Creative destruction takes place when inefficient producers are outcompeted by other firms, especially those brandishing new technologies. The concept, originally developed by Joseph Schumpeter in the 1940s, came to be accepted as a hallmark of market dynamics and capitalism. Successful market entrants rise to compete and eventually cripple incumbent producers who’ve grown stale in their offerings, inputs, or methods.

Creative destruction encourages long-term economic growth in several ways. First, it allows unproductive firms to fail, freeing resources to be absorbed by firms having solid growth opportunities. Second, creative destruction enables the diffusion of new technologies. Third, it motivates incumbents to improve their game, adapting to new realities in the marketplace. This is a continuous process. There are always firms that fail to keep pace with their competitors, whether old-line producers or failing risk-takers, but this is especially the case during periods of economic weakness.

Harmful Policy Menu

Attempting to prevent creative destruction via public policy is counter-productive, anti-competitive, and it impedes economic growth. Yet we constantly expend well-meaning energies to short circuit the process by attempting to promote uneconomic technologies, shield established firms from competition, and resuscitate dying firms. These efforts include industrial policies, barriers to foreign trade, excessive regulation of new technologies, selective taxation, certain bankruptcy reorganizations, and outright bailouts.

Creative destruction is a sign of flourishing competition, but it is subverted by industrial policies that subsidize politically-favored firms that otherwise would be uncompetitive. These policies create artificial advantages that waste public resources on what are often just bad ideas (see here and here).

Likewise, protectionism breeds weakness while shielding domestic producers from competition. And selective taxes, such as those on online sales, create an uneven playing field, blunting competitive forces.

Policies that encourage the survival of “zombie firms” also thwart creative destruction. These are companies with chronic losses that manage to hang on, sometimes for many years, with refinanced debt. Companies and their lenders can expend a great deal of internal effort forestalling bankruptcy. However, it’s not uncommon for zombie firms to languish for years but ultimately fail even after bankruptcy reorganizations, especially when the sole focus is on financial restructuring rather than business operations.

Government sometimes steps in to prolong the survival of struggling firms via subsidies, loan guarantees, and protracted efforts to keep interest rates low. Bailouts of various kinds have become all too common. Bailout activity creates perverse incentives with respect to risk. It also wastes resources by propping up inefficient operators, trapping resources in uses that return less to society than their opportunity costs.

Macro Maleficence

Ben Landau-Taylor makes a provocative but sensible claim in an article entitled “Industrial Greatness Requires Economic Depressions”. It’s about an unfortunate side effect of government policies intended to stabilize the economy: business failures occur with greater frequency during economic contractions, and that’s when policymakers are most apt to render aid via expansionary fiscal and monetary actions. No one likes economic downturns and unemployment, so “stimulative” policy is easy to sell politically, despite its all-too-typical failures in terms of timing and efficacy (see here and here). One intent is to support firms whose travails are revealed by a weak economy, including those relying on obsolete technologies. It might buy them survival time, but on the public dime. Ultimately, by forestalling creative destruction, these policies undermine economic growth.

Landau-Taylor emphasizes that creative destruction is not costless. Business failures and job losses are painful. And creative destruction brought on by dramatic advances can actually cause recessions or even depressions. Is that a rationale for delaying the inevitable failure of weak incumbents and impeding the broad adoption of new technologies? Our long-term well-being might dictate that we allow such transitions to take place by shunting aside interventionist temptations.

As a rationale for intervention, it’s sometimes said that we can’t regain the output lost during contractions. An appropriate riposte is that government efforts to counter recessionary forces are almost always futile. Furthermore, the lost output might be a pittance relative to the growth and permanent gains made possible by allowing creative destruction to run its course, liberating resources for better opportunities and growth.

On this point, Landau-Taylor says:

“If we want our descendants in 2125 to surpass our living standards the way we surpass our ancestors from 1925, then we will have to permit economic transformations at the scale that our ancestors did, including bankruptcies, job losses, and the cascading depressions that result. The individual pain of depressions does not have to be quite so severe as it once was. Because we are richer, we can and do spend vastly more on welfare, but this should be directed at individuals rather than at megacorporations. But there will always be some pain.“

Conclusion

Too often public policy creates obstacles to natural and healthy market processes, including creative destruction. This prevents the economy from reaching its true growth potential. Subsidies, bailouts, protectionism, and arguably macroeconomic stimulus, too often give safe harbor to struggling producers who manage to retain control over resources having more valued uses, including firms relying on obsolete and impractical technologies. Recessions typically expose firms with the weakest market prospects, but countercyclical fiscal and monetary policy may give them cover, forestalling their inevitable decline. Thus, we risk throwing good resources after bad, foregoing opportunities for growth and a more prosperous future.

Matt Yglesias tweeted on X that “the bond market does not appear to believe in DOGE”. He included a chart much like the updated one above to “prove” his point. Tyler Cowen posted a link to the tweet on Marginal Revolution, without comment … Cowen surely must know that any such conclusion is premature, especially based on the movement of Treasury yields over the past month (or more, since the market’s evaluation of the DOGE agenda preceded Trump’s inauguration).

Of course, there is a difference between “believing” in DOGE and being convinced that its efforts should have succeeded in reducing interest rates immediately amidst waves of background noise from budget and tax legislation, court challenges, Federal Reserve missteps (this time cutting rates too soon), and the direction of the economy in general.

In this case, perhaps a better way to define success for DOGE is a meaningfully negative impact on the future supply of Treasury debt. Even that would not guarantee a decline in Treasury rates, so the premise of Yglesias’ tweet is somewhat shaky to begin with. Still, all else equal, we’d expect to see some downward pressure on yields if DOGE succeeds in this sense. But we must go further by recognizing that DOGE savings could well be reallocated to other spending initiatives. Then, the savings would not translate into lower supplies of Treasury debt after all.

Certainly, the DOGE team has made progress in identifying wasteful expenditures, inefficiencies, and poor controls on spending. But even if the $55 billion of estimated savings to date is reliable, DOGE has a long way to go to reach Musk’s stated objective of $2 trillion. There are some juicy targets, but it will be tough to get there in 17 more months, when DOGE is to stand down. Still, it’s not unreasonable to think DOGE might succeed in accomplishing meaningful deficit reduction.

But if bond traders have doubts about DOGE, it’s partly because Donald Trump and Elon Musk themselves keep giving them reasons. In my view, Musk and Trump have made a major misstep in toying with the idea of using prospective DOGE savings to fund “dividend checks” of $5,000 for all Americans. These would be paid by taking 20% of the guesstimated $2 trillion of DOGE savings. Musk’s expression of interest in the idea was followed by a bit of clusterfuckery, as Musk walked back his proposal the next day even as Trump jumped on board. PLEASE Elon, don’t give the Donald any crowd-pleasing ideas! And don’t lose sight of the underlying objective to reduce the burden of government and the public debt.

Now, Trump proposes that 60% of the savings accomplished by DOGE be put toward paying for outlays in future years. Sure, that’s deficit reduction, but it may serve to dull the sense that shrinking the federal government is an imperative. The mechanics of this are unclear, but as a first pass, I’d say the gain from investing DOGE savings for a year in low-risk instruments is unlikely to outweigh the foregone savings in interest costs from paying off debt today! Of course, that also depends on the future direction of interest rates, but it’s not a good bet to make with public funds.

Nor can the bond market be comforted by uncertainty surrounding legislation that would not only extend the Trump tax cuts, but will probably include various spending provisions, both cuts and increases. As of now, the mix of provisions that might accompany a deal among GOP factions is very much up in the air.

There is also trepidation about Trump’s aggressive stance toward the Federal Reserve. He promises to replace Jerome Powell as Fed Chairman, but with God knows whom? And Trump jawbones aggressively for lower rates. The Fed’s ill-advised rate cuts in the fall might have been motivated in part by an attempt to capitulate to the then-President Elect.

Trump’s Executive Order to create a sovereign wealth fund (SWF), which I recently discussed here, is probably not the most welcome news to bond investors. All else equal, placing tax or tariff revenue into such a fund would reduce the potential for deficit reduction, to say nothing of the idiocy of additional borrowing to purchase assets.

