basis of the White House’s boast of fiscal restraint. But the difference is basically paid for with a couple of accounting tricks (see below). More charitably, one could say it’s paid for with higher taxes, aided by the assumption of slightly faster economic growth. The latter will be a good trick while undercutting incentives and wages with a big boost to the corporate tax rate.

The revenue projected by the While House from those taxes does not come anywhere close to eliminating the gap shown in the CBO’s chart above. Federal spending under Biden’s budget grows at about 4% annually, just a bit slower than nominal GDP. Thus, the federal share of GDP remains roughly constant and only slightly higher than the CBO’s current projection for 2034. Nevertheless, spending relative to GDP would continue at an historically high rate. Over the next decade, it would average more than 3% higher than its 50-year average. That would be about $1.3 trillion in 2034!

Meanwhile, the ratio of tax revenue to GDP under Biden’s proposal, as they project it, would average slightly higher than its 50-year average, reaching a full percentage point above by 2034 (and higher than the CBO baseline). That’s probably optimistic.

There is little real effort in this budget to reduce federal deficits, with Treasury borrowing rates now near 15-year highs. Interest expense has grown to an alarming share of spending. In fact, it’s expected to exceed spending on defense in 2024! Perhaps not coincidentally, the White House assumes a greater decline in interest rates than CBO over the next 10 years.

Treats or Tricks?

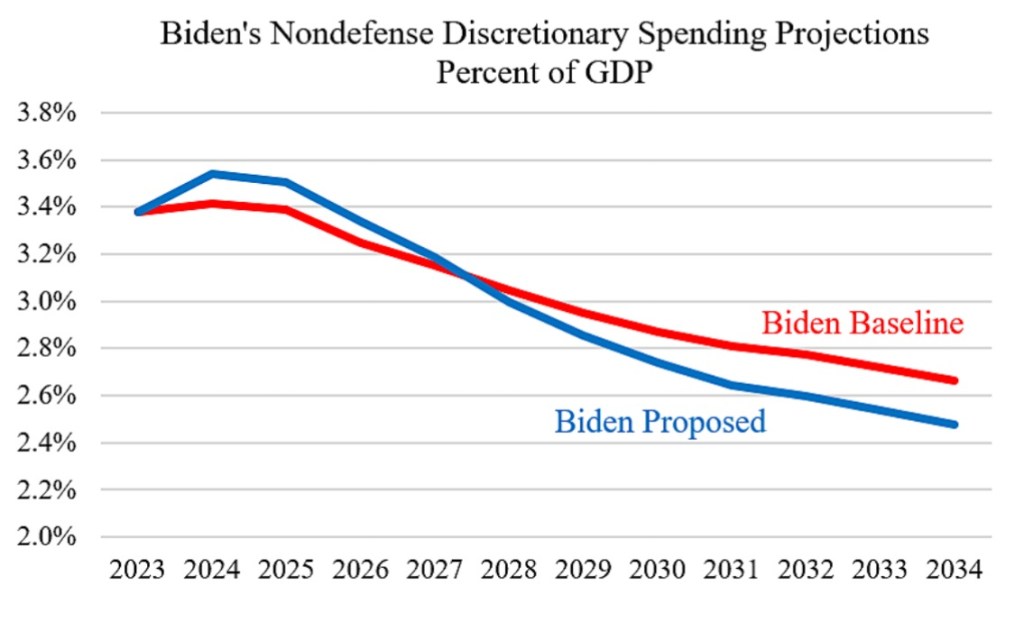

The situation is likely worse than the White House depicts, given that its budget incorporates assumptions that look generous to their claim of fiscal restraint. First, they frontload nondefense discretionary spending, allowing Biden to make extravagant promises for the near-term while pushing off steep declines in budget commitments to the out-years. The sharp reductions in this category of spending pares more than $2 trillion from the 10-year deficit. From the link above:

Biden also proposes to restore the expanded the child tax credit — for one year! How handy from a budget perspective: heroically call for an expanded credit (for a year) while avoiding, for the time being, the addition of a couple of trillion to the 10-year deficit.