Finally, Trump has proposed what might later prove to be massive foreign policy trial balloons. Some of these are bound up with the creation of the SWF. They might generate revenue for the government without borrowing (mineral rights in Ukraine? Or Greenland?), but at this point there’s also a chance they’ll create massive funding needs (Gaza development?). Again, Trump seems to be prodding or testing counterparties to various negotiations… prodding diplomacy. It’s unlikely that anything too drastic will come of it from a fiscal perspective, but it probably doesn’t leave bond traders feeling easy.

At this stage, it’s pretty rash to conclude that the bond market “doesn’t believe in DOGE”. In fact, there is no doubt that DOGE is making some progress in identifying potential fraud and inefficiencies. However, bond traders must weigh a wide range of considerations, and Donald Trump has a tendency to kick up dust. Indeed, the so-called DOGE dividend will undermine confidence in debt reduction and bond prices.

If you want to induce a shortage, a price ceiling is a reliable way to do it. Usury laws are no exception to this rule. Private credit can be supplied plentifully to borrowers only when lenders are able to charge rates commensurate with other uses of their funds. Importantly, the rate charged must include a premium for the perceived risk of nonpayment. That’s critical when extending credit to financially-challenged applicants, who are often deserving but may be less stable or unproven.

No doubt certain lenders will seek to exploit vulnerable borrowers, but those borrowers are made less vulnerable when formal, mainstream sources of credit are available. A legal ceiling on the price of credit short-circuits this mechanism by restricting the supply to low-income borrowers, many of whom rely on credit cards as a source of emergency funds.

A couple of odd bedfellows, Senators Josh Hawley (R-MO) and Bernie Sanders (D-CT), are cosponsoring a bill to impose a cap of 10% on credit card interest rates. Sanders is an economic illiterate, so his involvement is no surprise. Hawley is otherwise a small government conservative, but in this effort he reveals a deep ignorance. Unfortunately, President Trump would be happy to sign their bill into law if it gets through Congress, having made a similar promise last fall during the campaign. Unfortunately, this is a typically populist stance for Trump; as a businessman he should know better.

Many consumers in the low-income segment of the market for credit have thin credit reports, a few delinquencies, or even defaults. Most of these potential borrowers struggle with expenses but generally meet their obligations. But even a few with the best intentions and work ethic will be unable to pay their debts. The segment is risky for lenders.

Card issuers might be able to compensate along a variety of margins. These include high minimum payments, stiff fees for late payments, tight credit limits (on lines, individual purchases, or revolving balances), deep relationship requirements, and limits on rewards. However, the most straightforward option for covering the risk of default is to charge a higher interest rate on revolving balances.

The total return on assets of credit-card issuing banks in 2023 was 3.33%, more than twice the 1.35% earned at non-issuing banks, asreported by the Federal Reserve. But that difference in profitability is well aligned with the incremental risk of unsecured credit card lending. According to BBVA Research:

“… studies confirm that higher interest rates on credit cards are not related to limited market competition but to greater levels of risk relative to other banking activities backed or secured by collateral. … In fact, an investigation into the risk-adjusted returns of credit cards banks versus all commercial banks suggests that over the long term, credit cards banks do not enjoy a significant advantage. … the market is characterized by participants that operate a high-risk business that requires elevated risk premiums.”

So card issuers are not monopolists. They face competition from other banks, often on the basis of non-rate product features, as well as “down-market” lenders who “specialize” in serving high-risk borrowers. These include payday lenders, pawn shop operators, vehicle title lenders, refund anticipation lenders, and informal loan sharks, all of whom tend to demand stringent terms. People turn to these alternatives and other informal sources when they lack better options. Hawley, Sanders, and Trump would unwittingly throw more credit-challenged consumers into this tough corner of the credit market if the proposed legislation becomes law.

Much of this was discussed recently by J.D. Tuccille, who writes that many consumers:

“… find banks, credit card companies, and other mainstream institutions rigid, uninterested in their business, and too closely aligned with snoopy government officials. Often, the costs and requirements imposed by government regulations make doing business with higher-risk, lower-income customers unattractive to mainstream finance.

‘The regulators are causing the opposite of the desired effect by making it so dangerous now to serve a lower-income segment,’ JoAnn Barefoot, a former federal official, including a stint as deputy controller of the currency, told the book’s author. She emphasized red tape that makes serving many potential customers a legal minefield“

Tuccille offers a revealing quote attributed to a bank official from a 2015 article in the Albuquerque Journal:

“‘Banking regulations stemming from the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 and the Patriot Act of 2001 have created an almost adversarial credit environment for people whose finances are in cash.‘“

In other words, for some time the government has been doing its damnedest to choke off bank-supplied credit to low-income and risky borrowers, many of whom are deserving. It’s tempting to say this was well-intentioned, but the truth might be more sinister. Onerous regulation of lending practices at mainstream financial institutions, including caps on credit card interest rates, is political gold for politicians hoping to exploit populist sentiment. “Good” politics often hold sway over predictable but unintended consequences, which later can be blamed on the very same financial institutions.

I want a federal government with a less pervasive presence in the private sphere. That’s why I oppose a U.S. sovereign wealth fund (SWF), but President Trump issued an executive order (EO) on February 3 setting in motion the creation of an SWF. It would hold various assets with the ostensible intent to earn a return benefiting American taxpayers.

Here are a few comments on the form an SWF might take:

1) How would the SWF be funded?

—Sales of federal assets like federal land, buildings, and the sale of extraction rights? These are probably the least offensive possibilities for funding an SWF, but the proceeds, if and when they materialize, should be used to pay off our massive federal debt, not to fund a governmental piggy bank.

—Taxes/Tariffs? Funding an SWF via taxes or tariffs would be contrary to the EO’s stated objective to “lessen the burden of taxes on American families and small businesses”. Moreover, it would be contrary to a pro-growth agenda, undermining any gains an SWF might produce.

—Borrowing? Another contradiction of a basic rationale for the SWF, which is “to promote fiscal sustainability”. It would mean more debt on top of a mountain of debt that is already growing at an unsustainable rate.

—“Deals” that might place assets under government ownership? Already, potential buyers of TikTok are singing the praises of a partnership with the SWF. Trump seems to think the government can acquire interests in certain enterprises in exchange for allowing them to operate in the U.S. He also believes that federal dollars can be used for development in order to acquire ownership capital. The federal government should not engage in the development of private resources. Business enterprises should remain private or be privatized, to the extent that their ownership has nothing to do with the provision of public goods.

2) What kinds of investments would be held in the SWF? Stocks and bonds? TikTok shares? Private equity? Crypto? The Gaza Riviera REIT?

These are all terrible ideas. Government ownership of the means of production, or socialism, virtually guarantees underperformance and subservience to political objectives. Federal acquisition of private businesses is not a legitimate function of the state.

There is no point in having the government hold a Bitcoin or crypto reserve. First, giving the U.S. government an interest in the private blockchain undermines the very purpose that most users feel gives the blockchain value. Second, the return on crypto depends only on price changes, and most forms of crypto are volatile. It is a stretch to believe that crypto assets have value in promoting “fiscal sustainability” or national security.

3) How would the SWF’s assets and earnings ultimately be used?

The EO plainly states that earnings in the SWF are to be used to promote fiscal sustainability and benefit taxpayers. In the presence of a large and growing national debt, the best path toward those objectives would be to use any and all spare funds to pay off debt and limit the explosive interest burden it imposes. This puts the funds back into hands of private investors, who will respond to market incentives by deploying the capital as they see fit. Does anyone truly think government planners know better how to put those funds to use?

SWF and Future Debt Service

Just to clarify matters, let’s quantify two alternatives: 1) pay off debt immediately; 2) create an SWF to invest funds and pay off debt later. Suppose the government stumbles upon a spare $100. It can immediately pay off $100 of debt and avoid a certain $3.50 in interest expense in year one. If instead an SWF invests the funds at an expected (but uncertain) return of 7%, then perhaps a greater reduction in the debt can be made a year later. How much? Not $107, but only $103.50 (assuming the 7% return is realized) because the $3.50 interest expense on the debt was not avoided in year one. The SWF must earn twice the interest cost on debt to break even on the proposition. That might be possible for an average return over many years, but the returns will vary and the government is likely to botch the job in any case.

An Itch For Intervention

The SWF is subject to dangers inherent in many government activities. One is that the funds held in reserve might be used as a tool of market intervention and/or political mischief, much as Joe Biden attempted to tamp down oil prices by releasing millions of barrels from the Strategic Petroleum Reserve. An administration having available a large pool of financial assets might be tempted to use it to intervene in various markets to manipulate asset prices. And even if you happen to like the interventions of one administration, you might hate the interventions of another.

The Scratch That Corrupts

In testament to the inefficacy and corruption inherent in government intervention in private markets, Peter Earle offers a number of examples of government planning gone awry. It’s not difficult to understand the dysfunction:

“A sovereign wealth fund would not, whatever the intentions of its government administrators, be guided purely by market signals but rather by political interests. That virtually ensures poor investment choices, investments in politically favored industries, and/or wasteful subsidies tending to yield subpar returns.

“Government officials will not have the same rigorous concern for opportunity costs that drives private investors and for-profit managers, as bureaucratic decision-making is often guided by political priorities and budget cycles rather than the disciplined allocation of capital to its most productive use. The Knowledge Problem is real — and ignoring it is expensive.“

“…there are systemic governance issues and regulatory gaps that can enable SWFs to act as conduits of corruption, money laundering, and other illicit activities.“

Therefore, the management and operations of an SWF require great transparency as well as strong governance and oversight. This obviously adds a layer of cost as well.

Sound Planning

There is an economic rationale for holding funds in reserve for certain, earmarked purposes. For example, private businesses usually maintain reserves for the upkeep or replacement of physical capital. Shouldn’t the government do the same for public infrastructure such as highways or harbors? Public investments in physical capital should be planned such that the flow of tax revenue is adequate to replenish infrastructure from wear and tear. To the extent that the necessary expenditures are “lumpy”, however, a maintenance reserve fund is sound practice, as long as its management is transparent and accountable, and its holdings represent prudent risks.

Another example is the maintenance of a reserve fund for pension payments. This is a reasonable and even necessary practice under traditional defined benefit plans, but those plans have often fallen short of their obligations in practice. The private sector stayed ahead of this risk by shifting overwhelmingly to defined contribution plans. As part of this shift, the existing pension obligations of many private entities were converted to vested “cash value” balances. The public sector should do the same, putting employees in charge of their own retirement savings.

Countries with SWFs tend to be small and also tend to run budget surpluses. Very often, they are funded with revenue earned from abundant natural resources. But even those governments short-change their citizens by failing to reduce tax rates, which would promote growth.

Nonsensical Appeal to Nationalism

Why does the creation of an SWF sound so good to people who should know better? I think it has something to do with the nationalist urge to embrace symbols of patriotic strength. An SWF might evoke the emotive impact of phrases like “sound money” or “a strong dollar”. But in the presence of a large public debt and large, continuing budget deficits, the kind of SWF envisioned by Trump would be counterproductive. Future obligations to pay down the public debt are better addressed in the present, to the extent possible. The government has no business hoarding private financial assets as a means of outrunning debt. Sure, the return on equity usually exceeds the interest rate on public debt, but private investors are better at allocating capital than government, so government should not attempt to take on that role.

Ongoing increases in the resources dedicated to health care in the U.S., and their prices, are driven primarily by the abandonment of market forces. We have largely eliminated the incentives that markets create for all buyers and sellers of health care services as well as insurers. Consumers bear little responsibility for the cost of health care decisions when third parties like insurers and government are the payers. A range of government interventions have pushed health care spending upward, including regulation of insurers, consumer subsidies, perverse incentives for consolidation among health care providers, and a mechanism by which pharmaceutical companies negotiate side payments to insurers willing to cover their drugs.

It’s not yet clear whether the Trump Administration and its “Make America Healthy Again” agenda will serve to liberate market forces in any way. Skeptics can be forgiven for worrying that MAHA will be no more than a cover for even more centrally-planned health care, price controls, and regulation of the pharmaceutical and food industries, not to mention consumer choices. Robert F. Kennedy Jr., who is likely to be confirmed by the Senate as Donald Trump’s Secretary of Health and Human Services, has strong and sometimes defensible opinions about nutrition and public health policies. He is, however, an inveterate left-winger and is not an advocate for market solutions. Trump himself has offered only vague assurances on the order of “You won’t lose your coverage”.

Government Control

The updraft in health care inflation coincided with government dominance of the sector. Steven Hayward points out that the cost pressure began at about the same time as Medicare came into existence in 1965. This significantly pre-dates the trend toward aging of the population, which will surely exacerbate cost pressures as greater concentrations of baby boomers approach or exceed life expectancy over the next decade.

Government now controls or impinges on about 84% of health care spending in the U.S., as noted by Michael F. Cannon. The tax deductibility of employer-provided health insurance is a massive example of federal manipulation and one that is highly distortionary. It reinforces the prevalence of third-party payments, which takes decision-making out of consumers’ hands. Equalizing the tax treatment of employer-provided health coverage would obviously promote tax equity. Just as importantly, however, tax-subsidized premiums create demand for inflated coverage levels, which raise prices and quantities. And today, the federal government requires coverages for routine care, going beyond the basic function of insurance and driving the cost of care and insurance upward.

The traditional non-portability of employer-provided coverage causes workers with uninsurable pre-existing conditions to lose coverage when they leave a job. Thus, Cannon states that the tax exclusion for employer coverage penalizes workers who instead might have chosen portable individual coverage in a market setting without tax distortions. Cannon proposes a reform whereby employer coverage would be replaced with deposits into tax-free Universal Health Accounts owned by workers, who could then purchase their own insurance.

In 2024, federal subsidies for health insurance coverage were about $2 trillion, according to the Congressional Budget Office (CBO). Those subsidies are projected to grow to $3.5 trillion by 2034 (8.5% of GDP). Joel Zinberg and Liam Sigaud emphasize the wasteful nature of premium subsidiesfor exchange plans mandated by the Affordable Care Act (ACA), better known as Obamacare. Subsidies were temporarily expanded in 2021, but only until 2026. They should be allowed to expire. These subsidies increase the demand for health care, but they are costly to taxpayers and are offered to individuals far above the poverty line. Furthermore, as Zinberg and Sigaud discuss, subsidized coverage for the previously uninsured does very little to improve health outcomes. That’s because almost all of the health care needs of the formerly uninsured were met via uncompensated care at emergency rooms, clinics, medical schools, and physician offices.

Proportionate Consumption

Perhaps surprisingly, and contrary to popular narratives, health care spending in the U.S. is not really out-of-line with other developed countries relative to personal income and consumption expenditures (as opposed to GDP). We spend more on health care because we earn and consume more of everything. This shouldn’t allay concern over health care spending because our economic success has not been matched by health outcomes, which have lagged or deteriorated relative to peer nations. Better health might well have allowed us to spend proportionately less on health care, but this has not been the case. There are explanations based on obesity levels and diet, but important parts of the explanation can be found elsewhere.

It should also be noted that a significant share of our decades-long increases in health care spending can be attributed to quantities, not just prices, as explained at the last link above.

Health Consequences

The ACAdid nothing to slow the rise in the cost of health care coverage. In fact, if anything, the ACA cemented government dominance in a variety of ways, reinforcing tendencies for cost escalation. Even worse, the ACA had negative consequences for patient care. David Chavous posted a good X thread in December on some of the health consequences of Obamacare:

1) The ACA imposed penalties on certain hospital readmissions, which literally abandoned people at death’s door.

2) It encouraged consolidation among providers in an attempt to streamline care and reduce prices. This reduced competitive pressures, however, which had the “unforeseen” consequence of raising prices and discouraging second opinions. The former goes against all economic logic while the latter goes against sound medical decision-making.