Code Red

So where does this end? The ratio of federal debt to GDP will resume its ascent after a slight decline from the pandemic high. Here is the CBO’s projection:

The Biden budget shows a relatively stable debt to GDP ratio through 2034 due to the assumptions of slightly faster GDP growth, lower Treasury borrowing rates, and the aforementioned “fiscal restraint”. But don’t count on it!

The government’s growing dominance over real resources will have negative consequences for growth in the long-term. Purely as a fiscal matter, however, it must be paid for in one of three ways: revenue from explicit taxes, federal borrowing, or an implicit tax on the public more commonly known as the inflation tax. The last two are intimately related.

Bond investors always face at least a small measure of default risk even when lending to the U.S. Treasury. There is almost no chance the government would ever default outright by failing to pay interest or principal when due. However, investors hold an expectation that the value of their bonds will erode in real terms due to inflation. To compensate, they demand an “inflation premium” in the interest rate they earn on Treasury bonds. But an upside surprise to inflation would constitute a “soft default” on the real value of their bonds. This occurred during and after the pandemic, and it was triggered by a burgeoning federal deficit.

Brief Mechanics

John Cochrane has explained the mechanism by which acts of fiscal profligacy can be transmitted to the price of goods. The real value of outstanding federal debt cannot exceed the expected real value of future surpluses (a present value summed across positive and negative surpluses). If expected surpluses are reduced via some emergency or shock such that repayment in real terms is less likely, then the real value of government debt must fall. That means either interest rates or the price level must rise, or some combination of the two.

The Federal Reserve can prevent interest rates from rising (by purchasing bonds and increasing the money supply), but that leaves a higher price level as the only way the real value of debt can come into line. In other words, an unexpected increase in the path of federal deficits would be financed by money printing and an inflation tax. The incidence of this unexpected “implicit” tax falls not only to bondholders, but also on the public at large, who suffer an unexpected decline in the purchasing power of their nominal assets and incomes. This in turn tends to free-up real resources for government absorption.

Government Debt Is Risky

It appears that investors expect the future deficits now projected by the CBO (and the White House) to be paid down someday, to some extent, by future surpluses. That might seem preposterous, but markets apparently aren’t surprised by the projected deficits. After all, fiscal policy decisions can change tremendously over the course of a few years. But it still feels like excessive optimism. Whatever the case, Cochrane cautions that the next fiscal emergency, be it a new pandemic, a war, a recession, or some other crisis, is likely to create another huge expansion in debt and a substantial increase price level. Joe Biden doesn’t seem inclined to put us in a position to deal with that risk very effectively. Unfortunately, it’s not clear that Donald Trump will either. And neither seems inclined to seriously address the insolvencies of Social Security and Medicare. If unaddressed, those mandatory obligations will become real crises over the next decade.

The current protests on college campuses across the nation bring into focus differing opinions on the limits of free speech and assembly. Particular questions seem to defy resolution. Nevertheless, there is some misunderstanding regarding the settled breadth of the First Amendment.

The protestors have acted as if they have constitutional carte blanche to gather anywhere to say anything in opposition to Israel and its war against Hamas terrorists; a subset thinks this encompasses “occupation” of any space for any duration; a still smaller subset believes this includes a right to condemn Jews, all Jews.

I strongly doubt, however, that many of the protestors truly believe their constitutional protections extend to intimidation and bullying of Jewish students attempting to go about their business on campus (scroll to a few of the articles here), destruction of property, or the use of “fighting words”, or physical attacks on Jews or other “oppressors”.

It’s well known that the Constitution does not protect “fighting words”, including threats.Furthermore,Eugene Volokh explains that there is no constitutional right to “occupy” a college campus, either public or private.

Of course, private schools are not legally bound to respect free speech or assembly rights. They can regulate activity on their private campuses in any way they see fit. Some explicitly abide the same rights as public universities, which seems reasonable for any institution dedicated to the free spirit of inquiry.