3) The ACA forced insurers to offer fewer options, increasing the cost of insurance by encouraging patients to wait until they had a pre-existing condition to buy coverage. Care was almost certainly deferred as well. Ultimately, that drove up premiums for healthy people and worsened outcomes for those falling ill.

4) It forced drug companies to negotiate with Pharmacy Benefit Managers (PBMs) to get their products into formularies. The PBMs have acted as classic middlemen, accomplishing little more than driving up drug prices and too often forcing patients to skimp on their prescribed dosage, or worse yet, increasing their vulnerability to lower-priced quackery.

The Insurers

So the ACA drastically increased the insured population (including the new burden of covering pre-existing conditions). It also forced insurers to meet draconian cost-control thresholds. Little wonder that claim rejection increased, a phenomenon often at the root of public animosity toward health insurers. Peter Earle cites several reasons for the increase in denial rates while noting that claim rejection has made little difference in insurer profit margins.

Matt Margolis points out that under the ACA, we’ve managed to worsen coverage in exchange for higher premiums and deductibles. All while profits have been capped. Claim denials or delays due to pre-authorization rules (which delay care) have become routine following the implementation of Obamacare.

Perhaps the biggest mistake was forcing insurers to cover pre-existing conditions without allowing them to price for risk. Rather than forcing healthy individuals to pay for risks they don’t face, it would be more economically sensible to directly subsidize coverage for those in high-risk pools.

Noah Smith also defends the health insurers. For example, while UnitedHealth Group has the largest market share in the industry, its net profit margin of 6.1% is only about half of the average for the S&P 500. Other major insurers earn even less by this metric. Profits just don’t explain why American health care spending is so high. Ultimately, the services delivered and charges assessed by providers explain high U.S. health care spending, not insurer profits or administrative costs.

Under the ACA, insurance premiums pay the bulk of the cost of health care delivery, including the cost of services more reasonably categorized as routine health maintenance. The latter is like buying insurance for oil changes. Furthermore, there are no options to decline any of the ten so-called “essential benefits” under the ACA, thus increasing the cost of coverage.

Medical Records

Arnold Kling argues that the ACA’s emphasis on uniform, digitized medical records is not a productive avenue for achieving efficiencies in health care delivery. Moreover, it’s been a key factor driving the increasing concentration in the health care industry. Here is Kling:

“My point is that you cannot do this until you tighten up the health care delivery process, making it more rigid and uniform. And I would not try to do that. Health care does not necessarily lend itself to being commoditized. You risk making health care in America less open to innovation and less responsive to the needs of people.

“So far, all that has been accomplished by the electronic medical records drive has been to put small physician practices out of business. They have not been able to absorb the overhead involved in implementing these systems, so that they have been forced to lose their independence, primarily to hospital-owned conglomerates.”

Separating Health and State

The problem of rising health care costs in the U.S. is capsulized by Bryan Caplan in his call for the separation of health and state. The many policy-driven failures discussed above offer more than adequate rationale for reform. The alternative suggested by Caplan is to “pull the plug” on government involvement in health care, relying instead on the free market.

Caplan debunks a few popular notions regarding the appropriate role for markets in health care and health insurance. In particular, it’s often alleged that moral hazard and adverse selection would encourage unhealthy behaviors and encourage the worst risks to over-insure, causing insurance markets to fail. But these problems arise only when risk is not priced efficiently, precisely what the government has accomplished by attempting to equalizing rates.

Pulling the plug on government interference in health care would also mean deregulating both insurance offerings and pricing, encouraging the adoption of portable coverage, expediting drug approvals based on peer-country approvals, reforming pharmacy benefit management, ending deadly Medicare drug price controls, and encouraging competition among health care providers.

Value Vs. Volume

There are a host of other reforms that could bring more sanity to our health care system. Many of these are covered here by Sebastian Caliri, with some emphasis on the potential role of AI in improving health care. Some of these are at odds with Kling’s skepticism regarding digitized health records.

Perhaps the most fundamental reforms entertained by Caliri have to do with health care payments. One is to make payments dependent on outcomes rather than diagnostic codes established and priced by the American Medical Association. To paraphrase Caliri, it would be far better for Americans to pay for value rather than volume.

Another payment reform discussed by Caliri is expanding direct payments to providers such as capitation fees, whereby patients pay to subscribe to a bundle of services for a fixed fee. Finally, Caliri discusses the importance of achieving “site-neutral payments”, eliminating rules that allow health systems to charge a higher premium relative to independent providers for identical services.

For what it’s worth, Arnold Kling disagrees that changing payment metrics would be of much help because participants will learn to game a new system. Instead, he emphasizes the importance of reducing consumer incentives for costly treatments having little benefit. No dispute there!

Avoid the Single-Payer Calamity

I’ll close this jeremiad with a quote from Caliri’s piece in which he contrasts the knee-jerk, leftist solution to our nation’s health care dilemma with a more rational, market-oriented approach:

“Single payer solutions and government control favored by the left are no solutions at all. Moving to a monopsonist system like Canada is a recipe for strangling innovation and rationing access. Just ask our neighbors to the north who have to wait a year for orthopedic surgery. The UK’s National Health Service (NHS) is teetering on the brink of collapse. We need to sort out some other way forward.

“Other parts of the economy provide inspiration for what may actually work. In the realm of information technology, for example, fifty years has taken us from expensive four operation calculators to ubiquitous, free, artificial intelligence capable of passing the Turing Test. We can argue about the precise details but most of this miracle came from profit-seeking enterprises competing in a free market to deliver the best value for the buyer’s dollar.“

In a post a few years ago entitled “The National Endowment for Rich Farts”, I discussed a point that should be rather obvious: federal funding of the arts too often subsidizes the upper class, catering to their artistic tastes and underwriting a means through which they conduct social and professional networking. The topic is back in the news, with reports that the incoming Trump Administration, at the recommendation of the Department of Government Efficiency (DOGE), will attempt to eliminate funding for the Corporation for Public Broadcasting.

Great Big Stuff and Crowding Out

To opponents of federal arts funding, public radio is probably the bête noire of arts organizations due to its left-wing political orientation and the general affluence of its subscriber base. However, public arts funding goes way beyond subsidies for public radio.

Large nonprofits receive the bulk of government arts funding. Despite claims to the contrary, these organizations won’t go broke without the gravy provided by public funding. The federal government contributes about 3% of the revenue taken in by non-profit arts organizations, according to Americans For the Arts. These organizations are already heavily subsidized: their surpluses are tax exempt and private contributions are tax deductible. Tax deductions are worth more to those in high income-tax brackets, and involvement in such visible organizations is highly prized by elites.

It’s often argued that government should subsidize the arts because art has the qualities of a public good, but that’s a false premise. A good can be classified as “public” only when its consumption is non-exclusive and non-rivalrous. Can individuals be excluded from enjoying music? Of course. Can they be excluded from viewing a theatrical performance, a film, or any other piece of visual art? Generally yes, and art exhibitions and artistic performances are nearly always subject to paid and limited attendance.

In some contexts art is, or can be made, less excludable. Architecture can be admired (or detested) by anyone on the street. So can public monuments and street art. A concert or play can be performed free of charge, perhaps at a large, outdoor venue. Amplification and large video monitors can make a big difference in terms of non-exclusion. Museums can offer admission to the general public at no charge. And we can broaden the definition of a work to include copies or reproductions that might be available via public display or broadcast (on NPR!).

All these steps will help increase exposure to the arts. But you can’t make it mandatory. People will always self-exclude because they can. So, in which cases should taxpayers bear the costs of art, and of making it less exclusive? On the spectrum of legitimate functions of government, it’s hard to rank this sort of activity highly.

A claim less absurd than the public goods argument is that art has some positive spillover effects, or externalities. It should therefore be subsidized or underwritten with public funds lest it be underprovided. Unfortunately, the spillover effects of a piece of art (where relevant) are not always positive. After all, tastes vary considerably. One man’s art can be another man’s annoyance orprovocation. This undermines the case for public funding, at least for art that is controversial in nature.

Perhaps a better interpretation of art externalities is that exposure to the arts has positive spillover effects. Thus, additional art confers benefits to society above and beyond the edification of those exposed to it. Perhaps it makes us nicer and more interesting, but that’s a highly speculative rationale for public funding.