Volokh, however, cites Supreme Court precedents in which a majority held that government can prohibit camping in certain parks, for example, and that public colleges and universities can impose restrictions on campus activities:

“There is no First Amendment right to camp out in any university, public or private. Indeed, there is no First Amendment right to camp out even in public parks (see Clark v. CCNV (1984)), and the government’s power to limit the use of property used for a public university is even greater than its power as to parks (Widmar v. Vincent (1981)):

“‘A university differs in significant respects for public forums such as streets or parks or even municipal theaters. A university’s mission is education, and decisions of this Court have never denied a university’s authority to impose reasonable regulations compatible with that mission upon the use of its campus and facilities. We have not held, for example, that a campus must make all of its facilities equally available to students and nonstudents alike, or that a university must grant free access to all of its grounds or buildings.’

“Likewise, if UC Berkeley had held a law student party in the law school building rather than at Dean Chemerinsky’s house, it could have stopped students from using the party as an occasion to orate to the audience (especially with their own sound amplification devices, which the student brought to Chemerinsky’s house). See Spears v. Arizona Bd. of Regents (D. Ariz. 2019)(upholding public university’s right to stop people from speaking with sound amplification at an on-campus book fair).“

Volokh also notes, however, that public universities cannot restrict mere “offensive” expression, which would include certain antisemitic statements or evenswastikas (for example), as long as the expression falls short of “fighting words” or explicit threats. Do calls for the “extermination of Jews” qualify as fighting words? That deserves a resounding yes. It’s clearly hate speech, and it’s exactly the sort of expression that might be deemed so offensive to counterprotestors (for example) as to constitute an immediate threat to public order.

Does the meaning of “fighting words” include such chants as “From the river to the sea…”? Some say that depends on the speaker, but that can’t provide a sound basis of distinction. It is clearly associated with calls to eliminate the state of Israel. Some believe it also implies the genocide of Jews in Israel, and Jews can’t be blamed for finding it threatening. Okay, how about “Intifada”? I doubt all of the students involved in the current protests understand the genocidal implications of these words. The agitators understand them well enough.

This is a grey area in our understanding of the First Amendment. The “River to the Sea” chant, and Intifada, seemlike fighting words to me, but they might not qualify as direct threats to anyone on campus. By comparison, the swastika is “just” a party emblem, whatever policies it stands for, and apparently the Court did not deem it a direct threat to anyone in Skokie, Illinois. The legal distinctions here feel inadequate. Still, we say the “mere” expression of offensive ideas or symbols is protected speech, provided that it does not directly threaten harm to any party.

Many libertarians, with whom I usually agree, urge tolerance of the protests and encampments, including at least cautious tolerance of the protests. The Foundation for Individual Rights and Expression (FIRE) has strenuously objected to the actions of police in Austin, Texas in dispersing demonstrators at the University of Texas. Alex Tabarrak has reposted a tweet or two apparently critical of the government’s response to protestors in Texas and at Emory University in Atlanta, though it should be noted that the economics professor who was taken down and handcuffed on video had actually hit a police officer. Michael Munger, in a variation of his “worst enemy test” of government power, says that giving campus authorities “the power to crush us, at their discretion” is probably a bad idea. But they have that power if they choose to exercise it, for better or worse. (By “us”, I don’t think Munger intended to take sides).

I’m highly skeptical of the motives and incentives of some of the “occupiers” of campus spaces, not to mention their status as students. More importantly, there is ample evidence that “fighting words” and threats against Jews have been used by many of the protesters. This violates the codes of conduct at many schools, and should not only be censured, but any student identified as guilty of this sort of hate speech should be expelled, not merely suspended. There should be severe consequences for professors choosing to participate in these protests as well.

This behavior should have long-term consequences, and that is happening at some schools. I saw the following quote from P.J. O’Rourke on Instapundit, which seems appropriate here:

“There’s only one basic human right, the right to do as you damn well please. And with it comes the only basic human duty, the duty to take the consequences.”

The kids are wearing masks for a reason, and it ain’t Covid! Now, the protestors’ demands include “amnesty” for their participation in the protests. That shouldn’t play well if you’re provably guilty of calling for the extermination of a race of people. But here’s the thing: certain institutions like Columbia University have allowed the aberrant behavior to go on with little challenge, showing that the real limits to free speech and assembly are whatever acquiescent campus administrators are willing to put up with.

Removing these encampments is more than justified on constitutional grounds at any school, public or private. The arrest of some of the more intransigent elements among the protesters may be well justified. Insulting hate speech is one thing, but eliminationist hate speech constitutes fighting words and should not be tolerated. Of course, forcibly removing the encampments is risky in terms of public safety because some of the protestors will physically challenge the police. Comparatively innocent (though naive) students might get caught up in a conflict with law enforcement, but ignorance is no defense. They should not be there. Those risks must be taken to end the “hate encampments”, which are a direct threat to the rights of others wishing only to go about their business.

This is a first for me…. The following is partly excerpted from a post of two weeks ago, but I’ve made a number of edits and additions. The original post was way too long. This is a bit shorter, and I hope it distills a key message.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Failures of industrial policies are nothing new, but the current manipulation of electric power generation by government in favor of renewable energy technologies is egregious. These interventions are a reaction to an overwrought climate crisis narrative, but they have many shortcomings and risks of their own. Chief among them is whether the power grid will be capable of meeting current and future demand for power while relying heavily on variable resources, namely wind and sunshine. The variability implies idle and drastically underutilized hours every day without any ability to call upon the assets to producewhen needed.

The variability is vividly illustrated by the chart above showing a representative daily profile of power demand versus wind and solar output. Below, with apologies to Dante, I describe the energy hellscape into which we’re being driven on the horns of irrational capital outlays. These projects would be flatly rejected by any rational investor but for the massive subsidies afforded by government.

The First Circle of Dormancy: Low Utilization

Wind and solar power assets have relatively low rates of utilization due to the intermittency of wind and sunshine.Capacity factors for wind turbines averaged almost 36% in the U.S. in 2022, while solar facilities averaged only about 24%. This compared with nuclear power at almost 93%, natural gas (66%), and coal (48%).

Despite their low rates of utilization, new wind and solar facilities are always touted at their full nameplate capacity. We hear a great deal about “additions to capacity”, which overstate the actual power-generating potential by factors of three to four times. More importantly, this also means wind and solar power costs per unit of output are often vastly understated. These assets contribute less economic value to the electric grid than more heavily utilized generating assets.

Sometimes wind and solar facilities are completely idle or dormant. Sometimes they operate at just a fraction of capacity. I will use the terms “idle” and dormant” euphemistically in what follows to mean assets operating not just at low levels of utilization, but for those prone to low utilization and also falling within the Second Circle of Dormancy.

The Second Circle of Dormancy: Non-Dispatchability

The First Circle of Dormancy might be more like a Purgatory than a Hell. That’s because relatively low average utilization of an asset could be justifiable if demand is subject to large fluctuations. This is the often case, as with assets like roads, bridges, restaurants, amusement parks, and many others. However, capital invested in wind and solar facilities is idle on an uncontrollable basis, which is more truly condemnable. Wind and solar do not provide “dispatchable” power, meaning they are not “on call” in any sense during idle or less productive periods. Not only is their power output uncontrollable, it is not entirely predictable.

Again, variable but controllable utilization allows flexibility and risk mitigation in many applications. But when utilization levels are uncontrollable, the capital in question has greatly diminished value to the power grid and to power customers relative to dispatchable sources having equivalent capacity and utilization. It’s no wonder that low utilization, variability, and non-dispatchability are underemphasized or omitted by promoters of wind and solar energy. This sort of uncontrollable down-time is a drain on real economic returns to capital.