Less questionably, more art and more exposure to the arts does enrich society in ways that have nothing to do with external benefits. Culture and arts are by-products of normal social interactions between private individuals. The benefits of art exposure (and art education) are largely accrued privately. When artistic knowledge is shared to nourish or broaden one’s network, the benefits flow from private social interactions that arise naturally, rather than as a consequence of phantom external benefits.

The same danger looms when government provides a venue or manages aspects of a presentation of art, including curation of content. It’s an avenue through which art can become politicized. The problem, however, is not so much that a particular work might have political implications. As Samuel Andreyev, a Canadian composer says:

“Like any other subject, it is possible for political subjects to be handled sensitively by an artist, provided there is a strong enough element of abstraction and symbolism so that the work does not become merely journalistic.”

Andreyev makes a good point, but government funding and direction can create incentives to politicize art, encouraging more blatant expressions of political viewpoints at the expense of taxpayers.

I’ve certainly admired art despite subtle political implications with which I differed. One can hardly imagine a treatment of the human condition that would not invite tangential political commentary. Still, politicization of art should always be left as a private exercise, not one over which the government of a free society wields influence.

Do Markets Undervalue Art?

What about the artists themselves? The premise that artists deserve subsidies relies on the questionable presumption that the value of their work exceeds its commercial or market value. Thus, taxpayers are asked to pay handsomely for art that is not valued as highly by private buyers.

Artists who benefit from government arts funding are often well established professionally. Less fortunate artists scrape by, finding what market they can while working side gigs. In fact, many less celebrated artists work at their craft on a part-time basis while earning most of their income from day jobs. Should the government support these artists, or artists having few opportunities to promote their work?

It’s not clear that public funding should override the private market’s basis of valuation for established or unestablished artists. However, some government funding finds its way into less celebrated corners of the art world.This report uses data at the census tract level to show that arts organizations located in low income tracts, while receiving less, still get a disproportionate share of federal grant dollars relative to their share of the population. This finding should be viewed cautiously, as data at this level of aggregation has limitations. The findings do not imply that “starving artists” receive a disproportionate share of those dollars. Nor do they prove that federal grants benefit low-income individuals disproportionately via improved access to the arts. Again, the findings are based on the location of organizations. And again, large organizations receive the bulk of these grants.

Drawing the Line

So where do we draw the line on taxpayer subsidies for the arts? The standard, public-goods justification is false. While externalities may exist, they are not always positive, and it is hardly the state’s proper role to fund art that “challenges” notions about good and bad art. In that vein, just as law tends to be ineffective when it lacks consensus, public arts funding breeds dissent when the art is controversial.

The legitimacy of public arts funding ultimately depends on whether the art itself has a true public purpose. To varying degrees, this might include the architecture and interior design of public buildings, landscaping of parks, as well as certain monuments and statuary. Even within these disciplines, the selection of form, content, and the artists who will execute the work can be controversial. That might be unavoidable, though controversy will be minimized when the content of publicly-funded art remains within cultural norms.

Beyond those limited purposes, funding art at the federal level is difficult to justify. That role simply does not fall within the constitutionally-enumerated powers of the federal government. The tenuous rationale for subsidies implies that art is undervalued, despite the existence of a vibrant private ecosystem for art, including private support foundations and markets. To the extent that public subsidies line the pockets of elites or support art that would otherwise fail a market test, they represent a wasteful misallocation of resources.

Funding art might seem less troublesome at lower levels of government, where elected representatives and policymakers are in more intimate contact with voters and taxpayers. Still, the same economic reservations apply. At local levels, institutions like community orchestras and concerts series might be broadly supported. Publicly-funded museums, theatrical venues, and other facilities might be accepted by voters as well. If parents have educational choices and expect schools to teach art, it should be funded at public schools, so long as the content stays within cultural norms and is age-appropriate. Of course, all of these matters are up to local voters.

The greatest danger of public funding for the arts is that it tends to be utilized as a tool of political propaganda. Having the state select winners and losers in the arts invites politicization, undermining freedom and our system of government. On that point, Thomas Jefferson once made this observation:

“To compel a man to furnish contributions of money for the propagations of opinions which he disbelieves and abhors, is sinful and tyrannical.“

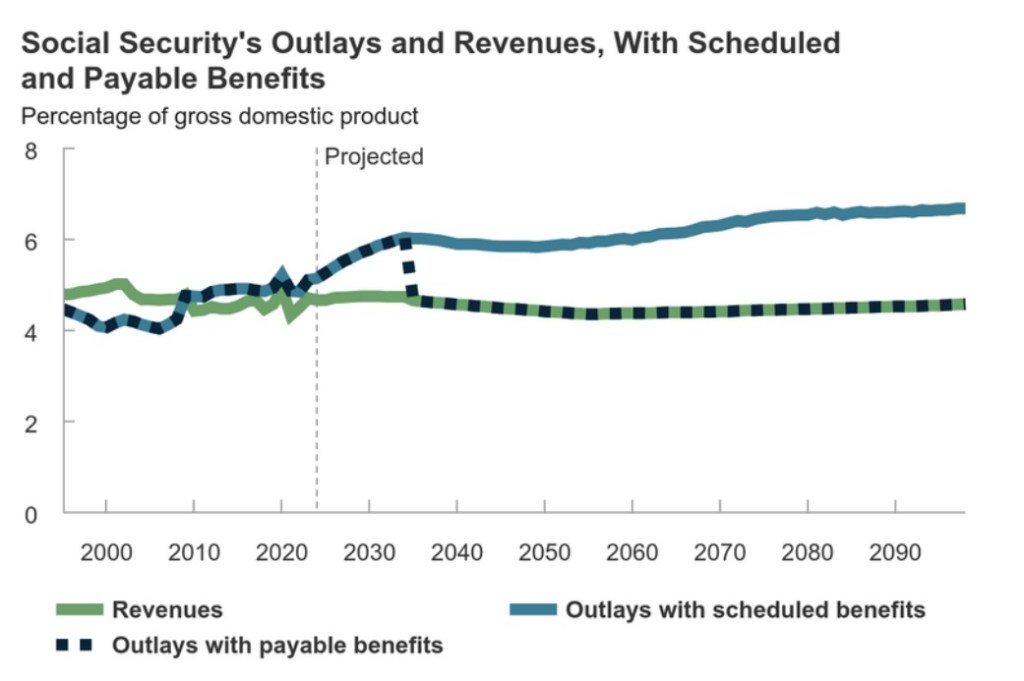

Social Security wasn’t designed as a true saving vehicle for workers. Instead, SS has always been a pay-as-you-go system under which current benefits are funded by the payroll taxes levied on the current employed population. In fact, many Americans earn lousy effective returns on their tax “contributions” (also see here), though low-income individuals do much better than those near or above the median income. Worst of all, under pay-as-you-go, the system can collapse like a Ponzi scheme when the number of workers shrinks drastically relative to the retired population, leading to the kind of situation we face today.

Unfunded Obligations

Payroll tax revenue is no longer adequate to pay for current Social Security and Medicare benefits, and the problem is huge: according to the Penn-Wharton Budget Model, the unfunded obligations of Social Security (including old age, survivorship and disability) through 2095 have a present value of $18.1 trillion in constant 2024 dollars (using a discount rate of 4.4%). The comparable figure for Medicare Part A is $18.6 trillion. Together these amount to more than the current national debt.

Barring earlier reform, the Social Security Trust Fund is expected to be exhausted in 2033 (excluding the disability fund). At that point, a 20% reduction in benefits will be required by law. (More on the trust fund below.)

What To Do?

The most prominent reform proposals involve reduced benefits for wealthy beneficiaries, increased payroll taxes on high earners, and an increase in the retirement age. However, President-Elect Donald Trump shows no inclination to make any changes on his watch. This is unfortunate because the sooner the system’s insolvency is addressed, the less draconian the necessary reforms will be.

A neglected reform idea is for SS to be privatized. Many observers agree in principle that current workers could earn better returns over the long-term by investing funds in a conservative mix of equities and bonds. The transition to private accounts could be made voluntary, so that no one is forced to give up the benefits to which they’re “entitled”.

Takers would receive an initial deposit from the government in a tax-deferred account. For participating pre-retirees, ongoing FICA contributions (in whole or in part) would be deposited into their private accounts. They could purchase a private annuity with the balance at retirement if they choose. The income tax treatment of annuity payments or distributions could mimic the current tax treatment of SS benefits.

Given that the balance remaining at death would be heritable, some individuals might be willing to accept an initial deposit less than the actuarial PV of the future SS benefits they’ve accumulated to-date (discounted at an internal rate of return equating future benefits “earned” to-date and contributions to-date). I also believe many individuals would willingly accept a lower initial deposit because they would gain some control over investment direction. Such voluntarily-accepted reductions in initial deposits to personal accounts would mean the government’s issue of new debt would be smaller than the decrease in future benefit obligations.

Nevertheless, funding the accounts at the time of transition would necessitate a huge and immediate increase in federal debt. Market participants and political interests are likely to fear an impossible strain on the credit market. Perhaps the transition could be staged over time to make it less “shocking”, but that would complicate matters. In any case, heavy debt issuance is the rub that dissuades most observers from supporting privatization.

Fiscal Theory of Price Level

The fiscal theory of the price level (FTPL) implies that such a privatization might not be an insurmountable challenge after all, at least in terms of comparative dynamics. Much background on FTPL can be found at John Cochrane’s Grumpy Economist Substack.

FTPL asserts that fiscal policy can influence the price level due to a constraint on the market value of government debt. This market value must be in balance with the expected stream of future government primary surpluses. This is known as the government budget constraint.

The primary surplus excludes the government’s interest expense, a budget component that must be paid out of the primary surplus or else borrowed. Of course, the market value of government debt incorporates the discounted value of future interest payments.

This budget constraint must be true in an expectational sense. That is, the market must be convinced that future surpluses will be adequate to pay all future obligations associated with the debt. Otherwise, the value of the debt must change.

Should a spending initiative require the government to issue new debt with no credible offset in terms of future surpluses, the market value of the debt must decline. That means interest rates and/or the price level must rise. If interest rates are fixed by the monetary authority (the Fed) then only prices will rise.

A SS Private Option Under FTPL

But what about FTPL in the context of entitlement reform, specifically a privatization of Social Security? Suppose the government issues debt and then deposits the proceeds into personal accounts to fund future benefits. Future government surpluses (deficits) would increase (decrease) by the reduction in future SS benefit payments.

This improved budgetary position should be highly credible to financial markets, despite the fact that benefits are not and never have been guaranteed. If it is credible to markets, the new debt would not raise prices, nor would it be valued differently than existing debt. There need not be any change in interest rates.

But Thin Ice

There are risks, of course. It might be too much to hope that other federal spending can be restrained. That kind of failure would subvert the rationale for any budgetary reform. A variety of other crises and economic shocks are also possible. Those could disrupt markets and jeopardize budget discipline as well. Given a severe shock, interest expense could more readily explode given the massive debt issuance required by the reform discussed here. So there are big risks, but one might ask whether they could turn out to be more disastrous in the absence of reform.

Other Details

The private account “offers” extended to workers or beneficiaries relative to the actuarial PVs of their future benefits would be controversial. Different offer percentages (discounts) could be tested to guage uptake.

Another issue: provisions would have to be made for individuals in “unbanked” households, estimated by the FDIC to be about 4.2% of all U.S. households in 2023. Voluntary uptake of the “offer” is likely to be lower among the unbanked and among those having less confidence in their ability to make financial decisions. However, even a simplified set of choices might be superior to the returns under today’s SS, even for low-income workers, not to mention the very real threat of future reductions in benefits. Furthermore, financial institutions might compete for new accounts in part by offering some level of financial education for new clients.

A similar reform could be applied to Medicare, which like SS is also technically insolvent. Participating beneficiaries could receive some proportion of expected future benefits in a private account, which they could use to pay for private or public health insurance coverage or medical expenses. From a budget perspective, the increase in federal debt would be balanced against the reduction in future Medicare benefits, which would constitute a credible increase (decrease) in future surpluses (deficits).

Credibility

But again, how credible would markets find the decrease in benefit obligations? Direct reductions in future entitlements should be convincing, though politicians are likely to find plenty of other ways to use the savings.

On the other hand, markets already give some weight to the possibility of future benefit cuts (or other policies that would reduce SS shortfalls). So it’s likely that markets will give the reform’s favorable budget implications significant but only “incremental credit”.

Another possible complication is that the market, prior to execution of the reform, might discount the uptake by workers and current retirees. This would necessitate better offers to improve uptake and more debt issuance for a given reduction in future obligations. Skepticism along these lines might worsen implications for the price level and interest rates.

The Trust Fund

Finally, what about the SS Trust Fund? Can it play in role in the reform discussed above? The answer depends on how the trust fund fits into the federal government’s budgetary position.

The trust fund holds as assets only non-marketable Treasury securities acquired in the past when SS contributions exceeded benefit payments. The excess payroll tax revenue was placed in the trust fund, which in turn lent the funds to the federal government to help meet other budgetary needs. Hence the bond holdings.

In terms of the government’s fiscal position, the money has already been pissed away, as it were. The bonds in the trust fund do not represent a pot of money. As noted above, with our age demographics now reversed, payroll taxes no longer meet benefits. Thus, bonds in the trust fund must be redeemed to pay all SS obligations. The Treasury must pay off the bonds via general revenue or by borrowing additional amounts from the public.

Post-reform, if continuing deficits are the order of the day, redeeming bonds in the trust fund would do nothing to improve the government’s fiscal position. If the trust fund “cashes them in” to help meet benefit payments, the federal government must borrow to raise that cash. In other words, the bonds in the trust fund would be more or less superfluous.

But what if the federal budget swings into a surplus position post-reform? In that case, federal tax revenue would cover the redemption of at least some of the bonds held by the trust fund. SS beneficiaries would then have a meaningful claim on federal taxpayers through the trust fund and the government’s surplus position, which would reduce the new federal debt required by the reform.

Conclusion

The Social Security and Medicare systems are in desperate need reform, but there is little momentum for any such undertaking. Meanwhile, exhaustion of the SS and Medicare trust funds creeps ever closer, along with required benefit cuts. All of the reform options would be painful in one way or another. A voluntary privatization would require a huge makeover, but it might be the least painful option of all. Current workers and beneficiaries would not be compelled to make choices they found inferior. Moreover, the new debt necessary to pay for the reforms would be matched by a reduction in future government obligations. The fiscal theory of the price level implies that the reform would not be inflationary and need not depress the value of Treasury bonds, provided the reform is accompanied by long-term budget discipline.

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

Note: the chart at the top of this post was produced by the Congressional Budget Office and appears in this publication.

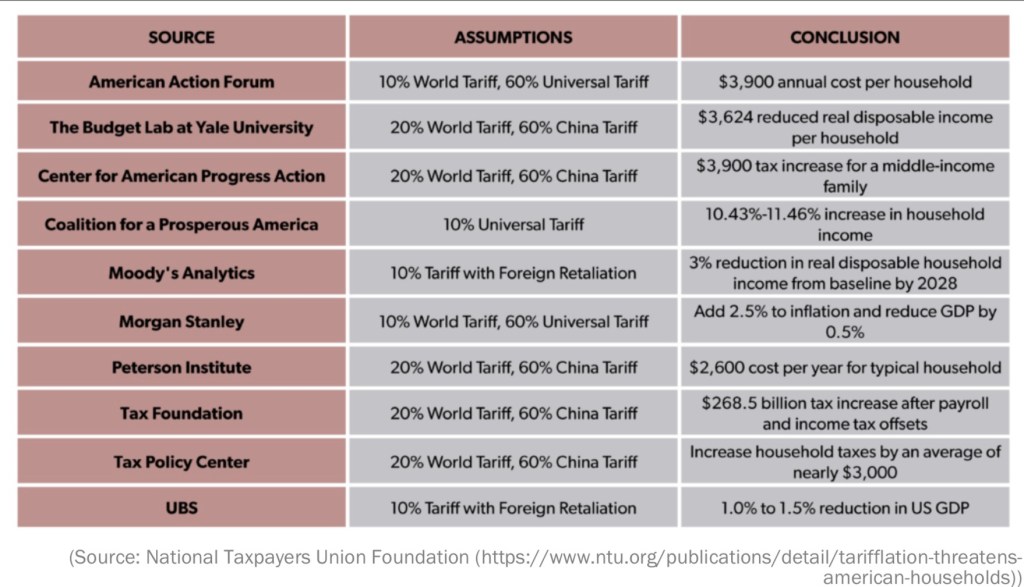

The table above is from Eric Boehm at Reason.com. It shows a variety of negative economic projections based on the likely imposition of tariffs by the incoming Trump Administration. Donald Trump’s protectionist agenda is motivated in large part by the notion that imports of foreign goods and services harm the U.S. economy. This misapprehension is common on both the populist left and the nationalist right, but it is also fueled by special interests averse to competition. Especially puzzling are those who extol the virtues of capitalism and free markets while claiming that free markets across borders are inimical to our nation’s economic interests.