The Third Circle of Dormancy: Transmission Infrastructure

The idleness that besets the real economic returns to wind and solar power generation extends to the transmission facilities necessary for getting power to the grid. Transmission facilities are costly, but that cost is magnified by the broad spatial distribution of wind and solar generating units. Transmission from offshore facilities is particularly complex. When wind turbines and solar panels are dormant, so are the transmission facilities needed to reach them. Thus, low utilization and the non-dispatchability of those units diminishes the value of the capital that must be committed for both power generation and its transmission.

The Fourth Circle of Dormancy: Backup Power Assets

The reliability of the grid requires that any commitment to variable wind and solar power must also include a commitment to back-up capacity. As another example, consider shipping concerns that are now experimenting with sails on cargo ships. What is the economic value of such a ship without back-up power? Can you imagine these vessels drifting in the equatorial calms for days on end? Even light winds would slow the transport of goods significantly. Idle, non–dispatchable capital, is unproductive capital.

Likewise, solar-powered signage can underperform or fail over the course of several dark, wintry days, even with battery backup. The signage is more reliable and valuable when it is backed-up by another power source. But again, idle, non-dispatchable capital is unproductive capital.

The needed provision of backup power sources represents an imposed cost of wind and solar, which is built into the cost estimates shown in a section below. But here’s another case of dormancy: some part of the capital commitment, either primary energy sources or the needed backups, will be idle regardless of wind and solar conditions… all the time. Of course, back-up power facilities should be dispatchable because they must serve an insurance function. Backup power therefore has value in preserving the stability of the grid even while completely idle. However, at best that value offsets a small part of the social loss inherent in primary reliance on variable and non-dispatchable power sources.

We can’t wholly “replace” dispatchable generating capacity with renewables without serious negative consequences. At the same time, maintaining existing dispatchable power sources as backup carries a considerable cost at the margin for wind and solar. At a minimum, it requires normal maintenance on dispatchable generators, periodic replacement of components, and an inventory of fuel. If renewables are intended to meet growth in power demand, the imposed cost is far greater because backup sources for growth would require investment in new dispatchable capacity.

The Fifth Circle of Dormancy: Outages

The pursuit of net-zero carbon emissions via wind and solar power creates uncontrollably dormant capital, which increasingly lacks adequate backup power. Providing that backup should be a priority, but it’s not.

Perhaps much worse than the cost of providing backup power sources is the risk and imposed cost of grid instability in their absence. That cost would be borne by users in the form of outages. Users are placed at increasing risk of losing power at home, at the office and factories, at stores, in transit, and at hospitals. This can occur at peak hours or under potentially dangerous circumstances like frigid or hot weather.

Outage risks include another kind of idle capital: the potential for economy-wide shutdowns across a particular region of all electrified physical capital. Not only can grid failure lead to economy-wide idle capital, but this risk transforms all capital powered by electricity into non-dispatchable productive capacity.

Reliance on wind and solar power makes backup capacity an imperative. Better still, just scuttle the wind and solar binge and provide for growth with reliable sources of power!

QuantifyingInfernal Costs

A “grid report card“ from the Mackinac Center for Public Policy gets right to the crux of the imposed-cost problem:

“… the more renewable generation facilities you build, the more it costs the system to make up for their variability, and the less value they provide to electricity markets.”

The report card uses cost estimates for Michigan from the Center of the American Experiment. Here are the report’s average costs per MWh through 2050, including the imposed costs of backup power:

—Existing coal plant: $33/MWh

—Existing gas-powered: $22

— New wind: $180

—New solar: $278

—New nuclear reactor (light water): $74

—Small modular reactor: $185

—New coal plant: $106 with carbon capture and storage (CCS)

—New natural gas: $64 with CCS

It’s should be no surprise that existing coal and gas facilities are the most cost effective. Preserve them! Of the new installations, natural gas is the least costly, followed by the light water reactor and coal. New wind and solar capacity are particularly costly.