Imports and Domestic Spending

Many assume that imports directly reduce GDP. In fact, on this point, some might be led astray by a superficial exposure to macroeconomics. As Noah Smith has noted, they might think back to the simple spending definition of GDP they learned as college freshmen:

GDP = C + I + G + (X – M),

where C is consumer spending on final goods and services, I is investment spending, G is government spending, X is foreign spending on U.S. exports, and M is U.S. spending on imports from abroad. So imports are subtracted! Doesn’t that mean imports directly reduce GDP?

The key here is to recognize that C, I, and G already include spending on imported goods. Therefore, imports must be subtracted from the spending totals to find the value spent on domestically-produced final goods and services. No, imports are not a direct, net subtraction from GDP.

Your Loathsome Foreign Car

Of course the domestic impact of imports goes deeper than this simple accounting framework. If someone decides to purchase an imported good instead of a close substitute produced domestically, what happens to GDP? If the decision has an immediate impact on production, then U.S. GDP declines. Otherwise, the domestic good is new inventory investment (part of I above), and there is no change. But if the import decision is repeated, the result is permanently lower U.S. GDP relative to the alternative, as producers won’t want to add to inventories indefinitely. The same is true if a domestic producer decides to purchase a component or raw material produced overseas rather than one produced at home.

The import decision causes a domestic producer to lose a sale along with the profit that sale would have earned. That puts pressure on the firm’s workers and wages as well. The firm still has the value of the unit in inventory, but if the import decision is repeated there will be more substantial follow-on effects on production, employment, spending, and saving.

Not So Fast

There is still more to the story, of course. By purchasing the foreign good,,which in the buyer’s estimation delivers greater value at that point in time, there is a gain in consumer surplus that is very real. To the buyer, that gain is perhaps equivalent to dollars in the bank. Their real wealth has increased relative to the surplus value of the foregone domestic purchase. This, too, will likely have follow-on effects in terms of spending and saving, but positive effects.

Therefore, to a first approximation, the immediate effects of an import purchase on total domestic welfare are ambiguous. Consumers of imports gain value; producers of import-competing goods lose value.

As to the loss of the domestic sale, competition is tough, but it greatly contributes to the efficiency of the free market system and to the well being of consumers. Let’s face it: ultimately, the whole point of economic activity is to enable consumption. Production has no other purpose. So producers must react to competition and strive to improve value for buyers along any margins they can. That, in turn, is unequivocally positive for potential buyers both here and abroad.

It’s also true that the purchase of foreign goods means that dollars must be sold in exchange for foreign currency. That weakens the dollar, but those “excess dollars” are generally used to purchase U.S. assets, including physical capital. That direct investment promotes economic growth.

Open Economy, Open Mind

No matter what you believe about the net benefits or costs of a single import transaction like the one described above, it is misleading to draw conclusions about the benefits of foreign trade based on a single transaction, or even a series of repeated transactions.

First, consumer sovereignty is based on freedom of choice, including the freedom to purchase from any seller, domestic or foreign. Consumers greatly benefit from that broad freedom. Add to that the benefit of producers who are free to purchase inputs from any source they believe to offer the greatest value (a benefit that ultimately flows through to consumers). These freedoms ultimately enhance productivity and well being.

Trade across borders leverages the same economic advantages as trade within borders. People tend to accept the latter as truth without giving it a thought, yet the former is often rejected reflexively. The question is inappropriately bound up in issues like patriotism and, over time, an excessive focus on high-visibility job losses in traditional industries.

Trade allows people and their countries to specialize in producing things at which they are comparatively efficient, i.e., in which they are lower-cost producers. This is at the very heart of mutually beneficial exchange: no party to a voluntary transaction expects to suffer a loss. And in trade, when an external, domestic party sustains a lost sale, for example, they have the opportunity to improve or reallocate their resources to endeavors to which they are better suited. So there are direct gains from trade and there are indirect gains via the discipline of competition, including the benefits of reallocating scarce resources from inefficient to efficient uses.

Tariff Gains

Now we shift gears to tariffs: interventions having benefits that are more concentrated than costs, and which tend to be more ephemeral:

— Domestic producers who compete with imports gain through the grant of additional market power, given the tax on foreign goods and services. These producers now have more pricing flexibility, and what is often more pertinent, survivability.

— Workers at domestic firms will benefit to the extent that their employers face reduced foreign competition. Some combination of employment, hours, and wages may rise.

— Some firms have mixed gains and losses, with more pricing power over final product but elevated costs due to the use of taxed foreign components.

Tariff Losses

Who pays when government succumbs to irrational protectionist pressure and attempts to restrict imports via tariffs?

— Domestic consumers suffer a loss of freedom and bear a large part of the burden of the tariff tax.

— Higher prices for imports lead to higher prices for competing domestic goods, causing consumers to experience a loss of purchasing power.

— Domestic businesses suffer a loss of control over input decisions. Those already utilizing foreign inputs (and their buyers downstream) bear some of the burden of the tariff tax. For example, tariffs could be quite damaging to the U.S. AI industry, a result that would run strongly contrary to Trump’s promise to promote American AI.

— The U.S. suffers a loss of foreign investment, which could engender higher interest rates, lower productivity growth, and lower real wages.

— As Tyler Cowen puts it in a review of this paper, “… lobbying, logrolling and political horse-trading were essential features of the shift toward higher US tariffs. A lot of the tariffs of the time [1870 -1909] depended on which party controlled Congress, rather than economic rationality.“

— Tariffs tend to reduce economic growth due to diminished productivity in tariff-protected industries, which also erodes real wages. Less productive firms capture a significant share of the benefits of tariffs, so that economic growth falls due to a compositional effect. Higher prices for imports and import-competing goods undermine the real gains of import-protected workers.

— Finally, tariffs invariably beget retaliatory tariffs by erstwhile friendly trading partners. Export industries and their employees take a direct hit. This retaliation damages the prospects of the most productive exporters, while weaker exporting firms might be forced to close shop unnecessarily.

One other note: the discussion of gains and losses above is essentially the same for policies that reward the use of American labor via tax breaks. This not only penalizes imports of final and intermediate foreign goods, it subsidizes high-cost domestic labor. Obviously, the upshot is a less competitive U.S. economy.

Tariff-Threat Policy

To be fair, Donald Trump has said he’d use the threat of tariffs strategically to achieve a variety of objectives, not all of which are directly related to trade. We can hope that many of those threats won’t be acted upon. On one hand, that’s more appealing than general tariffs, with potential foreign policy gains and less in the way of general damage to the economy. On the other hand, the discretionary application of tariffs could invite political favoritism and foster a corrupt rent-seeking environment.

Conclusion

Trade protectionism protects weak and strong producers alike. The weak should not be given artificial incentives to produce goods inefficiently. That’s simply a waste of resources. Protecting the strong is unnecessary and discourages the drive for efficiency as well as real value creation. It lends market power to already powerful firms, leading to higher prices and penalizing domestic consumers.

One last aside: tariffs cannot raise anywhere close to the revenue necessary to replace the income tax, an absurd claim made by Trump on the campaign trail.

Only free trade is consistent with the values of a free society. It enhances choice, makes markets more competitive, creates incentives for efficiency, and cultivates opportunities for economic growth, That would serve Trump and the nation much better than the fixation on tariffs.

Wow! We’re less than a week from Election Day! I’d hoped to write a few more detailed posts about the platforms and policies of Kamala Harris and Donald Trump, but I was waylaid by Hurricane Milton. It sent us scrambling into prep mode, then we evacuated to the Florida Panhandle. The drive there and back took much longer than expected due to the mass exodus. On our return we found the house was fine, but there was significant damage to an exterior structure and a mess in the yard. We also had to “de-prep” the house, and we’ve been dealing with contractors ever since. It was an exhausting episode, but we feel like we were very lucky.

Now, with less than a week left till the election, I’ll limit myself to a summary of the positions of the candidates in a number of areas, mostly but not all directly related to policy. I assign “grades” in each area and calculate an equally-weighted “GPA” for each candidate. My summaries (and “grades”) are pretty off-the-cuff and not adequate treatments on their own. Some of these areas are more general than others, and I readily admit that a GPA taken from my grade assignments is subject to a bit of double counting. Oh well!

Role of Government: Kamala Harris is a statist through and through. No mystery there. Trump is more selective in his statist tendencies. He’ll often favor government action if it’s politically advantageous. However, in general I think he is amenable to a smaller role for the public than the private sector. Harris: F; Trump: C

Regulation: There is no question that Trump stands for badly needed federal regulatory reform. This spans a wide range of areas, and it extends to a light approach to crypto and AI regulation. Trump plans to appoint Elon Musk as his “Secretary of Cost Cutting”. Harris, on the other hand, seems to favor a continuation of the Biden Administration’s heavy regulatory oversight. This encourages a bloated federal bureaucracy, inflicts high compliance costs on the private sector, stifles innovation, and tends to concentrate industrial power. Harris: F; Trump: A

Border Policy: Trump wants to close the borders (complete the wall) and deport illegal immigrants. Both are easier said than done. Except for criminal elements, the latter will be especially controversial. I’d feel better about Trump’s position if it were accompanied by a commitment to expanded legal immigration. We need more legal immigrants, especially the highly skilled. For her part, Harris would offer mass amnesty to illegals. She’d continue an open border policy, though she claims to want certain limits on illegal border crossings going forward. She also claims to favor more funds for border control. However, it is not clear how well this would translate into thorough vetting of illegal entrants, drug interdiction at the border, or sex trafficking. Harris: D; Trump: B-

Antitrust: Accusations of price gouging by American businesses? Harris! Forty three corporations in the S&P 500 under investigation by the DOJ? The Biden-Harris Administration. This reflects an aggressively hostile and manipulative attitude toward the business community. Trump, meanwhile, might wheedle corporations to act on behalf of certain of his agendas, but he is unlikely to take such a broadly punitive approach. Harris: F; Trump: B-

Foreign Policy: Harris is likely to continue the Biden Administration’s conciliatory approach to dealing with America’s adversaries. The other side of that coin is an often tepid commitment to longtime allies like Israel. Trump believes that dealing from a position of strength is imperative, and he’s willing to challenge enemies with an array of economic and political sticks and carrots. He had success during his first term in office promoting peace in the Middle East. A renewed version of the Abraham Accords that strengthened economic ties across the region would do just that. Ideally, he would like to restore the strength of America’s military, about which Harris has less interest. Trump has also shown a willingness to challenge our NATO partners in order to get them to “pay their fair share” toward the alliance’s shared defense. My major qualification here has to do with the candidates’ positions with respect to supporting Ukraine in its war against Putin’s mad aggression. Harris seems more likely than Trump to continue America’s support for Ukraine. Harris: D+; Trump: B-

Trade: Nations who trade with one another tend to be more prosperous and at peace. Unfortunately, neither candidate has much recognition of these facts. Harris is willing to extend the tariffs enforced during the Biden Administration. Trump, however, is under the delusion that tariffs can solve almost anything that ails the country. Of course, tariffs are a destructive tax on American consumers and businesses. Part of this owes to the direct effects of the tax. Part owes to the pricing power tariffs grant to domestic producers. Tariffs harm incentives for efficiency and the competitiveness of American industry. Retaliatory action by foreign governments is a likely response, which magnifies the harm.

To be fair, Trump believes he can use tariffs as a negotiating tool in nearly all international matters, whether economic, political, or military. This might work to achieve some objectives, but at the cost of damaging relations more broadly and undermining the U.S. economy. Trump is an advocate for not just selective, punitive tariffs, but for broad application of tariffs. Someone needs to disabuse him of the notion that tariffs have great revenue-raising potential. They don’t. And Trump is seemingly unaware of another basic fact: the trade deficit is mirrored by foreign investment in the U.S. economy, which spurs domestic economic growth. Quashing imports via tariffs will also quash that source of growth. I’ll add one other qualification below in the section on taxes, but I’m not sure it has a meaningful chance.

Harris: C-; Trump: F

Inflation: This is a tough one to grade. The President has no direct control over inflation. Harris wants to challenge “price gougers”, which has little to do with actual inflation. I expect both candidates to tolerate large deficits in order to fulfill campaign promises and other objectives. That will put pressure on credit markets and is likely to be inflationary if bond investors are surprised by the higher trajectory of permanent government indebtedness, or if the Federal Reserve monetizes increasing amounts of federal debt. Deficits are likely to be larger under Trump than Harris due in large part to differences in their tax plans, but I’m skeptical that Harris will hold spending in check. Trump’s policies are more growth oriented, and these along with his energy policies and deregulatory actions could limit the inflationary consequences of his spending and tax policies. Higher tariffs will not be of much help in funding larger deficits, and in fact they will be inflationary. Harris: C; Trump: C

Federal Reserve Independence: Harris would undoubtedly like to have the Fed partner closely with the Treasury in funding federal spending. Her appointments to the Board would almost certainly lead to a more activist Fed with a willingness to tolerate rapid monetary expansion and inflation. Trump might be even worse. He has signaled disdain for the Fed’s independence, and he would be happy to lean on the Fed to ease his efforts to fulfill promises to special interests. Harris: D; Trump: F

Entitlement Reform: Social Security and Medicare are both insolvent and benefits will be cut in 2035 without reforms. Harris would certainly be willing to tax the benefits of higher-income retirees more heavily, and she would likely be willing to impose FICA and Medicare taxes on incomes above current earning limits. These are not my favorite reform proposals. Trump has been silent on the issue except to promise no cuts in benefits. Harris: C-; Trump: F

Health Care: Harris is an Obamacare supporter and an advocate of expanded Medicaid. She favors policies that would short-circuit consumer discipline for health care spending and hasten the depletion of the already insolvent Medicare and Medicaid trust funds. These include a $2,000 cap on health care spending for Americans on Medicare, having Medicare cover in-home care, and extending tax credits for health insurance premia. She supports funding to address presumed health care disparities faced by black men. She also promises efforts to discipline or supplant pharmacy benefit managers. Trump, for his part, has said little about his plans for health care policy. He is not a fan of Obamacare and he has promised to take on Big Pharma, whatever that might mean. I fear that both candidates would happily place additional controls of the pricing of pharmaceuticals, a sure prescription for curtailed research and development and higher mortality. Harris: F; Trump: D+

Abortion: The Supreme Court’s 2022 decision in Dobbs v. Jackson essentially relegated abortion law to individual states. That’s consistent with federalist principles, leaving the controversial balancing of abortion vs. the unborn child’s rights up to state voters. Geographic differences of opinion on this question are dramatic, and Dobbs respects those differences. Trump is content with it. Meanwhile, Harris advocates for the establishment of expanded abortion rights at the federal level, including authorization of third trimester abortions by “care providers”. And Harris does not believe there should be religious exemptions for providers who do not wish to offer abortion services. No doubt she also approves of federally funded abortions. Harris: F; Trump: A